Egypt Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

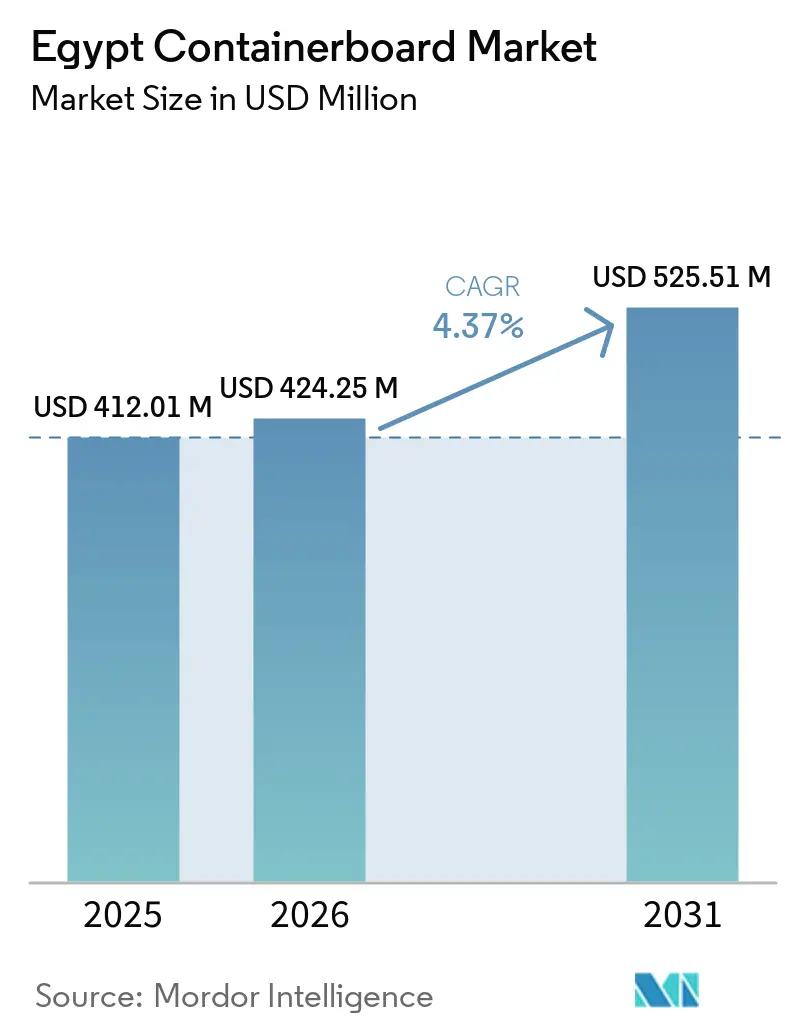

| Base Year Market Size (2025) | USD 412.01 Million |

| Market Size (2026) | USD 424.25 Million |

| Market Size (2031) | USD 525.51 Million |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

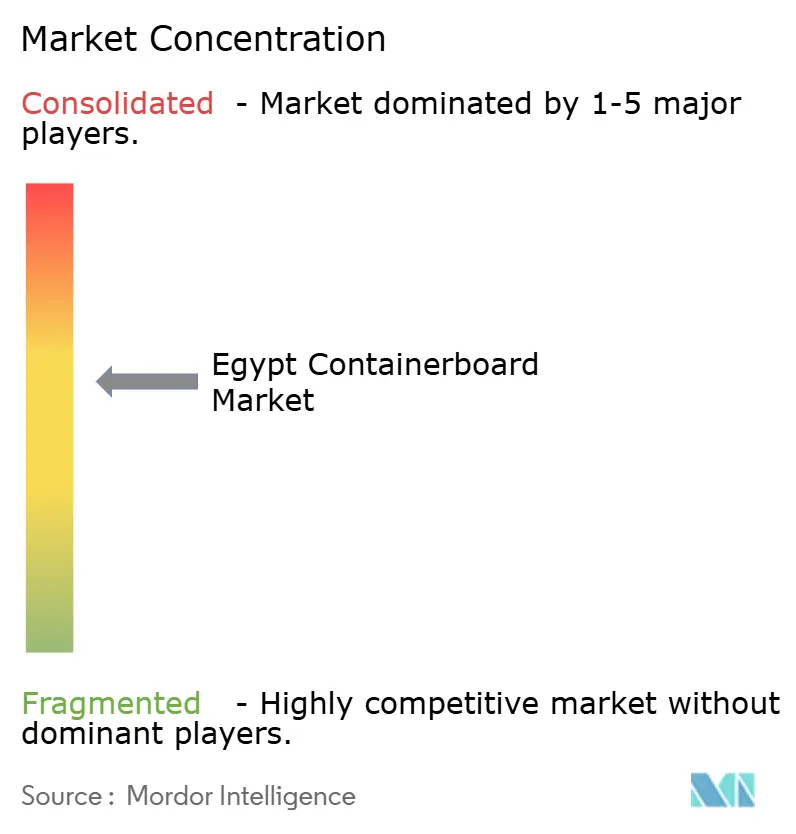

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Containerboard Market Analysis by Mordor Intelligence

The Egypt containerboard market size was valued at USD 412.01 million in 2025, USD 424.25 million in 2026, and reach USD 525.51 million by 2031, advancing at a CAGR of 4.37% from 2026 to 2031. Demand in the Egypt containerboard market remains tied to the country’s large food processing base, the continued rise in packaged food volumes, and the stronger export flow of processed food products. The Egypt containerboard market is also being supported by faster order fulfillment models in urban retail, where larger quick-commerce facilities are increasing the use of corrugated transit packaging and secondary packaging formats. At the same time, the Egypt containerboard market is moving through a supply-side upgrade cycle as new machine capacity and coating technology reduce dependence on imported higher-grade linerboard. Policy support is also improving the long-term outlook because packaging compliance rules are creating a more favorable setting for recyclable fiber formats. Margin conditions still face pressure from imported wastepaper and kraftliner costs, freight disruption across Red Sea routes, and possible changes to industrial water pricing, which is why growth remains steady rather than aggressive.

Key Report Takeaways

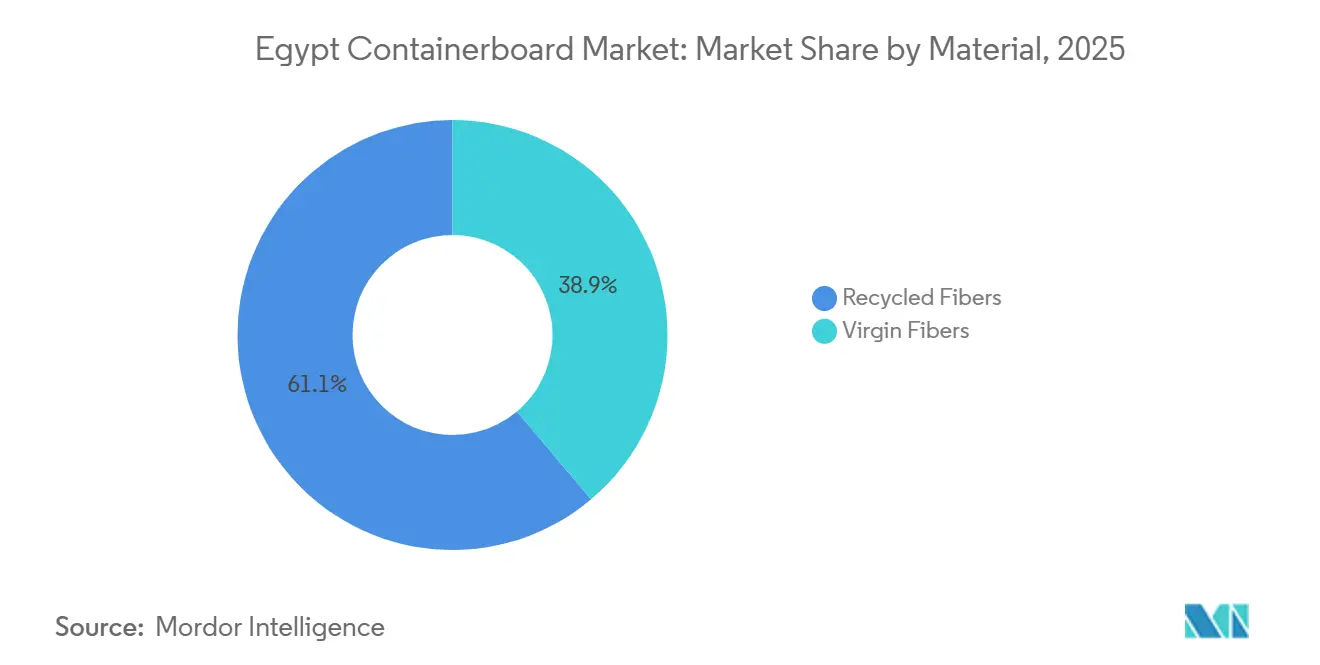

- By material, recycled fibers captured 61.15% of the Egypt containerboard market share in 2025.

- By product type, the Egypt containerboard market size for the kraftliners segment is forecast to advance at a 4.82% CAGR through 2031.

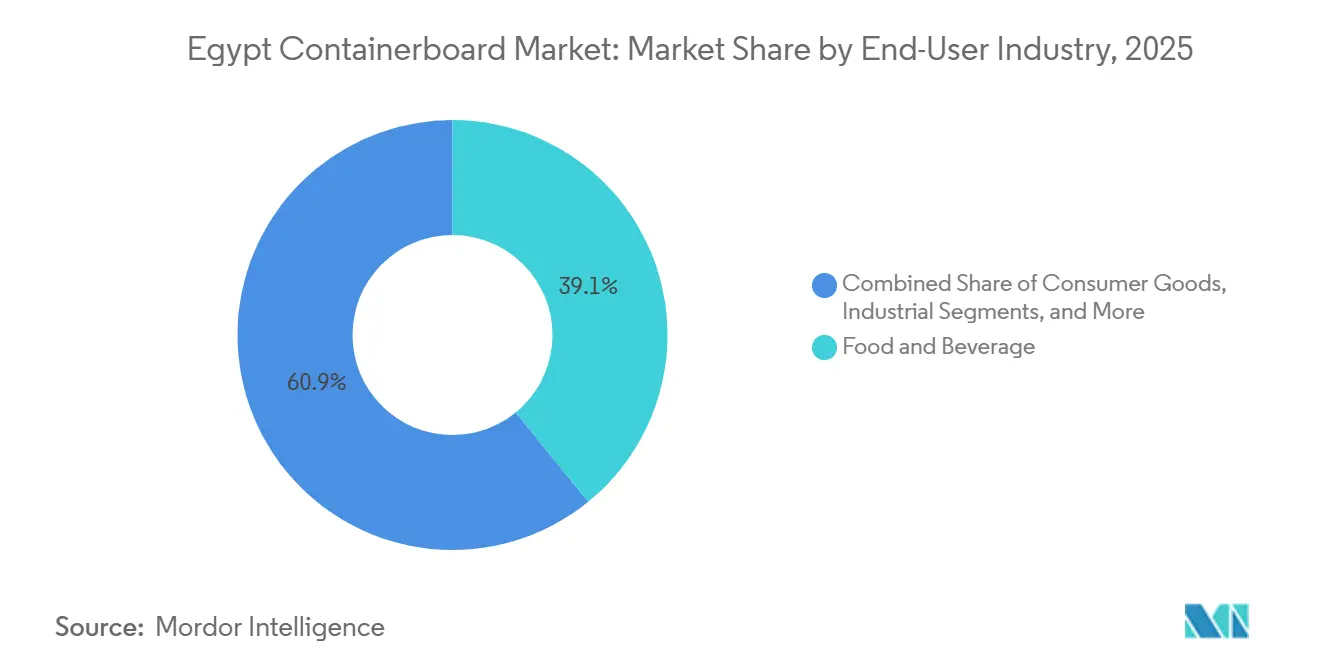

- By end-user industry, food and beverage captured 39.12% of the Egypt containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Food And Beverage Export Packaging Demand | +1.1% | National, with concentrated gains in Greater Cairo, Nile Delta, and Suez corridor industrial zones | Medium term (2-4 years) |

| E-Commerce And Quick-Commerce Order Growth | +0.9% | National, with early gains in Cairo, Alexandria, and Mansoura | Short term (≤ 2 years) |

| Sustainability-Led Shift Toward Recyclable Fiber Packaging | +0.7% | National, with spillover to export-facing manufacturers in industrial free zones | Long term (≥ 4 years) |

| FMCG Output Expansion And Shelf-Ready Packaging Demand | +0.6% | National, with early gains in Greater Cairo and Suez Canal Economic Zone | Medium term (2-4 years) |

| Greenliner PM1 Ramp-Up Closing Higher-Grade Supply Gaps | +0.5% | National, supply-side concentration in 10th of Ramadan City and Borg El Arab industrial corridors | Short term (≤ 2 years) |

| Beverage Carton Fiber Recovery Deepening Local Recycled Feedstock | +0.3% | National, with fiber recovery centered in Sadat City and Greater Cairo | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Food And Beverage Export Packaging Demand

Egypt’s processed food export base remains one of the strongest demand supports for the Egypt containerboard market because export growth lifts both box volumes and board performance requirements.[1]Daily News Egypt, “Egypt's Food Industry Exports Exceed USD 6.3bn in 11M 2025,” Daily News Egypt, dailynewsegypt.com Processed food exports reached USD 6.1 billion in 2024 and exceeded USD 6.3 billion in the first 11 months of 2025, while the Egyptian Food Export Council targeted USD 8 billion for 2026. During the first 8 months of 2025, exports to African markets reached USD 119 million, up from USD 64 million in the same period in 2024, underscoring the growing need for transit-resistant corrugated packaging.[2]Food Export Council of Egypt, “Egyptian Food Industry Exports and Performance in African Markets,” Food Export Council of Egypt, api.feceg.com Export customers are also pushing harder on compression strength and moisture performance, which is lifting demand for better liner grades and raising the value of mills that can serve multiple quality tiers. This separates the Egyptian containerboard market into an export-grade tier and a domestic-grade tier, supporting stronger pricing and greater margin potential for integrated producers with broader grade capabilities.

E-Commerce And Quick-Commerce Order Growth

Quick-commerce infrastructure is scaling fast enough to create a new layer of steady packaging demand in the Egypt containerboard market. Talabat Mart opened MENA’s largest quick-commerce fulfillment center in Cairo in April 2026, and the 22,405-square-meter facility can handle up to 1.6 million items per day while supporting more than 60 dark stores. That scale creates one of the country’s most concentrated demand nodes for corrugated trays, shippers, and secondary packaging used in rapid order picking and dispatch. Automated picking systems and high-throughput storage layouts also need more consistent caliper and better board performance, which favors mills that can supply stable, higher-basis-weight grades. As these fulfillment formats spread beyond Cairo, the Egypt containerboard market should see a wider move toward technically tighter domestic board specifications

Sustainability-Led Shift Toward Recyclable Fiber Packaging

Sustainability rules are giving fiber packaging a stronger regulatory position in the Egypt containerboard market.[3]Waste Management Regulatory Authority, “Extended Producer Responsibility,” Waste Management Regulatory Authority, wims.wmra.gov.eg Prime Ministerial Decree No. 662 of 2025 classified plastic shopping bags as priority EPR products, and producers became subject to a mandatory fee of EGP 37.5 per kilogram from June 2025. The Waste Management Regulatory Authority also continued the rollout of the national green-label certification system for plastic packaging, with technical guidelines launched in November 2024 and a broader packaging guide completed in November 2025. In January 2026, the Egypt Export Council for Printing, Packaging, Paper, Literary and Artistic Works linked sustainable packaging design and EPR compliance to export readiness ahead of the European Union’s CBAM transition. That linkage makes recyclable board selection less discretionary for exporters, which gives the Egypt containerboard market a longer runway for certified recycled-content and compliance-oriented packaging grades.

FMCG Output Expansion And Shelf-Ready Packaging Demand

FMCG output is creating another steady source of packaging demand for the Egypt containerboard market as producers shift toward shelf-ready corrugated formats.[4]State Information Service of Egypt, “Prime Minister Inspects Mars Egypt Factory Expansions,” Maspero, maspero.eg These formats use more display-ready cartons, lighter structures, and smaller stock-keeping units, which can reduce board weight per pack but raise the number of corrugated units moving through each production run. Mars Egypt’s expansion demonstrated the scale of this demand, with 8 fully automated production lines operating in May 2026 and 100% domestically sourced packaging materials. This supports demand for mid-weight testliner and related corrugated formats that domestic mills can supply competitively while keeping delivery times short. It also deepens the role of traceable recycled content in converter supply contracts, thereby strengthening the position of local recycled-fiber producers in the Egyptian containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported OCC, Pulp, And Kraftliner Cost Volatility | -0.8% | National, most acute for mills dependent on imported OCC from southern Europe and the MENA region | Medium term (2-4 years) |

| Red Sea Freight Disruptions And Longer Replenishment Cycles | -0.7% | National, concentrated impact on east-of-Suez sourcing lanes and import-dependent mill inventories | Short term (≤ 2 years) |

| Emerging Industrial Water Pricing And Quota Risk | -0.4% | National, most acute for water-intensive mills in Greater Cairo and the Nile Delta industrial zones | Medium term (2-4 years) |

| Recovered Fiber Quality Gaps For White-Top And High-Performance Grades | -0.3% | National, most acute for producers targeting export and multinational-quality customers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported OCC, Pulp, And Kraftliner Cost Volatility

The Egypt containerboard market remains exposed to imported raw material costs, even though local recovered fiber collection covers a large share of mill needs. Egypt’s largest OCC recycler stated that it sources around 80% of its wastepaper domestically, leaving the remaining 20% reliant on imports from regional markets and southern Europe. Virgin Kraft pulp used in top liner structures is also still tied to imported supply, so global fiber pricing can move faster than local box pricing can adjust. The Tetra Pak and Uniboard recycling program in Sadat City helps build a local buffer because the line targets 8,000 tonnes per year and creates an additional recovered fiber stream from used beverage cartons. Even with that progress, the Egypt containerboard market still faces margin pressure whenever imported OCC, pulp, or kraftliner prices rise faster than mills can pass costs through to converters.

Red Sea Freight Disruptions And Longer Replenishment Cycles

Red Sea shipping disruptions have become a direct operating risk for the Egypt containerboard market because import lanes for fiber and finished grades are more exposed to delay and freight inflation. Renewed insecurity since late February 2026 pushed major carriers to reroute vessels around the Cape of Good Hope, adding 15-20 days to affected routes and raising landed costs by 8-12%. Longer replenishment cycles force mills and converters to hold more safety stock, tying up working capital and narrowing cash flexibility for companies already dealing with input price volatility. Domestic substitution is improving as Greenliner ramps local capacity and BloomPack develops higher-value liner capability, but that shift is still in progress. Until that import gap narrows further, the Egypt containerboard market will remain sensitive to freight shocks and booking delays across east-of-Suez supply routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Hold The Base While Virgin Grades Gain Share

Recycled fibers held 61.15% of the Egyptian containerboard market share in 2025, reflecting the country’s long-established OCC-based mill network and collection activity in Greater Cairo, the Nile Delta, and Alexandria. This part of the Egyptian containerboard industry remains supported by local waste paper sourcing, as MMPP stated that it collects around 80% of its recovered paper domestically through depots and direct collection arrangements. That supply pattern keeps recycled-fiber grades central to domestic box production and supports the large installed base of mills that serve everyday corrugated demand at cost-sensitive price points. The feedstock base also widened after Tetra Pak and Uniboard established a used beverage carton recycling line in Sadat City, which added a new source of reclaimable fiber to the local system.

Virgin fibers were the smaller material category in 2025, but they are projected to grow at a 4.74% CAGR through 2031 as the higher-specification tier of the Egypt containerboard market size expands. Growth in this segment is tied to export cartons and multinational FMCG demand, where board performance, print surface, and consistency matter more than lowest-cost furnish. Greenliner’s PM1 start-up in 10th of Ramadan City and BloomPack’s move into white top liner technology both show how domestic producers are targeting this premium layer of demand with better machine capability and value-added grades. The result is a more tiered structure inside the Egypt containerboard industry, where recycled fibers continue to anchor volume while virgin-rich and premium grades gain share in the upper specification band.

By Product Type: Testliners Lead Volumes While Kraftliners Set The Pace

Testliners accounted for 41.95% of product demand in 2025, making them the largest product type in the Egypt containerboard market, as they align with the economics of domestic OCC supply and the needs of mainstream corrugated converting. Their position is reinforced by the structure of local box demand, where food, FMCG, and agricultural packaging volumes still favor practical domestic-grade board with acceptable compression and moisture performance. Fluting demand remains closely linked to this product group because most corrugated plants rely on paired liner and medium supply from local mills serving standard transport packaging applications. This keeps testliners at the center of volume production even as premium demand grows in selected export-facing applications.

Kraftliners are projected to grow at a 4.82% CAGR through 2031, and export-grade corrugated requirements and tighter quality demands from multinational plants are driving this segment of the Egypt containerboard market. Buyers serving the European and Gulf channels increasingly specify stronger outer liners for cartons exposed to longer transit cycles and more stringent handling conditions. BloomPack’s off-coated white top liner project and Greenliner’s newer machine platform both support the local shift toward higher-performing liner grades that had relied heavily on imports. Over the forecast period, Kraftliner growth should remain more export-led than Testliner growth, making product differentiation more important across the Egyptian containerboard market.

By End-User Industry: Food And Beverage Stay Largest While Consumer Goods Expand Faster

Food and beverage accounted for 39.12% of total demand in 2025, making it the largest end-user group in the Egyptian containerboard market and tying packaging demand closely to the country’s domestic food system and export pipeline. Processed food exports exceeded USD 6.3 billion in the first 11 months of 2025, while edible oil exports and cereal and biscuit preparations both recorded 42% growth, underscoring how packaging-intensive the food value chain has become. Cold-chain limitations further support the role of corrugated formats because a large share of food handling still occurs in ambient conditions, which preserves a natural use case for transport boards and secondary cartons. This makes food and beverage demand more durable than short-term consumer cycles alone would suggest in the Egyptian containerboard market.

Consumer goods are projected to grow at a 4.91% CAGR through 2031 as retail formalization and parcel-based distribution increase demand for packaging across home care, personal care, and smaller electronics categories. Huhtamaki Egypt received a Golden License in January 2025 to build a molded fiber packaging plant in Sadat City, with a total investment of EGP 1.47 billion (USD 29.4 million). Operations were expected to start in August 2026, with 70% of output directed to export markets. That investment signals confidence in Egypt’s broader fiber packaging value chain and supports the view that non-food demand is widening beyond a narrow industrial base. As consumer goods volumes rise, the Egypt containerboard market should benefit from a more balanced end-user mix that reduces dependence on any single packaging vertical

Geography Analysis

The Egypt containerboard market is concentrated around 3 industrial corridors, and Greater Cairo remains the main supply and demand center because it combines mill capacity, converter density, retail demand, and fulfillment infrastructure in one zone. The 10th of Ramadan City forms a major part of that cluster, where Greenliner started up PM1 in November 2025 and continued its production ramp-up through 2026. Cairo also saw stronger downstream packaging pull after Talabat opened its large quick-commerce fulfillment center on the Cairo-Suez Road, which increased demand for secondary corrugated formats across the capital. The concentration of converters, urban retail activity, and collection networks gives this corridor a strong advantage in speed, stock availability, and wastepaper sourcing. It also means changes in Cairo-area operating costs can influence the wider Egypt containerboard market more quickly than shifts in less industrialized regions.

Alexandria and Borg El Arab form the second established hub, where export access and industrial infrastructure support linerboard production and corrugated conversion for both domestic and trade-linked demand. The Northern Delta, including Damietta, Mansoura, and Tanta, is growing as a packaging demand node because food processing, agricultural produce handling, and manufacturing activity are concentrated across the Nile Delta. Sadat City and the wider Menofeya belt add a third important cluster, as the Uniboard and Tetra Pak recycling line has created a new fiber recovery point that supports downstream board production and circular supply development. In practice, location strategy in the Egypt containerboard market depends less on long-haul inland transport and more on proximity to recovered fiber sources, converters, and industrial demand pockets.

Egypt also stands out as one of the larger containerboard demand centers in Africa because it combines a sizable domestic population, a more developed corrugated converting base, and a stronger food export orientation than many nearby markets. Export growth raises board specifications, which pushes mills in Egypt toward a more competitive regional position in higher-value corrugated applications. The country’s location between North Africa, the eastern Mediterranean, and the Red Sea trade lanes also gives it a natural role in serving nearby markets when grade quality and delivery reliability improve. As intra-African trade links deepen, Egyptian producers are well placed to supply more packaging into North and East African corridors from an established manufacturing base. That geographic advantage does not remove freight and input risks, but it does strengthen the long-term external sales potential of the Egypt containerboard market

Competitive Landscape

The Egypt containerboard market is moving from a fragmented, price-led structure toward a more tiered model in which a limited group of integrated mills controls most of the serious-grade and capacity upgrades. Companies such as Greenliner, Uniboard, MMPP’s ELF unit, BloomPack, and ETAP represent the stronger tier of producers that can influence supply quality, furnish strategy, and converter relationships more than smaller standalone players. Their advantage comes from integration across waste collection, papermaking, and, in some cases, affiliated conversion, which gives them more control over cost, delivery, and grade positioning. Smaller converters still compete on price and turnaround speed, but the center of profitability is shifting toward mills that can serve multiple quality bands and defend margins with better technology.

Greenliner’s PM1 launch in November 2025 was the clearest recent example of that shift, as the 5.15-meter-deckle machine brought a major domestic addition to recycled corrugated case material capacity and continued ramping through 2026. BloomPack’s deployment of Valmet’s Curtain Coater for Egypt’s first off-coated white top liner line showed a parallel move into specialty grades that had long depended on imports. ETAP also pursued process improvement through a Toscotec press section rebuild, which raised post-press dryness and reduced paper breaks, showing that productivity gains are becoming a real competitive lever rather than a secondary issue. Tetra Pak and Uniboard added another layer of differentiation by building a closed-loop used beverage carton recycling line in Sadat City, which supports certified recovered fiber claims and strengthens raw material resilience. Together, these moves show that competition in the Egypt containerboard market is rising more through capability and supply-chain control than through volume alone.

The main white space still sits in premium segments such as off-coated white top liner, higher-basis-weight virgin kraftliner, and more demanding fluting grades for export packaging. That leaves room for domestic import substitution, but it also raises the bar for mills that want to serve multinational procurement teams and export-oriented box converters. Foreign and local investment support is helping this transition, as Egypt’s Golden License framework is attracting more capital into fiber-based packaging assets and adjacent value-chain projects. Over time, that should widen the gap between well-capitalized mills and the broader fringe of smaller operators that remain more exposed to price swings and weaker technology bases. The Egypt containerboard market, therefore, remains moderately fragmented today, but the direction of competition is clearly toward stronger concentration in the upper end of the margin pool.

Egypt Containerboard Industry Leaders

Greenliner

United Company for Paper Industry S.A.E. (Uniboard)

Lotus Paper Egypt

Nile Paper

El-Obour for Paper Production

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Talabat Egypt inaugurated MENA's largest AI-powered quick-commerce fulfillment center on the Cairo-Suez Road at YANMU East Logistics Park. The 22,405-square-meter facility handles up to 1.6 million items daily, supports more than 60 dark stores, and is expanding to 17 Egyptian cities. The scale of this logistics node fundamentally upgrades the volume and specification of corrugated secondary packaging consumed at Egypt's fulfillment layer, directly stimulating demand for consistent, higher-caliper domestic testliner and medium.

- November 2025: Greenliner started up PM1 at its 10th of Ramadan City mill, commissioning Egypt's largest containerboard machine, a 5.15-meter-deckle RCCM machine equipped with Valmet and Voith technology, producing from 80 g/m². The machine is in active production ramp-up throughout 2026, expanding both volume and grade capability to reduce Egypt's reliance on imported higher-grade containerboard and position Greenliner as a key regional exporter.

- October 2025: Tetra Pak, Beyti, Juhayna, and Uniboard jointly launched Egypt's first nationwide used beverage carton (UBC) recycling campaign, building on 4,000 tonnes of UBC collected since the mid-2024 inauguration of the EUR 2.5 million (USD 2.7 million) Sadat City recycling line. The campaign deepens domestic OCC-equivalent feedstock supply and advances the circular economy credentials of Uniboard's containerboard output.

- May 2025: BloomPack and Valmet announced the deployment of Egypt's first off-coated white top liner production line using Valmet's Curtain Coater technology. The system promises brightness and uniformity metrics surpassing existing domestic benchmarks, filling a specialty-grade supply gap that has historically required full reliance on imports.

Egypt Containerboard Market Report Scope

The Egypt Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Egypt Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of the Egypt containerboard sector?

The Egypt containerboard market was valued at USD 412.01 million in 2025 and is forecast to reach USD 525.51 million by 2031, growing at a 4.37% CAGR from 2026 to 2031.

Which material type leads demand in Egypt?

Recycled fibers led the material mix with 61.15% share in 2025, supported by the country's long-standing OCC-based mill network and local wastepaper collection system.

Which product category is growing the fastest through 2031?

Kraftliners are projected to post the fastest product growth at a 4.82% CAGR through 2031, helped by export-grade corrugated demand and stricter performance requirements.

Why does food and beverage remain the largest end-user segment?

Food and beverage held 39.12% of total demand in 2025 because Egypt's domestic food system is large and processed food exports exceeded USD 6.3 billion in the first 11 months of 2025.

How is e-commerce affecting corrugated packaging demand in Egypt?

Quick-commerce is raising demand for transit packaging and more consistent board grades, especially after Talabat opened a Cairo fulfillment center capable of handling 1.6 million items daily in 2026.

What are the main risks facing producers over the next few years?

The main risks are imported OCC and pulp cost volatility, Red Sea freight disruptions that extend replenishment cycles, and possible industrial water pricing changes that could pressure mill economics.

Page last updated on: