Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

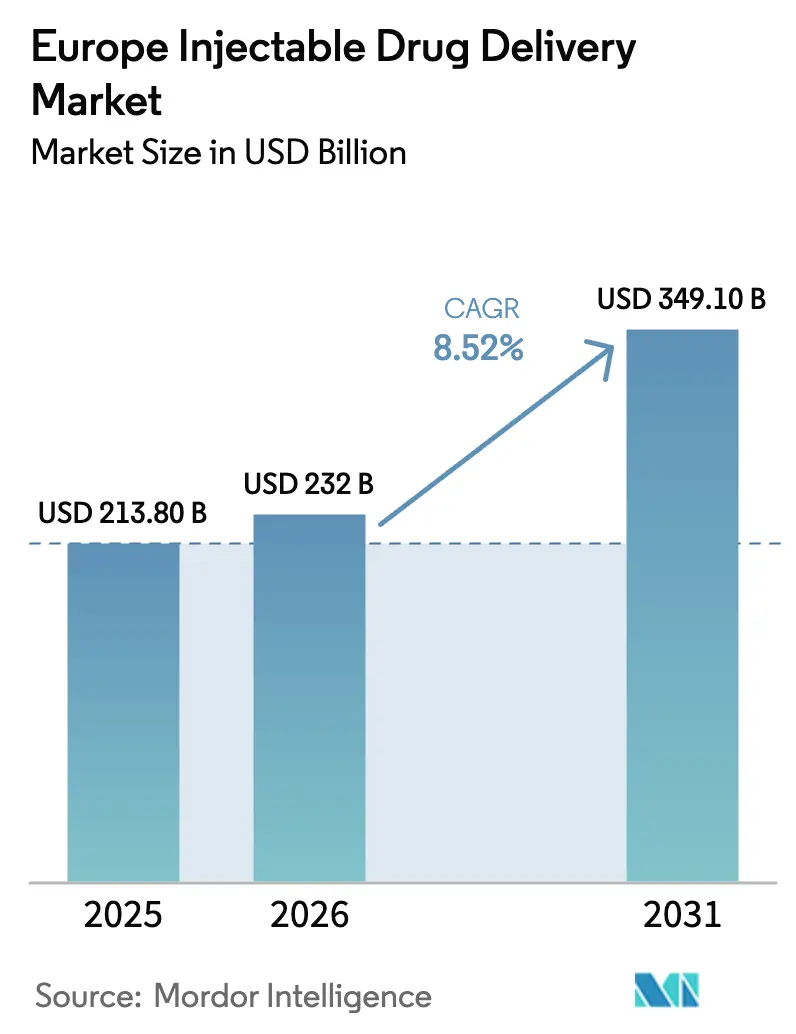

| Base Year Market Size (2025) | USD 213.80 Billion |

| Market Size (2026) | USD 232 Billion |

| Market Size (2031) | USD 349.10 Billion |

| Growth Rate (2025 - 2030) | 8.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Injectable Drug Delivery Market Analysis by Mordor Intelligence

The Europe Injectable Drug Delivery Market size was valued at USD 213.80 billion in 2025 and is estimated to grow from USD 232 billion in 2026 to reach USD 349.10 billion by 2031, at a CAGR of 8.52% during the forecast period (2026-2031).

Rising chronic-disease prevalence, a wave of biosimilar approvals, and mounting workforce shortages are moving parenteral care from hospitals into homes, accelerating the adoption of self-injectable formats and connected devices. Demographic aging amplifies demand for long-term biologic therapies, while European Union size-based recycling mandates spur material innovation in polymer syringes. Large-volume wearable injectors are replacing multihour infusions, saving infusion-suite chair time and boosting patient convenience. At the same time, non-invasive technologies such as oral GLP-1 analogs and microneedle patches signal competitive pressure on traditional needles, demanding continuous product differentiation by device makers.

Key Report Takeaways

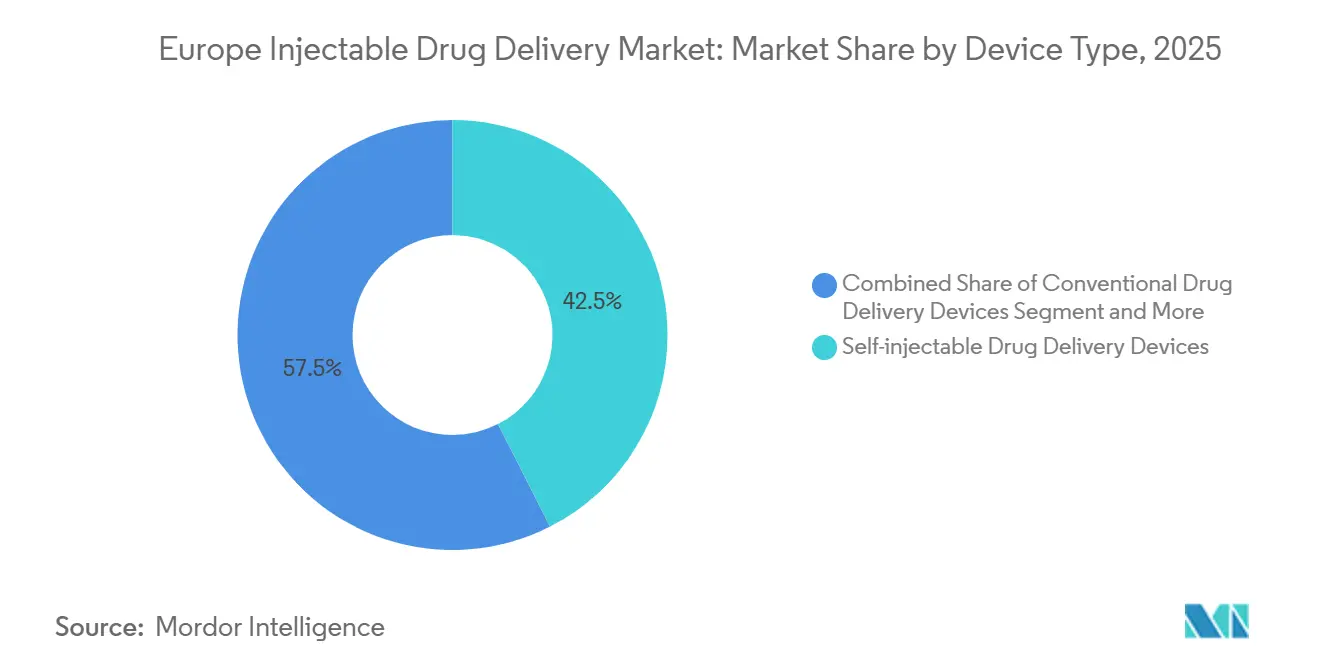

- Self-injectable devices led with 42.55% of the Europe Injectable Drug Delivery market share in 2025, while the same segment is forecast to expand at an 11.85% CAGR through 2031.

- Oncology applications are advancing at a 9.75% CAGR between 2026–2031, outpacing diabetes, which retained 38.53% of 2025 revenue.

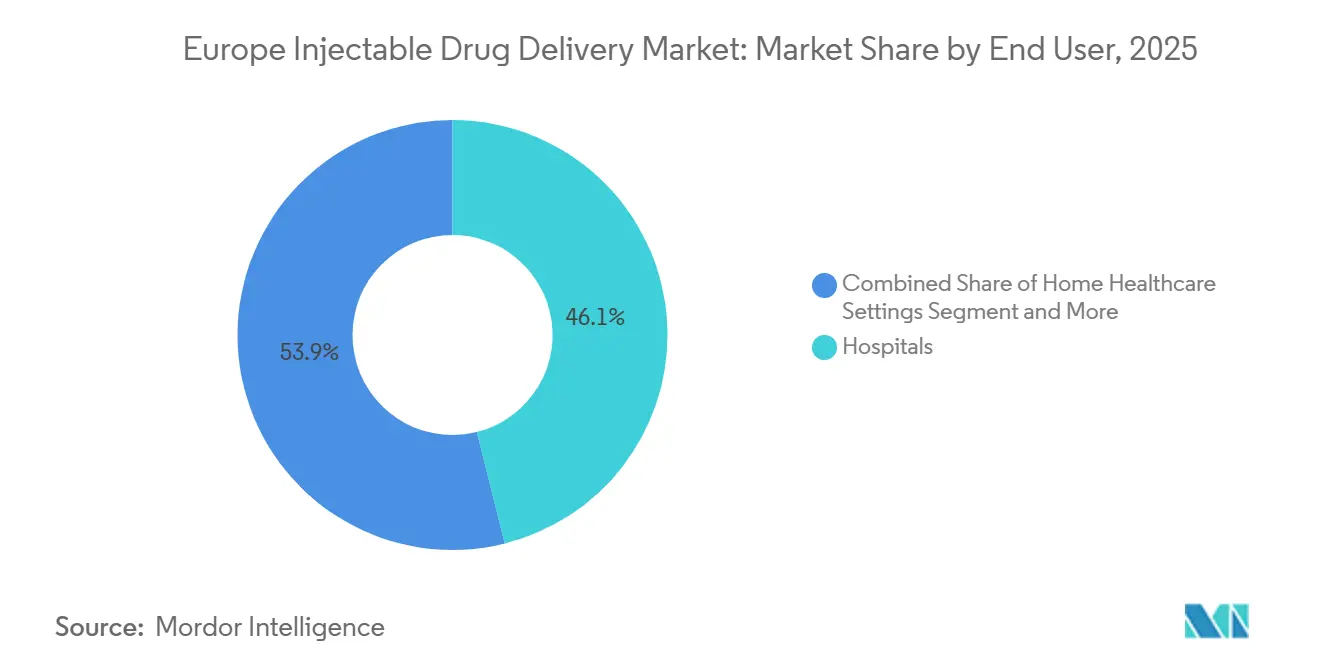

- Hospitals accounted for 46.15% of end-user revenue in 2025, but home healthcare settings represent the fastest trajectory at 11.82% CAGR.

- Borosilicate glass contributed 63.32% of raw-material revenue in 2025, whereas sustainable polymers will grow at a 9.29% CAGR to 2031.

- Germany dominated with 24.52% of regional revenue in 2025, yet Italy is projected to post the quickest geographic growth at a 9.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Injectable Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +2.1% | Pan-European, acute in Germany, France, Italy | Long term (≥ 4 years) |

| Preference for self-injectable devices | +3.2% | Northern Europe (Nordics, Benelux), expanding to Southern EU | Medium term (2–4 years) |

| Growth of biologics & biosimilars | +2.8% | Germany, France, UK, Spain | Long term (≥ 4 years) |

| Regulatory push for safety syringes | +0.9% | EU-wide (MDR/IVDR compliance zones) | Short term (≤ 2 years) |

| EU eco-design rules spurring polymer syringes | +0.7% | Germany, Netherlands, France (circular-economy leaders) | Medium term (2–4 years) |

| Integration of smart injectors with eHealth | +1.5% | Nordics, Germany, Estonia (digital-health frontrunners) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Cardiovascular disease, diabetes, and cancer together account for 60% of European mortality, creating persistent demand for injectable biologics that cannot survive gastrointestinal degradation[1]International Diabetes Federation, “IDF Diabetes Atlas,” diabetesatlas.org. Type 2 diabetes prevalence reached 9.2% among European adults in 2025, with incidence rising fastest in Eastern Europe, where preventive infrastructure lags. Oncology incidence climbed to 2.7 million new cases in 2025; subcutaneous trastuzumab and pembrolizumab now cut chair time by 75%, easing ambulatory-unit bottlenecks. Autoimmune disease burden is also climbing: biologic penetration in rheumatology surpassed 40% by 2025, buoyed by tumor-necrosis-factor and interleukin blockers in prefilled syringes. The European Commission’s 2024 Pharmaceutical Strategy harmonizes cross-border reimbursement, widening patient access to high-cost injectables.

Preference for Self-Injectable Devices

A 2024 survey of 3,200 European biologic users reported that 68% preferred self-injection over clinic visits, citing schedule flexibility and lower infection risk. Statutory insurers in Germany and the Netherlands reimburse home infusions at rates up to 40% below hospital tariffs, financially incentivizing adoption of auto-injectors and portable pumps. Ypsomed’s YpsoMate 2.5 autoinjector integrates Bluetooth sensors that transmit dose and time stamps, supporting value-based contracts that penalize non-adherence. UCB’s rozanolixizumab enables patient-controlled subcutaneous delivery for generalized myasthenia gravis, eliminating routine hospital infusions[2]European Medicines Agency, “Biosimilar Medicines: Overview,” ema.europa.eu. Compliance with ISO 11608 standards facilitates drug-device interoperability, further lowering switching costs for biosimilar substitution.

Growth of Biologics & Biosimilars

Biologics consumed 38% of European pharmaceutical spending in 2025. The EMA cleared 28 biosimilars in 2024, unlocking an estimated EUR 1.8 billion in health-system savings. Germany’s AMNOG rule caps biosimilar launch price at 85% of the reference product, yet adalimumab biosimilars reached 70% volume share within 18 months. Prefilled syringes dominate biosimilar packaging; Stevanato Group’s EZ-fill polymer platform now supplies 40% of European biosimilar fill-finish demand. High-concentration formulations above 100 mg/mL require ultra-low dead-volume syringes and viscosity-reduction excipients, intensifying collaboration between formulation scientists and device engineers. EFPIA forecasts a 6% annual rise in biologic approvals through 2030, cementing long-run demand for injectable systems.

Integration of Smart Injectors with eHealth

Connected injectors transform delivery devices into data-generating endpoints. Biocorp’s Mallya smart cap retrofits insulin pens with Bluetooth, synchronizing dosing data to diabetes-management platforms such as MySugr and Glooko. Denmark’s national eHealth portal mandates interoperability between medical devices and electronic records, allowing clinicians to monitor adherence in real time. SHL Medical’s Molly 2.5 wearable injector embeds near-field communication tags so oncology nurses can scan devices directly into electronic logs, minimizing transcription errors. Under the EU Medical Device Regulation, Unique Device Identification codes became compulsory in May 2025, aiding post-market surveillance and outcome-based reimbursement. Cybersecurity remains a concern; ENISA flagged multiple vulnerabilities in connected pumps in 2024, prompting ISO 81001 compliance audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to non-invasive delivery routes | -1.8% | Germany, UK, Nordics (oral GLP-1 uptake) | Medium term (2–4 years) |

| EMA combination-product hurdles & cost | -1.3% | EU-wide (MDR/pharmaceutical dual compliance) | Short term (≤ 2 years) |

| EU 'pharma-in-water' producer liability | -0.6% | Rhine basin countries (Germany, Netherlands, France) | Long term (≥ 4 years) |

| Shortages of borosilicate glass/resins | -0.9% | Pan-European supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift to Non-Invasive Delivery Routes

Oral, transdermal, and inhaled formulations are eating into injectable volumes in segments where adequate bioavailability has been achieved. Novo Nordisk’s oral semaglutide captured 15% of German GLP-1 prescriptions by late 2025, despite lower bioavailability, reflecting strong needle aversion among patients. Transdermal microneedle patches from 3M entered Phase III insulin trials in 2025 and deliver 85% bioequivalence relative to subcutaneous injection, while eliminating sharps waste. Inhaled insulin (Afrezza) regained EU authorization in 2024 and targets the 12% of type 1 diabetics unwilling to inject. Transmucosal opioid films are now preferred in palliative care, further curbing demand for injectable opioids. The restraint is most pronounced in pediatric and geriatric cohorts, where injection anxiety and manual-dexterity issues are common.

EMA Combination-Product Hurdles & Cost

Devices that deliver medicinal products must satisfy both Medical Device Regulation and pharmaceutical dossiers, stretching approval cycles and inflating regulatory fees. Industry surveys placed average EU combination-product review time at 22 months, eight months longer than pure devices, with direct submission costs topping EUR 500,000. Small manufacturers struggle to fund parallel notified-body and EMA reviews, reinforcing the advantage of vertically integrated incumbents. Post-market obligations also intensify; MDR Article 83 requires periodic safety reports linking device performance to drug stability in real time. The European Commission’s 2025 “single-portal” proposal seeks to streamline dual submissions but will not materialize before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Self-Injectables Command Innovation Pipeline

Self-injectable devices generated 42.55% of 2025 revenue and are on track to expand at an 11.85% CAGR through 2031, outpacing all other formats within the Europe Injectable Drug Delivery market[3]Stevanato Group, “Investor Presentation 2025,” stevanatogroup.com. Prefilled syringe demand is anchored by Stevanato Group’s EZ-fill polymer barrels that curb protein aggregation, supporting high-concentration biologics above 150 mg/mL. Auto-injectors such as YpsoMate 2.5 embed Bluetooth sensors for dose confirmation, opening the door to adherence-linked reimbursement models. Wearable injectors are disrupting infusion paradigms; BD’s Libertas can deliver 5 mL subcutaneously in 30 minutes, displacing multihour intravenous infusions for immunoglobulins. Needle-free jet injectors remain niche due to patient discomfort, yet PharmaJet’s Tropis system gained EMA clearance for intradermal vaccines, a sign of gradual acceptance.

Smart connected injectors are the fastest-moving subsegment of the Europe Injectable Drug Delivery market. Biocorp’s Mallya adapts legacy insulin pens for real-time data capture, an affordable retrofit sought by cost-conscious payers in Eastern Europe. Conventional glass syringes, vials, and ampoules still meet hospital demands where multi-dose vials lower per-unit antibiotic costs. Implantable pumps, such as Medtronic’s SynchroMed II, maintain niche roles in refractory pain management. Subcutaneous home-infusion pumps like Baxter’s Homepump Eclipse reduce cystic-fibrosis readmissions by 40% in UK pilots. Microneedle patches, currently in late-stage insulin trials, hold future promise for needle-phobic populations.

By Therapeutic Application: Oncology Overtakes Diabetes in Growth Velocity

Oncology applications are poised to advance at a 9.75% CAGR between 2026–2031, the fastest of any indication tracked within the Europe Injectable Drug Delivery industry. Subcutaneous pembrolizumab, approved in 2024, administers 600 mg in only five minutes, cutting infusion-suite utilization and freeing thousands of chair-hours annually. Trastuzumab biosimilars now command 62% share of HER2-positive breast-cancer starts in Germany, illustrating payer appetite for cost-saving injectables. Diabetes held 38.53% of 2025 revenue; however, oral semaglutide’s rise limits incremental injection growth. Autoimmune disorders such as rheumatoid arthritis and Crohn’s disease are robust, supported by quarterly wearable-injector formulations that simplify dosing schedules.

Cardiovascular injectables, led by Amgen’s evolocumab prefilled pen, hold steady as guideline updates broaden PCSK9 inhibitor usage for high-risk LDL profiles. Hepatitis injectables are waning as direct-acting antivirals migrate to oral formats. Pain-management injections face tighter opioid controls, while vaccine volumes normalize post-COVID-19. Fertility hormones and growth factors sustain stable demand as subcutaneous methotrexate transitions to autoinjectors in Nordic markets.

By End User: Home Healthcare Disrupts Hospital Dominance

Hospitals delivered 46.15% of 2025 sales, preserving critical roles in acute oncology, surgical anesthesia, and emergency cardiology. Yet the Europe Injectable Drug Delivery market size tied to home healthcare is projected to expand at an 11.82% CAGR through 2031, propelled by a forecast 1.2 million clinician shortfall by 2030. Germany’s statutory insurers raised home-biologic tariffs by 18% in 2025, equalizing profitability with hospital day-case reimbursements. Baxter’s Homepump Eclipse enables antibiotic therapy at home, trimming UK readmissions by 40% and validating outpatient infusion models. Specialty clinics remain important channels for rheumatology and dermatology, while ambulatory-surgery centers gain share as France pushes 70% outpatient eligibility by 2027.

Online pharmacies currently hold marginal injectable volumes due to cold-chain and prescription rules, yet Amazon Pharmacy’s 2024 entry into Germany hints at future e-commerce expansion. Home-based care sees the fastest equipment turnover, favoring connected auto-injectors that provide pharmacists with adherence data. The Europe Injectable Drug Delivery market share held by ambulatory settings is expected to grow as payer contracts reward providers for keeping patients out of inpatient settings.

By Raw Material: Sustainable Polymers Challenge Glass Hegemony

Borosilicate glass represented 63.32% of 2025 raw-material revenue, underpinned by Type I glass’s chemical inertness and legacy regulatory validation. Nevertheless, sustainable polymers—chiefly cyclic olefin copolymers—are forecast to rise at a 9.29% CAGR through 2031, buoyed by EU recycling quotas of 70% by 2030. Stevanato’s EZ-fill polymer syringes already account for 40% of European biosimilar fill-finish output. West Pharmaceutical’s NovaPure fluoropolymer-coated plungers curtail tungsten and silicone contamination, commanding premiums in high-concentration biologics. Biodegradable polymers remain experimental because degradation-rate variability clouds MDR biocompatibility compliance.

SCHOTT and Nipro have redirected capacity toward high-margin pharmaceutical tubing, creating sporadic glass shortages. The new Ecodesign for Sustainable Products Regulation mandates digital product passports disclosing material composition, raising compliance costs for multi-material injectors by roughly EUR 0.12 per unit. Stainless-steel components endure in reusable autoinjector shells, where 316L alloy’s corrosion resistance delivers long service life.

Geography Analysis

Germany generated 24.52% of regional revenue in 2025 as AMNOG pricing and pharmacist-substitution mandates accelerated biosimilar uptake. Gerresheimer’s Bünde facility boosted ready-to-fill syringe capacity by 30% in 2024, accommodating escalating fill-finish demand. The United Kingdom faces National Health Service budget strain, yet a 2025 home-infusion pilot for immunoglobulins cut admissions by 35%, foreshadowing a policy pivot toward outpatient delivery. France’s ambulatory-surgery plan, aimed at 70% outpatient eligibility, lifts demand for single-dose prefilled analgesics.

Italy is expected to log the fastest growth, at a 9.32% CAGR from 2026–2031, as AIFA imposes regional biosimilar quotas that close utilization gaps between southern and northern regions. Spain supports wearable injectors for hemophilia factor concentrates, halving infusion-center visits during Catalonia’s pilot. The remaining Europe Injectable Drug Delivery market territory—Nordics, Benelux, Poland, and Eastern Europe—benefits from EU Cohesion Fund allocations that underwrite diabetes-supply chains in underserved areas.

Nordic countries pioneer digital integration. Denmark’s sundhed.dk requires injector data interoperability with electronic records, and Estonia’s e-Prescription platform captures 99% of outpatient prescriptions, seamlessly populating national datasets. Belgium lifted home-biologic tariffs by 22% in 2025 to match hospital economics. The Netherlands ties wearable-injector reimbursement to patient-reported outcomes via value-based contracts, motivating device makers to embed sensors for real-time adherence tracking.

Competitive Landscape

The Europe Injectable Drug Delivery market remains moderately consolidated: the top suppliers—Gerresheimer, Eli Lilly and Company, Teva Pharmaceutical Industries Ltd, and others—control a sizable slice of device revenue via vertical integration. Becton Dickinson’s Libertas wearable platform leverages its syringe base to cut partner time-to-market by up to 18 months. Novo Holdings’ USD 16.5 billion acquisition of Catalent in 2024 gives Novo Nordisk internal fill-finish capacity while expanding third-party CDMO services. Ypsomed filed 14 European patents in 2024 for connectivity modules, revealing a focus on value-based reimbursement opportunities.

Large-volume subcutaneous delivery is the key white-space battleground. Enable Injections’ enFuse and SHL Medical’s Molly 2.5 vie to displace intravenous immunoglobulin infusions in hospitals facing chair shortages. Biocorp’s Mallya smart cap retails at one-tenth the price of integrated smart injectors, appealing to payers in cost-sensitive Eastern Europe. Competitive differentiation is shifting from mechanical precision to extractables and leachables performance; West Pharmaceutical’s NovaPure components eliminate tungsten residues, commanding 25% price premiums in high-protein formulations. Regulatory streamlining under the proposed single-portal submission could lower entry barriers for mid-sized innovators, yet full implementation remains years away.

Europe Injectable Drug Delivery Industry Leaders

Baxter

Gerresheimer AG

Teva Pharmaceutical Industries Ltd

Eli Lilly and Company

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sharp increased European injectable assembly and secondary-packaging capacity to meet rising demand for prefilled syringes and autoinjectors.

- October 2025: SCHOTT Pharma launched a 5.5 mL staked-needle glass syringe within its syriQ BioPure line, enabling large-volume home administration for biologics.

Europe Injectable Drug Delivery Market Report Scope

As per the scope of the report, injectable drug delivery devices are specialized tools for the delivery of a drug or therapeutic agent via a parenteral route of administration.

The Europe injectable drug delivery market is segmented by device type, therapeutic application, end user, raw material, and country. By device type, the market includes conventional drug delivery devices, self-injectable drug delivery devices, prefilled syringes, injection pens, auto-injectors, needle-free injectors, wearable injectors, smart connected injectors, implantable drug delivery devices, infusion pumps (sub-Q), and microneedle systems. By therapeutic application, the market covers cardiovascular disease, diabetes, oncology, autoimmune disorders, hepatitis, pain management, infectious diseases and vaccines, and others. By end user, the market is segmented into hospitals, specialty clinics, home healthcare settings, ambulatory surgery centers, and online pharmacies. By raw material, the segmentation includes borosilicate glass, plastics (COP/COC, PP, PC), and sustainable/biodegradable polymers. By country, the market is divided into Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. The report offers the value (in USD) for the above segments.

By Device Type

| Conventional Drug Delivery Devices | |

| Self-injectable Drug Delivery Devices | Prefilled Syringes |

| Injection Pens | |

| Auto-injectors | |

| Needle-free Injectors | |

| Wearable Injectors | |

| Smart Connected Injectors | |

| Implantable Drug Delivery Devices | |

| Infusion Pumps (Sub-Q) | |

| Microneedle Systems |

By Therapeutic Application

| Cardiovascular Disease |

| Diabetes |

| Oncology |

| Autoimmune Disorders |

| Hepatitis |

| Pain Management |

| Infectious Diseases & Vaccines |

| Others |

By End User

| Hospitals |

| Specialty Clinics |

| Home Healthcare Settings |

| Ambulatory Surgery Centers |

| Online Pharmacies |

By Raw Material

| Borosilicate Glass |

| Plastics (COP/COC, PP, PC) |

| Sustainable/Biodegradable Polymers |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Device Type | Conventional Drug Delivery Devices | |

| Self-injectable Drug Delivery Devices | Prefilled Syringes | |

| Injection Pens | ||

| Auto-injectors | ||

| Needle-free Injectors | ||

| Wearable Injectors | ||

| Smart Connected Injectors | ||

| Implantable Drug Delivery Devices | ||

| Infusion Pumps (Sub-Q) | ||

| Microneedle Systems | ||

| By Therapeutic Application | Cardiovascular Disease | |

| Diabetes | ||

| Oncology | ||

| Autoimmune Disorders | ||

| Hepatitis | ||

| Pain Management | ||

| Infectious Diseases & Vaccines | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home Healthcare Settings | ||

| Ambulatory Surgery Centers | ||

| Online Pharmacies | ||

| By Raw Material | Borosilicate Glass | |

| Plastics (COP/COC, PP, PC) | ||

| Sustainable/Biodegradable Polymers | ||

| Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe Injectable Drug Delivery market?

The Europe Injectable Drug Delivery market size reached USD 232.0 billion in 2026 and is set to climb toward USD 349.1 billion by 2031.

How fast is the market growing?

From 2026 to 2031 the market is projected to grow at an 8.52% CAGR, powered by self-injectables, biosimilar uptake, and home-care models.

Which device category is expanding the quickest?

Self-injectable platforms, including wearable on-body pumps, are advancing at an 11.85% CAGR as patients and payers prefer home administration.

Which therapeutic area shows the highest growth momentum?

Oncology leads with a 9.75% CAGR, thanks to subcutaneous checkpoint inhibitors and antibody-drug conjugates.

Which country will register the fastest revenue growth?

Italy is expected to deliver a 9.32% CAGR through 2031 as regional biosimilar quotas broaden biologic access in the south.

What material trends are shaping future device design?

Sustainable cyclic olefin polymers are the fastest-growing raw material, driven by EU recycling mandates and superior protein-stability profiles.

Page last updated on: