Counter Cyberterrorism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.96 Billion |

| Market Size (2031) | USD 40.94 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

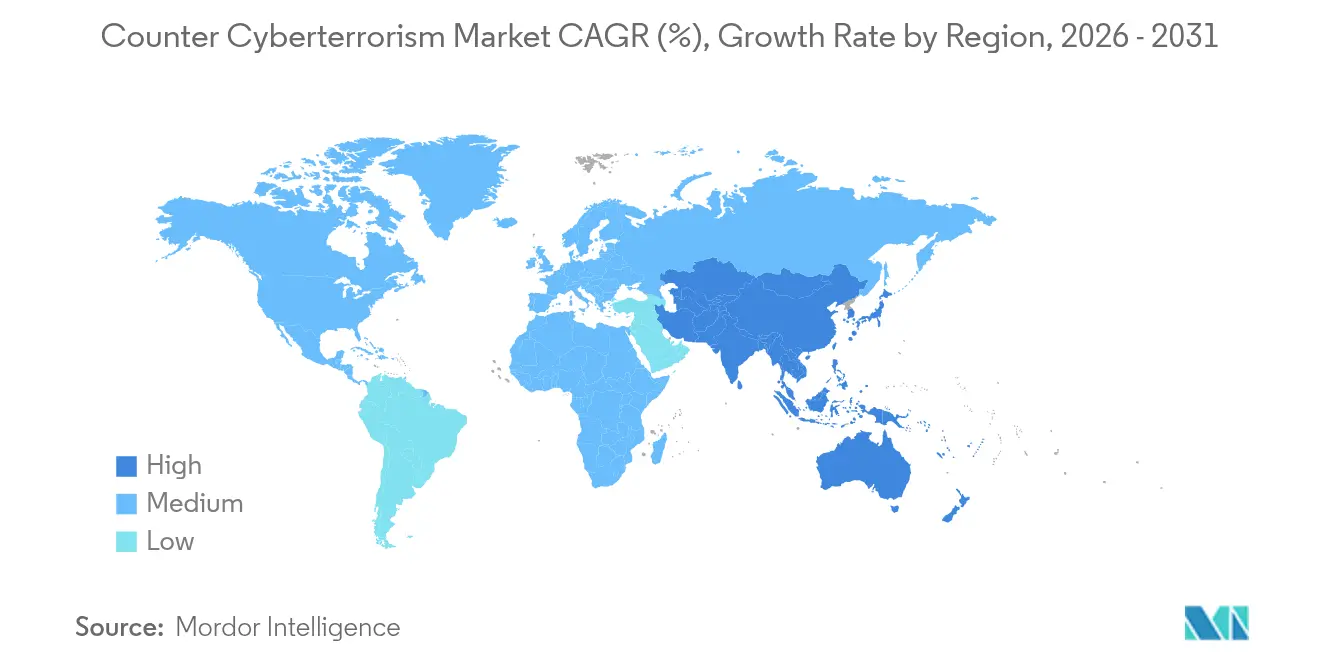

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

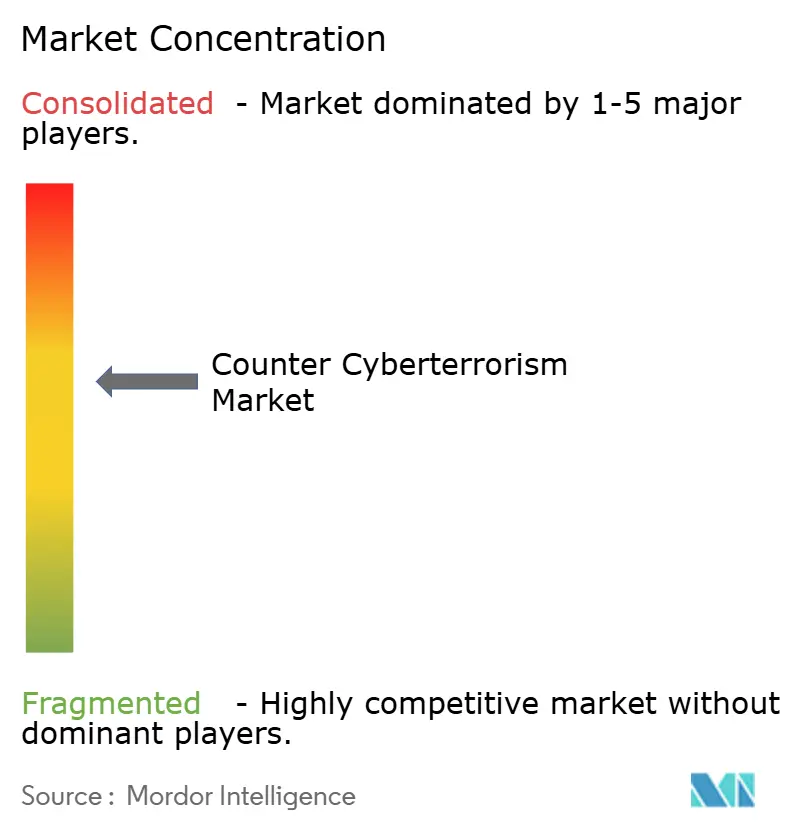

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Counter Cyberterrorism Market Analysis by Mordor Intelligence

The counter cyberterrorism market size was valued at USD 33.87 billion in 2025 and estimated to grow from USD 34.96 billion in 2026 to reach USD 40.94 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). Rising government allocations, escalating nation-state offensives, and wider adoption of AI-enabled security tools underpin this moderate but steady expansion. Federal programs such as the United States’ USD 27.5 billion cybersecurity budget and the Pentagon’s USD 14.5 billion cyber request demonstrate the scale of public-sector demand.[1]David Perera, “US Federal Budget Proposes $27.5B for Cybersecurity,” BankInfoSecurity, BANKINFOSECURITY.COM Growing defense-grade spending combines with corporate pivots from perimeter controls to threat-intelligence ecosystems, while cloud migration sustains demand for flexible deployment models. Vendor consolidation 362 cybersecurity deals worth USD 49.9 billion in 2024 also influences growth trajectories by bundling formerly discrete capabilities under integrated platforms.[2]CrowdStrike, “CrowdStrike Collaborates with NVIDIA to Advance Agentic AI,” CROWDSTRIKE.COM

Key Report Takeaways

- By solution type, network security led with 27.10% of the counter cyberterrorism market share in 2025, whereas AI-driven security is projected to expand at a 22.80% CAGR through 2031.

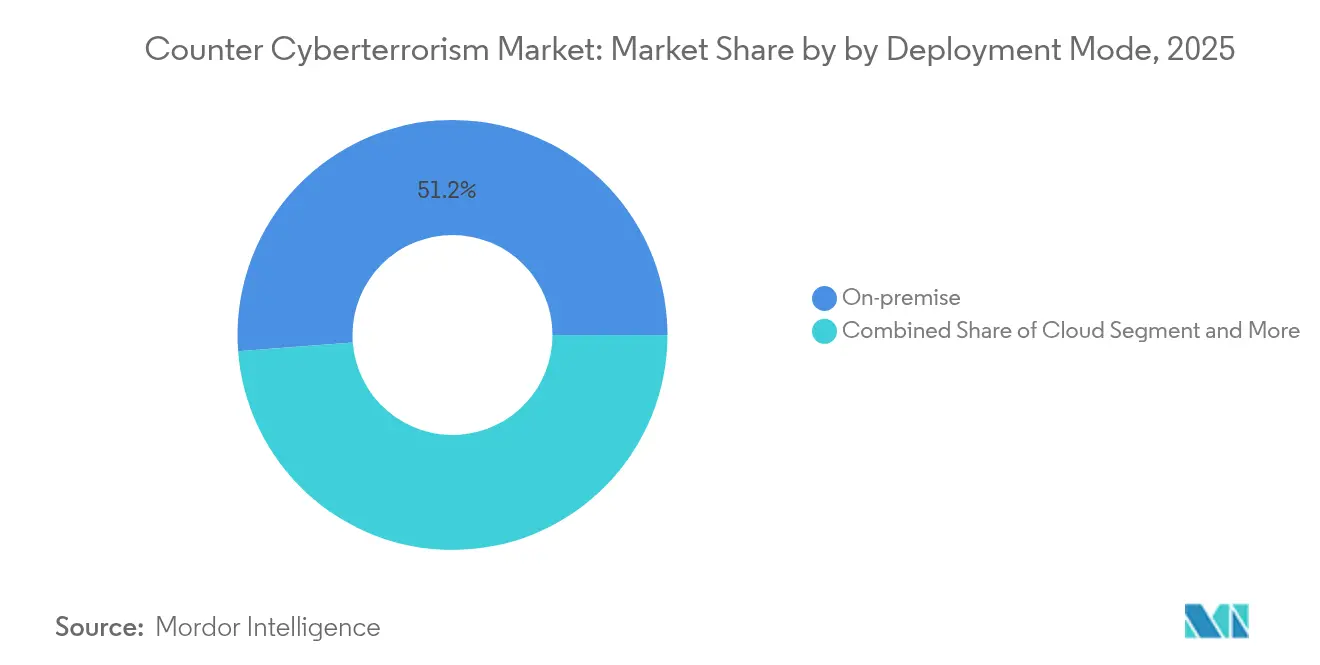

- By deployment mode, on-premise led with 51.20% of the counter cyberterrorism market share in 2025, whereas the cloud segment is projected to expand at a 13.20% CAGR through 2031.

- By security layer, network led with 29.55% of the counter cyberterrorism market share in 2025, whereas the data/cloud segment is projected to expand at an 17.80% CAGR through 2031.

- By geography, North America commanded 34.80% revenue share of the counter cyberterrorism market size in 2025, while Asia-Pacific is advancing at a 13.95% CAGR to 2031.

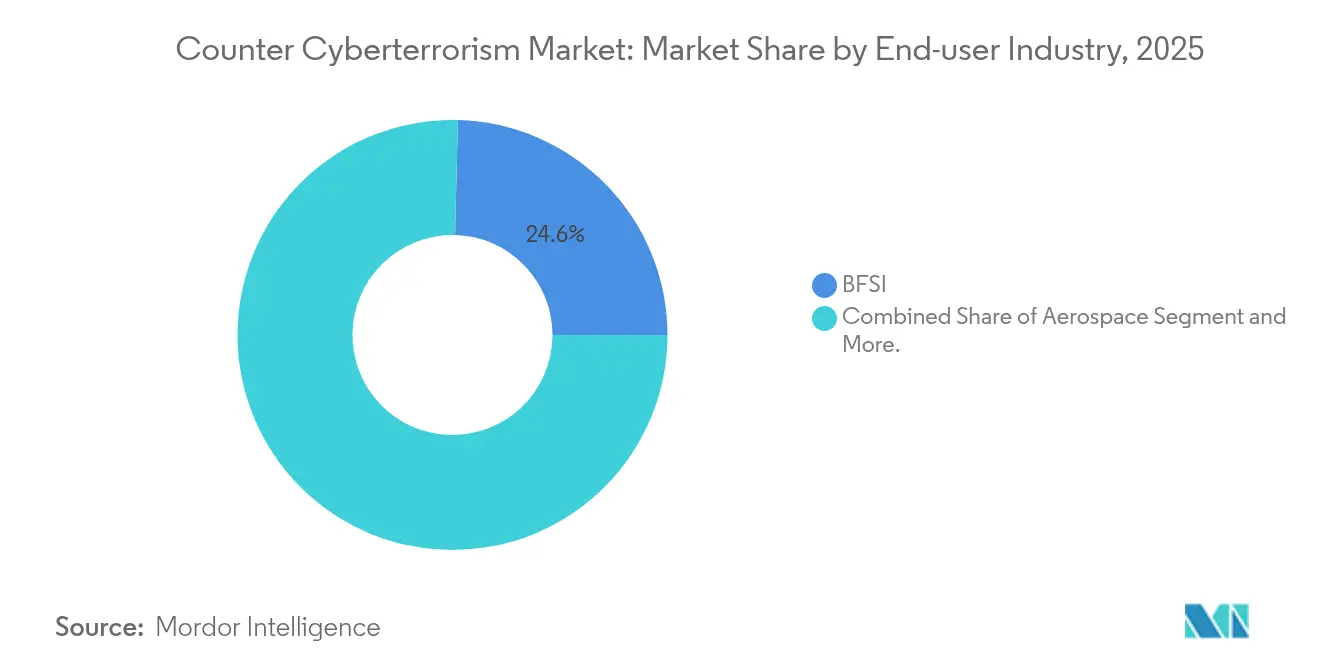

- By end-user, BFSI held 24.60% of the counter cyberterrorism market size in 2025; healthcare is accelerating at an 17.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Counter Cyberterrorism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing nation-state cyber offensives | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| AI-enabled threat detection adoption | +1.2% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Expansion of 5G/IIoT attack surface | +0.6% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Rise of Cybersecurity-as-a-Service (C-aa-S) | +0.9% | Global, with early adoption in North America | Medium term (2-4 years) |

| Escalating regulatory fines on data breaches | +0.7% | Europe and North America, expanding to APAC | Short term (≤ 2 years) |

| Real-time dark-web threat-intel exchanges | +0.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Nation-State Cyber Offensives Drive Defense Modernization

Persistent state-backed campaigns now target critical infrastructure and democratic processes with multi-vector tactics. The Pentagon earmarked USD 3.1 billion for zero-trust and next-generation encryption in its 2025 cyber budget, anchoring moves from incident response to active threat-hunting.[3]Colin Demarest, “Pentagon Seeks $14.5 Billion for Cyber Spending Including Zero Trust,” C4ISRNET, C4ISRNET.COMU.S. Cyber Command’s USD 1.7 billion appropriation further prioritizes counteroffensive readiness and multi-domain coordination.[4]U.S. Cyber Command, “FY 2025 Budget Justification,” DEFENSE.GOVSuch high-level focus incentivizes platform vendors to embed attribution, forensics, and automation features that satisfy national-security procurement criteria.

AI-Enabled Threat Detection Transforms Security Operations

Production-scale AI now shapes security operating centers as average breakout times shrink to 62 minutes. CrowdStrike-NVIDIA tests halve processing loads while doubling detection speeds, easing analyst fatigue. Adaptive models ingest endpoint, network, and cloud telemetry to predict adversary behavior, yet 40% of analyst hours still chase false positives. Vendors thus refine generative-AI enrichment and context-aware prioritization to boost signal-to-noise ratios and maximize limited human expertise.

Expansion of 5G/IIoT Attack Surface Creates New Vulnerabilities

Industrial 5G rollouts interconnect operational-technology assets once isolated from IT networks. Forty-five OT product families carry embedded flaws, exposing critical utilities to lateral-movement exploits. As quantum threats loom, NIST prioritizes post-quantum cryptography to safeguard 5G backbone encryption, accelerating market demand for data-layer protections and zero-trust segmentation even in legacy industrial environments.

Rise of Cybersecurity-as-a-Service Reshapes Market Dynamics

Managed security platforms democratize enterprise-grade defense for resource-constrained organizations. CrowdStrike’s USD 1 billion AWS Marketplace milestone highlights SaaS viability and price elasticity for scalable threat-hunting services. Providers leverage multi-tenant data lakes and AI correlation across clients, reducing per-tenant costs while elevating detection accuracy, a compelling value proposition amid the 4.8 million-person global skills gap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of tier-1 cyber warfare talent | -0.9% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Inter-agency data-sharing silos | -0.4% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Legacy OT systems with proprietary protocols | -0.6% | Global, concentrated in industrial regions | Long term (≥ 4 years) |

| High false-positive rates in ML models | -0.3% | Global, affecting early AI adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Tier-1 Cyber Warfare Talent Constrains Growth

The U.S. alone posts 663,000 unfilled roles, inflating wage premiums and throttling project rollouts. With advanced skills requiring 5-7 years of experiential learning, enterprises pivot to automation and MSSP partnerships to bridge gaps, reinforcing demand for C-aa-S offerings over in-house builds.

Classification barriers and incompatible formats undermine real-time collaboration despite programs like CISA’s USD 470 million Continuous Diagnostics and Mitigation initiative. Private firms often hold fresher threat data yet hesitate to exchange insights, stalling holistic situational awareness and dulling collective defense posture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Healthcare Accelerates Defensive Spend

Healthcare’s 17.20% CAGR through 2031 outpaces all sectors, even as BFSI retains the largest slice of the counter cyberterrorism market share in 2025. Daily incident losses reached USD 2 million, and 92% of providers reported targeted attacks, pushing hospitals to adopt zero-trust and managed detection despite budget constraints. Government grants worth USD 800 million help low-resourced facilities modernize defenses. BFSI maintains robust controls driven by regulatory audits and high-value data, while defense-aerospace budgets anchor classified-system requirements.

Rising ransomware premiums and patient-safety implications move boards to treat cybersecurity as enterprise risk, not IT overhead. Overlapping IoT medical devices and legacy electronic-health-record systems add complexity, reinforcing integration demand for AI-driven anomaly detection. Across sectors, the counter cyberterrorism market supports bespoke service tiers that map vertical regulations, demonstrating why industry-aligned MSSPs capture expanding wallet share.

By Solution Type: AI-Driven Innovation Outpaces Traditional Security

Network security tools hold 27.10% of the counter cyberterrorism market size; yet predictive AI solutions registering a 22.80% CAGR signal a strategic tilt from perimeter hardening to behavior analytics. Endpoint suites remain indispensable as remote work persists, and cloud security surges alongside multi-cloud adoption. Data-centric controls grow amid stricter privacy mandates, while identity platforms evolve continuous-auth models assessing both user intent and device posture.

Software-supply-chain attacks elevate application-security budgets, spurring demand for SBOM validation and DevSecOps automation. Vendors fuse threat-intel feeds with zero-trust orchestration, creating unified consoles that slash tool sprawl an attractive proposition as procurement favors platform breadth over point-solution depth.

By Deployment Mode: Cloud Gains Even as On-Premise Dominates

On-premise installations still account for 51.20% of the counter cyberterrorism market size due to sovereignty mandates and cultural trust in owned infrastructure. Yet cloud deployments are climbing at 13.20% CAGR, buoyed by the scalability of SaaS threat-intel engines. Hybrid models serve risk-averse enterprises that keep crown-jewel assets local while leveraging cloud analytics for less sensitive workloads.

Integration alliances such as CrowdStrike with Google Cloud secure workloads across multicloud estates, addressing a 75% spike in cloud intrusions. Regulatory frameworks increasingly codify encryption and logging standards rather than dictating location, easing adoption barriers and pushing procurement toward OPEX-friendly subscriptions.

By Security Layer: Data Protection Becomes Core Objective

Network-layer controls deliver 29.55% revenue but data-layer security is the fastest climber at 17.80% CAGR, reflecting acceptance that attackers often pierce perimeters. NIST’s quantum-resistant guidelines spur cryptography refresh cycles, and boards earmark funding for classification, tokenization, and immutable backups. Endpoint-layer investments persist as device sprawl and remote work expand attack surfaces, while application-layer defenses gain priority to blunt software-supply-chain exploits.

Organizations converge around data-centric frameworks that monitor assets regardless of hosting environment, reinforcing demand for encryption-key orchestration and real-time data-loss-prevention engines. Vendors differentiate via ease of integration and policy automation, advancing competitive friction from signature depth to orchestration breadth.

Geography Analysis

North America anchors 34.80% of the counter cyberterrorism market size, driven by the U.S. federal USD 27.5 billion cybersecurity allocation and USD 30 billion annual military cyber outlays. Canada cooperates through the U.S.–Canada Cyber Action Plan, and Mexico accelerates critical-infrastructure safeguards under trilateral frameworks. Mature compliance regimes such as CMMC and GLBA push enterprises toward continuous threat monitoring, sustaining platform renewals across sectors.

Asia-Pacific records the fastest 13.95% CAGR as governments respond to a 16% jump in weekly attacks and 50% growth in cyber-insurance uptake. China’s Data Security Law and India’s CERT-IN mandates expand mandatory reporting, while Japan funds USD 6 billion for industrial cyber-fortification. Australia’s 2025–2030 Cyber Strategy emphasizes sovereign capability development, amplifying MSSP demand across mid-market enterprises.

Europe holds a steady share under GDPR-driven accountability measures that levied EUR 1.2 billion in 2024 fines. The EU’s coordinated post-quantum roadmap catalyzes member-state grants for cryptographic retrofits, benefiting platform vendors offering hybrid encryption. The U.K.’s National Cyber Force merges offense-defense mandates, France accelerates SecNumCloud certifications, and Germany’s KRITIS-Dachgesetz expands critical-infrastructure scope, stimulating integrated-security procurement.

Competitive Landscape

Moderate consolidation defines the counter cyberterrorism market as leading suites integrate endpoint, network, and identity functions. CrowdStrike, Palo Alto Networks, Microsoft, and Cisco leverage scale, data-lake breadth, and AI pipelines to sustain double-digit product growth. Platform stickiness deepens as customers prioritize unified telemetry and automated response to combat analyst scarcity.

Acquisition momentum remained high with 362 deals in 2024; for example, Palo Alto’s buyout of cloud-security specialist Cider Security and Cisco’s takeover of Splunk closed Q1 2025, illustrating moves to fuse SIEM, SOAR, and XDR into cohesive fabrics. Partnerships eclipse one-off integrations: Zscaler–CrowdStrike Zero-Trust tie-ups enable shared risk scoring and policy orchestration, while Fortinet alliance plugs endpoint insight into next-gen firewalls for lateral-movement containment.

White-space remains in quantum-safe cryptography, where adoption sits near 0.03% despite NIST draft standards. Niche vendors exploit this gap with lattice-based key exchange plug-ins, while generative-AI innovators craft context-aware phishing-detection models. Competitive differentiation thus hinges on AI-model fidelity, integration openness, and time-to-value rather than feature checklists.

Counter Cyberterrorism Industry Leaders

Palo Alto Networks

Cisco Systems, Inc.

Microsoft Corporation

Fortinet, Inc.

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CrowdStrike collaborates with NVIDIA to double detection speed while cutting compute by 50%, easing SOC analyst overload.

- February 2025: CrowdStrike and Google Cloud broaden Mandiant MDR using Falcon to address 75% growth in cloud intrusions.

- December 2024: CrowdStrike adds AI container scanning for Amazon SageMaker workloads, extending shift-left protections.

- October 2024: CrowdStrike–Fortinet integrate endpoint and firewall intel for unified lateral-movement containment.

Global Counter Cyberterrorism Market Report Scope

Cyberterrorism refers to unlawful threats and attacks against networks, computers, and the information stored on them to force or frighten a government or its people to pursue political or social goals. Counter-cyberterrorism is a counterattack regarded as the most effective way of moving the attacker to forsake his plans. Cyber counterattacks are occasionally used as self-defense to restrict or even stop cyberattacks.

The counter-cyberterrorism market is segmented by end-user industry (defense, aerospace, BFSI, corporate, power and utilities, government, and other end-user industries) and by geography ( North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Defense |

| Aerospace |

| BFSI |

| Corporate/Enterprise |

| Power and Utilities |

| Government and Intelligence Agencies |

| Healthcare |

| Network Security Solutions |

| Endpoint Security Solutions |

| Cloud Security Solutions |

| Application Security |

| Data and Database Security |

| Identity and Access Management |

| Threat Intelligence and MSSP |

| On-premise |

| Cloud |

| Hybrid |

| Managed / Hosted |

| Network Layer |

| Endpoint Layer |

| Application Layer |

| Data / Cloud Layer |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By End-user Industry | Defense | ||

| Aerospace | |||

| BFSI | |||

| Corporate/Enterprise | |||

| Power and Utilities | |||

| Government and Intelligence Agencies | |||

| Healthcare | |||

| By Solution Type | Network Security Solutions | ||

| Endpoint Security Solutions | |||

| Cloud Security Solutions | |||

| Application Security | |||

| Data and Database Security | |||

| Identity and Access Management | |||

| Threat Intelligence and MSSP | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| Hybrid | |||

| Managed / Hosted | |||

| By Security Layer | Network Layer | ||

| Endpoint Layer | |||

| Application Layer | |||

| Data / Cloud Layer | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the counter-cyberterrorism market?

The counter cyberterrorism market size is USD 34.96 billion in 2026.

How fast is the sector expected to grow over the next five years?

It is forecast to expand at a 3.22% CAGR, reaching USD 40.94 billion by 2031.

Which geographic region is expanding the quickest?

Asia-Pacific leads with a projected 13.95% CAGR through 2031.

Which solution type is seeing the highest growth rate?

AI-driven security solutions are advancing at a 22.80% CAGR through 2031.

Page last updated on: