Vehicle Access Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

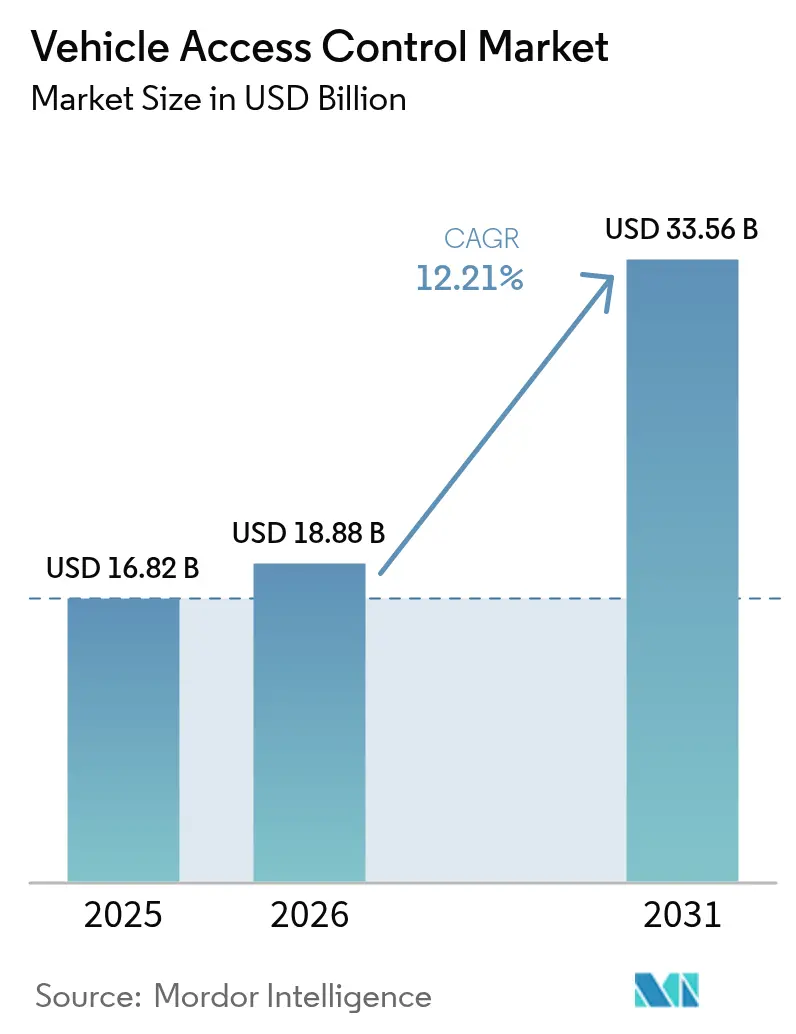

| Market Size (2026) | USD 18.88 Billion |

| Market Size (2031) | USD 33.56 Billion |

| Growth Rate (2026 - 2031) | 12.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

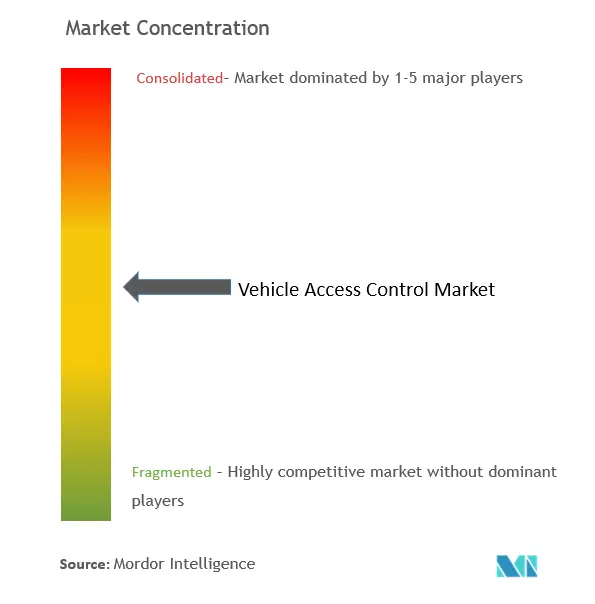

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vehicle Access Control Market Analysis by Mordor Intelligence

The vehicle access control market size is expected to grow from USD 16.82 billion in 2025 to USD 18.88 billion in 2026 and is forecast to reach USD 33.56 billion by 2031 at 12.21% CAGR over 2026-2031. Growth is propelled by tighter cybersecurity mandates, insurers’ premium incentives for anti-theft analytics, and rapid adoption of Ultra-Wideband (UWB) technology that counters relay attacks. Asia-Pacific anchors both volume and momentum, supported by China’s electric-vehicle surge and India’s manufacturing incentives. Biometric authentication is gaining double-digit traction, yet RFID and other non-biometric systems retain volume leadership because of mature supply chains. Commercial fleets and shared-mobility operators have become pivotal, demanding multi-user credential management that converts access hardware into recurring software revenues. Tier-1 suppliers remain influential, but disruptive semiconductor and cybersecurity specialists are carving defensible niches with post-quantum cryptography and secure element chipsets[1]"Regulation - 2024/2847 - EN", European Parliament and Council, eur-lex.europa.eu.

Key Report Takeaways

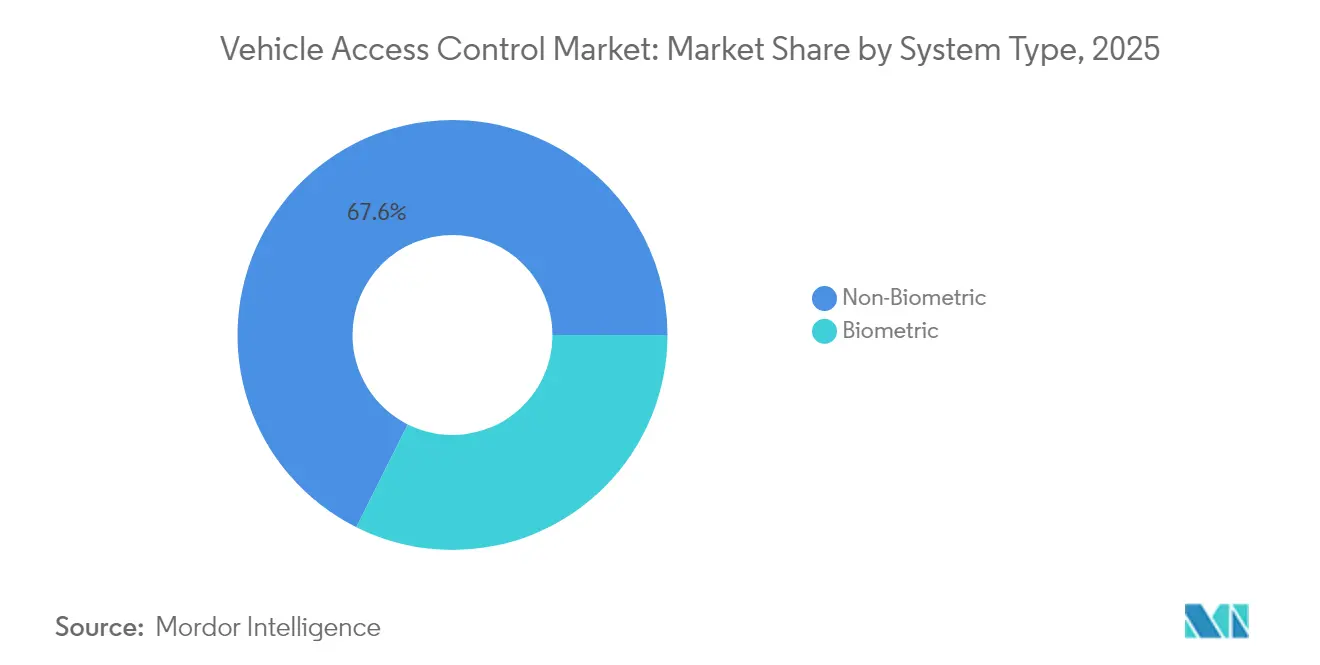

- By system type, non-biometric platforms held 67.62% of vehicle access control market share in 2025, while biometric systems are forecast to lead growth at 13.63% CAGR to 2031.

- By technology, RFID commanded 44.95% share of the vehicle access control market size in 2025, whereas UWB is projected to expand at 18.05% CAGR through 2031.

- By vehicle type, passenger cars captured 63.74% revenue share in 2025; shared-mobility and fleet vehicles are advancing at 13.98% CAGR to 2031.

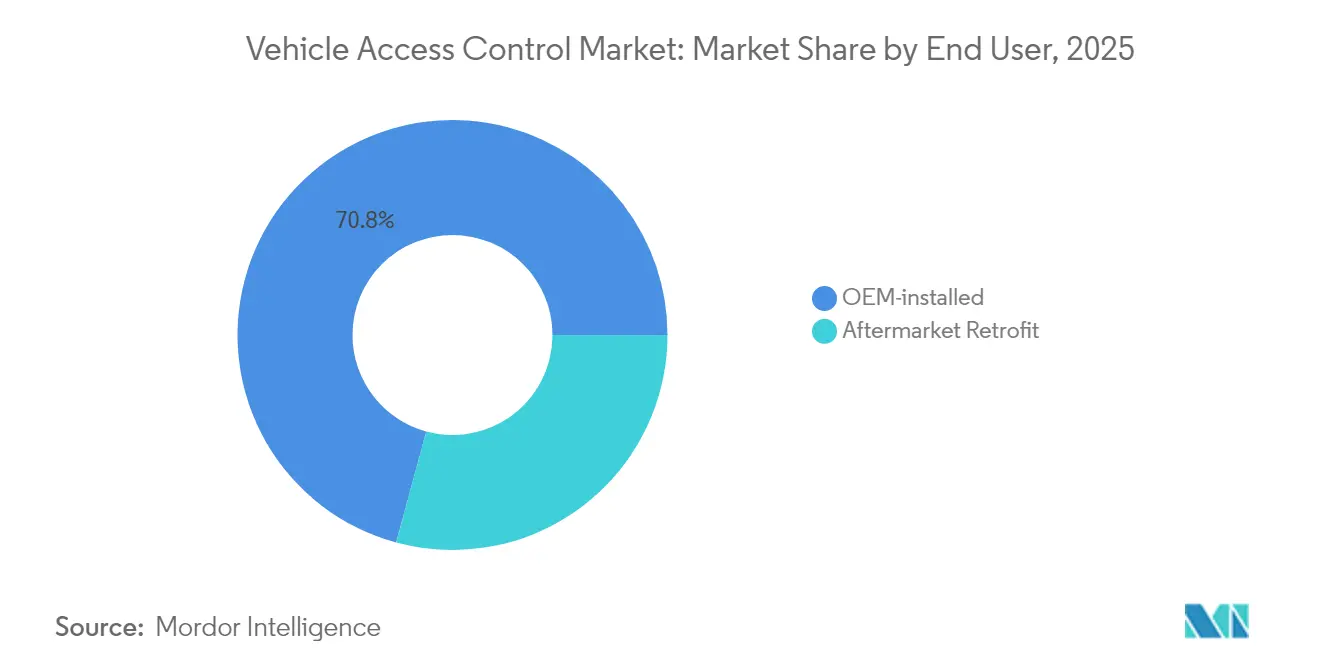

- By end user, OEM-installed solutions accounted for 70.78% of the vehicle access control market share in 2025, yet fleet and shared-mobility operators exhibit the highest 15.29% CAGR through 2031.

- By sales channel, direct-to-OEM transactions represented 65.11% of the vehicle access control market size in 2025, while e-commerce and aftermarket upgrades are growing at 15.43% CAGR.

- By geography, Asia-Pacific dominated with 42.87% share in 2025 and maintains the fastest 13.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vehicle Access Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Connected Vehicles | +2.5% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Push Toward Key-As-A-Service Platforms | +1.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Insurance Incentives for Integrated Anti-Theft Analytics | +1.2% | North America and EU core markets | Short term (≤ 2 years) |

| EU "Digit-Key" Regulation | +0.9% | EU primary, spillover to global standards | Medium term (2-4 years) |

| E-Commerce Dark-Hour Delivery Programs | +0.7% | Urban centers globally, led by North America and China | Short term (≤ 2 years) |

| Shift to Integrated Secure Element Chipsets | +0.6% | Global supply chain impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Connected And Autonomous-Ready Vehicles

Connected architectures have elevated access control from simple entry to the master authentication gateway for over-the-air updates, diagnostics, and autonomous coordination. BMW’s Digital Key Plus proves how UWB-driven spatial awareness enables automated parking and charging while preventing relay attacks[2]"BMW Digital Key Plus Ultra-Wideband", BMW Group, bmw.com . As the Car Connectivity Consortium codifies UWB in Digital Key 3.0, OEMs can justify higher per-unit pricing for secure positioning, accelerating adoption across premium and mass-market segments.

OEM Push Toward Key-As-A-Service Platforms

Subscription-based digital keys transform one-time hardware margins into recurring cloud revenue. Continental’s CoSmA allows multi-OEM credential lifecycle management, supporting dynamic feature upgrades that monetize convenience tiers. This model reduces key-fob logistics costs and supports shared-mobility by provisioning and revoking credentials in real time.

Insurance Incentives For Integrated Anti-Theft Analytics

Insurers now tie premium discounts to real-time theft-prevention analytics. Hyundai’s collaboration with AAA offers lower rates once upgraded software blocks key-cloning exploits[3]"Hyundai News Release", Hyundai Motor America, hyundainews.com. Reduced risk underwriting creates immediate ROI for both OEM and consumer, stimulating aftermarket retrofits that embed behavior analytics.

EU “Digit-Key” Regulation Mandating Tamper-Proof OTA Credentialing

The 2024 Cyber Resilience Act forces vehicle access control suppliers to embed hardware security modules that authenticate software throughout the vehicle lifecycle[4]"Cyber Resilience Act: A New Era In Product Cybersecurity", TÜV SÜD, tuvsud.com. Compliance costs reward firms with mature cybersecurity pipelines and ripple globally because suppliers standardize on the toughest rules to simplify platform deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cybersecurity and Zero-Day Exploits | -1.4% | Global, with higher impact in connected vehicle markets | Short term (≤ 2 years) |

| High BOM Cost for Premium Modules | -0.8% | Cost-sensitive markets, particularly emerging economies | Medium term (2-4 years) |

| Automotive E/E Architecture Consolidation | -0.6% | Developed markets with established aftermarket channels | Long term (≥ 4 years) |

| Fragmented Credential Standards Delaying V2X Trust | -0.5% | Global, with regional variations in implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity Vulnerabilities And Zero-Day Exploits

Open-source tools now clone eight remote-keyless protocols, with one fully compromised according to MIT research. Rapid attack evolution outpaces automotive patch cycles, keeping consumer anxiety high and inviting stricter oversight. Tesla’s past CVE-2022-37709 phone-key bypass exemplifies how even high-end designs can be undermined within months of launch.

High BOM Cost For Premium Biometric Modules

Automotive-qualified fingerprint ICs add USD 50-100 per vehicle, stressing margins in price-sensitive segments. Additional secure processing inflates budgets, restricting use to luxury models while volume cars persist with RFID or NFC.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Biometric Projects Challenge Non-Biometric Dominance

Non-biometric solutions sustained a 67.62% stronghold in 2025, driven by mature RFID and NFC price points and entrenched supply chains. Biometric alternatives, however, are pacing the vehicle access control market at a 13.63% CAGR as fingerprint and facial recognition find early success in luxury passenger cars. OEM pilots show that biometric modules dramatically cut theft claims, bolstering insurance rebates that erase part of the cost premium.

Volume adoption remains gated by sensor cost and privacy regulation, yet over 100 automakers and Tier-1s are prototyping biometric gateways. Continental’s 2025 CES showcase blended facial ID with vital-sign monitoring to detect unauthorized occupants, hinting at a future where access control doubles as a safety platform.

By Technology: UWB Surge Disrupts RFID Leadership

RFID retained 44.95% of 2025 revenue, but UWB’s 18.05% CAGR is resetting the competitive arc of the vehicle access control market. BMW, Volkswagen, and Hyundai embed UWB to build centimeter-grade secure zones that block signal amplification attacks. Semiconductor innovation, such as NXP’s NCJ29D5 chip, lowers integration hurdles and pushes UWB downmarket.

Bluetooth and NFC persist where cost ceilings matter or physical contact is preferred, for instance, in car-sharing pick-up spots. Wi-Fi and cellular serve background credential synchronization rather than immediate unlock.

By Vehicle Type: Fleets Break the Passenger-Car Mold

Passenger cars delivered 63.74% of 2025 revenue; nonetheless, fleet and shared-mobility vehicles are the new growth engines at 13.98% CAGR. Fleet operators value credential auditing, driver authentication, and automated maintenance triggers, monetizing access data in ways private owners cannot. Irdeto’s Keystone illustrates fine-grained, cloud-managed keys that feed compliance logs, a critical need in last-mile logistics.

Commercial adoption also spurs facial recognition to log driver shifts and tie access to telematics scoring for insurance optimization. Larger vehicles such as heavy trucks fold access control into broader domain control units, preparing the path for platooning and autonomous freight.

By End User: Shared Mobility Redefines Integration Priorities

OEM-installed hardware captured 70.78% in 2025 because factory integration simplifies warranty and functional safety validation. Yet shared-mobility and fleet customers expand fastest at 15.29% CAGR, demanding API-ready platforms that can hand out and revoke keys per trip. WirelessCar’s digital key suite underpins such dynamic workflows, cutting fob logistics and enabling monetization of vehicle time slots.

Aftermarket retrofits remain relevant in regions where older fleets seek insurance benefits quickly. Secure-element modules that marry CAN bus pins with Bluetooth Low Energy give aging vehicles modern defense without full E/E rewiring. However, continued consolidation of vehicle domain controllers may shrink addressable aftermarket nodes over the long term.

By Sales Channel: Online Upgrades Pressure Tier-1 Pipelines

Direct sales into OEM programs represented 65.11% of 2025 revenue. Vehicle electrification and centralized computing reinforce long design-in cycles that favor Tier-1 incumbents. Yet the aftermarket is blooming at 15.43% CAGR as consumers shop e-commerce kits to capture insurance discounts. Unified diagnostic connectors and plug-and-play harnesses simplify do-it-yourself installation, a trend especially visible in India’s aftermarket.

Over time, software-defined vehicles may re-centralize access credentials inside zonal controllers, limiting drop-in kit feasibility. Suppliers are responding with cloud-first key-management services that operate above the hardware layer, preserving aftermarket relevance in an ECU-consolidated world.

Geography Analysis

The Asia-Pacific’s 42.87% share in vehicle access control market in 2025 is rooted in strong EV volume and an integrated supply chain that spans semiconductors to final assembly. China’s 8 million EV sales in 2024 required secure keys that coordinate with charging infrastructure, while India’s domestic production push fuels demand for cost-optimized modules fueling growth of 13.12% CAGR through 2031. Japan and South Korea drive semiconductor innovation—Renesas and Samsung deliver secure microcontrollers that underpin next-generation credential vaults.

North America records a steady growth, leveraging high vehicle density and robust premium segments that readily pay for biometric and UWB additions. NHTSA guidelines and insurer incentives combine to standardize higher security baselines. The region’s leadership in ride-hailing and e-commerce fleets speeds multi-user credential experimentation, shaping global software-as-a-service feature sets.

Europe growth is moderate, but regulatory gravity outstrips raw growth. The Cyber Resilience Act cements tamper-proof OTA updating and post-quantum readiness as ticket-to-play requirements. Continental’s rebranding to Aumovio and pivot to software ecosystems reflect how suppliers adapt to regulation-led demand. OEMs often certify to EU standards first and roll the same architecture worldwide, making Europe’s policy stance a global bellwether.

Competitive Landscape

Moderate fragmentation typifies the vehicle access control market. Continental AG and Robert Bosch GmbH, both leverage decades-long OEM relationships, bundling keys with ignition, infotainment, and ADAS domains for cost efficiency. Valeo and Huf expand UWB portfolios to secure second-tier slots, while chipset vendors such as NXP and Infineon climb upstream with secure element solutions that close relay loopholes.

Disruptors exploit white space at the convergence of cybersecurity and access control. SEALSQ fields post-quantum-ready TPMs, solving long-horizon cryptographic compliance for OEMs. FiRa Consortium and Car Connectivity Consortium collaborations accelerate standards, rewarding early adopters with interoperability prestige. Competitive strategy tilts toward software, cloud credential orchestration locks in revenue far beyond hardware EBIT.

Acquisition appetite remains high as Tier-1s shore up software gaps. Bosch’s Perfectly Keyless passenger-car rollout demonstrates vertical integration, while Continental invests in AI-based occupant detection to merge personalization and security. The race now centers on securing end-to-end trust, from silicon root to OTA cloud, before autonomous features mandate formal safety certification.

Vehicle Access Control Industry Leaders

-

Continental AG

-

Lear Corporation

-

Robert Bosch GmbH

-

Denso Corporation

-

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SEALSQ Corp announced QVault TPM compliance with CRYSTALS-Dilithium and CRYSTALS-Kyber, enabling post-quantum protection for automotive keys.

- March 2025: Infineon showcased CRA-ready microcontrollers with RISC-V support for cost-effective automotive security.

- March 2024: NXP unveiled S32 CoreRide, merging processing, networking, and power domains to simplify secure key integration.

Global Vehicle Access Control Market Report Scope

Vehicle access control is a proximity detection system that allows controlled access and security of all vehicles on site, using several contactless technologies such as Bluetooth, Near field communications, and others.

The vehicle access control market is segmented into system type, technology, vehicle type, and geography. Based on the system type, the market is segmented into Biometric and Non-Biometric. Based on the technology, the market is segmented into near-field communications (NFC), bluetooth, RFID, and other technologies. Based on the vehicle type, the market is segmented into passenger cars and commercial vehicles. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Biometric | Fingerprint Recognition |

| Facial Recognition | |

| Iris / Retina Recognition | |

| Non-Biometric | RFID Tag and Reader |

| NFC / Bluetooth Low Energy | |

| Key Fob / Smart Card |

| RFID |

| Bluetooth |

| NFC |

| Ultra-Wideband (UWB) |

| Wi-Fi / Cellular |

| Passenger Cars | Hatchback |

| Sedan | |

| SUV / Crossover | |

| Commercial Vehicles | Light Commercial Vehicles |

| Heavy Trucks and Busses |

| OEM-installed |

| Aftermarket Retrofit |

| Direct to OEM |

| Tier-1 Supply |

| e-Commerce / Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| System Type | Biometric | Fingerprint Recognition |

| Facial Recognition | ||

| Iris / Retina Recognition | ||

| Non-Biometric | RFID Tag and Reader | |

| NFC / Bluetooth Low Energy | ||

| Key Fob / Smart Card | ||

| Technology | RFID | |

| Bluetooth | ||

| NFC | ||

| Ultra-Wideband (UWB) | ||

| Wi-Fi / Cellular | ||

| Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| SUV / Crossover | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Heavy Trucks and Busses | ||

| End User | OEM-installed | |

| Aftermarket Retrofit | ||

| Sales Channel (Cross-segmentation) | Direct to OEM | |

| Tier-1 Supply | ||

| e-Commerce / Aftermarket | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the vehicle access control market?

The vehicle access control market size stands at USD 18.88 billion in 2026 and will reach USD 33.56 billion by 2031.

Which region leads the vehicle access control market?

Asia-Pacific leads with 42.87% market share in 2025 and posts the fastest 13.12% CAGR through 2031.

Why is Ultra-Wideband technology gaining traction?

UWB offers centimeter-level positioning that blocks relay attacks, driving an 18.05% CAGR and challenging RFID dominance.

How are insurers influencing adoption?

Premium discounts for vehicles with anti-theft analytics make advanced access systems financially attractive, accelerating adoption.

Which segment is growing fastest by end user?

Shared mobility and fleet operators are expanding at 15.29% CAGR as they need real-time credential management.

What regulatory changes affect the market?

The EU’s Cyber Resilience Act mandates tamper-proof over-the-air credentialing, compelling global compliance upgrades in new systems.

Page last updated on: