Sustainable Pharmaceutical Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

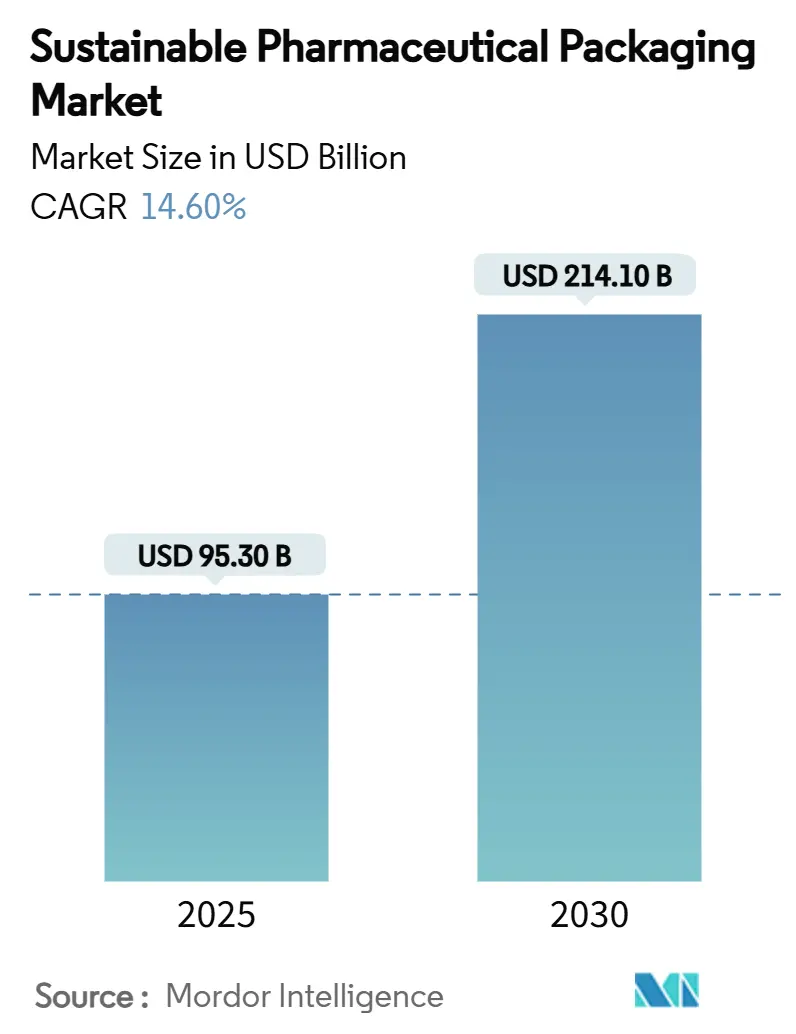

| Market Size (2025) | USD 95.30 Billion |

| Market Size (2030) | USD 214.10 Billion |

| Growth Rate (2025 - 2030) | 14.60% CAGR |

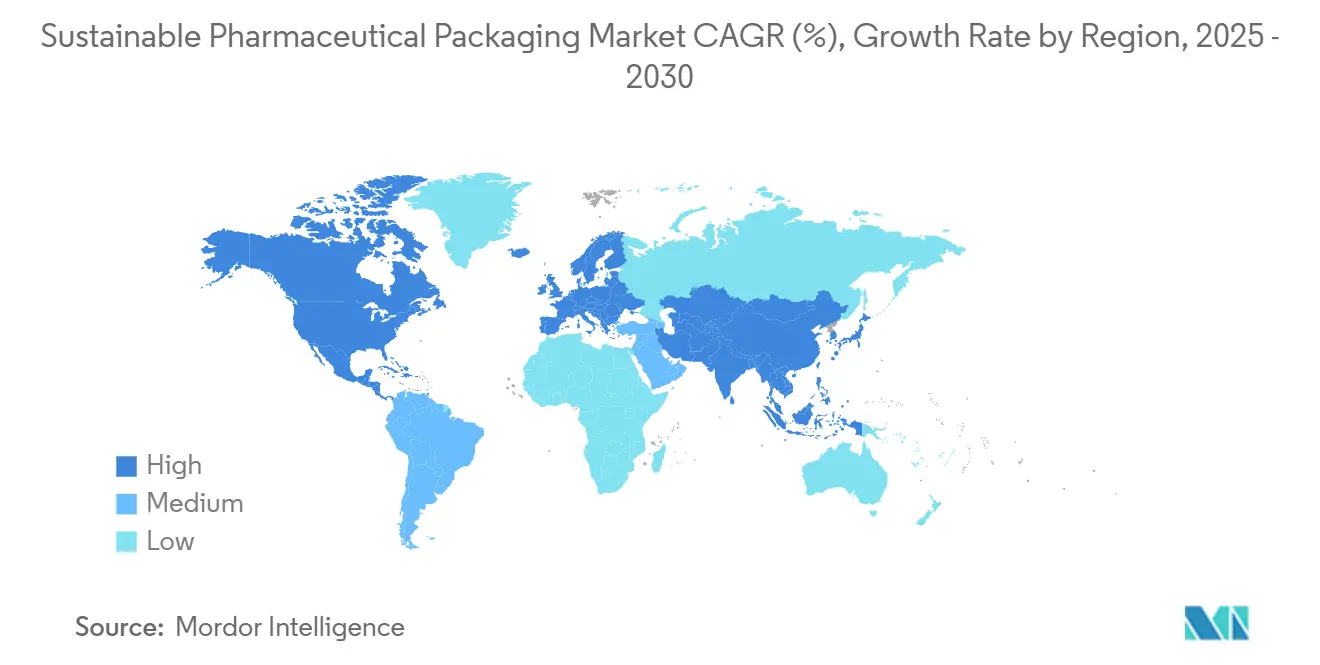

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sustainable Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The sustainable pharmaceutical packaging market size is expected to reach USD 95.3 billion in 2025, and it is forecast to reach USD 214.1 billion in 2030 while expanding at a 14.60% CAGR. Heightened Extended Producer Responsibility rules in Europe, the United Kingdom, and several U.S. states create immediate cost incentives for recyclable and low-carbon designs, which accelerate corporate investment in new materials and manufacturing systems. North America retains leadership through 2024 thanks to mature collection infrastructure and early circular-economy pilots, while Asia Pacific advances fastest as governments align export requirements with global sustainability standards. Packaging producers prioritize material lightweighting and post-consumer resin adoption to cut freight emissions and meet recycled-content quotas. AI-enabled design tools further trim material use without sacrificing integrity. Competitive intensity revolves around technological differentiation because regulatory compliance costs favor firms that can certify barrier performance and traceability at scale, limiting price-based rivalry and raising entry barriers.

Key Report Takeaways

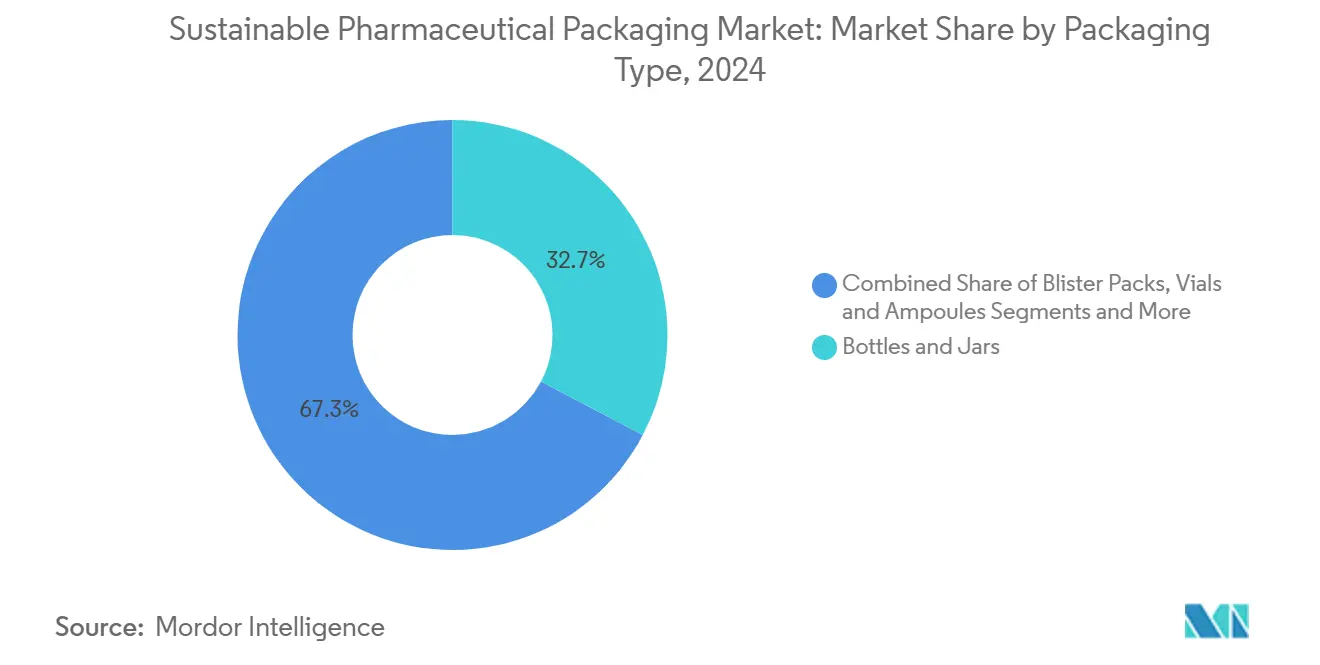

- By packaging type, bottles and jars held 32.7% of the sustainable pharmaceutical packaging market share in 2024, while pre-filled syringes and cartridges recorded the fastest 13.80% CAGR through 2030.

- By material type, conventional plastics led with a 45.2% share in 2024, whereas bioplastics and plant-based polymers are projected to grow at a 14.50% CAGR to 2030.

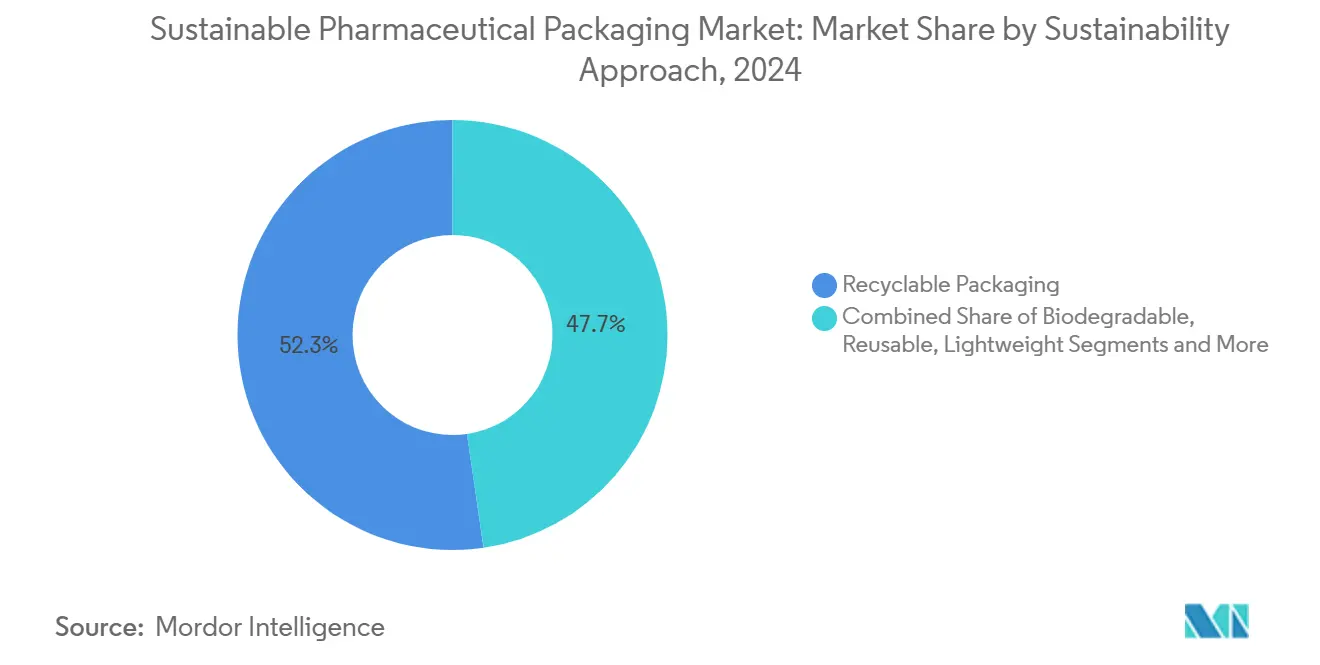

- By a sustainability approach, recyclable systems commanded 52.3% of the sustainable pharmaceutical packaging market size in 2024, and biodegradable or compostable formats will expand at 14.20% CAGR between 2025 and 2030.

- By drug form, solid dosage products accounted for 60.1% share in 2024, whereas parenteral packaging shows the highest 12.40% CAGR to 2030.

- By end user, pharmaceutical manufacturers controlled 68.8% share in 2024, while contract packaging organizations post the strongest 11.10% CAGR through 2030.

- North America captured 38.1% of the sustainable pharmaceutical packaging market size in 2024, whereas Asia Pacific accelerates at 15.80% CAGR toward 2030.

Global Sustainable Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EPR & recyclability mandates | +4.20% | Global, early focus in EU, UK, select U.S. states | Short term (≤ 2 years) |

| Rising eco-conscious buyer preference | +3.10% | North America and EU core, expanding to urban Asia Pacific | Medium term (2–4 years) |

| Cost optimization via lightweighting | +2.80% | Global manufacturing hubs, notably Asia Pacific | Medium term (2–4 years) |

| Pharma-sector net-zero pledges | +2.30% | Global, led by multinationals | Long term (≥ 4 years) |

| AI-driven cold-chain design optimization | +1.40% | North America and EU with spillover to developed Asia Pacific | Medium term (2–4 years) |

| Personalized-medicine micro-packaging | +0.80% | North America and EU, selective use in Japan and Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EPR & Recyclability Mandates

Extended Producer Responsibility requirements move waste-management costs onto packaging owners, prompting immediate redesign of primary containers and secondary cartons to eliminate hard-to-recycle polymers. The European Union mandates 30% recycled content for PET medicinal packaging by 2030 and bans PFAS in contact materials starting August 2026. Colorado and Oregon introduced parallel rules in July 2025, and the United Kingdom replaced its 2007 framework with stricter recycling targets that align with continental standards. Because compliance dates cluster within a two-year window, manufacturers can amortize tooling upgrades across multiple sales regions, which accelerates capital budgets for plant retrofits and post-consumer resin qualification. Demand for certified pharma-grade recyclate therefore outpaces short-term supply, resulting in strategic offtake agreements between drug makers and recyclers. Packaging suppliers that can validate traceability and purity gain first-mover pricing power while establishing templates for global rollouts in Asia and Latin America.

Rising Eco-Conscious Buyer Preference

Consumer surveys show 46% of respondents purposefully buy sustainable healthcare products, and 85% feel direct climate-change impacts in their daily lives. Hospitals and group purchasing organizations amplify this trend by adding carbon-footprint weighting to tender evaluations, which rewards drug brands with measurable environmental labels. Sanofi commits to producing only eco-designed launches after 2025, and its syringe vaccine program shifts toward blister-free corrugated trays to reduce landfill waste. Sustainability certification, therefore, becomes a proxy for brand equity as well as for institutional approval, encouraging sector-wide adoption of Life-Cycle-Assessment disclosure. The emphasis on environmental credibility helps premium formats command higher margins, offsetting incremental costs of bio-based resins and multilayer film separation technology. Growth momentum is strongest in North America and Western Europe. Yet, multinational retail pharmacies in Shanghai and Mumbai start listing carbon ratings on online product pages, which accelerates awareness across high-growth Asia Pacific metros.

Cost Optimization Via Lightweighting

Material-reduction initiatives decrease resin volumes by as much as 10% while maintaining functional performance through finite-element analysis and machine-learning shape optimization. Amazon’s algorithmic packaging cuts damage claims 24% and lowers freight cost 5%, demonstrating transferable benefits to pharmaceutical distribution where temperature-controlled payload weight drives fuel usage. Berry Global’s ClariPPil jar shows 71% lower cradle-to-gate CO₂ emissions than a legacy PET bottle while remaining fully recyclable. Such examples prove that sustainability can produce immediate operational savings rather than deferred compliance costs, making board-level approval easier in both branded and generic segments. Asia Pacific contract fillers embrace lightweighting because reduced material flow lowers import duties on primary containers and trims reverse-logistics fees for extended producer obligations, reinforcing growth for the sustainable pharmaceutical packaging market.

Pharma-Sector Net-Zero Pledges

Life-science greenhouse-gas emissions surpass the automotive sector by 55%, prompting executive boards to set aggressive Scope 3 targets that explicitly include packaging. AstraZeneca plans near-zero value-chain emissions by 2040, and Merck advances similar milestones for 2035, forcing suppliers to validate carbon intensity down to raw-material sourcing. Astellas launches a plant-origin blister pack that shrinks carbon footprint 40-60%, signaling mainstream acceptance of bio-composite laminates.[1]Katrina Megget, “Green Pharma,” Chemistry and Industry, soci.org These pledges guarantee multi-year demand visibility for recyclable and bio-based formats, encouraging capital investment in fermentation-based monomer capacity and microwave recycling plants. Financial markets reward such moves, as sustainable-bond issuance tied to packaging milestones lowers weighted average capital cost for compliant producers. The cumulative effect underpins long-cycle growth for the sustainable pharmaceutical packaging market beyond policy mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of green materials | -2.90% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Barrier-property performance gaps | -1.80% | Global, especially for moisture-sensitive formulations | Medium term (2–4 years) |

| Scarce pharma-grade recycled feedstock | -1.40% | North America and EU supply chains | Short term (≤ 2 years) |

| Composting-logistics carbon overhead | -0.70% | Regions with limited composting infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing of Green Materials

Bio-based resins often cost 20-50% more than fossil-derived plastics due to limited industrial scale and specialized processing requirements. Even when buyers accept higher input costs to secure allocations, volatility in feedstock supply exacerbates planning uncertainty in emerging markets where reimbursement margins are narrow. The U.S. federal plan to shift 90% of plastics to bio-based feedstock over two decades signals greater capacity intent but also highlights the magnitude of capital required to reach price parity. Pharmaceutical exporters into Africa and South-East Asia, where health-system budgets are constrained, thus face short-term cost hurdles that temper immediate adoption of premium sustainable formats.

Barrier-Property Performance Gaps

Active pharmaceutical ingredients often demand stringent moisture and oxygen protection that many early-generation biodegradable materials failed to meet. Hyperthermal hydrogen-induced cross-linking now lowers PLA oxygen transmission 99.7% and cuts water vapor passage 50.7%, narrowing the gap with high-density polyethylene.[2]Run Xu, “Improving the Oxygen and Water Vapour Barrier Properties of PLA via a Novel Interface Engineering,” npj Science of Food, nature.com Boric-acid-crosslinked poly(vinyl alcohol) coatings also enhance barrier reliability while retaining compostability. Yet full pharmacopoeia validation and regulatory filings lengthen commercialization timelines, keeping some moisture-sensitive drugs in glass or multilayer foil packaging. The temporary mismatch slows overall substitution, especially where shelf-life guarantees underpin global distribution contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Pre-filled Systems Drive Innovation

Pre-filled syringes and cartridges represent the fastest-growing segment with a 13.80% CAGR to 2030, buoyed by rising biologic therapies and self-administration trends that intensified during the COVID-19 era. Enhanced traceability through embedded RFID and design optimizations that minimize overfill, reduce product loss and medical errors, and improve value propositions for payers and providers. Bottles and jars continue to dominate, capturing 32.7% of the sustainable pharmaceutical packaging market share in 2024, predominantly serving solid oral doses and over-the-counter liquids. Vials and ampoules remain vital for vaccine campaigns and oncology injectables, and sachets or pouches address patient convenience in single-dose rehydration salts across low-income regions. The segment shows convergence as brands test bio-sourced HDPE bottles and wood-plastic hybrids that integrate with existing filling lines. Sustainable pharmaceutical packaging market size expansion, therefore, stems from both advanced-delivery adoption and retrofit innovation in legacy formats.

The sustainable pharmaceutical packaging market sees heightened R&D toward modular blister designs that reduce PVC use and enable mono-material recycling streams. Machinery suppliers advertise tool inserts that switch between blister and pouch lines within hours, shortening changeover and conserving energy. Contract fillers in Europe invest in robotic pick-and-place units capable of handling fragile glass vials with lower breakage rates, aligning efficiency savings with carbon-reduction targets. As industry volume migrates to higher potency drugs, contamination control demands escalate, favoring pre-sterilized nested formats over bulk fill-finish glass. This dynamic sustains premium pricing potential for advanced primary containers while encouraging continuous improvement of mainstream bottle and jar designs within the sustainable pharmaceutical packaging market.

By Material Type: Bioplastics Breakthrough Accelerates

Bioplastics and plant-based polymers grow fastest at 14.50% CAGR, driven by PHA and seaweed-derived feedstocks that degrade in home-compost settings within four weeks.[3]Claire Turrell, “Ocean-Grown Bioplastics,” Nature Biotechnology, nature.com Conventional plastics retain a 45.2% share in 2024 because of their proven performance and well-established pharmaceutical validation protocols. Glass, prized for chemical inertness and high barrier properties, remains indispensable for biologics and vaccine fill-finish, though lightweight borosilicate and aluminosilicate chemistries reduce energy needs during production. Paperboard replaces plastic clamshells for secondary packaging, and aluminum foils guard moisture-sensitive actives within blister units. Sustainable pharmaceutical packaging market size for bioplastic bottles continues to climb as companies like TotalEnergies Corbion adapt Luminy PLA grades that withstand autoclave sterilization, expanding end-use suitability beyond food-service domains.

Supply chains evolve as chemical recycling startups convert mixed polyolefin waste into naphtha-like feedstock suitable for pharma-grade resin cracking, narrowing purity gaps. Glass suppliers integrate oxy-fuel furnaces that cut energy consumption and CO₂ by up to 40%, thereby reinforcing the material’s eco-credentials amid weight concerns. Converters experiment with silicate barrier layers applied via plasma to bio-polymer bottles, enhancing oxygen resistance without compromising compostability. Investors increasingly fund regional pelletizing lines near pharma clusters to secure stable feedstock, improving cost structures and resilience, and strengthening bioplastic adoption trajectories in the sustainable pharmaceutical packaging market.

By Sustainability Approach: Recyclable Systems Dominate

Recyclable packaging commands a 52.3% share in 2024 because existing collection and reprocessing networks support rapid deployment. Closed-loop pilots such as the SCHOTT Pharma–Corplex–Takeda tray recovery project prove a 50% greenhouse-gas reduction against virgin benchmarks. Compostable and biodegradable formats rise at 14.20% CAGR as performance gaps close, especially with cross-linked PVA coatings that uphold moisture-barrier demands. Reusable shipping containers for temperature-controlled payloads gain traction for specialty biologics, expanding from 30% to 70% penetration in CEVA Logistics’ fleet by 2030. Lightweighting remains an evergreen tactic, with AI-powered structural analysis simplifying design iterations that conserve polymer mass.

Renewable-energy sourcing becomes a key differentiator as plants integrate rooftop solar arrays and commit to 100% renewable electricity, effectively embedding Scope 2 reductions into product carbon declarations. The multipronged nature of sustainability strategies allows producers to layer approaches, such as lightweight recyclable PET containing post-consumer resin that is produced in solar-powered facilities. This compounded benefit structure accelerates compliance readiness in the sustainable pharmaceutical packaging market.

By Drug Form: Parenteral Packaging Innovation Accelerates

Parenteral formats post the highest 12.40% CAGR as biologics and novel injectable therapies proliferate. ApiJect’s plastic injector study finds a lower carbon footprint and 100 times less water usage than traditional glass syringes, illustrating tangible ecological wins without sacrificing sterility. Solid dosage forms remain the volume anchor at 60.1% share in 2024, yet they face regulatory scrutiny over PVC/aluminum blisters that complicate recyclability. Liquid orals shift toward bio-HDPE bottles with tethered closures to meet single-use plastic directives. Topical creams adopt mono-material laminate tubes, and inhalable devices integrate post-consumer ABS housings as supply chains mature. Sustainable pharmaceutical packaging market share gains, therefore, hinge on the interplay between advanced therapy modalities and the continuing relevance of mainstream tablet and capsule flows.

Innovation centers focus on nested vial systems supplied ready-to-fill, which reduces on-site washing and depyrogenation, cutting water and energy use. RFID-enabled caps offer authentication for high-value oncology drugs, and near-field sensors record temperature excursions. For solid doses, shifting to push-through paper blisters improves recyclability without compromising shelf life. Collectively, these adaptations underscore the breadth of design pathways driving sustainable pharmaceutical packaging market growth.

By End User: Contract Packaging Expansion

Contract packaging organizations (CPOs) expand at 11.10% CAGR as drug makers outsource specialized capabilities to manage complex compliance footprints. PCI Pharma Services invests USD 365 million to add 545,000 square feet in Rockford, Illinois, and a new Dublin facility focused on injectable devices, signaling robust demand for scalable sustainability platforms. Pharmaceutical manufacturers retain strategic control with a 68.8% share in 2024, yet they increasingly form joint-development agreements with converters to co-engineer low-carbon primary containers. Hospitals seek on-site dose-dispensing systems that minimize secondary cartons, and retail pharmacies push for curbside-recyclable packs that align with corporate social-responsibility commitments. Academic institutes collaborate on material science breakthroughs that CPOs commercialize, accelerating tech-transfer cycles within the sustainable pharmaceutical packaging market.

CPOs leverage cross-customer volume to justify capital‐intensive barrier-coating lines and advanced digital inspection systems such as Antares Vision’s AI-Go tool, which monitors defect patterns in real time and reduces waste rates. Their shared-service model enables smaller biotech firms to launch therapies without building dedicated cleanrooms, aligning financial prudence with sustainability ambitions. The rise of multi-tenant facilities with modular filling suites further decentralizes manufacturing, cutting transport emissions and enhancing supply-chain resilience.

Geography Analysis

North America secured 38.1% of the sustainable pharmaceutical packaging market size in 2024 on the back of entrenched drug manufacturing clusters, well-funded recycling programs, and aggressive corporate sustainability commitments. Eli Lilly’s USD 2 billion Concord plant and Novo Nordisk’s USD 4.1 billion Clayton expansion incorporate robotic handling and rooftop solar arrays, signalling deep integration of environmental metrics in capital spending. Advanced material start-ups in California and Massachusetts secure venture funding for marine-origin PHA and enzymatic depolymerization technologies, anchoring regional competitiveness. Canada aligns labeling standards with the U.S. Pharmacopoeia to streamline cross-border trade in recycled-content containers. At the same time, Mexico enhances pharmaceutical export incentives that reward low-carbon packaging, widening the local customer base.

Asia Pacific posts the highest 15.80% CAGR toward 2030 as China and India scale biologics output under quality frameworks paralleling EU Good Manufacturing Practice rules. Provincial governments in China subsidize bio-polymer pilot lines, and Indian contract packagers secure green bonds to fund closed-loop PET reclamation. Japan pioneers cellulose-based blister alternatives through a consortium of material suppliers and university labs. At the same time, South Korea’s electronics giants leverage thin-film barrier expertise to develop high-performance compostable pouches. Regional trade agreements ease import tariffs on post-consumer resin, helping nascent recyclers scale. The geographic surge reflects both export market compliance pressures and domestic environmental legislation.

Europe maintains balanced growth under the EU Packaging and Packaging Waste Regulation that mandates recyclability by 2028 and defines recycled-content milestones. Germany leverages chemical-recycling leadership to supply pharma-grade monomers, and France drives carton innovation backed by EcoDesign tax credits. The United Kingdom harmonizes post-Brexit rules with continental standards, ensuring frictionless material flows. Italy’s glass hub in Emilia-Romagna adopts oxy-fuel furnaces, reducing kiln emissions 40%, and Spain integrates reverse-vending schemes that capture medicine bottles at pharmacies. Although compliance costs rise, integrated infrastructure and public funding mitigate margin pressure, sustaining the expansion of the sustainable pharmaceutical packaging market.

Competitive Landscape

The sustainable pharmaceutical packaging market demonstrates moderate fragmentation: the top five suppliers account for roughly 35–40% of combined revenue, while dozens of mid-scale converters and material innovators occupy specialist niches. Amcor, Gerresheimer, and SCHOTT AG differentiate via full-portfolio sustainability roadmaps that integrate recyclable polymers, high-recycled-content glass, and renewable-energy-certified operations. One Rock Capital Partners’ acquisition of Constantia Flexibles underlines private-equity confidence in sustainability as a value driver; Constantia’s Level A- Climate Change rating and EcoVadis Gold status validate its appeal.

Technological superiority outweighs pure scale: ApiJect’s medical-grade polypropylene injector challenges glass syringe incumbents, while SCHOTT’s ultra-thin SiO₂ barrier coating pushes glass-performance boundaries at lower weight. Digitalization becomes a front line as Antares Vision’s AI-Go platform enables 100% in-line inspection, trimming scrap, and improving carbon intensity ratios. Partners co-develop tailored solutions; BD collaborates with biotech clients on RFID-enabled pre-fillable syringes that satisfy both traceability and recyclability requirements. Rising innovators capitalize on ocean-grown bioplastic patents, while established firms lock in feedstock through multiyear offtake contracts, further elevating market-entry barriers.

Supply-chain resilience defines risk management. Glass producers hedge energy volatility through renewable power purchase agreements, and polymer converters diversify geographic suitors to offset potential logistical disruptions. The regulatory learning curve serves as an additional moat: legacy participants maintain in-house toxicology labs and regulatory-affairs units that fast-track dossier submissions, whereas new entrants must build similar capabilities or rely on partnerships. Overall, competitive dynamics favor players combining high-performance materials science, agile manufacturing, and documented compliance expertise.

Sustainable Pharmaceutical Packaging Industry Leaders

Amcor plc

WestRock Company

Berry Global Group Inc.

Gerresheimer AG

SCHOTT AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DS Smith launched TailorTemp, a fiber-based temperature-controlled shipper that holds cool conditions for 36 hours and cuts CO₂ emissions 40% relative to EPS alternatives.

- January 2025: BD displayed iDFill RFID-enabled prefillable syringes alongside Neopak XtraFlow for high-viscosity biologics at Pharmapack 2025.

- January 2025: Faller Packaging acquired land in Gebesee, Germany, to build a folding-carton and leaflet plant slated to open in early 2025.

- October 2024: GenNx360 Capital Partners announced Nutra-Med’s takeover of Legacy Pharma Solutions, expanding high-speed bottling and blistering capacity.

Global Sustainable Pharmaceutical Packaging Market Report Scope

| Bottles & Jars |

| Blister Packs |

| Vials & Ampoules |

| Sachets & Pouches |

| Pre-filled Syringes & Cartridges |

| Conventional Plastics (HDPE, PP, PVC) |

| Bioplastics & Plant-based Polymers |

| Glass |

| Paper & Paperboard |

| Aluminum & Foils |

| Recyclable Packaging |

| Biodegradable / Compostable Packaging |

| Reusable Packaging Systems |

| Lightweight / Reduced-material |

| Renewable-energy-sourced Packaging |

| Solid Dosage (Tablets, Capsules) |

| Liquid Oral |

| Parenteral & Injectable |

| Topical & Semi-solids |

| Inhalables & Others |

| Pharmaceutical Manufacturers |

| Contract Packaging Organisations (CPOs) |

| Hospitals & Clinics |

| Retail & Online Pharmacies |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Packaging Type | Bottles & Jars | |

| Blister Packs | ||

| Vials & Ampoules | ||

| Sachets & Pouches | ||

| Pre-filled Syringes & Cartridges | ||

| By Material Type | Conventional Plastics (HDPE, PP, PVC) | |

| Bioplastics & Plant-based Polymers | ||

| Glass | ||

| Paper & Paperboard | ||

| Aluminum & Foils | ||

| By Sustainability Approach | Recyclable Packaging | |

| Biodegradable / Compostable Packaging | ||

| Reusable Packaging Systems | ||

| Lightweight / Reduced-material | ||

| Renewable-energy-sourced Packaging | ||

| By Drug Form | Solid Dosage (Tablets, Capsules) | |

| Liquid Oral | ||

| Parenteral & Injectable | ||

| Topical & Semi-solids | ||

| Inhalables & Others | ||

| By End User | Pharmaceutical Manufacturers | |

| Contract Packaging Organisations (CPOs) | ||

| Hospitals & Clinics | ||

| Retail & Online Pharmacies | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of sustainable pharmaceutical packaging by 2030?

Forecasts place it at USD 214.1 billion, up from USD 95.3 billion in 2025.

How quickly is sustainable pharmaceutical packaging growing?

The segment is expanding at a 14.60% CAGR over 2025-2030.

Which packaging format is seeing the fastest uptake?

Pre-filled syringes and cartridges lead with a 13.80% CAGR thanks to biologics and self-administration trends.

Why is Asia Pacific considered the growth hotspot?

Manufacturing scale-up in China and India, coupled with stricter export-driven sustainability rules, drives a 15.80% CAGR in the region.

What material breakthroughs are shaping future adoption?

Plant-based and seaweed-derived bioplastics now deliver barrier performance close to petro-plastics while cutting carbon footprints.

How do contract packaging organizations influence sustainability goals?

CPOs add advanced low-carbon lines and regulatory expertise, letting drug makers outsource compliant production without heavy capital spend.

Page last updated on: