End Stage Renal Disease (ESRD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

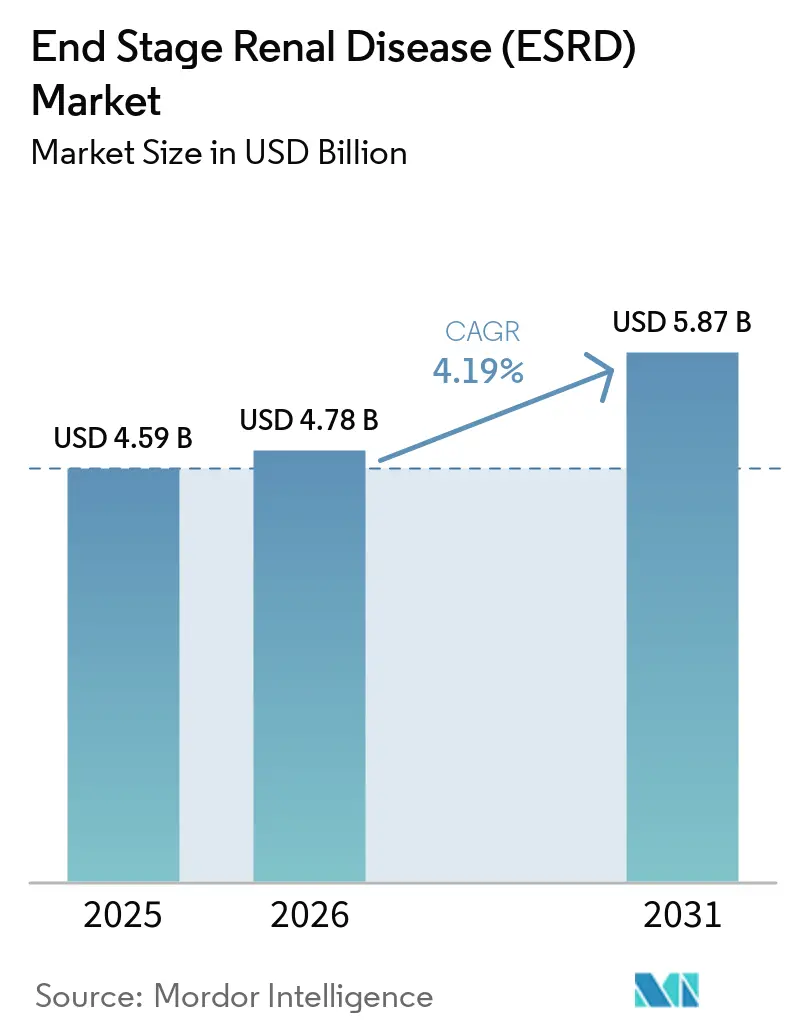

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

End Stage Renal Disease (ESRD) Market Analysis by Mordor Intelligence

The End Stage Renal Disease (ESRD) Market size is projected to expand from USD 4.59 billion in 2025 and USD 4.78 billion in 2026 to USD 5.87 billion by 2031, registering a CAGR of 4.19% between 2026 to 2031. The escalation is propelled by a growing chronic kidney disease (CKD) patient pool, the shift toward patient-centric care models, and rapid product innovation in high-value device and pharmaceutical categories. Demographic aging combines with lifestyle disorders such as diabetes and hypertension to keep incidence rates on an upward path, while public payers in high-income countries reimburse a widening spectrum of therapies. Home-based dialysis and remote monitoring platforms are gaining traction because they lower total treatment costs and improve quality-of-life metrics. Strategic divestitures and mergers are reshaping competitive boundaries as firms realign portfolios to focus on technology-rich segments, and artificial kidney research is opening a long-term pathway toward organ replacement alternatives. As a result, the ESRD market is transitioning from a volume-driven model dominated by in-center dialysis to a hybrid ecosystem that balances facility, home, and conservative management solutions.

Key Report Takeaways

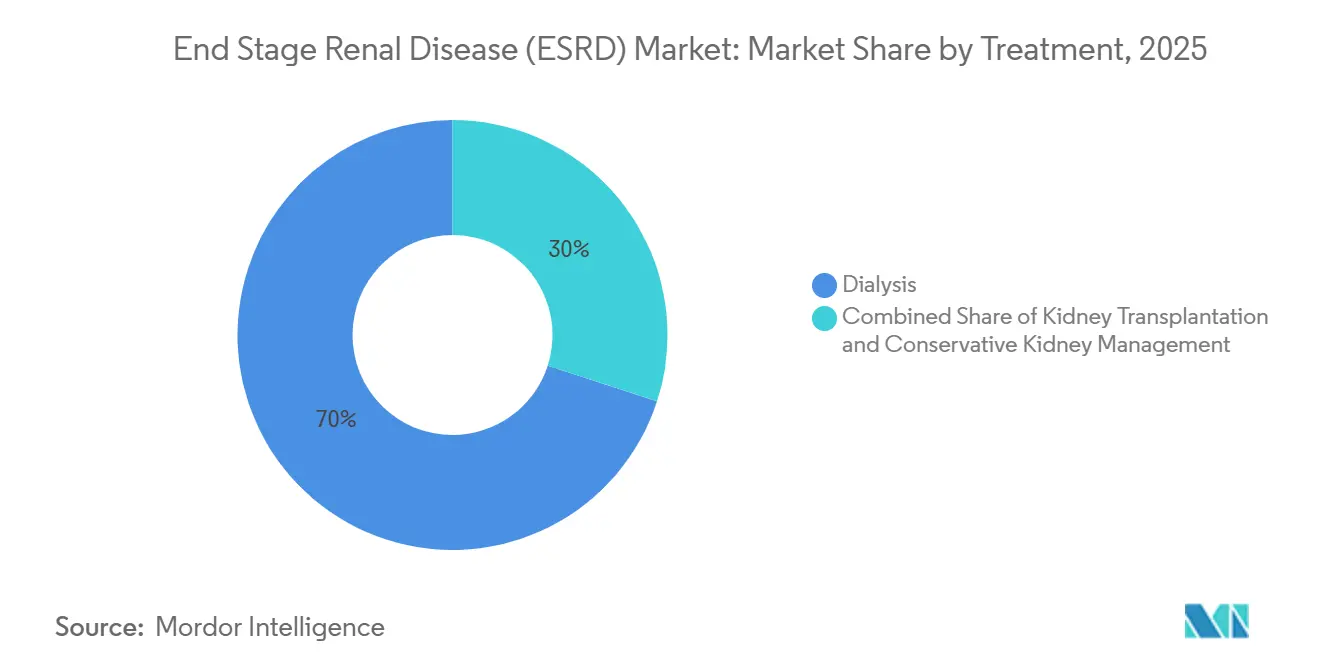

- By treatment, Dialysis led with 70.02% of End Stage Renal Disease (ESRD) market share in 2025, whereas Conservative Kidney Management is projected to grow at a 8.88% CAGR through 2031.

- By diagnosis, Blood Tests accounted for 45.10% of End Stage Renal Disease (ESRD) market share in 2025, while Imaging is expected to accelerate at a 9.42% CAGR to 2031.

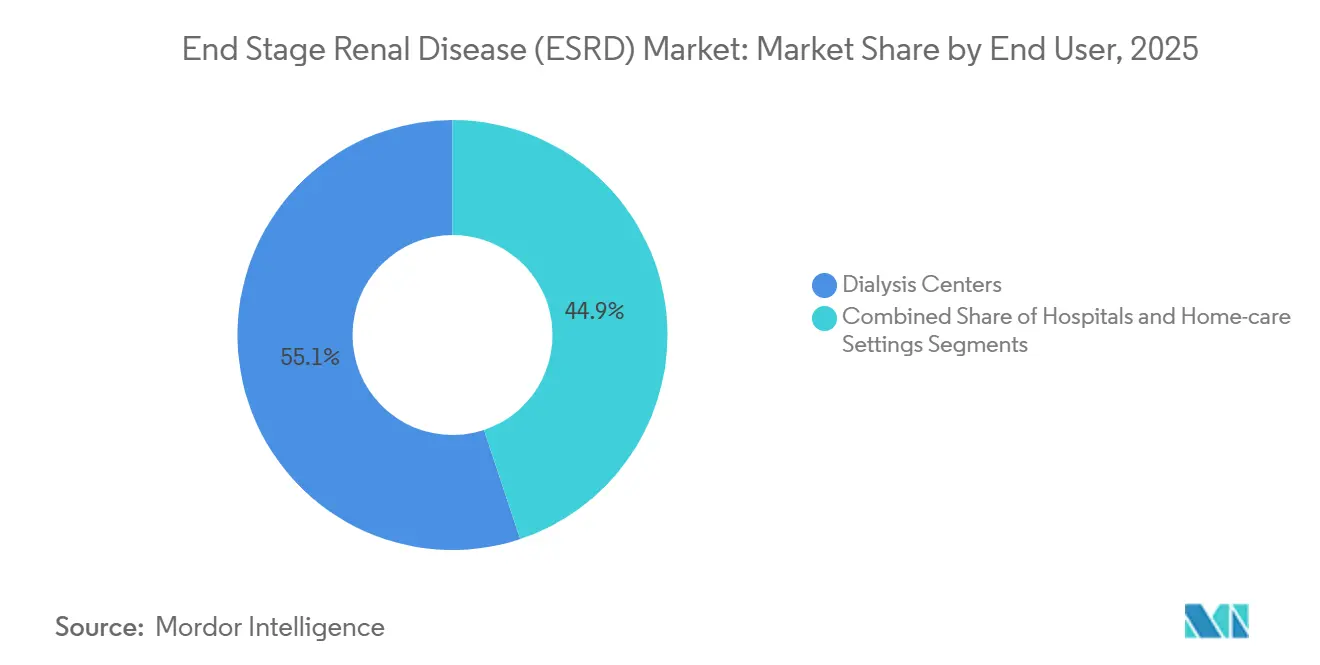

- By end user, Dialysis Centers held 55.10% of End Stage Renal Disease (ESRD) market share in 2025, yet Home-care Settings are advancing at a 8.96% CAGR to 2031.

- By product, Hemodialysis Equipment captured 39.10% of End Stage Renal Disease (ESRD) market share in 2025, whereas Transplant Immunosuppressants are set to expand at a 8.95% CAGR through 2031.

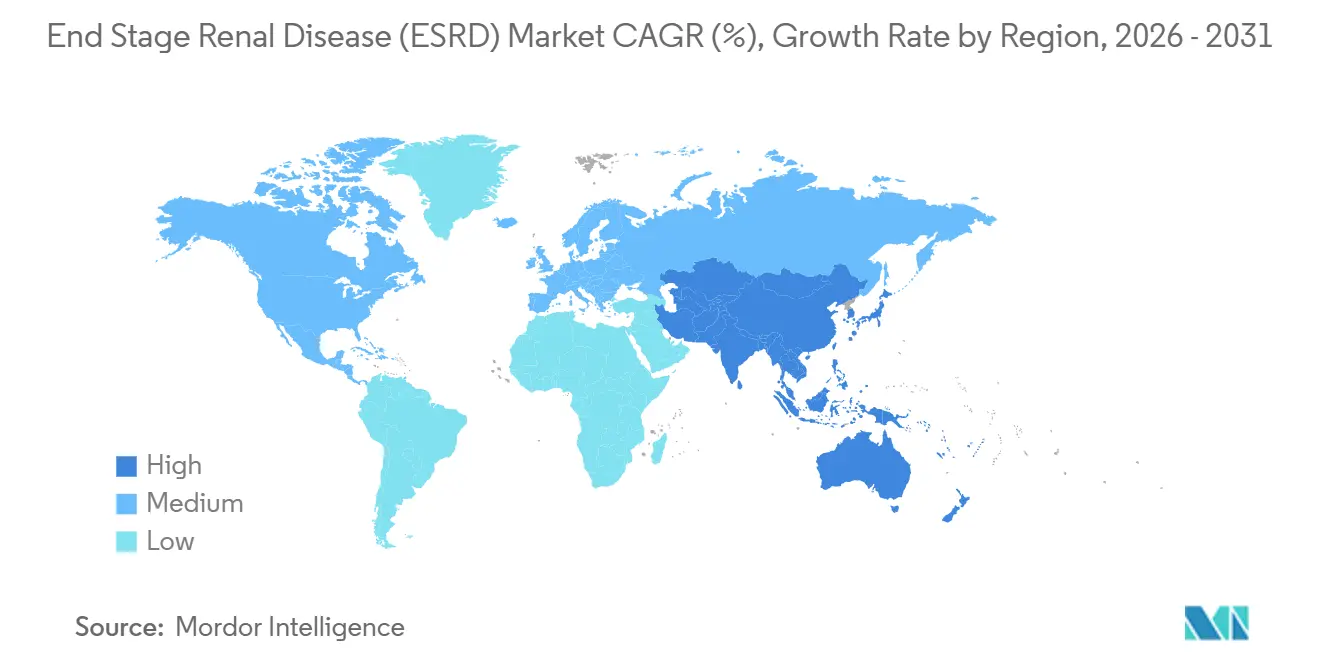

- By geography, North America commanded 35.20% of End Stage Renal Disease (ESRD) market share in 2025, and Asia-Pacific is poised for the fastest regional CAGR of 9.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of End Stage Renal Disease (ESRD) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CKD patient pool expansion (aging & lifestyle) | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rising diabetes & hypertension prevalence | +1.2% | Global, highest impact in Asia-Pacific & MEA | Medium term (2-4 years) |

| Government funding for dialysis infrastructure | +0.9% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Technological advances — high-flux & wearable HD | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Growth in home-based dialysis reimbursement | +0.5% | North America, selective EU markets | Short term (≤ 2 years) |

| Artificial kidney & xenotransplant R&D momentum | +0.3% | North America, limited EU participation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CKD Patient Pool Expansion Through Demographic and Lifestyle Convergence

The rising proportion of elderly citizens and the persistent spread of lifestyle diseases are enlarging the CKD base that ultimately progresses to end-stage renal disease, thereby broadening the ESRD market. Thirty-one percent of CKD cases remain undiagnosed in primary care, creating lost intervention opportunities and a USD 6.7 billion annual burden. Prevalence peaks at 50.94% in patients aged 90 years and older, while male incidence rates surpass female rates. AI-enabled biomarker panels and contrast-enhanced ultrasound tools are closing diagnostic gaps and paving the way for earlier treatment starts, which supports sustained growth in the ESRD market.

Rising Diabetes and Hypertension as Primary ESRD Catalysts

Diabetes and hypertension together underpin most ESRD admissions and are climbing fastest in urbanizing Asia-Pacific markets. Poorly controlled HbA1c levels accelerate CKD progression, necessitating earlier entry into the ESRD market. Medtronic’s Symplicity Spyral renal denervation catheter obtained CMS transitional pass-through status in late 2024, highlighting how adjunct technologies for hypertension management are aligning with renal care pathways[1]Medtronic plc, “CMS Grants Transitional Pass-Through Payment for Medtronic Symplicity Spyral Renal Denervation Catheter,” Medtronic, news.medtronic.com.

Government Infrastructure Investment Accelerating Access

National health systems are boosting dialysis capacity via capital grants and public-private partnerships, especially in Asia-Pacific and MEA. The 2023 ISN Global Kidney Health Atlas notes that while dialysis technology exists in 98% of countries, only 32% of patients in low-income economies receive therapy, leaving a sizeable addressable segment for the ESRD market. Japan’s knowledge-transfer programs to Southeast Asia stand out as replicable models.

Technological Innovation in High-Flux and Wearable Hemodialysis

High-flux membranes improve middle-molecule clearance and reduce cardiovascular events compared with low-flux alternatives, reinforcing patient preference and clinic adoption. Clinical trials on wearable artificial kidneys, financed by the NIH, promise true mobility, while United Therapeutics gained FDA approval to start pig-to-human xenotransplant trials in February 2025. These advances enhance treatment options and lift the technology mix across the ESRD market.

Restraints Impact Analysis of End Stage Renal Disease (ESRD) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Late/under-diagnosis of CKD | -0.8% | Global, highest impact in LMICs | Medium term (2-4 years) |

| Shortage of donor kidneys & transplant backlog | -0.6% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| High treatment cost burden in LMICs | -0.5% | APAC, MEA, South America | Long term (≥ 4 years) |

| Dialysis clinic staffing shortages | -0.4% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Late and Under-Diagnosis of CKD Limiting Market Potential

Systematic screening deficits keep a third of CKD patients undetected until advanced stages, delaying referral and raising emergency initiation rates. This late presentation curtails the volume of early-stage interventions that generate recurring revenue across the ESRD market, and it pushes up health-system costs due to higher morbidity.

Kidney Transplant Shortage Creating Systemic Treatment Bottlenecks

More than 90,000 patients wait for a kidney in the United States with average wait times of five years. The gap propels long-term dialysis dependence, sustaining demand yet limiting access to transplantation’s superior survival benefits. Xenotransplant trials mark progress, but commercial scale remains years away, keeping capacity tight and tempering growth in the ESRD market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

End Stage Renal Disease (ESRD) Market Segment Analysis

By Treatment:

Dialysis Dominance Amid Conservative Care EmergenceDialysis contributed 70.02% of revenue in the ESRD market during 2025, upholding its central role despite reimbursement pressures. Conservative Kidney Management is the rising alternative, expanding at a 8.88% CAGR on the strength of evidence showing comparable quality of life for frail elderly cohorts. Hemodialysis and peritoneal dialysis continue to split the modality mix, with PD gaining ground in countries that operate “PD First” policies.

Conservative care programs integrate symptom control, nutritional counseling, and palliative components, which align with patient-centred objectives and alleviate hospital utilization. Transplant uptake remains hindered by donor scarcity, although FDA-sanctioned xenotransplant trials could disrupt the treatment hierarchy in the long run. High-flux dialyzers and automated cyclers are broadening the technical capabilities underpinning modality choice and adding value layers within the ESRD market.

By Diagnosis:

Blood Testing Leadership Challenged by Imaging InnovationBlood Tests generated 45.10% of diagnostic revenue in 2025 as eGFR and creatinine remain the gateway markers for CKD staging. Imaging tools are advancing fastest at a 9.42% CAGR, fueled by AI platforms that reach 97.41% accuracy in kidney pathology identification, making them a powerful addition to the ESRD market toolbox.

Contrast-enhanced ultrasound and low-dose CT are detecting early structural changes before laboratory markers rise. Urine assays and emerging biomarker panels continue to play a complementary role. Integration of imaging outputs with electronic health records accelerates clinical workflow and supports risk-based patient stratification, reinforcing diagnostic ecosystem value creation.

By End User:

Home Care Transformation AcceleratingDialysis Centers retained a 55.10% revenue contribution in 2025, yet Home-care Settings are set to expand at a 8.96% CAGR as payers reward decentralized treatment. CMS’s ESRD Treatment Choices Model ties reimbursement to modality mix and transplant use, prompting providers to build home-dialysis pipelines.

Remote monitoring systems alert clinicians to fluid shifts and blood pressure deviations, cutting hospitalization risk. Hospitals keep their role in acute dialysis and complex transplant surgery but are increasingly integrating with outpatient networks. Staffing shortages in facility-based units strengthen the economic case for home modalities and sustain momentum in the ESRD market.

By Product Type:

Equipment Leadership Meets Immunosuppressant InnovationHemodialysis Equipment accounted for 39.10% of revenue in 2025, representing the backbone hardware of the ESRD market. Transplant Immunosuppressants, however, are growing fastest at 8.95% CAGR, underscoring renewed transplant optimism. Myhibbin and advanced tacrolimus formulations improve graft survival and enable transplantation among older and comorbid patients.

Dialysis consumables such as dialyzers and AV sets deliver dependable recurring revenue, while peritoneal solutions evolve toward glucose-sparing chemistries. Equipment vendors pursue compact, user-friendly designs that suit both clinic and home environments. Parallel device and drug innovation creates cross-segment synergies that deepen the product mix across the ESRD market.

Geography Analysis

North America End Stage Renal Disease (ESRD) Market

North America represented 35.20% of global revenue in 2025, reflecting robust Medicare funding that covers 67% of dialysis spend. DaVita treated about 200,800 patients across 2,675 outpatient centers and facilitated 8,000 transplants in 2023, illustrating the scale advantages in place. CMS value-based purchasing is reshaping provider incentives and encouraging modality diversification, while staffing shortages accelerate adoption of automated technologies and tele-nephrology.

APAC End Stage Renal Disease (ESRD) Market

Asia-Pacific is the fastest-growing territory with a 9.02% CAGR through 2031, propelled by demographic aging, growing health coverage, and concerted government investment in dialysis infrastructure. Japan treats 334,505 dialysis patients and exports best-practice protocols to Southeast Asia, demonstrating knowledge diffusion that widens regional bandwidth. China faces a sizable CKD burden and deploys blended reimbursement to spur therapy uptake, reinforcing expansion prospects for the ESRD market.

EMEA and South America End Stage Renal Disease (ESRD) Market

Europe, the Middle East and Africa, and South America present heterogeneous growth profiles. European markets benefit from universal reimbursement and established clinic networks yet confront capacity strains from aging populations. The ISN Global Kidney Health Atlas highlights that only 32% of patients in low-income countries within MEA can access dialysis despite technical availability, exposing a financing gap. South America is developing coverage models that stretch public budgets but still sees treatment costs exceed per capita income in many nations, making low-cost devices and micro-insurance important adoption drivers.

Competitive Landscape

The ESRD market exhibits moderate consolidation with leading firms investing in targeted growth pillars. Fresenius delivered 9% organic revenue growth in Q3 2024, while streamlining ancillary divisions to focus on core dialysis and care coordination. Baxter divested its kidney care division to Carlyle for USD 3.8 billion, launching Vantive as a dedicated organ-therapy company that now concentrates resources on high-flux hardware and cloud-enabled connectivity[3]Vantive, “Baxter Kidney Care Is Now Vantive, a New Standalone Vital Organ Therapy Company,” Vantive, vantive.com.

Value-based care is reshaping strategy. InterWell Health, Cricket Health, and Fresenius Health Partners merged to manage 270,000 covered lives and USD 11 billion in spend by 2025, combining predictive analytics with coordinated care pathways. Smaller disruptors such as Outset Medical and AWAK Technologies fight for share with compact hemodialysis machines and portable artificial kidneys that target home and acute-care niches.

Technology differentiation is central. AI-powered risk stratification, automated fluid management, and cloud telemetry reduce unplanned hospitalization and strengthen provider economics. Regulatory milestones in xenotransplantation and bioartificial kidneys attract investor capital and position innovators for future category leadership, deepening competitive intensity in the ESRD market.

End Stage Renal Disease (ESRD) Industry Leaders

Nipro Corporation

Fresenius SE & Co. KGaA

Baxter International Inc

Medtronic PLC

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

End Stage Renal Disease (ESRD) Market Companies Covered in this Report

- Fresenius

- Baxter

- Nipro

- B. Braun

- Medtronic

- Asahi Kasei

- Nikkiso Co. Ltd.

- Beckton Dickinson

- STERIS plc (Cantel)

- Toray Medical Co. Ltd.

- Terumo

- DaVita

- Diaverum AB

- Satellite Healthcare

- U.S. Renal Care

- Rockwell Medical

- AWAK Technologies

- Outset Medical

- Quanta Dialysis Technologies

- Biocon Ltd. (Immunosuppressants)

Recent Industry Developments in End Stage Renal Disease (ESRD) Market

- April 2025: The American Society of Nephrology unveiled a pilot Centers of Excellence in Home Dialysis program to recognize organizations that meet national standards for home modalities.

- August 2024: Baxter signed a definitive agreement with Carlyle to spin off its Kidney Care segment for USD 3.8 billion, subsequently named Vantive.

Global End Stage Renal Disease (ESRD) Market Report Scope

End-stage renal failure, also known as an end-stage renal disease (ESRD), is the final, permanent stage of chronic kidney disease, where kidneys can no longer function independently.

The End Stage Renal Disease (ESRD) Market is Segmented by Treatment (Kidney Transplantation and Dialysis), Diagnosis (Blood Test, Urine Test, Imaging Test, and Other Diagnoses), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America Brazil, Argentina, and Rest of South America)). The report offers value (in USD million) for the above segments.

Segmentation Overview

| Kidney Transplantation | |

| Dialysis | Hemodialysis |

| Peritoneal Dialysis | |

| Conservative Kidney Management |

| Blood Tests (eGFR, Creatinine) |

| Urine Tests (ACR, protein) |

| Imaging (Ultrasound, CT/MRI) |

| Other Diagnostics |

| Hospitals |

| Dialysis Centers |

| Home-care Settings |

| Hemodialysis Equipment |

| Dialysis Consumables (Dialyzers, AV sets) |

| Peritoneal Dialysis Solutions & Sets |

| Transplant Immunosuppressants |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment | Kidney Transplantation | |

| Dialysis | Hemodialysis | |

| Peritoneal Dialysis | ||

| Conservative Kidney Management | ||

| By Diagnosis | Blood Tests (eGFR, Creatinine) | |

| Urine Tests (ACR, protein) | ||

| Imaging (Ultrasound, CT/MRI) | ||

| Other Diagnostics | ||

| By End User | Hospitals | |

| Dialysis Centers | ||

| Home-care Settings | ||

| By Product Type | Hemodialysis Equipment | |

| Dialysis Consumables (Dialyzers, AV sets) | ||

| Peritoneal Dialysis Solutions & Sets | ||

| Transplant Immunosuppressants | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the end stage renal disease (ESRD) market and how fast is it growing?

The end stage renal disease (ESRD) market size is USD 4.78 billion in 2026 and is set to expand to USD 5.87 billion by 2031 at a 4.19% CAGR.

Which treatment modality holds the largest end stage renal disease (ESRD) market share?

Dialysis maintains leadership with 70.02% of end stage renal disease (ESRD) market share in 2025, driven by established reimbursement and infrastructure.

Why is home-based dialysis gaining momentum?

Value-based payment reforms and remote monitoring technology reduce hospitalization risk and incentivize providers to shift suitable patients to home settings.

Which region is projected to grow fastest in the end stage renal disease (ESRD) market?

Asia-Pacific is forecast to rise at a 9.02% CAGR through 2031 owing to demographic shifts, government investment, and expanding insurance coverage.

How are technological innovations shaping future end stage renal disease treatments?

High-flux dialyzers, wearable artificial kidneys, and FDA-approved xenotransplant trials diversify therapeutic options and may ease organ supply constraints.

Page last updated on: