Market Overview

| Study Period | 2020 - 2031 |

|---|---|

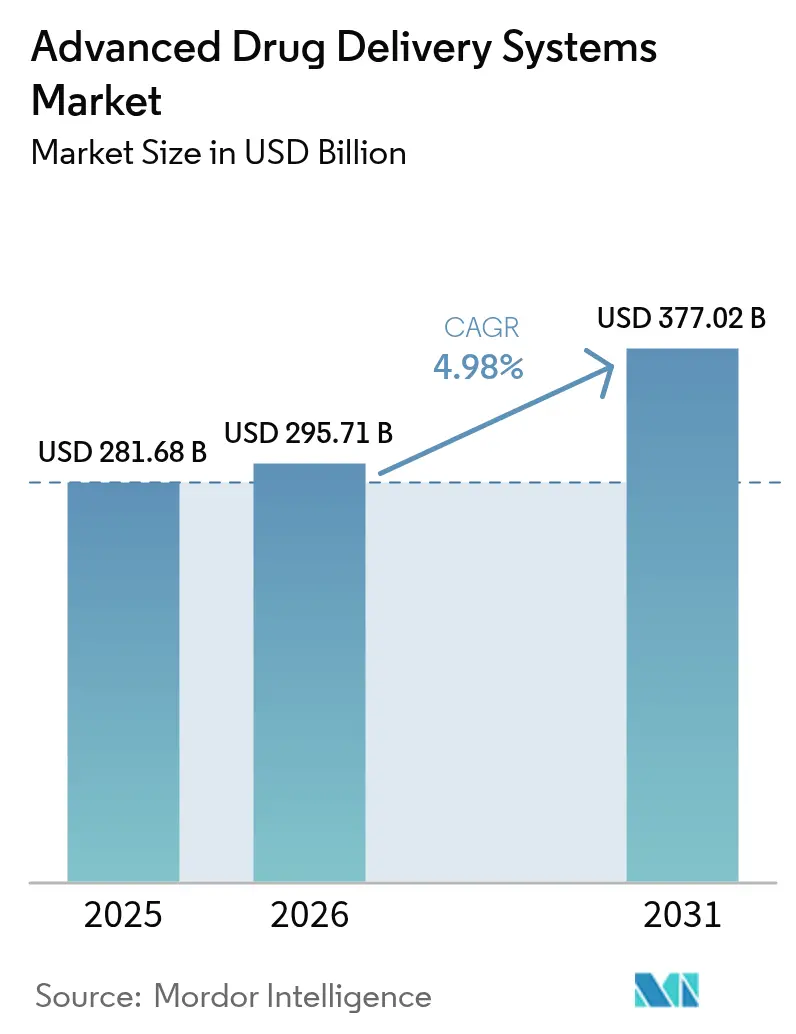

| Market Size (2026) | USD 295.71 Billion |

| Market Size (2031) | USD 377.02 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

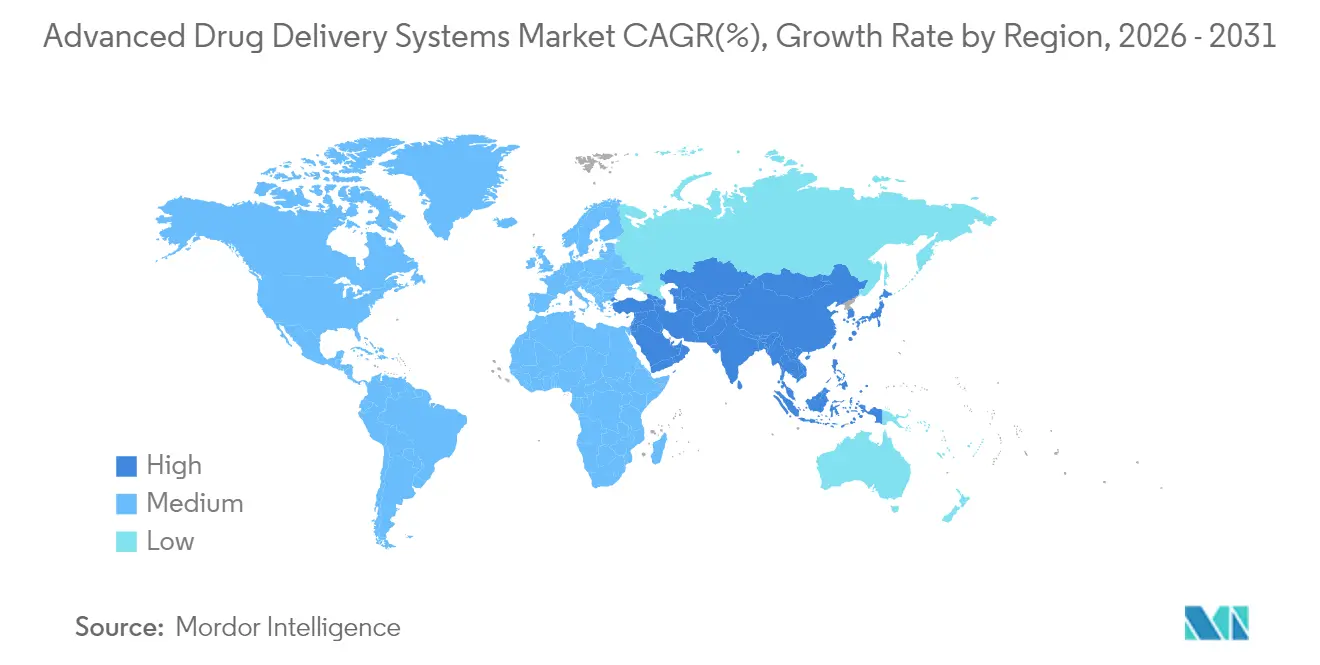

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Drug Delivery Systems Market Analysis by Mordor Intelligence

Advanced drug delivery systems market size in 2026 is estimated at USD 295.71 billion, growing from 2025 value of USD 281.68 billion with 2031 projections showing USD 377.02 billion, growing at 4.98% CAGR over 2026-2031. This steady climb reflects how sustained biologics innovation, nano-carrier breakthroughs, and patient-centric care models are reshaping therapeutic delivery. Lipid‐based nanoparticles, which already dominate formulation choices, are gaining traction in mRNA and siRNA pipelines, while smart electro-responsive implants show the fastest volume growth as they automate drug release in real time. Therapeutic demand concentrates in oncology, yet ophthalmology now logs the quickest rise owing to sustained-release ocular implants and drug-eluting contact lenses. Regionally, the advanced drug delivery systems market continues to lean toward North America, but Asia-Pacific’s regulatory convergence and low-cost production capacity are closing the gap. Competitive momentum intensifies as large pharmaceutical companies acquire agile platform developers to secure pipeline access and shorten launch timelines.[1]Novel Drug Delivery Systems: An Important Direction for Drug Innovation Research and Development, National Center for Biotechnology Information, pmc.ncbi.nlm.nih.gov

Key Report Takeaways

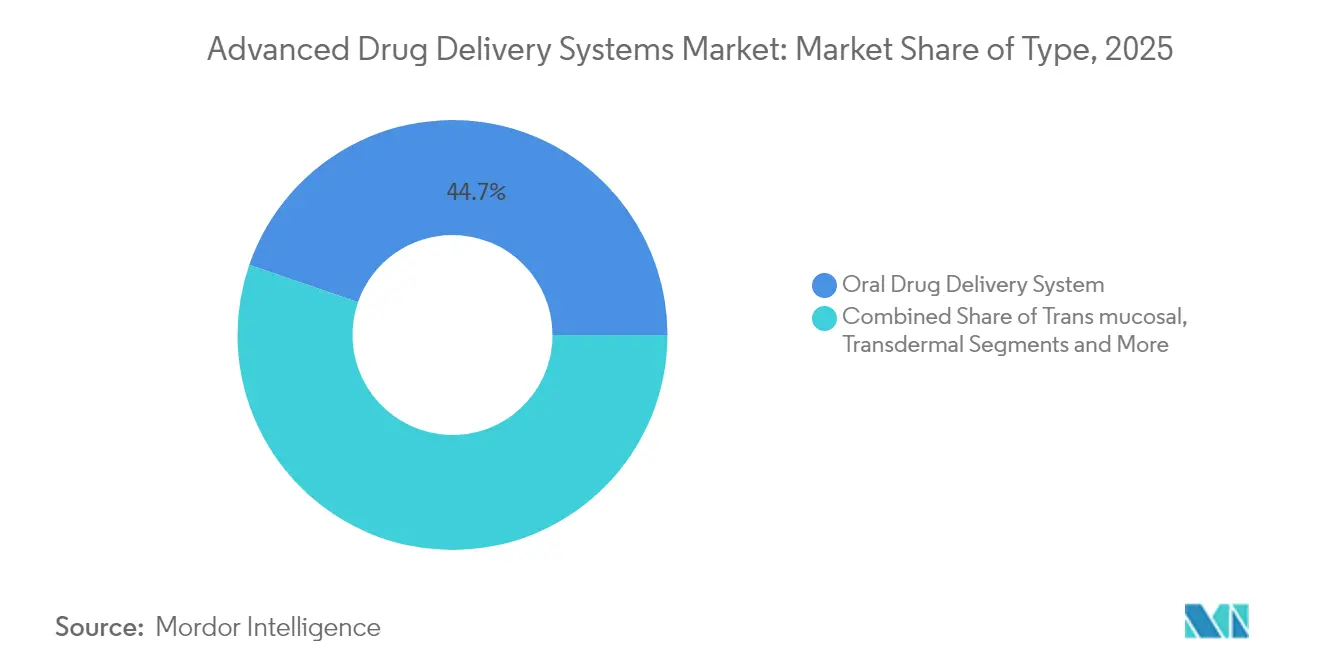

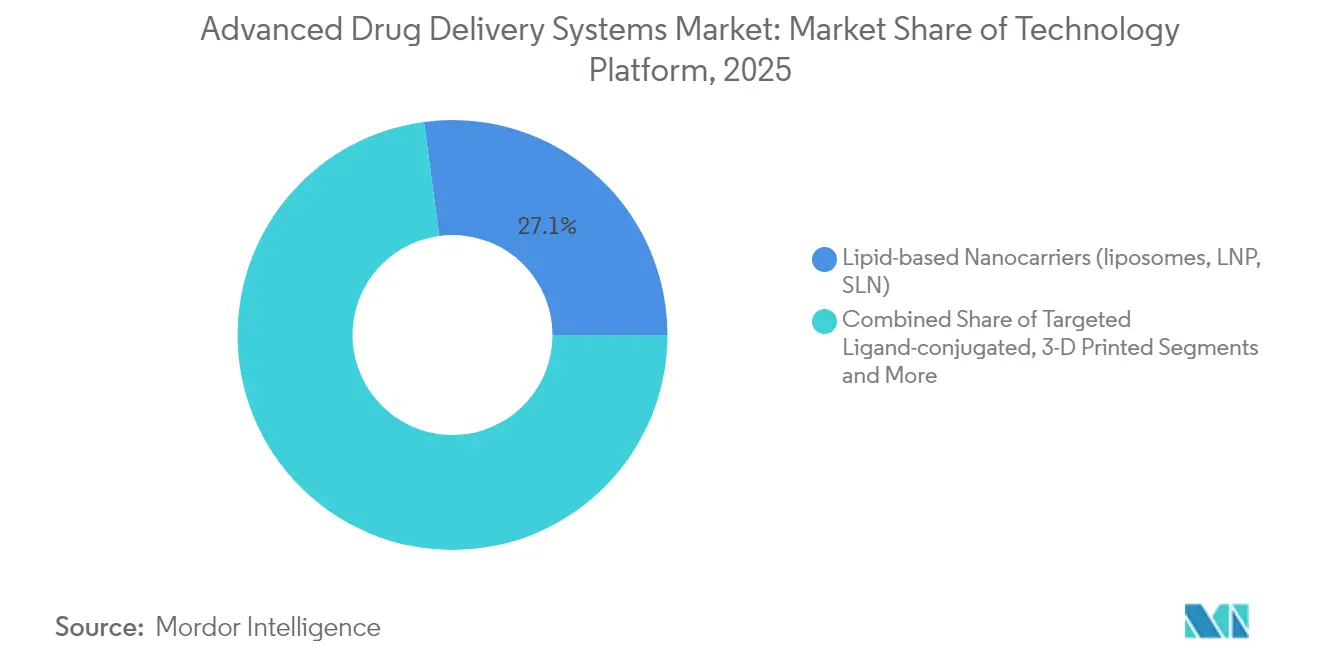

- By technology platform, lipid-based nanocarriers held 27.12% of the advanced drug delivery systems market share in 2025, while smart implantables and electro-responsive systems are projected to expand at a 9.41% CAGR to 2031.

- By application, oncology led with 29.83% revenue share in 2025; ophthalmology is forecast to grow at a 9.06% CAGR through 2031.

- By end-user, hospitals and clinics commanded 55.72% of the advanced drug delivery systems market size in 2025, while home-care and self-administration segments are advancing at an 8.44% CAGR.

- By geography, North America accounted for 37.05% of the advanced drug delivery systems market share in 2025; Asia-Pacific is set to expand at an 8.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Advanced Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics pipeline expansion | +1.2% | Global; strongest in North America and EU | Medium term (2-4 years) |

| Nano-carrier design breakthroughs | +0.9% | Global; APAC manufacturing hubs lead | Long term (≥ 4 years) |

| Chronic-disease prevalence & adherence focus | +0.8% | Global; amplified in aging economies | Long term (≥ 4 years) |

| Venture funding for platform DDS start-ups | +0.6% | North America & EU; APAC rising | Short term (≤ 2 years) |

| Micro-reservoir implants for digital therapeutics | +0.4% | North America & EU early adopters | Medium term (2-4 years) |

| 3D-printed personalized dosage forms | +0.3% | EU leads; North America follows | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biologics Pipeline Expansion

A widening biologics pipeline is reshaping delivery demands as proteins, antibodies, and nucleic-acid therapies require carriers that protect fragile structures and target complex tissues. Pfizer’s partnership with Bar-Ilan University on DNA nanorobots illustrates the push to marry biologic payloads with precision carriers. Oncology programs underscore this need: biologics now form more than 60% of active cancer trials, prompting delivery designs that cross vascular and cellular barriers without compromising potency. Combination products, such as Johnson & Johnson’s AKEEGA dual-action tablet, highlight how integrating two distinct mechanisms in one delivery format can cut disease progression by nearly half in BRCA-altered prostate cancer.

Nano-carrier Design Breakthroughs

Recent nano-carrier design wins are improving cell uptake, immune evasion, and payload capacity. Cubosome formulations achieve up to eight-fold greater cellular entry than traditional liposomes by fusing directly with membranes.[2]Lipid Nanoparticle Structure Shapes Cell Uptake, RMIT University, phys.org Ganglioside-based lipid nanoparticles remove PEG yet maintain stealth capabilities, addressing false-positive immunogenicity concerns.[3]Ganglioside-Incorporating Lipid Nanoparticles, Royal Society of Chemistry, pubs.rsc.org Artificial-intelligence screening now evaluates tens of millions of ionizable lipid candidates in silico, compressing discovery cycles and yielding delivery vectors optimized for mRNA therapeutics. Oregon State University’s lung-targeting nanoparticles extend these advantages into cystic fibrosis gene therapy trials.

Chronic-disease Prevalence & Adherence Focus

Relentless growth of chronic illnesses is fueling demand for devices that lessen dosing frequency and support home use. MIT’s ingestible capsule injects large-molecule drugs into the intestinal wall without needles, offering a future oral alternative for insulin or RNA therapies. Medtronic’s interoperable insulin pump links continuous glucose data with automated dosing to reduce burden on diabetes patients. Rice University’s biodegradable microcylinders release drugs steadily for up to five weeks, cutting refill frequency and bolstering adherence. The economic urgency is clear: US non-adherence still costs more than USD 100 billion yearly.

Venture Funding for Platform DDS Start-ups

Investors now view delivery technology as a scalable platform, not just a component of one therapy. BioSapien attracted USD 5.5 million for its 3D-printed localized oncology depot. Astraveus secured EUR 16.5 million to automate microfluidic cell and gene therapy manufacturing, aiming to trim production costs and timelines. NanoMedical Systems raised USD 7.21 million to adapt semiconductor processes for subcutaneous depots that meter medicine over months. Such rounds indicate growing confidence in plug-and-play platforms that can pivot across disease areas.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Batch-to-batch complexity & recalls | -0.7% | Global; stricter in North America & EU | Short term (≤ 2 years) |

| Stringent CMC & combination-product regulation | -0.5% | Global; FDA/EMA lead | Medium term (2-4 years) |

| Cold-chain cost escalation for biologic DDS | -0.4% | Global; heavier in emerging markets | Medium term (2-4 years) |

| Nano-carrier environmental toxicity concerns | -0.3% | EU scrutiny sets precedent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Batch-to-batch Complexity & Recalls

The FDA’s 2025 guidance on uniformity pressures manufacturers to adopt real-time analytics and continuous processing. Minor particle-size shifts in lipid nanoparticles can alter biodistribution and efficacy, exposing companies to costly recalls. Continuous manufacturing promises tighter control but demands high capital outlay and extensive validation, straining smaller firms.

Stringent CMC & Combination-product Regulation

Hybrid drug-device products blur oversight boundaries. The FDA’s draft guidance on essential device outputs for drug delivery adds new verification layers, extending development timelines. Nanomedicine dossiers now require full mechanistic toxicology studies. Latin American authorities still request country-specific artifacts, complicating global launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oral Dominance Faces Transdermal Disruption

Oral formulations retained 44.71% revenue share of the advanced drug delivery systems market in 2025, supported by familiar dosing and efficient manufacturing. Transdermal platforms are gaining at a 7.12% CAGR as microneedle patches and permeation enhancers deliver biologics without injections. The advanced drug delivery systems market size for oral products is projected to expand steadily, yet its share may slip as injectables and inhalables capture molecules that degrade in the gut. 3D-printed multilayer tablets, now in pilot production, show how oral systems will evolve to support precision dosing. Meanwhile, transdermal candidates leverage biodegradable microneedles that dissolve after insertion, eliminating sharp-waste handling. Pharmaceutical companies allocate R&D budgets toward long-acting transdermal contraceptives and hormone therapies that promise monthly or quarterly replacement cycles, boosting adherence and reducing clinic visits.

Patient acceptance drives this shift. Surveys indicate that more than 70% of adults prefer patch-based administration when equivalent efficacy is assured. Drug developers also appreciate the lower regulatory burden for line-extension strategies in transdermal formats because many excipients already hold GRAS status. However, achieving consistent flux across variable skin types remains a technical barrier. Collaborations with dermatology specialists aim to refine formulation rheology and backing-layer design to mitigate these challenges.

By Application: Oncology Leadership Challenged by Ophthalmology Surge

Oncology therapies commanded 29.83% of 2025 sales, a reflection of complex payload requirements and willingness to pay for targeted carriers. The advanced drug delivery systems market size for oncology is set to remain dominant as CAR-T, ADC, and radioligand pipelines reach commercialization. Johnson & Johnson’s TAR-200 intravesical system achieved an 82.4% complete response in bladder cancer, underscoring the potential of site-directed depots. Ophthalmology, however, grows fastest on the back of sustained-release implants like bimatoprost intracameral rings and anti-VEGF reservoirs. These devices cut injection frequency from monthly to twice yearly, reducing clinic burden.

Long-acting ocular inserts also widen chronic glaucoma coverage in regions with limited specialist access. Cardiovascular applications adopt biodegradable polymer stents that elute antiproliferative agents, while metabolic disorders advance weekly injectable GLP-1 analogs. Central nervous system indications face the blood-brain barrier hurdle, prompting research into focused ultrasound-activated carriers and intranasal routes that bypass systemic circulation.

By Technology Platform: Lipid Carriers Lead While Smart Systems Accelerate

Lipid nanoparticles, liposomes, and solid lipid carriers delivered 27.12% of 2025 revenue. Their modular structure suits both hydrophilic and lipophilic cargos, and scalable microfluidic manufacturing keeps costs predictable. Yet smart electro-responsive implants are on course for a 9.41% CAGR. These systems couple sensors with micro-pumps to adjust doses in real time, a transformative step for fluctuating conditions such as chronic pain. Polymeric carriers, including PLGA microspheres, maintain relevance by offering months-long depot action without hardware.

Targeted ligand-conjugated nanoparticles exploit tumor or tissue receptors to boost local concentrations while minimizing off-target impact. 3D printing supports prototype devices with integrated microfluidic channels, reducing iteration cycles from months to days. Microneedle arrays gain momentum for vaccines and biologics, as dissolving tips carry freeze-dried payloads that rehydrate in situ. The advanced drug delivery systems industry views combinatorial platforms—such as lipid-polymer hybrids—as a route to balance stability with responsive release.

By End-user: Hospital Dominance Shifts Toward Home Care

Hospitals and clinics held 55.72% share in 2025 thanks to infrastructure for infusion, monitoring, and complex dosing. Home-care and self-administration services, however, grow at 8.44% as payers encourage decentralized care. Remote-programmed auto-injectors, connected inhalers, and weekly oral capsules all support this migration. The advanced drug delivery systems market share for home-care segments should rise as Medicare and private insurers shift reimbursement toward outcome-based models that reward adherence.

Ambulatory specialty centers bridge inpatient and outpatient settings, providing oncology infusion suites and same-day procedures. Contract research and manufacturing partners supply customized micro-batch production, enabling rapid scaling of niche personalized therapies. Academic labs partner with start-ups to translate bench discoveries into GMP-ready candidates.

Geography Analysis

North America retained 37.05% revenue share in 2025, buoyed by a mature reimbursement system, deep venture pools, and the FDA’s support for innovative manufacturing pathways. The region also houses major contract manufacturers that can scale lipid nanoparticle production within validated clean-room suites. Johnson & Johnson allotted USD 1.56 billion for advanced delivery technologies within its MedTech division, ensuring sustained pipeline throughput. Novartis opened an Indianapolis radioligand facility to support targeted prostate cancer therapy, signaling confidence in complex carrier formats.

Asia-Pacific, expanding at an 8.02% CAGR, capitalizes on lower fabrication costs and robust government incentives. China channels public funds into nanotechnology hubs, while South Korea’s semiconductor expertise accelerates smart implant production. India’s pharmaceutical base is upgrading to accommodate sterile lipid nanoparticle lines, leveraging Make-in-India subsidies. Regulatory agencies across ASEAN align more closely with ICH guidelines, smoothing multi-country approvals.

Europe remains influential through rigorous safety standards and green manufacturing priorities. EMA’s guidance on nanotoxicology drives global benchmarks, compelling developers to adopt biodegradable excipients. Germany’s precision-engineering firms supply micro-molding equipment for implant housings, and Switzerland’s biotech cluster advances antibody-drug conjugate delivery. Post-Brexit, the United Kingdom implements accelerated pathways to keep pace with US fast-track programs.

Regulatory Landscape

Advanced drug delivery systems are increasingly regulated as drug-device combination products, which adds quality and labeling obligations that span both medicinal and device frameworks. In the United States, FDA combination products are governed under 21 CFR Part 4, which sets CGMP requirements when a product includes both drug and device constituent parts. This framework is central for autoinjectors, on-body injectors, prefilled syringes, and implantable delivery systems that fall within this report scope.

In the European Union, the Medical Device Regulation (EU) 2017/745 continues to shape the interface for integral drug-device combinations, including Article 117 requirements for a notified body opinion or CE certificate for the device part (with limited Class I exceptions). EMA coordination on these interface topics is supported through its Combination Products Operational Group (COMBO), reflecting the need to align medicinal-product dossiers with MDR general safety and performance requirements for the device element, as regulatory scrutiny extends into early 2026.

Value Chain Analysis

The value chain covers API and excipient sourcing, formulation and process development (including nanocarrier design and device-compatibility work), scale-up and GMP manufacturing, and final assembly and packaging of device-enabled formats such as prefilled syringes, autoinjectors, inhalation devices, and smart implantables. For lipid nanoparticles and other carrier systems, microfluidic mixing equipment and specialized raw materials feed into sterile drug-product operations. For combination products, device subcomponents (springs, plungers, molded housings) and primary containers (advanced glass syringes) become gating items alongside fill-finish capacity.

Bottlenecks increasingly cluster around long-lead device components and qualification activities tied to combination-product compliance, where procurement timing can affect launch schedules independent of clinical progress. In response, CDMOs and specialized partners are moving toward more integrated offerings that combine device assembly, sterile fill-finish, testing, and packaging, while manufacturers also invest in capacity and quality upgrades. This includes Sharp Services reported expansions in autoinjector and pen assembly capacity and broader commitments across prefilled syringe and autoinjector packaging infrastructure, alongside FDA quality system modernization under QMSR (effective February 2026), which raises the bar for device-constituent manufacturing controls.

Competitive Landscape

Competition spans pharmaceutical majors, mid-size device specialists, and venture-backed start-ups. Lipid nanoparticle production is relatively concentrated; firms with proprietary microfluidic reactors enjoy scale and quality advantages. Conversely, 3D-printed dosage forms remain fragmented as universities and early-stage companies experiment with printer architectures and photopolymer chemistries. Johnson & Johnson, Pfizer, Abbott, Medtronic, and Novartis collectively owned roughly one-third of global revenue in 2024, indicating a moderate consolidation trend.

Strategically, players shift toward platform versatility. Acquiring modular delivery technologies reduces time to market across therapy areas. Manufacturing innovation also drives differentiation: continuous processing lines cut changeover times, and inline spectroscopy verifies critical quality attributes without halting production. Artificial-intelligence tools fine-tune formulation parameters, predicting stability profiles and scaling needs faster than empirical trial-and-error.

Disruptors target immuno-oncology with cell-derived “attack particles,” challenge-testing the boundaries of conventional carrier thinking. Start-ups also pursue oral biologic routes, believing patient convenience will command premium pricing. Established firms answer by deepening collaborations with contract development and manufacturing organizations, exemplified by Samsung Biologics’ USD 223 million expansion of its Baxter partnership.

Advanced Drug Delivery Systems Industry Leaders

Boston Scientific Corporation

Becton, Dickinson and Company

Pfizer Inc

Novartis

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A core opportunity sits at the intersection of high-viscosity biologics and self-administration, where container-closure choices, device forces, and human factors performance determine whether therapies can shift from clinic administration toward home-care workflows. Recent industry actions provide concrete signals: BD expanded investment in U.S. manufacturing to support biologic drug delivery and, with Ypsomed, progressed higher-volume prefillable syringe compatibility for autoinjector platforms. Together, these steps reinforce the market whitespace for 5 mL-plus formats and integrated delivery systems designed to handle challenging formulations.

Technology whitespace is also visible in intelligent and miniaturized delivery devices that pair sensing with adaptive control, and in microneedle platforms positioned for minimally invasive delivery of peptides and biologics. Academic work in 2026 on programmable and spatially precise delivery concepts, alongside broader use of AI/ML for formulation optimization and PBPK modeling, supports development paths centered on tighter release control and faster iteration cycles. On the regulatory and operational side, FDA QMSR implementation (February 2026) and evolving post-market safety reporting expectations for drug-led combination products (including the move to E2B(R3) timing later in 2026) create an execution opportunity for manufacturers and partners that can standardize quality systems, documentation, and surveillance across global combination-product portfolios.

Recent Industry Developments

- July 2026: Novartis agreed to acquire Myricx Bio for USD 1.1 billion, bringing an ADC payload platform in-house. The acquisition strengthens vertical integration around targeted oncology modalities where delivery chemistry and linker-payload design influence efficacy and tolerability. It also reflects continued consolidation as large pharma secures differentiated delivery-enabling assets rather than relying solely on external platform access.

- June 2025: Johnson & Johnson received FDA approval for IMAAVY (nipocalimab-aahu) for generalized myasthenia gravis. The approval adds to the company's immunology portfolio and reinforces the commercial pull for delivery formats that support chronic administration and adherence. It also underscores the importance of CMC readiness and lifecycle planning for advanced therapies that may transition across care settings.

- April 2024: Medtronic filed 510(k) submissions for an interoperable insulin pump and an automated glycemic controller. These submissions support connected delivery ecosystems that combine sensing with automated dosing, aligning with the broader shift toward smart, patient-centric delivery devices. Progress in interoperable systems expands the addressable base for home-care and self-administration end users in advanced delivery markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the advanced drug delivery systems market is defined as the value of products and platforms that intentionally control how a drug is released and delivered to the body, so dosing, targeting, and patient use can be improved across care settings.

Scope exclusions: We exclude pure-play contract development services, primary packaging, and conventional or legacy syringes that do not provide an advanced delivery function.

Segmentation Overview

- By Type

- Oral Drug Delivery System

- Injection-based Drug Delivery System

- Inhalation/Pulmonary Drug Delivery System

- Transdermal Drug Delivery System

- Trans mucosal Drug Delivery System

- Carrier-based Drug Delivery System

- Other Types

- By Application

- Oncology

- Cardiovascular

- Metabolic (Diabetes, Obesity)

- CNS Disorders

- Infectious Diseases

- Ophthalmology

- Urology & Women’s Health

- Others

- By Technology Platform

- Pro-drug & Stimuli-responsive

- Lipid-based Nanocarriers (liposomes, LNP, SLN)

- Polymeric Nanocarriers (PLGA, PEG, micelles)

- Targeted Ligand-conjugated

- Smart Implantables & Electro-responsive

- 3-D Printed & Micro-needle

- Others

- By End-user

- Hospitals & Clinics

- Home-care & Self-administration

- Specialty & Ambulatory Centers

- CRO / CDMO & Academic Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to pin down the most repeatable external reference points. We relied on public sources such as the US FDA databases and guidance notes, the US Centers for Disease Control and Prevention, the World Health Organization, and published literature indexed in PubMed for therapy-level and delivery-route context.

To ground the commercial side, we also reviewed company annual reports, investor presentations, and product news releases, followed by checks on relevant association websites and reputable press coverage for device and formulation launches. Where needed, a paid subscription covering company financials and a patent database were used to cross-check ownership, platform focus, and stated pipeline direction. These examples are not exhaustive, and many other public sources were reviewed to fill gaps, validate inputs, and clarify assumptions.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with stakeholders across formulation and device development, manufacturing, procurement, and clinical-facing roles. Because adoption and reimbursement differ by geography, inputs were tested across APAC, EMEA, and the Americas, and then reconciled with route-level and therapy-area demand signals. When desk research created uncertainty around pricing or platform penetration, the assumptions were revisited with respondents and adjusted only when a consistent explanation was received from multiple angles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 50% |

| Mid tier: 49% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 20% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where therapy demand and treatment volumes are reconstructed by route of administration, and then translated into delivery-system value using realistic conversion assumptions. Results are then corroborated through selective bottom-up approximations, such as sampled price per unit times estimated patient or procedure volumes for key routes, plus channel checks to avoid overstating newer platforms.

Inputs used in the model include, for example, chronic disease treated population growth, injectable and self-administration penetration, shift toward controlled-release and depot use, device-enabled adherence trends, and expected pricing movement driven by mix (patches, inhaled products, implants, and nanocarrier-enabled formulations). When route-level data is incomplete, gaps are handled through proxy indicators such as procedure volumes, therapy regimen frequency, and expert-agreed adoption ranges, which are then narrowed during review.

Forecasts are developed using scenario analysis supported by a simple multivariate view of the main demand drivers, and then adjusted using primary feedback on uptake pace, regulatory timing, and product cycle effects. The final outlook is kept explainable so a client can trace each step back to a small set of measurable variables.

Data Validation & Update Cycle

Validation is done through multiple checks that look for mismatches between the model and independent signals, such as route-level volume trends, therapy mix shifts, and the pace of platform upgrades. If a number looks unusually high or low, we revisit the assumptions, re-check the desk sources, and then re-contact selected respondents to confirm what changed and why.

Before sign-off, the full workbook is reviewed in steps so that inputs, calculations, and outputs are consistent across regions and years. Reports are refreshed annually, and interim updates are done when a material event could change pricing, adoption, or supply availability. Right before delivery, a final pass is completed so the client receives the most current view available at that time.

Mordor Intelligence's Advanced Drug Delivery Systems Market Size Compared Against Other Published Estimates

Published market sizes for advanced drug delivery systems can vary more than expected, even when they seem to cover similar delivery platforms. The gaps usually come from different scope choices, different assumptions on pricing and mix, and differences in how quickly new delivery technologies are assumed to scale.

Some sources widen the definition by blending adjacent healthcare categories or by applying faster adoption curves to newer delivery formats, which can lift the near-term total. In Mordor Intelligence, value is counted only when an advanced delivery function is present in the commercialized product supply, and items like primary packaging, conventional syringes, and standalone development services are kept out to avoid double counting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 281.68 B (2025) | |

| Trade Publisher A | USD 299.60 B (2025) | Uses a broader inclusion set and a 2024 base-year framework that can roll adjacent administration and support elements into the value pool, which inflates the starting point versus a product-only count. |

| Global Consultancy B | USD 295.71 B (2026) | Anchors the headline number on a different current year and can shift results through currency timing and assumed mix of high-value platforms, making the 2026 snapshot not directly comparable to a 2025-based view. |

Overall, the spread in published values is explained by what gets counted as an advanced delivery system and by year alignment. Using a clear product scope, route-linked demand drivers, and repeated cross-checks from interviews keeps the estimate traceable, and it also makes updates easier when adoption pace or pricing changes.

Key Questions Answered in the Report

What is the current size of the advanced drug delivery systems market?

The market is valued at USD 295.71 billion in 2026 and is projected to reach USD 377.02 billion by 2031.

Which technology platform holds the largest share?

Lipid-based nanocarriers own 27.12% of 2025 revenue, reflecting their versatility for small-molecule and nucleic-acid payloads.

Which application is growing fastest?

Ophthalmology shows the highest CAGR at 9.06% through 2031, driven by sustained-release ocular implants and drug-eluting contact lenses.

Why is Asia-Pacific the fastest-growing region?

The region combines expanding healthcare budgets, harmonized regulations, and competitively priced manufacturing, supporting an 8.02% CAGR to 2031.

How are digital technologies influencing delivery systems?

Connected implants, RFID-tagged syringes, and AI-enabled pumps adjust dosing in real time and feed adherence data to clinicians, accelerating the transition to home-based care.

Page last updated on: