Automotive Jacks Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 17.60 Billion |

| Market Size (2030) | USD 22.57 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

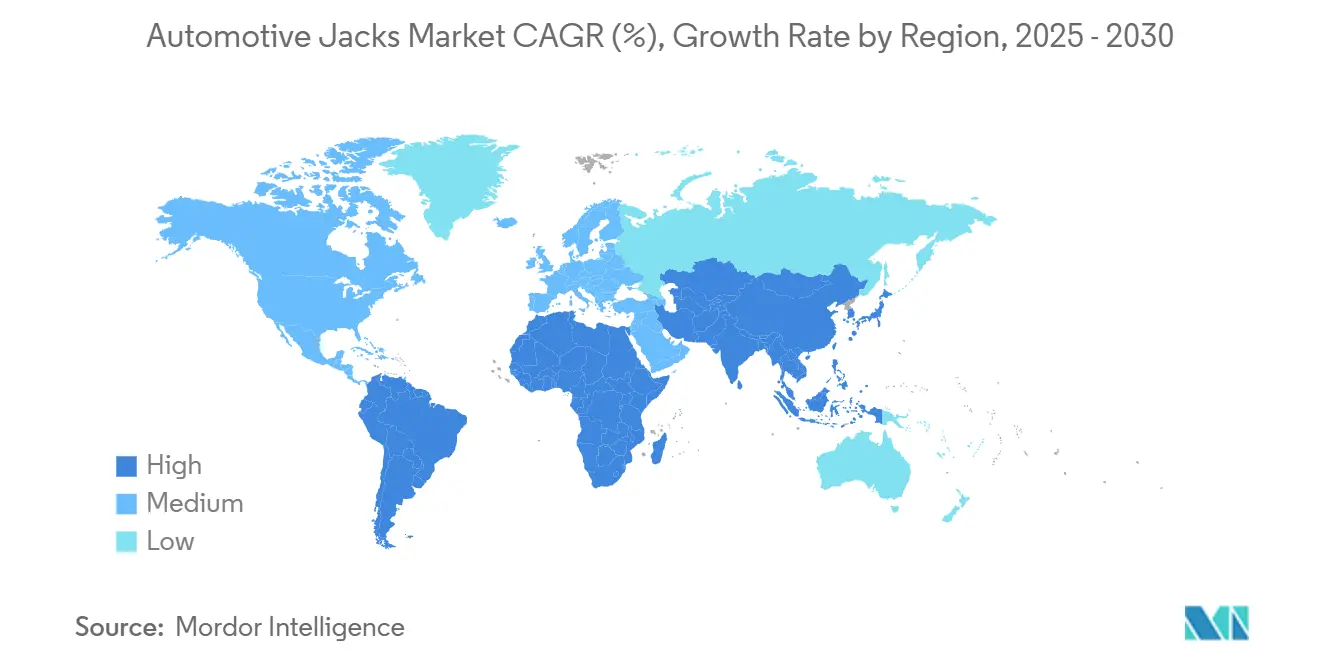

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Jacks Market Analysis by Mordor Intelligence

The automotive jacks market size stands at USD 17.6 billion in 2025 and is forecast to reach USD 22.57 billion by 2030, advancing at a 5.21% CAGR over the period. Sustained fleet expansion, particularly of SUVs and light trucks, underpins demand for higher-capacity lifting equipment, while electrification spurs investment in low-profile, battery-service jacks. Tightening global safety regulations, including OSHA’s six-month inspection mandate, reinforces the shift toward certified hydraulic systems. Growing e-commerce penetration enables direct-to-consumer sales that bypass traditional distributors, although offline channels remain dominant where professional consultation and immediate availability are critical. Competitive intensity remains moderate as leading brands differentiate through compliance with ASME PASE-2019, EV-specific designs, and connected maintenance features that align with fleet predictive-maintenance programs.

Key Report Takeaways

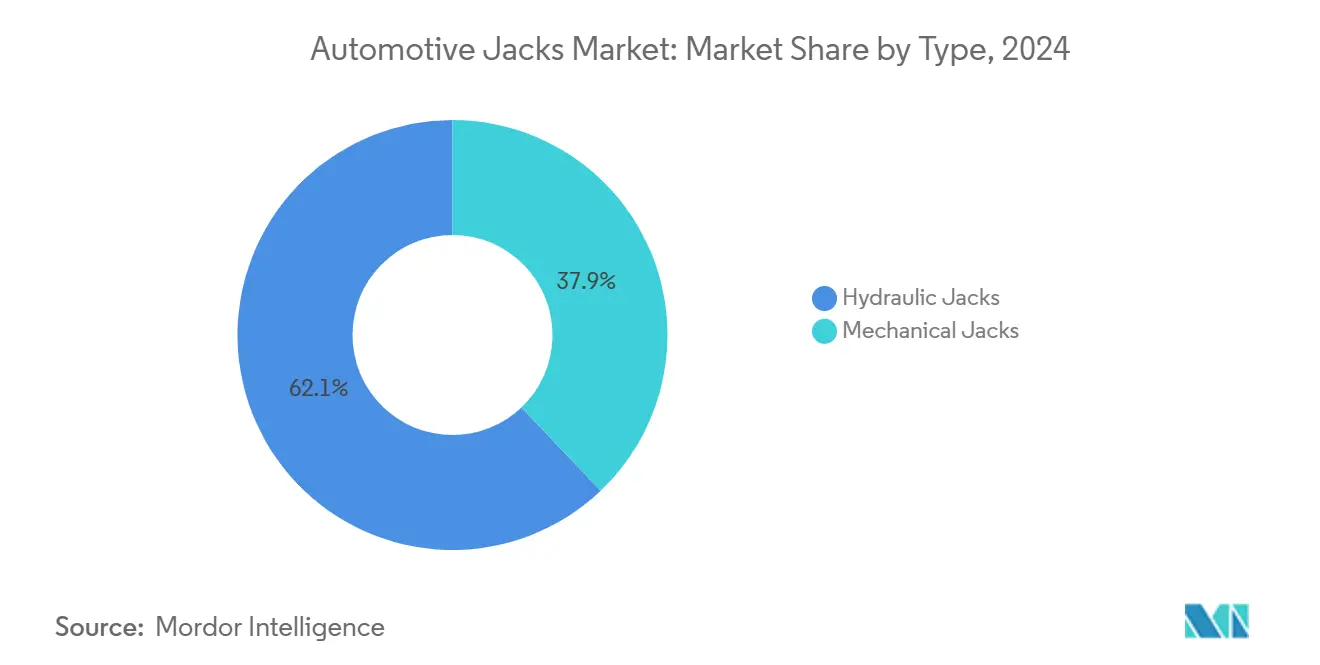

- By type, hydraulic jacks held 62.13 of % automotive jacks market share in 2024, while mechanical jacks posted a 6.82% CAGR to 2030.

- By jack type, floor jacks accounted for 34.97% of the automotive jacks market size in 2024; low-profile EV battery jacks grew fastest at an 8.47% CAGR through 2030.

- By weight capacity, the 2 to 4 tons segment captured 48.92% automotive jacks market share in 2024, whereas the above-4-tons category expands at 7.42% CAGR to 2030.

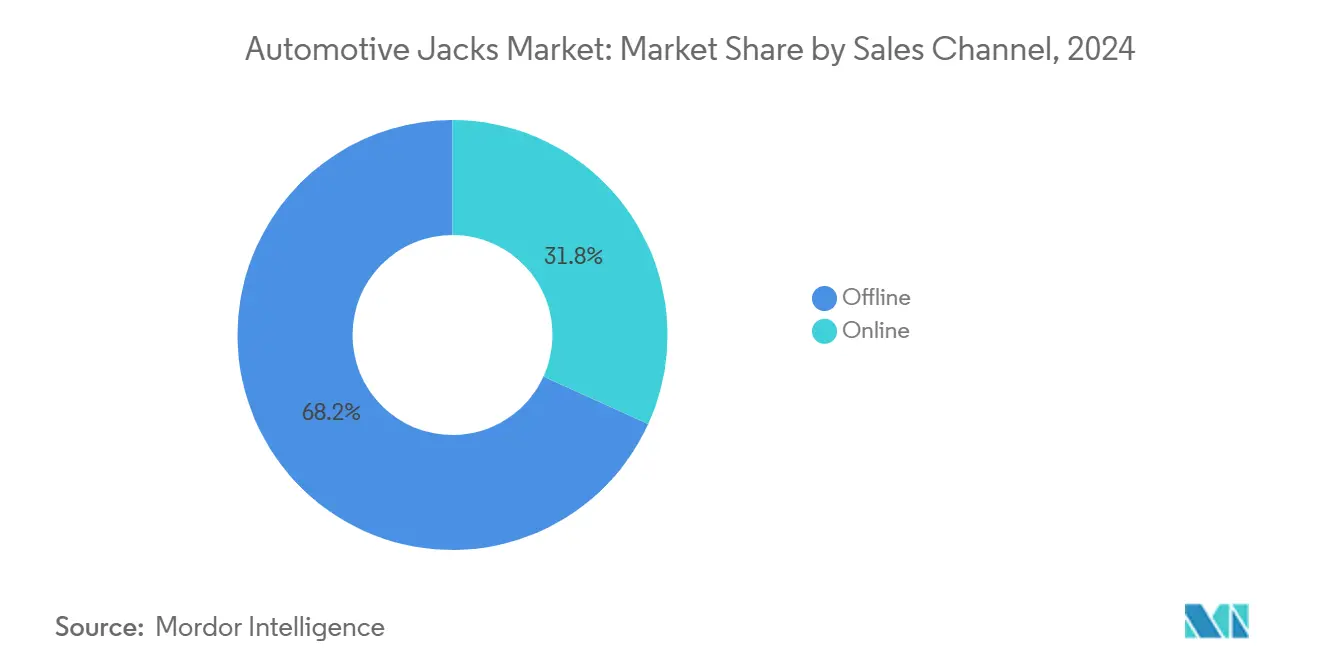

- By sales channel, offline outlets retained 68.16% revenue share in 2024, but online sales accelerated at a 9.19% CAGR through 2030.

- Asia-Pacific led with 38.07% automotive jacks market share in 2024, while South America records the highest regional CAGR at 6.91% to 2030

Global Automotive Jacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Vehicle Parc and Aging Fleet | +1.2% | North America, Europe, Global Emerging Markets | Long Term (≥ 4 Years) |

| EV-Specific Low-Profile Designs | +0.9% | North America, EU, China | Medium Term (2-4 Years) |

| DIY Repair Culture and E-Commerce Sales | +0.8% | North America, EU, Urban Asia-Pacific | Medium Term (2-4 Years) |

| Expansion of Professional Service Centers | +1.0% | Asia-Pacific Core, MEA, South America | Long Term (≥ 4 Years) |

| Higher SUV/Light-Truck Penetration | +0.6% | Global, Led by North America and China | Medium Term (2-4 Years) |

| IoT-Enabled Hydraulic Jacks | +0.4% | North America, EU Fleets | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Growing Global Vehicle Parc and Aging Fleet

The expanding global vehicle population in North America, creates sustained demand for maintenance equipment, including automotive jacks. This demographic shift particularly benefits the aftermarket, as vehicles over 10 years old account for 42.5% of parts and services spending according to MEMA data. The aging trend accelerates in emerging markets where vehicle ownership rates climb, but replacement cycles extend due to economic constraints. Fleet operators increasingly rely on predictive maintenance strategies, driving demand for professional-grade hydraulic jacks capable of supporting heavier, more complex vehicle architectures. OSHA's stringent jack inspection requirements every 6 months for constant use applications further institutionalize demand patterns[1]"Occupational Safety and Health Administration," U.S. Department of Labor, osha.gov..

Rise of DIY Repair Culture and E-Commerce Parts Sales

DIY automotive repair has expanded at a 5.96% CAGR since 2020, outpacing professional services growth of 4.29%[2]"The Growth of Do-it-Yourself Vehicle Repair and Maintenance," Haynes Publishing, us.haynes.com., with DIY representing approximately 20% of U.S. automotive parts sales. This trend gained permanence beyond pandemic-driven adoption, as younger demographics (45-50% aged 18-44) embrace self-maintenance for cost savings averaging USD 3,993 annually per household. E-commerce penetration in the automotive aftermarket rose in 2020, creating direct-to-consumer channels that bypass traditional distributor markups. The shift toward digital purchasing particularly benefits manufacturers offering consumer-grade jacks with clear specifications and safety certifications.

Expansion of Professional Service Centers in Emerging Markets

Professional automotive service infrastructure expands rapidly across Asia-Pacific and Latin America, driven by urbanization and vehicle fleet modernization programs. China's automotive parts exports reached USD 75.577 billion in 2021, up 33.76%[3]"The auto parts industry in China," The Sourcing Associate, thesourcingassociate.com. year-over-year, reflecting both domestic capacity building and export competitiveness in service equipment manufacturing. Brazil's fragmented service network of approximately 22,000 independent service stations plus 33,000 gas stations performing quick services creates substantial demand for portable and mid-capacity jacks suited to space-constrained operations. Service center expansion in emerging markets often prioritizes cost-effective, durable equipment over premium features, creating opportunities for manufacturers offering value-engineered products meeting local safety standards. The trend toward franchise-based service models, particularly in markets like India and Southeast Asia, standardizes equipment procurement and creates volume purchase opportunities.

Increased SUV and Light-Truck Penetration (Higher-Load Jacks)

Light trucks represented approximately 78% of new vehicle sales in 2023, driving demand for higher-capacity jacks capable of supporting increased curb weights and ground clearances. This vehicle mix shift creates sustained demand for jacks in the 2-4 ton and above-4 ton capacity ranges, particularly as electric SUVs and trucks add battery weight that can exceed traditional jack specifications. Commercial fleet operators increasingly specify higher-capacity equipment to accommodate diverse vehicle types within single service bays. The trend toward off-road and adventure vehicle segments further drives demand for specialized jacks like SUNEX's 2-ton off-road jack (model 6602RJ) designed for rough terrain applications. Regulatory compliance becomes critical as OSHA requires jack capacity ratings to exceed actual loads with appropriate safety margins, making capacity specification a key competitive differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Recalls and Stricter Standards | -0.7% | North America, EU | Short Term (≤ 2 Years) |

| Counterfeit Low-Cost Jacks | -0.5% | Global Online Channels | Medium Term (2-4 Years) |

| Heavier EV Curb Weights vs Legacy Capacity | -0.4% | Global EV Markets | Medium Term (2-4 Years) |

| Run-Flat Tires and Sealant Kits | -0.3% | North America, EU Premium | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Safety Recalls and Stringent Lift-Equipment Standards

High-profile safety recalls, exemplified by Harbor Freight's recall of over 1.7 million Pittsburgh Automotive jack stands due to collapse risks, intensify regulatory scrutiny and consumer safety awareness. OSHA's comprehensive jack safety requirements under 29 CFR 1910.244 mandate regular inspections, proper capacity marking, and immediate removal of defective equipment, creating compliance costs that disproportionately impact smaller manufacturers. Australian regulatory enforcement demonstrates global tightening, with multiple retailers paying penalties exceeding AUD 10,000 for selling non-compliant jacks that failed mandatory safety testing. The trend toward mandatory third-party testing and certification increases product development costs while extending time-to-market for new designs. Manufacturers must balance innovation with compliance, as safety failures can trigger industry-wide reputation damage and regulatory backlash that constrains market growth.

Proliferation of Counterfeit Low-Cost Jacks

Counterfeit automotive jacks represent a significant portion of the estimated USD 45 billion global counterfeit automotive parts market, with 94% originating from China according to EUIPO enforcement data. These products undercut legitimate manufacturers by avoiding research, development, and safety testing costs while exploiting online marketplace distribution channels. The safety risks are substantial, as counterfeit jacks typically use substandard materials and bypass regulatory compliance requirements, creating liability exposure for distributors and end users. Brand protection efforts require significant investment in marketplace monitoring, test purchases, and legal enforcement across over 150 online platforms. The problem intensifies in price-sensitive segments where consumers prioritize cost over safety certifications, particularly in emerging markets where regulatory enforcement remains limited. Legitimate manufacturers face margin pressure and market share erosion while investing in anti-counterfeiting measures and consumer education programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hydraulic Dominance Drives Innovation

Hydraulic jacks command 62.13% market share in 2024, reflecting their superior load capacity, operational efficiency, and professional adoption across service centers and fleet operations. The hydraulic segment grows at 6.82% CAGR through 2030, driven by technological advances in pump design, seal materials, and integrated safety features that address OSHA compliance requirements. Mechanical jacks retain relevance in consumer and emergency applications where simplicity, reliability, and lower cost outweigh hydraulic advantages. The segment benefits from DIY repair culture growth, particularly among younger demographics who value mechanical systems' transparency and repairability.

Professional service centers increasingly specify hydraulic systems for their speed and precision, while mechanical alternatives find favor in rural markets and developing regions where hydraulic fluid availability and maintenance expertise remain limited. Enerpac's focus on high-pressure hydraulic solutions and battery-powered portable pumps exemplifies innovation trends that blur traditional boundaries between hydraulic and mechanical categories. Regulatory compliance factors increasingly favor hydraulic systems that can integrate pressure monitoring and safety shutoff features required by evolving workplace safety standards.

By Jack Type: EV Adaptation Reshapes Product Mix

Floor jacks maintain the largest share at 34.97% in 2024, benefiting from their versatility across passenger and light commercial applications, while Low-Profile EV Battery Jacks emerge as the fastest-growing segment at 8.47% CAGR through 2030. This growth reflects the automotive industry's electrification transition and the specialized service requirements of underfloor battery systems. Bottle jacks retain strong positions in emergency and space-constrained applications, while farm jacks serve specialized agricultural and off-road markets with unique lifting requirements. Scissor jacks face pressure from run-flat tire adoption and OEM cost reduction initiatives but maintain relevance in aftermarket replacement and DIY segments.

The emergence of Tesla-specific jack pads and EV-compatible lifting solutions, such as SUNEX's model 66TLP4, demonstrates how product innovation responds to evolving vehicle architectures. Professional service requirements drive demand for specialized transmission jacks and underhoist stands, with SUNEX offering capacities from 700 to 3,000 pounds across multiple configurations. ASME PASE-2019 certification becomes increasingly important as professional users prioritize safety compliance and liability protection. The "Other Jacks" category includes emerging designs for specific applications, from IoT-enabled fleet maintenance solutions to lightweight composite materials that reduce operator fatigue while maintaining load capacity.

By Sales Channel: Digital Transformation Accelerates

Offline channels maintain 68.16% market share in 2024, reflecting the importance of physical inspection, professional consultation, and immediate availability in jack purchasing decisions. However, online sales accelerate at 9.19% CAGR through 2030, driven by e-commerce platform improvements, detailed product specifications, and competitive pricing that appeals to both DIY consumers and small commercial operators. The channel shift gained momentum during pandemic-era supply chain disruptions when traditional distributor networks faced inventory and delivery challenges.

Independent auto repair shops demonstrate mixed online adoption patterns, with 50.2% using public e-commerce websites in 2021, down from pandemic peaks but still above pre-2020 levels. Smaller shops (1 to 3 bays) show higher online procurement rates and greater price sensitivity, while larger operations prefer established supplier relationships for faster delivery and technical support. Enerpac's e-commerce expansion across 18 European countries, generating significant transaction volumes and lead generation, exemplifies how traditional manufacturers adapt to digital channels. The trend toward direct-to-consumer sales challenges traditional distributor markups while requiring manufacturers to invest in digital marketing, customer service, and logistics capabilities.

By Weight Capacity: Heavy-Duty Segment Gains Momentum

The 2 to 4 Tons segment holds 48.92% market share in 2024, reflecting the sweet spot for passenger vehicle and light commercial applications where capacity meets portability requirements. The Above 4 Tons category grows fastest at 7.42% CAGR through 2030, driven by commercial vehicle fleet expansion, heavy-duty pickup truck adoption, and electric vehicle weight increases that challenge traditional capacity assumptions. The Below 2 Tons segment serves emergency, consumer, and specialized applications where weight and storage constraints outweigh maximum capacity considerations.

Commercial fleet operators increasingly standardize on higher-capacity equipment to accommodate diverse vehicle types within single service bays, while regulatory requirements mandate capacity margins above actual vehicle weights. The trend toward SUV and light truck dominance, representing 78% of new vehicle sales in 2023, creates sustained demand for mid-range and heavy-duty jacks. Electric vehicle adoption complicates capacity planning as battery packs add significant weight to traditional vehicle categories, requiring service centers to upgrade equipment specifications. OSHA compliance requirements for proper capacity marking and load testing create additional considerations for manufacturers targeting professional markets where safety documentation and traceability become competitive differentiators.

Geography Analysis

Asia-Pacific dominated with 38.07% automotive jacks market share in 2024, fueled by China’s 25 million-unit annual vehicle output and extensive domestic parts supply chains. Government policies such as Made in China 2025 and export rebate incentives support local jack manufacturing clusters, enabling price-competitive hydraulic models that meet AS 2615:2016 standards. India’s vehicle parc crossed 295 million units in 2024, and service-center franchising accelerates equipment standardization across tier-2 cities. Japan and South Korea contribute design innovations in seals and alloys that flow into global premium offerings.

North America retains significant relevance as the average vehicle age surpasses 12.6 years, intensifying aftermarket activity. USMCA rules of origin that require 75% regional content for light vehicles nudge OEMs to source lifting equipment domestically, benefitting U.S. and Mexican plants. The region’s entrenched DIY culture continues to favor mechanical scissor jacks, yet professional workshops replace aging 3-ton floor jacks with 4-ton hybrid-steel designs to accommodate heavier EVs. Canada’s parts retailers expand curbside pickup for >30-kilogram equipment, blending online ordering with offline fulfillment to bridge channel preferences.

South America exhibits the fastest CAGR at 6.91% to 2030, anchored by Brazil’s 22,000 independent service stations requiring cost-effective, durable jacks. MERCOSUR tariff alignment promotes intra-regional trade, stimulating localized assembly of bottle and floor jacks to sidestep import duties. Argentina’s macro volatility tempers short-term spending, yet government fleet-renewal programs spur procurement of heavy-duty hydraulic units. Rural infrastructure expansion, including USD 18.3 billion earmarked for Brazilian roads, lengthens travel distances and raises roadside service risks, indirectly boosting market demand.

Competitive Landscape

The automotive jacks market features moderate concentration. Players like Snap-on and SUNEX focus on brand trust and ASME certification to differentiate from lower-priced imports. Snap-on’s 2013 acquisition of Challenger Lifts broadened its under-car portfolio and enabled cross-selling into dealer networks where OEM-specific adapters command premium margins. Enerpac leverages industrial-grade hydraulic expertise to penetrate fleet and heavy-vehicle segments, achieving 5.0% organic sales growth in FY 2025 on the back of new portable pump launches.

Regional specialists such as GEDORE in Europe and Matco Tools in North America reinforce positions with annual tool fairs and award-winning innovations that keep product lines fresh. Counterfeit risk drives established brands to invest in serialization and warranty registration programs, an area where smaller challengers struggle to match resource commitments. Product roadmaps converge on low-profile EV solutions, sensor integration, and aluminum-alloy frames to reduce jack weight without compromising capacity, all supporting a shift toward premiumization within the automotive jacks market.

White-space opportunities lie in telematics-enabled jacks for fleet compliance documentation and affordable ASME-certified units for emerging-market workshops. Entrants with proprietary IoT stacks can collaborate with fleet-management software vendors, while local assembly partnerships help mitigate import tariffs in price-sensitive regions. Manufacturers that align with tightening safety regimes and offer comprehensive training packages solidify trust among professional users wary of liability exposure

Automotive Jacks Industry Leaders

-

Torin Jacks Inc. (Big Red)

-

Shinn Fu Corporation of America (SFA)

-

Snap-on Incorporated

-

Harbor Freight Tools USA Inc.

-

Sunex Tools Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Harbor Freight Tools showcased Badland 1.5T Off-Road Jack and Daytona 3T Super Duty Floor Jack at SEMA Show 2024, demonstrating continued product development in consumer and professional segments.

- November 2024: SUNEX Tools released 2-ton off-road jack (model 6602RJ) featuring compact design, 28.4-inch lift height, heavy-duty wheels, and dual pistons for rapid lift capability suitable for rough terrain applications.

Global Automotive Jacks Market Report Scope

| Mechanical Jacks |

| Hydraulic Jacks |

| Floor Jacks |

| Bottle Jacks |

| Farm Jacks |

| Scissor Jacks |

| Other Jacks |

| Online |

| Offline |

| Below 2 Tons |

| 2 to 4 Tons |

| Above 4 Tons |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of APAC | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Mechanical Jacks | |

| Hydraulic Jacks | ||

| By Jack Type | Floor Jacks | |

| Bottle Jacks | ||

| Farm Jacks | ||

| Scissor Jacks | ||

| Other Jacks | ||

| By Sales Channel | Online | |

| Offline | ||

| By Weight Capacity | Below 2 Tons | |

| 2 to 4 Tons | ||

| Above 4 Tons | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of APAC | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which jack type is growing fastest?

Low-profile EV battery jacks post an 8.47% CAGR through 2030 as service centers adapt to electric vehicles.

What regional market is expanding quickest?

South America records the highest CAGR at 6.91% thanks to Brazil’s expanding independent service network.

Why are hydraulic jacks preferred in workshops?

Hydraulic systems offer superior load capacity, faster lift cycles, and easier compliance with OSHA safety standards.

How is e-commerce influencing jack sales?

Online channels grow at 9.19% CAGR as detailed specifications and certified-seller programs build buyer confidence.

What safety regulations affect jack manufacturers most?

Compliance with ASME PASE-2019 and OSHA 29 CFR 1910.244 drives certification costs and product-design priorities.

Page last updated on: