Transplantation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.88 Billion |

| Market Size (2031) | USD 23.39 Billion |

| Growth Rate (2026 - 2031) | 9.47% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transplantation Market Analysis by Mordor Intelligence

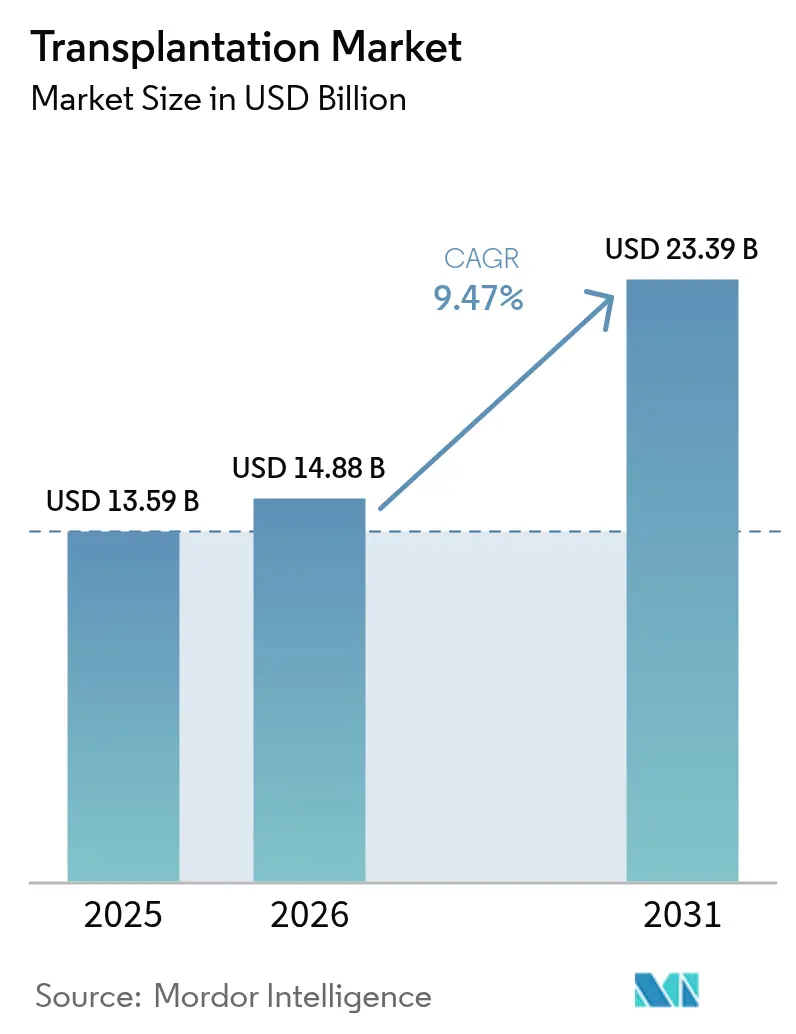

The transplantation market size is expected to grow from USD 13.59 billion in 2025 to USD 14.88 billion in 2026 and is forecast to reach USD 23.39 billion by 2031 at 9.47% CAGR over 2026-2031. Growth is propelled by the widening gap between organ supply and demand, rapid progress in preservation technology, and policy reforms that accelerate donor identification and allocation efficiency. Immunosuppressive drug innovations remain central, yet ex-vivo perfusion devices push the therapeutic frontier by extending viable preservation windows beyond 20 hours. Artificial-intelligence algorithms now refine donor–recipient matching, reducing wait-list mortality and maximizing organ utilization efficiency. Simultaneously, emerging xenotransplantation trials signal a potential paradigm shift that could ease the chronic donor shortage while reshaping the competitive contours of the transplantation market.

Key Report Takeaways

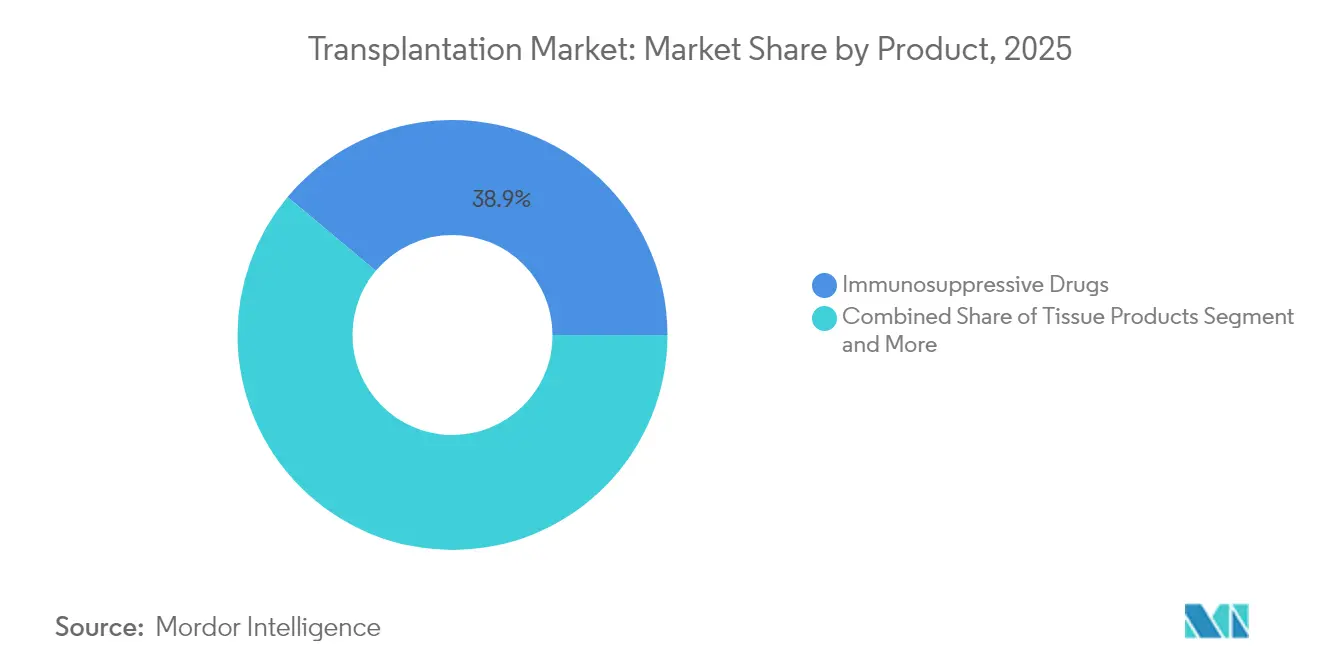

- By product category, immunosuppressive drugs led with 38.92% of transplantation market share in 2025, while preservation solutions and systems are forecast to rise at a 11.86% CAGR to 2031.

- By application, organ transplantation accounted for 53.97% of 2025 revenues; tissue transplantation is advancing at a 13.22% CAGR through 2031.

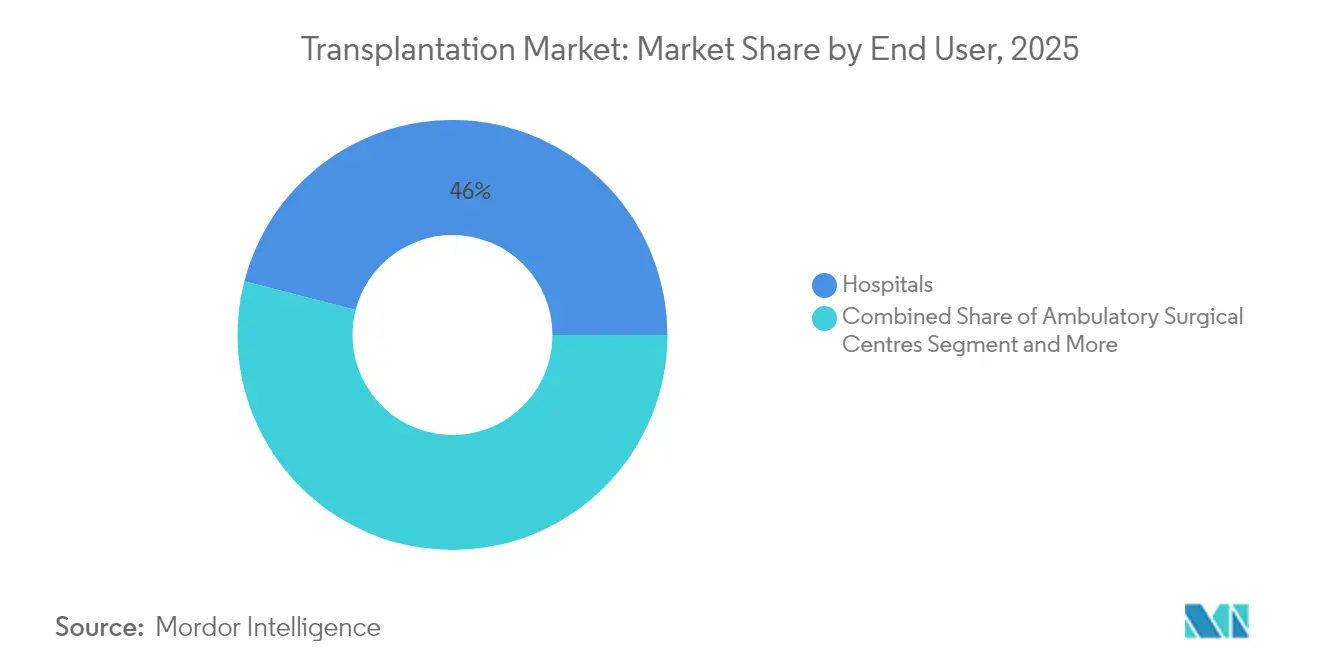

- By end user, hospitals held 45.98% of the transplantation market size in 2025, whereas ambulatory surgical centers are expanding at a 12.12% CAGR to 2031.

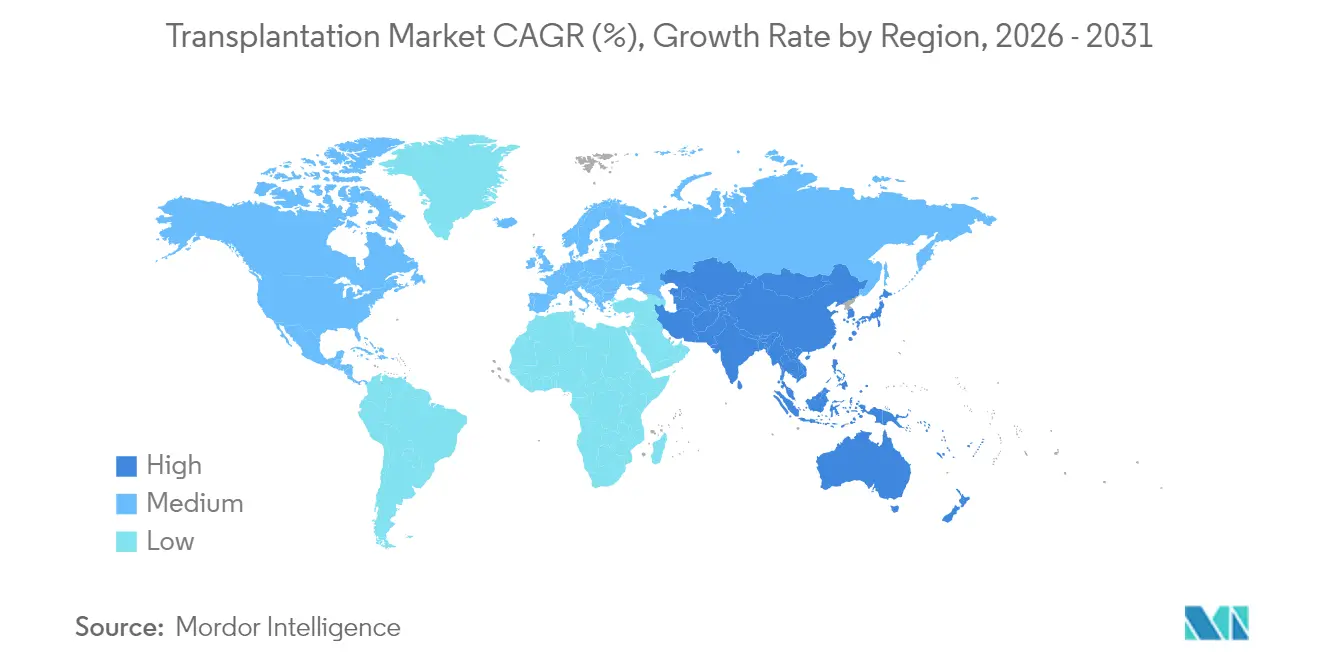

- By geography, North America dominated with a 37.35% revenue share in 2025, but Asia-Pacific is projected to post the fastest regional CAGR of 11.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transplantation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Burden Of Chronic Diseases | +2.1% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Increasing Burden Of Organ Failure | +1.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Technological Advancements In Transplantation Techniques | +1.5% | North America & EU leading, APAC adoption accelerating | Long term (≥ 4 years) |

| AI-Driven Donor-Recipient Matching Algorithms | +1.2% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Ex-Vivo Organ Perfusion Extending Preservation Windows | +1.4% | Global, with early adoption in North America | Medium term (2-4 years) |

| Tokenised Blockchain Donor-Registry Incentives | +0.8% | Pilot implementations in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Chronic Diseases

Rising prevalence of diabetes-related kidney failure, hepatitis-driven liver cirrhosis, and cardiovascular disorders enlarges the candidate pool for solid-organ procedures. In the United States, end-stage renal disease now affects over 750,000 individuals, driving kidney transplant demand at ratios exceeding 4:1 against donor availability. Aging populations in Western economies intensify chronic disease incidence, while healthcare systems expand transplant-center networks to manage rising caseloads. Nevertheless, structural supply constraints within the transplantation market persist despite incremental gains in donor registration.

Technological Advancements In Transplantation Techniques

Robotic-assisted surgeries reduce peri-operative complications, broadening eligibility to higher-risk recipients. Machine perfusion technologies stretch organ preservation from 6 hours to more than 20 hours, improving inter-regional sharing efficiency[1]International Society for Heart and Lung Transplantation, “Machine Perfusion Extends Long-Distance Heart Transplant Possibilities,” news-medical.net. Meanwhile, biomarker-guided immunosuppression minimizes rejection risk and improves long-term graft survival. These advances collectively strengthen patient outcomes and support wider adoption across the transplantation market.

AI-Driven Donor-Recipient Matching Algorithms

Machine-learning systems that evaluate genomic, immunologic, and clinical parameters now achieve 95% predictive accuracy for graft survival, outperforming conventional scoring methods[2]Rajkiran Deshpande, “Smart Match: Revolutionizing Organ Allocation Through Artificial Intelligence,” Frontiers in Artificial Intelligence, frontiersin.org. The UK-DTOP model reduced kidney wait-list mortality by nearly 20%, demonstrating the tangible clinical benefit of AI integration news-medical.net. Data-rich allocation strategies improve fairness, reduce organ discard rates, and create new service niches within the transplantation market.

Ex-Vivo Organ Perfusion Extending Preservation Windows

Hypothermic and normothermic perfusion platforms maintain physiologic temperatures and supply oxygenated perfusate, cutting primary graft dysfunction by more than 50% in heart transplants. Perfusion allows real-time viability assessment, enabling acceptance of extended-criteria organs and expanding the effective donor pool. Logistics flexibility resulting from longer preservation windows directly supports the geographic expansion of the transplantation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Organ Donors | -2.5% | Global, most acute in developing markets | Short term (≤ 2 years) |

| Ethical & Cultural Objections | -1.2% | Regional variations, highest in MENA & parts of APAC | Long term (≥ 4 years) |

| Antibiotic-Resistant Infections Raising Post-Transplant Risk | -1.8% | Global, concentrated in hospital-dense regions | Medium term (2-4 years) |

| Supply-Chain Fragility For Tacrolimus & Other APIs | -1.1% | Global, with regional supply disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Organ Donors

Only 3 out of every 1,000 deaths meet donation criteria, limiting available grafts even as waiting lists exceed 103,000 patients in the United States[3]Donald J. Trump, “National Donate Life Month, 2025,” Federal Register, federalregister.gov. Variability in consent rates and cultural barriers suppress donor pools in emerging economies, constraining the transplantation market despite technological advances.

Antibiotic-Resistant Infections Raising Post-Transplant Risk

Resistance to beta-lactams and carbapenems elevates morbidity among immunosuppressed recipients, with 75% of kidney transplant patients experiencing bacterial infection within the first year. Extended hospital stays add 40–60% to treatment costs, increasing economic pressure on providers and potentially inhibiting volume growth in the transplantation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Immunosuppressive Drugs Lead Despite Preservation Innovation

Immunosuppressive drugs accounted for 38.92% of the transplantation market size in 2025, reflecting their indispensable role in preventing graft rejection. Tacrolimus and mycophenolate retain physician preference even as generic uptake remains cautious because of narrow-therapeutic-index concerns. Supply disruptions—such as the FDA downgrade of Accord Healthcare’s tacrolimus bioequivalence status—spotlight vulnerabilities that can ripple across the transplantation market. Preservation devices, while still a smaller revenue pool, are the fastest-growing category at a 11.86% CAGR, underscoring strong clinician demand for longer organ storage and improved peri-operative outcomes.

Breakthrough platforms like Paragonix PancreasPak and SherpaPak differentiate on thermal control and real-time monitoring, encouraging broader adoption beyond leading academic centers. Tissue-engineering scaffolds are gaining clinical traction, expanding surgical options for corneal, bone, and cartilage repair. These dynamics suggest a gradual broadening of revenue sources within the transplantation industry as device-led innovations converge with long-established pharmacotherapy.

By Application: Tissue Transplantation Accelerates Beyond Organ Procedures

Solid-organ procedures retained 53.97% of 2025 revenue, with kidney transplants representing nearly 85% of organ volumes. The transplantation market share for tissue procedures is rising, propelled by corneal, bone, and cartilage grafts that benefit from streamlined outpatient pathways and improved reimbursement alignment. Living-donor liver programs and split-liver techniques also bolster organ utilization efficiency.

Tissue transplantation is projected to grow at 13.22% CAGR through 2031, driven by blindness-prevention initiatives and regenerative-medicine advances. Corneal transplants post 91.4% primary success, while cartilage repair leverages chondrocyte-based constructs that promise faster recovery. These gains illustrate how diversified clinical indications will underpin the next growth phase for the transplantation industry.

By End User: Ambulatory Centers Challenge Hospital Dominance

Hospitals commanded 45.98% of the transplantation market size in 2025, reinforced by integrated surgical suites, intensive-care capacity, and multidisciplinary expertise required for complex organ work. Academic centers remain referral hubs for heart and lung procedures. Yet the payer shift toward value-based models accelerates case migration to ambulatory surgical centers (ASCs), particularly for corneal and bone grafts.

ASCs are forecast to grow at a 12.12% CAGR as device miniaturization and enhanced peri-operative protocols enable safe same-day discharge. Collaborative programs between ASCs and hospital transplant teams enable higher-acuity patients to transition through hybrid care pathways. Research institutes further support innovation, conducting trials on AI-guided surveillance and sensor-based organ monitoring that could refine real-time post-operative management across the transplantation industry.

Geography Analysis

North America held a 37.35% revenue share in 2025, supported by mature reimbursement frameworks, donor-registry optimization, and adoption of ex-vivo perfusion technologies. The United States perennially conducts more than 40,000 transplants per year under OPTN stewardship and continues to refine allocation policies that integrate AI-based scoring for equitable distribution. Canada’s cross-border cooperation and Mexico’s medical-tourism offerings contribute incremental procedure volumes, reinforcing regional leadership within the transplantation market.

Asia-Pacific is projected to post an 11.25% CAGR to 2031, driven by regulatory harmonization and expanding private investment in transplant infrastructure. China, India, and Japan collectively accelerate installation of perfusion equipment and launch public-awareness drives aimed at raising donor consent rates. Regional governments adopt frameworks echoing European SoHO regulation standards, a move expected to improve quality assurance and cross-border tissue circulation. As disposable incomes climb and insurance coverage widens, procedural volumes surge, positioning Asia-Pacific as the fastest-growing cluster of the transplantation market.

Europe maintains steady growth on the back of harmonized procurement protocols and high donor rates in Spain, Portugal, and Croatia. Implementation of EU SoHO rules is set to further streamline tissue and cell movement across member states, benefiting multi-center research collaborations. Innovations in blockchain-based traceability and AI-enabled matching are tested through EU-funded pilot programs, reinforcing Europe’s influential role in shaping global best practices across the transplantation market.

Competitive Landscape

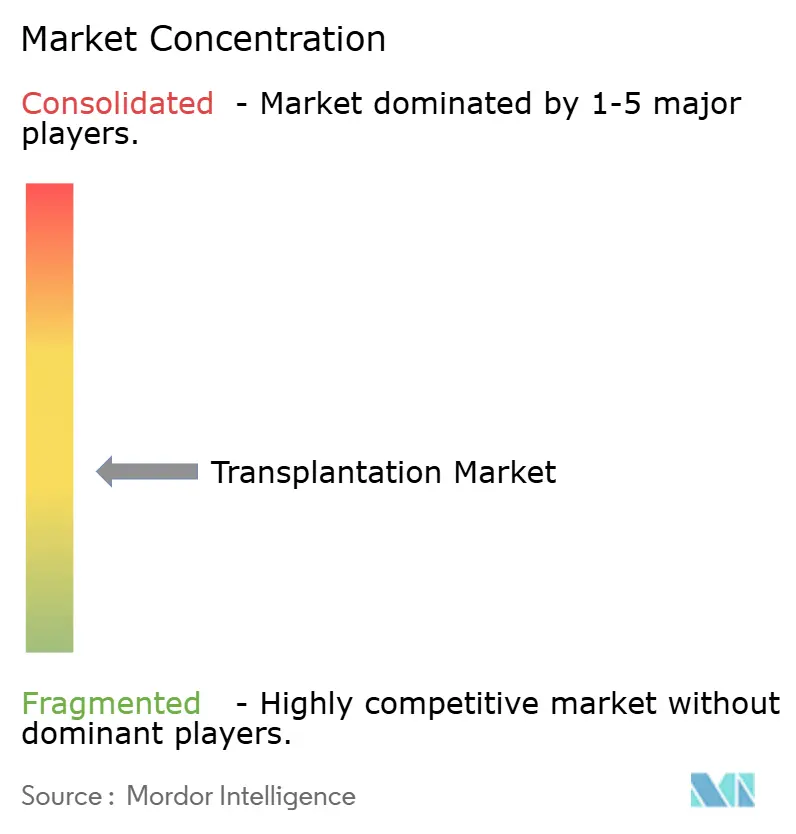

The transplantation market is moderately fragmented, with pharmaceutical majors such as AbbVie, Novartis, and Pfizer dominating immunosuppressive revenues while specialized device firms capture preservation-technology growth. Getinge’s acquisition of Paragonix consolidates leading cold-chain and perfusion capabilities under a unified portfolio, signaling intensifying strategic investment in device niches. Werfen’s USD 25 million purchase of Omixon expands access to next-generation transplant diagnostics, highlighting the commercial value of precision-matching data platforms.

Diagnostic providers including CareDx, Natera, and Eurofins Transplant Genomics expand post-graft surveillance offerings, often bundling molecular assays with AI-driven analytics. This service-centric positioning differentiates them from therapeutic incumbents and opens new subscription revenues within the transplantation market. Concurrently, United Therapeutics advances xenotransplantation milestones with successful UKidney and UThymoKidney procedures, potentially unlocking large-scale organ supply if long-term safety is confirmed.

Patent expirations on first-generation tacrolimus spur price competition and generic entry, while innovators shift focus to novel formulations such as LP-10 with protection through 2035. Device manufacturers accelerate R&D around normothermic perfusion, real-time sensor integration, and single-use disposables designed for ASCs. Start-ups leverage blockchain to secure end-to-end traceability, addressing ethical and compliance pressures as the transplantation market globalizes.

Transplantation Industry Leaders

Zimmer Biomet

Novartis AG

21st Century Medicine

Arthrex, Inc.

Strykers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace in transplantation sits at the intersection of preservation hardware and biologics. Transplant centers want longer out-of-body time, real-time viability assessment, and tighter immune-control without adding systemic toxicity. Evidence in 2026 research points to targeted, site-specific immunomodulation approaches (for example, nanotechnology-based and theranostic delivery concepts in pancreas transplantation and targeted nanodelivery tested in ex vivo lung perfusion models). This aligns with the report scope covering immunosuppressive drugs and preservation solutions and systems.

Another opportunity area is operational integration of advanced matching and monitoring workflows into routine transplant pathways as programs expand the use of extended-criteria organs. On the supply side, the market has incentives to broaden adoption of ex-vivo and machine-perfusion systems that extend preservation windows beyond 20 hours, improving inter-regional organ sharing and scheduling flexibility. On the therapy side, the continuing dominance of immunosuppressive drugs (38.92% share in 2025) alongside supply fragility for key agents, including tacrolimus API vulnerabilities noted in the report, supports demand for differentiated formulations, biomarker-guided dosing, and adjunct diagnostics aimed at reducing rejection and infection risk while standardizing outcomes across hospitals, transplant centers, and ambulatory settings.

Recent Industry Developments

- June 2026: United Therapeutics announced US FDA approval of the LungFX device for centralized ex vivo lung perfusion. The approval strengthens the commercial pathway for device-enabled organ preservation workflows and reinforces the role of perfusion infrastructure in expanding usable lung supply.

- April 2026: TransMedics highlighted the Controlled Hypothermic Organ Preservation System (CHOPS) around the International Society of Heart and Lung Transplantation 2026 Annual Meeting. The move underscores competitive emphasis on active, controlled preservation systems that fit alongside existing perfusion and logistics offerings used by transplant programs.

- April 2024: Zimmer Biomet reported progress on ROSA Shoulder usage, including first-surgery activity, advancing its robotics-enabled surgical ecosystem. While not an organ-transplant-specific product, the expansion of integrated surgical platforms supports broader operating-room modernization that can influence adoption of complex transplant and graft-related procedures in hospital settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the transplantation market is defined as the global value of products and services that enable human organ and tissue grafting across the transplant pathway, from preservation to post procedure management.

Scope exclusions: Cosmetic hair restoration and cell-therapy procedures that do not culminate in a grafted organ or tissue are excluded.

Segmentation Overview

- By Product

- Tissue Products

- Allograft Tissues

- Xenograft Tissues

- Synthetic Scaffolds & Matrices

- Immunosuppressive Drugs

- Calcineurin Inhibitors

- mTOR Inhibitors

- Antiproliferative Agents

- Monoclonal Antibodies

- Steroids & Others

- Preservation Solutions & Systems

- Static Cold Storage Solutions

- Hypothermic Machine Perfusion Solutions

- Normothermic Perfusion Systems

- Tissue Products

- By Application

- Organ Transplantation

- Kidney

- Liver

- Heart

- Lung

- Pancreas & Islet Cell

- Tissue Transplantation

- Cornea

- Bone & Cartilage

- Skin & Vascular Tissues

- Organ Transplantation

- By End User

- Hospitals

- Transplant Centres

- Ambulatory Surgical Centres

- Research & Academic Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to ground the size model in measurable activity signals, and to keep assumptions consistent across regions. We relied on public transplantation activity and health system references such as national transplant registries and annual reports (for example, UNOS and other country registries), WHO health statistics, OECD health data, and CDC health indicators where they apply to transplant related disease burden.

To translate activity into value, we reviewed peer-reviewed clinical and health economics literature on graft survival and therapy duration, plus government and hospital procurement notices where available, along with macro trade and customs summaries for relevant medical products. Company filings, investor presentations, and reputable press were also used to cross-check product mix trends and stated exposure to transplant drugs, preservation, and tissue products, supported by selective paid subscriptions for company financials and patent landscapes. These desk research sources are not exhaustive, and we also used other public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test the model where public data is thin, especially for average treatment duration, mix of maintenance versus induction therapy, and the real-world split of organ versus tissue workflows. We spoke with transplant clinicians, procurement and pharmacy leads, distributors, and product specialists across APAC, EMEA, and the Americas, which helped us align assumptions on pricing ranges, adoption of preservation solutions, and what is counted as transplant enabling spend.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 17% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where transplant procedure volumes and active patient pools are reconstructed by region, then mapped to spend buckets that sit logically in the transplant pathway. The value is derived by applying a market-consistent mix of immunosuppressive therapy, tissue product usage, and organ preservation solutions, followed by adjustments for differences in reimbursement access and hospital purchasing patterns.

To keep totals realistic, we ran selective bottom-up approximations as cross-checks. These included sampled ASP ranges multiplied by estimated unit volumes for major therapy classes and preservation solutions, and distributor channel checks for typical ordering frequency. The variables that drove the model most were transplant volumes by organ and major tissue types, graft survival and re-transplant rates, induction versus maintenance therapy shares, penetration of advanced preservation methods, and regional price corridors after currency conversion and inflation effects.

Forecasting was mainly supported through scenario analysis, since adoption and volume are sensitive to donor availability, policy shifts, and center capacity. The scenarios were tied to variables such as waiting list growth, transplant center throughput, and expected therapy duration trends, then refined using the consensus ranges heard in interviews. Where bottom-up data could not be cleanly built for smaller countries, we filled gaps using proxy rates based on comparable health system spend and transplant intensity, and then validated the implied per-procedure spend against expert feedback.

Data Validation & Update Cycle

Validation was done through a step-by-step set of checks where model outputs were compared with independent signals, including reported transplant activity, therapy utilization patterns discussed by clinicians, and public procurement pricing markers. If a region showed an unusual jump in implied spend per transplant, assumptions were revisited, and follow-up outreach was used to confirm whether the driver was a mix shift or pricing.

Before sign-off, the model and narrative are reviewed by another analyst to catch arithmetic issues and scope drift. We also sanity-checked the final dataset against recent events that could move demand or supply. The report is refreshed annually, and interim updates are made when material developments occur in policy, supply, or clinical practice. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Transplantation Market Size Versus Other Published Estimates

Published market sizes for transplantation can vary quite a bit, even when they sound like they cover the same topic. Differences usually come from what is counted as transplantation spend, which year is treated as the sizing anchor, and how procedure volume is translated into revenue.

The table highlights that the spread often comes from scope and counting rules, followed by how therapy duration and price progression are handled over time. Some estimates widen the basket to include adjacent hospital services and broader transplant care delivery costs, while others assume faster uptake of newer preservation approaches without matching that to reported procedure growth.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.88 B (2026) | |

| Industry Publisher A | USD 20.02 B (2026) | Uses a broader inclusion set that can blend in wider transplant service delivery spending and supporting hospital costs, which increases the value beyond product and procedure enabling revenue. |

| Market Tracker B | USD 32.70 B (2025) | Anchors the model on a different base year and appears to use a wider organ plus tissue definition with less transparent splits for drugs, tissue products, and preservation solutions, which can inflate totals after currency and inflation treatments. |

The table shows a higher 2026 figure when the spend basket is expanded, and under Mordor Intelligence's scope the number stays tied to transplant enabling products and solutions (including immunosuppressive drugs, tissue products, and organ preservation solutions) rather than the full hospital care cost around transplantation. When the same procedure signals and therapy duration checks are applied consistently, the output becomes easier to trace back to clear variables and to repeat each year with minimal scope drift.

Key Questions Answered in the Report

What is the global transplantation market’s current size and growth outlook?

The market is valued at USD 14.88 billion in 2026 and is projected to reach USD 23.39 billion by 2031, registering a 9.47% CAGR.

Which product category holds the largest transplantation market share?

Immunosuppressive drugs lead the landscape with 38.92% revenue share in 2025.

Which region will experience the fastest transplantation market growth?

Asia-Pacific is forecast to expand at an 11.25% CAGR through 2031, outpacing all other regions.

How do modern preservation technologies benefit transplant outcomes?

Ex-vivo perfusion platforms extend organ viability beyond 20 hours and cut primary graft dysfunction rates in heart transplants by more than 50%.

Why are ambulatory surgical centers gaining traction in transplantation services?

They provide cost-efficient, convenient settings for tissue and select organ procedures and are growing at a 12.12% CAGR.

Page last updated on: