Highway Driving Assist Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 8.87 Billion |

| Market Size (2031) | USD 17.02 Billion |

| Growth Rate (2026 - 2031) | 13.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Highway Driving Assist Market Analysis by Mordor Intelligence

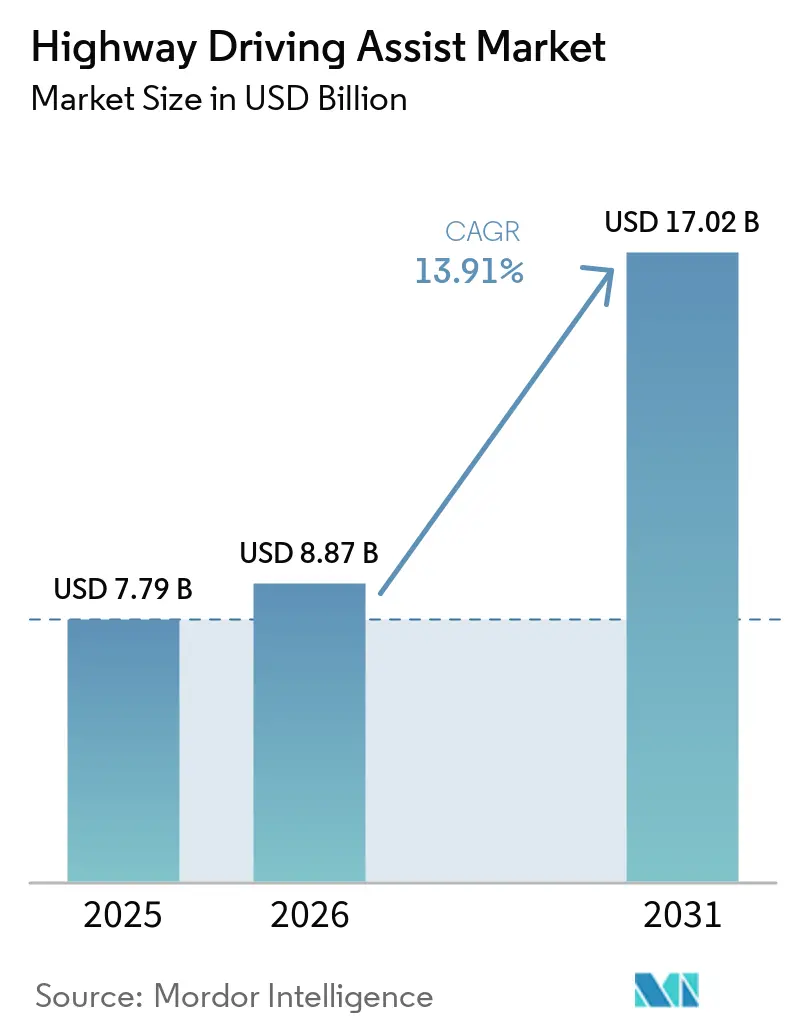

The highway driving assist market size was valued at USD 7.79 billion in 2025, is projected to reach USD 8.87 billion in 2026, and is expected to reach USD 17.02 billion by 2031, growing at a CAGR of 13.91% from 2026 to 2031. Momentum is coming from synchronized NCAP upgrades that position Level 2 functionality as an entry requirement for five-star safety ratings. Automakers are therefore bundling basic assist functions into volume trims and reserving premium lane-change and navigation features for subscription tiers. Semiconductor suppliers are vertically integrating compute platforms, compressing hardware costs, and accelerating time-to-market for mid-tier vehicles. Finally, usage-based insurance programs that reward ADAS adoption are nudging buyers toward vehicles equipped with highway-assist packages.

Key Report Takeaways

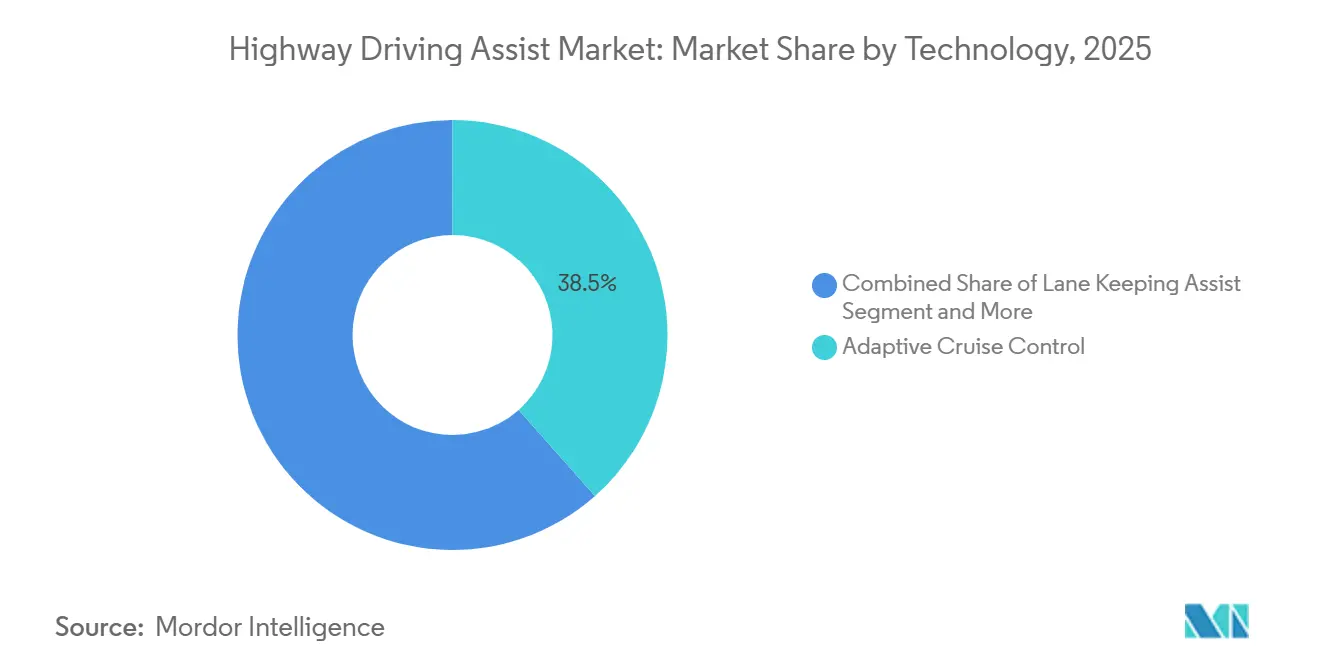

- By technology, adaptive cruise control led the highway driving assist market with a 38.48% share in 2025, while automated lane change is forecasted to expand at a 17.62% CAGR through 2031.

- By vehicle type, passenger cars accounted for 68.15% of the highway driving assist market share in 2025, whereas medium- and heavy-duty commercial vehicles are projected to grow at a 14.45% CAGR through 2031.

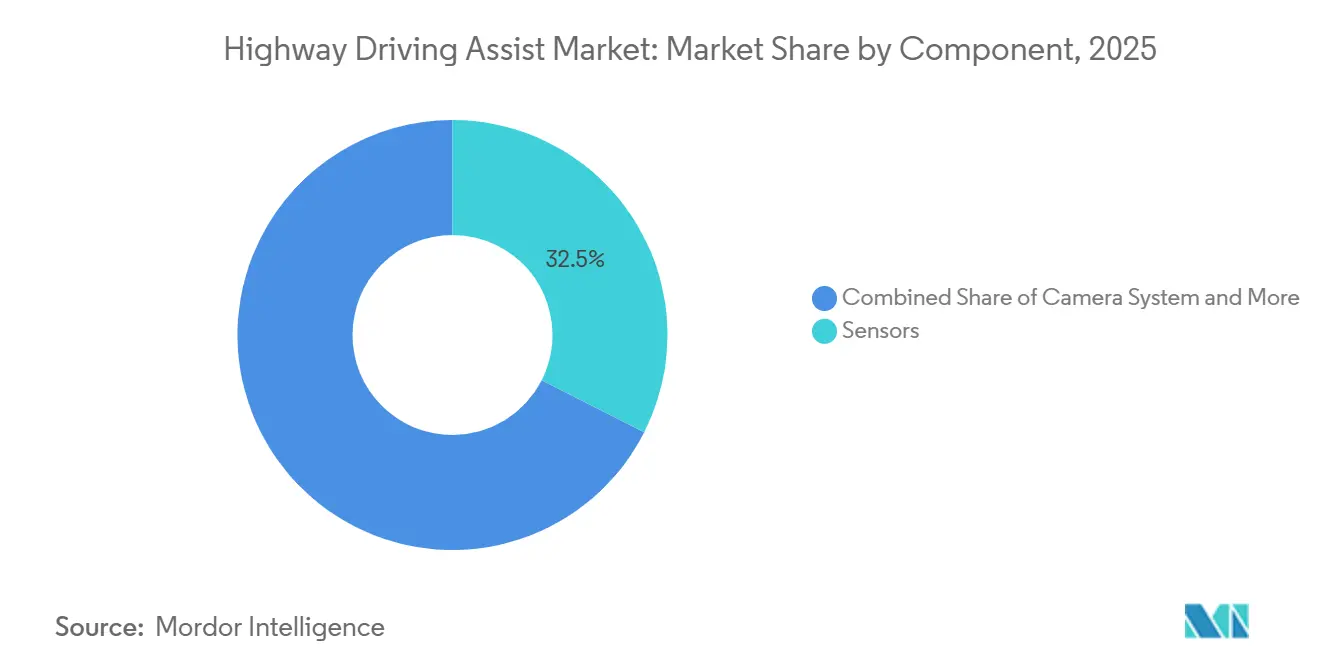

- By component, sensors accounted for 32.46% of the highway driving assist market share in 2025, but software is the fastest-growing element, with a 16.09% CAGR over the forecast period.

- By end use, personal use accounted for 71.15% share of the highway driving assist market in 2025, and ride-sharing services are expected to record the fastest growth, with a 14.88% CAGR through 2031.

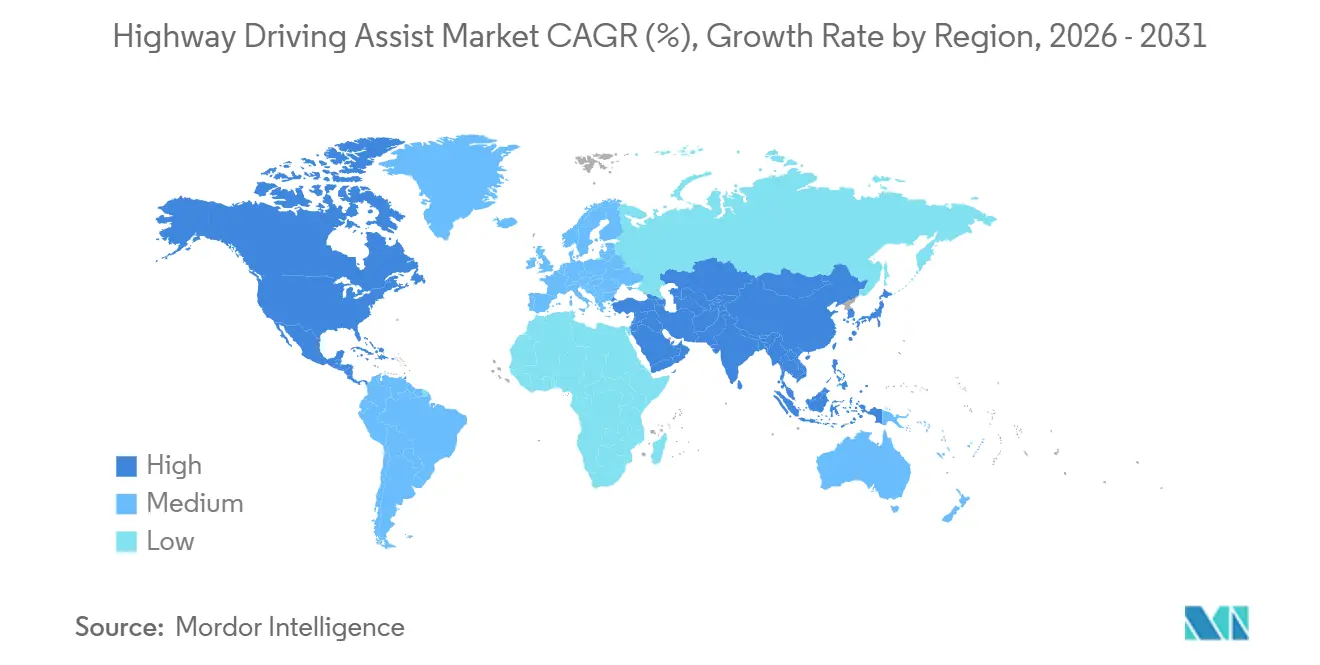

- By geography, Asia-Pacific commanded 36.98% of the highway driving assist market in 2025 and also posts the highest regional expansion at a 15.09% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Highway Driving Assist Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Mandates and NCAP Upgrades | +3.2% | Global, with early adoption in EU and North America | Short term (≤ 2 years) |

| L2/L2+ Features | +2.8% | Global, led by premium OEMs in developed markets | Medium term (2-4 years) |

| Falling Radar and Camera Costs | +2.1% | Global, with manufacturing concentration in APAC | Short term (≤ 2 years) |

| HDA Service Revenues | +1.9% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| 5G HD-map Crowd-sourcing | +1.5% | Urban centers in developed markets, expanding globally | Long term (≥ 4 years) |

| Usage-based-insurance (UBI) Incentives | +1.2% | North America and Europe, pilot programs in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Safety Mandates and NCAP Upgrades

Euro NCAP started grading assisted-driving systems in 2025, effectively forcing Level 2+ capability into mainstream vehicle programs[1]"Kia, Porsche, Renault, and Toyota raise the standard for Assisted Driving systems – Tesla and Volvo could do better", Euro NCAP, euroncap.com. NHTSA’s 2024-2033 roadmap follows a similar path by adding Lane Keeping Assist and Adaptive Cruise Control to its baseline crash-avoidance menu. In China, draft Level 3 rules issued by MIIT for 2027 mirror the requirements of ISO 21434 and UNECE R155, reducing country-specific engineering overhead[2]Liu Miao, "New Chinese regulations push L3 autonomous vehicles closer to L4 capabilities with enhanced safety protocols", CarNewsChina, carnewschina.com. UNECE Working Party 29 is finalizing Level 3/4 frameworks to harmonize homologation across more than 60 contracting markets. Together, these measures shift highway driving assist from an optional convenience to an essential compliance item, compressing product-planning cycles across the global value chain.

Automaker Roll-out of L2/L2+ Features

Manufacturers are racing to blanket their product lines with Level 2 functionality before stricter rules take effect, turning highway-assist from a premium perk into a showroom staple. Early movers benefit from software reuse across shared platforms, enabling rapid migration from luxury flagships to high-volume crossovers without restarting design cycles from scratch. Subscription dashboards also reveal which driver-assist elements attract the most engagement, guiding over-the-air updates that refine steering and distance-keeping behavior in real time. This feedback loop tightens alignment between engineering priorities and consumer experience, helping brands secure recurring digital revenue as hardware margins erode. In parallel, standardized feature sets provide insurers with consistent telemetry, reinforcing discounts that further stimulate take rates for factory-installed systems.

Falling Radar and Camera Costs

Component makers have reached volume levels where economies of scale outpace inflation, letting them quote multi-sensor bundles at price points acceptable to mass-market platforms. Cost relief lowers the barrier for smaller OEMs that previously relied on single-function warning systems, widening the customer base for turnkey highway-assist modules. Leaner bills of material also free budget for redundant compute and cybersecurity safeguards now demanded by UNECE rules, improving end-to-end system robustness. As sensors commoditize, differentiation shifts toward perception algorithms that extract higher fidelity from identical hardware, spurring healthy competition in software quality rather than physical parts. Ultimately, declining sensor prices accelerate feature standardization across trims, expanding the total addressable market without requiring aggressive incentives.

Subscription-based HDA Service Revenues

The decoupling of hardware shipment from feature monetization changes corporate finance models throughout the automotive value chain. Automakers recognize revenue over the life of the vehicle rather than at the point of sale, smoothing cash flow and aligning interests with ongoing customer satisfaction. Continuous deployment enables iterative refinement of lane-change logic and driver-monitor prompts, thereby sustaining perceived value and supporting renewal rates. Regulatory acceptance of secure over-the-air updates under UNECE R156 further legitimizes the subscription path, removing earlier doubts about software authenticity and safety compliance. As buyers grow accustomed to paying monthly for convenience tech, the model reinforces a self-funding cycle that finances next-generation assist innovations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost | -2.1% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| OTA Compliance Burden | -1.6% | EU, Japan, South Korea, Australia (UNECE parties) | Medium term (2-4 years) |

| ADAS Talent Shortage | -1.3% | Germany, US, Romania (engineering hubs) | Long term (≥ 4 years) |

| Performance Gaps | -0.8% | Northern EU, Canada, US Midwest, mountainous regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront System Cost

Even with cheaper sensors, the complete bill for redundant compute, high-definition maps, and cybersecurity certification can add thousands of dollars to a vehicle, straining affordability in emerging markets. Buyers of entry trims often confront a stark choice between comfort options and advanced assist packages, which tempers penetration outside premium segments. Fleet managers weigh the investment against tight operating margins, delaying adoption until insurance discounts or regulatory credits offset capital outlay. Automakers experiment with modular offerings that keep basic lane-keeping standard while paywalling automated lane change, but this tiering fragments the user experience and complicates marketing. Until total system cost aligns with mass-market price points, rollout speed will remain uneven across regions.

Cyber-security and OTA Compliance Burden

UNECE Regulation 155 obliges manufacturers to maintain active cybersecurity management throughout the vehicle lifecycle, converting what was once a launch-phase task into a permanent operational duty. Meeting audit requirements demands specialized talent that is already in short supply, stretching project timelines and inflating payroll budgets. Frequent renewal cycles add recurring paperwork and validation testing, redirecting resources from new feature development toward regulatory maintenance. Differing interpretations of global standards force automakers to tailor software update strategies on a country-by-country basis, fracturing platform uniformity and raising overhead. These layered obligations slow time-to-market and dilute the financial upside promised by over-the-air feature expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Automated Lane Change Becomes The Premium Differentiator

Adaptive Cruise Control accounted for 38.48% of the technology slice of the highway driving assist market in 2025. Its ubiquity stems from radar commoditization and regulatory nudges that treat longitudinal control as a baseline safety layer. Suppliers now embed the feature in cost-optimized modules that integrate seamlessly with power-train and braking ECUs, reducing integration friction for mass-market platforms. As the function becomes standard, automakers are shifting their marketing focus away from raw specifications toward driver-monitoring fidelity and robust road-edge detection. In parallel, advanced mapping interfaces allow continuous cloud calibration, keeping even entry vehicles compliant with evolving lane-center standards.

Automated Lane Change is growing at a 17.62% CAGR, the fastest pace within the technology hierarchy. Premium trims rely on the feature to distinguish themselves through hands-free overtaking and cooperative merge logic. The complexity of validating lateral autonomy across multi-lane scenarios has prompted new simulation workflows that cut physical-drive mileage while preserving safety claims. Cloud-deployed software stacks also enable over-the-air expansion from basic lane-keeping to predictive lane selection once edge AI maturity allows. Consequently, a bifurcated pattern is emerging where legacy functions commoditize, while subscription-gated capabilities sustain margin headroom.

By Vehicle Type: Commercial Fleets Pursue Operating Cost Relief

Passenger cars accounted for 68.15% of the highway driving assist market share in 2025, owing to the dominance of private ownership in large addressable markets. Highway driving assist adoption in this segment mirrors consumer appetite for convenience, blended with rising insurance incentives tied to risk scores. Automakers leverage established infotainment channels to upsell monthly subscriptions that unlock higher-order assist modes, maintaining engagement well past the initial sale. As regulations progressively require basic ADAS in new models, consumer expectations are also normalizing around some form of hands-on driver support. This baseline sets the stage for increased acceptance of semi-autonomous capabilities.

Medium and heavy commercial vehicles, advancing at a 14.45% CAGR, illustrate how fleet economics can accelerate technology turnover. Highway assist reduces fatigue-related incidents, a major cost factor for long-haul operators, and qualifies assets for telematics-based insurance rebates. Retrofit-ready sensor pods enable existing tractors to gain lane-keeping and cooperative cruise control without a full platform redesign, reducing downtime. Driver-shortage pressures further strengthen the case as automated functions extend allowable operating hours within legal safety envelopes. As a result, suppliers are curating modular kits that integrate with prevalent telematics gateways, turning highway assist into a line item in total-cost-of-ownership planning.

By Component: Software Claims the Value Frontier

Sensors accounted for 32.46% revenue share in 2025, reflecting their foundational role in environmental perception for the highway driving assist market. Multi-mode radar, solid-state LiDAR, and high-dynamic-range cameras form redundant layers that satisfy functional-safety and NCAP visibility tests. Suppliers keep margins afloat by bundling calibration, diagnostics, and extended warranties into service contracts rather than relying solely on hardware markup. Meanwhile, processor vendors are collapsing dedicated ADAS ECUs into domain controllers, simplifying wiring and cutting weight. This architectural pivot lowers entry barriers for emerging EV platforms that must optimize power budgets.

Software leads component growth at a 16.09% CAGR as features migrate to cloud-linked licensing. Over-the-air pathways let automakers decouple revenue recognition from production cycles, unbundling advanced lane management, traffic-jam pilot, and enhanced visualizations as optional tiers. Safety regulators increasingly accept software-centric change management provided cybersecurity and fail-operational rules are met, turning continuous deployment into a compliance-friendly practice. The approach also addresses hardware obsolescence by shifting perception upgrades from sensor replacements to neural-network retraining. Consequently, competitive moats are forming around data pipelines and validation frameworks rather than physical bill-of-materials.

By End-Use: Shared-Mobility Accelerates Platform Learning

Personal use dominated the highway driving assist market, capturing 71.15% of the market share in 2025. Retail buyers increasingly associate highway-assist features with reduced fatigue and enhanced comfort. Automakers bolster this perception, promoting these benefits alongside advanced infotainment packages, underscoring their lifestyle value. Word of mouth, especially through owner forums and social media, has cemented the expectation that today's vehicles should autonomously steer and brake on divided highways. Recognizing this trend, regulatory bodies have incorporated related tests into safety assessments, helping sustain adoption momentum. From dealers to insurers, all stakeholders emphasize the safety advantages of automated longitudinal and lateral support.

Ride-sharing services show the fastest growth, with a 14.88% CAGR, reflecting a business case built on asset utilization and incident-rate reduction. Fleet managers track driver-assist engagement time as a proxy for fatigue mitigation, linking it directly to customer-satisfaction scores. Because shared-mobility vehicles accumulate high mileage, subscription payback periods shrink, making advanced features financially attractive sooner than in privately owned cars. Data captured during every ride feeds into perception-model refinement, shortening validation loops for corner cases. In effect, shared fleets double as rolling sensor networks that continuously fortify the highway driving assist market knowledge base.

Geography Analysis

Asia-Pacific held 36.98% of the highway driving assist market in 2025 and is set to post the fastest climb at a 15.09% CAGR through 2031. China’s rollout of roadside V2X units and its alignment with ISO-based cybersecurity rules reduce localization burdens and unlock rapid feature certification. Japan focuses on elderly-driver assistance, prompting local OEMs to refine takeover alerts that resonate with demographic realities. South Korea scales cooperative cruise on expressways using nationwide 5G coverage, illustrating how infrastructure readiness underpins adoption. Emerging economies such as India see early signs of mass-market penetration as domestic manufacturers integrate cost-optimized sensor suites into popular SUV lines.

North America benefits from NHTSA-driven harmonization that inserts core assist functions into the safety mainstream. Subscription economics dominate strategic dialogues, with major automakers using trial-to-paid conversion metrics to refine pricing ladders. Insurers lower premiums for vehicles that provide verifiable lane-centering and driver-monitoring telemetry, creating a virtuous feedback loop that boosts installation rates. Cross-border alignment with Canadian standards minimizes homologation overhead, enabling unified North American vehicle specifications. Meanwhile, aftermarket retrofits gain regulatory recognition, opening a secondary channel for older vehicle fleets to join the momentum of the highway driving assist market.

Europe advances under the General Safety Regulation, which mandates Intelligent Speed Assistance and Lane Keeping Assist on new vehicle types. Euro NCAP’s expanded metrics spur manufacturers to exceed baseline compliance in pursuit of marketing leverage. Regional OEMs pilot Level 3 traffic-jam features on controlled-access roads, using geofencing to stay within regulatory comfort zones while collecting usage data for future expansions. Supply-chain stresses related to semiconductor availability encourage partnerships with domestic chipmakers and foster dialogue on resilience. Although growth trails Asia-Pacific, Europe’s policy clarity underpins steady scale-up across member states.

Competitive Landscape

The highway driving assist market shows moderate concentration, with the five largest suppliers together responsible for just over half of global revenue. Traditional Tier-1s are transitioning from hardware bundling to end-to-end platforms that include perception software, over-the-air update tools, and cybersecurity libraries. This strategic shift cushions revenue against hardware commoditization shocks and taps recurring licensing streams. Simultaneously, semiconductor firms leverage their compute dominance to court automakers directly, blurring historic customer-supplier lines. The resulting competitive arena rewards those able to balance silicon roadmaps with robust software ecosystems.

Data-centric newcomers challenge incumbents by offering crowd-sourced mapping and simulation libraries that accelerate the validation of corner-case scenarios. Their proposition resonates with OEMs seeking shorter development loops without scaling physical test fleets. Legacy sensor specialists answer by integrating on-board self-test and predictive maintenance analytics, adding operational uptime to their value arguments. Regulatory demand for explainable AI also tilts importance toward suppliers that package annotated datasets and verification reports ready for audit submission. Consequently, alliances form between compute vendors, perception startups, and mapping houses to pool complementary strengths.

Commercial-vehicle retrofits emerge as a white-space niche attracting both established Tier-1s and agile startups. Fleets view add-on sensor bars and plug-and-play ECUs as cost-effective ways to earn insurance credits and retain drivers. Suppliers differentiate through installation time, telematics compatibility, and compliance documentation that simplifies fleet-wide certification. As the retrofit funnel grows, competitive barriers shift from brand legacy to network effects in service coverage and firmware update velocity. The landscape, therefore, blends long-tenured industrial players with software-native entrants, each vying to define de facto standards for upgradeable autonomy.

Highway Driving Assist Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

ZF Friedrichshafen AG

-

Aptiv PLC

-

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Subaru rolled out a complimentary software update for select Outback models in the U.S., activating the brand's inaugural hands-free highway assist feature.

- October 2025: General Motors confirmed plans to enable eyes-off driving on the future Cadillac ESCALADE IQ, using dashboard lighting to signal when the system takes over control.

- September 2025: U.S. chipmaker Qualcomm and BMW unveiled an automated driving suite delivering hands-free highway assist, automatic lane change, and self-parking.

- July 2025: Ford unveiled BlueCruise 1.5, its updated hands-free driving software, now offering fully automatic lane changes. This enhancement improves the Mustang Mach-E's competitiveness against General Motors’ Super Cruise. The update also features upgraded interface alerts, better lane centering, and faster response times powered by improved hardware.

Global Highway Driving Assist Market Report Scope

The Highway Driving Assist market is analyzed across technology, vehicle type, component, end-use, and geography.

By Technology, the market is segmented into Adaptive Cruise Control, Lane Keeping Assist, Automated Lane Change, Traffic Jam Assist, and Collision Avoidance. By Vehicle Type, the market is segmented into Passenger Car, Light Commercial Vehicle, and Medium and Heavy Commercial Vehicle. By Component, the market is segmented into Sensors, Camera Systems, Control Units, Software, and Radar Systems. By End-Use, the market is segmented into Personal Use, Fleet Management, and Ride-Sharing Service. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

The Market Forecasts are Provided in Terms of Value (USD).

| Adaptive Cruise Control |

| Lane Keeping Assist |

| Automated Lane Change |

| Traffic Jam Assist |

| Collision Avoidance |

| Passenger Car |

| Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

| Sensors |

| Camera System |

| Control Units |

| Software |

| Radar Systems |

| Personal Use |

| Fleet Management |

| Ride-Sharing Service |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Adaptive Cruise Control | |

| Lane Keeping Assist | ||

| Automated Lane Change | ||

| Traffic Jam Assist | ||

| Collision Avoidance | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicle | ||

| Medium and Heavy Commercial Vehicle | ||

| By Component | Sensors | |

| Camera System | ||

| Control Units | ||

| Software | ||

| Radar Systems | ||

| By End-Use | Personal Use | |

| Fleet Management | ||

| Ride-Sharing Service | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the highway driving assist market in 2026?

The highway driving assist market size reached USD 8.87 billion in 2026, reflecting steady expansion since 2025.

Which region leads demand for highway driving assistance?

Asia-Pacific currently commands the largest share, supported by rapid infrastructure deployment and harmonized safety rules.

Which technology segment is growing the fastest?

Automakers increasingly favor the Automated Lane Change technology, projecting it to grow at a robust CAGR of 17.62% through 2031, positioning it as a premium feature ready for subscription models.

Why are commercial fleets investing in highway assist?

Fleet operators pursue lower insurance rates and reduced driver fatigue, making retrofit-friendly highway assist an attractive operational upgrade.

What is driving software growth in this space?

Over-the-air feature unlocks allow continuous revenue after vehicle sale, positioning software as the primary value-creation layer.

Page last updated on: