In-Car Infotainment System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

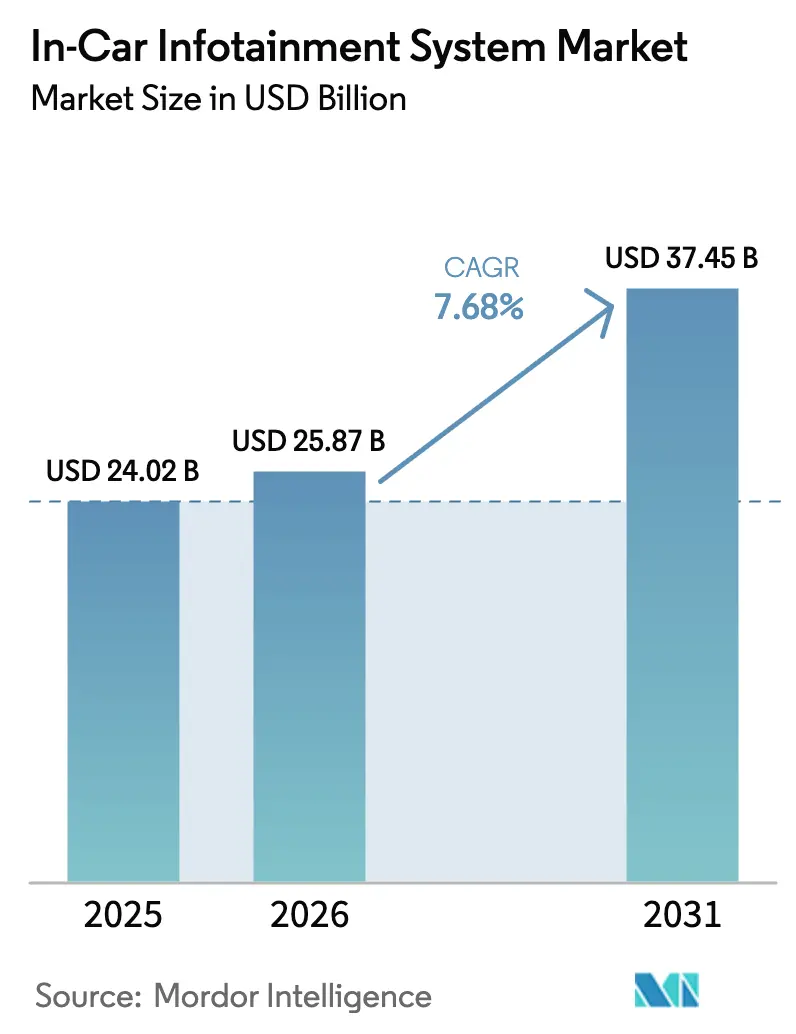

| Market Size (2026) | USD 25.87 Billion |

| Market Size (2031) | USD 37.45 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

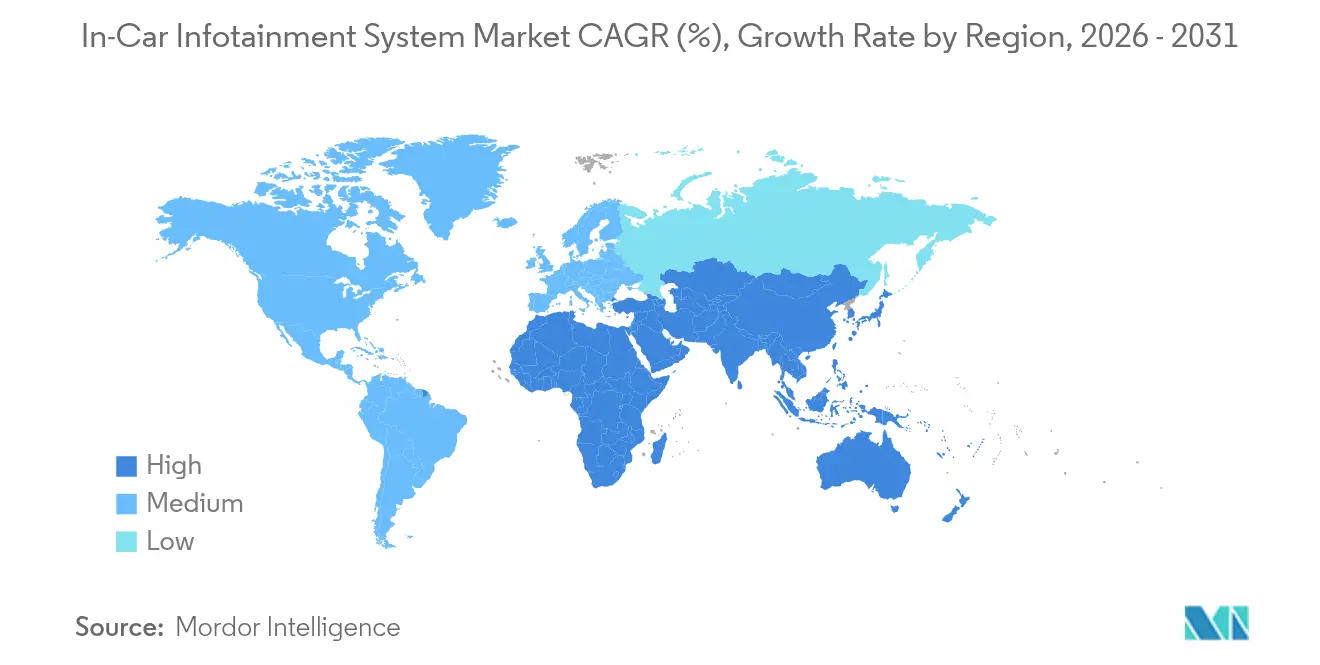

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

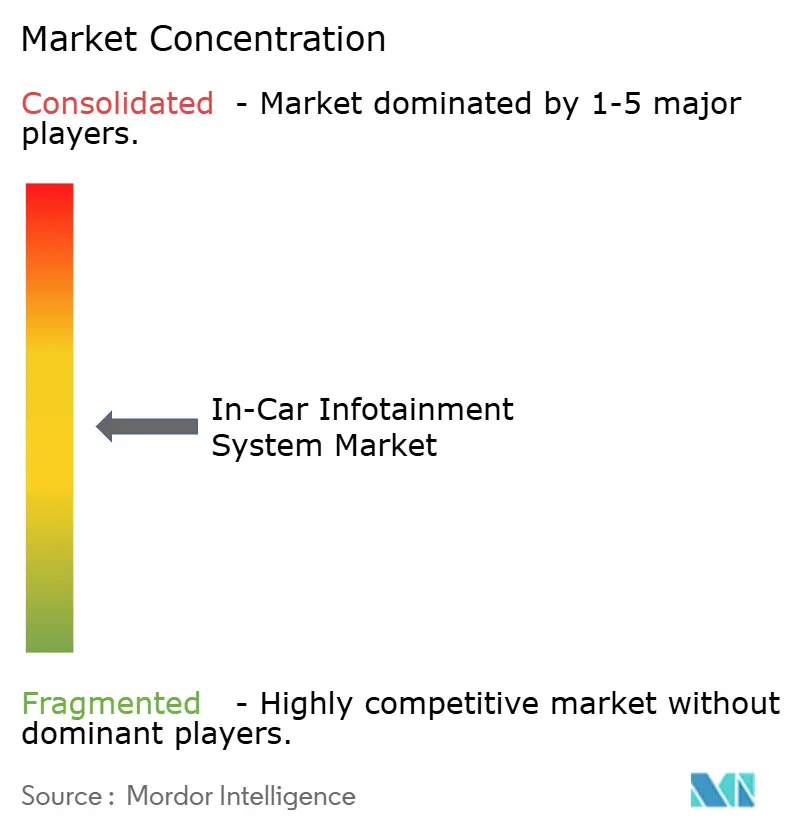

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

In-Car Infotainment System Market Analysis by Mordor Intelligence

The in-car infotainment system market size was valued at USD 24.02 billion in 2025 and estimated to grow from USD 25.87 billion in 2026 to reach USD 37.45 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031). Over the next five years, penetration will deepen as voice-first human–machine interfaces mature, 5G vehicle-to-everything modems drop in cost, and global eCall regulations entrench connectivity as standard equipment. Automakers are shifting from discrete head units to software-defined cockpits that pool instrument-cluster, driver-assistance, and entertainment workloads on centralized compute, compressing hardware bills yet raising software complexity. Suppliers able to certify cybersecurity compliance under UNECE WP.29 R155 and ISO/SAE 21434 are favored for new programs, while display makers gain from the larger real estate demanded by augmented-reality navigation and passenger streaming services. Subscription-based upgrades, such as on-demand acceleration boosts and in-vehicle payments, underpin fresh revenue streams that lift the in-car infotainment system market beyond one-off hardware sales[1]Michael Gorissen, "Huf passed cyber security audit based on ISO/SAE 21434," Huf Magazine, huf-group.com.

Key Report Takeaways

- By component, display units led with 41.02% revenue share in 2025, whereas communication units will accelerate at an 11.34% CAGR to 2031.

- By operating system, Android platforms accounted for 64.15% of the in-car infotainment system market share in 2025. Android Automotive OS is projected to exhibit the fastest growth at a 13.48% CAGR through 2031.

- By installation type, in-dash systems captured 77.15% of the 2025 value, while rear-seat infotainment is forecasted to grow at a 10.92% CAGR to 2031.

- By vehicle type, SUVs and MPVs controlled 71.10% of 2025 revenue; the group is poised for a 9.52% CAGR over the forecast period.

- By geography, Asia-Pacific dominated with 36.05% of the in-car infotainment system market in 2025, while the Middle East and Africa are projected to post the fastest 8.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In-Car Infotainment System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI Voice Assistants | +2.8% | Global, with early adoption in North America, Europe, and premium segments in China | Medium term (2-4 years) |

| Integration of Smartphone Mirroring (CarPlay, Android Auto) | +2.3% | Global, mandated by major OEMs in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Connected-Car Data Services | +1.9% | North America, Europe, and urban Asia-Pacific markets; spillover to MEA | Medium term (2-4 years) |

| Regulatory Mandates | +1.6% | Europe (EU mandate), Russia, Brazil, India; expanding to GCC and ASEAN | Long term (≥ 4 years) |

| Demand for Advanced Vehicles | +1.4% | Global, with concentration in North America, Europe, and China | Long term (≥ 4 years) |

| Monetization of Cockpit Data | +1.2% | North America and Europe pilot programs; limited Asia-Pacific deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Emergence of Generative-AI Voice Assistants

Generative-AI models now power voice assistants capable of free-form queries that span routing, maintenance, and commerce. Mercedes-Benz began rolling out ChatGPT inside its MBUX stack in 2023, allowing conversational restaurant searches and contextual vehicle control. Automakers view these assistants as subscription gateways that generate lifetime revenue while reducing driver distraction compared with deep menu navigation. Early deployments cluster in premium segments that tolerate software fees and offer the processing headroom required for on-device inference. Broader rollout depends on edge accelerators that minimize cloud latency and on compliance with GDPR and China’s Personal Information Protection Law, both of which shape data-handling architectures.

Rising Integration of Smartphone Mirroring (CarPlay, Android Auto)

Apple CarPlay and Android Auto have shifted from optional add-ons to baseline expectations, now shipping on nearly every new vehicle in North America and Europe. The architecture forces tier-1 suppliers to design head units that toggle seamlessly between native and mirrored environments, raising bill-of-material costs. Consumer backlash to the removal of these interfaces, as seen when one major U.S. OEM announced a phase-out, highlights the strategic risk of narrowing platform choice. Next-generation CarPlay, scheduled for 2025 models, will render instrument clusters and HVAC controls, effectively placing the smartphone at the center of the human–machine interface. Automakers must still expose CAN data securely, maintaining the cybersecurity posture mandated by UNECE WP.29 R155[2]Myriam Joire, "Here's the real reason Android Automotive is still kind of a mess in EVs," TechRadar, techradar.com..

Growing Adoption of Connected-Car Data Services

Connected-car platforms now bundle predictive maintenance, usage-based insurance, and in-vehicle payments. BMW’s ConnectedDrive, for instance, aggregates sensor data to pre-order parts, shaving dealership downtime. Fleet operators quantify return on investment through reduced insurance premiums and optimized routing, justifying the added hardware cost of 4G and 5G telematics. While the business case is compelling, data-sovereignty rules fragment deployments: Europe requires user consent under GDPR, whereas China mandates on-shore data storage, driving localized cloud instances and inflating total cost of ownership.

Regulatory Mandates for eCall & Telematics

Europe’s eCall rule has lowered emergency response times by up to 40% in rural accidents, prompting copy-cat frameworks in Russia, Brazil, and India. GCC nations are piloting similar mandates to advance Vision 2030 smart-city goals. Automakers amortize the incremental USD 50–USD 100 connectivity hardware by bundling navigation and entertainment features on the same telematics control unit. Aftermarket retrofits of eCall modules in older fleets create a secondary revenue pathway for suppliers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Price Sensitivity | -2.1% | South America, Southeast Asia, Africa, and rural India | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities | -1.5% | Global | Medium term (2-4 years) |

| Complexity in System Integration | -1.2% | Global | Medium term (2-4 years) |

| Thermal & Power-Management Limits | -0.8% | Middle East, North Africa, and hot-climate regions in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & Price Sensitivity in Emerging Markets

Advanced infotainment hardware ranges from USD 800 to USD 3,000, a steep premium for buyers in India, Southeast Asia, and Africa who prioritize basic transport and safety. Entry-level models frequently ship with only Bluetooth audio, leaving consumers to install aftermarket Android head units at a fraction of the cost. Automakers tier feature bundles, preserving margins but slowing market-wide penetration. Exchange-rate volatility further widens this affordability gap because most electronic components are priced in USD or EUR[3]"Emergency Communications", Electronic Communications Committee, www.cept.org..

Cyber-Security Vulnerabilities in Connected Vehicles

Demonstrated hacks have moved cybersecurity from compliance box-ticking to board-level priority. UNECE Regulation 155 obliges manufacturers to run cyber-security management systems across the vehicle life cycle, forcing additional validation loops and extending development timelines. The U.S. Executive Order on critical infrastructure cybersecurity, enacted in 2024, cascades to automotive suppliers, mandating zero-trust architectures. Suppliers now compete on secure-boot attestation, intrusion detection, and over-the-air patching capacity. Non-conformance risks recall costs, brand damage, and import bans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Communication Units Drive Connectivity Premium

Communication units are on track for an 11.34% CAGR from 2026 to 2031, propelled by mainstream adoption of 5G C-V2X modems and dual-SIM eSIMs that support regional roaming. The in-car infotainment system market size for communication units is expected to outpace displays even as curved OLED panels dominate luxury dashboards. Qualcomm’s Snapdragon Digital Chassis underpins 2025 launches from multiple global OEMs, bundling Wi-Fi 7, GNSS, and Bluetooth LE Audio on a single chipset. Display units retain the largest value slice due to larger diagonals, higher pixel density, and the quota of dual-screen cockpits in premium trims. Audio and navigation units see modest growth as their functions increasingly virtualize onto centralized domain controllers.

Modular architectures pool infotainment, cluster, and driver-assistance workloads on shared hardware, trimming wiring and unit counts. This consolidation compresses supplier bills yet demands tighter software orchestration to avoid latency spikes that degrade user experience. As communication units mature, over-the-air features such as paid acceleration boosts and map-on-demand become cost-effective, further monetizing connectivity. Component vendors that can deliver cybersecurity-certified firmware and power-efficient silicon win design slots, given automakers’ focus on thermal headroom and battery range, especially in electric vehicles.

By Operating System: Android Automotive OS Captures OEM Mandates

Android platforms held 64.15% of the in-car infotainment system market share in 2025, and Android Automotive OS is forecast for a commanding 13.48% CAGR up to 2031 as OEMs seek a mature app ecosystem and rapid over-the-air updates. Volvo, Polestar, and Renault already run full Google stacks, streamlining maintenance while tapping Play Store revenue splits. Linux persists in commercial vehicles requiring hard real-time performance and open-source customization, while QNX remains entrenched for safety-critical clusters demanding ASIL-D certification.

Automakers value the reduced development burden of Android but must weigh data-sharing implications in regions where Google services face restriction. Chinese brands continue to favor AliOS and HarmonyOS, maintaining control over user data. The in-car infotainment system market size for Linux distributions remains steady as tier-1 suppliers adapt bespoke flavors for truck fleets and specialty vehicles. Cross-domain hypervisors now enable the coexistence of multiple operating systems on one system-on-chip, allowing safety-critical functions to run isolated from the infotainment domain, thus meeting both regulatory and user-experience goals.

By Installation Type: Rear-Seat Systems Monetize Premium Cabins

In-dash infotainment accounted for 77.15% of 2025 revenue, cementing its role as the primary interface. Nevertheless, rear-seat installations will expand at 10.92% CAGR, targeting chauffeur-driven vehicles and multi-child households. The in-car infotainment system market size for rear-seat units gains from OLED cinema displays surpassing 30 inches, integrated cloud gaming, and personalized streaming profiles. BMW’s Theatre Screen exemplifies the upsell potential, while Mercedes-Benz’s rear-seat MBUX packages merge comfort, entertainment, and commerce.

Wireless content mirroring and 5G piping support low-latency gameplay and videoconferencing, monetized through data packages or subscription bundles. In contrast, fleet sedans and entry-level hatchbacks in mature markets maintain single-screen setups to cap costs. As edge processing offloads cloud latency, rear-seat systems may integrate gesture control and occupancy-based audio zoning, making second-row experiences more immersive. Suppliers innovating in low-power display drivers and heat management win bids, especially in hot-climate markets where OLED longevity is a concern.

By Vehicle Type: SUVs and MPVs Command Cockpit Investment

SUVs and MPVs controlled 71.10% of 2025 segment value and will log a 9.52% CAGR through 2031, driven by cabin space that accommodates larger screens and multi-zone audio. The in-car infotainment system market size for SUVs aligns with premium features like augmented-reality head-up displays and biometric driver monitoring. Panoramic curved dashboards, first seen in high-end electric SUVs, filter down to near-luxury trims, signaling design convergence.

Hatchbacks and sedans focus on cost-optimized infotainment framed around smartphone mirroring and basic navigation, though electric hatchbacks use advanced touchscreens to telegraph innovation. MPVs in Asia-Pacific stress rear-seat connectivity for family passengers, leveraging sliding-door access to mount bigger panels. Body style distinctions blur as skateboard EV platforms free interior volume, yet the revenue bias toward SUVs persists thanks to higher average selling prices and consumer preference for elevated seating positions.

Geography Analysis

Asia-Pacific contributed 36.05% of 2025 revenue to the in-car infotainment system market, buoyed by China’s production scale and India’s rising auto volumes. Domestic Chinese suppliers, backed by robust state support, deliver cockpit domains at prices 40% below Western equivalents, enabling mass-market electric sedans to ship with dual-screen layouts once reserved for luxury nameplates. Japan’s major automakers have standardized CarPlay and Android Auto to cut software maintenance, while South Korea accelerates C-V2X rollouts under its 5G smart-city program. Southeast Asia remains price sensitive; yet, India’s AIS-140 telematics mandate pushes OEMs to integrate basic connectivity, underpinning steady demand. Asia-Pacific is forecast to post a 7.21% CAGR to 2031, sustained by electric-vehicle growth and edge-processed feature monetization.

The Middle East and Africa is projected as the fastest-growing region at 8.91% CAGR, fueled by GCC smart-city budgets, mandatory fleet tracking, and premium vehicle imports in Saudi Arabia and the UAE. High ambient temperatures necessitate LCDs with specialized coatings or active cooling, although top-tier SUVs now ship with cooled OLEDs. Vision 2030 programs in Saudi Arabia include nationwide telematics for public transport, laying a connectivity foundation that benefits infotainment uptake. Africa’s patchy cellular grids constrain always-on services, so suppliers prioritize offline navigation and robust Bluetooth audio. Despite lower unit volumes, the high content per vehicle in luxury segments offsets the region’s smaller base.

North America and Europe are mature yet lucrative. North America advances at a 6.34% CAGR as consumers favor ever-larger screens and wireless smartphone mirroring. Regulatory focus shifts to data privacy and over-the-air recall management, adding cost but also standardizing cybersecurity best practices. Europe’s 5.88% CAGR reflects saturation—98% of new cars already ship with advanced infotainment—yet the region sets the compliance bar, driving global suppliers to certify to UNECE and GDPR standards. South America, though smaller, gains from Brazil’s eCall rules and a rebound in Argentina, clocking a 7.32% CAGR despite currency swings that temper premium feature adoption.

Competitive Landscape

The in-car infotainment system market is moderately concentrated: the top five suppliers, Harman International, Continental AG, Panasonic Automotive Systems, Robert Bosch, and Visteon, command 61% combined share. Competition is pivoting from bespoke hardware to software ecosystems. Harman’s Ready Care platform layers biometric monitoring and well-being alerts, giving automakers differentiation beyond display size. Continental teams with Google to preload Android Automotive OS into cockpit computers, trimming OEM integration timelines and prompting rivals to craft similar turnkey stacks.

Semiconductor firms are reshaping the value chain. Qualcomm’s Snapdragon Digital Chassis offers a reference design that enables carmakers to source application software directly from niche vendors, compressing hardware margins yet expanding service opportunities. Nvidia’s DRIVE platform merges infotainment, cluster, and driver-assistance workloads on a unified system-on-chip, facilitating software-defined features upgraded over the air. Cybersecurity compliance is emerging as a key differentiator; suppliers able to provide secure boot, intrusion detection, and incident-response dashboards win program bids as automakers brace for UNECE audits.

White-space remains in commercial telematics and fleet management, segments underserved by consumer-centric stacks. Regional specialists develop ruggedized head units with driver-behavior scoring, aiming at logistics fleets where fuel savings and insurance discounts justify higher upfront costs. Meanwhile, legacy navigation firms face eroding margins as smartphone mirroring cannibalizes standalone GPS demand. Strategic alliances—tier-1s with cloud providers, chipmakers with game studios—signal a market gravitating toward platform-based competition rather than point solutions.

In-Car Infotainment System Industry Leaders

-

Continental AG

-

Harman International

-

Pioneer Corporation

-

Denso Corporation

-

Panasonic Automotive Systems Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Hyundai Motor India revealed India’s first Android Automotive OS infotainment platform, arriving in an A-segment hatchback and an SUV in early 2027.

- September 2025: BMW unveiled Panoramic iDrive technology at CES 2025, featuring a windshield-spanning display with Operating System X based on Android Open Source Project. The system includes 3D head-up displays and enhanced Intelligent Personal Assistant capabilities with third-party app integration.

- June 2025: Harman introduced a Neo QLED automotive display debuting in the Tata Harrier.ev, marking the technology’s first in-vehicle use.

- April 2025: Porsche announced a region-specific infotainment system slated for 2026, underscoring the trend toward localized cockpit software.

Global In-Car Infotainment System Market Report Scope

In-car infotainment systems, commonly referred to as in-car entertainment (ICE), deliver both information and entertainment to vehicle occupants. These systems frequently enable connections to various electronic devices, including smartphones, smartwatches, headphones, and computers. Connections can be made through cables like USB or HDMI, or wirelessly via Bluetooth. Notably, certain infotainment systems have the capability to interface with multiple Bluetooth devices simultaneously.

In Car Infotainment Market is segmented component, operating system, installation type and geography. Based on the component, the market is segmented into audio unit, display unit, navigation unit and communication unit. Based on the operating system, the market is segmented into android, linux, Microsoft and others. Based on the installation type, the market is segmented into in-dash infotainment and rear infotainment. Based on the geography, the market is segmented into the North America, Europe, Asia Pacific and Rest of the World. For each segment, market sizing and forecast have been done on the basis of value (USD).

| Audio Unit |

| Display Unit |

| Navigation Unit |

| Communication Unit |

| Android |

| Linux |

| QNX |

| Others |

| In-dash Infotainment |

| Rear-seat Infotainment |

| Hatchbacks |

| Sedans |

| SUVs and MPVs |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Audio Unit | |

| Display Unit | ||

| Navigation Unit | ||

| Communication Unit | ||

| By Operating System | Android | |

| Linux | ||

| QNX | ||

| Others | ||

| By Installation Type | In-dash Infotainment | |

| Rear-seat Infotainment | ||

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| SUVs and MPVs | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the growth outlook for the in-car infotainment system market to 2031?

The in-car infotainment system market is projected to rise from USD 25.87 billion in 2026 to USD 37.45 billion by 2031, reflecting a 7.68% CAGR.

Which component segment will expand the fastest?

Communication units, propelled by 5G modems and V2X protocols, are set for an 11.34% CAGR between 2026 and 2031.

Why are Android platforms gaining share in vehicle cockpits?

Automakers adopt Android Automotive OS to access Google apps, cut maintenance costs, and enable rapid over-the-air updates, driving a 13.48% CAGR for the operating system segment.

Which region will record the highest growth?

The Middle East and Africa leads regional growth at a projected 8.91% CAGR, supported by smart-city investments and luxury vehicle demand.

How are suppliers differentiating in a software-defined cockpit era?

Vendors focus on cybersecurity certification, AI-powered voice assistants, and subscription business models rather than pure hardware specifications.

What impact do eCall mandates have on market demand?

Mandatory emergency-call regulations in Europe, India, and other regions require embedded connectivity, ensuring baseline installation of infotainment telematics hardware across new vehicles.

Page last updated on: