Hepatitis C Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.83 Billion |

| Market Size (2031) | USD 18.96 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hepatitis C Market Analysis by Mordor Intelligence

The Hepatitis C market size is expected to grow from USD 15.26 billion in 2025 to USD 15.83 billion in 2026 and is forecast to reach USD 18.96 billion by 2031 at 3.69% CAGR over 2026-2031. The shift from interferon regimens to highly curative direct-acting antivirals (DAAs) remains the principal force behind present revenue, yet the same curative success gradually shrinks the chronic patient pool. Intensifying universal screening campaigns, expansion of point-of-care testing, and government-funded elimination programmes counterbalance this contraction by pulling undiagnosed individuals into care pathways. Price negotiation frameworks in high-income countries and aggressive generic entry in emerging economies are pressing manufacturers to pursue ultra-short regimens, resistance-guided therapy, and geographical expansion. Digital “test-to-treat” models delivered through community pharmacies and telemedicine platforms are also reshaping patient acquisition and retention dynamics.

Key Report Takeaways

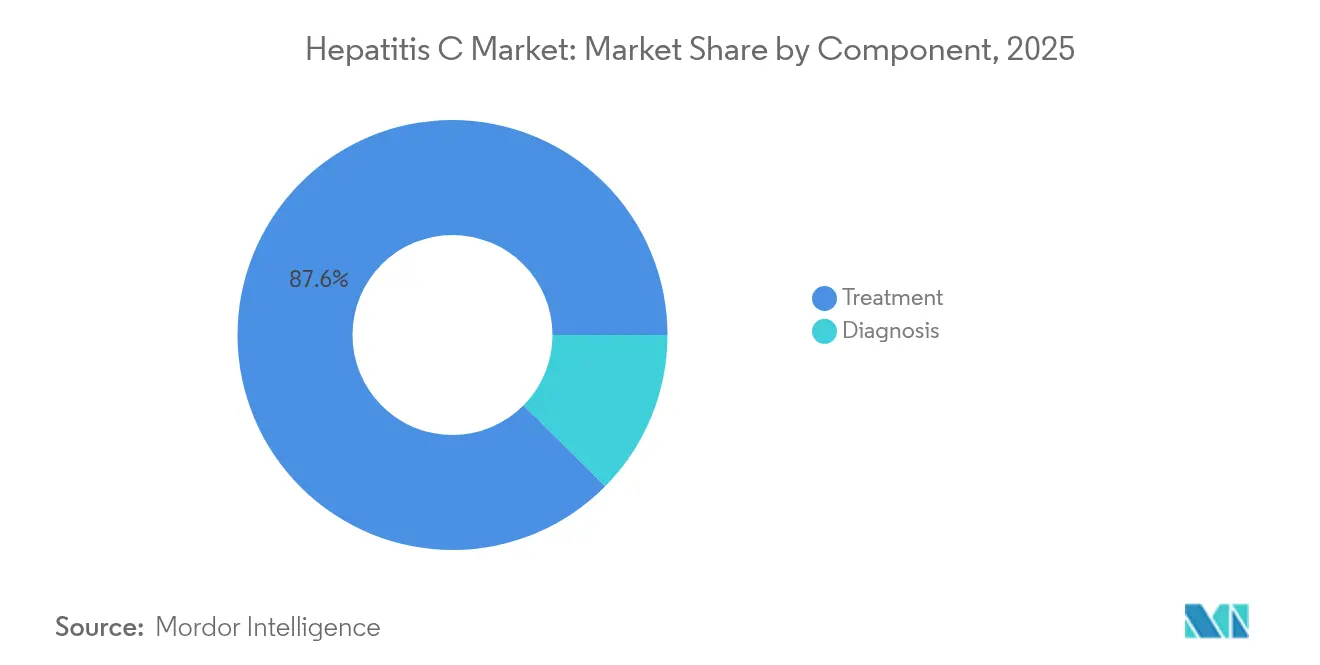

- By component, treatment held 87.58% of the Hepatitis C market share in 2025, whereas diagnostics is projected to register a 5.62% CAGR through 2031.

- By age group, the 18–45 cohort captured 62.11% of the Hepatitis C market size in 2025 and is expanding at a 4.19% CAGR to 2031.

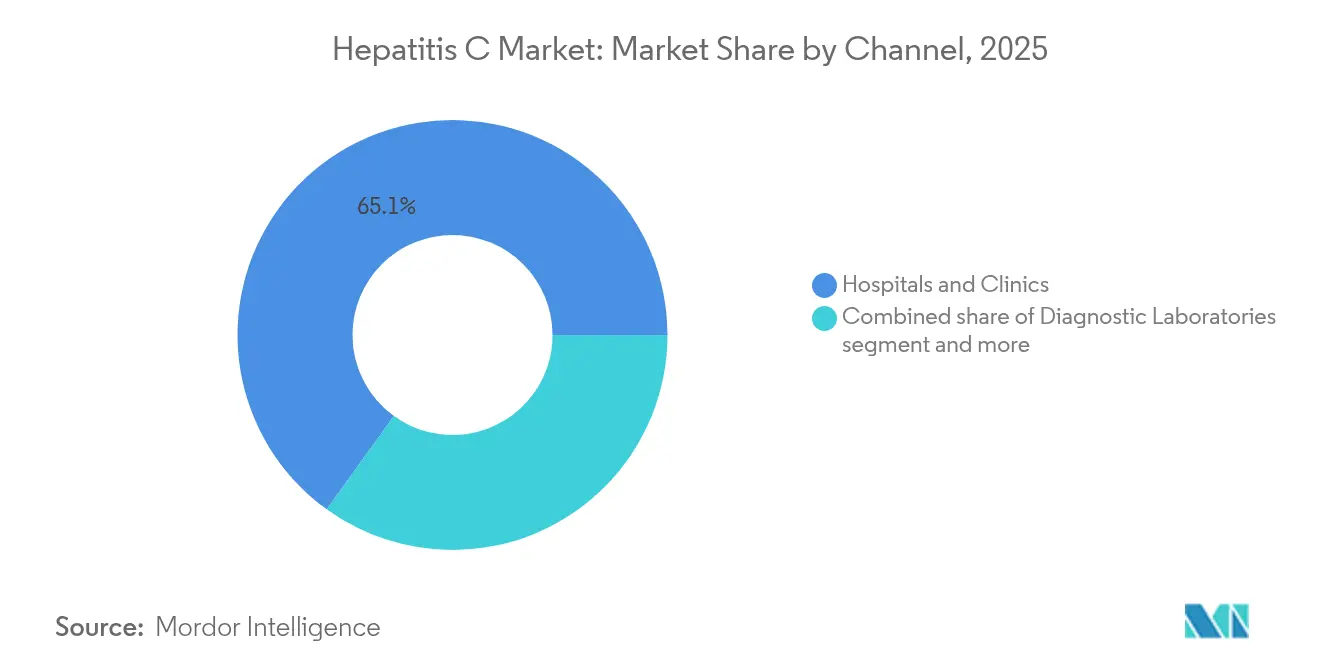

- By distribution channel, hospitals and clinics accounted for 65.05% of 2025 revenue, while community pharmacies and retail clinics show the fastest growth at a 5.38% CAGR.

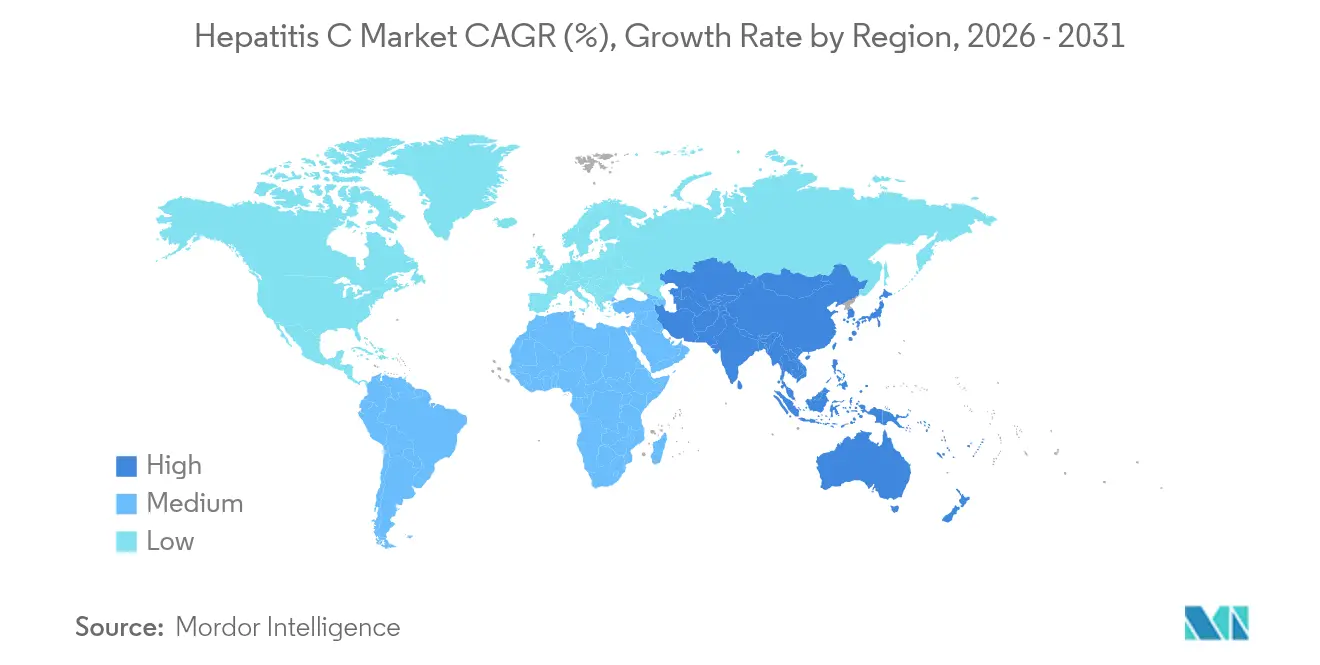

- By geography, North America led with 39.76% 2025 revenue, yet Asia-Pacific is poised for the quickest advance with a 4.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hepatitis C Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HCV Prevalence & Mandatory Universal Screening | +1.2% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Government-Funded National Elimination Initiatives | +0.9% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Advances in Point-of-Care and Molecular Diagnostics | +0.8% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Superior Cure Rates & Shorter Regimens of DAAs | +0.6% | Global | Long term (≥ 4 years) |

| Pharmacy-Led Decentralized "Test-To-Treat" Models | +0.5% | Global, with early gains in developed markets | Medium term (2-4 years) |

| AI-Guided Personalized DAA Regimen Optimization | +0.3% | North America & EU, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HCV Prevalence & Mandatory Universal Screening

Universal one-time or birth-cohort screening replaces risk-based approaches and uncovers hidden cases in rural and suburban populations. US Centers for Disease Control modelling shows that only one-third of diagnosed Americans achieved virologic cure between 2013 and 2022, underscoring latent demand for streamlined linkage-to-care pathways. Whole-population surveys in Europe reveal prevalence pockets above 1% among individuals[1]Kuan-Chen Pan, “Prevalence-based screening by anti-HCV reflex HCV antigen test and accessible post-screening care towards elimination of hepatitis C in rural villages,” BMC Gastroenterology, bmcgastroenterol.biomedcentral.com born between 1965 and 1985, far exceeding prior estimates. Countries meeting the World Health Organization’s 90% diagnosis target demonstrate markedly steeper treatment adoption curves than nations still at sub-30% awareness levels. As more public health agencies set mandatory screening in primary-care and emergency-department settings, diagnostic volumes continue to rise even while the chronic prevalence rate falls.

Government-Funded National Elimination Initiatives

Egypt’s national elimination programme treated over 4 million citizens and reached 87% cure, validating large-scale, publicly financed models. Australia, Canada, and Spain now provide unlimited DAA access through subscription or capped-payment contracts that align payer incentives with elimination targets. In the United States, a proposed USD 11 billion federal fund would cover the uninsured population and support state Medicaid treatment expansion, potentially adding 400,000 annual treatment starts by 2027. These schemes lock in predictable volumes[2]David W Matthews, “The Payer License Agreement, or “Netflix model,” for hepatitis C virus therapies enables universal treatment access, lowers costs and incentivizes innovation and competition,” Liver International, pmc.ncbi.nlm.nih.gov, allowing manufacturers to exchange price concessions for certainty while accelerating progress toward the 2030 elimination milestone.

Advances in Point-of-Care and Molecular Diagnostics

Cepheid’s finger-stick GeneXpert assay delivers confirmed RNA results in under an hour and boosts same-day treatment initiation rates to 84% in community clinics. Implementation studies in Vietnam indicate that a single-visit screen-confirm-treat workflow retains 92% of patients through cure, compared with 54% under conventional two-visit testing. High-throughput next-generation sequencing labs in the United Kingdom now provide real-time resistance surveillance, informing local procurement of salvage regimens. Cost per diagnosis falls as cartridge prices descend below USD 7 in tender markets, making population screening financially viable for middle-income governments.

Superior Cure Rates & Shorter Regimens of DAAs

Pan-genotypic combinations such as sofosbuvir/velpatasvir consistently exceed 95% sustained virologic response across all fibrosis stages. Pipeline agents aim to compress therapy to 2–4 weeks to improve adherence and cut pharmacy costs, with Atea Pharmaceuticals advancing Bemnifosbuvir plus Ruzasvir combination[3]Atea Pharmaceuticals, “Atea Pharmaceuticals Announces Dosing of First Patient in C-BEYOND, Phase 3 Study Evaluating Regimen of Bemnifosbuvir and Ruzasvir for Treatment of Hepatitis C Virus,” ateapharma.com into Phase 3. High success rates, however, shorten average revenue per patient lifetime and compel firms to diversify into retreatment niches, co-morbid liver disorders, and geographic expansion. Resistance-associated substitutions emerging in 3–5% of previously treated patients underpin demand for salvage therapies, while pan-genotypic potency simplifies procurement for resource-limited buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Branded-Therapy Cost & Reimbursement Gaps | -0.7% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Large Undiagnosed Pool & Social Stigma | -0.4% | Global, with higher impact in developing regions | Long term (≥ 4 years) |

| Specialist-Prescription & Retreatment Restrictions | -0.3% | North America & EU, regulated healthcare systems | Medium term (2-4 years) |

| Emerging Antiviral-Resistance Mutations | -0.2% | Global, concentrated in treatment-experienced populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Branded-Therapy Cost & Reimbursement Gaps

Course prices for branded pan-genotypic DAAs remain near USD 24,000 in many high-income markets, leading to restrictive payer criteria based on fibrosis stage or sobriety requirements. Out-of-pocket cost exposure discourages treatment among uninsured or under-insured populations, even where community health centres offer low-cost screening. Generic sofosbuvir/velpatasvir is available for under USD 100 in India, Pakistan, and Egypt, yet patent claws and exclusivity clauses keep list prices elevated elsewhere. The cumulative spend, including confirmatory RNA tests, fibrosis staging, and specialist visits, can exceed USD 30,000 per person, hampering uptake despite proven cost-effectiveness.

Large undiagnosed pool & social stigma

An estimated 81% of people with chronic infection worldwide remain unaware of their status. Fear of discrimination tied to injection-drug use, incarceration history, or migrant status deters many from voluntary testing. Passive screening in primary care settings misses asymptomatic individuals, while provider bias leads to under-ordering of HCV assays for older adults without obvious risk factors. The resulting late diagnoses coincide with advanced liver disease, raising treatment complexity and healthcare costs. Community-based outreach programmes combined with anonymity-preserving rapid tests have begun to close this gap, yet stigma continues to dampen overall market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Treatment maintains revenue dominance

Treatment accounted for 87.58% of the Hepatitis C market share in 2025, reflecting the high unit value of DAAs that sell at premium prices in many countries. Direct-acting antivirals anchored by sofosbuvir combinations generated the bulk of segment turnover, with Harvoni and Epclusa alone surpassing USD 9 billion in global sales in 2024. Pegylated-interferon/ribavirin now constitutes a single-digit niche for interferon-eligible patients, while immunomodulatory adjuncts are under investigation for non-responders. The Hepatitis C market size for treatment could reach USD 16.85 billion by 2031 if current reimbursement frameworks hold.

Diagnosis, although smaller, is rising at a 5.62% CAGR as universal screening, antenatal testing, and prison-based programmes increase test volumes. Point-of-care antibody assays, reflex RNA cartridges, and high-throughput NAAT platforms dominate procurement tenders in Asia-Pacific and Latin America. Molecular sub-typing and resistance sequencing deliver incremental revenue by guiding personalized therapy. An integrated “test-to-treat” workflow retains patients and extends value capture across both component categories, mitigating treatment-segment contraction caused by shrinking prevalence.

By Age Group: Baby boomers underpin demand

Adults aged 18–45 represented 62.11% of the 2025 Hepatitis C market size, a legacy of widespread transfusion-related and injection-drug transmission during the 1960s–1980s. As this cohort ages into Medicare or equivalent public coverage, payer policies increasingly cover pan-genotypic regimens without fibrosis restrictions, sustaining growth at a 4.19% CAGR. The Hepatitis C market size attached to this cohort is projected to exceed USD 10.62 billion by 2031.

Patients under 18 account for a low revenue base due to limited vertical transmission; nevertheless, pediatric approvals of sofosbuvir/velpatasvir since 2024 broaden accessible therapy. Individuals over 45 contribute a stable but slower-growing share, often presenting with cirrhosis or co-morbidities that heighten monitoring costs. Age-linked pharmacokinetic shifts call for dose adjustments, creating incremental demand for real-time drug-interaction software embedded into electronic health records.

By Channel: Decentralization accelerates

Hospitals and specialist clinics retained 65.05% of the Hepatitis C market share in 2025 owing to historic reliance on hepatologists and infectious-disease physicians for prescription and monitoring. Yet community pharmacies and retail clinics, growing at a 5.38% CAGR, are redefining patient flow by offering on-site RNA confirmation and same-day dispensing. Randomized evaluations in the United States show pharmacy-initiated treatment achieving 90.3% cure, compared with 39.4% under referral pathways.

Telemedicine platforms embedded in opioid-substitution clinics extend reach into rural zones, while mobile vans screen high-risk groups at festivals and homeless shelters. Diagnostic laboratories keep stable revenue via bulk testing contracts with correctional facilities and antenatal clinics. As payer networks reimburse pharmacist prescribing and remote monitoring, the Hepatitis C market is gradually shifting towards a more distributed footprint that counters capacity constraints in tertiary centres.

Geography Analysis

North America commanded 39.76% of the Hepatitis C market share in 2025, powered by comprehensive screening mandates, premium branded pricing, and broad Medicaid coverage. However, growth moderates to a 3.28% CAGR as prevalence declines in previously untreated baby boomers. The proposed federal elimination fund, if enacted, could still add large treatment volumes by underwriting uninsured care. Canada aligns drug pricing with health-technology assessments, capping list prices, while Mexico’s Seguro Popular programme is beginning to subsidise locally manufactured generics, anchoring volume growth despite lower per-patient spend.

Europe accounts for a sizeable share and shows a 3.01% CAGR through 2031. Joint procurement initiatives under the Beneluxa coalition and national subscription deals in Spain and Portugal have trimmed treatment course prices by 45% since 2022. The United Kingdom reports a 51.6% drop in chronic infection prevalence after integrating whole-genome surveillance with direct community outreach. Eastern European nations, backed by Global Fund transition grants, are scaling harm-reduction, testing, and treatment packages among people who inject drugs, unlocking additional diagnostic volumes.

Asia-Pacific is the fastest-growing territory, expanding at 4.83% CAGR. China’s volume-based procurement brought down the sofosbuvir/velpatasvir price ceiling by 68% in the 2024 tender round, catalysing provincial bulk-buy orders. India’s National Viral Hepatitis Control Programme finances generics at under USD 100 per course and reimbursed more than 550,000 treatments in 2024. Malaysia, Thailand, and Vietnam deploy the “Netflix” capped-price model, facilitating mass campaigns among high-burden populations. The Hepatitis C market share derived from Asia-Pacific is expected to climb above 28.64% by 2031, powered by aggressive elimination goals paired with domestic manufacturing.

Competitive Landscape

The Hepatitis C market remains oligopolistic. Gilead Sciences holds a significant share in the United States and also in the European Union through Harvoni and Epclusa franchises. AbbVie’s MAVYRET secures the main counterweight, offering an 8-week pan-genotypic regimen and discount contracting. Bristol Myers Squibb’s daclatasvir-based combinations and Merck’s grazoprevir/elbavir retain smaller shares, largely in lower-income markets.

Competition is tempered by formidable entry barriers: Phase 3 trial costs, stringent virologic endpoints, and post-marketing safety surveillance. The curative character of DAAs also constricts the obtainable patient pool, obliging companies to diversify into advanced liver disease, non-alcoholic steatohepatitis, and rare cholestatic conditions. Gilead’s USD 4.3 billion acquisition of CymaBay in 2024 moves the firm into primary biliary cholangitis and illustrates a shift toward adjacent hepatology indications.

Technology partnerships with digital-health firms aim to safeguard market position through algorithmic adherence platforms and AI-guided resistance dashboards. Legal challenges linger: Gilead’s 2023 10-K confirms ongoing patent and pricing litigations across multiple jurisdictions, spotlighting the regulatory complexity underpinning this mature therapeutic area. Despite those pressures, the combined top-five share still surpasses 85%, preserving high market concentration.

Hepatitis C Industry Leaders

Abbott Laboratories Inc.

Bristol-Myers Squibb Co.

F. Hoffmann-La Roche

Gilead Sciences Inc.

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Médecins Sans Frontières expanded its hepatitis C programme in the Rohingya camps of Cox’s Bazar, Bangladesh, targeting 30,000 treatments by 2026.

- March 2025: The UK Health Security Agency launched a national genomic surveillance project to track antiviral resistance in circulating HCV strains.

- December 2024: Atea Pharmaceuticals announced progression to Phase 3 trials for its ultra-short bemnifosbuvir/ruzasvir combination.

- July 2024: Pakistan unveiled the Prime Minister’s Hepatitis C Eradication Programme, pledging free nationwide treatment.

Global Hepatitis C Market Report Scope

Hepatitis C is a viral infection that causes liver inflammation, sometimes leading to severe liver damage. Hepatitis C testing and therapeutic interventions are essential components in managing hepatitis C.

The hepatitis C market is segmented by type (diagnosis (liver biopsy, blood tests, and other diagnoses) and treatment (antiviral drugs, immune modulator drugs, and other treatments)), end-user (hospitals and clinics, diagnostic laboratories, and other end-users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Diagnosis | Blood Tests |

| Rapid/POC Tests | |

| Molecular (PCR, NAAT) | |

| Sequencing-based Genotyping | |

| Others | |

| Treatment | Direct-Acting Antivirals (DAAs) |

| Pegylated Interferon + Ribavirin | |

| Adjunct Immunomodulators |

| Below 18 |

| 18 - 45 |

| Above 45 |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Community Pharmacies & Retail Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Diagnosis | Blood Tests |

| Rapid/POC Tests | ||

| Molecular (PCR, NAAT) | ||

| Sequencing-based Genotyping | ||

| Others | ||

| Treatment | Direct-Acting Antivirals (DAAs) | |

| Pegylated Interferon + Ribavirin | ||

| Adjunct Immunomodulators | ||

| By Age Group | Below 18 | |

| 18 - 45 | ||

| Above 45 | ||

| By Channel | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Community Pharmacies & Retail Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Why do direct-acting antivirals remain the core revenue driver in the hepatitis C market?

Their ability to cure infection with short, well-tolerated oral regimens keeps them the default therapeutic choice, sustaining high per-patient value even as overall patient volume falls.

How are universal screening policies reshaping demand for hepatitis C diagnostics?

Mandated one-time or birth-cohort testing is uncovering previously hidden infections, greatly increasing test throughput and accelerating linkage-to-care workflows.

What impact are government-funded elimination programs having on commercial strategies?

Large, prepaid treatment contracts give manufacturers predictable volumes in exchange for lower per-course pricing, prompting companies to prioritize public-health tenders over traditional retail channels.

Why are community pharmacies and retail clinics gaining traction for hepatitis C care delivery?

Decentralized “test-to-treat” models at these venues remove specialist bottlenecks, enable same-day therapy initiation, and improve adherence among hard-to-reach populations.

How is generic competition influencing pricing dynamics for branded hepatitis C drugs?

Entry of low-cost generics in emerging markets is pressuring brand owners to offer tiered pricing or shorter regimens in order to remain competitive and defend market share.

Page last updated on: