Non-Viral Drug Delivery Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

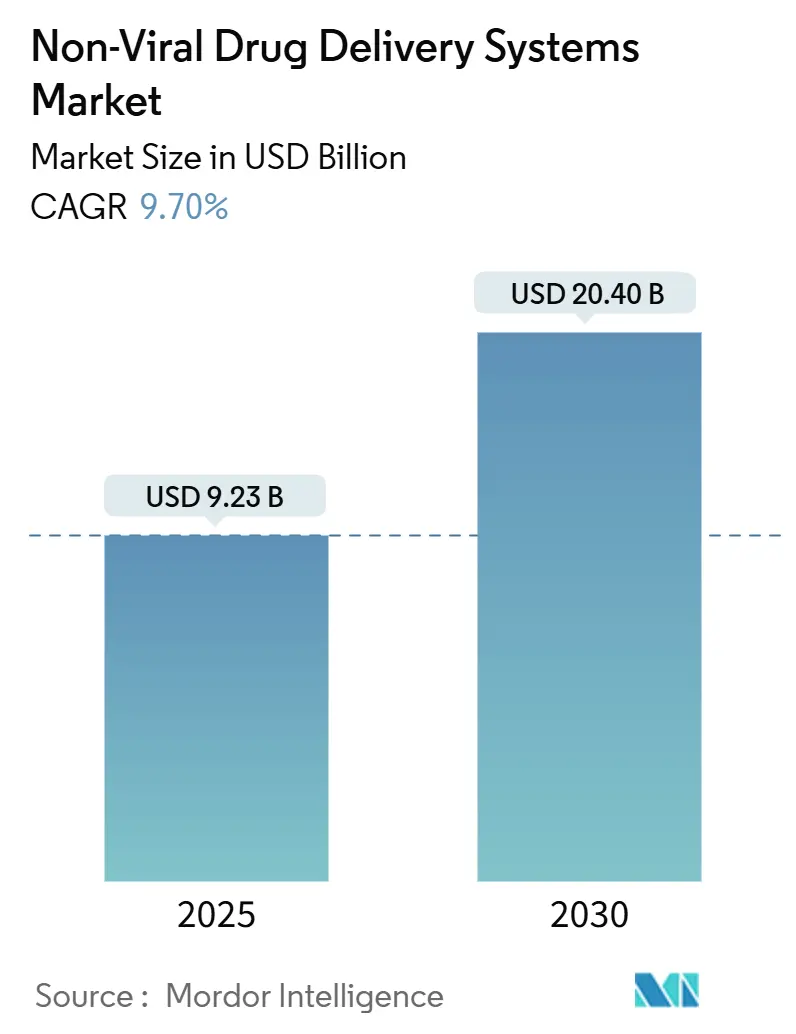

| Market Size (2025) | USD 9.23 Billion |

| Market Size (2030) | USD 20.40 Billion |

| Growth Rate (2025 - 2030) | 9.70% CAGR |

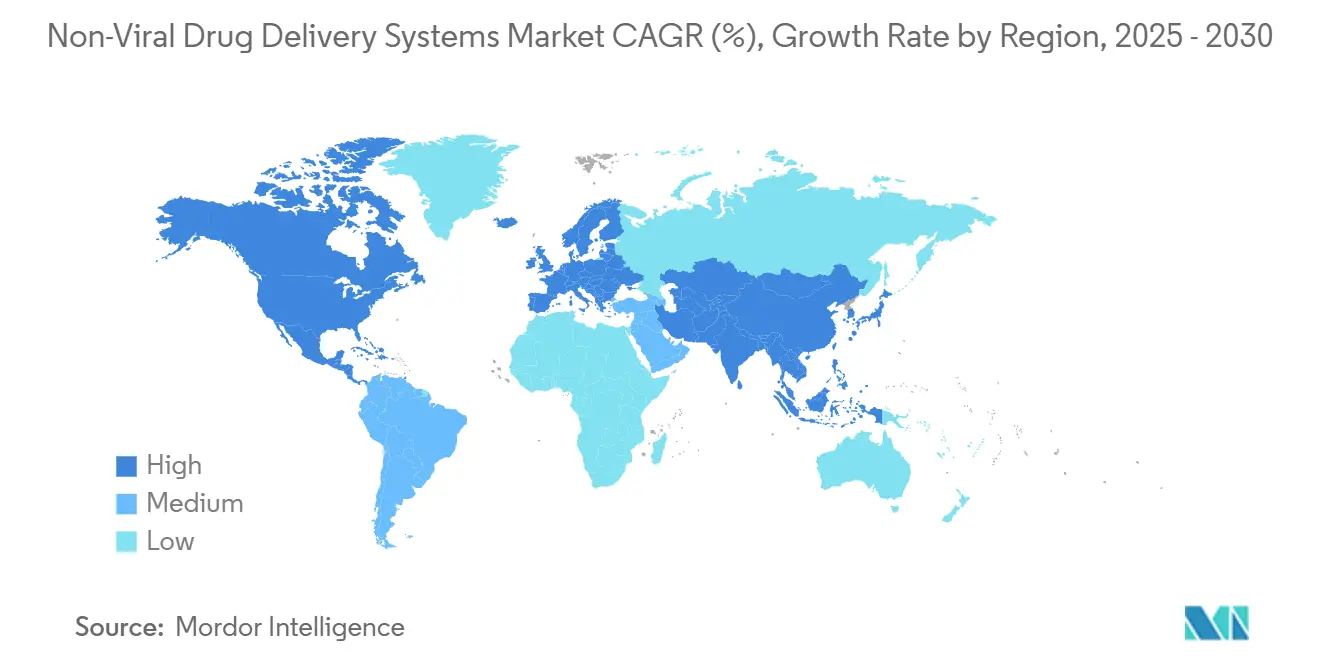

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Viral Drug Delivery Systems Market Analysis by Mordor Intelligence

The non-viral drug delivery systems market size reached USD 9.23 billion in 2025 and is projected to advance to USD 20.4 billion by 2030, expanding at a 9.7% CAGR during the forecast period. Rapid scale-up of validated lipid nanoparticle (LNP) facilities, a 50% cost-of-goods reduction achieved through microfluidic continuous manufacturing, and growing confidence in mRNA and self-amplifying RNA (saRNA) have repositioned the Non-viral drug delivery systems market from exploratory science to mainstream therapeutics. Venture funding for nanomedicine surged, exceeding USD 570 million for exosome pipelines alone in 2025, and large pharma committed multi-billion-dollar budgets to expand non-viral capacity. Regulatory fast-track programs covering oligonucleotides and LNPs shorten approval timelines, while AI-guided lipid design accelerates the discovery of novel carriers with enhanced transfection and tissue specificity. Despite these drivers, capital-intensive GMP production and unresolved questions about long-term nanoparticle biodistribution present persistent hurdles that industry stakeholders must address collaboratively.

Key Report Takeaways

- By therapeutic payload, mRNA and saRNA commanded 42.7% of the Non-viral drug delivery systems market share in 2024 and are forecast to post a 19.7% CAGR through 2030.

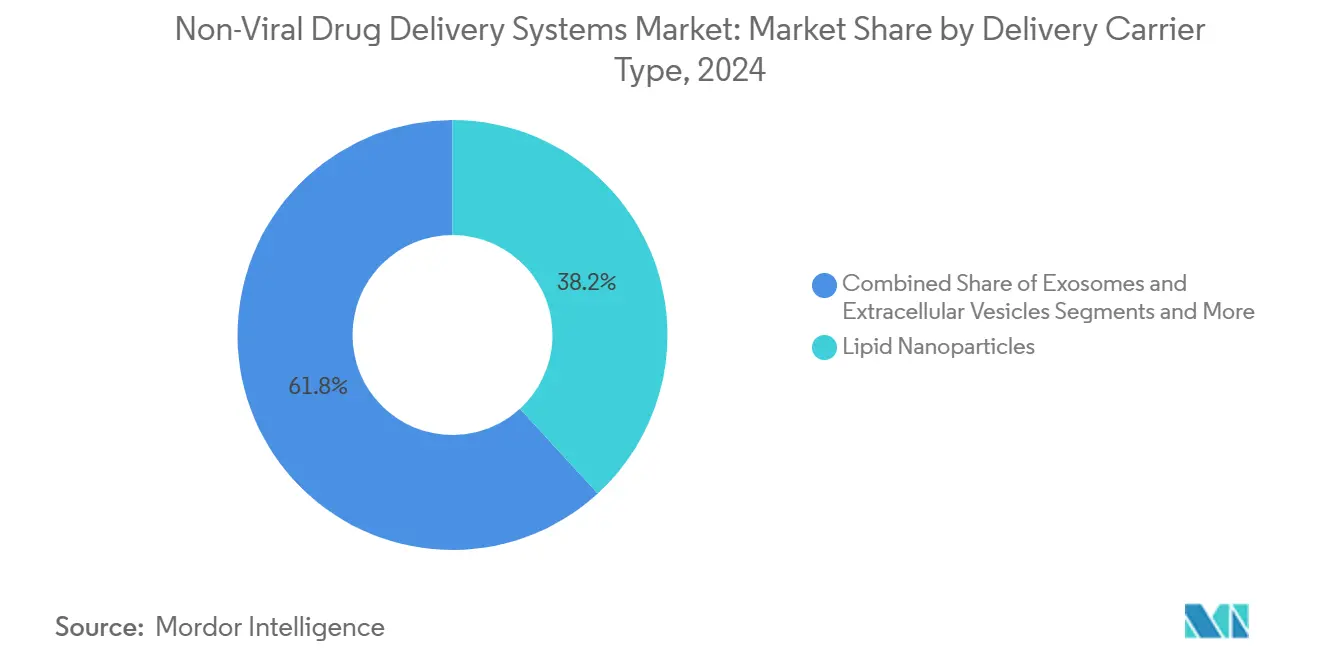

- By delivery carrier, lipid nanoparticles held 38.2% revenue in 2024, while exosomes and extracellular vesicles are set to grow at an 18.4% CAGR to 2030.

- By route of administration, intravenous solutions led with 51.9% share in 2024; intranasal formulations are advancing at a 14.2% CAGR on the back of nose-to-brain programs.

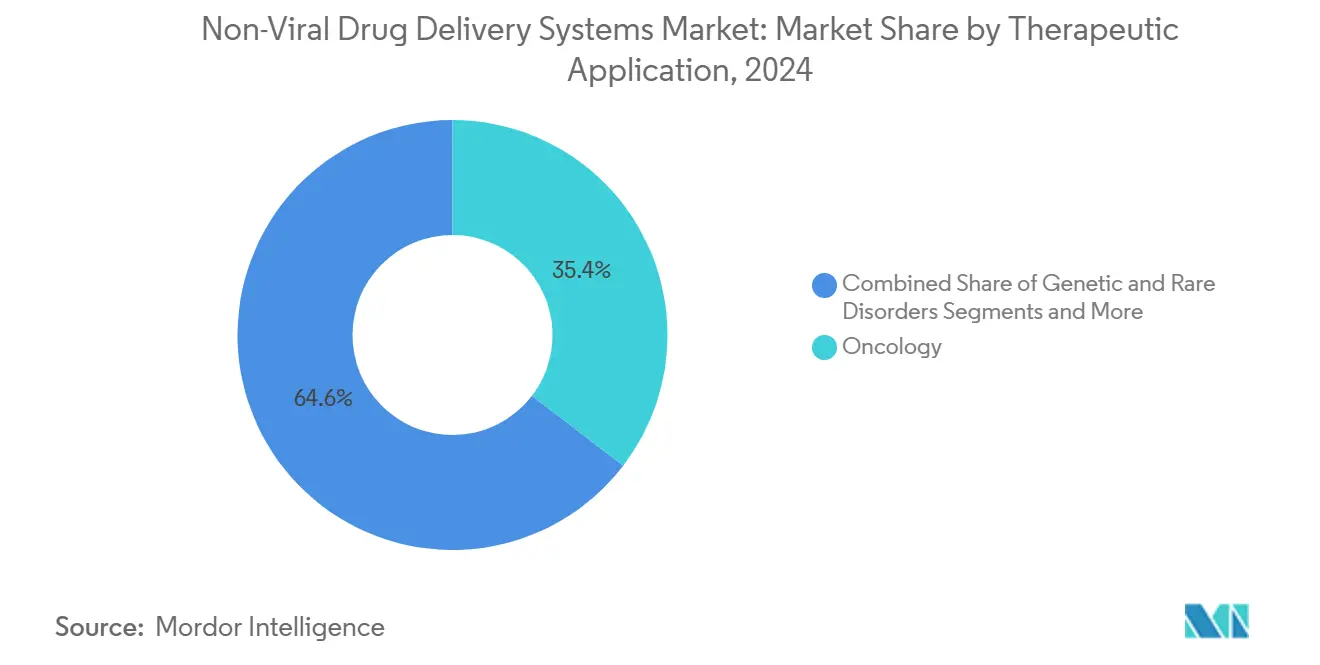

- By therapeutic application, oncology accounted for 35.4% of the Non-viral drug delivery systems market size in 2024, while genetic and rare disorders will expand at a 17.3% CAGR during the outlook period.

- By end user, pharmaceutical and biotechnology companies captured 48.1% of spending in 2024, yet CDMOs and CROs are projected to register a 12.8% CAGR as outsourcing demand rises.

- By geography, North America represented 42.7% revenue share in 2024, while the Asia Pacific is forecast to expand the fastest at 11.5% CAGR through 2030.

Global Non-Viral Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Scale-Up Of Lipid Nanoparticle (LNP) Platforms Post-mRNA-Vaccine Validation | +2.10% | Global, with North America & EU leading | Short term (≤ 2 years) |

| Surge In Funding For Nanomedicine & Gene-Editing Therapeutics | +1.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising Burden Of Hard-To-Treat Cancers Requiring Targeted Carriers | +1.50% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Regulatory Fast-Track Pathways For Non-Viral Delivery Therapeutics | +1.30% | North America & EU, with spillover to APAC | Medium term (2-4 years) |

| AI-Guided Lipid & Polymer Design Unlocking Novel Carrier Libraries | +1.20% | Global, concentrated in R&D hubs | Long term (≥ 4 years) |

| Microfluidic Continuous Manufacturing Driving Sub-50% COGS Reduction | +1.00% | Global manufacturing centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-Up of LNP Platforms Post-mRNA Validation

Mass vaccination campaigns proved that LNPs can be manufactured and distributed globally at pharmaceutical grade, prompting firms such as Moderna to allocate USD 4.5 billion to broaden non-vaccine pipelines in oncology and rare diseases.[1]BioProcess Insider, “Internal and External Investment to Grow Moderna Beyond COVID,” bioprocessintl.com Contract suppliers ramped production, with CordenPharma expanding lipid output across Switzerland, France, and Colorado to secure consistent raw-material flows. Established regulatory precedents now allow developers to leverage prior CMC packages and fast-track new LNP-based therapeutics with similar compositions. The outcome is compressed development timelines and higher confidence among investors who witnessed successful commercial deployment.

Surge in Funding for Nanomedicine & Gene-Editing Therapeutics

Venture and corporate capital poured USD 570 million into exosome programs spanning 120 active assets in 2025.[2]MENAFN Staff, “Exosome Therapeutics Market Attracts USD 570 Million Investment in 2025,” MENAFN.com, menafn.com Major alliances illustrate how that cash is deployed; Moderna paid USD 40 million upfront to Generation Bio for novel cell-targeted LNP technology that broadens tissue reach. Funding accelerates multi-asset development, mitigating single-program risk. Fast Track status granted to Arcturus’ H5N1 saRNA vaccine shows regulators are willing to expedite review when robust preclinical data support unmet needs.

Rising Burden of Hard-to-Treat Cancers Requiring Targeted Carriers

Cancer’s persistence fuels demand for carriers that navigate tumor microenvironments without provoking systemic toxicity. Recent approvals of gene therapies for ultra-rare conditions opened the door for similar platforms in oncology. Lipids designed with adjustable pKa values enhance tumor penetration and minimize off-target exposure. Concurrently, CRISPR-ready LNPs specific to solid tumors enter clinical testing, introducing precision options where viral vectors fall short.

Regulatory Fast-Track Pathways for Non-Viral Delivery Therapeutics

Dedicated FDA guidance for oligonucleotides and the Platform Designation Program supply developers with clearer roadmaps and rolling data review, compressing development cycles. The UK MHRA’s draft rules on individualized mRNA cancer vaccines reinforce global alignment

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex, Capital-Intensive GMP Production Of Nanocarriers | -1.40% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Uncertain Long-Term Toxicity & Biodistribution Profiles | -1.10% | Global, with stricter oversight in EU & US | Long term (≥ 4 years) |

| Patent Thicket On Proprietary Ionizable Lipids Restricting Freedom-To-Operate | -0.80% | Global, with concentrated impact in North America & EU | Medium term (2-4 years) |

| Environmental-Health Concerns Over Nanoparticle Waste Streams | -0.60% | EU & North America leading, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex, Capital-Intensive GMP Production of Nanocarriers

Building an LNP facility that satisfies GMP can exceed USD 100 million and demands high-precision control over lipid ratios, flow rates, and purification. Analytical instrumentation for particle characterization adds operating cost and talent shortages in emerging economies slow technology transfer.

Uncertain Long-Term Toxicity & Biodistribution Profiles

Nanoparticles interact with biological systems in complex ways. Metal-based particles can cause oxidative stress and endothelial dysfunction, underscoring the need for lifetime monitoring frameworks even for ostensibly biodegradable lipids.[3]Xianqiang Wang, “Cardiovascular Toxicity of Metal-Based Nanoparticles,” International Journal of Molecular Sciences, mdpi.com Regulatory agencies now request extended toxicology packages, particularly for pediatric and chronic indications where cumulative exposure matters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Carrier Type: Exosomes Drive Next-Generation Targeting

Lipid nanoparticles controlled 38.2% revenue in 2024, underpinned by validated large-scale manufacturing. Exosomes, however, will capture the fastest share of new dollars at 18.4% CAGR by 2030, owing to intrinsic biocompatibility and blood-brain barrier traversal. The Non-viral drug delivery systems market rewards platforms that pair scalable processes with tissue-targeting precision, and exosome engineering now benefits from improved purification and payload-loading methods.

Polymeric carriers sustain steady, application-specific adoption, especially where controlled release is paramount. Hybrid inorganic–lipid constructs such as silicon-stabilized LNPs add imaging functionality and offer modular surfaces for ligand attachment. Regulators are refining modality-tailored CMC checklists, which level the field for diversified carrier portfolios inside the broader Non-viral drug delivery systems market.

By Therapeutic Payload: mRNA Dominance Expands Beyond Vaccines

The mRNA and saRNA cluster accounted for 42.7% of 2024 revenues and will grow 19.7% annually to 2030, reinforcing its central role in the Non-viral drug delivery systems market size forecast. Platform versatility allows rapid coding of any protein, and saRNA reduces dose requirements without compromising potency.

siRNA, DNA plasmids, and CRISPR cargoes maintain double-digit momentum by addressing oncology and rare-disease indications that require permanent or highly specific edits. Lipid nanoparticle delivery of DNA-encoded biologics achieved strong in-vivo expression with favorable safety, paving the way for larger structural genes previously off-limits to viral vectors.

By Route of Administration: Intranasal Delivery Gains Momentum

Intravenous formulations held 51.9% of 2024 sales, benefiting from established dosing protocols and straightforward pharmacokinetic monitoring. Intranasal programs, however, headline growth at 14.2% CAGR, capitalizing on direct nose-to-brain pathways that sidestep first-pass metabolism and systemic dilution.

Oral and transdermal approaches progress via structural engineering that protects nucleic acids against harsh gastric or dermal environments. Patent activity around nasal spray devices confirms an innovation boom focused on neurological disorders with high unmet need. The spread of route-optimized platforms broadens the Non-viral drug delivery systems market and improves patient adherence.

By Therapeutic Application: Genetic Disorders Accelerate Translation

Oncology retained a 35.4% revenue lead in 2024, fueled by rapid uptake of tumor-targeted nanoparticle formulations designed to evade immune detection. Yet genetic and rare disorders—energized by first-in-class approvals like ELEVIDYS—are projected to expand 17.3% annually through 2030, shifting the Non-viral drug delivery systems market toward lifelong disease-modifying therapies.

Infectious diseases remain a steady contributor thanks to plug-and-play vaccine templates, while neurological and metabolic categories gather momentum as carriers capable of crossing the blood-brain barrier and targeting specific cell types advance toward late-stage trials.

By End User: CDMOs Capitalize on Manufacturing Complexity

Pharma and biotech firms generated 48.1% of 2024 revenue by driving discovery and commercialization. Contract development and manufacturing organizations recorded a 12.8% CAGR and are poised to capture a larger slice of the Non-viral drug delivery systems market as sponsors outsource lipid synthesis, nanoparticle formulation, and fill-finish services.

Examples include Vernal Biosciences’ expansion into GMP mRNA and LNP production and Evonik’s alignment with ST Pharm to offer end-to-end nucleic acid solutions. Strong compliance track records and global capacity position leading CDMOs as indispensable partners to companies lacking in-house manufacturing depth.

Geography Analysis

North America accounted for 42.7% of 2024 spending, supported by FDA guidance that clarifies oligonucleotide pharmacology and by cumulative corporate R&D outlays topping USD 4.5 billion per year. Strategic tie-ups, such as Moderna’s Generation Bio alliance, demonstrate a cluster effect in Boston and San Diego where venture networks, manufacturing facilities, and regulatory expertise co-locate.

Europe sustains a significant slice of the Non-viral drug delivery systems market thanks to harmonized EMA policies and an established supply base in Germany, Switzerland, and the United Kingdom. BioNTech’s USD 1.25 billion acquisition of CureVac consolidated intellectual property and manufacturing across the continent, aiming to unlock next-generation personalized vaccines. Partnerships between Evonik and KNAUER to refine LNP scale-up reflect Europe’s focus on advanced manufacturing and sustainability principles.

Asia-Pacific is the fastest-growing geography with an 11.5% CAGR. Japan invests in domestic mRNA facilities, exemplified by Meiji Seika Pharma’s stake in ARCALIS to strengthen local supply chains. China scales CDMO capacity for oligonucleotides, attracting global clients seeking cost-effective yet compliant manufacturing. Regional regulators increasingly align with ICH standards, reducing barriers for cross-border product registrations and enlarging the addressable Non-viral drug delivery systems market.

Competitive Landscape

The non-viral drug delivery systems market remains moderately fragmented. Top players integrate upstream lipid synthesis with downstream fill-finish to offer turnkey solutions, while mid-tier innovators focus on niche carriers or disease areas. BioNTech’s CureVac and Biotheus deals illustrate a consolidation arc aimed at unifying mRNA design, manufacturing, and clinical pipelines under one umbrella.

Intellectual-property intensity is rising: over 1,300 fusogen-powered delivery patents have been filed since 2017, creating both white-space opportunities and freedom-to-operate challenges. Partnerships between CordenPharma and Certest to co-develop ionizable lipids address patent bottlenecks while ensuring commercial supplies.

Competitive advantage now hinges on AI-enabled formulation, agile continuous manufacturing, and established regulatory rapport. Firms achieving these three pillars secure faster approvals, lower cost structures, and differentiated clinical performance, positioning them to command premium pricing and larger slices of future Non-viral drug delivery systems market growth.

Non-Viral Drug Delivery Systems Industry Leaders

Moderna Inc.

BioNTech SE

Acuitas Therapeutics

Arcturus Therapeutics

Precision NanoSystems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioNTech agreed to acquire CureVac in an all-stock deal valued at USD 1.25 billion to merge mRNA expertise for next-generation cancer vaccines.

- April 2025: BioNTech and Triastek unveiled a potential USD 1.2 billion partnership to develop 3D-printed oral RNA therapeutics.

- April 2025: The FDA granted Fast Track designation to Arcturus’ saRNA H5N1 vaccine ARCT-2304.

- January 2025: Evonik partnered with ST Pharm to co-offer nucleic acid synthesis and LNP formulation services, streamlining end-to-end RNA drug development.

Global Non-Viral Drug Delivery Systems Market Report Scope

| Lipid Nanoparticles |

| Polymeric Nanoparticles |

| Liposomes |

| Exosomes & Extracellular Vesicles |

| Inorganic / Hybrid Nanocarriers |

| mRNA & saRNA |

| siRNA / RNAi |

| DNA Plasmids & Gene-Editing Systems (CRISPR/Cas, TALEN) |

| Small-Molecule APIs |

| Proteins & Peptides |

| Intravenous |

| Intranasal |

| Oral |

| Transdermal / Topical |

| Others (Ocular, Inhalation, etc.) |

| Oncology |

| Genetic & Rare Disorders |

| Infectious Diseases |

| Neurological Disorders |

| Metabolic & Endocrine Diseases |

| Pharmaceutical & Biotechnology Companies |

| CDMOs / CROs |

| Academic & Research Institutes |

| Hospitals & Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Delivery Carrier Type | Lipid Nanoparticles | |

| Polymeric Nanoparticles | ||

| Liposomes | ||

| Exosomes & Extracellular Vesicles | ||

| Inorganic / Hybrid Nanocarriers | ||

| By Therapeutic Payload | mRNA & saRNA | |

| siRNA / RNAi | ||

| DNA Plasmids & Gene-Editing Systems (CRISPR/Cas, TALEN) | ||

| Small-Molecule APIs | ||

| Proteins & Peptides | ||

| By Route of Administration | Intravenous | |

| Intranasal | ||

| Oral | ||

| Transdermal / Topical | ||

| Others (Ocular, Inhalation, etc.) | ||

| By Therapeutic Application | Oncology | |

| Genetic & Rare Disorders | ||

| Infectious Diseases | ||

| Neurological Disorders | ||

| Metabolic & Endocrine Diseases | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| CDMOs / CROs | ||

| Academic & Research Institutes | ||

| Hospitals & Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Non-viral drug delivery systems market and its expected growth by 2030?

It stood at USD 9.23 billion in 2025 and is forecast to reach USD 20.4 billion by 2030, posting a 9.7% CAGR.

Which payload type leads revenue in Non-viral drug delivery systems?

MRNA and saRNA together held 42.7% share in 2024 and remain the fastest-growing payload class.

Why are contract manufacturers gaining share in this space?

GMP production of lipid nanoparticles is capital-intensive, prompting sponsors to outsource to CDMOs that specialize in complex formulation and regulatory compliance.

Which geographic region is expanding fastest?

Asia-Pacific, growing at an 11.5% CAGR, driven by Japanese R&D leadership and Chinese CDMO capacity.

What is the main restraint affecting long-term adoption?

Uncertainty around chronic-dose toxicity and biodistribution demands extended safety studies, slowing late-stage progression.

Page last updated on: