Tennis Racquet Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

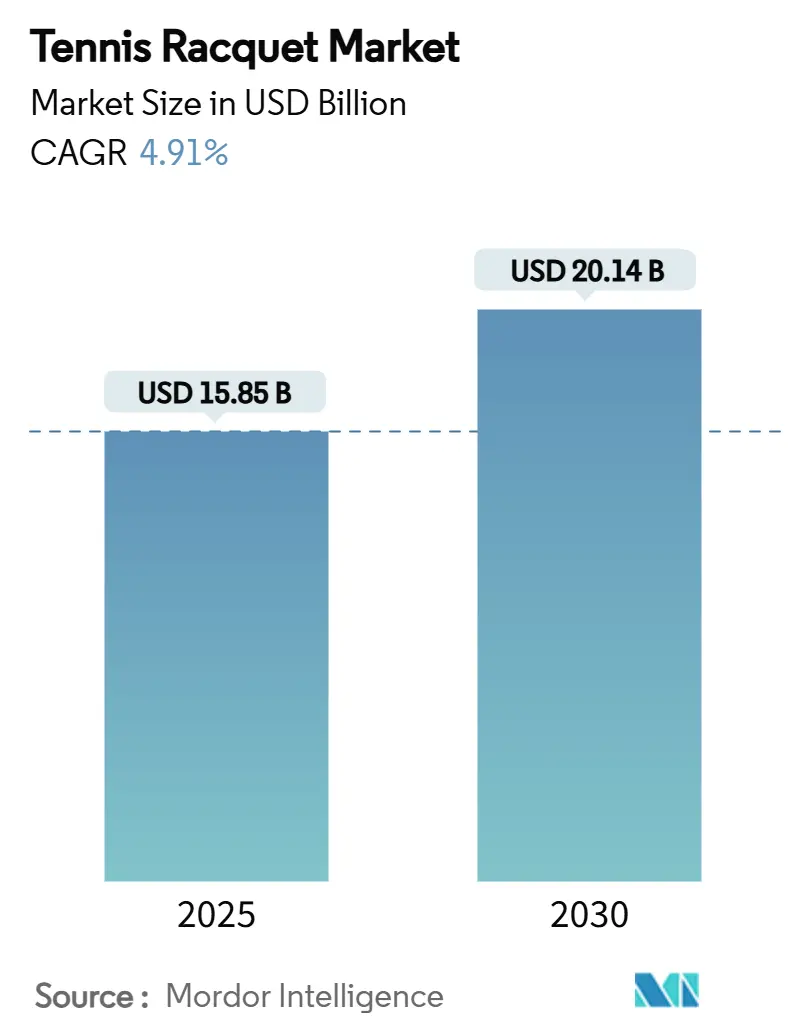

| Market Size (2025) | USD 15.85 Billion |

| Market Size (2030) | USD 20.14 Billion |

| Growth Rate (2025 - 2030) | 4.91% CAGR |

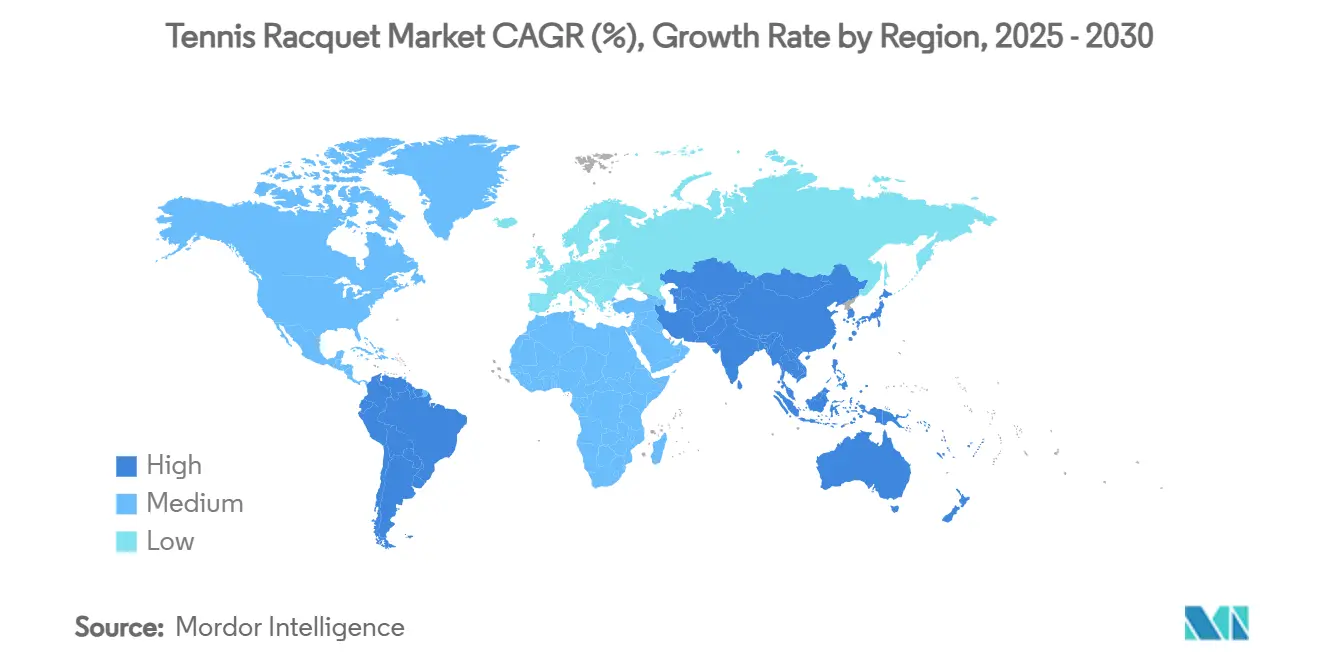

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tennis Racquet Market Analysis by Mordor Intelligence

The tennis racquet market size is estimated to be USD 15.85 billion in 2025 and is projected to reach USD 20.14 billion by 2030, growing at a 4.91% CAGR. This steady rise reflects how technological advances in carbon-fiber engineering, sustained participation growth, and expanding youth programs combine to strengthen demand across ability levels. The popularity of “cardio-tennis” classes, smart-court installations, and climate-resilient facilities widens the customer base beyond traditional club players and feeds consistent replacement cycles. At the same time, premium price tolerance grows as recreational users gravitate toward lightweight, arm-friendly frames that mimic professional equipment. Besides, online channels compress discovery time and expose global shoppers to limited-edition launches, while omnichannel retailers refine virtual fitting tools to replicate the in-store demo experience. Collectively, these shifts lock in a durable growth runway for the tennis racquet market.

Key Report Takeaways

- By head type, midsize/mid-plus frames commanded 62.15% of the tennis racquet market share in 2024, whereas oversize/super-oversize heads are projected to expand at a 5.27% CAGR through 2030.

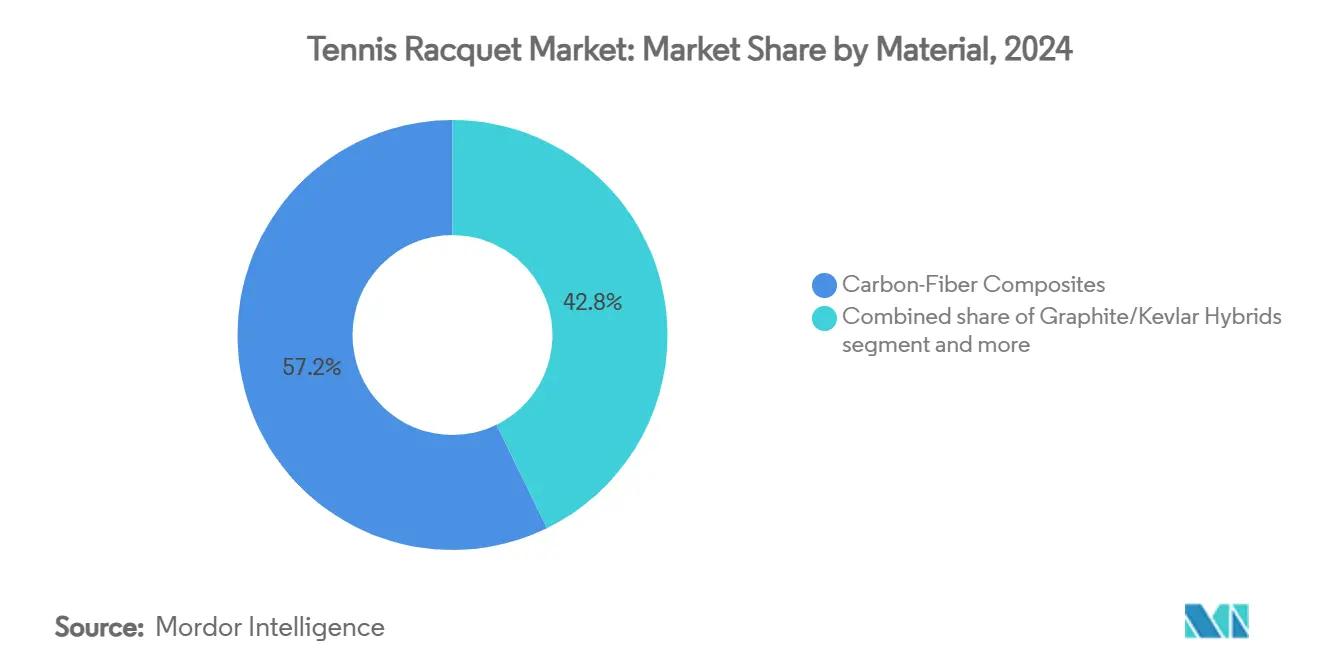

- By material, carbon-fiber composites accounted for 57.24% of the tennis racquet market size in 2024, while graphite/kevlar hybrids show the fastest 5.79% CAGR to 2030.

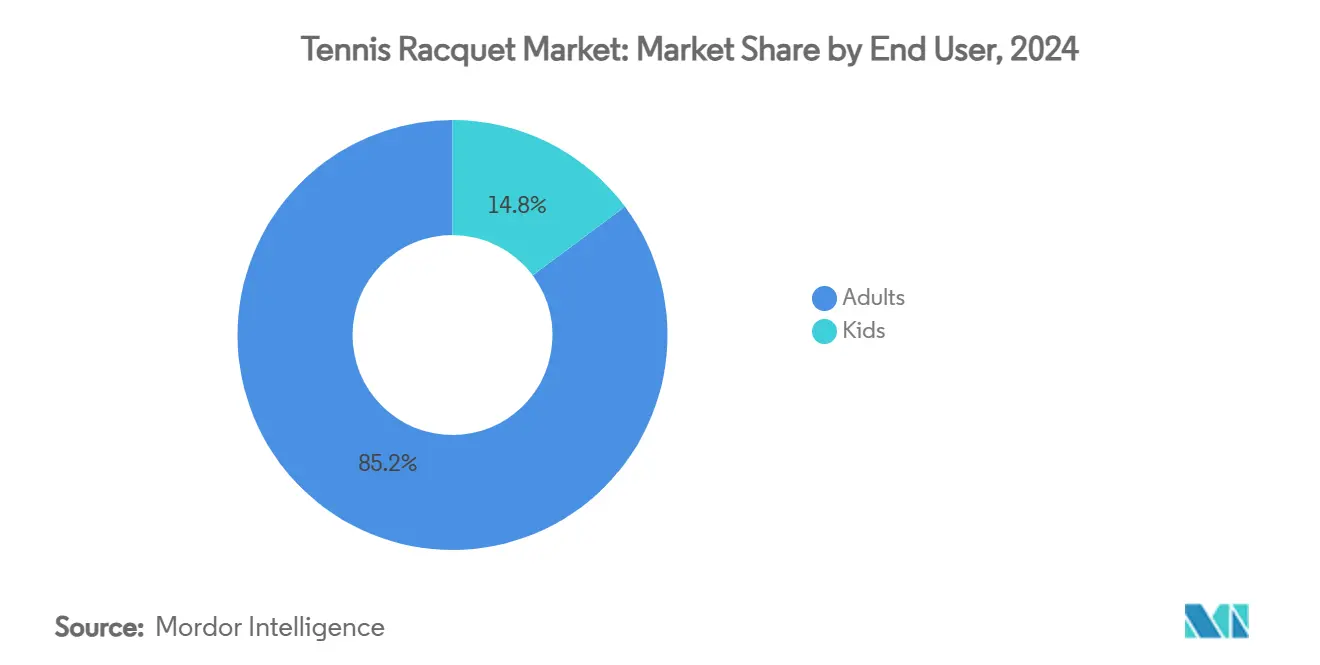

- By end user, adults captured 85.19% of revenue in 2024; the kids segment is advancing at a 6.73% CAGR through 2030.

- By distribution channel, offline retail retained 55.38% share of the tennis racquet market size in 2024, as online platforms record a 5.90% CAGR to 2030.

- By geography, North America led with 35.62% revenue share in 2024, and Asia-Pacific is forecast to post a 6.02% CAGR through 2030.

Global Tennis Racquet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in health and fitness awareness | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rising youth engagement and school programs | +0.8% | Global, with early gains in Asia-Pacific and North America | Long term (≥ 4 years) |

| Development of weather-resilient tennis facilities | +0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of organized cardio-tennis programs | +0.4% | Europe and North America, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Rising sponsorship and endorsement spend by brands | +0.5% | Global, concentrated in major markets | Short term (≤ 2 years) |

| Growth of sustainable, bio-based racquet materials | +0.3% | Europe and North America, early adoption phase | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Health and Fitness Awareness

The increasing emphasis on health and wellness in the post-pandemic market, combined with demographic shifts toward an aging population, has created significant market opportunities for accessible fitness activities like tennis. The United States Tennis Association's (USTA) strategic partnership with the President's Council on Sports, Fitness and Nutrition in March 2024 marks the first collaboration between a national governing body and the White House sports committee. This institutional alignment strengthens tennis's market position in addressing sedentary lifestyle concerns and cardiovascular health requirements. Studies indicate that regular tennis participation delivers measurable improvements in cardiovascular performance, blood pressure regulation, metabolic function, and bone density metrics. The sport's established infrastructure and market presence position it as a viable physical activity solution for consumers seeking improved health outcomes. The USTA's integrated nutrition education program within tennis activities has established a comprehensive wellness product offering. Similarly, Tennis Australia's strategic distribution of 6,000 Hot Shots Tennis racquets to children during the 2024 Australian Open demonstrates effective market penetration through health-focused equipment initiatives [1]Source: Tennis Australia, "A record-breaking Australian Open – AO 2024 by the numbers", tennis.com.au. This market approach has expanded tennis's consumer base from traditional sports enthusiasts to health-conscious market segments seeking sustainable fitness solutions.

Rising Youth Engagement and School Programs

Youth development programs generate consistent revenue streams through structured pathways that convert recreational players into equipment consumers throughout their competitive progression. For instance, Tennis Australia's Super 10s program implements this business model by offering team-based competition for children aged 10 and under using modified equipment, including specialized Dunlop green balls. The program operates skill development sessions through its Advantage Program, managed by Tennis Australia's Talent Team, establishing a development pipeline that drives participants toward advanced equipment acquisition. Similarly, the All India Tennis Association's investment in 13 international tournaments for 2025, with Rs 10 crore (USD 1.2 million) in prize money, indicates market expansion in emerging economies. As junior players progress through competitive tiers, their equipment requirements increase in sophistication, creating sustained market demand. This model transforms youth programs into profit centers by establishing brand preferences during players' formative years.

Development of Weather-Resilient Tennis Facilities

Climate change impacts are reshaping the global tennis racquet market, requiring manufacturers to enhance product development beyond standard performance metrics. Weather resilience has become a requirement in facility design and equipment development, as severe temperatures, humidity, and variable conditions affect court infrastructure and equipment performance. The US Open has implemented operational changes and player safety measures in response to increasing temperatures, as reported by The New York Times. Manufacturers are developing materials and coatings to ensure consistent performance in diverse weather conditions. For instance, the USD 65 million tennis and pickleball complex planned for Louisville in April 2025, incorporating solar power and weather-resistant surfaces, demonstrates how infrastructure investments influence equipment specifications. The implementation of smart courts and environmental monitoring systems generates demand for weather-adaptive racquets. This development has transformed weather resilience from a facility requirement to a product differentiator, enabling premium pricing strategies and market expansion. The market is projected to experience increased research and development investment, strategic partnerships with environmental technology firms, and increased consumer demand for durable, sustainable equipment.

Expansion of Organized Cardio-Tennis Programs

The global tennis racquet market demonstrates growth driven by the expansion of organized cardio tennis programs. Cardio tennis, implemented in 2005 by the United States Tennis Association (USTA) and Tennis Industry Association, integrates tennis drills with high-intensity cardiovascular exercise and music in a structured group fitness format. For instance, U.S. participation achieved 23.8 million by 2024, with program implementation across 30 countries and thousands of tennis facilities [2]Source: United States Tennis Association (USTA), "U.S. tennis participation surges to new high of 25.7 million players following five consecutive years of growth", usta.com . The format generates market expansion through its focus on fitness benefits and social interaction versus competitive play. Tennis facilities report increased revenue from cardio tennis classes, which incorporate performance monitoring technology such as heart rate monitors. Besides, in New England, cardio tennis represents a high-growth fitness segment, contributing to increased market penetration. This market development has generated demand for specialized racquets designed for high-volume, group-based training applications, as consumers require equipment that delivers both performance and durability. Manufacturers have responded by developing products with reduced frame weight and enhanced durability specifications to address cardio tennis requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from pickleball and padel | -1.1% | North America and Europe, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Fluctuating raw material prices | -0.6% | Global, with strongest impact on manufacturing hubs | Medium term (2-4 years) |

| High cost of professional training and facilities | -0.4% | Global, particularly in emerging markets | Long term (≥ 4 years) |

| Relatively niche status in some regions | -0.3% | Middle East and Africa and South America, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Pickleball and Padel

The emergence of sports such as pickleball and padel is affecting tennis participation rates and equipment sales. These alternative racquet sports provide benefits including greater accessibility, reduced space requirements, and attract recreational players seeking social, low-impact activities. The global tennis racquet market experiences increased competition for consumer expenditure and facility utilization from these emerging sports. This development may restrict growth potential for racquet manufacturers, specifically in the casual and entry-level segments. Alternative racquet sports are impacting tennis's market share, with pickleball participation increasing 50% while tennis records only 1% growth in 2023, according to United States Tennis Association (USTA) data. This market shift influences facility allocation, evidenced by Louisville's USD 65 million complex, which will incorporate extensive pickleball court space alongside tennis facilities when it opens in April 2025. Market demand is moving toward sports with lower entry barriers and accelerated learning periods. Pickleball specifically targets older market segments that traditionally engaged in tennis, resulting in increased competition for facility utilization and equipment sales. Moreover, the USTA reports a 14% reduction in tennis players under 18 in 2023, indicating that alternative sports are capturing potential youth market share. This demographic transition affects long-term equipment demand as senior tennis players exit the market without adequate replacement from younger segments.

High Cost of Professional Training and Facilities

The high operational costs of training programs and facility maintenance restrict the growth of the global tennis racquet market, particularly in emerging economies where participation expenses exceed average household income levels. The Lawn Tennis Association's December 2024 allocation of grassroots funding across Great Britain demonstrates the substantial capital requirements for maintaining competitive infrastructure. Professional coaching fees generate recurring operational expenses, restricting quality training access to high-income market segments. The United States Tennis Association's (USTA) USD 800 million capital investment in US Open facilities in 2025 illustrates the operational expenditure required for professional venues that attract elite players and major tournaments. These market conditions create segmentation, with premium racquet sales concentrated in established, high-income consumer segments, while impeding market penetration among new and casual players. This market dynamic diverts potential consumers toward lower-cost sports alternatives, reducing the entry-level consumer base. The limited market accessibility and high operational costs, particularly in price-sensitive regions, create strategic challenges for racquet manufacturers pursuing global market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Carbon Fiber Leadership Challenged by Hybrid Innovation

Carbon-fiber composites maintain a 57.24% market share in 2024, establishing the material as the primary choice for manufacturers requiring optimal strength-to-weight ratios. The graphite/kevlar hybrid segment demonstrates the strongest growth at 5.79% CAGR through 2030, due to increased demand for enhanced vibration control and improved handling. This market shift indicates consumer requirements for both comfort and performance, enabling manufacturers to develop premium products. Additionally, in 2024, Head Sports' implementation of bio-circular carbon fiber in prototype tennis rackets shows the industry's investment in sustainable manufacturing while meeting performance requirements. Also, the University of Manchester's research in lignin-based carbon fiber production indicates potential manufacturing cost reductions and environmental improvements.

Aluminum continues to serve entry-level segments effectively, while wood and steel maintain specific market segments for traditional applications. LANXESS's development of thermoplastic composites from recycled or bio-based materials provides manufacturers with sustainable options that meet performance requirements. The development of new materials using recycled thermoplastic polyurethane and bio-based polyamide 10.10 indicates technological advancement in materials engineering. Thus, market success depends on manufacturers' ability to implement sustainable materials while maintaining performance standards, creating market opportunities in environmentally conscious segments.

By Head Type: Midsize Dominance Faces Oversize Innovation

The midsize/mid-plus segment maintains a 62.15% market share in 2024, as professional players favor control and precision. The oversize/super oversize segment demonstrates a 5.27% CAGR through 2030, driven by recreational players requiring enhanced power and stability. This pattern indicates market development as manufacturers optimize larger head sizes to deliver improved performance while maintaining maneuverability. For instance, Wilson's Clash V3 introduction in 2025 demonstrates this market development through its flexible frame technology that ensures power balance across different head sizes. This development enables larger frames to deliver controlled power, addressing key concerns about oversized racquets' precision limitations.

Moreover, the market structure is evolving as manufacturers implement hybrid technologies that integrate the benefits of different size categories. Head's Gravity 2025 series, incorporating Auxetic 2 technology for improved shock absorption, increases the appeal of larger head sizes to players requiring control. Performance specifications, rather than size alone, now determine purchase decisions. Manufacturers who integrate advanced materials and engineering across all head size categories create opportunities for premium positioning and margin improvement.

By End User: Adult Dominance Meets Youth Acceleration

Adults hold 85.19% of the market share in 2024, reflecting their higher purchasing capacity and established equipment requirements that generate premium product demand. The kids segment is experiencing growth at a 6.73% CAGR through 2030, driven by development programs that convert junior players into consistent equipment consumers. This market pattern indicates sustained expansion as youth programs generate future adult consumers with established product preferences. For instance, Tennis Australia's Super 10s program demonstrates successful youth engagement through the implementation of modified equipment and structured competition frameworks. The program implements specialized Dunlop green balls and age-appropriate racquets to establish clear equipment progression pathways.

Meanwhile, in 2025, Yonex's partnership with Supreme for a limited edition EZONE 100 racquet demonstrates the manufacturer's strategy to capture the youth market share through brand collaborations. This approach reflects the understanding that youth purchase decisions are influenced by market trends alongside performance requirements. The market rewards manufacturers who integrate youth-specific product specifications with strategic brand positioning, enabling higher price points and increased customer retention.

By Distribution Channel: Digital Transformation Accelerates

Offline retail stores maintain a 55.38% market share in 2024, as consumers prefer physical locations for product evaluation and professional fitting services for racquet purchases. Online retail stores are experiencing growth at a 5.90% CAGR through 2030, driven by expanded inventory, price competitiveness, and improved service capabilities. The digital transformation in tennis equipment retail has resolved several operational constraints of online sporting goods sales. For instance, in June 2024, the acquisition of Tennis-Point by Fromuth Racquet Sports demonstrates the strategic value of online distribution in market expansion.

Moreover, online retailers are implementing solutions for virtual racquet purchases through digital fitting systems, detailed product specifications, and standardized return processes. Wilson's direct-to-consumer strategy for the Roland-Garros 2025 collection demonstrates the company's utilization of online channels for exclusive product distribution while maintaining retail partnerships. Distribution effectiveness now requires an integrated operational model combining online operations with in-store expertise, providing market advantages to companies that successfully implement omnichannel retail strategies.

Geography Analysis

North America accounts for 35.62% market share in 2024, attributed to developed infrastructure, high consumer purchasing power, and established market penetration. Market expansion continues through capital investments from organizations like the USTA, including the USD 800 million US Open infrastructure development project scheduled for 2025. The market experiences competitive pressure from pickleball, impacting facility utilization rates and consumer participation.

Asia-Pacific exhibits 6.02% CAGR through 2030, driven by expanding consumer base, government investment initiatives, and increased market penetration across key markets. China demonstrates substantial market development with infrastructure expansion to 30,000 tennis courts and consumer base growth to 14 million in 2024, from 1 million in 1988. Market performance metrics include WTA Wuhan Open's 80% attendance increase and China Open's 60% revenue growth. Similarly, in 2025, India's market development progresses through AITA's implementation of 13 tournaments with an INR 10 crore prize allocation.

Europe maintains consistent market growth through established distribution channels and infrastructure investments. The Lawn Tennis Association's (LTA) capital expenditure across Great Britain shows market development through infrastructure investments. According to the LTA, its total operating expenditure increased to GBP 114 million in 2023 from GBP 89.03 million in 2022 [3]Source: Lawn Tennis Association, "LTA’s Finance and Governance Report for 2023", lta.org.uk . This increase indicates the financial allocation required to expand access, maintain facilities, and support grassroots programs, which drive participation and market development in the United Kingdom. Besides, South America, and Middle East and Africa present growth opportunities in underpenetrated markets. Market performance depends on manufacturers' ability to optimize product portfolios according to regional market conditions and consumer demand patterns.

Competitive Landscape

The tennis racquet market demonstrates moderate fragmentation, allowing both established manufacturers and new entrants to gain market share through differentiated positioning strategies. Wilson, Babolat, Head, and Yonex maintain their market position through professional endorsements, research and development, and comprehensive product portfolios across consumer segments. Companies like Solinco have expanded their operations from string manufacturing to racquet production by leveraging their manufacturing expertise and distribution networks. The market structure rewards companies that combine product innovation with strategic brand positioning, enabling growth in both premium and value segments.

Technology integration has become essential for market competitiveness, with manufacturers investing in AI-powered performance analysis and sustainable materials research. Agassi Sports Entertainment's July 2025 partnership with IBM for AI-powered racquet sports solutions demonstrates the strategic value of technology partnerships. This collaboration focuses on performance analytics and product recommendations, potentially transforming consumer purchasing behavior. Similarly, the June 2024 acquisition of Tennis-Point by Fromuth indicates market consolidation and emphasizes the significance of distribution capabilities and brand portfolio management. Market opportunities exist in sustainable materials, youth-oriented products, and performance monitoring technologies.

Regional and demographic variables influence market dynamics. Local manufacturers in Asia and Europe dominate their domestic markets through product customization aligned with regional preferences. In North America and Australia, specialized manufacturers focus on specific market segments with engineered products for club players and semi-professionals. International manufacturers are implementing regional marketing strategies and market-specific product development to increase market penetration. The growth in female athletic participation and junior tournaments drives product development for specific segments, increasing market diversification. With expanding global participation, market success depends on operational flexibility and targeted market strategies.

Tennis Racquet Industry Leaders

-

Head Sport GmbH

-

Amer Sports, Inc.

-

Babolat

-

Yonex Co., Ltd.

-

Sumitomo Rubber Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wilson launched the Clash v3 Tennis Racquet series, which featured the company's new SI3DTM technology. The updated design combined flexibility with stability to deliver power, comfort, and control. The Clash v3 line comprised four models: 100, 100 Pro, 100L, and 108. The racquets were available through wilson.com and retail stores at USD 229.

- January 2025: Solinco expanded its tennis racket lineup by introducing the Whiteout and Blackout frames. The California-based manufacturer subsequently released three models of the Whiteout V2. The enhanced carbon fiber design improved playability, incorporating customer feedback to optimize the frame's performance.

- August 2024: Wilson launched the RF Collection, a tennis equipment line designed and developed in collaboration with Roger Federer. The RF 01 line included three racket models, each of which was tested by Federer. The collection also included performance bags and accessories. The RF Collection was available for purchase online and in Wilson stores.

Global Tennis Racquet Market Report Scope

| Midsize/Mid Plus |

| Oversize/Super Oversize |

| Carbon Fiber Composites |

| Aluminum |

| Graphite/Kevlar Hybrids |

| Others (Wood, Steel) |

| Adults |

| Kids |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Head Type | Midsize/Mid Plus | |

| Oversize/Super Oversize | ||

| By Material | Carbon Fiber Composites | |

| Aluminum | ||

| Graphite/Kevlar Hybrids | ||

| Others (Wood, Steel) | ||

| By End User | Adults | |

| Kids | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the tennis racquet market?

The tennis racquet market size is USD 15.85 billion in 2025 and is projected to reach USD 20.14 billion by 2030.

Which region is growing fastest in tennis racquet sales?

Asia-Pacific is the fastest-growing region, posting a 6.02% CAGR through 2030 due to rising middle-class participation and government sports investment.

Which head size category leads the market?

Midsize/mid-plus racquets lead with 62.15% revenue share, though oversize frames are expanding at 5.27% CAGR.

How are online sales influencing the industry?

Online platforms are advancing at a 5.90% CAGR as virtual fitting tools, flexible returns, and limited-edition drops gain customer trust.

Page last updated on: