Amniotic Membrane Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

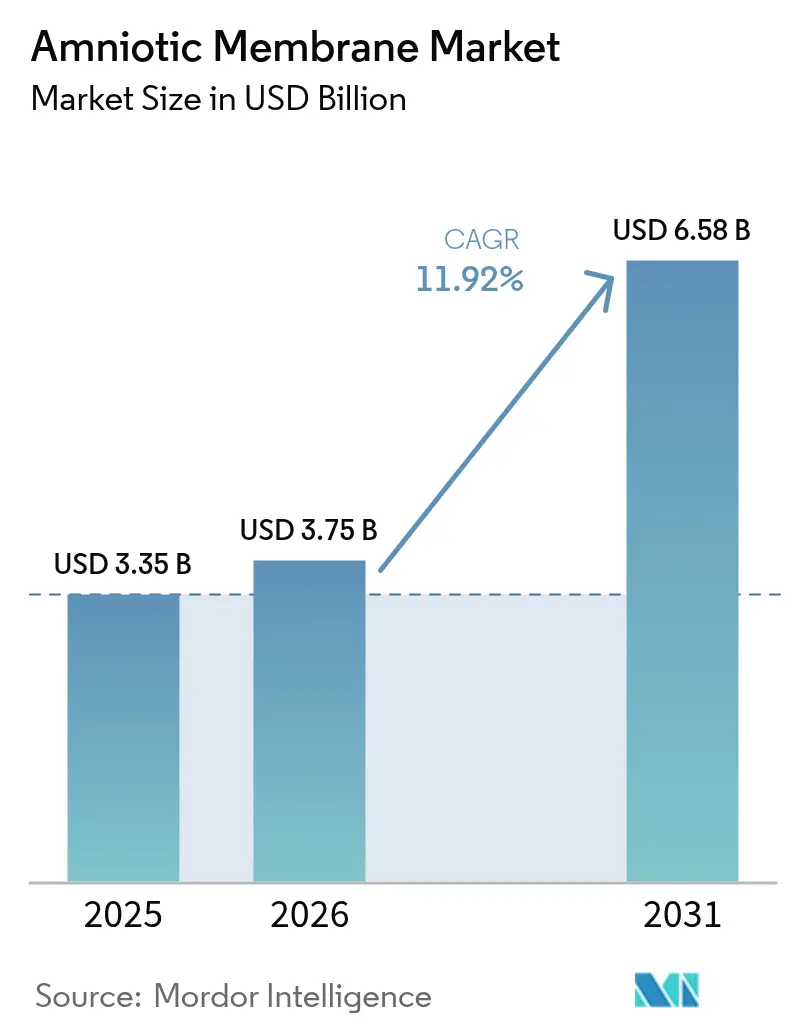

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 6.58 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Amniotic Membrane Market Analysis by Mordor Intelligence

amniotic membrane market size in 2026 is estimated at USD 3.75 billion, growing from 2025 value of USD 3.35 billion with 2031 projections showing USD 6.58 billion, growing at 11.92% CAGR over 2026-2031. Intensifying clinical validation across ophthalmology, trauma and chronic wound management keeps demand high, while reimbursement clarity in key markets accelerates routine use of these biologic dressings. Dehydrated grafts still dominate day-to-day practice because they store at room temperature, yet hospitals increasingly adopt cryopreserved alternatives to capture the higher growth-factor load that speeds tissue regeneration. Aging populations undergoing more ocular surgeries, together with the global rise in road-traffic injuries, continue to expand clinical indications and procedure volumes [1]Y. He et al., “Matrix Component HC-HA/PTX3 in Tissue Regeneration,” PubMed, pubmed.ncbi.nlm.nih.gov . Regionally, North America remains the revenue leader owing to Medicare support for advanced wound care, whereas Asia-Pacific is delivering the fastest unit growth on the back of large-scale healthcare investments in China and improved regulatory pathways in Japan and South Korea. Competitive intensity stays moderate; no single vendor exceeds a fifth of global sales, keeping innovation pressure high and pricing comparatively stable.

Key Report Takeaways

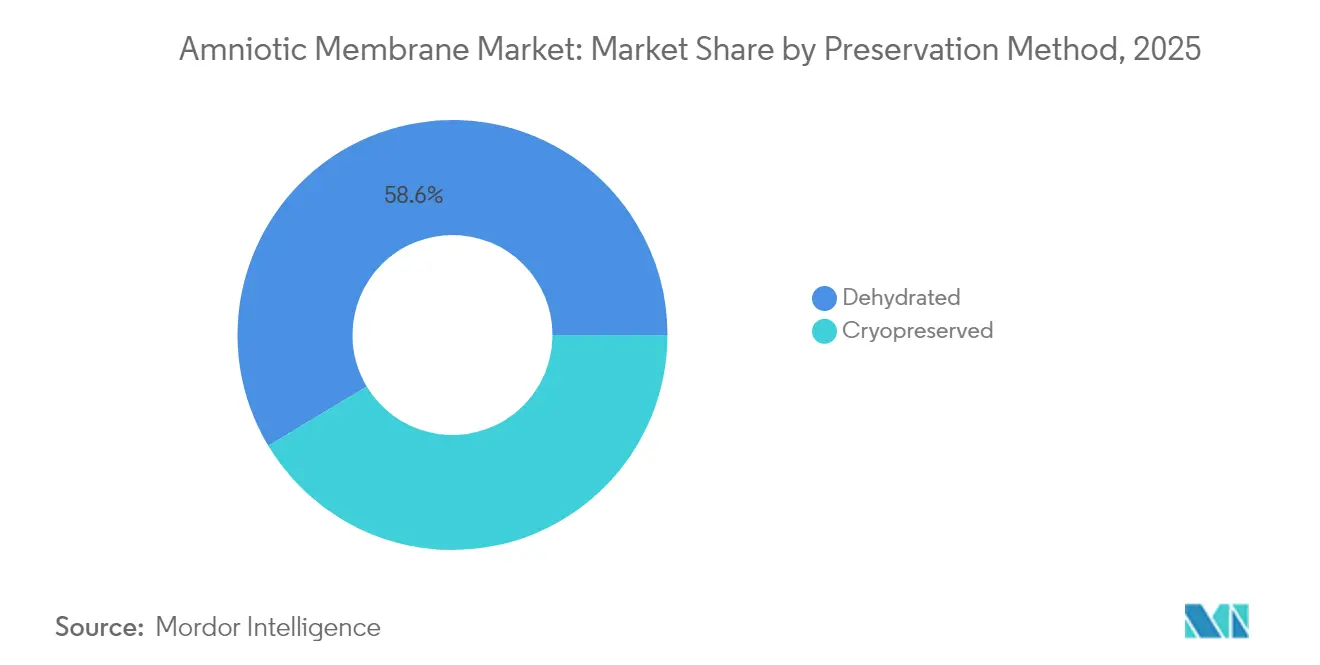

- By preservation method, dehydrated formats held 58.62% of amniotic membrane market share in 2025; cryopreserved grafts are projected to post a 12.41% CAGR to 2031.

- By thickness, single-layer products captured 68.10% revenue share in 2025, while multi-layer configurations are advancing at a 12.55% CAGR through 2031.

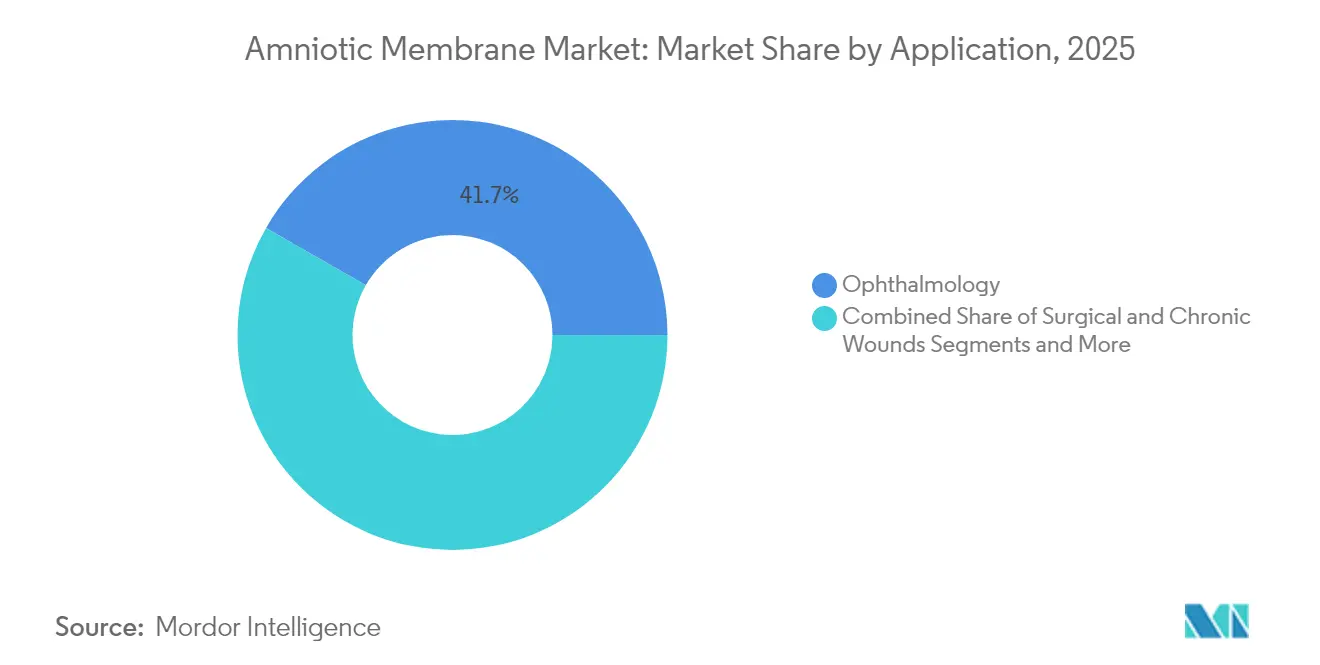

- By application, ophthalmology led with 41.70% of the amniotic membrane market size in 2025; surgical and chronic wounds are expanding the fastest at a 12.48% CAGR.

- By end-user, hospitals accounted for 62.55% share of the amniotic membrane market in 2025; specialty clinics are the quickest growing channel at 12.36% CAGR.

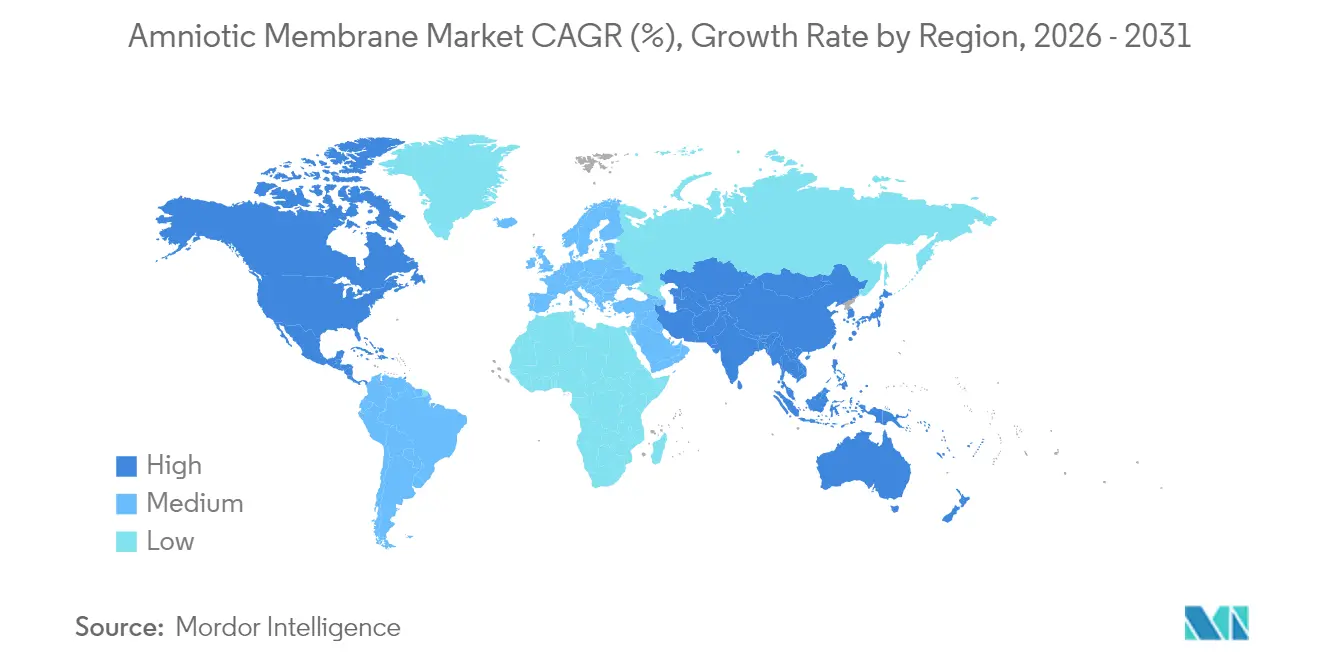

- By region, North America contributed 41.85% revenue in 2025, whereas Asia-Pacific is slated to deliver the highest 12.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amniotic Membrane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise In Road-Traffic Accident & Trauma Burden | +2.1% | Global, with highest impact in APAC and MEA | Medium term (2-4 years) |

| Escalating Ophthalmic Surgery Volumes in Ageing Populations | +2.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Growing Clinical Evidence & Awareness of Amniotic-Derived Biologics | +2.3% | Global, led by North America and EU | Short term (≤ 2 years) |

| Government Incentives for Advanced Wound-Care Adoption | +1.9% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Rapid Uptake of Composite Amnion-ECM Combination Grafts | +1.7% | North America, EU | Short term (≤ 2 years) |

| Emerging Veterinary Ophthalmology Use-Cases | +0.8% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in road-traffic accident & trauma burden

Emergency departments worldwide treat a growing number of complex wounds that benefit from biological dressings able to shorten healing time. Cryopreserved amniotic membranes have shown a 95.5% median wound-size reduction after 12 weeks in burn patients [2]G. Izadi et al., “Human Amniotic Membrane in Burn Wound Management,” MDPI, mdpi.com . National trauma guidelines increasingly reference these grafts for rapid epithelialization, and the World Health Organization prioritizes affordable trauma care protocols in developing regions. The resulting pull from both high-income and low-income markets underpins steady unit expansion during the medium term.

Escalating ophthalmic surgery volumes in ageing populations

Longer life expectancy drives higher rates of corneal repair, pterygium excision and severe dry-eye interventions. A sutureless dehydrated amniotic application reduced Ocular Surface Disease Index scores by 65% at six months in a recent randomized study. Medicare’s HCPCS code V2790 now allows separate billing for human amniotic membrane when used with select ocular CPT codes, cementing routine use in U.S. ambulatory surgery centers [3]Sònia Travé-Huarte, "Sutureless Dehydrated Amniotic Membrane (Omnigen) Application Using a Specialised Bandage Contact Lens (OmniLenz) for the Treatment of Dry Eye Disease: A 6-Month Randomised Control Trial," MDPI, mdpi.com. Comparable reimbursement pathways are emerging in Western Europe and Japan, making ophthalmology the anchor segment of the amniotic membrane market.

Growing clinical evidence & awareness of amniotic-derived biologics

Large-scale meta-analyses confirm that amniotic membrane therapy closes chronic wounds faster than standard dressings, largely owing to the HC-HA/PTX3 matrix that modulates inflammation. Publication momentum has moved the graft from “experimental” to guideline-backed in both wound care and ophthalmology societies, quickening adoption even among late-majority clinicians.

Government incentives for advanced wound-care adoption

The U.S. Physician Fee Schedule for 2025 set a national payment rate of USD 1,149 for amniotic allografts used on non-healing ulcers. Furthermore, Local Coverage Determinations now deem the product “reasonable and necessary” after four weeks of unsuccessful standard care, guaranteeing reimbursement when clinical criteria are met. Parallel reforms in China tie hospital bonuses to adoption of evidence-based regenerative products under the country’s RMB 205 trillion health-spending blueprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Standardized Processing Guidelines & Skilled Tissue-Bank Staff | -1.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| High Cost of Cryopreservation Logistics | -1.4% | Global, particularly affecting rural and remote areas | Short term (≤ 2 years) |

| Ethical / Procurement Controversies Around Placental Tissue | -0.9% | Select regions with cultural/religious restrictions | Long term (≥ 4 years) |

| Donor-Dependent Supply‐Chain Fragility | -1.6% | Global, with regional variations in donor availability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of standardized processing guidelines & skilled tissue-bank staff

Amniotic membrane processing demands rigorous donor screening and aseptic technique, yet regulatory guidance still varies widely. The American Association of Tissue Banks reports that many facilities struggle to align with evolving FDA expectations, slowing scale-up in resource-constrained settings. Training bottlenecks hinder capacity growth even when raw tissue supply is available.

High cost of cryopreservation logistics

Continuous ultra-low-temperature storage inflates total delivered cost in regions with limited cold-chain infrastructure. Lyopreserved grafts now retain parity with cryopreserved tissue while tolerating ambient shipment, according to comparative data on viable lyopreserved amnion. Adoption of such formats should ease cost pressure, yet capital outlays for new drying equipment slow near-term uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Preservation Method: Cryopreservation captures momentum despite dehydrated leadership

Dehydrated grafts commanded 58.62% amniotic membrane market share in 2025 thanks to shelf-stable logistics that fit lean hospital inventories. Nonetheless, cryopreserved products are growing at a 12.41% CAGR because they keep cellular components intact, boosting growth-factor delivery for recalcitrant wounds. One multicenter burn study showed cryopreserved allografts outperformed dehydrated peers in time-to-closure, underpinning the segment’s expansion.

Developers are closing the logistics gap via next-gen lyophilization that retains cell viability while allowing ambient storage—a hybrid model projected to widen total amniotic membrane market size for advanced preservation platforms by 2031. Suppliers able to scale both dehydration and cryopreservation lines stay best positioned to capture mixed provider preferences.

By Thickness: Multi-layer construction fuels premium sub-segment

Single-layer sheets still own 68.10% of revenue; yet multi-layer formats are accelerating at 12.55% CAGR because they withstand mechanical stress and release bioactive signals over longer intervals. Ultra-thick constructs enabled orbit socket reconstructions impossible with earlier patches, expanding the overall amniotic membrane market. However, extra lamination steps raise quality-control complexity, providing a moat for firms with automated stacking technologies.

As freeze-dried multi-layer lines reach parity in handling time with single-layer sheets, clinicians increasingly deploy them for orthopedic or large-area burns. That premium adoption trajectory lifts total amniotic membrane market size even in mature regions.

By Application: Surgical wounds outpace legacy ophthalmology base

Ophthalmology retained 41.70% revenue in 2025, yet the surgical and chronic wound segment is clocking the highest 12.48% CAGR. Surgeons now integrate amniotic grafts into total-joint revisions and abdominal closures to curb adhesions and speed re-epithelialization. Burn units cite reductions in analgesic use and better cosmetic outcomes versus conventional mesh dressings. The amniotic membrane market thus broadens beyond ocular care into core surgical pathways.

Veterinary orthopedics and sports-medicine clinics also trial injectable amnion hydrogels, demonstrating expansion into adjacent health verticals that could elevate the amniotic membrane market size over the next decade.

By End-User: Specialty clinics reshape distribution

Hospitals delivered 62.55% of 2025 sales, yet ambulatory and specialty clinics are gaining at 12.36% CAGR as reimbursement parity allows outpatient treatment. A cost study showed ProKera in-office application at CAD 699 versus CAD 1,561 for traditional transplantation in hospital theaters. Manufacturers now package pre-cut, ready-to-use disks targeting chairside use, broadening the amniotic membrane market footprint among community ophthalmologists and wound-care podiatrists.

Hospital demand remains solid for trauma and complex reconstructions, maintaining balanced channel dynamics and lowering single-buyer risk for suppliers.

Geography Analysis

North America held 41.85% of global revenue in 2025, driven by Medicare’s national payment rate and a clear regulatory path for tissue allografts. The amniotic membrane market size in the United States grows steadily as clinics shift chronic-ulcer care toward regenerative protocols. Canada’s provincial payers are adding coverage, and Mexico gears policy pilots around diabetic-foot management, securing region-wide momentum.

Asia-Pacific is the growth engine, slated for a 12.67% CAGR through 2031. China’s RMB 205 trillion health-spending plan subsidizes hospitals that adopt innovative biologics, propelling volume uptake. Japan and South Korea fast-track approvals under regenerative-medicine frameworks, while India’s expanding private hospital network pursues cost-effective wound solutions, enlarging the amniotic membrane market across diverse payer models.

Europe shows mid-single-digit revenue expansion backed by mature reimbursement but tempered by stringent tissue directives that slow new-product launches. Germany and the United Kingdom drive procedure counts, whereas Southern Europe advances gradually amid fiscal constraints.

Middle East & Africa and South America grow from a smaller base. Gulf states fund premium grafts in burn centers, yet donor-tissue logistics remain hurdles elsewhere. Brazil’s SUS system pilots outpatient amniotic therapy for diabetic ulcers, signaling longer-term lift for regional amniotic membrane market adoption.

Competitive Landscape

The field is moderately fragmented; the top five suppliers collectively control roughly 45% of global turnover. MiMedx leverages an extensive patent estate around dehydrated hydroburst processing, while Integra LifeSciences scales cryopreserved throughput through its NeoGenesis platform. Organogenesis emphasizes data generation, running multicenter trials that support payer negotiations. Smaller entrants develop amnion-collagen hybrids and injectable hydrogels to occupy white space not yet defended by established vendors.

Recent FDA guidance that reclassifies some grafts as 351 biologics complicates compliance and could prompt consolidation as smaller firms lack resources for full‐license submissions.

Meanwhile, lyopreservation innovators such as BioTissue position shelf-stable cryografts that undercut cold-chain costs and open new export lanes. Strategic alliances with tissue banks—and long-term supply contracts with hospital groups—remain the chief levers to expand the amniotic membrane market share without heavy price discounting.

Amniotic Membrane Industry Leaders

-

Human Regenerative Technologies, LLC

-

Katena Products. Inc.

-

MIMEDX

-

Amnio Technology, LLC

-

TissueTech, Inc. (BioTissue)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: BioTissue unveiled CAM360 AmnioGraft, a shelf-stable cryopreserved membrane aimed at bypassing cold-chain hurdles.

- July 2024: Medicare set a USD 1,149 payment rate for human amniotic membrane allografts in its 2025 Physician Fee Schedule.

- March 2024: MiMedx announced FDA designation of AXIOFILL as a 351 biologic and initiated legal action contesting the ruling.

Global Amniotic Membrane Market Report Scope

The amniotic membrane consists of a combination of tissues and cells, and it is the innermost layer of the placenta, which is widely used in ophthalmology and wound healing.

The amniotic membrane market is segmented by enzyme, application, end user, and geography. By enzymes, the market is segmented as cryopreserved amniotic membrane and dehydrated amniotic membrane. By application, the market is segmented as ophthalmology, surgical wounds, and other applications. By end user, the market is segmented as hospitals, ambulatory surgical centers, and other end users. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (USD) for the above segments.

| Cryopreserved |

| Dehydrated |

| Single-layer |

| Multi-layer |

| Ophthalmology |

| Surgical and Chronic Wounds |

| Orthopedics & Sports Medicine |

| Burn Management |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Preservation Method | Cryopreserved | |

| Dehydrated | ||

| By Thickness | Single-layer | |

| Multi-layer | ||

| By Application | Ophthalmology | |

| Surgical and Chronic Wounds | ||

| Orthopedics & Sports Medicine | ||

| Burn Management | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the amniotic membrane market?

The amniotic membrane market size stands at USD 3.75 billion in 2026 and is forecast to reach USD 6.58 billion by 2031.

Which preservation method is growing the fastest?

Cryopreserved grafts are expanding at a 12.41% CAGR because they maintain viable cells that accelerate healing.

Why is Asia-Pacific the fastest-growing region?

Large-scale healthcare spending in China and regulatory fast-tracking in Japan and South Korea are pushing Asia-Pacific toward a 12.67% CAGR.

What application represents the largest revenue share?

Ophthalmology leads with 41.70% of revenue thanks to routine use in corneal reconstruction and severe dry-eye procedures.

How do reimbursement policies affect adoption in the United States?

Medicare’s national payment rate of USD 1,149 per graft and clear coverage criteria for non-healing ulcers have accelerated provider uptake.

Are multi-layer grafts replacing single-layer sheets?

Multi-layer formats are gaining ground at 12.55% CAGR for complex wounds, but single-layer products remain dominant for routine cases due to lower cost and easier handling.

Page last updated on: