Coronary Artery Bypass Grafting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

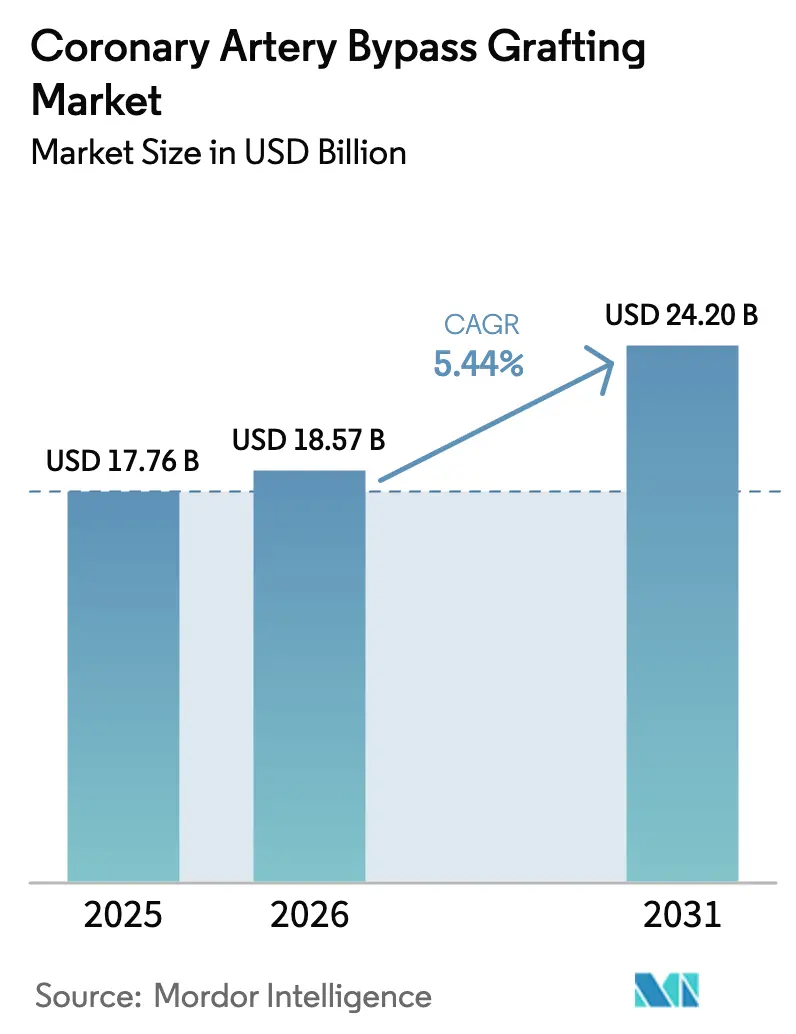

| Market Size (2026) | USD 18.57 Billion |

| Market Size (2031) | USD 24.20 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

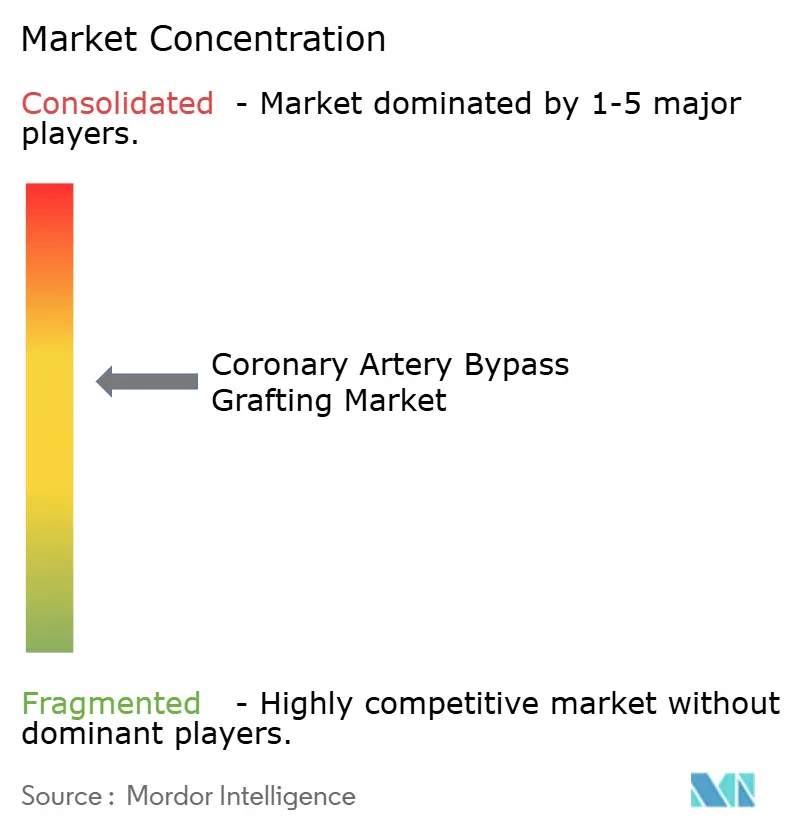

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coronary Artery Bypass Grafting Market Analysis by Mordor Intelligence

The Coronary Artery Bypass Grafting Market size is expected to grow from USD 17.76 billion in 2025 to USD 18.57 billion in 2026 and is forecast to reach USD 24.20 billion by 2031 at 5.44% CAGR over 2026-2031.

Hospitals continue to reserve surgery for complex multivessel disease, while routine lesions migrate to percutaneous coronary intervention, which keeps overall volumes stable but lifts average procedure value. Rising multimorbidity in aging G-20 populations and the documented survival edge of surgery over PCI in high SYNTAX-score cases reinforce demand even as robotic platforms compress length of stay.[1]United Nations Department of Economic and Social Affairs, “World Population Ageing 2020 Highlights,” United Nations, un.org Device makers counter competitive pressure with service contracts that cushion hardware cycles and with external stent innovations that extend graft longevity. Meanwhile, bundled-payment pilots in the United States and Germany reward centers that deliver complete revascularization with fewer readmissions, nudging hospitals toward multi-arterial grafting.

Key Report Takeaways

- On-pump surgery captured 54.73% of 2025 procedure-type revenue; minimally invasive and robotic CABG is projected to expand at a 9.24% CAGR through 2031.

- Heart positioners and tissue stabilizers led the 2025 product and services category with 26.63% of sales, while endoscopic vessel-harvesting systems are forecast to post the fastest growth at an 8.13% CAGR to 2031.

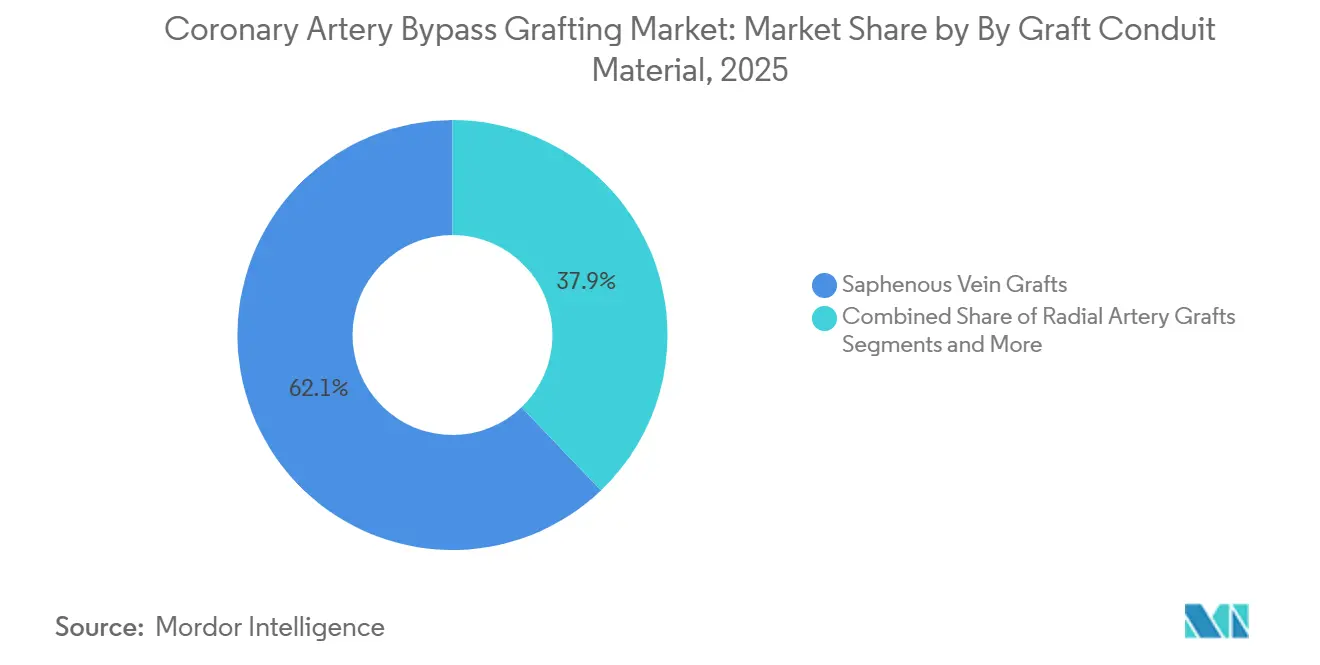

- Saphenous vein grafts commanded 62.14% of 2025 conduit value; synthetic and bio-engineered grafts are expected to grow at an 8.56% CAGR over the same period.

- Triple bypass procedures accounted for 30.53% of surgery complexity share in 2025, whereas quadruple-and-higher bypass operations are set to advance at a 9.23% CAGR through 2031.

- Hospitals held 64.25% of end-user revenue in 2025; ambulatory surgical centers represent the fastest-growing site of care with a 7.44% CAGR to 2031.

- North America controlled 36.44% of geographic revenue in 2025, while Asia-Pacific is projected to register the strongest regional expansion, at a 7.03% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coronary Artery Bypass Grafting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of complex multivessel CAD and diabetes | +1.2% | Asia-Pacific, Middle East showing highest absolute case growth | Medium term (2-4 years) |

| Aging population in G-20 economies expanding surgical candidate pool | +1.5% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Guideline preference for CABG over PCI in high SYNTAX-score disease | +0.8% | North America, Western Europe | Short term (≤ 2 years) |

| Transition to mini-sternotomy and robotic CABG unlocking day-7 discharge | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Commercialization of external stents for saphenous vein grafts | +0.6% | Europe, early adoption in North America | Medium term (2-4 years) |

| Regional bundled-payment pilots rewarding multi-arterial grafting outcomes | +0.5% | United States, Germany, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Complex Multivessel CAD and Diabetes

Diabetes sharply increases vessel disease complexity, and patients with both conditions see better survival with surgery than with PCI.[2]Chao Gao, “Temporal Trends in Cardiovascular Mortality Across the BRICS,” The Lancet Regional Health - Western Pacific, thelancet.comThe International Diabetes Federation expects diabetic adults to climb to 783 million by 2045, with most of the growth in low- and middle-income countries. In parallel, Asia faces a projected 91.2% jump in cardiovascular mortality by 2050, keeping surgical demand on a steep upward slope.[3]Chao Gao, “Temporal Trends in Cardiovascular Mortality Across the BRICS,” The Lancet Regional Health - Western Pacific, thelancet.com Because diabetic multivessel disease often exceeds SYNTAX 22, guidelines now direct such cases to heart teams for CABG referral. As screening improves and populations age, the coronary artery bypass grafting market gains a sizeable inflow of high-complexity candidates.

Aging Population in G-20 Economies Expanding Surgical Candidate Pool

Citizens aged 65 and older will represent 24.3% of the G-20 population by 2050. Older patients present diffuse disease and more left main involvement, both indications for complete surgical revascularization. Japan, Germany, Italy, and South Korea face the steepest demographic curves, while the U.S. training pipeline has doubled cardiothoracic residents since 2008. However, perfusionist numbers lag; half of the current U.S. workforce may retire by 2031. This imbalance fuels wait lists in Canada and the United Kingdom, intensifying pressure on hospitals to streamline case scheduling.

Guideline Preference for CABG Over PCI in High SYNTAX-Score Disease

The 2021 ACC/AHA/SCAI revascularization guideline assigns Class I status to CABG for left main or multivessel disease with SYNTAX > 22. Real-world evidence from 2024 shows minimally invasive direct CABG cutting myocardial infarction risk by 54% versus second-generation drug-eluting stents. Electronic medical record decision-support tools now flag high-SYNTAX cases for surgical consult, shifting referral volumes toward operating rooms in academic networks.

Transition to Mini-Sternotomy and Robotic CABG Unlocking Day-7 Discharge

A 2024 meta-analysis reported 96% graft patency and sub-1% mortality for robotic CABG, with median stay shortened by two to three days. Leasing plans introduced by Intuitive Surgical in 2024 lower capital barriers, letting mid-sized hospitals adopt the technology. CMS bundled-payment rules reward institutions that discharge patients sooner and curb readmissions, so robotic programs increasingly move low-risk cases into same-week discharge pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PCI drug-eluting stent iterations lowering repeat-intervention rates | –0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Limited global stock of CABG-skilled surgeons and perfusionists | –0.9% | Global, acute in Canada, United Kingdom, Australia | Short term (≤ 2 years) to Long term (≥ 4 years) |

| Procedural CO₂ footprint scrutiny in EU ETS phase-in | –0.3% | Europe with spill-over to United Kingdom, Switzerland | Short term (≤ 2 years) |

| Rising U.S. tariffs on precision CABG components inflating ASPs | –0.4% | United States with ripple effects on global supply chains | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PCI Drug-Eluting Stent Iterations Lowering Repeat-Intervention Rates

Biodegradable-polymer stents cut four-year major adverse events to 14.2% from 23.0% in recent randomized work. With second-generation everolimus devices delivering sub-10% five-year failure, intermediate SYNTAX cases now lean toward PCI. Johnson & Johnson’s 2024 purchase of Shockwave Medical adds lithotripsy that lets interventionalists tackle calcified lesions once sent to surgery. As the technology diffuses, the coronary artery bypass grafting market faces gradual patient leakage in Western referral patterns.

Limited Global Stock of CABG-Skilled Surgeons and Perfusionists

Canada has only 375 perfusionists for 39 million citizens, and vacancies stand near 40. A CBC investigation tied 80 deaths to delayed surgery in Quebec during 2023-2024. U.S. surveys predict a 35.1% perfusionist shortfall by 2031. Low-income nations lack accredited schools, pushing hospitals to recruit overseas staff, which inflates costs and caps procedure volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Robotic Platforms Reshape Length-of-Stay Economics

On-pump techniques retained 54.73% of revenue in 2025, maintaining the largest coronary artery bypass grafting market share, while the coronary artery bypass grafting market size for minimally invasive and robotic platforms is set to expand at a 9.24% CAGR through 2031. Hospitals value on-pump CABG for reliable myocardial protection when tackling three-vessel disease. Off-pump surgery holds niche appeal for calcified aortas but shows no survival edge in pooled data. Robotic systems close the cosmetic gap with PCI, reducing sternotomy discomfort and freeing ICU beds within 48 hours. Training curves have shortened to roughly 20 cases, and new leasing models spread capital outlays across five-year horizons.

Growth in robotic procedures also enables select cases in ambulatory centers, especially single- or double-vessel disease with preserved ventricular function. CMS pays a single bundled rate, so facilities that discharge on or before postoperative day 3 keep more of the margin. As hospitals chase these savings, the phrase coronary artery bypass grafting market will increasingly denote an ecosystem where acuity stratification, not volume, drives revenue.

By Product and Services: Endoscopic Harvesting Gains as Surgeons Prioritize Cosmesis

Heart positioners and tissue stabilizers led 2025 sales at 26.63%, but endoscopic harvesting devices will grow fastest at 8.13% through 2031. Their use drops leg-wound infection to below 2% and trims operative time by nearly 25 minutes in contemporary series. Cardiopulmonary bypass consoles face elongated replacement cycles—often exceeding 15 years—as vendors deliver modular oxygenator upgrades. Services tied to those consoles generate 30% of Getinge’s cardiovascular revenue, smoothing demand across purchase cycles.

Anastomosis assist tools gain traction in robotic cases where instrument articulation is limited. Meanwhile, regional suppliers compete on cannula price, especially in India and Brazil, although U.S. centers pay a premium for heparin-bonded tubing that reduces hemolysis. Vendor consolidation continues; 62% of U.S. programs have trimmed their supplier list by at least 20% since 2021. This shift concentrates bargaining power and reinforces the dominance of multinational brands in the coronary artery bypass grafting market.

By Graft / Conduit Material: External Stents Extend Saphenous Vein Durability

Saphenous vein grafts held 62.14% value in 2025, but the coronary artery bypass grafting market size for synthetic and bio-engineered conduits is projected to grow at 8.56% through 2031. External stents like VEST reduce intimal hyperplasia, lifting four-year perfect patency by 33 percentage points. Internal thoracic arteries remain the gold standard for the left anterior descending artery with >90% ten-year patency, and their bilateral use is rising despite a slightly higher sternal infection risk in diabetics.

Radial artery grafts deliver 80-85% ten-year patency when paired with ≥70% target stenosis, making them the conduit of choice for right coronary lesions. Tissue-engineered constructs enter adult trials in 2026, promising off-the-shelf options that remodel into living vessels. Once safety data mature, these innovations could redefine the coronary artery bypass grafting market landscape by shrinking the gap between surgical and endovascular durability.

By Surgery Complexity: Quadruple Bypass Surges as Diabetes Drives Diffuse Disease

Triple grafting made up 30.53% of 2025 cases, yet quadruple-plus procedures will grow at 9.23%, the highest rate among complexity tiers. Diffuse plaque in diabetic and older patients often mandates four or five distal anastomoses to avoid incomplete revascularization. Bilateral thoracic artery use in these extensive cases reduces ten-year mortality by 20% but doubles sternal-wound infection to near 2-3% in diabetes cohorts.

Asia-Pacific sees the sharpest rise in high-complexity surgeries as late presentation converges with rising diabetes prevalence. Operative times stretch past five hours, and conduit demand increases, boosting sales of connector systems that speed sequential anastomoses. This shift underlines how procedure mix, not just total case count, shapes revenue pools within the coronary artery bypass grafting market.

By End User: Ambulatory Centers Pilot Same-Day CABG

Hospitals retained 64.25% share in 2025 and will stay dominant because they own ICUs and perfusion teams. Still, ambulatory surgical centers are forecast to log a 7.44% CAGR through 2031 as robotic technology and enhanced recovery protocols make same-day discharge feasible for select patients. Cardiac centers anchored to academic institutes run early trials and training that validate safety before diffusion to community settings.

The broadened end-user mix dilutes fixed-cost coverage for hospital theaters, pushing administrators to focus on complex referrals and hybrid OR upgrades. Clinics that master perioperative tele-monitoring can capture follow-up revenue while lowering readmission risk, a critical advantage in bundled-payment economics. Collectively, these dynamics reinforce segmentation depth within the coronary artery bypass grafting market.

Geography Analysis

North America generated 36.44% of 2025 revenue, rooted in roughly 200,000 annual U.S. procedures and early adoption of robotic consoles. Medicare reimbursement for multi-arterial grafting plus bundled payments under BPCI Advanced keep profit pools attractive despite stable case counts. Canada’s perfusionist shortage produced 80 surgery-delay deaths in Quebec during the 18 months to mid-2024. Mexico continues to send complex cases north, bolstering regional volumes.

Asia-Pacific will record a 7.03% CAGR through 2031, the fastest of any region, as diabetes prevalence and infrastructure investment collide. China has added more than 200 cardiac surgery units since 2020; many feature hybrid suites capable of both CABG and transcatheter valve work. India’s market splits between high-volume private chains in metros and resource-limited public hospitals elsewhere. Japan and South Korea aim to mitigate workforce gaps by expanding integrated six-year cardiothoracic residencies, helping preserve procedure capacity as populations age past 30% elderly.

Europe trails in growth but retains significant volume, led by Germany’s 70,000 annual cases. The EU Emissions Trading System now pressures hospitals to curb OR carbon output, nudging procurement toward reusable instruments. The United Kingdom adopted the VEST external stent in five trusts, setting precedent for technology appraisal across the bloc. Gulf nations in the Middle East recruit international surgical teams to build regional hubs, while Brazil and Argentina ramp private-sector robotic programs to serve patients once bound for U.S. centers.

Competitive Landscape

Five multinational firms such as Medtronic, Edwards Lifesciences, LivaNova, Getinge, and Terumocontrol the majority of capital equipment sales, leaving consumables to a fragmented set of regional vendors. Edwards booked USD 5.44 billion in 2024 net sales, with surgical products at USD 981.3 million and R&D at 19% of revenue. Medtronic bundles heart-lung machines with long-term service, locking in customers for a decade. LivaNova leverages its Sorin heritage to dominate oxygenators while branching into neuromodulation.

Getinge derives 30% of cardiovascular turnover from service contracts and now offers remote perfusion circuit monitoring. Terumo competes on hi-flow tubing and low-prime oxygenators popular in off-pump cases. Intuitive Surgical upended capital cycles by rolling out a leasing plan in 2024, sparking interest among community hospitals that previously balked at USD 2 million list prices.

White-space innovation targets external vein stents and tissue-engineered grafts. Vascular Graft Solutions awaits U.S. clearance after its pivotal trial failed to meet the primary endpoint, but subset wins keep surgeons engaged. Smaller firms like AtriCure bundle atrial fibrillation ablation tools with CABG kits, broadening addressable spend per procedure. As buyers consolidate vendors, integrated portfolios and post-sale support become decisive in the coronary artery bypass grafting market.

Coronary Artery Bypass Grafting Industry Leaders

Medtronic Plc

Getinge AB

Terumo Corporation

LivaNova PLC

Edwards Lifesciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: A Bengaluru hospital executed a combined robot-assisted minimally invasive direct coronary artery bypass and radical prostatectomy in one session, marking a multidisciplinary milestone.

- January 2026: The U.S. FDA cleared non-force-feedback instruments for Intuitive’s da Vinci 5 system during cardiac procedures, expanding tool options for robotic surgeons.

- April 2025: Teleflex received FDA 510(k) clearance for the AC3 Range intra-aortic balloon pump intended for patient transport.

Global Coronary Artery Bypass Grafting Market Report Scope

As per the scope of the report, coronary artery bypass grafting (CABG) is a surgical treatment for patients with coronary artery disease (CAD) in which an alternate passage is created for blood to flow to the heart. It is common for three or four coronary arteries to be bypassed during surgery.

The Coronary Artery Bypass Grafting Market Report is segmented by Procedure Type, Product and Services, Graft / Conduit Material, Surgery Complexity, End User, and Geography. By Procedure Type, the market is segmented into On-pump CABG, Off-pump CABG, and Minimally Invasive and Robotic-Assisted CABG. By Product and Services, the market is segmented into Cardiopulmonary Bypass Machines, Endoscopic Vessel Harvesting Systems, Heart Positioners & Tissue Stabilizers, Cannulas & Tubing Sets, Anastomosis Assist Devices, Services, and Others. By Graft / Conduit Material, the market is segmented into Saphenous Vein Grafts, Internal Thoracic Artery Grafts, Radial Artery Grafts, and Synthetic & Bio-engineered Grafts. By Surgery Complexity, the market is segmented into Single Bypass, Double Bypass, Triple Bypass, and Quadruple & Higher bypass procedures. By End User, the market is segmented into Hospitals, Cardiac Centres & Clinics, Ambulatory Surgical Centres, and Academic & Research Institutes. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America.The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| On-pump CABG |

| Off-pump CABG |

| Minimally Invasive and Robotic-Assisted CABG |

| Cardiopulmonary Bypass Machines |

| Endoscopic Vessel Harvesting Systems |

| Heart Positioners & Tissue Stabilizers |

| Cannulas & Tubing Sets |

| Anastomosis Assist Devices |

| Services |

| Others |

| Saphenous Vein Grafts |

| Internal Thoracic Artery Grafts |

| Radial Artery Grafts |

| Synthetic & Bio-engineered Grafts |

| Single Bypass |

| Double Bypass |

| Triple Bypass |

| Quadruple & Higher |

| Hospitals |

| Cardiac Centres & Clinics |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | On-pump CABG | |

| Off-pump CABG | ||

| Minimally Invasive and Robotic-Assisted CABG | ||

| By Product and Services | Cardiopulmonary Bypass Machines | |

| Endoscopic Vessel Harvesting Systems | ||

| Heart Positioners & Tissue Stabilizers | ||

| Cannulas & Tubing Sets | ||

| Anastomosis Assist Devices | ||

| Services | ||

| Others | ||

| By Graft / Conduit Material | Saphenous Vein Grafts | |

| Internal Thoracic Artery Grafts | ||

| Radial Artery Grafts | ||

| Synthetic & Bio-engineered Grafts | ||

| By Surgery Complexity | Single Bypass | |

| Double Bypass | ||

| Triple Bypass | ||

| Quadruple & Higher | ||

| By End User | Hospitals | |

| Cardiac Centres & Clinics | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the coronary artery bypass grafting market in 2026?

The coronary artery bypass grafting market size reached USD 18.57 billion in 2026 and is projected to grow steadily through 2031.

What is the expected CAGR for global CABG revenue?

Market revenue is forecast to increase at a 5.44% CAGR from 2026 to 2031.

Which CABG procedure type is growing fastest?

Minimally invasive and robotic CABG is projected to post a 9.24% CAGR, the highest among all procedure types.

Why are external stents drawing attention in vein grafting?

Devices such as VEST cut intimal hyperplasia and raise four-year perfect patency from 48% to 81%, improving long-term graft durability.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to expand at a 7.03% CAGR to 2031, propelled by rising diabetes prevalence and ongoing infrastructure investment.

How are bundled-payment models influencing CABG practice?

Programs like CMS BPCI Advanced reward complete revascularization with short stays, pushing hospitals toward multi-arterial and robotic strategies that lower readmissions.

Page last updated on: