Commercial Vehicle ADAS Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

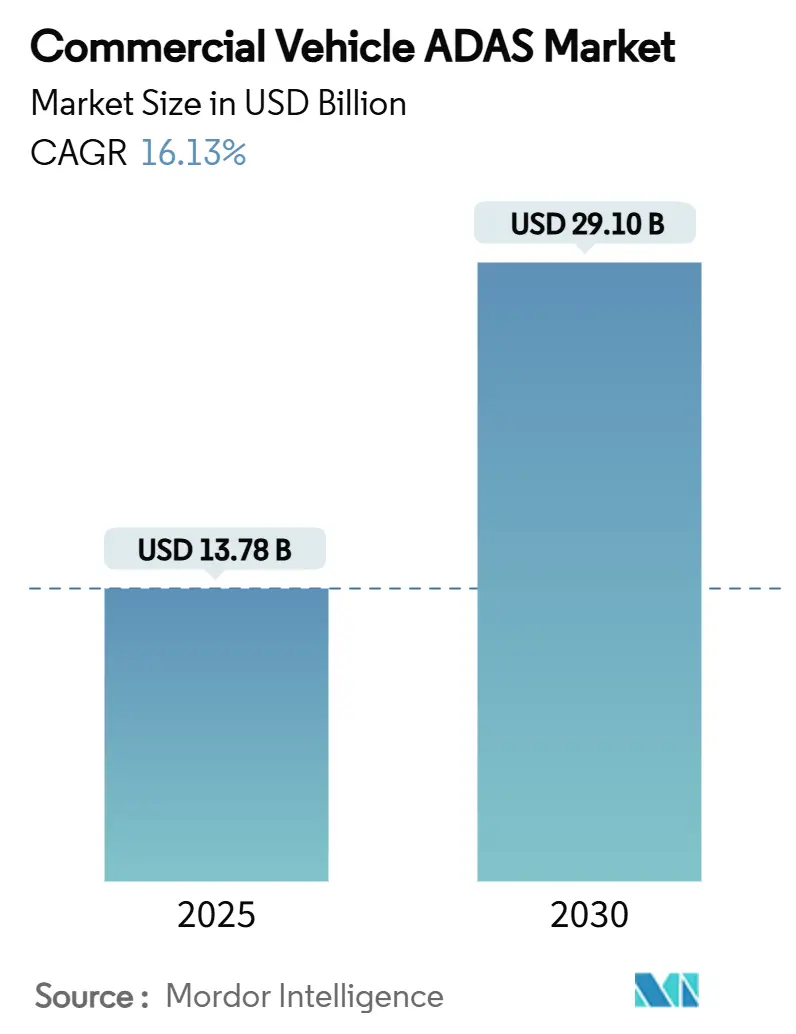

| Market Size (2025) | USD 13.78 Billion |

| Market Size (2030) | USD 29.10 Billion |

| Growth Rate (2025 - 2030) | 16.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Vehicle ADAS Market Analysis by Mordor Intelligence

The Commercial Vehicle ADAS Market size is estimated at USD 13.78 billion in 2025, and is expected to reach USD 29.10 billion by 2030, at a CAGR of 16.13% during the forecast period (2025-2030). This trajectory reflects the alignment of regulatory mandates, maturing sensor fusion architectures, and the clear economic case for crash-avoidance technology. The Federal Motor Carrier Safety Administration (FMCSA) estimates that every USD 1 spent on advanced driver-assistance systems returns USD 5.09 in crash-related savings, driver retention, and insurance benefits.[1]“Benefit-Cost Analyses for Advanced Driver Assistance in Commercial Vehicles,” Federal Motor Carrier Safety Administration, fmcsa.dot.gov Radar, camera, and LiDAR costs have fallen steadily since 2024, allowing OEMs to embed sophisticated Level 2 functionality across light, medium, and heavy platforms without a price premium discouraging buyers. At the same time, insurers in North America and Europe now grant average premium discounts of 6-12% for vehicles equipped with forward-collision warning, blind-spot detection, and driver monitoring—a further incentive for fleets navigating razor-thin operating margins.

Key Report Takeaways

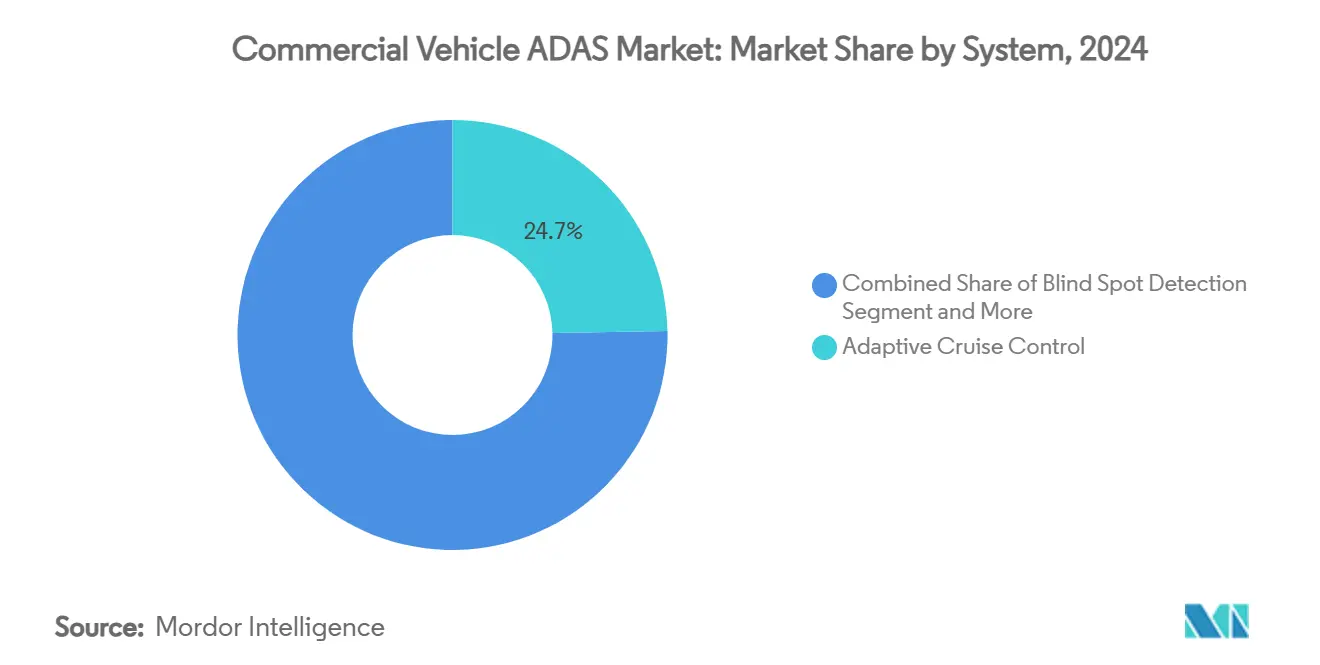

- By system, adaptive cruise control accounted for 24.71% of commercial vehicle ADAS market share in 2024, while Driver Monitoring Systems posted the fastest expansion at a 16.72% CAGR through 2030.

- By sensor, radar sensors held 48.17% of the commercial vehicle ADAS market size in 2024; LiDAR solutions lead the growth curve at 16.57% CAGR to 2030.

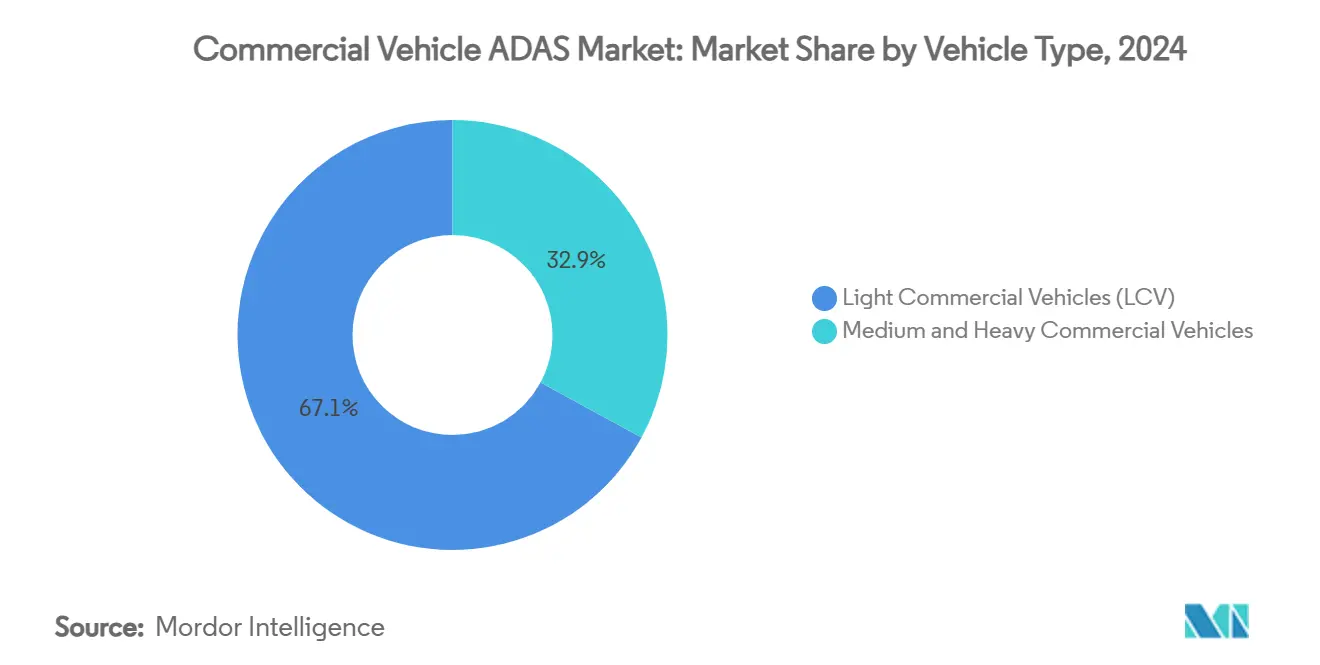

- By vehicle type, light commercial vehicles commanded 67.13% of the commercial vehicle ADAS market size in 2024, yet Medium and Heavy Commercial Vehicles are set to grow at 16.38% CAGR.

- By distribution channel, OEM-installed systems represented 73.15% of commercial vehicle ADAS market share in 2024, whereas aftermarket retrofits are expanding at a 16.85% CAGR.

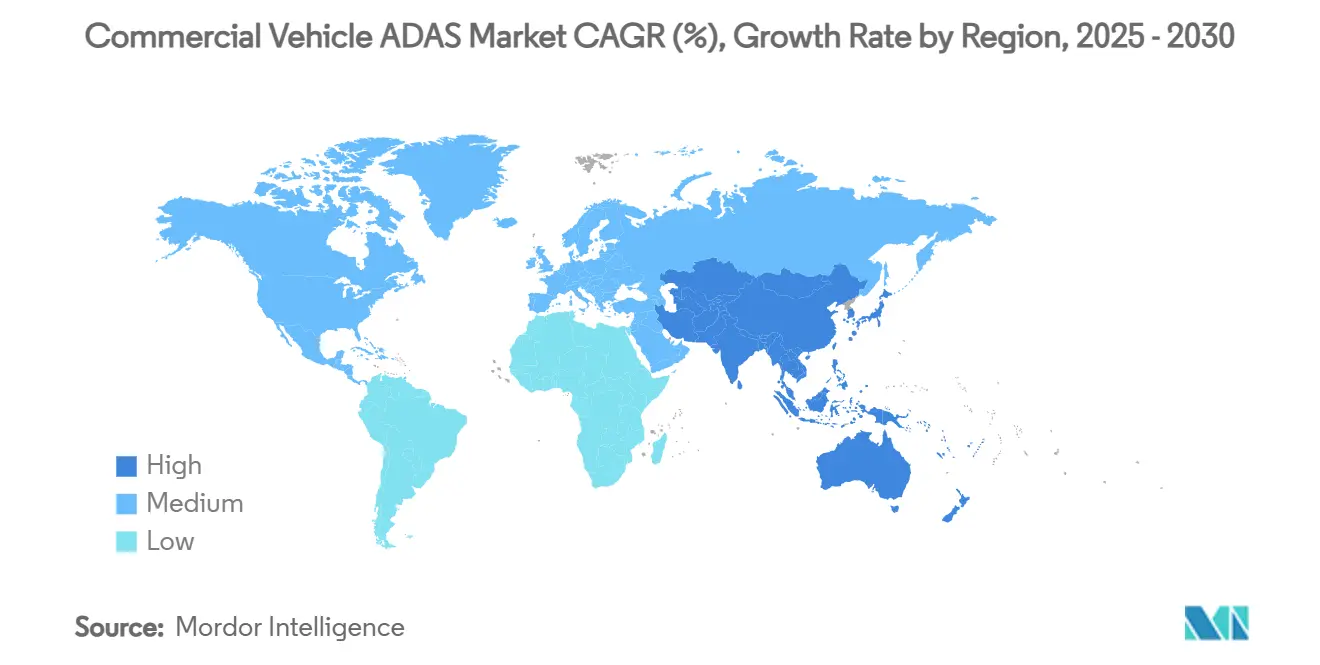

- By geography, Asia-Pacific contributed 38.73% of global revenue in 2024 and is projected to sustain leadership with a 16.24% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Vehicle ADAS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Road-Safety Regulations | +3.8% | Global, with EU and India leading | Short term (≤ 2 years) |

| Technological Advances | +3.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Fleet TCO Optimisation | +3.1% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Insurance-Telematics-Linked ADAS | +2.4% | North America and EU primarily | Short term (≤ 2 years) |

| EU Driver-Monitoring Mandate | +1.9% | EU, with spillover to aligned markets | Short term (≤ 2 years) |

| Standardised Retrofit Kits | +1.3% | Global, focus on mature fleet markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Road-Safety Regulations

National and supranational bodies have converged on a minimum ADAS baseline for new trucks and buses. The European Union’s General Safety Regulation obliges advanced emergency braking, intelligent speed assistance, and driver drowsiness warning for all new commercial vehicles sold after July 2024.[2]“General Safety Regulation 2019/2144,” European Commission, europa.eu India will mandate similar functionality for buses and heavy trucks from 2026, elevating the world’s second-largest freight market to global best practice. The United States is finalising an automatic emergency-braking requirement that mirrors the FMCSA’s own research findings. Harmonised rules are erasing regional engineering divergence, enabling Tier-1 suppliers to develop global hardware-software stacks and capture economies of scale. Over time this legislative pressure removes non-ADAS variants from OEM line-ups, anchoring the commercial vehicle ADAS market as a default safety attribute rather than a discretionary upgrade.

Technological Advances in Autonomous/ADAS Stacks

The transition from Level 2 warning aids to predictive intervention hinges on sensor fusion accuracy and AI-enabled scene interpretation. Sixth-generation radar from Continental brings 360-degree coverage at elevated sampling rates, while Bosch and Microsoft are applying generative AI to classify hazards faster than rule-based algorithms.[3]“Generative AI for Automated Driving,” Bosch, bosch.comLiDAR costs have dropped to one-tenth of 2019 levels, and single-photon avalanche diode breakthroughs now give 8 mm range resolution, extending identification capabilities under rain or fog. Thermal imaging paired with 77 GHz radar helps differentiate pedestrians from roadside infrastructure at night. These converging technologies shorten development cycles for Level 3 freight corridors, with Daimler Truck aiming to field SAE Level 4 rigs on US highways by 2027.

Fleet TCO Optimisation Mandates

For fleet operators, safety electronics have matured into a quantifiable return-on-investment lever. Telematics-integrated driver coaching has cut insurance claims by 10-45% and trimmed fuel waste by up to 20% across North American line-haul segments. Tokio Marine’s Drive Agent telematics platform reduced claim counts by 13% within a year of deployment. Against an inflationary backdrop for premiums, CFOs now treat ADAS expenditure as a hedge rather than an additional cost line. Technology vendors capitalise on this shift by bundling collision-avoidance data with maintenance diagnostics, giving fleet managers a consolidated dashboard that maps safety metrics directly to operating cash flow.

Insurance-Telematics-Linked ADAS Incentives

Insurers have started to reward real-time risk transparency. Policies that integrate forward-collision-warning data or camera-verified near-miss events are priced 6-12% lower than conventional fleet cover in the UK and Germany, accelerating ADAS option-take rates for new vehicle purchases. Some US underwriters now embed quarterly premium adjustments based on hard-braking incidents logged through cloud APIs. The feedback loop is dampening historically cyclical premium spikes and reinforcing the commercial vehicle ADAS market’s economic narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial ADAS Component Cost | -2.8% | Global, particularly in price-sensitive markets | Medium term (2-4 years) |

| Retrofit Complexity | -1.9% | Mature markets with aging commercial fleets | Long term (≥ 4 years) |

| Urban Radar-Spectrum Congestion | -1.2% | Dense urban areas globally | Short term (≤ 2 years) |

| Driver Disengagement | -0.9% | Global, varying by driver demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial ADAS Component Cost

Despite falling sensor prices, LiDAR still commands four-figure unit costs that owner-operators in Latin America or parts of ASEAN deem prohibitive. Full sensor suites incorporating radar, ultrasonic, and domain controllers add several thousand dollars to a new chassis, eroding the payback horizon for small fleets. The aftermarket faces comparable hurdles: only 30% of repair shops possess alignment bays large enough for camera calibration. Mobileye’s 2024 decision to wind down its retrofit division underscored short-term volume limitations. As silicon supply normalises and economies of scale ramp, Tier-2 vendors expect camera modules to decline another 20% in average selling price by 2026, narrowing the affordability gap.

Retrofit Complexity for Pre-CAN Vehicles

Pre-2005 vehicles often require reverse engineering of proprietary wiring to capture throttle and brake signals. Research teams at German OEMs have automated channel discovery, yet fleet workshops still struggle with calibration repeatability. Fault codes in anti-lock brakes or stability control frequently cascade into ADAS diagnostics, adding labour hours and warranty disputes. The business case therefore tilts in favour of new-vehicle turnover, moderating retrofit penetration in regions with ageing fleets such as Eastern Europe and parts of South America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Driver Monitoring Leads Innovation Wave

Driver-assistance installations cluster around functions that fleets deem immediately profitable. Adaptive Cruise Control accounted for 24.71% of 2024 revenue, a reflection of proven fuel-efficiency gains during highway platooning. The commercial vehicle ADAS market size for Driver Monitoring Systems is expanding at a 16.72% CAGR because regulators now define fatigue detection as critical. Tier-1 suppliers integrate eye-closure metrics, heart-rate variability, and facial-landmark tracking, turning the cabin into a biometric safety zone.

In parallel, Automatic Emergency Braking adoption accelerated after draft FMCSA rules outlined a 0.45 g minimum deceleration requirement at 40 mph. Blind-spot detection gained momentum once the Eurospec code introduced right-turn cyclist-protection tests. Forward-collision warning remains foundational but is being subsumed into multi-modal fusion stacks that also host night-vision overlays.

By Sensor: Radar Dominance Faces LiDAR Challenge

With 48.17% revenue share of commercial vehicle ADAS market in 2024, radar remains the backbone of collision mitigation. Price points below USD 50 per short-range module and proven performance in rain keep it indispensable. However, LiDAR is registering a 16.57% CAGR through 2030 as per-unit costs dip below USD 350 and resolution climbs to 200 lines per degree. The Korea Institute of Science and Technology produced single-photon avalanche diodes with 56-picosecond jitter, raising urban mapping fidelity to sub-decimeter levels.

Sensor fusion strategy has moved from redundancy to complementarity. Magna’s thermal-radar hybrid extends detection to 200 meters and cuts false positives by 50% compared with radar-only systems. Domain control units manage 10-gigabit per second Ethernet streams, ensuring deterministic latency for collision-avoidance algorithms.

By Vehicle Type: Heavy Vehicles Drive Premium Growth

Light vans dominate numerically, translating to 67.13% commercial vehicle ADAS market share in 2024. Yet the commercial vehicle ADAS market grows fastest in medium- and heavy-duty trucking, posting a 16.38% CAGR as asset values and liability exposure soar. Volvo Trucks introduced an Active Side-Collision Avoidance Suite that applies brakes during right-turn cyclist detection; field tests show a 24% reduction in near-miss events. Daimler’s Level 4 strategy leverages redundant steering and braking lines, positioning heavy rigs for hub-to-hub autonomy on controlled corridors by 2027.

Regulatory timelines differ: the EU’s Advanced Driver Distraction Warning becomes compulsory for heavy trucks six months ahead of light LDV schedules, nudging OEM R&D budgets toward larger platforms first. Drivers of articulated vehicles often maintain longer tenures, which further supports return-on-training investments for complex ADAS interfaces. Over-the-air software updates allow fleets to roll out lane-centering to 15,000-unit tractor pools overnight, compared with the staggered upgrade cycles typical in sprinter van fleets.

By Distribution Channel: Aftermarket Gains Despite OEM Dominance

Factory-installed hardware secured 73.15% of commercial vehicle ADAS market revenue share in 2024, benefitting from assembly-line economies and warranty integration. Still, aftermarket suppliers are recording a 16.85% CAGR. Continental’s mid-2025 launch of multifunction cameras for retrofit targets mixed-brand fleets that cannot standardise on a single OEM. Packages include wiring looms, ECUs, and calibration panels, reducing installation time by 40% for workshops enrolled in Continental’s training. ZF’s Smart Camera will become available in early 2025, supporting traffic-jam assistance and lane-keeping. Demand comes from regional parcel carriers and municipal bus operators seeking to extend asset life beyond 12 years while meeting new safety mandates.

Only 30% of repair shops currently offer ADAS replacement, constrained by bay size and tooling. Mobile calibration vans deploy portable targets and LiDAR alignment lasers to bridge the gap, cutting downtime for long-haul tractors that cannot afford lengthy depot stays. Suppliers increasingly bundle cloud licensing with hardware, capturing recurring revenue through driver-coaching analytics and remote diagnostics.

Geography Analysis

Asia-Pacific retained 38.73% of global commercial vehicle ADAS market revenue share in 2024 and will maintain pole position at a 16.24% CAGR through 2030. China’s rapid electrification overlaps Level-2 penetration in new passenger cars, creating a shared supply chain that lowers ADAS costs for trucks. Commercial fleets in Guangdong and Zhejiang provinces deploy forward-collision warning as standard, encouraged by provincial insurance subsidies. Nonetheless, local road-marking inconsistencies and mixed traffic demand AI models trained on heterogeneous data sets.

North America represents a mature yet still expanding arena. Automatic emergency braking legislation under review at the National Highway Traffic Safety Administration will formalise a de facto standard already adopted by most long-haul fleets. Insurance telediagnostics create a feedback loop where crash-avoidable cases trim claim costs by 30%, internalising the benefit for operators. Canada mirrors US rules, and cross-border freight corridors encourage specification parity. Europe’s July 2024 blanket requirement cements ADAS as a non-optional feature. The continent also leads on driver-monitoring, with mandatory camera-based fatigue detection scheduled for 2026. Scandinavia pilots truck platooning in winter conditions, stress-testing sensor fusion under snow and slush. Eastern European adoption lags due to an ageing fleet; retrofit subsidies under the EU’s Connecting Europe Facility aim to close the gap.

South America and the Middle East remain nascent. Brazil’s National Road Safety Plan endorses lane-departure alarms but lacks binding timelines. Gulf Cooperation Council fleets exploring hydrogen trucks also evaluate camera-mirror systems to tackle desert glare. In each emerging region the commercial vehicle ADAS industry faces twin obstacles of high import tariffs and limited calibration infrastructure, although falling sensor costs promise gradual inroads through 2030.

Competitive Landscape

Tier-1 powerhouses—Bosch, Continental, and ZF Friedrichshafen—anchor the ecosystem by bundling radar, camera, and domain controllers. Bosch’s 2025 tie-up with Microsoft on generative AI shortens perception-stack training times by 30% and embeds continuous-learning loops via Azure Edge.[4]“Bosch Partnership on Azure Edge for Automated Driving,” Microsoft, microsoft.com Continental leverages its sixth-generation radar to offer a turnkey perception platform dubbed ProViu360, pitched at OEMs seeking single-supplier simplicity. ZF commits EUR 18 billion R&D outlay by 2026, much channeled to Level 4 highway automation.

Pure-play sensor houses such as Velodyne, Innoviz, and Ouster carve slots in the commercial vehicle ADAS market by licensing reference designs that drop into OEM roofline pods. Their volumes remain modest, yet strategic alliances with Asian contract manufacturers promise scale. Fleet-service providers Netradyne and Lytx blur category lines, combining driver monitoring, video telematics, and predictive maintenance. Their SaaS platforms appeal to logistics majors wanting one invoice for cameras, AI analytics, and compliance reporting.

Collaborative ventures reshape competition. Volvo Group and Daimler Truck devised a joint software-defined vehicle backbone, pooling 30 million lines of code to accelerate road-map execution. TRATON turned to Applied Intuition for simulation, lowering physical test miles by half and expediting homologation cycles. Meanwhile, chipmakers Nvidia and Qualcomm integrate hardware accelerators into reference ADAS stacks, courting OEMs that prefer vertical integration. The commercial vehicle ADAS market thus exhibits moderate concentration: legacy Tier-1s still command bulk share, yet software and silicon entrants erode margins through faster iteration.

Commercial Vehicle ADAS Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen

Autoliv

Valeo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TRATON GROUP and Applied Intuition expanded their partnership to deliver modular operating systems and developer toolchains across Scania, MAN, and Navistar lines, targeting faster over-the-air feature rollout.

- March 2025: Volkswagen Group, Valeo, and Mobileye agreed to co-develop Level 2+ functions on the MQB platform, integrating 360-degree camera and radar arrays for hands-free cruising.

- March 2025: Samsara and Hyundai Translead unveiled HT LinkVue, a factory-installed 360-degree trailer camera transmitting live feeds to the tractor cab to cut aftermarket installation downtime.

Global Commercial Vehicle ADAS Market Report Scope

| Adaptive Cruise Control |

| Blind Spot Detection |

| Lane Departure Warning System |

| Automatic Emergency Braking |

| Forward Collision Warning |

| Night Vision System |

| Driver Monitoring |

| Tyre-Pressure Monitoring System |

| Head-Up Display |

| Park Assist System |

| Others |

| Radar |

| LiDAR |

| Ultrasonic |

| Image |

| Others |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles |

| OEM-Fitment |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By System | Adaptive Cruise Control | |

| Blind Spot Detection | ||

| Lane Departure Warning System | ||

| Automatic Emergency Braking | ||

| Forward Collision Warning | ||

| Night Vision System | ||

| Driver Monitoring | ||

| Tyre-Pressure Monitoring System | ||

| Head-Up Display | ||

| Park Assist System | ||

| Others | ||

| By Sensor | Radar | |

| LiDAR | ||

| Ultrasonic | ||

| Image | ||

| Others | ||

| By Vehicle Type | Light Commercial Vehicles (LCV) | |

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | OEM-Fitment | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the commercial vehicle ADAS market by 2030?

The commercial vehicle ADAS market size is forecast to reach USD 29.10 billion by 2030, growing at a 16.13% CAGR.

Which ADAS system currently generates the highest revenue share?

Adaptive Cruise Control leads with 24.71% of commercial vehicle ADAS market share in 2024.

Why are Driver Monitoring Systems expanding faster than other ADAS functions?

Post-2026 EU mandates, combined with measurable reductions in fatigue-related crashes, propel a 16.72% CAGR for driver monitoring.

How significant is radar in the ADAS sensor mix?

Radar held 48.17% of 2024 revenue due to its reliability in poor weather and attractive cost profile, although LiDAR growth is accelerating.

What keeps aftermarket ADAS retrofits from scaling faster?

High calibration complexity and limited workshop readiness mean only 30% of service centres can currently replace or align ADAS components, slowing adoption.

Which region is likely to register the fastest growth through 2030?

Asia-Pacific, led by China and India, is projected to advance at a 16.24% CAGR, supported by regulatory mandates and large fleet populations.

Page last updated on: