Transdermal Drug Delivery Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

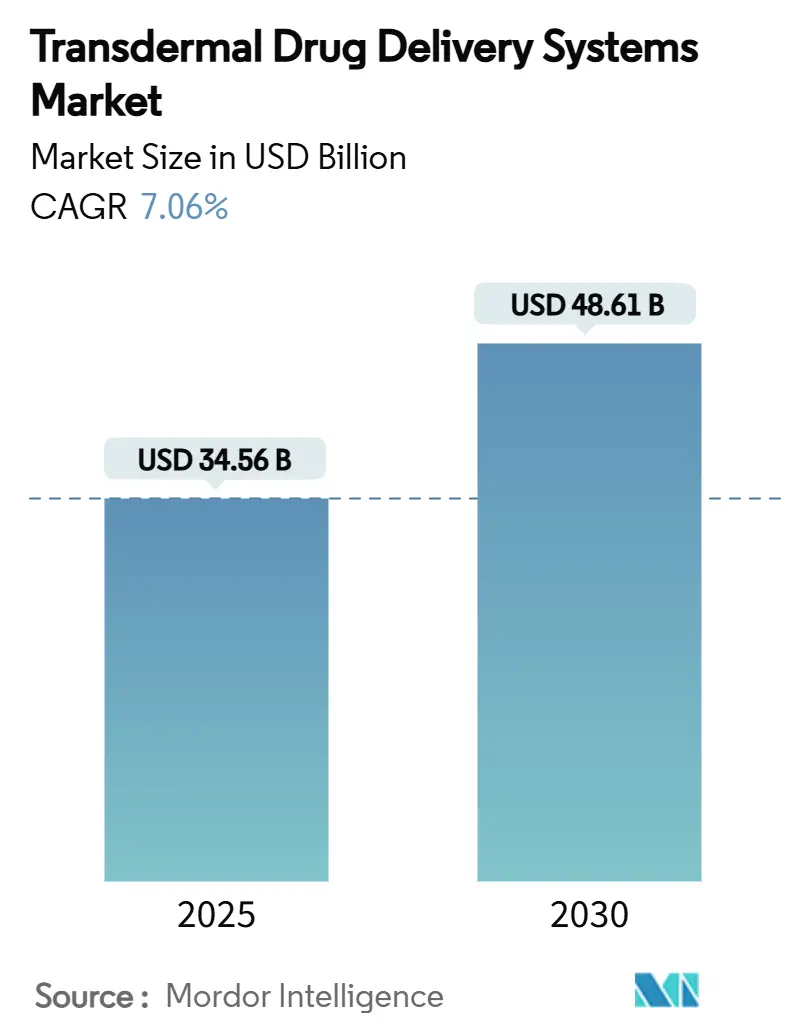

| Market Size (2025) | USD 34.56 Billion |

| Market Size (2030) | USD 48.61 Billion |

| Growth Rate (2025 - 2030) | 7.06% CAGR |

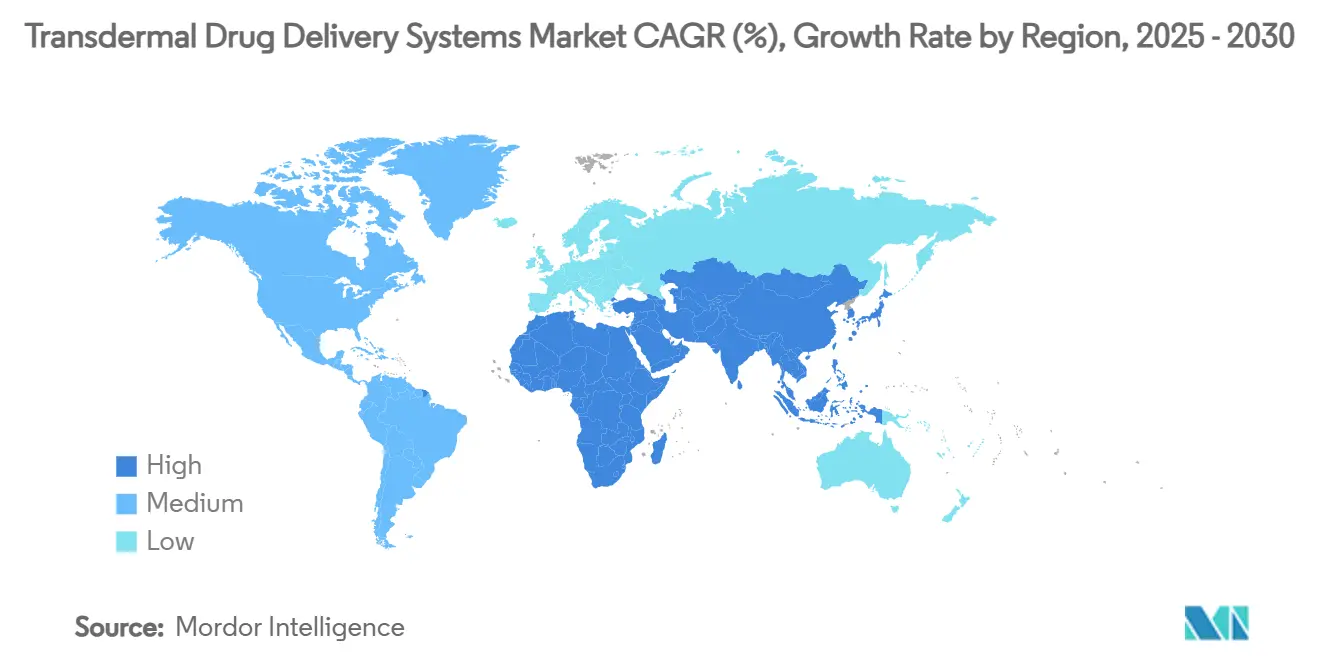

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transdermal Drug Delivery Systems Market Analysis by Mordor Intelligence

The transdermal drug delivery systems market size reached USD 34.56 billion in 2025 and is forecast to reach USD 48.61 billion by 2030, reflecting a 7.06% CAGR. Demand growth rests on patient-centric delivery formats that bypass first-pass metabolism, advanced patch designs, and digital monitoring features that convert passive patches into active therapeutic tools. The transdermal drug delivery systems market is also supported by regulatory momentum for opioid alternatives, rapid progress in biodegradable films, and widening access to home-care services. Competitive intensity is shaped by a mix of large pharmaceutical companies and focused technology firms, each pushing microneedle, iontophoretic, and smart-patch solutions. Asia-Pacific’s high CAGR signals a geographic rebalancing even as North America remains the revenue leader. Sustainability mandates, particularly in Europe, add pressure to innovate with compostable substrates and solvent-free adhesives.

Key Report Takeaways

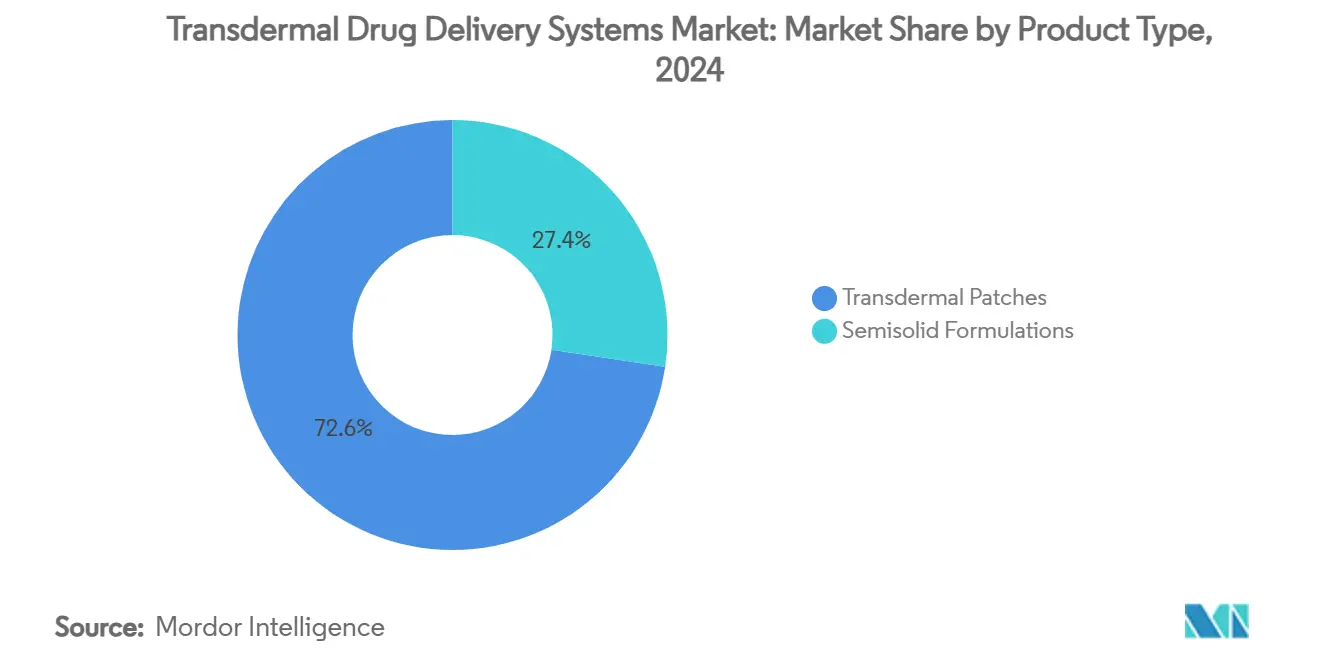

- By product type, transdermal patches led with 72.64% transdermal drug delivery systems market share in 2024; semisolid formulations are projected to expand at an 8.34% CAGR through 2030.

- By delivery type, passive systems accounted for 78.65% share of the transdermal drug delivery systems market size in 2024, while active systems are forecast to grow at 9.63% CAGR to 2030.

- By patch type, drug-in-adhesive designs held 42.36% transdermal drug delivery systems market share in 2024; microneedle patches show the highest 11.55% CAGR through 2030.

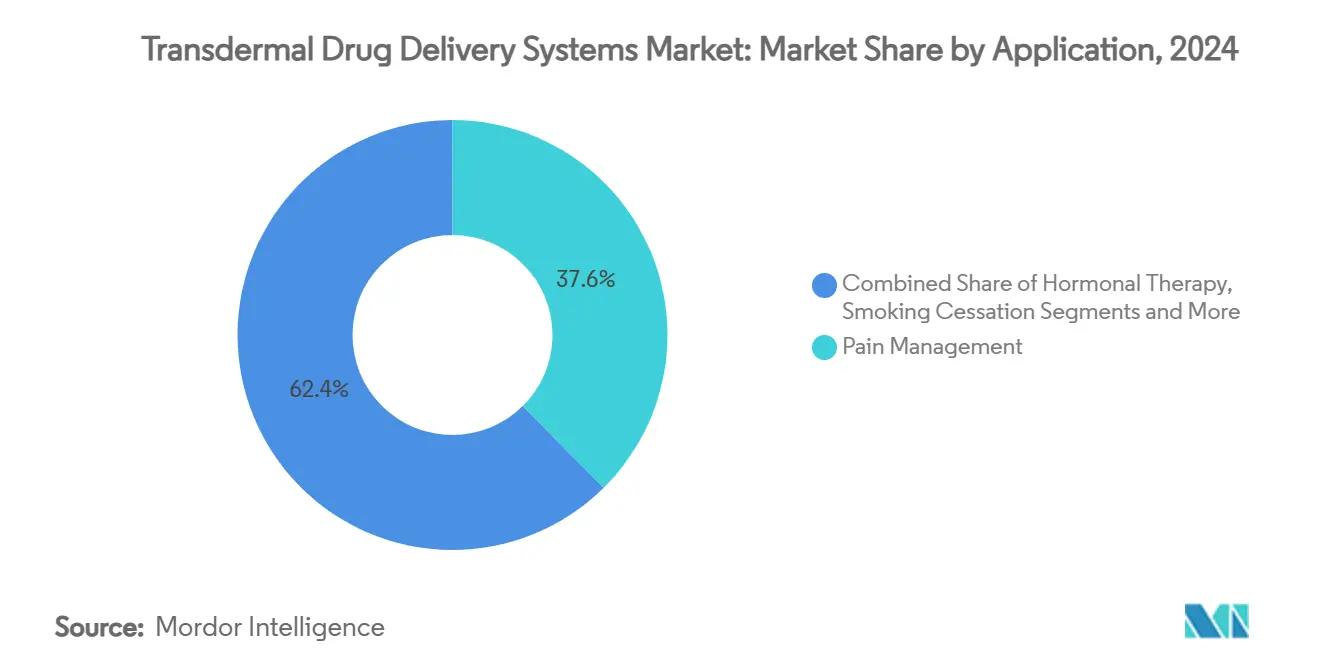

- By application, pain management commanded 37.58% of the transdermal drug delivery systems market size in 2024; hormonal therapy advances at an 8.12% CAGR to 2030.

- By end user, home-care settings captured 56.48% revenue share in 2024 and will post a 9.04% CAGR to 2030.

- By geography, North America retained 41.23% transdermal drug delivery systems market share in 2024, yet Asia-Pacific is growing at 9.37% CAGR through 2030.

Global Transdermal Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.8% | Global; North America & Europe concentrated | Long term (≥ 4 years) |

| Patient preference for non-invasive delivery | +1.2% | Global; strongest in Asia-Pacific | Medium term (2-4 years) |

| Advances in patch design & adhesion materials | +0.9% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Wearable electronics enabling dose personalisation | +0.7% | North America & EU core markets | Long term (≥ 4 years) |

| Demand for biologic delivery via microneedles | +1.1% | Global; early adoption in developed markets | Long term (≥ 4 years) |

| Sustainability push for biodegradable patch films | +0.4% | EU leading; expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Chronic ailments such as diabetes, cardiovascular disease, and persistent pain enlarge the patient base for transdermal systems by favoring steady-state drug levels and fewer dosing steps. Diabetes now affects 537 million adults worldwide, while chronic pain burdens more than 50 million people in the United States alone. Flexible, ultrasound-powered implants that work in concert with skin patches illustrate how the transdermal drug delivery systems market is shifting from passive release to active management. This approach supports continuous therapy models, aligning with value-based care incentives that reward adherence and outcome stability.

Patient Preference for Non-Invasive Delivery

Acceptance rates for patches exceed 95% among individuals who refuse oral medicines, far surpassing injection acceptance. Clinical studies on nicotine patches show improved endothelial progenitor cell function without hemodynamic compromise, adding cardiovascular benefit to smoking cessation protocols.[1]Ting-Yi Tien, “Transdermal Nicotine Patch Increases the Number and Function of Endothelial Progenitor Cells,” pubmed.ncbi.nlm.nih.govHigher tolerance levels in psychiatric and geriatric cohorts further enlarge the transdermal drug delivery systems market by reducing clinic visits and enabling self-application.

Advances in Patch Design & Adhesion Materials

Seven-day wear times are now achievable with pressure-sensitive adhesives that hold through perspiration and mechanical strain. Medherant’s TEPI technology demonstrates water-resistant, high-load patches that stay intact under 30% stretch, cutting premature replacement incidents that once exceeded 30%.[2]Medherant, “Innovative Patch Technology for Transdermal Drug Delivery,” nature.com Coupling surface acoustic waves with lipid nanocapsules produces release profiles matched to patient physiology, strengthening therapy control.

Wearable Electronics Enabling Dose Personalisation

Smart patches integrate sensors, processors, and delivery reservoirs on flexible substrates. Professor Kyung-In Jang’s foldable patch measures cardiovascular signals and dispenses medication in the same unit. A smartphone-controlled microneedle device can release multiple drugs selectively, reflecting how the transdermal drug delivery systems market is merging with digital therapeutics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin irritation & contact dermatitis | -0.8% | Global; higher sensitivity in Asia-Pacific | Short term (≤ 2 years) |

| Limited drug-molecule suitability | -1.2% | Global; all therapeutic areas | Long term (≥ 4 years) |

| Regulatory scrutiny over opioid patch diversion | -0.6% | North America & EU | Medium term (2-4 years) |

| Environmental concerns on patch disposal | -0.3% | EU leading; expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skin Irritation & Contact Dermatitis

Contact dermatitis affects up to 20% of patch users, undermining adherence in extended-wear designs. Daily corticosteroid creams can change release kinetics, requiring delicate balance between skin comfort and drug performance.[3]Lori Reisner, “Opioid Patches,” pain.ucsf.edu Hypoallergenic adhesives and pH-neutral layers are therefore critical to market growth, especially among pediatric and geriatric populations.

Limited Drug-Molecule Suitability

Most molecules exceed 600 Daltons or lack the lipophilicity needed for passive diffusion. Microneedles, iontophoresis, and sonophoresis broaden the reachable portfolio but add device complexity and cost. Even when penetration barriers are solved, drugs must remain stable at skin temperature for days, curbing pipeline candidates despite technology gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Formats Gain Momentum

Transdermal patches contributed 72.64% of 2024 revenue, demonstrating deep clinical trust and scalable production economics. Semisolid gels, although smaller, are on track for an 8.34% CAGR, capitalizing on dose-flexible, site-specific delivery that appeals to dermatology and hormonal applications. The transdermal drug delivery systems market therefore balances reliable patch sales with novel gel rollouts, aided by electrospun nanofiber composites for psoriasis that mix patch adhesion and ointment-level precision.

Second-generation hybrids combine adhesive layers with gel reservoirs, letting clinicians titrate doses without replacing the entire device. Such versatility supports personalized medicine and may expand formulary inclusion among payers seeking outcome-based pricing models.

By Delivery Type: Electronics Expand Reach

Passive diffusion remains the workhorse with 78.65% share, yet active systems are the clear growth engine at 9.63% CAGR. Mini-pumps, electroporation, and low-voltage iontophoresis allow macromolecules to traverse the skin, strengthening the transdermal drug delivery systems market position in biologics. A vialess heterogeneous patch that houses force-driven micro-pumps exemplifies battery-free engineering that preserves flexibility.

In chronic diseases requiring variable dosing, app-linked controllers modulate delivery rates in response to real-time biometrics. Such closed-loop capability elevates patches from dispensers to decision-support nodes, harmonizing with telehealth workflows.

By Patch Type: Microneedles Accelerate

Drug-in-adhesive designs, holding 42.36% of 2024 revenue, remain the baseline option, thanks to low material cost and established regulatory pathways. Microneedle arrays, however, will climb at an 11.55% CAGR as their ability to deliver biologics, vaccines, and nucleic acid therapies becomes indispensable. Biodegradable double-network microneedles merge gelatin methacrylate strength with acellular neural matrix bio-compatibility, easing insertion pain while ensuring complete dissolution.

Matrix and reservoir formats persist in high-dose or moisture-sensitive formulations, but value shifts toward microneedle solutions that unlock premium indications and command higher reimbursements.

By Application: Hormonal Therapy Surges

Pain management dominated with 37.58% revenue in 2024 due to chronic lower-back and cancer pain prevalence. Hormonal therapy, rising at 8.12% CAGR, benefits from evidence that estradiol patches match injectable androgen deprivation in metastatic prostate cancer.

Testosterone patches for post-menopausal women also reinforce demand. CNS disorders, cardiovascular diseases, and smoking cessation hold stable shares yet await molecule-suitability breakthroughs to reignite faster growth.

By End User: Home-Care Leads and Accelerates

Home-care environments generated 56.48% of 2024 sales and will keep a 9.04% CAGR through 2030 as payers encourage outpatient treatment. Smart patches that pair continuous glucose monitoring with drug dosing fit this ecosystem, lowering clinic visit frequency.

Hospitals and clinics still prefer patches for acute pain and controlled settings, but shifting reimbursement models push chronic therapy volumes to consumer channels.

Geography Analysis

North America’s leadership arises from streamlined approvals like the March 2025 generic lidocaine 1.8% patch, which broadened access at lower cost. Growing chronic pain and diabetes cases reinforce patch utilization, and high per-capita healthcare spend supports premium technologies. Canada and Mexico benefit from cross-border tech transfer and joint pharmacovigilance frameworks that accelerate regional market entries.

Asia-Pacific races ahead on the back of large populations and manufacturing economies of scale. China, Japan, and South Korea innovate in flexible electronics and microneedle tooling, enabling domestic firms to export cost-competitive smart patches. India and Australia improve healthcare reach through telemedicine that pairs well with self-applied transdermal systems. Government initiatives to manage diabetes and cardiovascular disease intensify demand for long-acting patches in rural areas, boosting the transdermal drug delivery systems market.

Europe’s steady growth is tied to its green agenda. Projects such as biodegradable suction patches for peptide delivery earn public funding and fast-track reviews, aligning medical innovation with environmental regulation. Germany and the United Kingdom invest in advanced adhesion chemistries, while France and Spain emphasize chronic disease self-management through reimbursement reforms that favor home-care patches.

Competitive Landscape

The market shows moderate fragmentation. Hisamitsu Pharmaceutical dominates external pain relief with SALONPAS patches and leverages decades-long expertise in drug-in-adhesive technology. Agile Therapeutics, now part of Insud Pharma, gains wider geographic reach for its hormonal patch franchise. Start-ups such as Anodyne Nanotech target GLP-1 peptide delivery, signaling a shift toward metabolic disease indications.

Strategic moves concentrate on platform expansion. Established firms add digital layers for adherence tracking, while newcomers license microneedle molds or adhesive patents to accelerate entry. Partnerships with wearable sensor companies are common, reflecting convergence between med-tech and pharma. Pricing pressure and sustainability demands encourage shared manufacturing lines that minimize solvent use and improve waste recovery.

Transdermal Drug Delivery Systems Industry Leaders

Hisamitsu Pharmaceutical Co., Inc.

Novartis AG

Johnson & Johnson

Viatris Inc.

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA cleared the first generic lidocaine 1.8% patch from Aveva Drug Delivery Systems, giving clinicians a cost-saving option against ZTlido.

- February 2025: STAMPEDE trial data confirmed transdermal estradiol patches are non-inferior to standard injectables for metastatic prostate cancer.

- December 2024: Anodyne Nanotech announced >50% bioavailability for GLP-1 drugs via HeroPatch, with Phase I trials slated for 2025.

Global Transdermal Drug Delivery Systems Market Report Scope

| Transdermal Patches |

| Semisolid Formulations (Gels, Ointments) |

| Passive Systems |

| Active Systems (Iontophoresis, Microneedles, Sonophoresis) |

| Drug-in-Adhesive |

| Matrix |

| Reservoir |

| Microneedle-Based |

| Pain Management |

| Central Nervous System Disorders |

| Hormonal Therapy |

| Cardiovascular Diseases |

| Smoking Cessation |

| Others (Motion Sickness, Oncology, etc.) |

| Home-Care Settings |

| Hospitals & Clinics |

| Others (Retail Pharmacies, E-commerce) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Transdermal Patches | |

| Semisolid Formulations (Gels, Ointments) | ||

| By Delivery Type | Passive Systems | |

| Active Systems (Iontophoresis, Microneedles, Sonophoresis) | ||

| By Patch Type | Drug-in-Adhesive | |

| Matrix | ||

| Reservoir | ||

| Microneedle-Based | ||

| By Application | Pain Management | |

| Central Nervous System Disorders | ||

| Hormonal Therapy | ||

| Cardiovascular Diseases | ||

| Smoking Cessation | ||

| Others (Motion Sickness, Oncology, etc.) | ||

| By End User | Home-Care Settings | |

| Hospitals & Clinics | ||

| Others (Retail Pharmacies, E-commerce) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the transdermal drug delivery systems market?

The market reached USD 34.56 billion in 2025 and is projected to hit USD 48.61 billion by 2030 at a 7.06% CAGR.

2. Which product type dominates sales?

Traditional transdermal patches held 72.64% of 2024 revenue, outpacing semisolid gels.

3. Why are microneedle patches gaining attention?

They enable delivery of large molecules such as peptides and biologics, driving an 11.55% CAGR in their category.

4. Which region is expanding fastest?

Asia-Pacific is forecast to grow at 9.37% CAGR thanks to manufacturing scale and widening healthcare access.

5. How important is home-care use?

Home-care settings already account for 56.48% of sales and will expand at 9.04% CAGR, propelled by smart patches that combine monitoring with dosing.

Page last updated on: