Trailer Telematics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.26 Billion |

| Market Size (2030) | USD 2.15 Billion |

| Growth Rate (2025 - 2030) | 11.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

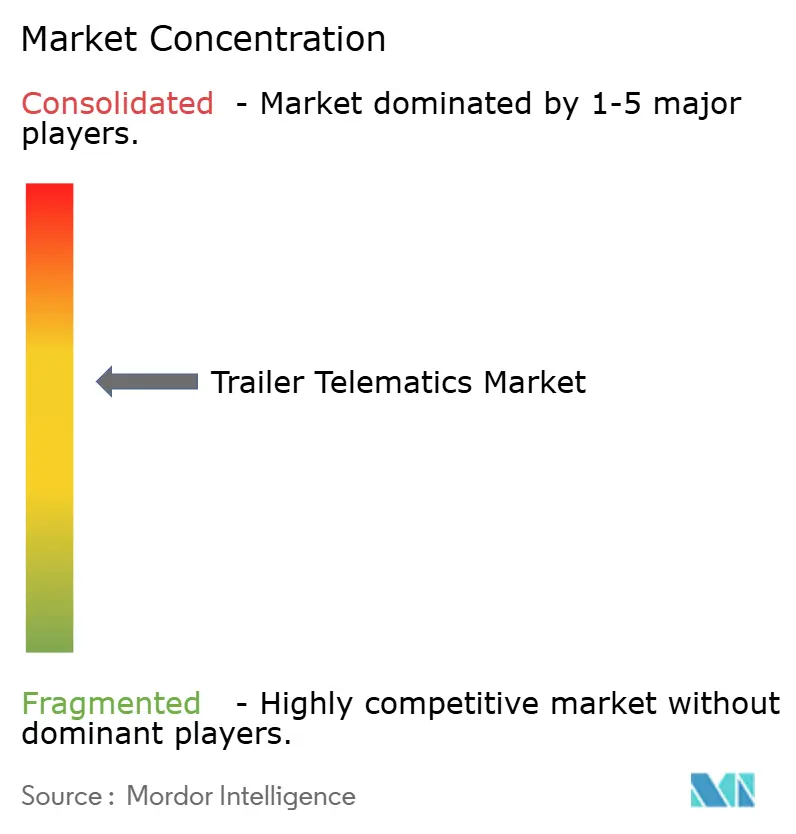

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trailer Telematics Market Analysis by Mordor Intelligence

The trailer telematics market size stood at USD 1.26 billion in 2025 and is projected to reach USD 2.15 billion by 2030, advancing at an 11.27% CAGR during the forecast period (2025-2030). Escalating regulatory demands, falling hardware and connectivity costs, and e-commerce–led logistics complexity are collectively elevating adoption rates across fleet classes. Software-centric propositions are outpacing hardware growth as cloud platforms, predictive analytics, and edge AI unlock asset-level optimization. Consolidation among leading vendors and OEM partnerships are reshaping competitive dynamics, while battery-electric refrigeration and sustainability mandates widen the solution scope. North America retains scale leadership, yet Asia-Pacific is racing ahead in growth on the back of rapid infrastructure upgrades and cold-chain investment.

Key Report Takeaways

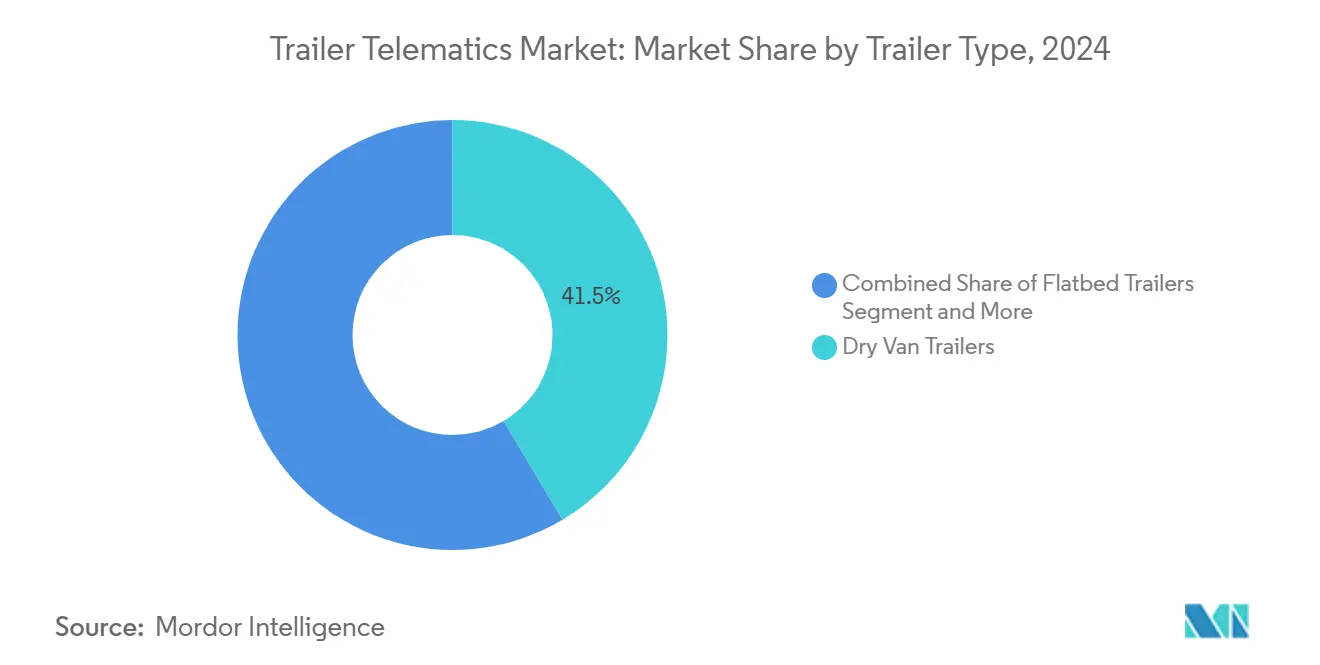

- By trailer type, dry van maintained a 41.45% share of the trailer telematics market in 2024, while refrigerated units are forecast to expand at a 13.36% CAGR through 2030.

- By communication technology, GPS tracking held 55.67% of the 2024 trailer telematics market share; cellular connectivity is projected to grow at a 15.85% CAGR to 2030.

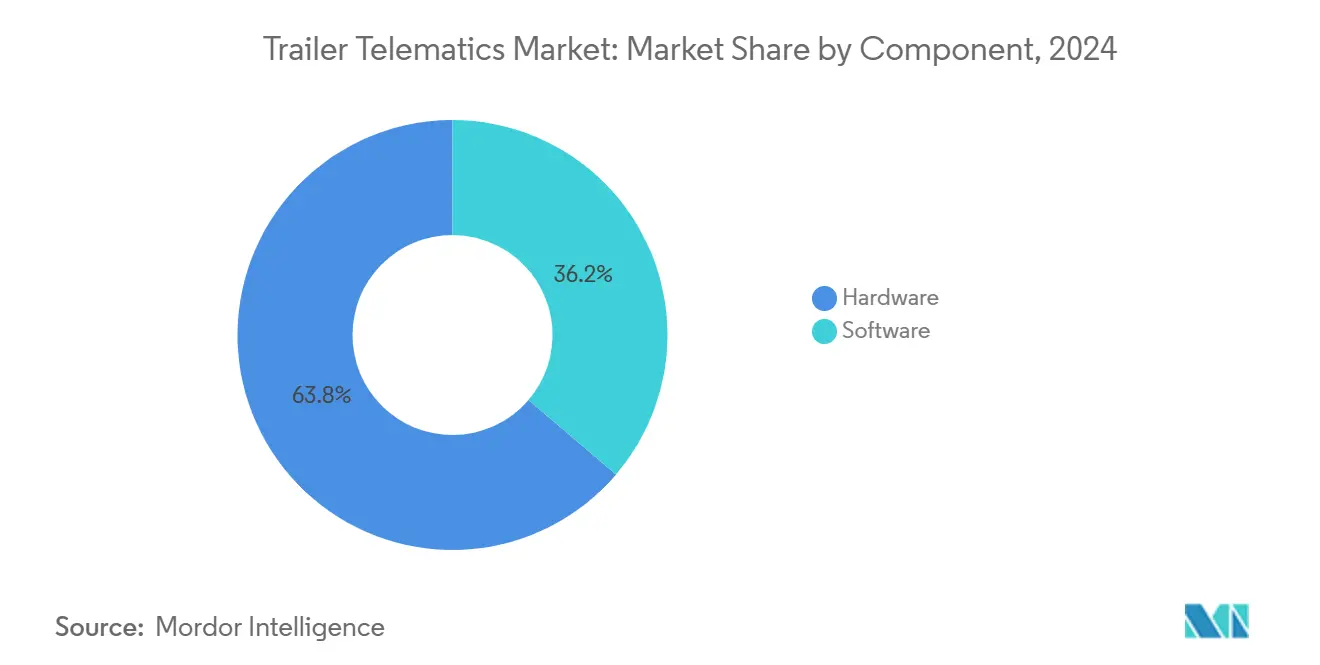

- By component, hardware commanded 63.76% of the trailer telematics market size in 2024, whereas software is set to scale at a 13.49% CAGR over the same period.

- By application, fleet management led with 47.57% revenue share of the trailer telematics market size in 2024; predictive maintenance is on course for a 15.42% CAGR to 2030.

- By deployment type, cloud-based solutions captured 69.84% of the 2024 trailer telematics market share, and the segment will progress at a 15.85% CAGR through 2030.

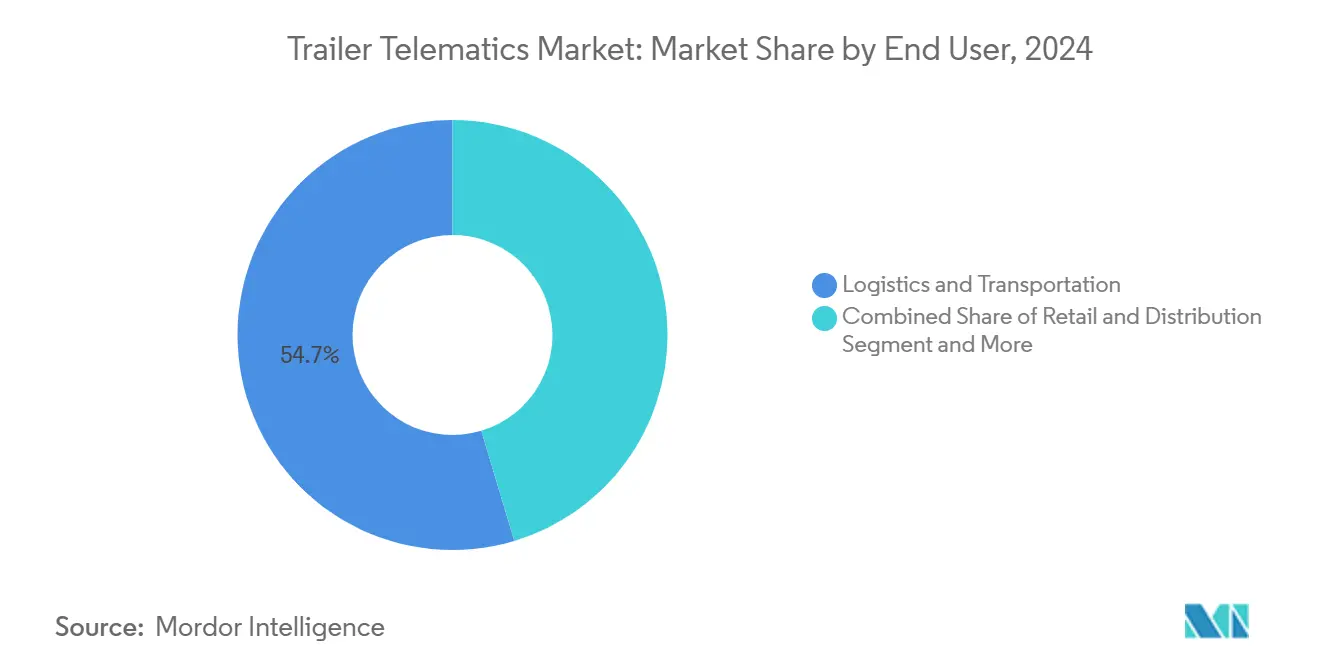

- By end user, logistics and transportation accounted for 54.65% of the trailer telematics market size in 2024, while retail and distribution is anticipated to rise at a 12.68% CAGR toward 2030.

- By distribution channel, aftermarket routes generated 61.74%of the trailer telematics market size in 2024; OEM-integrated systems are poised for a 12.31% CAGR up to 2030.

- By geography, North America captured 46.56% share of the trailer telematics market in 2024, while Asia-Pacific is projected to be the fastest growing at 11.76% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Trailer Telematics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time Fleet Visibility and Utilization Optimisation | +2.2% | Global, with highest adoption in North America and Europe | Medium term (2-4 years) |

| Regulatory Mandates | +1.8% | North America primary, expanding to APAC and South America | Short term (≤ 2 years) |

| Declining Hardware and Cellular Costs | +1.5% | Global, with accelerated impact in price-sensitive APAC markets | Long term (≥ 4 years) |

| E-Commerce and Cold-Chain Growth | +1.2% | Global, concentrated in urban centers and emerging markets | Medium term (2-4 years) |

| Cargo Sensing for Volumetric Analytics | +0.9% | North America and Europe early adoption, APAC following | Long term (≥ 4 years) |

| Insurance Premium Discounts | +0.7% | North America and Europe, limited emerging market penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Fleet Visibility and Utilization Optimization

Asset-level transparency is correcting historically low 60% utilization benchmarks by enabling dynamic load assignments that add 15-20% productive capacity. Volumetric sensors and weight gauges translate available cube into actionable dispatch data, shrinking empty miles and detention times. Dispatchers leverage dwell-time analytics to forecast customer behavior and reposition trailers pre-emptively for higher service levels. The Federal Motor Carrier Safety Administration’s ELD specification, which obliges a trailer number in each output file, creates a compliance backbone that expands tracking beyond tractors[1]“Appendix A to Subpart B of Part 395—Functional Specifications for All Electronic Logging Devices (ELDs),” Federal Motor Carrier Safety Administration, ecfr.gov. As regulatory and operational incentives converge, fleets increasingly treat real-time visibility as a prerequisite for procurement and strategic contracting.

Regulatory Mandates on ELD, FSMA, and Cargo Security

U.S. ELD rules now intertwine with the Food Safety Modernization Act’s sanitation standards, making continuous temperature and location data compulsory for food haulers. Combined with Canadian ELD certification needs, cross-border fleets seek single platforms that satisfy multiple jurisdictions while minimizing device counts. Electronic documentation streamlines roadside inspections, reducing out-of-service risk and administration overhead. As regulators elsewhere emulate North American frameworks, multi-regional fleets demand globally certifiable devices, amplifying vendor differentiation on compliance credentials. Integrated platforms capable of pivoting rule sets via over-the-air updates gain a strategic edge in long-life trailer deployments.

Declining Hardware and Cellular Costs

Rapid semiconductor advances have cut tracker bill-of-materials nearly 40% since 2020, bringing sub-USD 130 price points within reach of SME operators. Simultaneously, 4G sunsets and 5G rollouts are prompting carriers to offer aggressive IoT data plans that slash per-device operating costs. Integrated GNSS, accelerometer, and LTE modems inside compact form factors halve installation time, curbing truck-down intervals. Five-year battery lives now match trailer trade cycles, simplifying total cost-of-ownership math for financial controllers. These economics accelerate adoption across aging fleets and stimulate tiered subscription models that balance capital and operating expenses.

E-Commerce and Cold-Chain Growth

Same-day delivery promises drive fleets to shorten sorting cycles and deploy high-turn utility trailers for omnichannel fulfillment hubs. Electric refrigeration units, now gaining municipal incentives in low-emission zones, need telematics interfaces for battery health, charge scheduling, and remote temperature management. Real-time alerts help avoid cold-chain breaches that could spoil pharmaceuticals or perishables, protecting cargo values exceeding USD 300,000 per load. Urban congestion charges pressure dispatchers to route multi-drop reefers efficiently, a task simplified when telematics feeds merge with traffic and curb-side availability data. Thermo King’s battery-powered E-COOLPAC shows how equipment makers are embedding connectivity as standard[2]“Thermo King Introduces E-COOLPAC Battery Solutions for Truck, Trailer and Marine Container Refrigeration Units,” Thermo King, thermoking.com.

Restraints Impact Analysis of Trailer Telematics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Costs for SMEs | -1.1% | Global, particularly acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Data-Privacy and Cyber-Security Compliance | -0.8% | Europe and North America primary, expanding globally | Medium term (2-4 years) |

| Battery-Life Limits | -0.6% | Arctic, desert, and tropical regions with temperature extremes | Long term (≥ 4 years) |

| Data-Standard Fragmentation | -0.4% | Global, with particular complexity in multi-OEM fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs for SMEs

Independent operators managing fleets of under 100 trailers often confront per-unit outlays equal to 2-3% of book value, excluding downtime. Older trailers lack standardized power looms, forcing installers to drill chassis and run external conduits that risk corrosion. Downtime erodes slim capacity margins, leading some owners to stagger installations over months, diluting ROI. Financing remains scarce because telematics lacks tangible collateral value, unlike tractors or reefers that lenders can repossess. Consequently, adoption skews toward large enterprises, creating technology gaps that further disadvantage resource-constrained carriers.

Data-Privacy and Cybersecurity Compliance

GDPR’s extraterritorial reach compels all providers touching European freight to encrypt personally identifiable information, anonymize route histories, and respond to right-to-erasure requests within 30 days. Implementing role-based dashboards and multi-factor authentication raises development costs and lengthens release cycles. Cyberattack vectors targeting over-the-air update channels necessitate real-time intrusion detection, pushing vendors into always-on security operations center postures. Legal uncertainty around data residency in cross-border cloud clusters can stall enterprise rollouts pending counsel review. The compliance burden hits smaller suppliers hardest, encouraging partnering or acquisition by security-mature platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Trailer Telematics Market Segment Analysis

By Trailer Type:

Dry-Van Dominance Faces Refrigerated UpswingDry-van units commanded 41.45% of the trailer telematics market's 2024 revenues, underlining their ubiquity in general freight routes that prize cube efficiency and standardized loading. Their long maintenance cycles enable straightforward telematics integration, anchoring the trailer telematics market’s installed base. Yet the refrigerated cohort’s 13.36% CAGR signals robust cold-chain demand tied to pharmaceuticals, fresh produce, and direct-to-consumer grocery models. Flatbeds and tankers each maintain niche relevance, with hazardous-materials rules pushing premium sensor packages that secure higher average selling prices.

Refrigerated adoption increasingly intertwines with electrification, as battery-powered refrigeration units require energy-state visibility to avoid dwell-time pre-chill losses. Schmitz Cargobull’s S.KOe COOL, which fuses a high-voltage pack, regenerative axle, and embedded telemetry, epitomizes this convergence. Vendors that consolidate location, temperature, and energy data on a single dashboard reduce driver workload and simplify compliance reporting. Such capabilities elevate the refrigerated share of the trailer telematics market size and amplify software revenue opportunities around predictive reefer maintenance.

By Communication Technology:

Cellular Connectivity AcceleratesGPS-only devices retained 55.67% of the trailer telematics market size in 2024, reflecting legacy refresh cycles and a cost-focused SME segment. The cellular segment, however, is rising at 15.85% CAGR, driven by two-way diagnostics, remote firmware updates, and near real-time ETA calculations that static beacons cannot support. Satellite links survive in ultra-remote corridors but remain cost-heavy, while Bluetooth remains confined to yard automation and driver handheld pairings.

Cellular’s ascendancy coincides with carriers adopting app-driven workflows where customers track loads to the minute and receive automated exception alerts. As 5G coverage densifies, edge processing at the device level offloads cloud costs, enabling sophisticated analytics on the trailer itself. In effect, cellular capability transforms the trailer telematics market from dots-on-a-map utilities to full operating-system environments, spawning value-add app marketplaces and integrations.

By Component:

Software Surges AheadHardware components command a 63.76% share of the trailer telematics market size in 2024, reflecting the capital-intensive nature of device deployment and installation across trailer fleets. Yet software is projected to climb 13.49% annually as fleets pivot toward recurring SaaS contracts that bundle analytics, compliance logs, and over-the-air feature releases. Hardware commoditization pressures vendors into thinner margins, reinforcing the push to monetizable data services.

Advanced platforms stitch trailer feeds into enterprise resource planning, maintenance, and customer-facing portals, delivering compound operational insights that pure hardware lacks. Predictive failure models for door-ajar sensors or brake-lining wear encourage uptime-based contract terms that align vendor revenue with fleet performance. In turn, these service models deepen customer lock-in, underpinning longer-term growth of the trailer telematics market.

By Application:

Predictive Maintenance Gains MomentumFleet management remained the anchor, hoisting 47.57% of the trailer telematics market size in 2024 via route planning, geofencing, and detention analytics. Asset tracking fulfills baseline location-aware requirements; cargo monitoring layers on security and environmental telemetry for sensitive goods. Predictive maintenance, expanding 15.42% per year, leverages sensor fusion, temperature, vibration, and brake stroke to forecast component failures days ahead.

Proactive maintenance minimizes roadside breakdowns, avoids cargo spoilage, and extends asset life, outcomes that translate swiftly into total cost-of-ownership gains. Software algorithms refine themselves on increasing data pools, raising the accuracy of prognostics and justifying premium subscription tiers. As fleets internalize the savings, predictive modules accelerate their share of the trailer telematics market size across all trailer classes.

By Deployment Type:

Cloud Pre-eminenceCloud-hosted platforms secured a 69.84% share of the trailer telematics market in 2024 because fleets prize elastic storage, remote access, and seamless integration with transport-management systems. On-premise solutions serve specialized applications where data security or connectivity constraints require local processing capabilities. The cloud’s 15.85% CAGR through 2030 mirrors enterprise IT migrations and aligns with vendor ambitions for continuous delivery models.

Zero-touch updates empower vendors to roll out machine-learning refinements without disrupting operations, while multi-tenant architectures drive economies of scale. Smaller carriers circumvent hiring dedicated IT staff, instead relying on vendor SOCs and support desks. Consequently, cloud deployment models particularly benefit smaller fleet operators to manage on-premise infrastructure while providing scalability for growing operations.

By End User:

Retail Ramps UpLogistics and transportation operators captured 54.65% of the trailer telematics market size in 2024 by virtue of sheer trailer counts and contractual service-level obligations. Construction, agriculture, and energy verticals each exploit telematics for project site coordination or hazardous material compliance. Retail and distribution emerge as the fastest-growing segment at 12.68% CAGR, driven by e-commerce expansion and direct-to-consumer fulfillment models that require enhanced visibility and customer service capabilities.

As traditional wholesale distribution evolves, the retail segment is increasingly adopting omnichannel fulfillment strategies. These modern strategies necessitate the integration of trailer telematics with inventory management systems, platforms for customer notifications, and coordination of last-mile deliveries, moving beyond the confines of traditional logistics. Furthermore, retailers are showing a pronounced readiness to invest in premium pricing for advanced features, underscoring their direct influence on customer experience and competitive edge.

By Distribution Channel:

OEM Integration Catches UpAftermarket channels dominate with a 61.74% share of the trailer telematics market in 2024, underscoring the trend of retrofitting telematics into existing trailer fleets and highlighting the flexibility of third-party solutions. Meanwhile, OEM integration emerges as the fastest-growing channel, boasting a 12.31% CAGR. This surge signals a growing acknowledgment among trailer manufacturers of the competitive edge and customer value that telematics capabilities offer.

The OEM channel enjoys benefits like factory integration, warranty coordination, and a smoother customer experience, all of which simplify deployment and reduce the need for ongoing support. Early adopters leaned towards aftermarket solutions for their immediacy, while newer entrants gravitate towards integrated solutions that promise reduced complexity and enhanced reliability. Furthermore, by partnering with OEMs, telematics providers can tap into wider customer demographics and leverage the expansive sales and service networks of manufacturers, amplifying both market reach and customer support.

Geography Analysis

North America Trailer Telematics Market

North America preserved 46.56% of the trailer telematics market in 2024 due to a mature ELD regime that codifies trailer identification and enforces digital record-keeping. Fleet familiarity with tractor telematics accelerates trailer attach-rates, raising expectations for holistic visibility dashboards. The United States leads battery-electric reefer pilots, opening early ground for energy-centric data services, while Canadian cross-border carriers demand bilingual and multi-jurisdictional compliance platforms. Private equity interest remains strong, funding platform roll-ups that consolidate regional specialists into national networks.

APAC Trailer Telematics Market

Asia-Pacific is charting an 11.76% CAGR, underscored by China’s rapid e-commerce penetration and government-backed logistics corridors. Tier-1 ports now require digital slot booking and real-time container-chassis matching, nudging fleets toward telematics. In India and Southeast Asia, cold-chain gaps expose vaccines and produce to spoilage; low-power trackers paired with solar panels address grid unreliability. Japanese OEMs export factory-equipped smart trailers across the region, giving local fleets upgrade pathways without heavy retrofits.

Broader European Markets

Europe occupies a steady yet evolving middle ground shaped by GDPR oversight and ambitious decarbonization targets. Low-emission zones spur adoption of electric transport refrigeration units needing continuous power analytics. Multimodal rail-road corridors overlay differentiated data-sharing requirements, rewarding vendors with flexible API policies. Eastern European growth centers on cross-docking and finished-vehicle logistics, where trailer telematics underpins tight handoff schedules. Russia and the CIS favor ruggedized hardware designed for temperature extremes, channeling niche demand that supplements broader European volumes.

Competitive Landscape

The trailer telematics market shows moderate concentration, with the top five vendors controlling the majority of the 2024 share, yet platform-level churn remains vigorous as fleets reassess multi-year contracts. Spireon and ORBCOMM hold sizable installed bases but face challenger momentum from cloud-native entrants leveraging AI and open APIs. PowerFleet’s USD 200 million acquisition spree folded Fleet Complete into its stack, boosting total subscribers to 2.6 million and adding vertical-specific apps that widen addressable revenue.

Platform Science’s agreement to absorb Trimble’s transportation telematics arm, covering roughly USD 300 million in trailing revenue, signals an industry pivot toward integrated in-cab ecosystems that pool tractor, trailer, and driver data. Integrated suites entice fleets looking to condense vendor rosters and standardize analytics schemas. Meanwhile, OEM partnerships densify, with Daimler Truck North America pre-installing telematics boxes that activate instantly upon delivery, shortening the time-to-value equation for fleets.

Edge-AI startups pursue niche opportunities in volumetric sensing and cargo imaging, often licensing technology to established platform vendors that wish to accelerate roadmap delivery. Geographic specialists tailor solutions for harsh climates or low-bandwidth regions, filling capability gaps major platforms have yet to prioritize. The resulting interplay between consolidation at the platform tier and innovation at the sensor tier maintains competitive tension that ultimately benefits fleet customers through faster innovation cycles and falling unit economics.

Trailer Telematics Industry Leaders

Spireon, Inc.

ORBCOMM Inc.

SkyBitz, Inc.

Phillips Connect Technologies LLC

Samsara Inc.

- *Disclaimer: Major Players sorted in no particular order

Trailer Telematics Market Companies Covered in this Report

- Spireon, Inc.

- ORBCOMM Inc.

- SkyBitz, Inc.

- Phillips Connect Technologies LLC

- Geotab Inc.

- Samsara Inc.

- Trimble Inc.

- PowerFleet, Inc.

- Verizon Connect Inc.

- MiX Telematics Limited

- Omnitracs, LLC

- CalAmp Corp.

- Sensata Technologies Holding plc

- Great Dane LLC

- Hyundai Translead, Inc.

- Utility Trailer Manufacturing Company

- Wabash National Corporation

- Schmitz Cargobull AG

- Bernard Krone Holding SE & Co. KG

- TIP Trailer Services Management B.V.

Recent Industry Developments in Trailer Telematics Market

- August 2025: Samsara introduced a Pre-Delivery Installation program with Daimler Truck North America and Fontaine Modification, allowing customers to receive new trucks equipped with telematics and cameras on day one.

- July 2025: Frotcom partnered with KRONE to pipe factory-installed trailer data directly into the Frotcom platform, eliminating aftermarket hardware needs.

- March 2025: Utility Trailer Manufacturing unveiled UTILITY TrailerConnect, integrating IoT sensors and third-party feeds for comprehensive fleet visibility.

- February 2025: Thermo King expanded its telematics suite with TracKing Smart Trailer, enriching health and cargo analytics for refrigerated fleets.

Global Trailer Telematics Market Report Scope

Segmentation Overview

| Flatbed Trailers |

| Refrigerated Trailers |

| Dry Van Trailers |

| Tanker Trailers |

| GPS Tracking |

| Cellular Connectivity |

| Satellite Communication |

| Bluetooth |

| Hardware |

| Software |

| Fleet Management |

| Asset Tracking |

| Predictive Maintenance |

| Cargo Monitoring |

| Cloud-Based |

| On-Premise |

| Logistics and Transportation |

| Retail and Distribution |

| Construction |

| Agriculture |

| Others |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Trailer Type | Flatbed Trailers | |

| Refrigerated Trailers | ||

| Dry Van Trailers | ||

| Tanker Trailers | ||

| By Communication Technology | GPS Tracking | |

| Cellular Connectivity | ||

| Satellite Communication | ||

| Bluetooth | ||

| By Component | Hardware | |

| Software | ||

| By Application | Fleet Management | |

| Asset Tracking | ||

| Predictive Maintenance | ||

| Cargo Monitoring | ||

| By Deployment Type | Cloud-Based | |

| On-Premise | ||

| By End User | Logistics and Transportation | |

| Retail and Distribution | ||

| Construction | ||

| Agriculture | ||

| Others | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global trailer telematics market in 2025?

The trailer telematics market size reached USD 1.26 billion in 2025 and is forecasted to expand at an 11.27% CAGR through 2030.

Which trailer type is growing fastest?

Refrigerated trailers are projected to grow at a 13.36% CAGR, benefiting from cold-chain and e-commerce demand.

Why are cellular-connected devices gaining share?

Two-way diagnostics, real-time ETA updates, and over-the-air firmware needs are driving a 15.85% CAGR for cellular solutions.

What role does predictive maintenance play?

Predictive maintenance is the fastest-rising application at 15.42% CAGR because it reduces breakdowns and optimizes total cost of ownership.

Which region shows the highest growth outlook?

Asia-Pacific leads in growth, anticipated to post an 11.76% CAGR due to infrastructure investment and rising digital commerce.

Page last updated on: