Organ Transplantation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

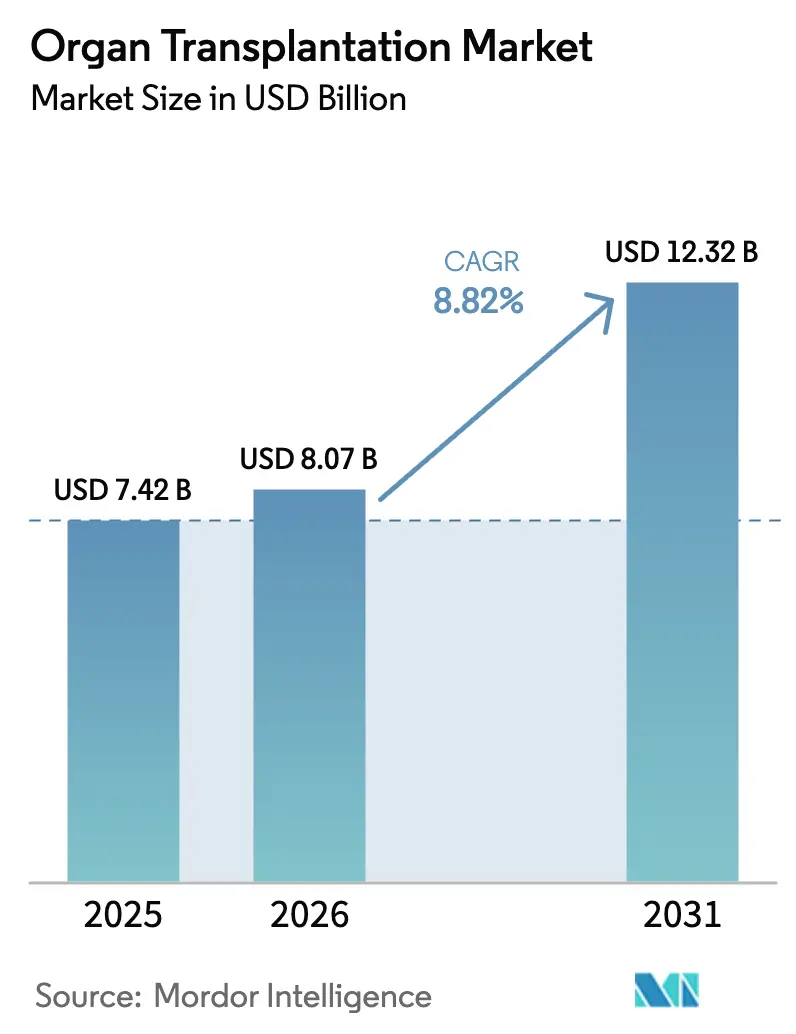

| Market Size (2026) | USD 8.07 Billion |

| Market Size (2031) | USD 12.32 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

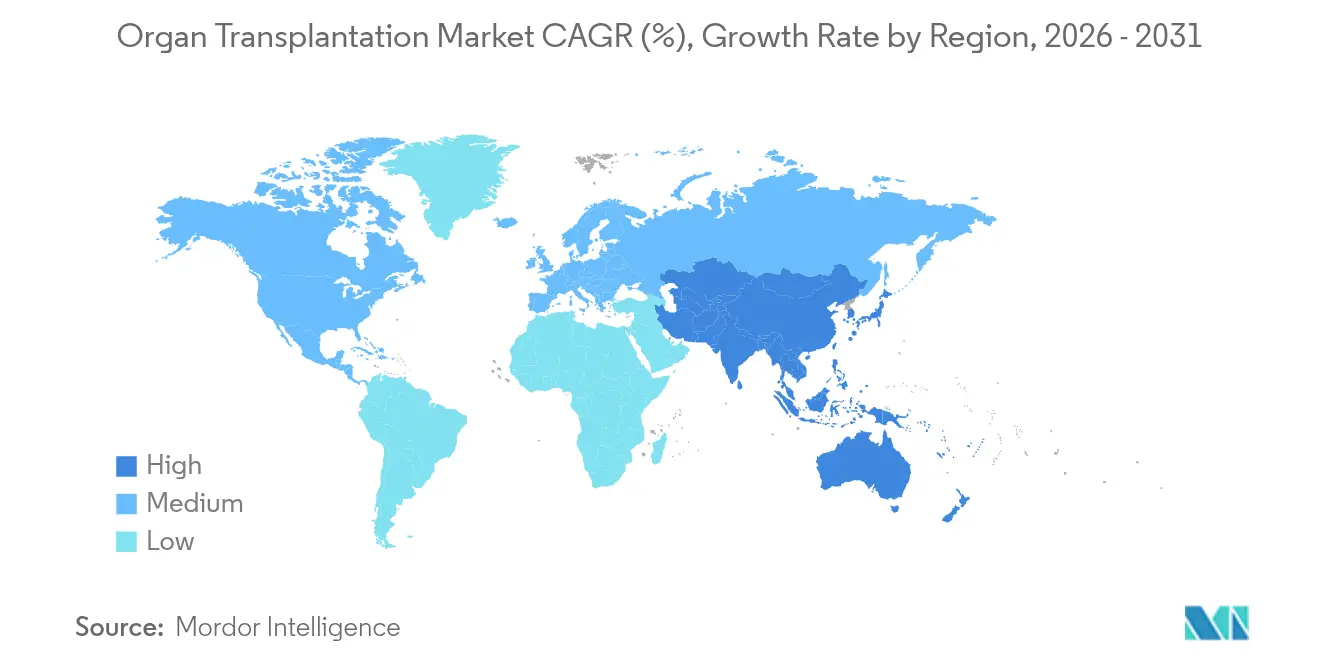

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

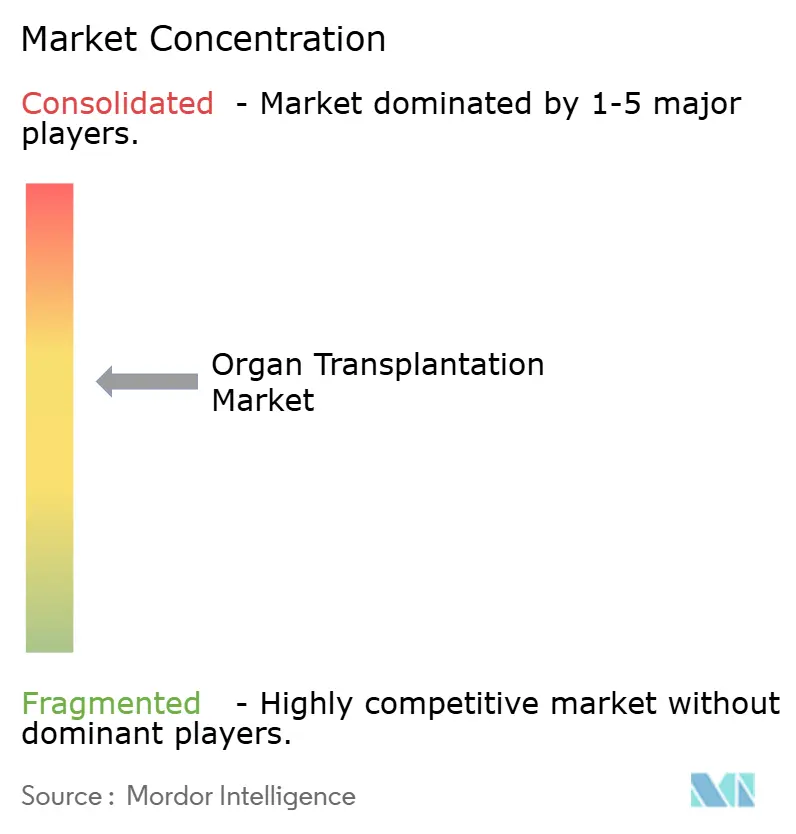

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organ Transplantation Market Analysis by Mordor Intelligence

The organ transplantation market size was valued at USD 7.42 billion in 2025 and estimated to grow from USD 8.07 billion in 2026 to reach USD 12.32 billion by 2031, at a CAGR of 8.82% during the forecast period (2026-2031). Strong demand stems from the rising incidence of end-stage organ failure, breakthrough approvals for xenotransplantation studies, and the rapid uptake of next-generation preservation devices that extend viability far beyond traditional cold-storage thresholds. North American pilot programs for pig-to-human transplants and global investments in normothermic machine perfusion collectively broaden the effective donor pool while reducing post-surgical complications. Digital tools—from AI-based donor-recipient matching to blockchain logistics—streamline allocation and tracking, enabling faster organ placement and improving graft survival outcomes. Expanding access to affordable immunosuppressive therapies in Asia-Pacific further boosts procedures, while government-backed awareness drives help narrow the gap between registered donors and wait-list demand.

Key Report Takeaways

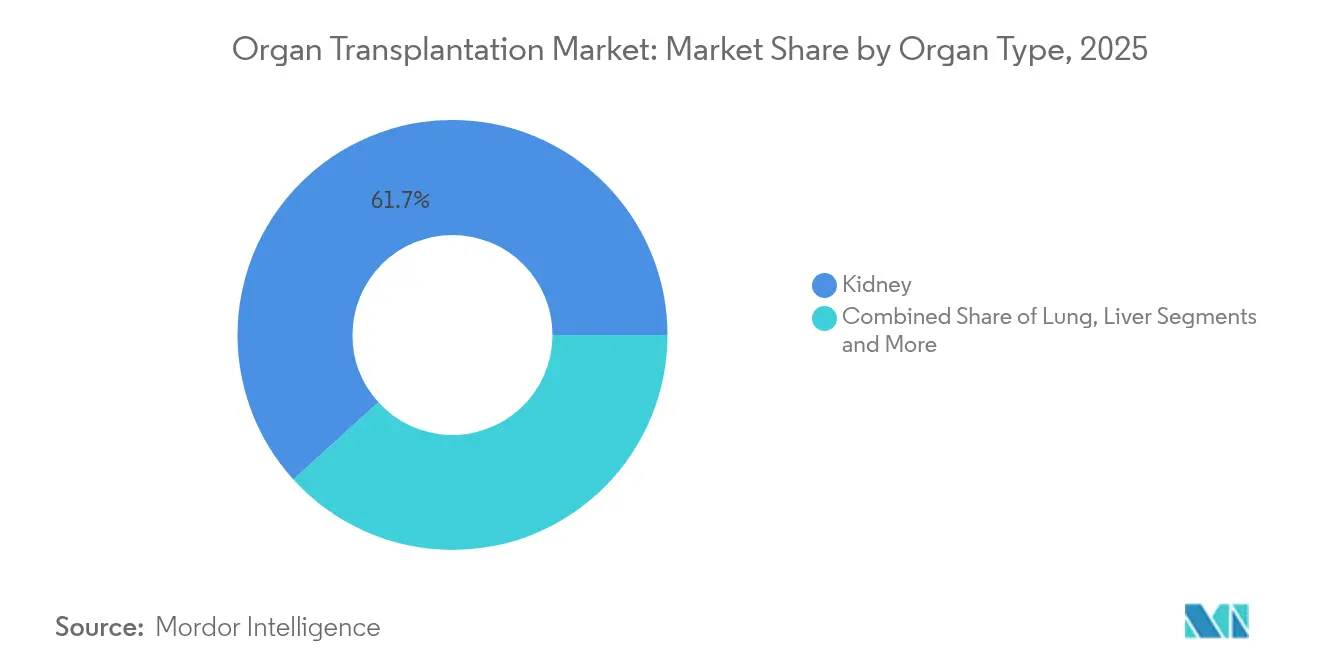

- By organ type, kidneys led with 61.74% of organ transplantation market share in 2025; lung transplants are projected to grow at a 9.11% CAGR to 2031.

- By donor type, deceased donor procedures accounted for 69.02% of the organ transplantation market size in 2025, while living‐donor volumes are advancing at a 9.22% CAGR to 2031.

- By type of transplant, allogeneic surgeries dominated with 83.35% share in 2025; xenotransplant and composite tissue procedures are expanding at a 12.95% CAGR through 2031.

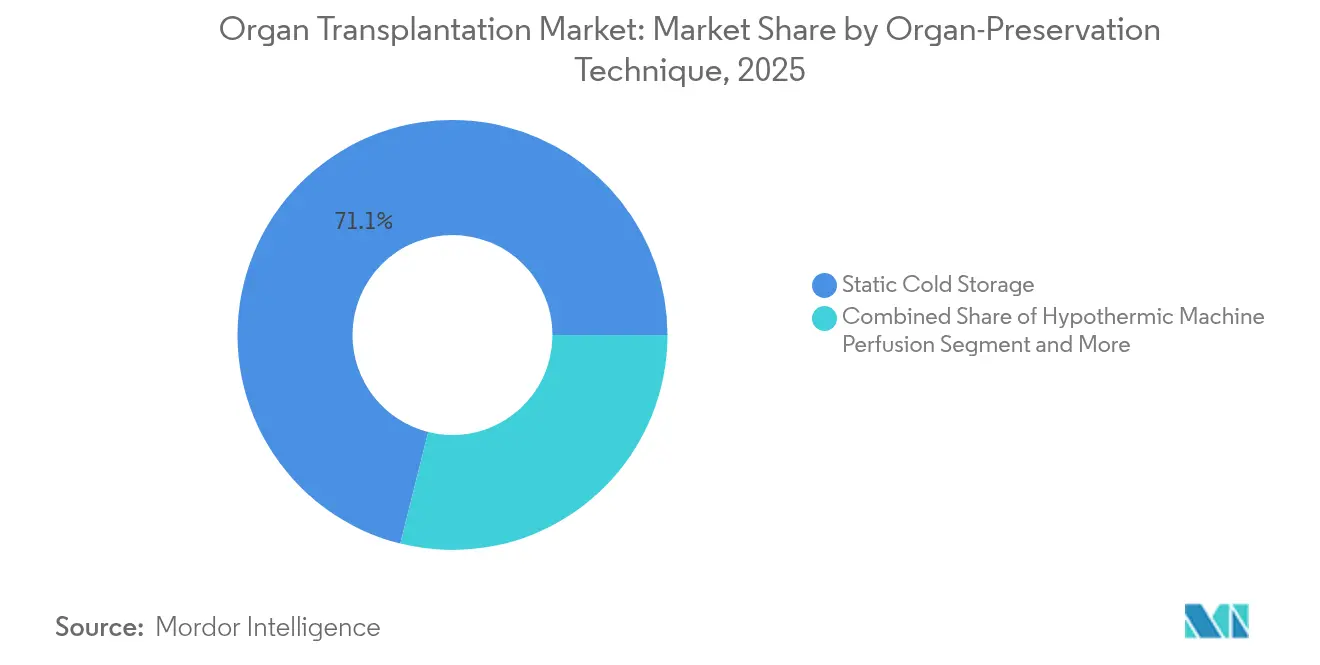

- By preservation technique, static cold storage retained 71.10% share in 2025, whereas normothermic machine perfusion is rising fastest at a 15.22% CAGR.

- By product type, immunosuppressant drugs held 51.05% share in 2025; digital and tele-transplant platforms are growing at an 18.15% CAGR to 2031.

- By end user, hospitals commanded 56.98% share in 2025, while ambulatory clinics are set to post a 12.31% CAGR through 2031.

- By geography, North America captured 36.40% of the organ transplantation market size in 2025; Asia-Pacific is forecast to register the quickest regional expansion at a 14.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Organ Transplantation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Chronic Diseases Leading To End-Stage Organ Failure | 2.1% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Advances In Organ Preservation & Perfusion Technologies | 1.8% | Global, early adoption in North America, EU, Australia | Short term (≤ 2 years) |

| Government Initiatives & Awareness Programs On Organ Donation | 1.4% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Improved Success Rates From Next-Generation Immunosuppressants | 1.2% | Global, with premium pricing in developed markets | Long term (≥ 4 years) |

| Blockchain-Enabled Organ Traceability & Logistics Optimisation | 0.9% | Early adoption in North America, EU, Brazil | Medium term (2-4 years) |

| Clinical Progress Of Bio-Printed Tissues For Transplant Back-Up | 0.7% | Research-intensive markets: US, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden Of Chronic Diseases Leading To End-Stage Organ Failure

Persistent growth in diabetes, cardiovascular disease, and chronic kidney disease propels procedure volumes across every major economy. More than 100,000 people remain on the U.S. wait-list, underscoring systemic shortfalls between supply and demand. Ageing populations in Europe add complexity, as older recipients often face eligibility constraints even while experiencing higher failure rates. In Asia-Pacific, hepatitis B prevalence and shifting alcohol consumption patterns accelerate liver failure cases. Payers increasingly view transplantation as cost-effective: 5-year mortality after kidney transplant is 68% lower than for patients on dialysis[3]American Transplant Foundation, “Affording Organ Transplant and Help if You’re Uninsured,” americantransplantfoundation.org.

Advances In Organ Preservation & Perfusion Technologies

Normothermic and hypothermic machine perfusion extend out-of-body times up to 20 hours and cut post-operative complications by 27% versus static cold storage. The FDA has cleared multiple platforms—including Organ Care System Heart and OrganOx metra—that enable real-time viability assessment during transport[1]Center for Devices and Radiological Health, “Organ Care System Heart System – P180051/S001,” FDA, fda.gov. Portable perfusion devices ease geographic mismatches between donors and recipients, facilitating interstate and international organ sharing while trimming four-year mortality by 54% in clinical cohorts.

Government Initiatives & Awareness Programs On Organ Donation

Policy reforms widen donor pools: the U.S. DoNation Campaign added 639,000 registrations, while India grants 42 days of paid leave to civil-service donors, removing employment disincentives. The WHO’s Resolution WHA77.4 sets a global target of universal access to transplantation by 2035, reinforcing coordinated national frameworks. Financial incentives and educational outreach narrow donor disparities among culturally diverse populations in Australia, where targeted grants have begun addressing a 15% under-representation gap.

Improved Success Rates From Next-Generation Immunosuppressants

Novel agents such as axatilimab-csfr and Vanrafia (atrasentan) reduce chronic rejection while limiting infection risk, achieving 75% clinical response in refractory graft-versus-host disease trials. Ready-to-use pediatric formulations improve adherence, and AI-guided pharmacogenomics platforms optimize dosing, boosting long-term graft survival predictions.

Restraints Impact Analysis of Organ Transplantation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Donor Organ Shortage & High Waiting-List Mortality | -2.3% | Global, most severe in developing countries | Short term (≤ 2 years) |

| High Procedure & Post-Transplant Therapy Costs | -1.7% | Global, limiting access in emerging markets | Medium term (2-4 years) |

| Regulatory Uncertainty Around Xenotransplantation Trials | -1.1% | Global, varying approval timelines by region | Long term (≥ 4 years) |

| Cold-Chain Gaps In Low-Income Regions Limiting Organ Viability | -0.8% | Sub-Saharan Africa, parts of Asia, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Donor Organ Shortage & High Waiting-List Mortality

Only 10% of global transplant need is currently met, and in the United States 17 people die daily while awaiting an organ. Cultural barriers further depress deceased-donor rates in Malaysia and parts of the Middle East, creating extended wait times for ethnic minorities and pediatric candidates.

High Procedure & Post-Transplant Therapy Costs

A single heart transplant can exceed USD 1.6 million in the United States, while liver transplant costs have climbed 10.9% following recent policy changes. Immunosuppressive regimens add lifelong expenses that may top USD 50,000 annually, reinforcing inequities where public insurance coverage is incomplete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Organ Transplantation Market Segment Analysis

By Organ Type:

Kidney Dominance Drives Volume GrowthThe kidney segment commanded 61.74% of organ transplantation market share in 2025 as end-stage renal disease prevalence continues to climb. This dominance is reinforced by living-donor compatibility programs that contribute about one-third of kidney volumes, delivering better long-term survival than deceased-donor alternatives. Broader use of AI-enhanced matching and cross-matching algorithms uplifts graft longevity and reduces acute rejection incidents.

Livers form the second-largest cohort, backed by expanding hepatocellular carcinoma caseloads and refined surgical methods that handle marginal grafts more safely. Lung transplants, however, represent the fastest-growing sub-segment at a 9.11% CAGR to 2031, reflecting advances in hypothermic oxygenated perfusion and relaxed donor criteria. Heart, pancreas, and intestinal procedures maintain smaller bases but benefit from innovations like FDA-cleared perfusion carriers that extend preservation windows.

By Donor Type:

Living Donation Gains MomentumDeceased donations delivered 69.02% of 2025 transplant volumes, sustained by robust procurement networks and emerging donation-after-circulatory-death protocols. Yet living-donor activities are expanding at 9.22% CAGR, powered by reimbursement schemes that offset travel, surgery, and wage-loss expenses for altruistic donors. Paired kidney exchanges and voucher programs enlarge donor pools by linking incompatible pairs through sophisticated optimization engines, while living-donor liver transplantation gains acceptance for pediatric indications in high-volume Asian centers.

By Type of Transplant:

Allogeneic Procedures Dominate Clinical PracticeAllogeneic operations represented 83.35% of 2025 procedures and remain standard care across kidneys, livers, hearts, and lungs. Continuous improvement in HLA typing, supported by machine-learning models, keeps acute rejection rates on a downward trajectory. Autologous transplants are still limited to hematopoietic contexts, yet regenerative scaffolds are under active investigation for future solid-organ use.

Xenotransplantation and composite tissue allografts form the fastest-growing niche, expanding at 12.95% CAGR. FDA-cleared trials for gene-edited pig kidneys and livers have moved into first-in-human phases, and United Therapeutics has logged initial successful outcomes under compassionate-use protocols. Composite tissue procedures such as hand and face transplants leverage tailored immunosuppression and now receive earmarked federal research funding.

By Organ-Preservation Technique:

Advanced Perfusion Technologies Transform StandardsStatic cold storage remains prevalent, covering 71.10% of graft shipments in 2025 because of its low cost and global familiarity. However, organ transplantation market size linked to normothermic machine perfusion is expanding swiftly as hospitals quantify tangible drops in delayed graft function.

Normothermic platforms supply warm, oxygenated perfusate, permitting viability checks and repair interventions mid-transport. The OrganOx metra system alone has supported more than 5,000 liver procedures with complication reductions of 27%. Hypothermic perfusion modalities are gaining acceptance for kidneys, particularly in Europe and Australia, where randomized trials show consistent graft survival benefits.

By Product Type:

Digital Platforms Drive InnovationImmunosuppressants held 51.05% revenue share in 2025, while biosimilars and next-generation monoclonal antibodies reshape competitive pricing. Yet the digital therapeutics and tele-transplant cluster is scaling at an 18.15% CAGR, driven by blockchain tracking pilots in Brazil and AI-enabled education portals that improve adherence.

Organ preservation solutions and devices remain core revenue generators as normothermic adoption accelerates. Tissue-engineering firms leverage 3-D bioprinting to develop scaffolds for vascularized grafts, setting the stage for autologous constructs that could eventually reduce the dependence on human donors.

By End User:

Ambulatory Care Expands AccessHospitals accounted for 56.98% of 2025 revenues, reflecting their pivotal role in complex surgery, intensive monitoring, and high-acuity infection control. High-volume academic centers improve outcomes by concentrating expertise and offering advanced organ preservation suites.

Ambulatory clinics and same-day surgical centers are the fastest-growing channel at 12.31% CAGR. Living-donor nephrectomies increasingly take place in these settings, supported by enhanced-recovery pathways and minimally invasive techniques that allow discharge within 24 hours. Telemedicine follow-up reduces travel burdens, and integrated care pathways deliver cost savings without compromising patient safety.

Geography Analysis

North America Organ Transplantation Market

North America held 36.40% of global revenue in 2025 on the strength of FDA fast-track authorizations for xenotransplantation and sustained federal investment, including USD 12 million dedicated to reconstructive transplant research. The organ transplantation market size for the region is reinforced by a well-coordinated procurement network, national donor registries exceeding 180 million participants, and large-scale AI trials that refine allocation efficiency.

Europe Organ Transplantation Market

Europe benefits from unified frameworks like Eurotransplant and upcoming Regulation (EU) 2024/1938, which will harmonize substances-of-human-origin protocols by 2027. Cross-border organ circulation, bolstered by standardized logistics, improves match rates especially for pediatric and rare HLA types. Venture funding fuels device start-ups; OrganOx raised USD 142 million to scale perfusion platforms.

APAC Organ Transplantation Market

Asia-Pacific delivers the fastest regional CAGR at 14.29% as governments invest in transplant infrastructure, establishing new liver-surgery hubs in China and promoting public-awareness campaigns in Japan. India and Pakistan expand kidney programs through subsidized dialysis-to-transplant pathways, although rural cold-chain gaps still limit timely organ movement. Targeted regional guidelines on immunosuppression adapt dosing to genetic polymorphisms frequent in Asian populations, enhancing drug safety.

LATAM and MEA Organ Transplantation Market

Sub-Saharan Africa and parts of Latin America face persistent barriers around funding, trained personnel, and reliable storage. Yet pilot initiatives such as blockchain-based tracking in Brazil demonstrate scalable models for improving transparency and reducing illicit trafficking. Iran’s regulated kidney compensation system remains unique but controversial, illustrating divergent policy responses to acute donor shortages.

Competitive Landscape

Competition centers on end-to-end solutions that couple preservation devices with advanced analytics, driving moderate consolidation in the organ transplantation market. Getinge’s USD 477 million acquisition of Paragonix Technologies positions it to integrate perfusion hardware with in-house ICU platforms, aiming for seamless donor-to-recipient workflows. OrganOx’s USD 142 million capital infusion accelerates expansion of its metra platform, while X-Therma’s USD 22.4 million Series B funds cryopreservation R&D geared toward longer-term biobanking.

Pharmaceutical–device alliances emerge as firms such as Enovis partner with Ossium Health to distribute bone-marrow-derived graft materials, complementing solid-organ pipelines. Logistics giants like DHL now own specialized cold-chain operators, tightening control over time-critical shipments and boosting service reliability.

Disruptors focus on xenotransplantation and regenerative medicine; United Therapeutics has secured FDA Investigational New Drug clearance for its UKidney trial enrolling up to 50 participants, marking a pivotal step toward commercial pig-organ supply. Technology differentiation increasingly hinges on measurable clinical improvements: controlled trials show perfusion-enabled hearts achieve 4-year survival gains of 6 percentage points versus static methods.

Organ Transplantation Industry Leaders

Novartis AG

AbbVie Inc.

TransMedics, Inc.

F. Hoffmann-La Roche Ltd

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Organ Transplantation Market Companies Covered in this Report

- Novartis

- Abbvie

- Sanofi

- Roche

- Astellas Pharma

- Pfizer

- Veloxis Pharmaceuticals

- Medtronic

- Organ Recovery Systems

- TransMedics Inc.

- Paragonix Technologies

- Organox

- Bridge to Life Ltd.

- Xvivo Perfusion

- Terumo

- BioLife Solutions

- Artivion Inc.

- United Therapeutics Corp.

- Miromatrix Medical Inc.

- Arthrex

Recent Industry Developments in Organ Transplantation Market

- May 2025: OrganOx raised new funding from Intuitive Ventures, Terumo Ventures, and Piper Heartland Healthcare to expand organ-technology operations.

- February 2025: United Therapeutics received FDA clearance for its UKidney xenotransplantation clinical trial, with first transplants slated for mid-2025.

Organ Transplantation Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, our study defines the organ transplantation market as revenue generated from the surgical removal, preservation, and implantation of whole human organs, together with the immediate hospital procedure and procurement charges that surround each transplant event.

We exclude ongoing immunosuppressive drug therapy, stand-alone tissue grafts, and regenerative or artificial organ technologies.

Segments Covered in This Report

- By Organ Type

- Kidney

- Liver

- Heart

- Lung

- Pancreas

- Intestine

- By Donor Type

- Deceased Donor

- Living Donor

- By Type of Transplant

- Allogeneic

- Autologous

- Xenotransplant & Composite Tissue

- By Organ-Preservation Technique

- Static Cold Storage

- Hypothermic Machine Perfusion

- Normothermic Machine Perfusion

- Other Novel Methods

- By Product Type

- Organ Preservation Solutions & Devices

- Transplant Diagnostics

- Immunosuppressant Drugs

- Tissue Products & Biologics

- Digital & Tele-transplant Platforms

- By End User

- Hospitals

- Transplant Centres

- Ambulatory Surgical & Out-patient Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed transplant surgeons, organ procurement leaders, perfusion device engineers, and major payors across North America, Europe, and Asia. These discussions validated price points, filled regional gaps, and tested early findings from secondary work.

Desk Research

Our desk work taps open sources such as the WHO Global Observatory on Donation and Transplantation, United Network for Organ Sharing, Eurotransplant, OECD Health Data, and leading clinical journals to map procedure volumes, donor trends, and survival outcomes. We add company 10-Ks, payer tariffs, and health ministry fee schedules to refine price assumptions.

We also access paid collections in Mordor's library, D&B Hoovers for provider finances and Dow Jones Factiva for deal flow, which clarify center capacity and technology rollouts.

The sources cited are illustrative; many other datasets supported data capture and cross-checks.

Market-Sizing & Forecasting

We open with a top-down build that multiplies verified transplant counts (donor rates and discard ratios) by average bundled surgical tariffs. Limited bottom-up checks, sample consumables invoices and capacity roll-ups at select centers, calibrate totals. Model drivers include deceased donor growth, living donor conversion, multi-organ retrieval, cross-match success, and mean reimbursement per organ. A multivariate regression, informed by GDP per capita and diabetes prevalence, extends forecasts to 2030.

Data Validation & Update Cycle

To ensure consistency, we run layered variance scans, benchmark outputs against registry statistics and trade flows, and reconfirm anomalies with experts. Models refresh each year, with interim updates after major policy or technology events, so clients always receive the latest vetted baseline.

How Mordor Intelligence's Organ Transplantation Market Size Compares to Other Published Estimates

We recognize that published estimates often differ because publishers select varied product bundles, price anchors, and refresh timelines.

Our review indicates the largest gaps arise when broader studies fold tissue transplants, long-term drug revenue, or preservation devices into the same pool or rely on aged base years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.42 B (2025) | Mordor Intelligence | - |

| USD 10.96 B (2024) | Regional Consultancy A | Tissue and drug revenue bundled; sparse primary validation |

| USD 16.50 B (2023) | Global Consultancy B | Older base year; macro scaling; wider scope than procedures |

| USD 17.73 B (2024) | Industry Association C | Preservation devices counted; producer sales basis |

We believe the comparison shows that by focusing on procedure linked revenue and updating models yearly with live market signals, Mordor Intelligence supplies a balanced, transparent baseline decision makers can rely on.

Key Questions Answered in the Report

What is the current value of the organ transplantation market?

The organ transplantation market is valued at USD 8.07 billion in 2026 and is projected to reach USD 12.32 billion by 2031.

Which organ type contributes the most to procedure volumes?

Kidneys account for 61.74% of total transplants thanks to high end-stage renal disease prevalence and strong living-donor participation.

Why is normothermic machine perfusion attracting attention?

It lengthens organ viability to 20 hours and cuts post-operative complications by 27%, improving recipient outcomes.

Which region shows the fastest growth rate?

Asia-Pacific leads with an anticipated 14.29% CAGR through 2031, driven by rising transplant infrastructure investments.

How are governments addressing donor shortages?

Initiatives range from paid-leave policies for donors to nationwide awareness campaigns and blockchain-based tracking systems that boost registration and transparency.

What technologies could redefine future transplantation?

Gene-edited pig organs, 3-D bioprinted tissues, and AI-driven donor-recipient matching platforms are all advancing toward clinical adoption, promising to alleviate chronic organ shortages.

Page last updated on: