Tennis Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.67 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tennis Market Analysis by Mordor Intelligence

The global tennis market was valued at USD 4.48 billion in 2025 and is projected to reach USD 4.67 billion in 2026, with an anticipated growth to USD 6.01 billion by 2031, registering a CAGR of 5.16% during the forecast period. Market growth is primarily driven by the rising adoption of tennis as a fitness-oriented and recreational activity, which sustains demand for tennis products and services. Increased interest in active lifestyles, structured training programs, and participation in competitive sports is contributing to the frequent use and replacement of tennis-related products. Furthermore, the influence of professional tournaments, heightened athlete visibility, and the growing prominence of sports culture are boosting consumer interest and expanding the global reach of tennis. Advancements in product design, enhanced comfort, improved durability, and performance-oriented offerings are also fostering greater consumer adoption and encouraging product upgrades.

Key Report Takeaways

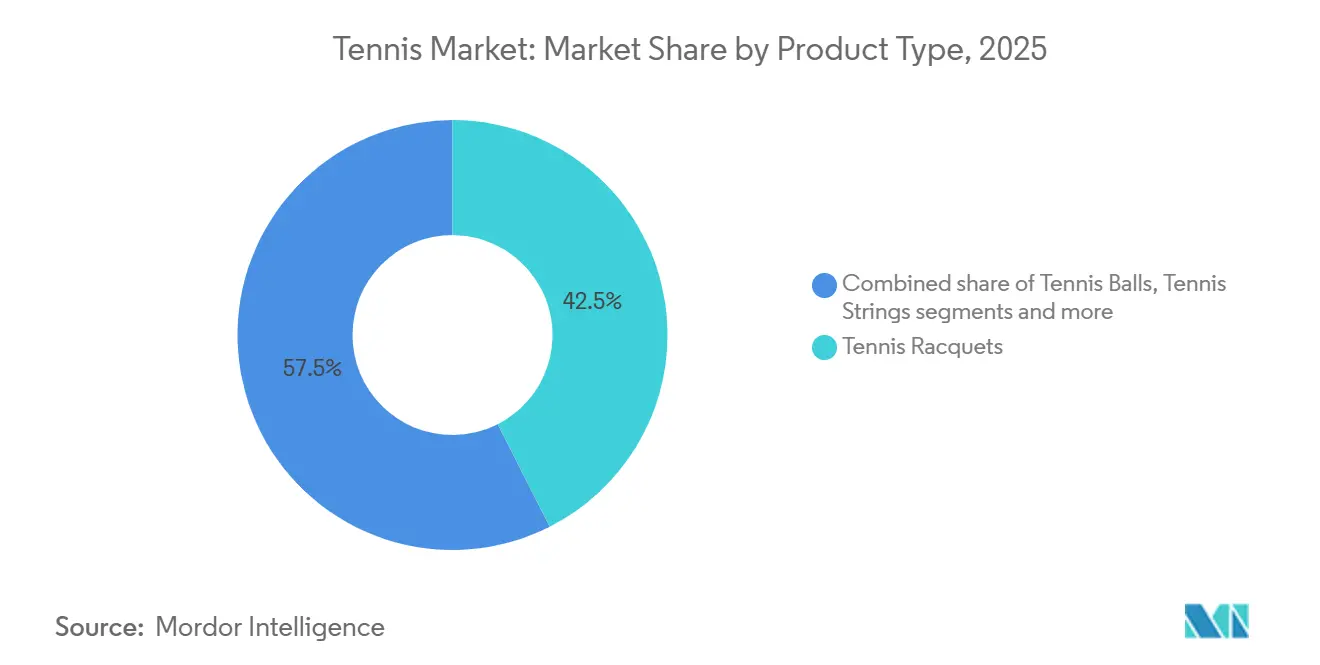

- By product type, Tennis Racquets accounted for 42.52% share of the tennis market size in 2025, while Tennis Apparel is forecast to expand at 6.24% CAGR through 2031.

- By court surface, Hard Court held 58.91% of the tennis market share in 2025, while Clay Court is projected to grow at 5.72% CAGR through 2031.

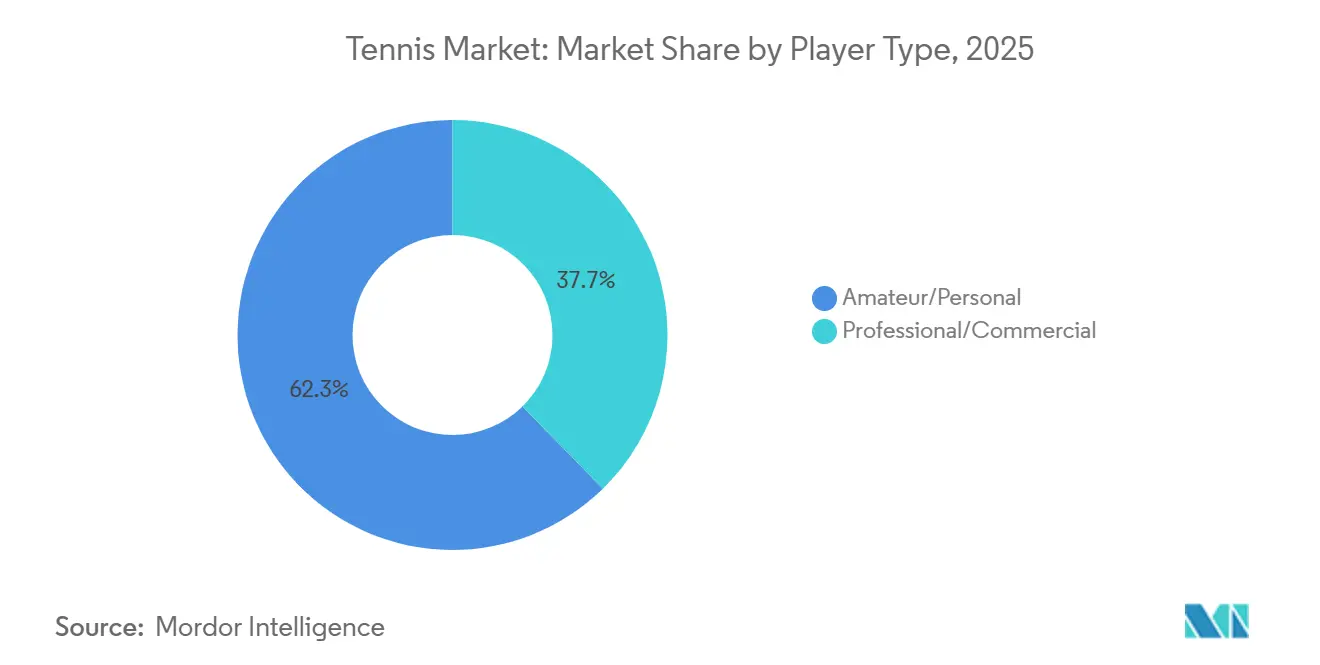

- By player type, Amateur/Personal players captured 62.33% of 2025 revenue, while Professional/Commercial players are expected to advance at 6.78% CAGR through 2031.

- By end-user, Men represented 53.24% of 2025 value, while Women are projected to grow at 6.91% CAGR through 2031.

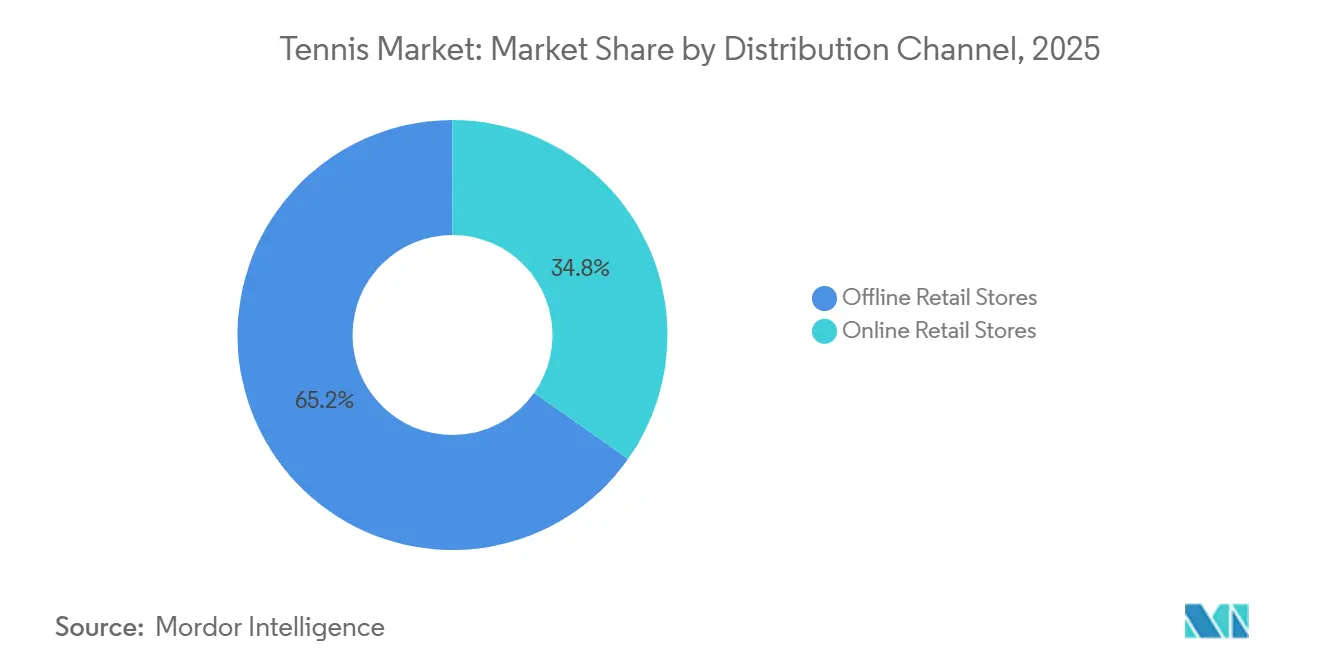

- By distribution channel, Offline Retail Stores held 65.21% of 2025 sales, while Online Retail Stores are set to expand at 7.09% CAGR through 2031.

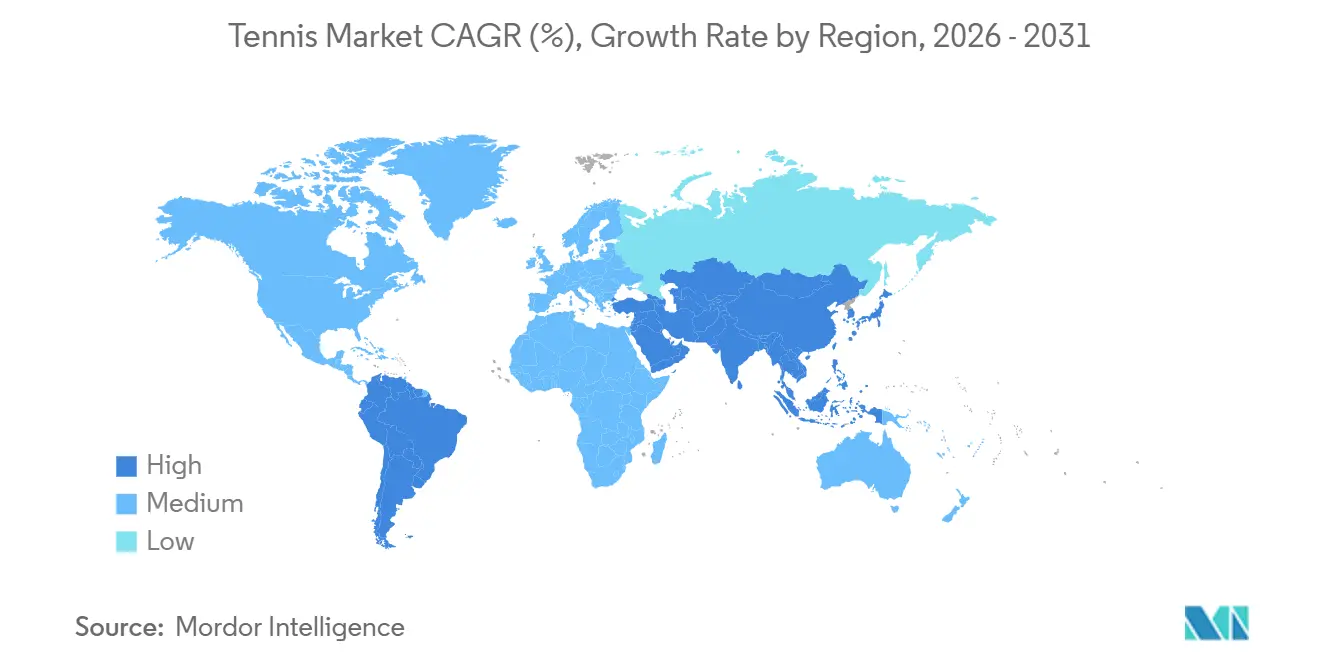

- By geography, North America held 34.19% of global value in 2025, while Asia-Pacific is projected to record the fastest growth at 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tennis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in tennis for fitness and recreation | +1.2% | Global, with concentrated uplift in North America and Asia-Pacific | Medium term (2-4 years) |

| Growth of tennis training academies and coaching programs | +0.6% | Global; early-stage gains in India, Brazil, Malaysia, and Southeast Asia | Long term (≥ 4 years) |

| Growing government and sports association initiatives | +0.5% | North America, Europe, and selected Asia-Pacific markets including India and Australia | Medium term (2-4 years) |

| Impact of tennis celebrities and athlete endorsements | +0.9% | Global, strongest in North America, Western Europe, and East Asia | Short term (≤ 2 years) |

| Technological advancements in tennis equipment | +1.1% | Global, led by mature markets with high premium-equipment adoption | Long term (≥ 4 years) |

| Growing focus on health, wellness, and active lifestyles | +0.5% | Global, particularly North America, Europe, and urban Asia-Pacific centres | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising participation in tennis for fitness and recreation

The increasing participation in tennis for fitness and recreation is driving consistent demand for tennis equipment, apparel, and accessories among regular players. The popularity of tennis as a recreational activity is boosting the purchase of essential products such as racquets, balls, strings, footwear, and clothing, while frequent play generates recurring replacement demand. According to Sport England, tennis participation in England reached approximately 1.04 million participants during 2024–25, indicating sustained interest in the sport [1]Source: Sport England, "Number of tennis participants in England", sportengland.org. This growing player base is enhancing product consumption across both casual and organized playing settings, as consumers seek appropriate tennis products for practice, fitness routines, and recreational matches, thereby contributing to the overall growth of the tennis market.

Growth of tennis training academies and coaching programs

The growth of tennis training academies and structured coaching programs is contributing to the development of a robust ecosystem for skill enhancement, competitive preparation, and sustained player engagement. The expansion of professional coaching facilities has increased the demand for tennis-specific products, as players participating in regular training require reliable access to racquets, balls, strings, footwear, apparel, and accessories designed for frequent practice. Structured programs emphasizing player development, match preparation, and physical conditioning are also driving higher equipment usage and replacement rates, thereby supporting overall market demand. For example, in April 2026, Sania Mirza launched the High Performance Tennis Programme at her academy in Hyderabad, India, in partnership with Marco Seruca. This initiative aims to develop competitive players through structured coaching, fitness training, match strategy, and mental conditioning.

Growing government and sports association initiatives

Government and sports association initiatives are contributing to the growth of the global tennis market by enhancing player development pathways, improving access to organized training programs, and promoting greater participation in competitive tennis. These efforts establish a structured ecosystem by supporting talent identification, coaching programs, athlete development, and tournament exposure. This, in turn, drives the demand for tennis equipment, apparel, and accessories necessary for regular training and competition. Additionally, government-backed programs and collaborations with sports organizations help broaden the reach of tennis by providing players with improved resources and development opportunities. For example, in January 2024, the Government of Maharashtra Department of Sports and MahaTennis Foundation, in collaboration with the Maharashtra State Lawn Tennis Association (MSLTA), launched the “Lakshyavedh” tennis program aimed at supporting tennis players in Maharashtra.

Impact of tennis celebrities and athlete endorsements

The global tennis market is influenced by tennis celebrities and athlete endorsements, which enhance product visibility, strengthen brand recognition, and shape consumer purchasing decisions. Professional players significantly contribute to promoting tennis products, as fans and aspiring players often associate the equipment and apparel used by athletes, such as racquets, footwear, and accessories, with performance and reliability. Endorsement deals, signature product lines, and athlete-inspired designs enable brands to establish stronger emotional connections with consumers, fostering product adoption and repeat purchases. Additionally, high-profile tennis personalities raise awareness of new product offerings through tournaments, media coverage, and digital platforms, broadening the appeal of tennis-related products beyond professional players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of tennis equipment and accessories | -0.7% | Emerging markets in Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Competition from other popular sports | -0.6% | Europe (padel), Latin America (padel/football), Asia-Pacific (badminton) | Short term (≤ 2 years) |

| Seasonal and weather-related limitations | -0.4% | Northern Europe, Canada, and United States | Short term (≤ 2 years) |

| Risk of sports injuries among players | -0.3% | Global, with higher sensitivity among older recreational demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of tennis equipment and accessories

The high cost of tennis equipment and accessories is hindering the growth of the global tennis market by reducing affordability and creating obstacles for new and casual players. Tennis involves the use of various essential products, including racquets, balls, strings, footwear, apparel, bags, and other accessories, which collectively increase the overall cost of participation. Furthermore, recurring expenses such as replacing worn-out balls, restringing racquets, and upgrading equipment contribute to the long-term ownership costs for players. Premium tennis products, which offer greater durability, comfort, and performance, are often priced higher, making them less accessible to price-sensitive consumers. These costs can deter beginners from taking up the sport and decrease purchase frequency among recreational players, thereby limiting broader adoption and constraining market growth potential.

Competition from other popular sports

Competition from other popular sports is limiting the growth of the global tennis market by making it more challenging to attract and retain players in a diverse sports landscape. The availability of alternative sports activities provides consumers with a wider range of options, potentially diverting interest away from tennis and affecting consistent engagement with the sport. Many competing sports are more accessible, require less equipment, involve shorter learning curves, or offer team-based experiences, making them more attractive to beginners and casual participants. Furthermore, increased media coverage, the establishment of professional leagues, and the growth of recreational communities around these sports can influence consumer preferences and decrease the frequency of tennis participation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Racquets Anchor Revenue, Apparel Closes the Gap

The tennis racquets segment accounted for 42.52% of the global tennis market in 2025, contributing significantly to market growth. This is attributed to the rising demand for high-performance, durable, and technologically advanced equipment that enhances the overall playing experience. Increasing participation in tennis for fitness, recreation, and competitive purposes is sustaining consistent demand for racquets, which are essential for the sport. Ongoing product innovations, such as lighter frames, improved weight distribution, enhanced power generation, better control, and advanced shock absorption features, are prompting players to replace and upgrade their racquets more frequently. Additionally, the growing preference for personalized equipment tailored to playing style, comfort, grip, and performance needs is further driving adoption.

The tennis apparel segment is projected to achieve the highest growth, with a CAGR of 6.24% from 2026 to 2031. This growth is driven by the segment's higher replacement frequency and broader purchasing patterns compared to other tennis products. Recurring demand arises as players require multiple apparel items for practice sessions, tournaments, seasonal needs, and personal preferences. The increasing demand for tennis-specific clothing, including shirts, shorts, skirts, dresses, jackets, and other performance wear, is boosting product sales across various consumer categories. Furthermore, the rising influence of tennis fashion and the integration of tennis apparel into lifestyle and casual wear have expanded its usage occasions, creating additional growth opportunities.

By Court Surface: Hard Courts Command Volume, Clay Courts Accelerate

Hard courts accounted for 58.91% of the global tennis market in 2025, driven by their widespread adoption as a preferred playing surface due to durability, consistent playing conditions, and compatibility with various playing styles. This surface supports faster gameplay compared to alternatives while maintaining predictable ball movement, making it suitable for both training and competitive matches. Its strong presence in tennis facilities is further supported by lower maintenance requirements and a longer surface lifespan, encouraging continued usage and investment. Additionally, the demanding nature of hard courts increases the need for surface-specific products, such as durable footwear, balls, and accessories designed to withstand higher impact and frequent play.

Clay courts are the fastest-growing surface segment, with a CAGR of 5.72% from 2026 to 2031, driven by increasing preference for their unique playing characteristics and training benefits. Clay courts create slower ball speeds and longer rallies, promoting greater focus on endurance, strategy, and skill development, which supports their adoption among players aiming to enhance gameplay techniques. The surface is also valued for providing a softer playing experience with reduced impact stress compared to harder surfaces, making it appealing for longer practice sessions and frequent play. Furthermore, the specialized maintenance requirements and surface characteristics of clay courts drive demand for dedicated tennis products, including footwear, balls, and accessories optimized for clay surfaces.

By Player Type: Amateurs Drive Volume, Professionals Drive Value Intensity

Amateur or personal players accounted for 62.33% of the market value in 2025, driven by steady demand from individuals purchasing tennis products for recreational play, personal fitness, skill development, and leisure activities. This segment generates higher product consumption due to its broad consumer base, which requires essential tennis products such as racquets, balls, apparel, and accessories for regular personal use. Unlike organized professional settings, amateur players often make independent purchasing decisions based on comfort, preferences, and playing needs, resulting in diverse demand across multiple product categories. Additionally, repeat purchases from casual and club-level players, particularly for frequently replaced items and upgraded equipment as skills improve, further support this segment.

The professional or commercial player segment is the fastest-growing, with a CAGR of 6.78% projected through 2031. This growth is driven by the expansion of organized competitive tennis, professional training ecosystems, and commercial tennis activities. The increasing number of structured tournaments, coaching programs, academies, and professional development pathways is fueling demand for high-quality tennis products designed for intensive and frequent use. According to the International Tennis Federation (ITF), in 2025, a total of 11,595 players participated in 1,261 tournaments, up from 10,979 players and 1,200 events in 2024 [2]Source: International Tennis Federation (ITF), "11,500 players, 1261 events: The 2025 ITF World Tennis Tour in numbers", itftennis.com. This growth in competitive opportunities and professional-level engagement is driving higher consumption of performance-oriented racquets, apparel, and other tennis products, as professional environments require regular equipment replacement and adherence to consistent product standards.

By End-User: Men Hold Share, Women Drive the Next Growth Phase

Men accounted for 53.24% of the market value in 2025, driven by strong demand for products across competitive, recreational, and training-based tennis activities. This segment benefits from higher consumption of tennis equipment and apparel, supported by frequent product replacement needs and a wide range of products tailored to varying playing requirements. Men's tennis products, including racquets, footwear, clothing, strings, and accessories, continue to experience robust demand due to established purchasing patterns and a preference for performance-oriented products. The availability of diverse product ranges designed for different playing intensities and preferences further bolsters demand, positioning men as the leading end-user category contributing to the overall tennis market.

Women represent the fastest-growing end-user segment, with a CAGR of 6.91% projected through 2031. This growth is driven by increasing demand for tennis products designed to meet women-specific preferences, comfort, and playing requirements. The segment is experiencing strong expansion due to the growing availability of women-focused tennis collections, including apparel, footwear, and accessories tailored for various performance needs and style preferences. Rising demand for tennis apparel that combines on-court functionality with lifestyle usage is driving higher purchase frequency, particularly in clothing and footwear categories. Additionally, the increasing visibility of women’s tennis, greater commercial focus on female athletes, and enhanced representation across competitive platforms are strengthening consumer interest and boosting product adoption.

By Distribution Channel: Offline Leads on Volume, Online Accelerates on Value

Offline retail stores accounted for 65.21% of the global tennis market value in 2025, driven by consumer preference for evaluating products physically and experiencing personalized purchasing processes, particularly for performance-oriented tennis products. Purchases of tennis equipment often rely on factors such as racquet weight, grip size, balance, footwear comfort, and apparel fit, prompting customers to visit physical stores before making decisions. Offline channels also offer expert guidance, product demonstrations, customization services, and immediate product availability, which enhance customer confidence during the purchasing process. Furthermore, specialty sports outlets and retail stores provide a broad assortment of tennis products, enabling consumers to compare options based on their playing requirements and preferences.

Online retail stores represent the fastest-growing distribution channel, with a CAGR of 7.09% projected through 2031. This growth is fueled by the increasing consumer shift toward convenient and flexible purchasing options for tennis products. Digital platforms provide access to a wider range of racquets, apparel, footwear, balls, and accessories, along with detailed product information, customer reviews, and easy product comparisons. The availability of exclusive online collections, direct-to-consumer sales models, customization options, and attractive promotional strategies is encouraging more consumers to shop for tennis products online. Additionally, improved return policies, size guides, and product recommendation features are enhancing buyer confidence, supporting the rapid expansion of online retail stores.

Geography Analysis

North America accounted for 34.19% of the global tennis market value in 2025, driven by its well-established tennis ecosystem, strong demand for premium tennis equipment, and widespread availability of organized playing facilities. The region benefits from a mature base of recreational and competitive players, which supports consistent purchases of racquets, balls, apparel, footwear, and accessories. Additionally, strong retail networks, professional coaching structures, and continuous demand for replacement and upgraded tennis products further reinforce North America's leading position in the global tennis market.

Asia-Pacific is the fastest-growing region, with a CAGR of 6.57% projected through 2031. This growth is supported by increasing utilization of tennis facilities, rising interest in organized sports activities, and growing adoption of tennis products in emerging markets. For example, according to the Singapore Department of Statistics, tennis court bookings in Singapore reached approximately 215,140 in 2024, up from around 205,700 in 2023, indicating growing engagement with the sport [3]Source: Singapore Department of Statistics, "Number of tennis court bookings in Singapore", singstat.gov.sg. The rising frequency of tennis activities is driving demand for equipment replacement, sportswear, accessories, and training-related products, positioning Asia-Pacific as the fastest-expanding regional market.

Europe continues to gain momentum in the tennis market, supported by its strong tennis culture, established club systems, and demand for specialized tennis products tailored to different playing surfaces. South America, particularly Brazil and Argentina, represents an emerging demand center for the tennis market. This growth is driven by expanding tennis communities, increasing interest in competitive play, and the growing availability of tennis infrastructure, which supports the region's market development. The Middle East and Africa remain in the early stages of tennis market development. Growth in these regions is supported by the expansion of sports facilities, the introduction of tennis programs, and the gradual adoption of tennis as both a recreational and competitive activity. These factors create future opportunities for market expansion in the region.

Competitive Landscape

The global tennis market is moderately consolidated, with leading companies competing through product innovation, brand positioning, athlete partnerships, and the expansion of tennis-specific product portfolios. Key players in the market include Amer Sports, Inc. (Wilson), Yonex Co., Ltd., Head Sport GmbH, MF Brands Group (Tecnifibre), Nike, Inc., and Babolat, among others. These companies focus on strengthening their presence across categories such as racquets, balls, strings, footwear, apparel, and accessories by introducing products aimed at enhancing player experience, comfort, and performance.

Technology adoption has emerged as a significant competitive strategy, with manufacturers incorporating advanced materials, smart design features, and performance-enhancing solutions into tennis equipment. For example, Babolat’s Evo range of tennis racquets integrates advanced technologies, including an aerodynamic frame structure and Spin Alpha technology, to facilitate easier spin generation and increased power with reduced effort. Similarly, companies are emphasizing lightweight materials, improved frame engineering, vibration control systems, and customized equipment solutions to differentiate their offerings and meet evolving player needs.

Additionally, the market is experiencing growing adoption of AI-enabled performance analytics and digital tennis solutions, which allow players to track performance, analyze techniques, and enhance training outcomes. Companies are utilizing connected devices, smart sensors, and data-driven platforms to improve customer engagement beyond traditional equipment sales. The combination of advanced product development, digital integration, and performance-focused innovation is intensifying competition among established brands while driving long-term growth in the global tennis market.

Tennis Industry Leaders

-

Amer Sports, Inc. (Wilson)

-

Head Sport GmbH

-

Yonex Co., Ltd.

-

MF-Brands group (Tecnifibre)

-

Nike, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adidas introduced CLIMACOOL+ performance fabric for tennis, designed with 3D raised structures to enhance airflow and keep athletes cool and dry. This innovation was developed through athlete insights, physiological testing, and sport-specific performance analysis.

- April 2026: Yonex introduced the new Muse tennis racket series, designed specifically for recreational players and aimed at encouraging individuals to return to the sport. This marks a departure for the brand, which is traditionally recognized for producing high-performance, tour-level frames.

- April 2026: Wilson Sporting Goods launched their newest performance racket, the Blade v10. Designed for optimal control and responsive impact, the Blade v10 ensures consistent performance for aggressive gameplay.

Global Tennis Market Report Scope

The tennis market encompasses the industry focused on the production, promotion, and sale of tennis-related products. The tennis market is segmented by product type, court surface, player type, end-user, distribution channel, and geography. Based on product type, the market is segmented into tennis racquets, tennis balls, tennis strings, tennis apparel, and others. Based on court surface, the market is segmented into hard court, clay court, grass court, and carpet courts. Based on player type, the market is segmented into professional/commercial and amateur/personal. Based on end-user, the market is segmented into men, women, and kids/children. Based on distribution channel, the market is segmented into online retail stores and offline retail stores. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Tennis Racquets |

| Tennis Balls |

| Tennis Strings |

| Tennis Apparel |

| Others |

| Hard Court |

| Clay Court |

| Grass Court |

| Carpet Courts |

| Professional/Commercial |

| Amateur/Personal |

| Men |

| Women |

| Kids/Children |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tennis Racquets | |

| Tennis Balls | ||

| Tennis Strings | ||

| Tennis Apparel | ||

| Others | ||

| By Court Surface | Hard Court | |

| Clay Court | ||

| Grass Court | ||

| Carpet Courts | ||

| By Player Type | Professional/Commercial | |

| Amateur/Personal | ||

| By End-User | Men | |

| Women | ||

| Kids/Children | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the tennis market?

The tennis market was valued at USD 4.48 billion in 2025 and stands at USD 4.67 billion in 2026, with growth expected to continue through 2031.

How fast is tennis expected to grow through 2031?

The tennis market is forecast to reach USD 6.01 billion by 2031, growing at a 5.2% CAGR from 2026 to 2031.

Which product category leads tennis sales today?

Tennis Racquets led with 42.52% of 2025 revenue, reflecting the segment’s central role in player spending and premium product innovation.

Which sales channel is growing the fastest for tennis products?

Online Retail Stores are projected to expand at 7.09% CAGR through 2031, even though Offline Retail Stores still held 65.21% of 2025 sales.

Page last updated on: