Automotive Automated Parking System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 6.88 Billion |

| Growth Rate (2026 - 2031) | 15.41% CAGR |

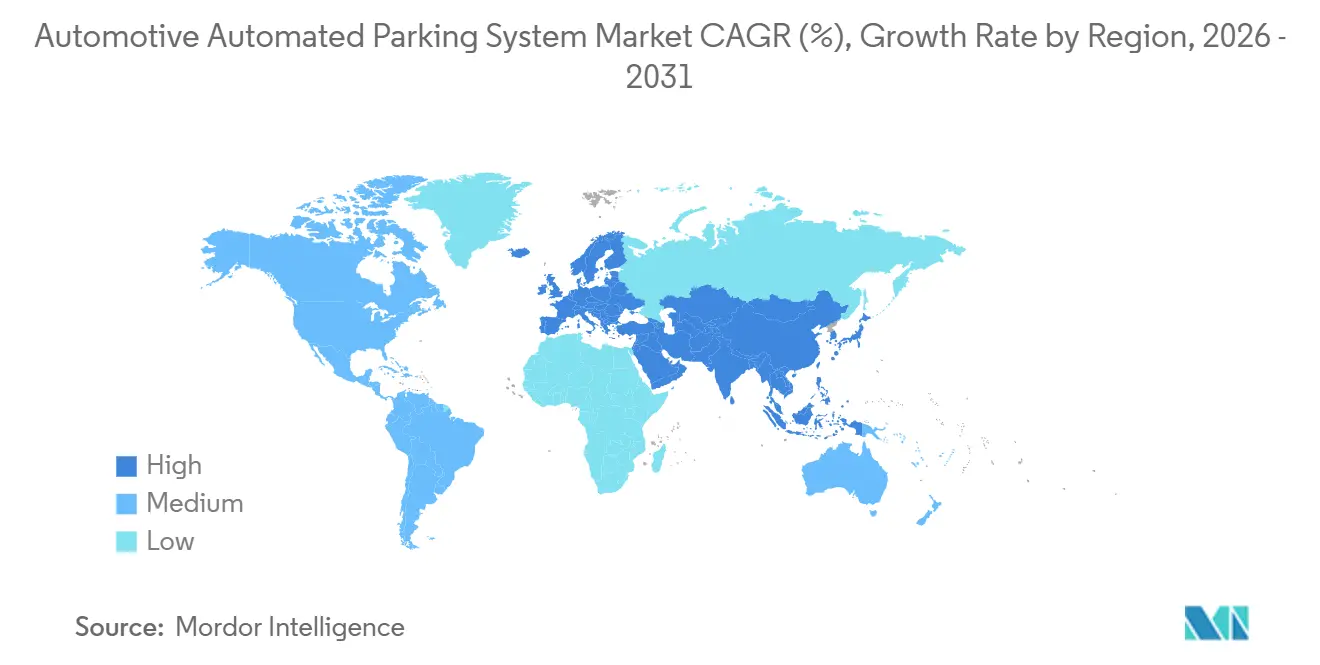

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

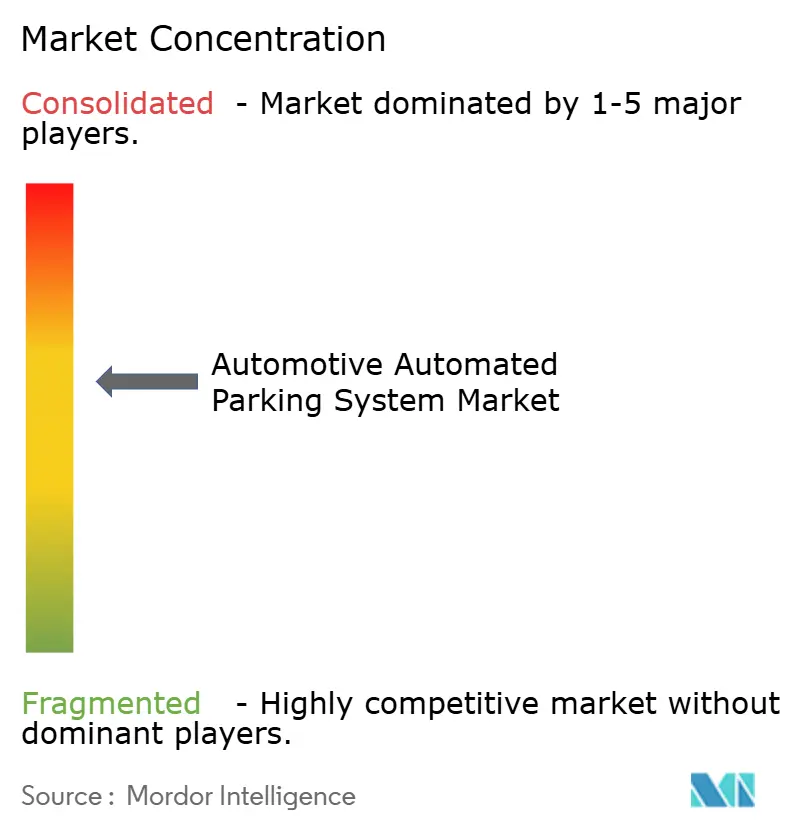

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Automated Parking System Market Analysis by Mordor Intelligence

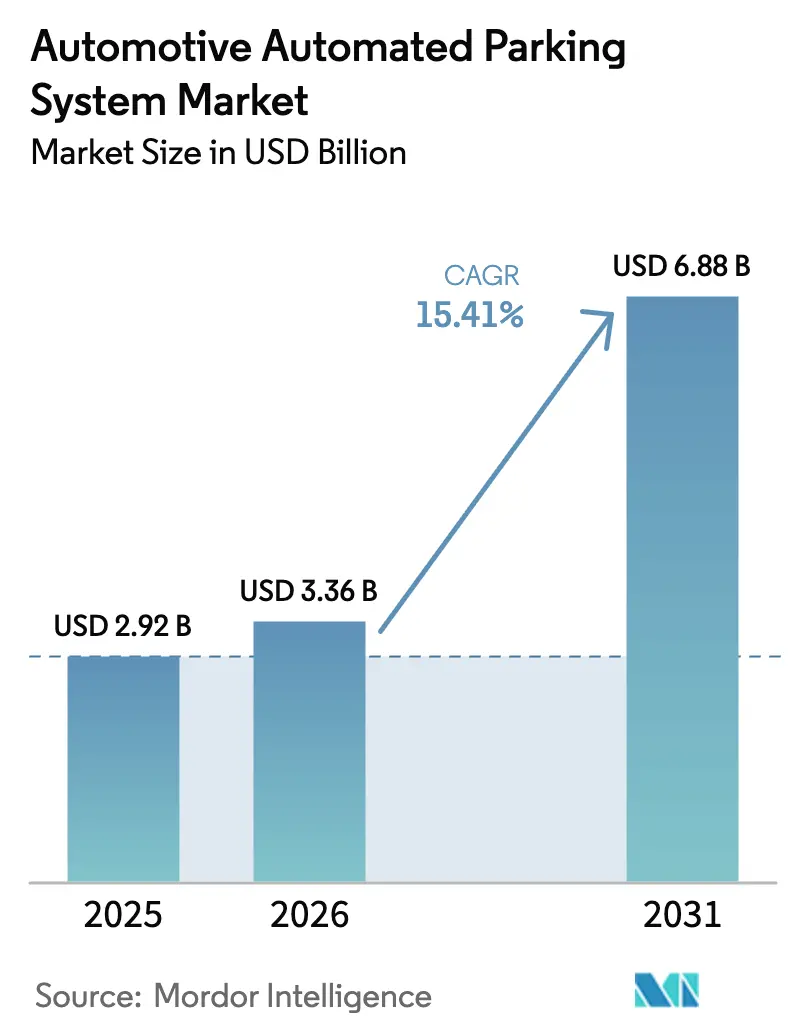

The automotive automated parking system market size is expected to grow from USD 2.92 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 6.88 billion by 2031 at 15.41% CAGR over 2026-2031. Surging land prices in dense downtowns, zoning incentives that reward footprint reduction, and the steady electrification of vehicle fleets are pushing developers toward space-saving robotic garages. Operators are layering software subscriptions on top of hardware, converting one-time construction projects into recurring revenue streams. ISO-based standards for automated valet parking are accelerating fully automated deployments, while ESG scoring frameworks now assign tangible value to enclosed, energy-efficient structures that curb heat-island effects. Collectively, these forces underpin robust growth even as high capital outlays and cybersecurity exposure temper adoption in some regions.

Key Report Takeaways

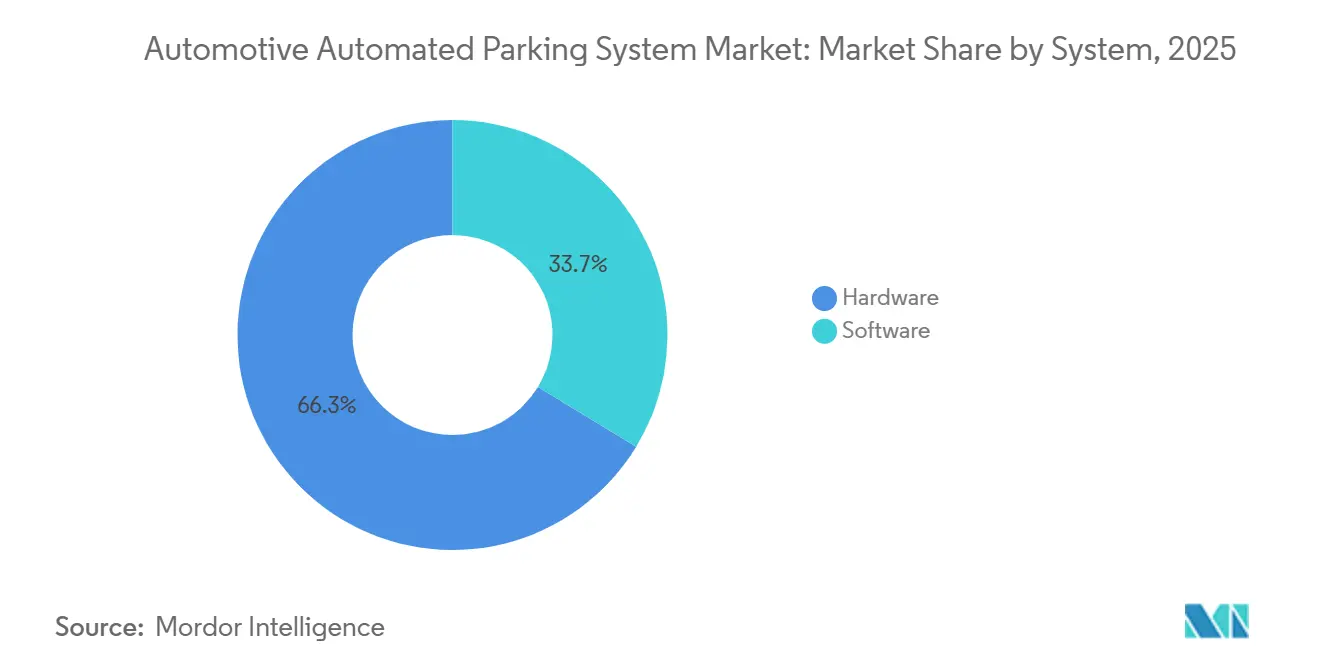

- By component, hardware contributed 66.25% of 2025 revenue, whereas software is the fastest-growing slice, expanding at an 18.65% CAGR through 2031.

- By automation level, fully automated designs captured 55.03% of 2025 revenue and are advancing at a 23.01% CAGR, markedly ahead of semi-automated alternatives.

- By platform type, pallet-based systems led with 58.12% of 2025 revenue; non-palletted solutions are increasing at a 16.05% CAGR.

- By drive technology, hydraulic lifts retained 49.33% of 2025 installations, yet robotic AGV and shuttle platforms are the pace-setters at an 18.12% CAGR.

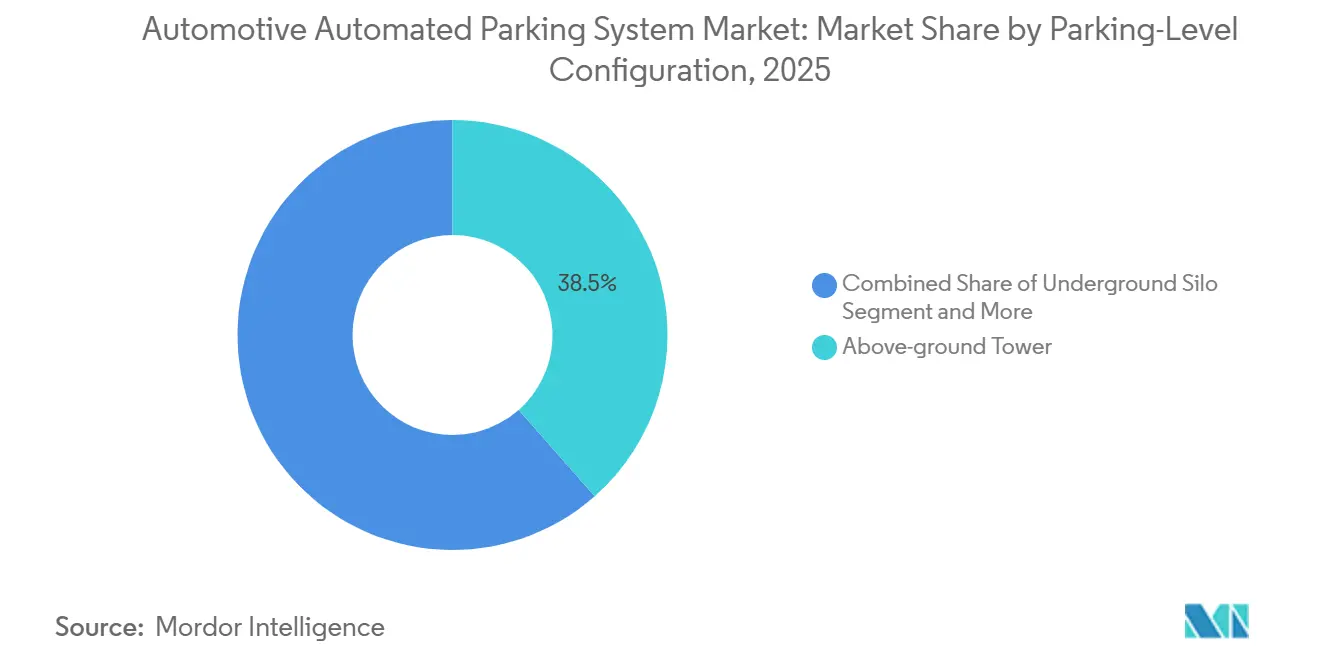

- By parking-level configuration, the above-ground tower captured 38.46% of 2025 revenue, while the shuttle and AGV-based segment will grow at a 17.02% CAGR.

- By end user, commercial venues supplied 60.13% of 2025 deployments, while residential projects recorded the quickest rise at 17.54% CAGR.

- By mode of sales, new installations captured 73.44% in 2025 revenue, while refrofit channel is set to expand at a 16.74% CAGR.

- By geography, Europe held 40.18% of 2025 revenue; Asia-Pacific posts the strongest regional trajectory at a 16.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Automated Parking System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land Scarcity and Real-Estate Inflation | +3.2% | Global, the highest in North America and the Asia-Pacific mega-cities | Long term (≥ 4 years) |

| Mandates for Connected Parking | +2.8% | Europe, North America, the United Arab Emirates, and Saudi Arabia | Medium term (2-4 years) |

| Vehicle Ownership in Mega-Cities | +2.5% | China, India, and Latin American capitals | Long term (≥ 4 years) |

| Automated Valet Parking | +2.1% | Germany, Japan, United States pilot corridors | Medium term (2-4 years) |

| Parking-as-a-Service Models | +1.6% | Early adoption in North America and Europe | Short term (≤ 2 years) |

| ESG and Green-Building Incentives | +1.4% | Europe, North America, emerging Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban Land Scarcity and Real-Estate Inflation

In Manhattan, condominium parking spaces are highly valued. Meanwhile, construction costs have significantly increased in cities like Tokyo, Singapore, and Sydney during 2020-2025. Automated parking systems reduce the space required per car, freeing up leasable area and enhancing the internal rates of return for projects. For example, Amsterdam’s Vijzelgracht tower requires substantially less land compared to a traditional ramp garage and operates under a long-term service contract. Similarly, developers in Brickell, Miami, are leveraging these benefits, recovering their automated parking investments within a few years through higher condo prices.

Smart-City Mandates for Connected Parking Infrastructure

By 2027, Washington, D.C. will require new commercial buildings to pre-wire a portion of their bays for electric vehicle (EV) charging. Meanwhile, California's CalGreen code offers density bonuses to those who meet parking minimums using automated solutions. European airports are also adapting: In 2025, Frankfurt Airport installed ultrasonic sensors, enabling mobile apps to direct drivers to available parking slots. These initiatives are driving up the demand for cloud-connected systems that can relay occupancy data in real-time through V2X links.

Rising Vehicle Ownership and Congestion in Mega-Cities

In 2025, Delhi experienced a significant surge in its vehicle count, while Bengaluru also witnessed substantial growth in its fleet, leading to increased pressure on already limited parking spaces. This rapid rise in vehicle numbers has highlighted the urgent need for innovative parking solutions in urban areas. Meanwhile, China has taken proactive steps by implementing numerous robotic garages, with Shanghai conducting trials of underground parking spots at various locations. These automated towers, designed to accommodate a large number of vehicles within a footprint smaller than a basketball court, offer a practical and efficient solution for urban areas facing land constraints and rising vehicle density. By optimizing space usage and reducing the dependency on traditional parking methods, such technologies are becoming increasingly relevant in addressing the challenges posed by urbanization and growing vehicle ownership.

Automated Valet Parking (AVP) Roll-Outs for Level-4 AV Fleets

ISO 23374-1:2023 establishes the protocols for Level-4 vehicles operating within robotic garages, ensuring seamless and efficient navigation. These standards are designed to facilitate the safe and autonomous movement of vehicles in controlled environments. In Germany, Bosch and APCOA have approved several locations, including Stuttgart Airport, where vehicles can autonomously transition from designated drop-off zones to parking spaces. This process is facilitated by infrastructure-provided occupancy maps, which guide the vehicles to available spots with precision. Such advancements highlight the growing adoption of automated parking solutions. Simultaneously, BMW and Valeo are working to integrate these advanced Level-4 valet capabilities into their upcoming vehicle models, aiming to enhance convenience, safety, and automation for users. These developments signify a significant step forward in the evolution of autonomous vehicle technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex and ROI Uncertainty | -2.2% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Operational Reliability and Safety | -1.8% | Worldwide, especially in residential settings | Medium term (2-4 years) |

| Cyber-Security Risks | -1.6% | North America and Europe have high connectivity | Short term (≤ 2 years) |

| Lag In Building Codes | -1.3% | North America and many Asia-Pacific countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and ROI Uncertainty

In urban centers, capital outlays per stall can lead to extended payback periods, with suburban areas experiencing even longer durations due to lower population density and reduced demand. At Brickell House, an early-generation system encountered multi-day outages, which disrupted operations and culminated in a substantial legal judgment in 2024. This incident underscores the significant financial risks associated with operational downtime, particularly for property owners relying on consistent system performance. Although Parking-as-a-Service eases the upfront financial burden by reducing initial capital requirements, the revenue share taken by the service provider diminishes long-term profit margins, potentially impacting the overall financial viability of such investments.

Operational Reliability and Safety Concerns

In 2024, Klaus Multiparking effectively utilized predictive analytics to address critical issues such as oil leaks and pump failures in hydraulic lifts, achieving a significant reduction in unplanned downtime. This proactive approach not only enhanced operational efficiency but also minimized disruptions in service. However, despite the existence of global safety standards like EN 14010:2003, which require interlocks to prevent pedestrian entry during lift motion, compliance levels remain alarmingly low across many regions. This lack of adherence has led to increased risks and subsequently higher insurance costs for businesses operating in the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Software Monetization Outpaces Hardware Sales

Hardware commanded 66.25% of 2025 revenue, yet software is expanding at an 18.65% CAGR, a notable increase posted by hardware. The automotive automated parking system market size for software platforms is projected to add significant revenue between 2026 and 2031 as operators monetize data, licensing, and mobile payments. Smart Parking Limited’s FY 2024 results showcase the model, with cloud fees, ANPR penalties, and analytics underwriting significant gross margins [1]“FY 2024 Investor Presentation,” Smart Parking Limited, smartparking.com.

Retrofit demand is strong: Orlando International Airport awarded over USD 13 million in 2025 to overlay camera-based guidance across five existing garages, cutting driver search time by 40%. Vendors echo a wider industrial shift where software enjoys 60-80% margins versus 15-25% for hardware, prompting bundled 10-15-year service contracts that guarantee uptime and steady cash flow.

By Automation Level: Fully Automated Systems Dominate

Fully automated designs controlled 55.03% of 2025 sales and are climbing at 23.01% CAGR. At Lyon Airport, several Stan AGVs park or retrieve a vehicle in under two minutes, a metric impossible for semi-automated lifts that demand driver alignment onto pallets. Residential towers in Miami replicate the speed, retrieving cars within four minutes and enabling 15-30% premium fees.

Semi-automated platforms still suit low-turnover office blocks due to 20-30% lower capex, but ISO 23374-1 compliance is pushing fleet owners toward systems capable of hands-free drop-off. The automated parking system market share for fully automated configurations is expected to rise significantly by 2031, widening today’s lead.

By Platform Type: Pallet Systems Prevail, But AGVs Gain

Pallet-based architectures held 58.12% of 2025 revenue because they retrofit easily into older garages, and a single seized pallet can be swapped in hours rather than days. European mixed-use developments, such as Düsseldorf’s MIZAL, embed pallets fitted with EV-charging contacts, future-proofing stalls as electrification accelerates.

Non-palleted AGV solutions are scaling quickly with a 16.05% CAGR, where new builds allow designers to shave eight inches of headroom per level. AGVs directly grasp wheels, accommodating heavier electric SUVs without the pallet weight penalty. Stanley Robotics’ 3-ton robots raise per-cubic-meter density by up to 50%, a decisive saving in land-scarce airports.

By Drive Technology: Robotic AGVs Cut Energy

Hydraulics still account for 49.33% of installed stalls and remain popular in deep underground silos, particularly in seismic zones. Yet robotic AGV and shuttle systems, which draw only 1.5-3 kWh per cycle, are growing fastest at 18.12% CAGR. Alliance deals like the Hyundai WIA–Hyundai Elevator MOU aim to lift payload capacity to 3.4 tons, supporting heavier commercial EVs.

Electro-mechanical chain-drive lifts offer a midpoint in cost and energy use, and regenerative braking now recovers up to 20% of descent energy. As utility tariffs rise and ESG scoring intensifies, operators increasingly model total-cost-of-ownership, tilting procurement toward lower-energy formats despite higher sticker prices.

By Parking-Level Configuration: Horizontal Shuttles Challenge Towers

Above-ground towers captured 38.46% share in 2025, while the shuttle and AGV-based segment will expand at a 17.02% CAGR. Iconic above-ground towers such as Lödige’s DOKK1 showcase engineering prowess but lock owners into fixed capacity. Shuttle and AGV layouts grow horizontally; facilities can add extra robots rather than new concrete, paring expansion lead-time by 12 months. Underground silos remain in vogue where land costs are high, evident in London’s nine-level Fitzjohn project.

Puzzle and stacker lifts dominate smaller residential jobs, packing 10-50 vehicles at roughly half the per-stall capex of tower solutions. Hybrid schemes that splice silos with shuttles are appearing on sloped or heritage sites where a single geometry is impractical, keeping design-and-build specialists busy across Europe and Asia.

By End User: Residential Segment Accelerates

Commercial properties—airports, malls, offices—commanded 60.13% of 2025 revenue, yet multifamily complexes book the sharpest climb at 17.54% CAGR. United States rules that require a significant share of EV-ready stalls in new apartments by 2027 make automated options attractive because load-balancing software caps peak electrical draw. Luxury towers in Miami and Dubai even bundle robotic parking into penthouse amenities, converting a former expense into a profit center.

Government pilots in Amsterdam and Copenhagen aim to reclaim curb space for pedestrians, and logistics campuses add automated bays that flex with shift changes. Single-family uptake remains niche but showcases technical possibilities, from car-collection showpieces to subterranean “man-caves.”

By Mode of Sales: Retrofit Share Expands

In 2025, new-builds accounted for 73.44% of revenue, with Hong Kong's 1,800-stall robotic Park-and-Fly serving as a prominent example of this trend. Despite the dominance of new-builds, retrofit work is gaining traction, recording a robust 16.74% CAGR. This growth highlights the increasing appeal of retrofitting as a cost-effective alternative to constructing new facilities, especially in markets where space and resources are limited.

Airports in Orlando and Minneapolis have demonstrated the potential of retrofits by adopting sensor overlays and software dashboards, which have increased revenue per parking space by up to 15% without requiring any concrete work. Retrofits typically achieve break-even in 3-5 years, significantly faster than the payback period for new constructions. This shorter horizon, combined with the ability to enhance existing infrastructure, is driving the growing share of retrofits in the automated parking system market.

Geography Analysis

Europe led the automated parking system market with 40.18% of 2025 revenue and is poised for a notable CAGR to 2031. Clear codes under EN 14010 and TÜV certifications compress permitting to as little as nine months, giving German suppliers like Klaus Multiparking a home-field edge [2]“Annual Report 2024,” Klaus Multiparking, klaus-multiparking.com . Scandinavian cities deploy robotic garages to reclaim waterfront acreage for bicycle lanes, while the United Kingdom leans on retrofits that tuck systems into century-old basements.

Asia-Pacific delivers the steepest ascent at 16.35% CAGR. China fields several automated facilities and is piloting subterranean bays in Shanghai alone, aligning with its smart-city blueprint. With a significant number of registered vehicles, India's metros are outpacing surface supply, driving a surge in demand for space-efficient towers. In Japan, the earthquake-prone landscape leans towards hydraulic-damped silos, while South Korea gears up to export its AGV platforms by 2026. North America held a notable share of the market in 2025. United States airports, including Austin-Bergstrom and Orlando, invested heavily in 2025-2026 on smart garages, highlighting a focus on revenue and passenger ease. In Miami and Toronto, condo developers are turning to robotic parking to navigate stringent zoning laws, and California’s CalGreen code is spurring automated setups close to light-rail stations.

The Middle East and Africa contributed to the global revenue. In Dubai, automated parking bays are being integrated into LEED-Platinum skyscrapers, aligning with the UAE’s ambitious 2050 net-zero goals. Meanwhile, Riyadh’s Vision 2030 is planning several multi-level robotic garages within its mega-projects. However, in sub-Saharan Africa, unreliable power grids and limited project financing hinder broader adoption, leaving puzzle lifts as the prevalent choice. South America, with a small share, grapples with economic fluctuations. While malls in São Paulo are testing AGV pilots, currency volatility has postponed definitive orders. In Buenos Aires, commercial landlords are opting for retrofit sensors to boost existing utilization instead of constructing new facilities.

Competitive Landscape

Top suppliers Klaus Multiparking, Wöhr, Lödige, Westfalia Parking, and Hyundai Elevator dominate a significant portion of the market, indicating a moderately concentrated field. Long-duration service contracts serve as a protective barrier: Lödige has secured long-term, performance-guaranteed contracts in Amsterdam and Düsseldorf, ensuring customer loyalty through bundled maintenance and software upgrades. In a strategic move, Klaus Multiparking acquired U.S. distributor Harding Steel in 2024, merging German engineering with local fabrication to navigate around tariffs.

AGV specialists are shaking things up. Stanley Robotics, acquired by HL Robotics in 2024, operates extensively at Lyon Airport and is in the running at Gatwick, aiming to expand operations significantly by 2028[3]“HL Robotics Acquisition Press Release,” Stanley Robotics, stanley-robotics.com . Meanwhile, Hyundai Elevator has teamed up with Hyundai WIA, targeting Level-4 AV fleets and banking on ISO 23374 compliance and rapid retrievals to clinch bids at transit hubs.

Software capabilities are now the distinguishing factor: dynamic pricing enhances revenue per stall, predictive analytics reduces downtime, and ISO 27001 cyber audits command a premium. After notable CVEs in 2025, municipal buyers have started prioritizing vendors based on penetration-test outcomes and mechanical uptime.

Automotive Automated Parking System Industry Leaders

Westfalia Parking

Wohr Parking

Klaus Multiparking

Lodige Industries

Hyundai Elevator Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fort Smith Regional Airport and Republic Parking activated an automated ticket-and-gate solution, fully operational since January.

- November 2025: Cochin Smart Mission Ltd launched “ParKochi,” an AI-powered platform overseeing 2,000 city-wide bays across 30 zones.

- October 2025: Autech-Otis unveiled an XY “chess-type” robotic garage aimed at overseas dense-core projects.

- August 2025: Hyderabad Metro Rail Ltd neared completion of India’s first pallet-less, fully automated public garage at Nampally via a PPP model with Novum and Palis technology.

Global Automotive Automated Parking System Market Report Scope

The scope includes segmentation by system (hardware and software), automation level (semi-automated and fully automated), platform type (palleted and non-palleted), drive technology (hydraulic, electromechanical, and robotic AGV/shuttle), parking-level configuration (above-ground tower, underground silo, puzzle/stacker, shuttle and AGV-based, and hybrid structures), end user (residential, commercial, government, and industrial), and mode of sales (new installation and retrofit). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. Market size and growth forecasts are presented in terms of value in USD.

| Hardware |

| Software |

| Semi-Automated |

| Fully Automated |

| Palleted |

| Non-Palleted |

| Hydraulic |

| Electro-Mechanical |

| Robotic (AGV/Shuttle) |

| Above-ground Tower |

| Underground Silo |

| Puzzle/Stacker |

| Shuttle and AGV based |

| Hybrid Structures |

| Residential | Single-family homes |

| Multi-family complexes | |

| Commercial | Office buildings |

| Shopping malls and Retail centers | |

| Hotels and Hospitality | |

| Airports and Transportation hubs | |

| Hospitals and Healthcare facilities | |

| Universities and Education | |

| Government and Municipal | |

| Industrial and Logistics facilities |

| New Installation |

| Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By System | Hardware | |

| Software | ||

| By Automation Level | Semi-Automated | |

| Fully Automated | ||

| By Platform Type | Palleted | |

| Non-Palleted | ||

| By Drive Technology | Hydraulic | |

| Electro-Mechanical | ||

| Robotic (AGV/Shuttle) | ||

| By Parking-Level Configuration | Above-ground Tower | |

| Underground Silo | ||

| Puzzle/Stacker | ||

| Shuttle and AGV based | ||

| Hybrid Structures | ||

| By End User | Residential | Single-family homes |

| Multi-family complexes | ||

| Commercial | Office buildings | |

| Shopping malls and Retail centers | ||

| Hotels and Hospitality | ||

| Airports and Transportation hubs | ||

| Hospitals and Healthcare facilities | ||

| Universities and Education | ||

| Government and Municipal | ||

| Industrial and Logistics facilities | ||

| By Mode of Sales | New Installation | |

| Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the automated parking system market expected to grow through 2031?

It is projected to advance at a 15.41% CAGR from 2026-2031, lifting value to roughly USD 6.88 billion by the end of the period.

Which component of automated garages is expanding quickest?

Software platforms, thanks to cloud subscriptions and data services, are rising at an 18.65% CAGR.

Why are fully automated configurations gaining share?

They meet Level-4 AV standards, retrieve cars in under four minutes, and now claim more than half of global revenue.

What regions show the strongest future demand?

Asia-Pacific leads with a 16.35% CAGR due to vehicle-ownership surges in China and India and smart-city mandates.

Page last updated on: