Trailer Assist System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.13 Billion |

| Market Size (2031) | USD 0.21 Billion |

| Growth Rate (2026 - 2031) | 10.01% CAGR |

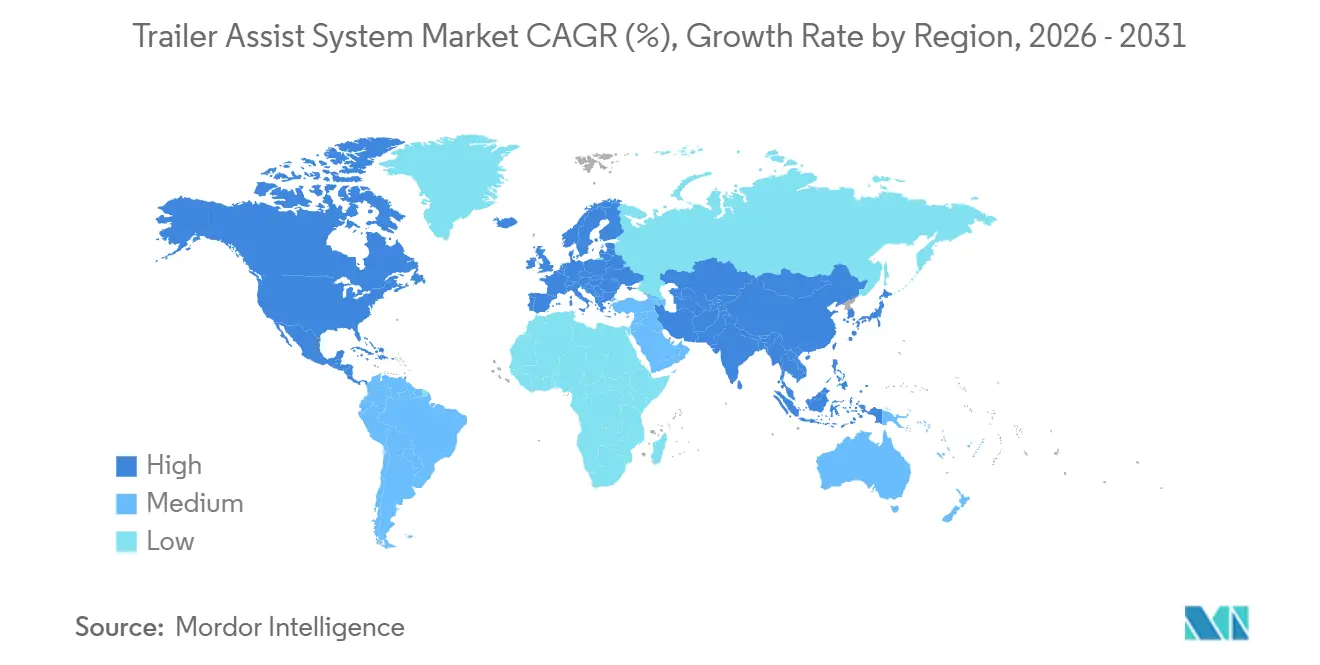

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trailer Assist System Market Analysis by Mordor Intelligence

The Trailer assist system market size is projected to expand from USD 0.12 billion in 2025 and USD 0.13 billion in 2026 to USD 0.21 billion by 2031, registering a CAGR of 10.01% between 2026 and 2031. This upward trajectory stems from regulatory requirements for trailer safety, a rise in recreational towing among younger buyers, and the convergence of smart-trailer telematics with vehicle-side ADAS architectures. OEMs are shifting from basic reversing aids to integrated sensor-fusion suites that handle hitch detection, path planning, and collision avoidance across SAE Levels 1 through 4 of automation. Semi-autonomous packages dominate current adoption because they balance cost with liability clarity, while highly automated systems move from pilots to commercial rollouts in controlled parking environments. Value creation has already begun to tip from hardware toward proprietary software and over-the-air feature upgrades, positioning algorithms as the key profit lever through 2031. Competitive intensity remains moderate because a handful of Tier-1 suppliers control sensors and ECUs. Still, OEM differentiation now depends on unique user interfaces, neural-network hitch-angle estimation, and subscription-based feature unlocks.

Key Report Takeaways

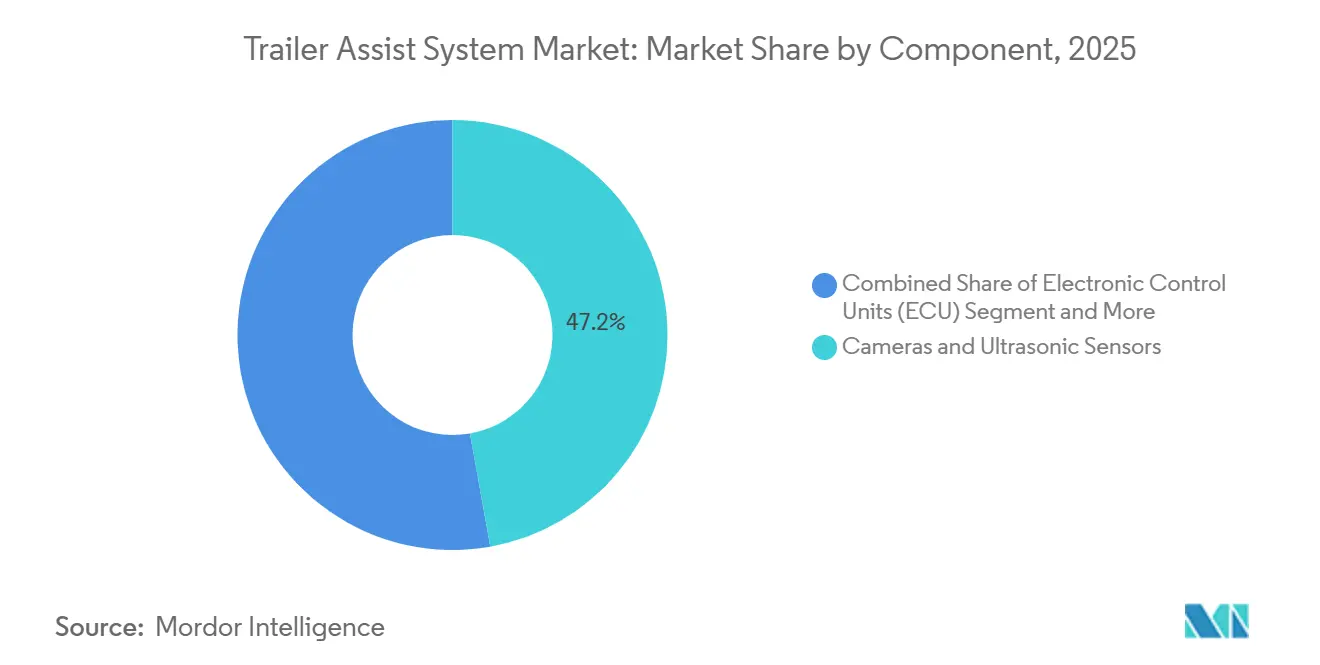

- By component, cameras and ultrasonic sensors held 47.15% of the Trailer assist system market share in 2025, while software modules are forecast to advance at a 13.28% CAGR through 2031.

- By vehicle type, passenger cars accounted for 67.04% of the Trailer assist system market in 2025 and are projected to grow at a 11.57% CAGR through 2031.

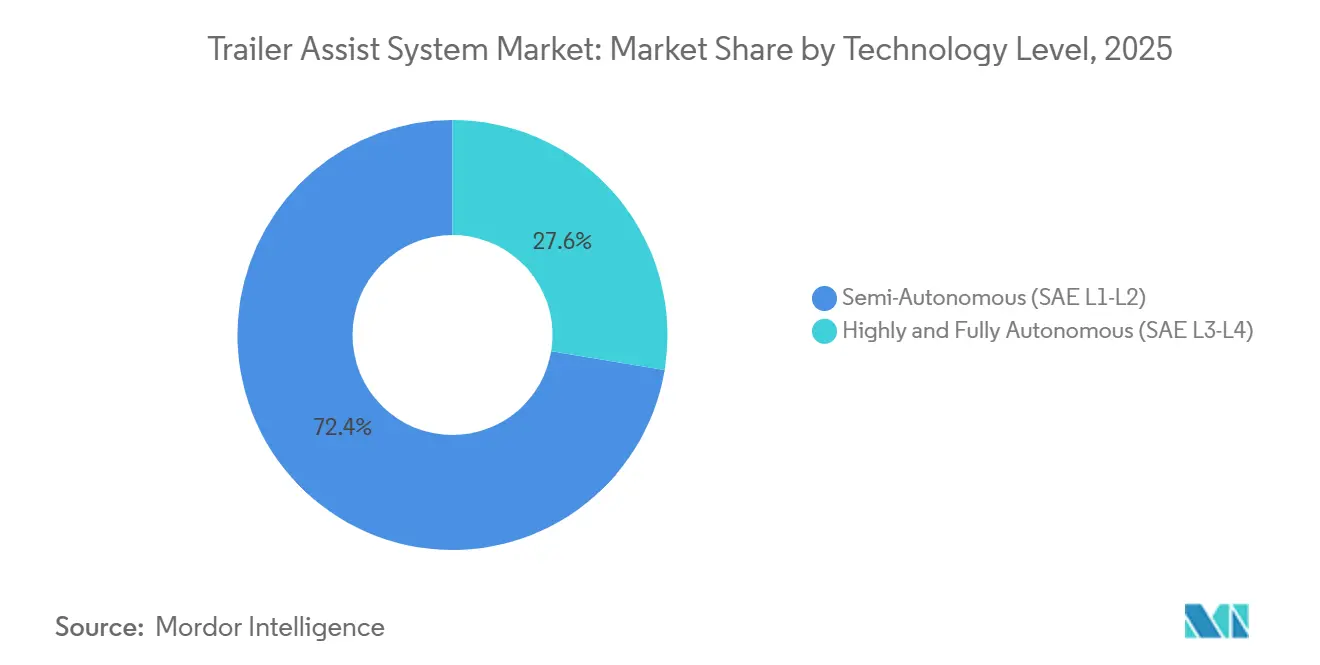

- By technology level, semi-autonomous systems led with 72.35% of the Trailer assist system market share in 2025; highly and fully autonomous systems are set to escalate at an 18.33% CAGR through 2031.

- By end market, OEM-fitted systems accounted for 90.44% of revenue in 2025, while aftermarket retrofits are poised to post a 15.51% CAGR over 2026-2031.

- By geography, North America dominated with 39.12% share in 2025, while Asia-Pacific is set to grow at a 14.36% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trailer Assist System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for Trailer Safety | +2.1% | North America and EU | Medium term (2-4 years) |

| OEM Move Toward SAE L2–L3 | +1.9% | Global; early adoption in Germany, United States, and China | Long term (≥4 years) |

| Towing in North America and Europe | +1.8% | North America and EU | Short term (≤2 years) |

| Integration of Cameras and Sensor Fusion | +1.5% | Global | Medium term (2-4 years) |

| Smart-Trailer Telematics Convergence | +1.3% | Global; concentrated in logistics corridors | Medium term (2-4 years) |

| Electrified Trailer Hitch-Assist Demand | +1.0% | North America and EU; emerging China | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Mandatory Trailer Safety Features

National and supranational bodies are embedding trailer-specific rules into broader vehicle automation frameworks, compelling automakers to accelerate deployment of camera and sensor suites. UNECE’s GRVA advanced performance text for low-speed maneuvers in 2025 implicitly covers trailer reversing and parking scenarios [1]“GRVA Automated Driving Guidance,” UNECE, unece.org. In the United States, NHTSA finalized FMVSS 305a in 2024 and opened rulemaking on automatic emergency braking for light commercial vehicles, indirectly rewarding trucks that can detect hitches and obstacles using surround-view arrays. Compressed compliance timelines force Tier-1 suppliers to deliver production-ready hardware in 18–24 months. New rules also tighten performance parity between OEM packages and aftermarket kits by prescribing minimum detection ranges and false-positive thresholds.

OEM Move Toward SAE L2–L3 Automated Parking Suites

Automakers are increasingly integrating trailer-assist features into their advanced automated parking systems. In Europe, Mercedes-Benz and Bosch unveiled the Intelligent Park Pilot, marking the debut of an SAE Level 4 commercial parking system that operates in designated car parks. Ford Otosan demonstrated its autonomous trailer parking in 2024, significantly improving parking efficiency compared to seasoned drivers, thanks to RRT* (Rapidly-exploring Random Tree Star) planners and model-predictive control. Meanwhile, BMW's Parking Assistant Professional not only remembers frequent routes but also allows smartphone control, though drivers retain legal responsibility under existing laws.

Rising Recreational Towing in North America and Europe

In 2025, Millennials and Generation Z accounted for a significant portion of new RV purchases, a notable increase from 2020. This shift has heightened the demand for trailer-assist features, making the hookup and reversing process more efficient. The RV Industry Association projects a median of 349,000 RV shipments in 2026, a 2.8% YoY rise, with travel trailers and fifth wheels leading volumes [2]“2026 Shipment Outlook,” RV Industry Association, rvia.org. Younger owners expect trailer backup cameras, hitch-alignment overlays, and smartphone-based remote parking, which echo lane-keeping assist in their daily-driver vehicles. European caravan markets echo this trend, led by Germany and the United Kingdom. Higher attach rates support OEM margins, which in turn fund next-generation functions such as AI-based jackknife prediction.

Integration of Surround-View Cameras and Sensor Fusion

OEMs are transitioning from single rear cameras to 360-degree systems that combine ultrasonic, radar, and camera inputs for estimating hitch angle and issuing collision warnings. AUMOVIO’s Xelve Trailer, unveiled at CES 2026, exemplifies active intervention rather than passive guidance. Equipped with multiple cameras, radars, and ultrasonic sensors, Mercedes-Benz's MB.DRIVE ASSIST PRO utilizes the same hardware stack for its trailer modes. Bosch's Radar Gen 7 Premium, developed by Bosch, can detect small objects at significant distances, significantly reducing instances of false braking. Meanwhile, Fusion enhances safety by providing predictive jackknife warnings that monitor both hitch-angle velocity and steering-wheel input.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| System Cost for Mass-Market Vehicles | -1.6% | Global; acute in price-sensitive segments | Short term (≤2 years) |

| Sensor Limitations in Poor Weather | -1.2% | Global; severe in Northern Europe, Canada, Northeast US | Medium term (2-4 years) |

| Ambiguity for AI-Driven Collisions | -0.9% | Global; uncertainty in the United States, Asia-Pacific | Long term (≥4 years) |

| Low-Towing Culture in Economies | -0.7% | South America, Africa, parts of Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Incremental System Cost for Mass-Market Vehicles

Trailer-assist packages significantly increase vehicle prices, which limits their adoption in entry-level trucks. Ford offers its customer-installed Trailer Sensor Kit, while GM provides the IntelliHaul 3.0 camera kit. These costs reflect camera modules, housings, and licenses that suppliers amortize over far fewer units than mainstream ADAS features such as automatic emergency braking. Budget-conscious buyers frequently prioritize fuel efficiency or payload over convenience, resulting in subdued adoption rates.

Sensor Performance Limitations in Poor Weather

Rain, snow, and fog diminish the effectiveness of cameras and LiDAR, compromising their reliability at critical moments for drivers. Testing by SAE and Magna in wind tunnels revealed that camera visibility can drop to zero under heavy rainfall at moderate speeds. In heavy rain, LiDAR's range significantly decreases. Conversely, radar retains only a portion of its range in thick fog. Advancements in detection technology have been introduced in recent years, but real-world validation of these improvements remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Algorithms Outpace Hardware Growth

Cameras and ultrasonic sensors contributed 47.15% of 2025 revenue, anchoring the perception layer that feeds hitch detection and obstacle avoidance. Yet proprietary code will drive the next wave of value as software modules are forecast to compound at 13.28% through 2031. Neural-network controllers replace rule-based algorithms, learning trailer weight and driver style to refine interventions. In 2024, General Motors secured a patent for a vision-only hitch-angle estimator, streamlining its Bill of Materials (BOM) by eliminating the need for dedicated yaw sensors. At the same time, as Electronic Control Units (ECUs) increasingly integrate into centralized compute nodes like NVIDIA DRIVE, the industry witnesses a decline in costs associated with individual features. Chinese manufacturers have begun offering 720p wireless cameras at competitive prices, putting pressure on hardware profit margins. Through subscription-based over-the-air updates, features such as multi-trailer profiles and predictive jackknife warnings are now monetized, safeguarding software profit margins. While hardware remains crucial—especially with high-bandwidth imaging and radar inputs feeding algorithms—it's the software that drives differentiation in user experience and ongoing enhancements.

Forecasts indicate that the software segment of the trailer assist system market will outpace the sensor segment in growth. This surge is largely attributed to over-the-air updates, which empower Original Equipment Manufacturers (OEMs) to monetize features even after a vehicle's sale. A 2024 analysis highlighted the efficiency of linear quadratic regulators, achieving real-time control with significant computation advantages over the more complex nonlinear model predictive control. This efficiency enables deployment on budget-sensitive ECUs. As the software layer integrates AI inference engines for hitch-angle recognition, suppliers are poised to incorporate specialized accelerators, ensuring swift response times. Looking ahead, revenues from algorithm licensing and data analytics are set to eclipse those from perception hardware.

By Vehicle Type: Passenger Cars Lead, Commercial Vehicles Gain Share

Passenger cars represented 67.04% of revenue in 2025, sustaining an 11.57% CAGR as millennials demand towing capability for travel trailers and boats. Models such as the Ford F-150, Chevrolet Silverado, and RAM 1500 offer trailer backup cameras, knob-based steering aids, and smartphone apps, creating stickiness through brand ecosystems. Light commercial vehicles make up the second-largest slice, favored by contractors seeking time-saving hookup routines and insurance-reducing jackknife prevention. Heavy commercial vehicles remain small today, yet accelerate adoption in distribution centers where automated yard handling improves throughput. Knorr-Bremse’s ATLAS-L4 truck, under contract for 2028 delivery, signals mainstream adoption in the latter half of the decade [3]“ATLAS-L4 Contract Announcement,” Knorr-Bremse AG, knorr-bremse.com .

Fleet standardization propels light commercial uptake: unified camera layouts simplify driver training and incident forensics. Recreational culture keeps passenger-car volumes dominant, especially in North America, but Asia-Pacific logistics modernization will lift the commercial share. The Trailer assist system market share for heavy trucks will jump as geofenced depots trust Level 4 yard maneuvers to cut labor hours and back-over incidents. OEM incentives align because electrified powertrains need software-enabled efficiency gains to offset towing-related range losses.

By Technology Level: Semi-Autonomous Base, L3–L4 Acceleration

Semi-autonomous (SAE L1–L2) suites accounted for 72.35% of revenue in 2025, as they require regulatory approval and keep drivers legally responsible. They rely on driver monitoring to ensure drivers keep their hands on the wheel, limiting liability creep. Higher automation (SAE L3–L4) captured the remainder but will grow at a 18.33% CAGR as regulators finalize liability rules and as infrastructure, such as sensor-equipped parking garages expand. Mercedes-Benz/Bosch Intelligent Park Pilot already operates commercially in Stuttgart, pairing vehicle-side perception with garage sensors. BMW’s Parking Assistant Professional adds memorized routes but holds back legal autonomy. Chinese firms like Xpeng bet on visual memory to bypass costly external sensors.

OEMs frame Level 3–4 trailer functions as premium extensions of automated valet parking, upselling subscription bundles once legislative clarity arrives. As feature over-the-air activation gains traction, vehicles shipped with dormant high-spec hardware can unlock trailer autonomy later, spreading costs across the ownership cycle. The Trailer assist system market size for L3–L4 packages will therefore expand even after the initial hardware sales plateau.

By End Market: OEM Dominance, Aftermarket Surge

OEM-fitted systems accounted for 90.44% of revenue in 2025 because factory integration guarantees CAN bus access, warranty alignment, and seamless infotainment displays. Yet the aftermarket will accelerate at 15.51% CAGR owing to wireless kits appealing to owners of 2010-2020 trucks without factory cameras. Ford’s plug-and-play kit and GM’s IntelliHaul 3.0 lead organized dealer accessories, while EchoMaster serves mixed-brand fleets with a three-year warranty.

Aftermarket products lack advanced hitch-angle analytics but still satisfy regulatory rear-visibility requirements at lower prices. Growing e-commerce for DIY installs and YouTube tutorials further eases adoption. Over the period, the Trailer Assist System industry expects aftermarket vendors to bundle telematics modules and subscription analytics, narrowing functionality gaps with OEM packs while retaining cost advantages.

Geography Analysis

North America captured 39.12% of 2025 revenue, driven by a strong recreational towing culture and early adoption of knob-based backup systems. Growth moderates as premium truck customers near saturation and as price-sensitive trims balk at USD 1,000-plus option prices. Europe ranked second, aided by Regulation 2022/1426, which green-lights SAE Level 4 valet parking in predefined domains, and by Germany’s 2021 driverless law, which enabled Stuttgart pilots. Asia-Pacific will post a 14.36% CAGR through 2031, driven by Chinese and Indian fleet modernization, logistics automation, and government incentives for electric heavy trucks that bundle ADAS features.

India recorded 754,067 commercial-vehicle sales during April-December FY2026, up 10% YoY, and freight demand expanded, coinciding with robust GDP growth. However, with an average fleet age stretching over a decade, there's a clear pent-up demand for trucks, especially those featuring integrated trailer assist systems. Meanwhile, in China, electric heavy trucks accounted for a significant share of sales in the first half of 2025. With a trade-in incentive encouraging the replacement of older vehicles, projections suggest this figure could increase substantially by 2026. Furthermore, expansive battery-swap corridors are alleviating range anxiety for drivers. This makes advanced trailer backing aids increasingly crucial, especially for conserving energy during yard maneuvers.

South America, the Middle East, and Africa remain early-stage markets because recreational towing is marginal and cost sensitivity dominates commercial fleet purchases. Over the forecast, government safety mandates and falling camera prices could spark incremental uptake, but contributions to global revenue stay small through 2031.

Competitive Landscape

The trailer assist system market is moderately concentrated, with key players such as Bosch, Continental, ZF-WABCO, Magna, and Valeo supplying sensors and ECUs. Bosch offers advanced solutions like Radar Gen 7 Premium and Vehicle Motion Management, enabling long-range object detection. Continental has partnered with Aurora to focus on Level 4 freight platforms and continues to strengthen its position in autonomous mobility. Magna's ClearView vision suite has been introduced on RAM models, enhancing surround-view capabilities. Knorr-Bremse is advancing its ATLAS-L4 driverless truck, which is expected to enter serial production in the coming years.

OEMs are differentiating themselves through proprietary software innovations. In 2024, General Motors patented a camera-only neural hitch-angle estimator, which reduces hardware costs. Ford has integrated its Pro Trailer Backup Assist, offering a user-friendly steering-knob interface. Mercedes-Benz is leveraging its DRIVE PILOT stack to extend its functionality to trailers. Emerging market opportunities include electrified hitch-assist systems that account for energy consumption during route planning and unified telematics solutions that integrate trailer cameras, GPS, and TPMS data with vehicle-side ADAS.

Chinese OEMs are adopting cost-effective strategies by relying on onboard visual SLAM technology to record and replay trailer routes. This infrastructure-light approach allows them to compete on cost and undercut Western rivals. These developments highlight the growing focus on innovation and efficiency in the trailer assist system market, as companies aim to address evolving customer needs and technological advancements.

Trailer Assist System Industry Leaders

Robert Bosch GmbH

Continental AG

Magna International

Valeo SA

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hyundai Translead partnered with Lytx to integrate HT LinkVue 360-degree trailer cameras into the Lytx telematics platform, giving fleets unified access to trailer video, vehicle data, and operational analytics.

- December 2025: AUMOVIO released an advanced reversing aid and a trailer collision warning feature that returns a vehicle-trailer combination to its starting point at the touch of a button while protecting against pedestrian or obstacle impact.

Global Trailer Assist System Market Report Scope

The scope includes segmentation by component (cameras and ultrasonic sensors, software modules and algorithms, and electronic control units), vehicle type (passenger cars, light commercial vehicles, and heavy commercial vehicles), technology level (semi-autonomous (SAE L1-L2), and highly and fully autonomous (SAE L3-L4)), and end market (OEM-fitted systems and aftermarket retrofits). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Cameras and Ultrasonic Sensors |

| Software Modules and Algorithms |

| Electronic Control Units (ECU) |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Semi-Autonomous (SAE L1-L2) |

| Highly and Fully Autonomous (SAE L3-L4) |

| OEM-Fitted Systems |

| Aftermarket Retrofits |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Cameras and Ultrasonic Sensors | |

| Software Modules and Algorithms | ||

| Electronic Control Units (ECU) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| By Technology Level | Semi-Autonomous (SAE L1-L2) | |

| Highly and Fully Autonomous (SAE L3-L4) | ||

| By End Market | OEM-Fitted Systems | |

| Aftermarket Retrofits | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global size of the trailer assist system market today and where is it headed by 2031?

The segment stands at USD 0.13 billion in 2026 and is projected to reach USD 0.21 billion by 2031, reflecting a 10.01% CAGR over 2026-2031.

Which vehicle category is adopting trailer assist technology the fastest?

Passenger cars lead with a 67.04% revenue share in 2025 and are forecast to grow at an 11.57% CAGR as millennials and Gen Z towing demand expands.

How do regulatory mandates influence adoption decisions?

UNECE and NHTSA rules require enhanced trailer safety detection ranges, pushing OEMs to integrate surround-view cameras and sensor fusion suites sooner than planned.

How does adverse weather affect system reliability?

Heavy rain can cut LiDAR range by up to 80% and collapse camera visibility, prompting OEMs to add redundant sensors and AI vision algorithms that partly offset the loss.

Page last updated on: