Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

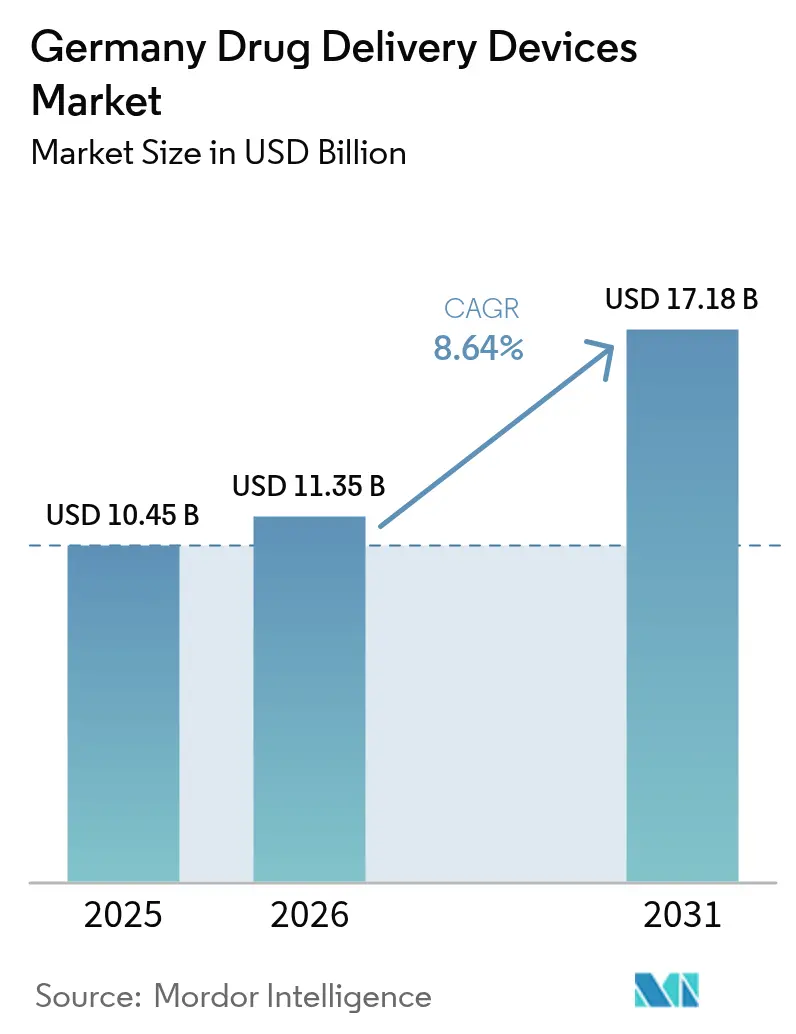

| Base Year Market Size (2025) | USD 10.45 Billion |

| Market Size (2026) | USD 11.35 Billion |

| Market Size (2031) | USD 17.18 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Drug Delivery Devices Market Analysis by Mordor Intelligence

The Germany drug delivery devices market size was valued at USD 10.45 billion in 2025 and estimated to grow from USD 11.35 billion in 2026 to reach USD 17.18 billion by 2031, at a CAGR of 8.64% during the forecast period (2026-2031). Continuous gains stem from the country’s broad statutory insurance coverage, strong manufacturing base in high-value syringes and autoinjectors, and an expanding pipeline of biologics that require precise administration technologies. High diabetes prevalence, a rising cancer burden, and Germany’s well-resourced hospital network keep demand for injectable systems elevated, while rapid shifts toward home-based care and sustainability goals are opening space for connected, reusable formats. EU-wide joint clinical assessments introduced in 2025, domestic fast-track pathways, and real-time digital adherence tools together shorten launch timelines and support uptake of next-generation devices, even as reference-price rules temper premium options.

Key Report Takeaways

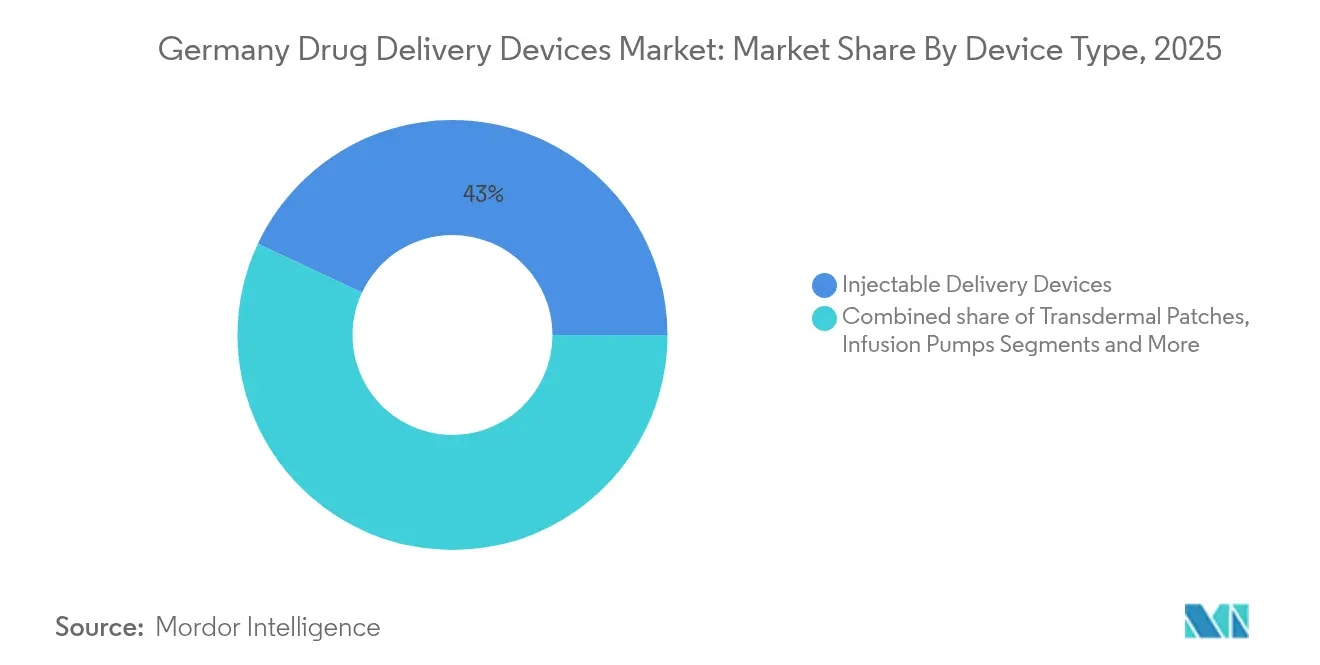

- By device type, injectable delivery devices led with 43.02% of Germany drug delivery devices market share in 2025; implantable systems are projected to expand at an 9.96% CAGR to 2031.

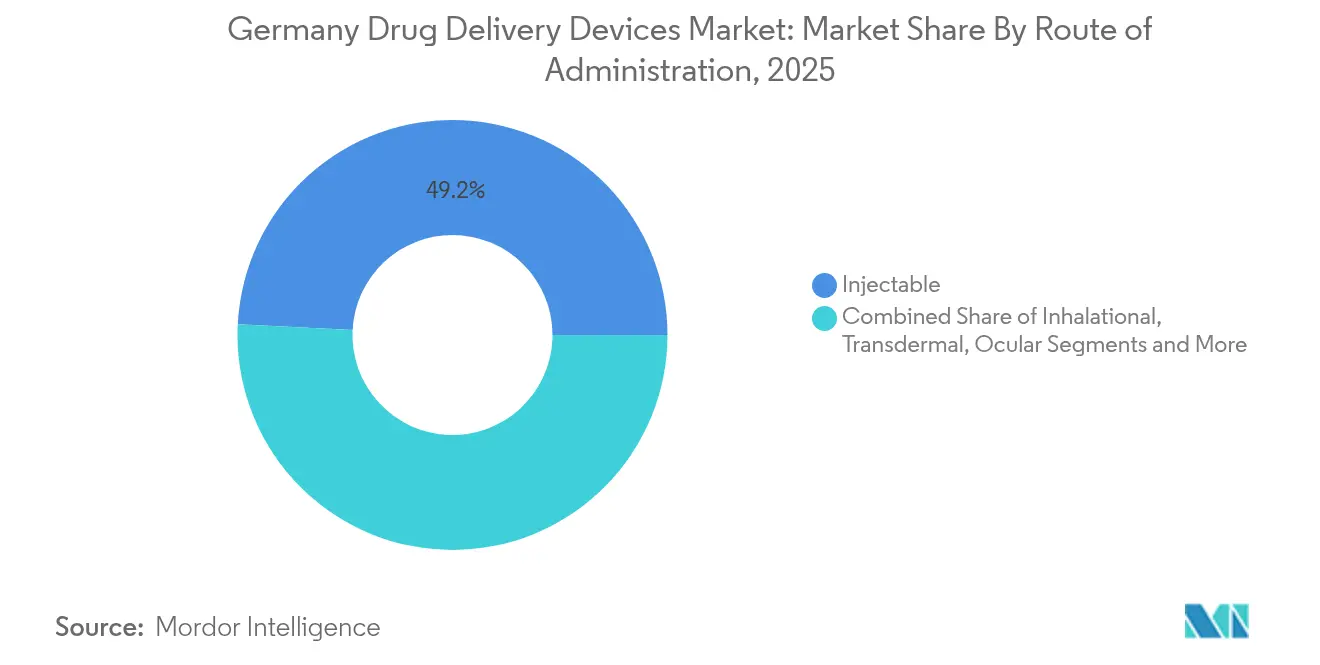

- By route of administration, injectable routes accounted for 49.21% share of the Germany drug delivery devices market size in 2025, while transdermal delivery is advancing at a 9.81% CAGR through 2031.

- By application, diabetes captured 30.05% of Germany drug delivery devices market size in 2025; oncology exhibits the fastest growth at a 9.73% CAGR between 2026-2031.

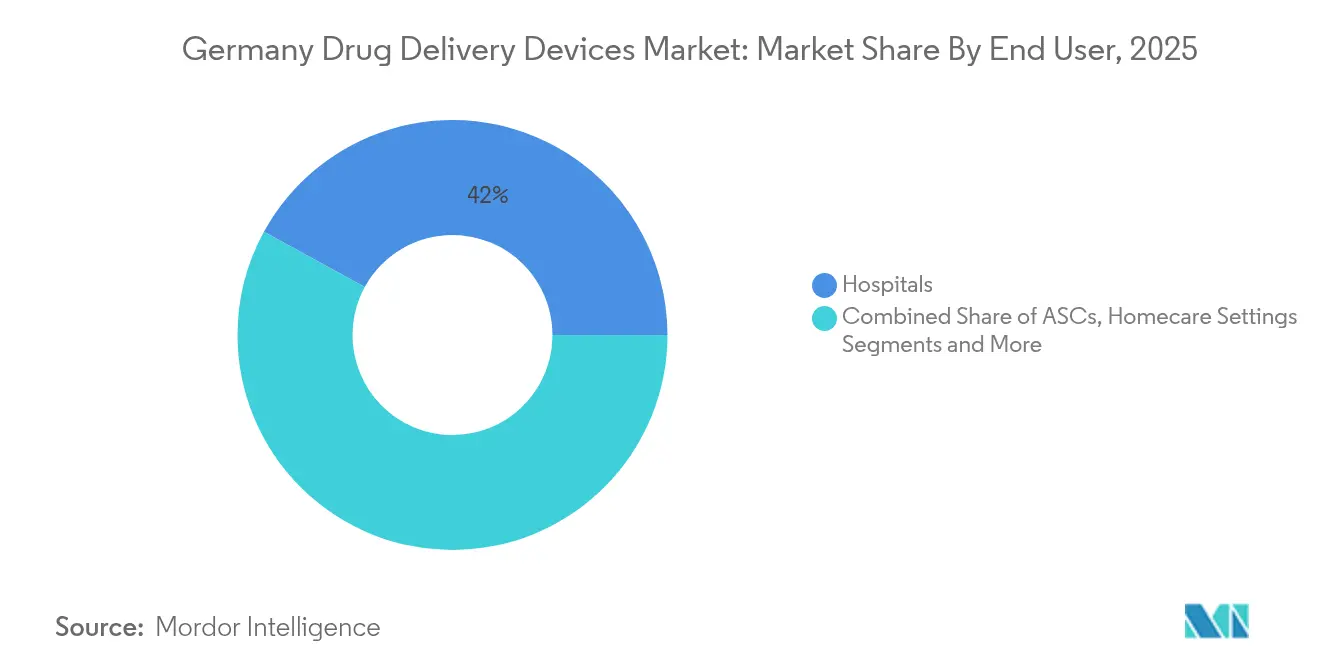

- By end-user, hospitals held 42.03% revenue share in 2025, whereas homecare settings are set to grow at an 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence and Incidence of Chronic and Infectious Diseases | +1.8% | Germany, with spillover to broader EU healthcare systems | Long term (≥ 4 years) |

| Growing Trend of Home Healthcare and Aging Population | +1.6% | Germany core, with demographic parallels across Western Europe | Medium term (2-4 years) |

| Increasing Investment in Biosimilar and Biologics Product Innovation and Development | +1.4% | Germany & EU regulatory zones, global pharmaceutical hubs | Medium term (2-4 years) |

| Government Initiatives Supporting Fast Track Approval and Reimbursement | +1.2% | Germany national, with EU harmonization effects | Short term (≤ 2 years) |

| Technological Advancement and Digitalization | +1.1% | Global, with early adoption in Germany's industrial centers | Medium term (2-4 years) |

| Expansion of Contract-Manufacturing Hubs | +0.9% | Germany & Central Europe manufacturing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence and Incidence of Chronic and Infectious Diseases

Germany reports higher-than-EU-average prevalence for diabetes (8.4%), cardiovascular diseases (6.8%), and chronic respiratory diseases (11.4%).[1]Robert Koch Institute, “Health in Germany,” rki.de This chronic-disease load drives steady demand for advanced injectors, insulin pens, smart pumps, and sustained-release implants that improve adherence and outcomes. Diabetes alone is projected to affect 10.9-14.2 million Germans by 2040, pushing continuous upgrades in automated insulin delivery ecosystems. Oncology demand follows a similar path: micro-/nano-robots under development at the German Cancer Research Center aim to raise tumour-site uptake while cutting systemic toxicity.[2]German Cancer Research Center, “Smart Technologies for Tumor Therapy,” dkfz.de Together, disease trends and research breakthroughs keep the Germany drug delivery devices market on an innovation-driven trajectory.

Growing Trend of Home Healthcare and Aging Population

People aged ≥ 65 will rise from 21% of the population in 2023 to nearly 30% by 2050. Concurrently, those requiring long-term care could climb to 14 million by 2050. These shifts amplify the need for devices that non-professionals can use safely in domestic settings. On-body injectors such as Gerresheimer’s Gx SensAir® allow weekly subcutaneous dosing of monoclonal antibodies without clinical visits, cutting travel-related emissions and easing caregiver burdens. Consumer familiarity with telehealth platforms further accelerates uptake of connected inhalers, pens, and patches that integrate adherence dashboards, reinforcing market momentum in Germany drug delivery devices market.

Increasing Investment in Biosimilar and Biologics Product Innovation and Development

Biopharma sponsors are funnelling capital into mRNA, GLP-1, and cell-and-gene therapies that demand sophisticated containers and administration tools. SCHOTT Pharma boosted revenue from prefillable syringes by 54% to EUR 344 million in 2024 after expanding domestic capacity. Its TOPPAC freeze polymer syringe tolerates cryogenic storage for mRNA vaccines, while cartriQ cartridges target insulin and large-molecule drugs. Continuous spending by industry players underpins steady growth in the Germany drug delivery devices market.

Government Initiatives Supporting Fast Track Approval and Reimbursement

The Medical Research Act (October 2024) slashes red tape for clinical trials and first-in-human studies, compressing development timelines.[3] Germany’s Digital-Health-Applications route reimburses lower-risk connected devices once positive care effect is proven, granting access to more than 90% of the insured population. Alignment with the EU Health Technology Assessment Regulation from 2025 streamlines post-launch benefit assessments, shortening the path from prototype to prescription and strengthening demand across the Germany drug delivery devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Requirements and Product Recalls | -1.3% | Germany national, with EU-wide regulatory alignment | Long term (≥ 4 years) |

| G-BA Price Regulation Capping Premiums for Innovative Systems | -1.1% | Germany national, with potential EU policy spillover | Short term (≤ 2 years) |

| Market Saturation in Conventional Systems Coupled with Patient Compliance and Acceptance Issues | -0.8% | Germany core, with similar patterns in mature European markets | Medium term (2-4 years) |

| Limited Availability of Specialized Microfluidics & Combination-Product Engineering Talent | -0.6% | Germany & broader European technical talent pools | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Requirements and Product Recalls

Germany enforces EU Medical Device Regulation (MDR) alongside its Medical Device Law Implementation Act. Combination products must satisfy dual drug-device evidence packages, and higher-risk classes require third-party conformity assessments.[3]Federal Institute for Drugs and Medical Devices, “Medical Research Act,” bfarm.deResulting cost spikes and recall liabilities weigh heaviest on SMEs, occasionally pausing launches and trimming the Germany drug delivery devices market growth curve.

The Federal Joint Committee assigns reference groups that set maximum reimbursable prices; devices lacking additional benefit evidence must sit at least 10% below comparators. While confidential prices are possible for select innovations, many premium connected or implantable systems still face tight margins, dampening aggressive commercial rollouts in the Germany drug delivery devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Injectable Systems Maintain Leadership as Implants Accelerate

Injectable devices represented 43.02% of all revenues in 2025, cementing their role in the Germany drug delivery devices market size. Sustained demand arises from biologic therapies that dominate new drug approvals and from continuing preference among clinicians for parenteral accuracy. SCHOTT Pharma’s capacity surge in polymer and glass syringes underscores industry confidence.

Implantable pumps, micro-chips, and bioresorbable depots post the quickest gains at an 9.96% CAGR. Patient-friendly inhalers preserve share amid a high national burden of chronic respiratory illness, while transdermal patches earn incremental adoption for hormone and pain management. Across categories, embedded connectivity features enhance dose logging and feedback loops, lifting adherence and data-driven care pathways within the Germany drug delivery devices market.

By Route of Administration: Injectable Dominance with Transdermal Upswing

Injectable delivery retained a 49.21% revenue stake in 2025, reflecting clinician trust in intravenous, subcutaneous, and intramuscular routes for vaccines and large-molecule drugs. This proportion anchors the Germany drug delivery devices market share and is bolstered by next-gen autoinjectors that lower activation force and support 2-5 mL volumes.

Transdermal formats scale fastest at a 9.81% CAGR on the back of microneedle arrays and wirelessly powered acoustic patches that raise payload size limits. Oral mucosal films gain traction for rapid pain relief, while inhaled, ocular, and nasal modalities extend options for targeted local therapy, together enriching clinical toolkits available to practitioners in the Germany drug delivery devices market.

By Application: Diabetes Commands Revenues while Oncology Propels Future Growth

Diabetes accounted for 30.05% of the Germany drug delivery devices market size in 2025. Closed-loop AID systems that synchronise CGM and pump algorithms are now widely prescribed, with paediatric guidelines highlighting superior time-in-range during exercise scenarios.

Oncology devices advance at a 9.73% CAGR as micro-robots, nanoparticle shuttles, and on-body injectors aim to chip away at hospital infusion visits. Cardiovascular, respiratory, and CNS segments maintain steady share, whereas infectious-disease applications spur interest in single-use dual-chamber syringes that simplify lyophilised vaccine reconstitution in the Germany drug delivery devices market.

By End-user: Hospitals Reign but Homecare Gains Ground

Hospitals generated 42.03% of 2025 turnover, reflecting concentration of complex oncology and critical-care infusions. Integrated pharmacy automation and staff familiarity with multi-channel pumps reinforce their centrality.

Yet homecare settings are on a double-digit growth trajectory (10.62% CAGR) as statutory insurers reimburse nurse visits and connected devices for self-administration. Ambulatory surgical centres and specialist clinics fill the gap between inpatient and home use, widening distribution nodes for suppliers active in the Germany drug delivery devices market.

Geography Analysis

Germany’s advanced hospital density, export-oriented manufacturing, and universal insurance base combine to support a vibrant domestic ecosystem for drug delivery innovation. Nationwide reimbursement rules guarantee broad patient access while price corridors guide cost containment, creating predictable albeit competitive revenue pools.

Urban Länder such as North-Rhine-Westphalia and Baden-Württemberg house clusters of device engineers, glass manufacturers, and pharma R&D hubs, accelerating prototype-to-pilot cycles. Eastern regions, historically underserved, are seeing targeted federal grants directed at digital-health rollouts and elder-care technology pilots, gradually balancing regional adoption.

The demographic reality of a median age nearing 47 and an expanding cohort of multimorbid seniors ensures enduring demand for both high-acuity hospital devices and simplified self-care formats. This blend of sophisticated infrastructure and home-centred preferences cements Germany’s role as the reference market for European launches and attracts cross-border investment into the Germany drug delivery devices market.

Regulatory Landscape

Drug delivery devices and drug-device combination products in Germany are regulated under EU-level rules, led by the EU Medical Device Regulation (MDR) 2017/745 (as implemented and supplemented nationally through the Medizinprodukterecht-Durchfuehrungsgesetz, MPDG), with medicinal-product legislation (including Directive 2001/83/EC) determining the primary regulatory route based on the product's principal mode of action. Where a medicinal product integrates a device component, the device part must meet the MDR General Safety and Performance Requirements (GSPR) within the marketing authorization dossier, which adds documentation and testing depth for prefilled syringes, pens, on-body injectors, and other integrated systems.

Operationally, Germany uses BfArM processes for medical devices, including authorization of clinical investigations, and the German Medical Devices Information and Database System (DMIDS) remains the submission and data route in several areas until the European database EUDAMED becomes fully functional. The anticipated EUDAMED start point (noted as 28 May 2026 in BfArM-facing materials, followed by a transition period) is a near-term compliance anchor for manufacturers and importers managing registrations, vigilance reporting, and study administration alongside MDR conformity assessment requirements.

Value Chain Analysis

Germany's drug delivery devices value chain starts with upstream inputs such as specialty glass and metals, medical-grade polymers (including silicones and engineered resins), and precision tooling (micro-molds and components used in high-tolerance assemblies). Midstream work covers device design and engineering, component molding and machining, and regulated manufacturing under quality systems, followed by aseptic integration steps for drug-device combination products where device assembly, packaging, and coordination with fill-finish partners are required for ready-to-use formats used in injectables and cartridges.

Downstream, products move through warehousing and cold-chain or controlled logistics where needed, and distribution channels serving hospitals, clinics, ambulatory settings, and homecare. CDMO-style models are prominent for complex combination work, with companies such as Gerresheimer (device development and contract manufacturing) and Vetter (device assembly and packaging services) supporting pharma sponsors that need scalable, compliant production. On the system-enablement side, initiatives such as the COMBINE program (involving PEI, BfArM, and ethics committees) address administrative friction in combined studies across CTR, MDR, and IVDR, while industry feedback (for example, SPECTARIS survey findings highlighting widespread supply chain disruptions) points to persistent bottlenecks linked to regulatory burden, input availability, and cost pressures.

Competitive Landscape

The Germany drug delivery devices market is moderately fragmented: global pharma groups supply combination products, mid-sized German engineering firms specialise in precision components, and contract manufacturers offer scalable fill-and-finish services. Strategic alliances predominate. Gerresheimer’s tie-up with Aptar Digital Health pairs mechanical expertise with software analytics to deliver integrated oncology support tools.

SCHOTT Pharma, leveraging decades of glass science, is shifting toward polymer solutions fit for low-temperature biologics while expanding ready-to-use cartridge lines. Vetter invests in fill-finish expansions in Ravensburg and Langenargen to meet surging outsourcing orders for injectables. Start-ups focusing on microneedle and acoustic-patch platforms inject further dynamism.

Sustainability credentials are fast becoming bid criteria: on-body systems featuring reusable drive units and recyclable disposables align with hospital and insurer green targets. Meanwhile, price-reference caps prompt firms to highlight total-cost-of-care savings through adherence gains and reduced hospitalisations, sharpening competitive narratives across the Germany drug delivery devices market.

Germany Drug Delivery Devices Industry Leaders

Bayer AG

Becton, Dickinson and Company

Gerresheimer AG

Ypsomed Holding AG

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The intersection of home-based therapy and biologics delivery offers a focused entry point, since Germany's chronic-disease load and insurer-backed care pathways reward devices that simplify self-administration while producing usable adherence evidence. Device makers are actively productizing this direction, including Gerresheimer's on-body delivery (Gx InPuls), autoinjector platform (Gx Inbeneo), and digital support add-on (Gx InMonit). These offerings align mechanical delivery with patient-support data flows that fit diabetes and oncology use cases already central to German demand.

Manufacturing and services capacity for combination products is a second opportunity cluster, spanning high-quality primary containers (syringes and cartridges), assembly, and regulated packaging, where German and Germany-linked suppliers differentiate on precision and compliance. Digitalization at both the company and system levels also creates practical pull for connected formats and information-enabled use, including the vfa-backed diGItal pilot that evaluates replacing printed package inserts with digital information (with implementation starting in Q3 2026). Alongside that, regulatory process modernization, including Germany's COMBINE initiative and the planned shift from DMIDS toward EUDAMED-based workflows, supports companies that invest early in data-ready compliance and post-market evidence generation for connected and combination delivery systems.

Recent Industry Developments

- June 2026: Bayer completed its acquisition of Perfuse Therapeutics, securing full rights to the PER-001 sustained-release small molecule delivery platform for ocular diseases. The transaction strengthens Bayer's access to proprietary delivery technology where dosing duration and localized administration can shape device and formulation choices. For drug delivery device ecosystems, the move highlights continued interest in integrated delivery platforms tied to targeted therapeutic areas such as ophthalmology.

- April 2026: BD introduced the BD Pyxis Pro Dispensing Solution and the BD Incada Connected Care Platform in Europe, expanding its medication-management and connected-care footprint. The launch increases the installed base of digital infrastructure that can support tighter medication workflows and data capture across care settings. This reinforces demand for interoperability and traceability features that also influence adoption of connected drug delivery devices used in hospitals and outpatient pathways.

- June 2024: Vetter announced expansion activities tied to rising demand for outsourced injectable production, including manufacturing capacity additions in Ravensburg and Langenargen, Germany. The expansion supports higher-throughput supply for injectable and combination-product programs that rely on specialized, compliant operations. It also signals sustained outsourcing momentum among biopharma sponsors seeking scale and quality in Germany-linked fill-finish and related services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the value of drug delivery devices sold in Germany that are used to administer therapeutic agents into the body through routes such as injectable, inhalation, transdermal, buccal or nasal, ocular, and implant based delivery.

Scope exclusions: We exclude basic packaging and logistics services, in-vitro diagnostic-only devices, and single-use hospital consumables such as IV bags and catheters.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal and Sublingual)

- Ocular

- Nasal

- By Application

- Diabetes

- Oncology

- Cardiovascular

- Respiratory

- Central Nervous System Disorders

- Infectious Diseases

- Others

- By End-user

- Hospitals

- Ambulatory Surgical Centres

- Homecare Settings

- Clinics and Speciality Centres

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the baseline for demand signals, care setting mix, and device adoption context across Germany. We mainly relied on public health and statistics sources such as the German Federal Statistical Office (Destatis), the Robert Koch Institute, the European Medicines Agency, and the World Health Organization, along with selected publications from the OECD and peer-reviewed clinical journals.

On the commercial side, we reviewed annual reports, investor presentations, and product literature to understand device portfolios and typical pricing logic by route of administration. Import and export trade statistics and an import-export shipment-level database were also used selectively to cross-check device flows and to spot step changes in volumes. The desk sources noted above are illustrative and not exhaustive, and many other public references were used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work was used to validate what gets counted as a drug delivery device in Germany, and to pressure test assumptions on replacement cycles, channel markups, and utilization in hospitals versus homecare. We spoke with a mix of manufacturers, distributors, pharmacists, clinicians, and procurement stakeholders so that pricing and volume assumptions could be confirmed from more than one angle, and then reconciled back to desk signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 20% | |

| Mid tier: 47% | Functional/Unit leaders: 21% | |

| Smaller Players: 21% | Managers: 59% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool view, where treated population and therapy delivery patterns in Germany were translated into device volumes, which were then converted to value using route-specific price bands and channel adjustments. To keep totals realistic, we corroborated results with selective bottom-up approximations such as sampled average selling price multiplied by estimated units for common device categories, followed by channel checks with distributors and care providers.

Key inputs that shaped the model included diabetes and respiratory patient counts, self-injection penetration in chronic therapies, inhaler and pump utilization norms by care setting, replacement frequency for reusable systems, and mix shift toward homecare and specialty pharmacy dispensing. For forecasting, scenario analysis was used so adoption speed, price progression, and utilization changes could be flexed in a controlled way, and the final path was aligned to expert consensus gathered in interviews. When gaps appeared in bottom-up cross-checks (for example, limited visibility on smaller imported niches), the missing portion was estimated using proxy ratios from comparable device classes and then re-validated through follow-up discussions.

Data Validation & Update Cycle

Outputs were triangulated across independent signals, including epidemiology direction, observed channel behavior, and implied per-patient device spend, and then reviewed for outliers before sign-off. If a segment showed an unusual jump, we revisited assumptions, rechecked price bands, and re-contacted sources to confirm whether the change was real or a modeling artifact.

The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts, reimbursement changes, or large product transitions. Before delivery, an analyst performs a final update pass so clients receive the most recent view of the market and its underlying assumptions.

Mordor Intelligence's Germany Drug Delivery Devices Market Estimate Compared With Other Published Estimates

Different published figures for Germany drug delivery devices can look far apart because each publisher groups products differently, uses different base years and currency timing, and may apply different adoption curves across hospital and homecare settings.

Some external estimates bundle in broader hospital consumables and adjacent infusion disposables, which can lift the headline value even if device adoption is unchanged. For Mordor Intelligence, revenues are counted only for devices that actively deliver a therapeutic agent through defined administration routes, and items like IV bags and catheters are excluded so consumables do not get mixed into device totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.45 B (2025) | |

| Market Research Firm A | USD 1.49 B (2023) | Uses an earlier base year and a narrower device basket by route grouping, which can leave out delivery formats that are included in broader route coverage, and it can apply different channel price assumptions in Germany. |

| Market Research Firm B | USD 1.98 B (2031) | Shows a later forecast-year value and a lower growth trajectory, which can reduce the implied impact of homecare shift, replacement cycles, and utilization intensity for higher-value delivery systems. |

Taken together, the spread is mainly explained by inclusion decisions (devices versus consumables), plus the year used and the growth curve applied. When scope and inputs are kept consistent, the market size becomes easier to reconcile to patient demand signals, utilization patterns, and repeatable pricing steps.

Key Questions Answered in the Report

What is the current value of the Germany drug delivery devices market?

The market stands at USD 11.35 billion in 2026 and is projected to grow to USD 17.18 billion by 2031.

Which device type generates the highest revenue?

Injectable systems lead with a 43.02% share due to their central role in biologics and chronic-disease therapy.

How fast is the homecare segment growing?

Home-based use of drug delivery devices is advancing at an 10.62% CAGR through 2031 on the back of demographic ageing and telehealth adoption.

Why are transdermal patches gaining popularity?

New microneedle and acoustic-wave technologies boost skin permeation while offering painless, self-administered dosing.

What role do German regulations play in device approvals?

The Medical Research Act and EU HTA alignment shorten clinical-trial and reimbursement timelines, although stringent MDR requirements still raise development costs.

Which therapeutic area shows the fastest growth?

Oncology devices post a 9.73% CAGR thanks to micro-robotic carriers and on-body injectors aimed at precise tumour targeting

Page last updated on: