Modular Trailer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

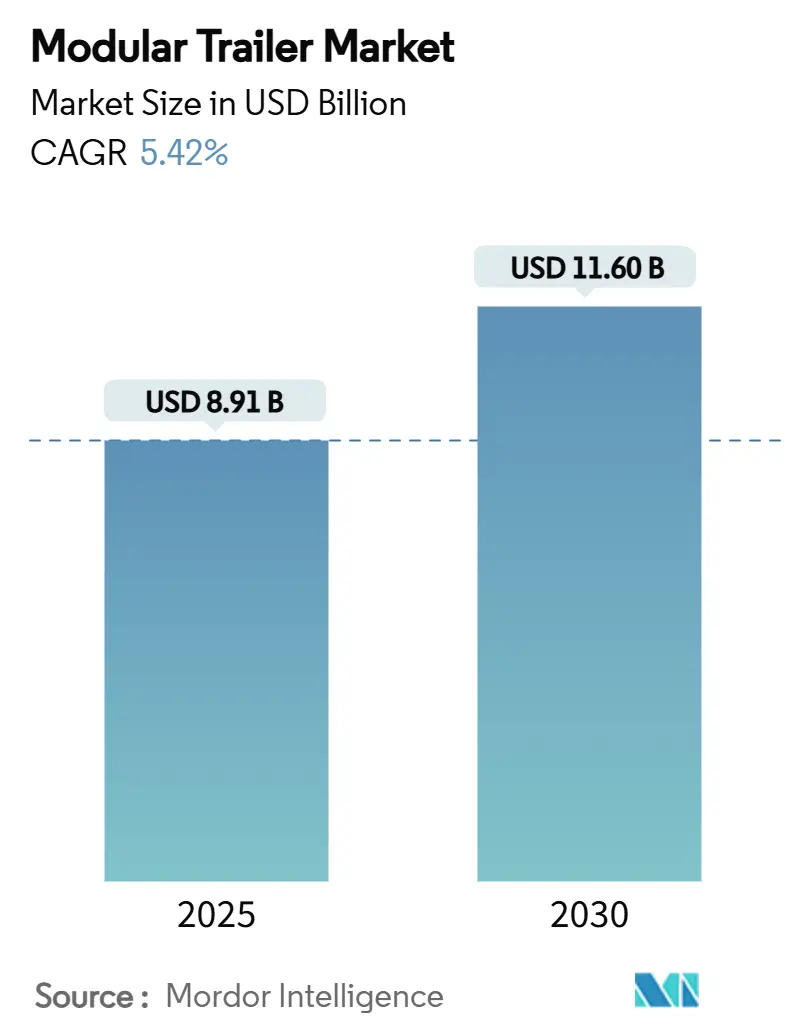

| Market Size (2025) | USD 8.91 Billion |

| Market Size (2030) | USD 11.60 Billion |

| Growth Rate (2025 - 2030) | 5.42% CAGR |

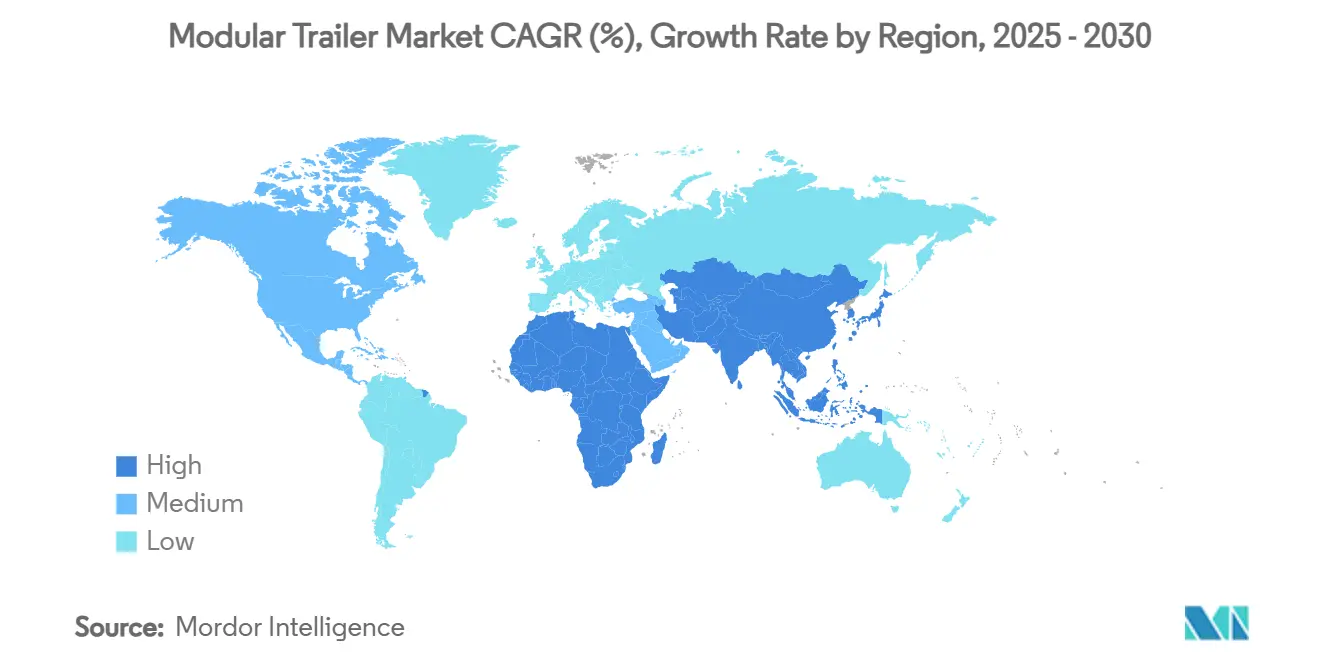

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Modular Trailer Market Analysis by Mordor Intelligence

The modular trailer market is poised to be at USD 8.91 billion in 2025 and is forecast to reach USD 11.60 billion by 2030, registering a 5.42% CAGR over the period. Stricter EU CO₂ limits, surging wind-energy logistics, and rapid adoption of innovative telematics collectively underpin this expansion. North America commands the largest 32.05% modular trailer market share, benefitting from mature heavy-haul corridors, while Asia-Pacific is projected to post the fastest 7.80% CAGR on the back of a USD 26 trillion infrastructure drive. OEMs are investing in lightweight chassis to meet the mandated 7.5%/10% CO₂ cuts for drawbar and semi-trailers by 2030. Electrified axle solutions such as ZF’s AxTrax 2 deliver up to 16% fuel savings for diesel tractors and as much as 40% when operated in plug-in mode. However, persistent steel-price swings and a deepening shortage of certified heavy-haul drivers are weighing on profit margins and asset utilisation.

Key Report Takeaways

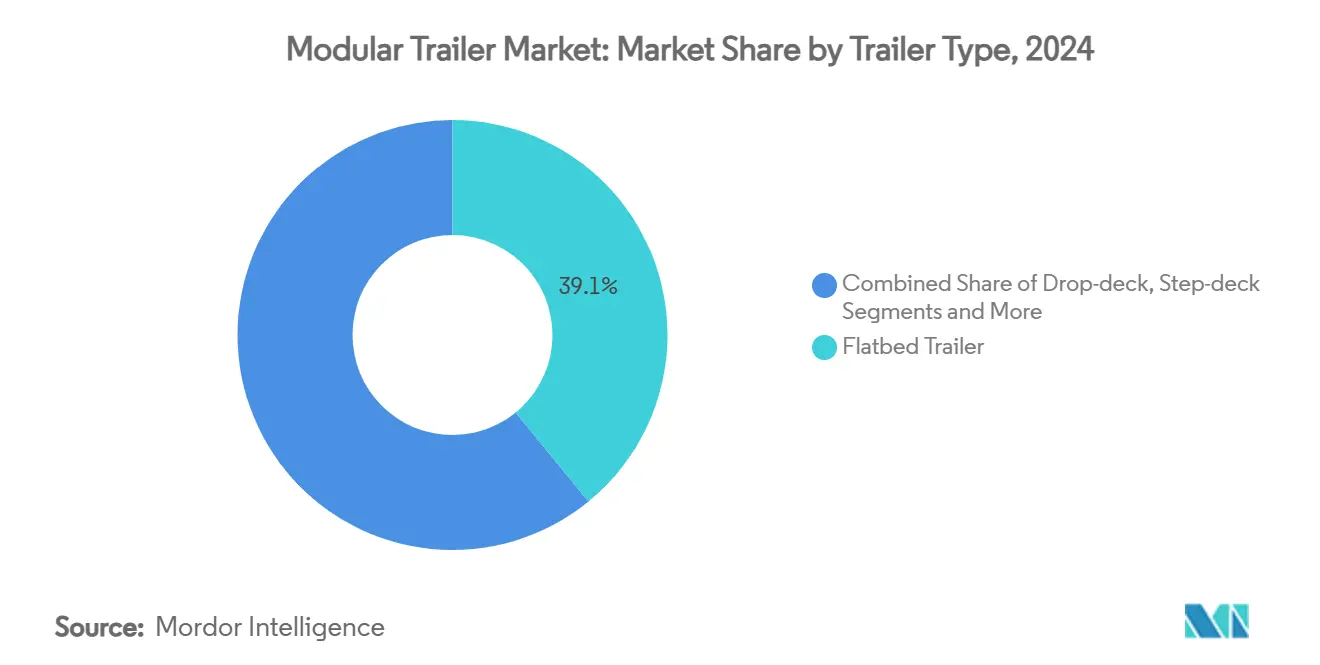

By trailer type, flatbed units held 39.05% of modular trailer market share in 2024, whereas low-boy platforms are forecast to advance at an 8.20% CAGR through 2030.

By axle configuration, tandem systems captured 46.28% share of the modular trailer market size in 2024, while quad and above assemblies are projected to expand at a 7.55% CAGR to 2030.

By material, carbon-steel dominated with 70.95% modular trailer market share in 2024; aluminum frames are expected to grow at a 6.90% CAGR during the forecast window.

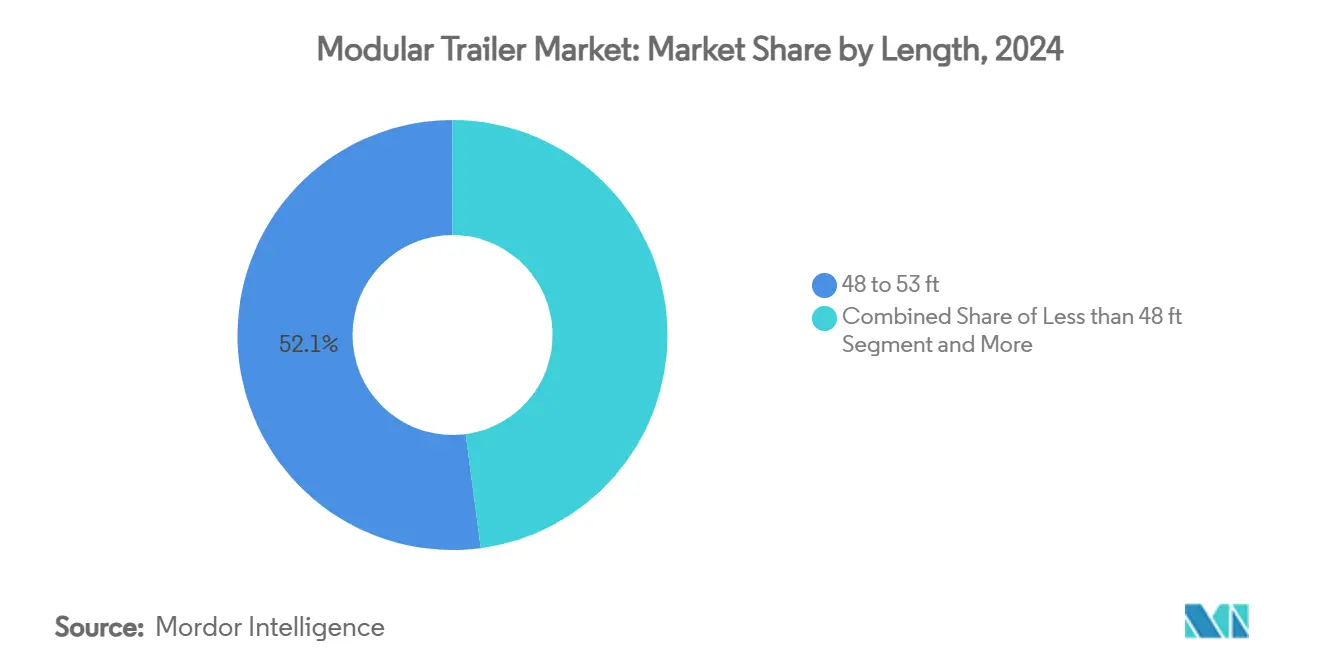

By length, the 48 to 53 ft category commanded 52.10% share of the modular trailer market size in 2024, and trailers longer than 60 ft are set to grow at a 9.31% CAGR up to 2030.

By end-user industry, construction and infrastructure led with 24.12% revenue share in 2024, whereas wind-energy logistics is projected to rise at an 11.30% CAGR through 2030.

By geography, North America accounted for 32.05% of the modular trailer market share in 2024, while Asia-Pacific is anticipated to deliver the fastest 7.80% CAGR over 2025-2030.

Global Modular Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wind-Blade Logistics Spurring Extendable Trailers | +1.2% | North America, Europe, APAC | Medium term (2-4 years) |

| Southeast Asian Mega-Infrastructure Corridors | +0.9% | APAC, spill-over to MEA | Long term (≥ 4 years) |

| Lightweight Aluminium-Steel Hybrid Chassis | +0.8% | Europe, North America, Global | Medium term (2-4 years) |

| EU CO₂ Trailer Rules (EU 2019/1242) | +0.7% | Europe, Global influence | Short term (≤ 2 years) |

| Smart-Sensor Telematics Lowering TCO | +0.6% | North America, Global | Short term (≤ 2 years) |

| Rare-Earth-Free E-Axle Modules | +0.4% | Europe, North America, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Wind-Blade Logistics Driving Extendable Modular Trailers

Wind turbine blade transportation demands are fundamentally reshaping trailer design specifications as modern blades exceed 80 meters in length and entire assemblies surpass 700 tons in weight. Route planning complexity intensifies with each project requiring multiple visual inspections and swept path analyses to navigate infrastructure constraints, as demonstrated by the Southland Wind Farm in New Zealand and Golden Plains Wind Farm in Australia[1] Luke Smith, Josh Tracey and Andrew Metherell, " Overcoming challenges in wind turbine transportation: Why route assessments are critical," Stantec, stantec.com.. Manufacturers are responding by developing modular systems that extend beyond traditional length limits while maintaining structural integrity for oversized component delivery. The complexity of wind blade logistics creates barriers to entry for smaller fabricators, consolidating market share among specialized heavy-haul providers with engineering capabilities.

Growth of South-East Asian Mega-Infrastructure Corridor Projects

Southeast Asia's infrastructure transformation requires over USD 26 trillion in transport investments through 2030, with freight transport demand projected to increase nearly 80% between 2015 and 2030[2]Yasuyuki Sawada, "Asia’s Next Infrastructure Boom," ADB, adb.org. . The Southern Economic Corridor connecting Bangkok, Phnom Penh, and Ho Chi Minh City exemplifies this shift, facilitating cross-border trade and private sector participation in logistics infrastructure. Cambodia's Industrial Development Policy emphasizes multimodal transport systems, including the National Road No. 5 Improvement Project enhancing logistics capacity between Phnom Penh and the Thai border. Maritime shipping accounts for 90% of freight ton-kilometres in the region, creating demand for specialized port-to-inland transport solutions. The region's focus on special economic zones and simplified customs procedures drives demand for container chassis and intermodal trailer configurations.

OEM Pivot to Lightweight Aluminum-Steel Hybrid Chassis

Material innovation accelerates as manufacturers pursue weight reduction strategies to enhance payload capacity and fuel efficiency, with high-strength steel achieving 10% weight reductions in commercial vehicles and 30% savings in main frame components. Constellium's participation in Project M-LightEn demonstrates industry commitment to ultra-lightweight chassis structures, targeting 50% carbon intensity reduction and 25% weight savings using 80% recycled aluminum materials. CarbonTT's CFRP chassis development achieved 185-kilogram weight reduction and 36% payload increase for specialized commercial vehicles, addressing urban logistics constraints under 3.5 MT weight limits[3]Stewart Mitchell, "Pultruded CFRP chassis enables 36% payload increase for specialized commercial vehicles," Composites Worlds, compositesworld.com.. Great Dane's carbon-fiber concept trailer demonstrated 4,000-pound weight savings compared to conventional designs, with carbon fiber costs declining to approximately USD 10 per pound[4]Ryan Gehm, "Carbon-fiber concept trailer from Great Dane cuts weight by 4000 lb," SAE International, sae.org..

Tightening EU CO₂ Trailer Compliance Rules (EU 2019/1242)

European Union regulations mandate CO₂ emission reductions of 7.5% for drawbar trailers and 10% for semi-trailers by 2030, with broader heavy-duty vehicle targets reaching 90% by 2040. The Vehicle Energy Consumption Calculation Tool (VECTO) implementation requires manufacturers to demonstrate compliance through aerodynamic optimization, weight reduction, and tire rolling resistance improvements. Financial penalties for non-compliance reach EUR 4,250 per gCO2/tkm in 2025 and EUR 6,800 in 2030, creating immediate cost pressures for manufacturers. Schmitz Cargobull's S.KOe COOL fully electric refrigerated trailer exemplifies compliance strategies, meeting zero-emission urban logistics requirements. The regulation's technology-neutral approach allows manufacturers flexibility in compliance methods while incentivizing zero-emission vehicle integration. Road charging advantages for efficient trailers provide operational cost benefits, promoting market uptake of compliant designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Heavy-Haul Drivers | -1.1% | North America, Europe, Global | Medium Term (2–4 Years) |

| Slow Homologation of Autonomous Trailer Control Systems | -1.0% | Europe, North America | Long Term (4+ Years) |

| Volatile Steel Prices | -0.8% | Global, Pronounced in Emerging Markets | Short Term (≤ 2 Years) |

| Port Bottlenecks Delaying Oversized-Cargo Permits | -0.7% | Global Seaports, Especially Asia and EU | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices Squeezing Small Regional Fabricators

Small regional fabricators face disproportionate impacts due to limited hedging capabilities and reduced negotiating power with steel suppliers compared to large OEMs. Tariffs on steel and aluminum imports compound cost pressures, with some manufacturers exploring supplier diversification and reshoring strategies to mitigate supply chain disruptions. The delay in tariff implementation until April 2025 provides temporary relief but maintains uncertainty for production planning and pricing strategies. Carbon steel's 70.95% market dominance amplifies price sensitivity across the industry, particularly affecting smaller players with limited material alternatives. Manufacturers adapt through inventory management optimization and strategic supplier partnerships, though margin compression remains inevitable during volatile periods.

Shortage of Certified Heavy-Haul Drivers Globally

The United States faces a driver shortage exceeding 80,000 positions, projected to double by 2030 due to retirement, stress, and fatigue factors affecting the profession. Heavy-haul operations require specialized certifications and experience with oversized cargo permits, creating additional barriers to driver recruitment and retention. The shortage particularly impacts modular trailer utilization rates, as qualified operators command premium wages and limit fleet deployment flexibility. Autonomous trailer development accelerates as a response, with companies like Aurora and Waymo seeking regulatory exemptions for safety equipment modifications. Driver-as-a-Service and Capacity-as-a-Service business models emerge to address workforce constraints while maintaining operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trailer Type: Flatbed Trailer Dominance Amid Low-Boy Acceleration

Flatbed trailers maintained 39.05% market share in 2024, reflecting their versatility across general freight applications and established supply chain integration. Low-boy configurations emerge as the fastest-growing segment at 8.20% CAGR through 2030, driven by wind energy logistics and heavy machinery transport demands requiring specialized loading capabilities. Flatbed trailers serve construction and infrastructure projects, particularly benefiting from Asia-Pacific's USD 26 trillion infrastructure investment pipeline. Drop-deck and step-deck configurations address height-restricted cargo while maintaining payload efficiency for industrial equipment transport.

Container chassis demand correlates with maritime trade volumes, as Southeast Asia's freight transport is projected to increase 80% through 2030. Tanker trailers benefit from oil and gas sector activity, though growth moderates due to energy transition pressures. ZF's TrailTrax electrification system demonstrates cross-segment applicability, achieving 16% energy savings for diesel applications and 40% improvements through plug-in charging. The segment's evolution reflects specialization trends, with manufacturers developing purpose-built solutions rather than one-size-fits-all approaches.

By Axle Configuration: Tandem Systems Lead While Quad-Plus Accelerates

Tandem axle configurations dominate with 46.28% market share in 2024, offering optimal weight distribution and maneuverability for standard freight operations across diverse road conditions. Quad and above configurations post 7.55% CAGR growth through 2030, driven by super-heavy cargo transport and wind turbine component delivery requiring maximum load distribution. Single axle systems serve lighter applications and urban delivery, while tridem configurations bridge capacity gaps for specialized industrial transport.

The shift toward heavier cargo loads necessitates advanced axle technologies, with Schmitz Cargobull celebrating production of its 2,000,000th axle in 2024 while implementing fully automated manufacturing processes. Electric generator axles gain traction as telematics integration expands, supporting smart trailer functionality and predictive maintenance capabilities. Regulatory compliance drives axle configuration optimization, as EU CO₂ standards require manufacturers to balance weight distribution with aerodynamic efficiency. Multi-axle systems enable modular design flexibility, allowing operators to configure trailers based on specific cargo requirements and route constraints.

By Material: Carbon-Steel Dominance Faces Aluminum Challenge

Carbon-steel maintains 70.95% market share in 2024 due to cost advantages and established manufacturing processes, though aluminum alternatives grow at 6.90% CAGR as weight reduction becomes critical for fuel efficiency and payload optimization. Hybrid aluminum-steel configurations emerge as compromise solutions, balancing weight savings with structural integrity requirements for heavy-duty applications. High-strength steel innovations achieve 10% weight reductions in commercial vehicles while maintaining durability standards.

Constellium's ultra-high-strength aluminum production using 80% recycled materials demonstrates sustainability integration with performance benefits. Carbon fiber applications remain niche but show promise, with Great Dane's concept trailer achieving 4,000-pound weight savings at declining material costs. Steel price volatility creates opportunities for alternative materials, though manufacturers must balance initial costs with lifecycle benefits. Material selection increasingly considers regulatory compliance, as EU emission standards incentivize weight reduction strategies across all trailer configurations.

By Length: Mid-Range Dominance With Extended Growth

Trailers measuring 48 to 53 feet command 52.10% market share in 2024, representing the industry standard for general freight and intermodal applications optimized for road infrastructure compatibility. Extended trailers exceeding 60 feet post the highest growth rate at 9.31% CAGR through 2030, driven by wind energy component transport and specialized industrial cargo requiring maximum length utilization. Sweden's approval of vehicle combinations exceeding 25.25 meters, including Nordic combinations reaching approximately 27 meters, demonstrates regulatory accommodation for longer configurations.

Shorter trailers under 48 feet serve urban delivery and specialized applications where maneuverability outweighs capacity considerations. The 53 to 60 feet segment balances capacity with regulatory compliance across diverse jurisdictions. Wind turbine blade transport drives demand for extendable configurations, as modern blades exceed 80 meters and require sophisticated route planning. Length optimization reflects operational efficiency priorities, with longer trailers reducing per-unit transport costs while shorter configurations enhance urban accessibility and parking flexibility.

By End-User Industry: Construction Leadership Amid Wind Energy Surge

Construction and infrastructure sectors command 24.12% market share in 2024, benefiting from global infrastructure investment programs and urbanization trends across developing markets. Wind energy emerges as the fastest-growing segment at 11.30% CAGR through 2030, reflecting renewable energy expansion and specialized transport requirements for turbine components exceeding conventional size limits. Oil and gas applications maintain steady demand despite energy transition pressures, while mining and metals benefit from critical mineral extraction initiatives, including the U.S. Department of Defense's USD 870 million investment in domestic supply chains.

Defense and aerospace applications require specialized configurations for military equipment transport, with Rheinmetall's TGS-Mil Protected demonstrating modular design capabilities for mission-specific requirements. Each end-user segment drives distinct trailer specifications, from wind energy's length requirements to defense sector's protection standards. The diversification across industries provides market stability while specialized segments command premium pricing for engineered solutions.

Geography Analysis

North America's 32.05% market share in 2024 reflects the region's mature heavy-haul infrastructure and established regulatory frameworks that facilitate oversized cargo transport across state boundaries. The United States faces critical challenges with over 80,000 driver shortages projected to double by 2030, accelerating autonomous trucking development with potential 13% adoption rates by 2035. Freight bottlenecks cause 243 million truck hours of delay annually, costing approximately USD 7.8 billion and driving infrastructure improvement initiatives. Canada benefits from resource extraction activities requiring specialized transport solutions, while Mexico's manufacturing sector expansion supports trailer demand growth.

Asia-Pacific emerges as the fastest-growing region with 7.80% CAGR through 2030, driven by Southeast Asia's infrastructure boom requiring over USD 26 trillion in transport investments through 2030. Freight transport demand is projected to increase nearly 80% between 2015 and 2030, with maritime shipping accounting for 90% of freight tonne-kilometres creating port-to-inland transport opportunities. The Southern Economic Corridor connecting Bangkok, Phnom Penh, and Ho Chi Minh City facilitates cross-border trade and logistics infrastructure development. China's manufacturing dominance and India's infrastructure development create substantial trailer demand, while Indonesia and other ASEAN nations benefit from regional connectivity improvements.

Europe maintains significant market presence while navigating stringent CO₂ compliance requirements mandating 7.5% emission reductions for drawbar trailers and 10% for semi-trailers by 2030. Sweden's approval of vehicle combinations exceeding 25.25 meters demonstrates regulatory adaptation to specialized transport needs. Germany leads manufacturing innovation with companies like Schmitz Cargobull investing over EUR 97 million in product development and sustainability initiatives while achieving 25% European market share. The region's focus on decarbonization drives electrification initiatives, with ZF's TrailTrax system achieving 16% energy savings for diesel applications.

Competitive Landscape

The modular trailer market exhibits moderate fragmentation with established European manufacturers maintaining leadership positions through technological innovation and manufacturing scale advantages. Schmitz Cargobull demonstrates market consolidation trends, increasing European market share while producing around 60,000 vehicles annually and generating EUR 2.4 billion in revenue. Strategic partnerships reshape competitive dynamics, as evidenced by Schmitz Cargobull's 26% stake acquisition in Australia's MaxiTRANS and Faymonville Group's Arkansas facility development targeting North American expansion. Technology differentiation accelerates through electrification initiatives, with ZF's TrailTrax system partnerships and Range Energy's eTrailer achieving up to USD 20,000 annual savings per trailer.

White-space opportunities emerge in autonomous trailer systems and smart telematics integration, as demonstrated by patent applications for bearing condition monitoring and power supply optimization technologies. Competitive intensity increases as manufacturers navigate regulatory compliance requirements, with EU CO₂ standards creating differentiation opportunities for companies developing aerodynamic and lightweight solutions. Smaller regional fabricators face margin pressure from steel price volatility and limited scale advantages, potentially accelerating industry consolidation. The emergence of Trailers-as-a-Service models, exemplified by Wabash's national network approach, challenges traditional ownership structures and creates new competitive dynamics focused on utilization optimization rather than asset sales.

Modular Trailer Industry Leaders

-

Schmitz Cargobull

-

Goldhofer

-

Faymonville

-

Scheuerle (TII Group)

-

Wabash National Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Trailer builder Montracon was acquired by investment firm Martin Group, with the new ownership committing to invest in the company's brand, people, and products while maintaining unchanged operations.

- February 2025: ZF and Range Energy announced partnership integration of ZF's AxTrax 2 e-axle into Range's eTrailer System, projecting USD 20,000 annual savings per trailer and 70% emission reductions with initial deliveries expected in 2025.

- January 2025: Schmitz Cargobull announced expansion of its delivery center for refrigerated and box body semi-trailers at Vreden site, creating 750 new parking spaces and reducing CO₂ emissions by approximately 150 tonnes annually.

Global Modular Trailer Market Report Scope

| Flatbed |

| Drop-deck |

| Step-deck |

| Low-boy |

| Tanker |

| Container Chassis |

| Single |

| Tandem |

| Tridem |

| Quad and Above |

| Carbon-steel |

| Aluminium |

| Hybrid Aluminium-Steel |

| Less than 48 ft |

| 48 to 53 ft |

| 53 to 60 ft |

| More than 60 ft |

| Construction and Infrastructure |

| Wind-Energy |

| Oil and Gas |

| Mining and Metals |

| Defense and Aerospace |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Trailer Type | Flatbed | |

| Drop-deck | ||

| Step-deck | ||

| Low-boy | ||

| Tanker | ||

| Container Chassis | ||

| By Axle Configuration | Single | |

| Tandem | ||

| Tridem | ||

| Quad and Above | ||

| By Material | Carbon-steel | |

| Aluminium | ||

| Hybrid Aluminium-Steel | ||

| By Length | Less than 48 ft | |

| 48 to 53 ft | ||

| 53 to 60 ft | ||

| More than 60 ft | ||

| By End-user Industry | Construction and Infrastructure | |

| Wind-Energy | ||

| Oil and Gas | ||

| Mining and Metals | ||

| Defense and Aerospace | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the modular trailer market?

The modular trailer market size equalled USD 8.91 billion in 2025 and is forecast to reach USD 11.60 billion by 2030.

Which region will grow fastest?

Asia-Pacific is projected to record the highest 7.80% CAGR through 2030 on the back of a USD 26 trillion infrastructure pipeline.

How are EU regulations affecting trailer design?

EU 2019/1242 obliges drawbar and semi-trailers to cut CO₂ by 7.5% and 10% respectively by 2030, spurring wider adoption of lightweight materials and aerodynamic kits.

Which trailer type is expanding most quickly?

Low-boy trailers are advancing at an 8.20% CAGR owing to heightened wind-energy and heavy-equipment transport needs.

Page last updated on: