Truck Trailer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

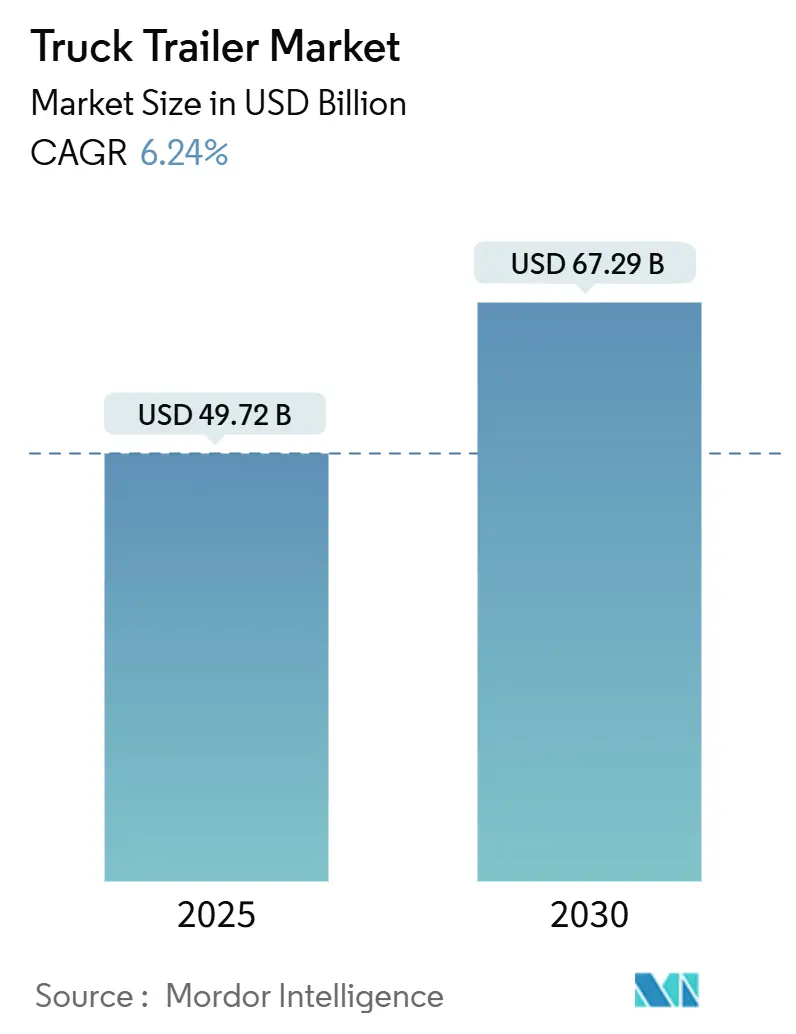

| Market Size (2025) | USD 49.72 Billion |

| Market Size (2030) | USD 67.29 Billion |

| Growth Rate (2025 - 2030) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Truck Trailer Market Analysis by Mordor Intelligence

The Truck Trailer Market size is estimated at USD 49.72 billion in 2025, and is expected to reach USD 67.29 billion by 2030, at a CAGR of 6.24% during the forecast period (2025-2030). Continued e-commerce parcel growth, infrastructure build-outs, and fleet digitalization collectively expand addressable demand while keeping the truck trailer market resilient to cyclical freight swings. Parcel networks favor high-throughput dry vans, construction programs lift flatbed and lowboy volumes, and cold-chain mandates accelerate refrigerated trailer uptake. At the same time, lightweight composites and aluminum alloys trim tare weight to preserve fuel efficiency under tightening axle limits, and smart telematics elevate asset utilization by linking trailers to real-time load-matching platforms. Competitive white-space surrounds hydrogen-powered refrigeration and autonomous ready chassis, positioning innovators to gain share as regulation and sustainability targets converge.

Key Report Takeaways

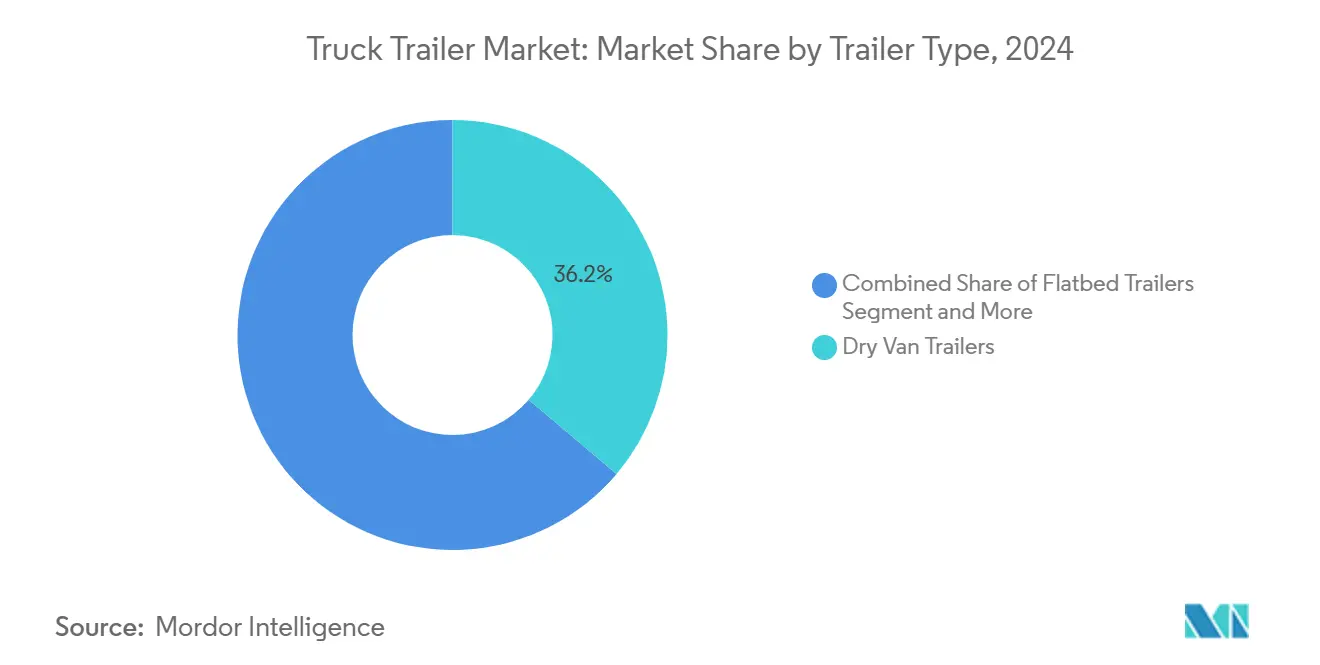

- By trailer type, dry vans held 36.17% of the truck trailer market share in 2024 while refrigerated trailers are projected to expand at a 6.26% CAGR through 2030.

- By material, steel accounted for 63.22% of the truck trailer market share in 2024; composites are forecast to post a 6.28% CAGR to 2030.

- By tonnage capacity, the 25–50 ton range captured 41.28% of the truck trailer market share in 2024, whereas the sub-25 ton bracket is poised for a 6.37% CAGR through 2030.

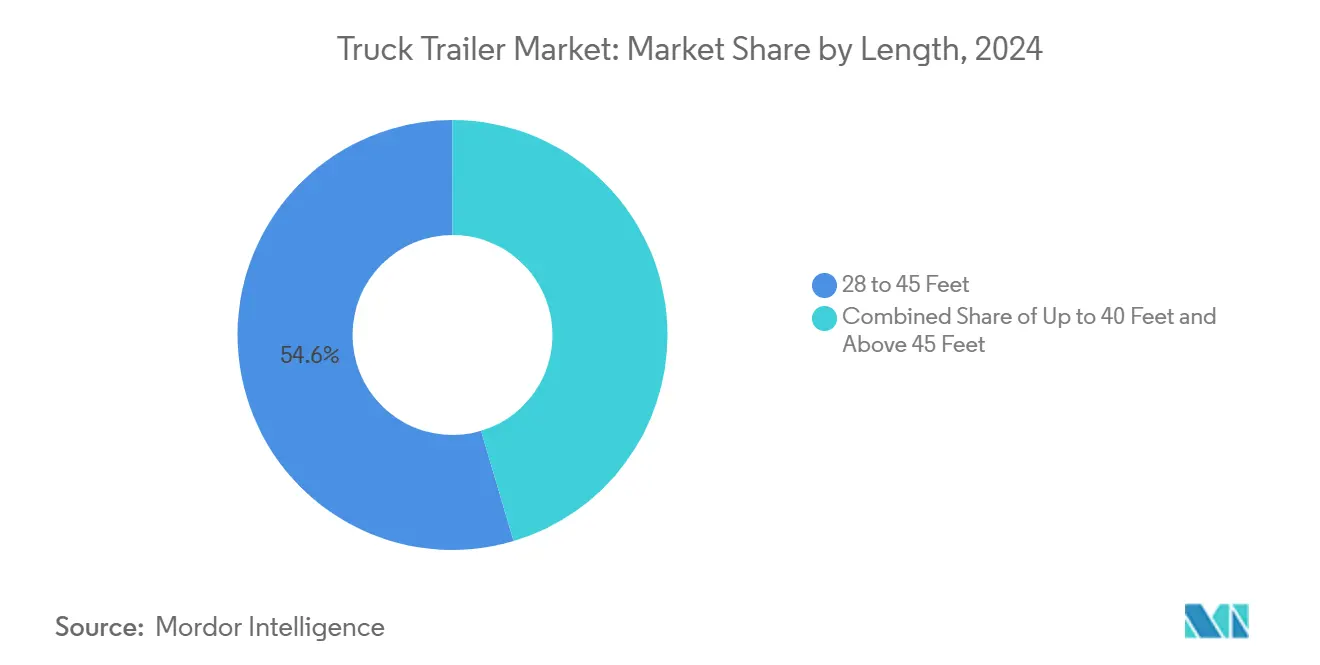

- By length, 28–45 ft units commanded 54.56% of the truck trailer market size in 2024; trailers up to 40 ft are expected to advance at a 6.39% CAGR to 2030.

- By end-use industry, retail and e-commerce represented 34.11% of the truck trailer market size in 2024 and are projected to grow at a 6.31% CAGR through 2030.

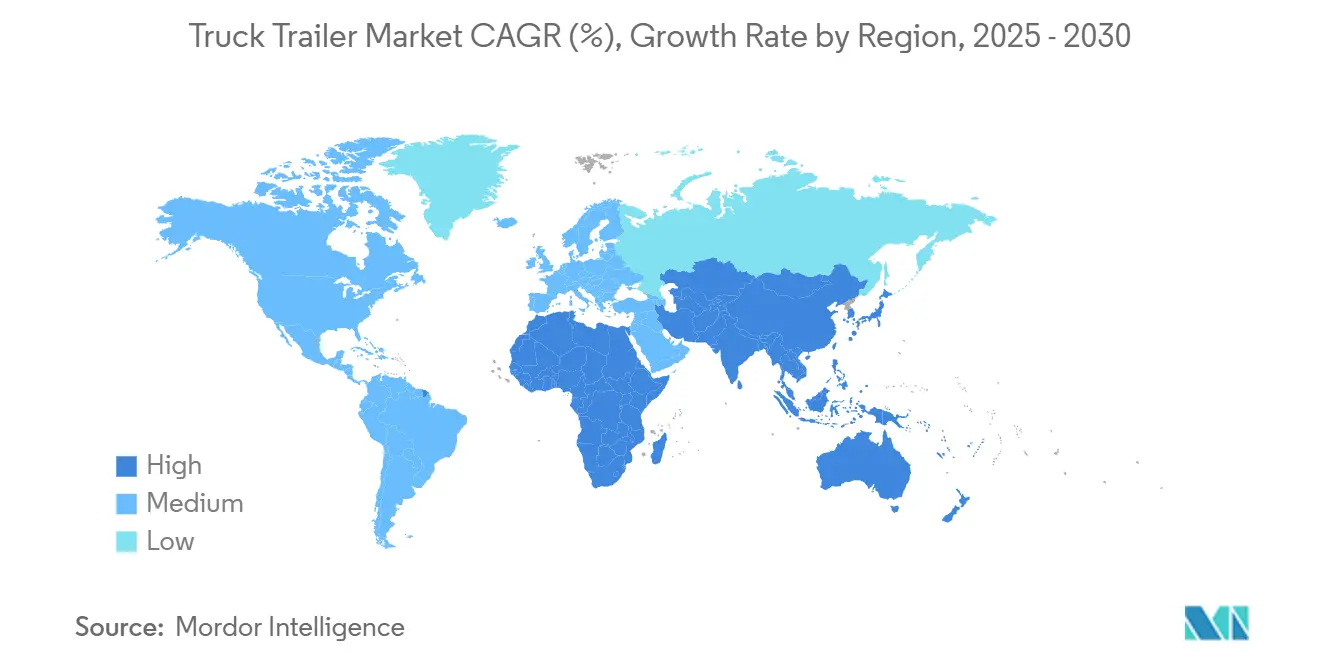

- By geography, Asia-Pacific led with 38.74% truck trailer market share in 2024 while expanding at a 6.34% CAGR to 2030.

Global Truck Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Driven Parcel Volumes | +1.8% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Infrastructure & Construction Up-Cycle | +1.2% | Asia Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Cold-Chain Network Expansion | +0.9% | Global, early gains in developed markets | Medium term (2-4 years) |

| Fleet Renewal To Lightweight Materials | +0.8% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Smart Telematics | +0.6% | North America and EU core markets | Short term (≤ 2 years) |

| Hydrogen-Powered Refrigeration Adoption | +0.4% | EU and North America pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Parcel Volumes

Parcel networks built for same-day fulfillment rely on dense shuttle loops between micro-fulfillment centers and sorting hubs, increasing dry van turns per day. Amazon’s rollout of branded trailers for Prime fulfillment demonstrates how retailers internalize capacity to safeguard service levels[1]“Sustainability and Transportation Updates,” Amazon, amazon.com. Standard dock-height configurations enable rapid cross-docking while lift-gate equipped rigs improve urban drop density. Simultaneously, packaging right-sizing drives demand for trailers with adjustable e-track and logistics posts that accommodate mixed carton heights. Real-time location and dwell-time analytics help fleet managers cycle trailers through regional hubs more efficiently, shrinking idle time and releasing latent capacity.

Infrastructure & Construction Up-Cycle

New road, rail, and renewable-energy projects in China, India, and Southeast Asia keep flatbed and lowboy assembly lines busy. China’s Belt and Road Initiative channels bulk cement, structural steel, and turbine blades across trans-continental corridors, elevating demand for extendable and multi-axle trailers[2]“Belt and Road Project Logistics Data,” Ministry of Commerce PRC, gov.cn. India’s National Infrastructure Pipeline lists 9,000+ projects, prompting local fleets to upsize to 51–100 ton rigs for heavy equipment haulage. Wind farm build-outs need blade carriers with hydraulic steering to negotiate rural access roads, while solar farm developers favor drop-frame flatbeds that maximize module stack density. Long-term public-private funding visibility allows OEMs to plan localized weld and paint capacity near project clusters.

Cold-Chain Network Expansion

Pharmaceutical distributors now embed GDP (Good Distribution Practice) protocols into trailer procurement, requiring temperature mapping and data-logging across every pallet position. Carrier Transicold’s hydrogen cell reefers cut in-route emissions and extend cold-soak endurance, giving fleets both compliance and ESG upside[3]“Hydrogen Fuel Cell Reefer Trials,” Carrier Transicold, carrier.com. Grocery retailers add multi-temperature bulkheads so frozen, chilled, and ambient SKUs travel in a single drop to dark-store fulfillment nodes. Pandemic-era vaccine corridors matured into permanent cold-chain lanes, allowing OEMs to justify insulated panel assembly lines in emerging markets. Aggregators of cloud kitchens and meal-kits also source compact reefer trailers compatible with class-B tractors for city distribution.

Fleet Renewal to Lightweight Materials

Composite sidewalls and aluminum cross-members shave up to 450 kg from a 53 ft dry van, equivalent to minimal fuel savings on North American long-haul routes. Wabash National’s molded structural composite panels resist corrosion, extending service life beyond 15 years and lowering total cost of ownership. Fleet operators respond to carbon-pricing schemes by valuing payload-per-kg metrics, pushing steel-dominant designs toward price-sensitive buyer niches. Adoption cascades from grocery and parcel carriers into regional LTL fleets as repair networks become familiar with composite patch kits. Meanwhile, material suppliers co-locate curing ovens at OEM clusters to trim logistics costs on bulky molded parts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel & Aluminium Prices | -0.7% | Global, acute in manufacturing hubs | Short term (≤ 2 years) |

| Axle-Weight Regulatory Limits | -0.5% | North America and EU core markets | Medium term (2-4 years) |

| Shortage Of Certified Trailer Mechanics | -0.4% | Global, severe in developed markets | Medium term (2-4 years) |

| Cyber-Security Risks | -0.3% | North America and EU, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Steel & Aluminum Prices

Benchmark hot-rolled coil swung two-fifth in 2024, compressing OEM gross margins and complicating long-term order-book pricing. Aluminum import tariffs in the United States added USD 250 per ton, narrowing the cost delta between aluminum and composite builds. Manufacturers resorted to quarterly price-adjustment clauses, but smaller dealers struggled to pass surcharges to end users. Hedging contracts partially offset exposure yet demanded cash collateral that tied up working capital. In response, some fleets delayed replacement cycles, temporarily softening demand until raw material pricing stabilized.

Axle-Weight Regulatory Limits

The U.S. Federal Bridge Formula caps axle group loads, pressing engineers to distribute weight over additional axles or adopt pusher configurations that raise build cost. Within Europe, member-state variance forces cross-border haulers to under-load trailers to meet the strictest limit encountered on a given lane, eroding payload efficiency. Enforcement cameras with weigh-in-motion sensors increased fine incidence, prompting fleets to specify on-board scales. Lobbying for harmonized 44-ton gross limits across EU corridors progresses, but consensus remains elusive, keeping design and operational complexity high for international operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trailer Type: Dry Van Leadership and Reefer Momentum

Dry vans retained 36.17% of the truck trailer market share in 2024, underscoring their fit for cube-oriented parcel and general merchandise loads. Refrigerated trailers, while capturing a smaller base, are projected for a 6.26% CAGR through 2030, outpacing all other categories as fresh grocery and pharma volumes multiply. Flatbeds continue serving construction steel, lumber, and machinery shipments where side or top loading is critical, while lowboys satisfy oversize excavator moves for infrastructure projects. Tankers remain essential for hazardous liquids, and extendable blade carriers gain prominence in wind-energy corridors.

E-commerce operators retrofit dry vans with captive logistics posts and load bars to accelerate parcel cube density. In contrast, cold-chain specialists invest in multi-zone reefers leveraging hydrogen or electric standby systems to comply with city emissions caps. Over the forecast period, the truck trailer market will see higher telematics penetration across every trailer type, enabling real-time load status and predictive maintenance scheduling. OEMs that bundle connectivity with standard warranty packages will likely secure sticky fleet contracts, further consolidating the fragmented supplier landscape.

By Material: Steel Sustains Volume, Composites Capture Premium

Steel builds commanded 63.22% of the truck trailer market share in 2024 due to cost competitiveness and well-established service networks. However, composite and aluminum variants will post a 6.28% CAGR, climbing toward one-third of new builds by 2030 as fleets chase fuel savings and corrosion resistance. Steel’s recyclability and upfront price advantage keep it entrenched in price-sensitive dry van fleets. Still, weight-sensitive reefer and tanker operators increasingly justify the higher capex of advanced materials through lower operating expenses.

Composite sandwich panels resist delamination and maintain insulation R-values longer than traditional steel skins, reducing life-cycle energy consumption. Meanwhile, hybrid designs combine steel coupler regions with aluminum side rails to balance cost and weight. Material suppliers collaborating with OEM design studios advance finite-element modeling to optimize panel lay-ups, ensuring strength margins without over-engineering. As sustainability procurement policies spread, life-cycle assessments will tilt more orders toward alternative materials, gradually rebalancing the truck trailer market size shares between steel and composites.

By Tonnage Capacity: Mid-Range Efficiency Prevails

Trailers rated 25 to 50 tons secured 41.28% of the truck trailer market share in 2024, reflecting their alignment with regional distribution weight bands and regulatory constraints. Sub-25-ton trailers will expand at a 6.37% CAGR, fueled by urban consolidation centers that favor lighter rigs capable of maneuvering narrow streets and curbside docks. At the high end, 51–100 ton and super-heavy segments remain vital for energy, mining, and construction logistics, though their volume growth lags the mid-range as infrastructure megaprojects phase between planning and execution cycles.

Regulators tighten axle-weight enforcement, pressuring fleets to right-size capacity, preventing over-specification and empty-backhaul inefficiencies. Lightweight material adoption amplifies payload potential within each capacity band, helping fleets offset the weight added by emissions-control hardware. Over the forecast horizon, telematics-enabled load monitoring will let dispatchers allocate the correct tonnage class to each shipment, minimizing fuel burn and non-revenue miles across the broader truck trailer market.

By Length: Standard 28–45 ft Dominance Meets Compact Growth

Standard 28 to 45 ft configurations held 54.56% of the truck trailer market share in 2024, mirroring dock heights and intermodal rail compatibility across North America and Europe. Yet trailers under 40 ft will log a 6.39% CAGR as cities impose curb-space fees and right-turn restrictions that penalize long wheelbases. Conversely, segments exceeding 45 ft stay essential for volumetric loads such as insulation panels and furniture, but face little regulatory headroom for length extensions.

Fleet route modeling increasingly integrates GIS restrictions, recommending compact trailers for congested districts during peak hours. OEMs answer with modular chassis inserting or removing center bays, offering fleets a single asset class for urban and regional lanes. Over time, standardization pressure around parcel cube dimensions may tilt future design norms toward a 32-ft sweet spot, redistributing shares inside the truck trailer industry’s length segments.

By End-Use Industry: Retail & E-Commerce Outpace Traditional Verticals

Retail and e-commerce maintained 34.11% of the truck trailer market size in 2024, riding omnichannel demand for blended store and direct-to-consumer fulfillment. They will continue at a 6.31% CAGR as same-day delivery footprint widens beyond tier-1 cities. Food and beverage shippers trail closely, underpinning reefer demand via fresh-produce and meal-kit growth. Construction sites underpin flatbed lift, whereas oil, gas, and chemical consignors count on tankers equipped with multi-compartment safety systems.

Digitalization reshapes every end-use vertical: retailers integrate IoT tags for SKU-level visibility, agribusiness deploys sensor-fitted grain hoppers that monitor moisture in transit, and petrochemical fleets link ELD data to ESG dashboards. End-users now mandate predictive uptime guarantees in procurement RFPs, nudging OEMs to embed analytics into base specifications. As sustainability auditing tightens, customers scrutinize life-cycle emissions, favoring trailer builders that certify low-carbon steel sourcing or offer hydrogen-ready reefer lines.

Geography Analysis

Asia-Pacific led the truck trailer market with a 38.74% of the truck trailer market share in 2024, anchored by China’s manufacturing corridor and India’s GST-enabled logistics consolidation. The region is forecast to have the highest 6.34% CAGR through 2030 as e-commerce penetration rises and infrastructure spending sustains heavy-haul demand. Government incentives supporting Euro-VI equivalent emission norms accelerate fleet replacement cycles, providing incremental upside to regional OEM output.

North America ranks second in volume and remains a bellwether for telematics adoption and lightweight material penetration. The United States drives composite uptake among large parcel carriers, while Canada’s resource-based economy sustains demand for multi-axle tankers and bulk trailers. The USMCA framework simplifies cross-border capacity rebalancing, enabling fleets to reposition assets between regions to absorb seasonal freight surges without newbuild purchases.

Europe prioritizes sustainability, pushing OEMs toward recyclable composites and alternative-fuel refrigeration units to align with the EU Green Deal. Member-state axle-weight disparities complicate long-haul routings, but corridor harmonization efforts may unlock standardized 44-ton gross limits within the forecast window. The United Kingdom recalibrates supply chains post-Brexit, importing more finished trailers while nurturing domestic refurb capacity to extend asset life amid import tariffs. Emerging Eastern European assemblers target price-sensitive fleets by leveraging lower operating costs, challenging incumbents in the western core.

Competitive Landscape

The truck trailer market remains moderately fragmented, with regional champions retaining scale advantages yet facing rising technology thresholds. CIMC leverages China-based manufacturing scale to supply Asia Pacific and export markets, while Wabash National differentiates via composite body patents that lower tare weight and maintenance cost. Schmitz Cargobull invested heavily in IoT-enabled digital services, such as bundling sensor hardware with predictive maintenance subscriptions. TerraVest’s purchase of EnTrans consolidates specialty tanker and cryogenic trailer capabilities under one North American platform.

Strategic alliances blossom around hydrogen refrigeration pilots, pairing trailer OEMs with fuel-cell integrators and grocery fleets seeking zero-emission cold chains. Private-equity entrants hunt roll-up plays among regional builders unlikely to fund their own telematics roadmaps. Meanwhile, start-ups focusing on autonomous-ready dollies and self-powered chassis attract venture funding, though regulatory timelines temper near-term revenue impact. Steel and aluminum price volatility favors vertically integrated producers that hedge material inputs, pressuring smaller fabricators to outsource panel kits and narrow product lines.

OEMs that secure ISO 9001 and Advance Quality Planning certifications erect compliance walls against new entrants and win long-term contracts with global parcel networks. Digital twins of trailer builds shorten engineering lead-times, boosting make-to-order throughput for customized specs. Over the outlook period, success hinges on pairing manufacturing scale with software-centric service bundles that lift revenue per unit and lock in customers on multi-year data subscriptions.

Truck Trailer Industry Leaders

CIMC Vehicles (Group) Co., Ltd.

Wabash National Corporation

Schmitz Cargobull AG

Fahrzeugwerk Bernard Krone GmbH

Hyundai Translead

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TerraVest Industries completed the acquisition of EnTrans International for USD 546 million, expanding production capacity and specialty tanker coverage across North America.

- October 2024: Schmitz Cargobull AG invested EUR 50 million in IoT sensor and predictive maintenance integration, enhancing its smart logistics service portfolio.

Global Truck Trailer Market Report Scope

| Dry Van Trailers |

| Flatbed Trailers |

| Refrigerated (Reefer) Trailers |

| Lowboy Trailers |

| Tankers |

| Extendable Trailers |

| Steel |

| Aluminum |

| Composite Materials |

| Below 25 Tons |

| 25 to 50 Tons |

| 51 to 100 Tons |

| Above 100 Tons |

| Up to 40 Feet |

| 28 to 45 Feet |

| Above 45 Feet |

| Food & Beverage |

| Construction |

| Oil & Gas |

| Agriculture |

| Retail & E-Commerce |

| Chemicals |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Trailer Type | Dry Van Trailers | |

| Flatbed Trailers | ||

| Refrigerated (Reefer) Trailers | ||

| Lowboy Trailers | ||

| Tankers | ||

| Extendable Trailers | ||

| By Material | Steel | |

| Aluminum | ||

| Composite Materials | ||

| By Tonnage Capacity | Below 25 Tons | |

| 25 to 50 Tons | ||

| 51 to 100 Tons | ||

| Above 100 Tons | ||

| By Length | Up to 40 Feet | |

| 28 to 45 Feet | ||

| Above 45 Feet | ||

| By End-Use Industry | Food & Beverage | |

| Construction | ||

| Oil & Gas | ||

| Agriculture | ||

| Retail & E-Commerce | ||

| Chemicals | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the truck trailer market by 2030?

The market is expected to reach USD 67.29 billion by 2030.

Which trailer type is growing the fastest?

Refrigerated trailers are projected to grow at a 6.26% CAGR through 2030.

How large is Asia-Pacific’s share today?

Asia-Pacific holds 38.74% of global revenue and is the fastest-growing region.

Why are composites gaining popularity in trailer builds?

Composites reduce tare weight, resist corrosion, and lower fuel consumption, driving a 6.28% CAGR in adoption.

What impact do steel and aluminum prices have on manufacturers?

Price volatility compresses margins, forcing OEMs to adopt hedging and dynamic pricing strategies.

Which technology trend offers new revenue streams for trailer OEMs?

Integrated telematics and predictive maintenance subscriptions boost lifetime revenue per unit and differentiate offerings.

Page last updated on: