Racket Sports Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

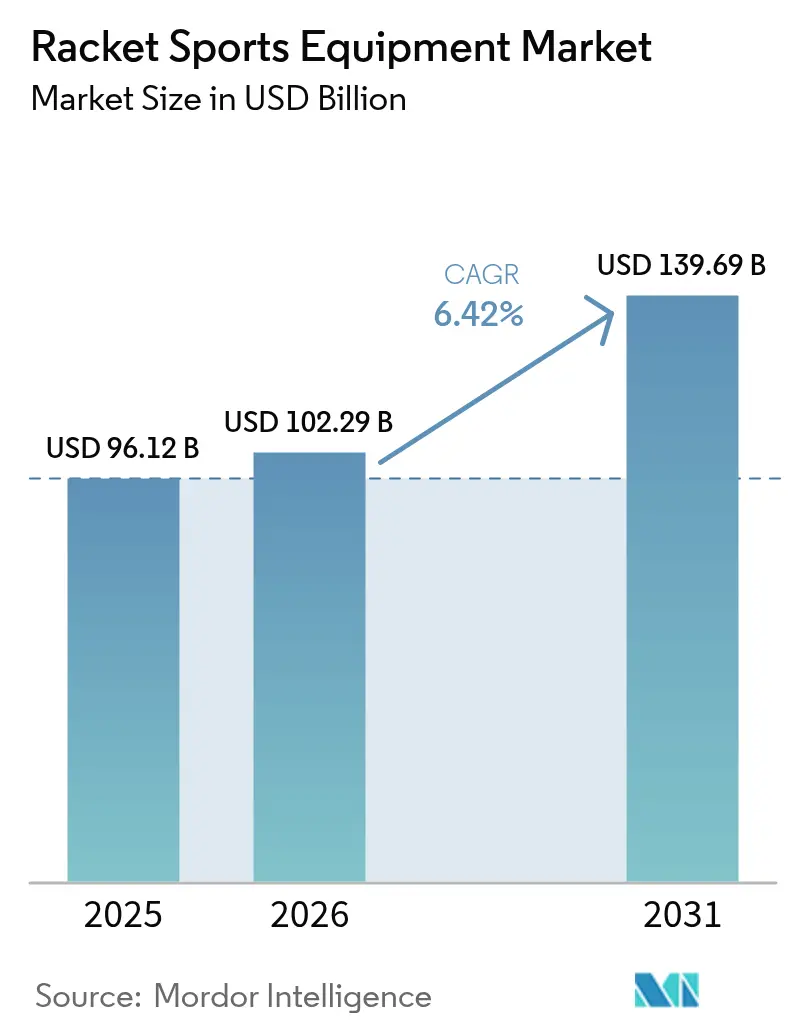

| Market Size (2026) | USD 102.29 Billion |

| Market Size (2031) | USD 139.69 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

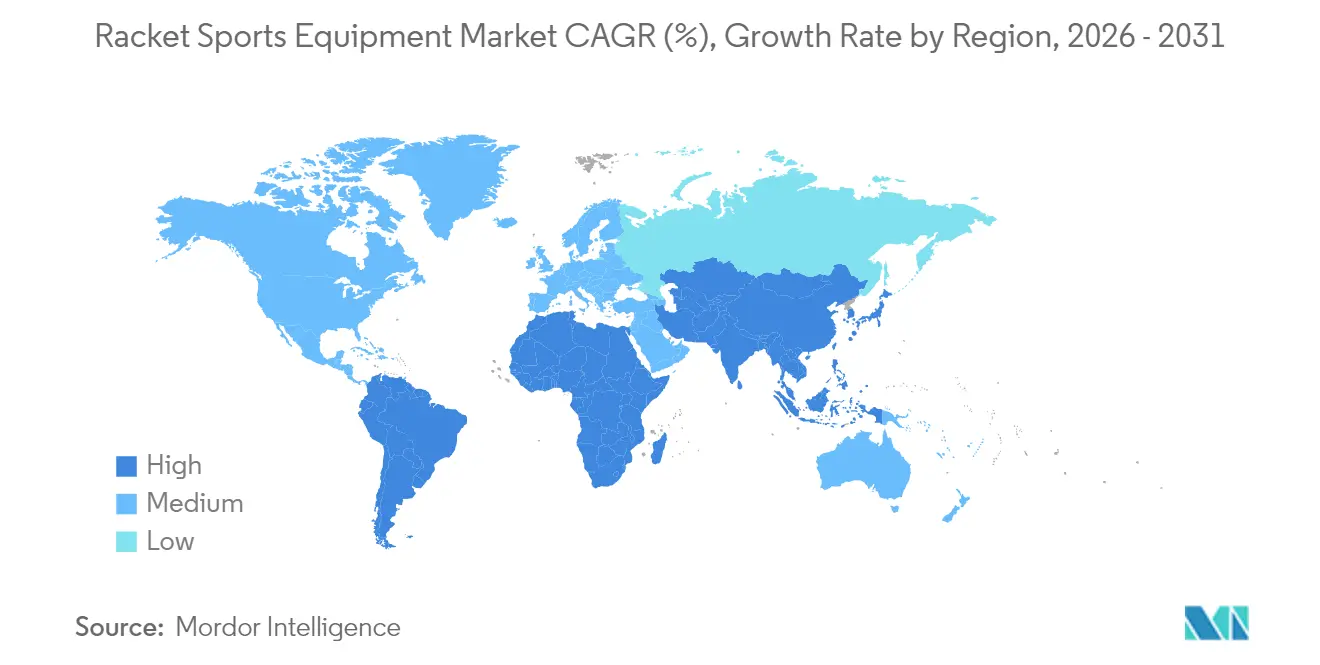

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Racket Sports Equipment Market Analysis by Mordor Intelligence

The racket sports equipment market size is expected to grow from USD 96.12 billion in 2025 to USD 102.29 billion in 2026 and is forecast to reach USD 139.69 billion by 2031 at 6.42% CAGR over 2026-2031. The market's growth is driven by the increasing establishment of indoor and outdoor courts, rising youth participation, and rapid advancements in product innovation, such as the integration of lightweight composites with smart sensor technologies. Government initiatives to fund facility expansions and the growing popularity of high-profile tournaments are further boosting market visibility and encouraging aspirational purchases. Additionally, evolving consumer preferences for sustainability, digital coaching solutions, and convenience are reshaping the market landscape. To meet these demands, companies are introducing recyclable frames, data-enabled rackets, and subscription-based services for grip and string replacements. While the Asia-Pacific region is experiencing the fastest growth, North America remains the largest contributor to overall market spending.

Key Report Takeaways

- By product type, rackets and bats led with 47.05% of the Racquet sports equipment market share in 2025, while bags and accessories are projected to expand at a 7.2% CAGR through 2031.

- By sport type, badminton accounted for 35.02% of revenue in 2025, while other sports types are projected to expand at an 7.85% CAGR through 2031.

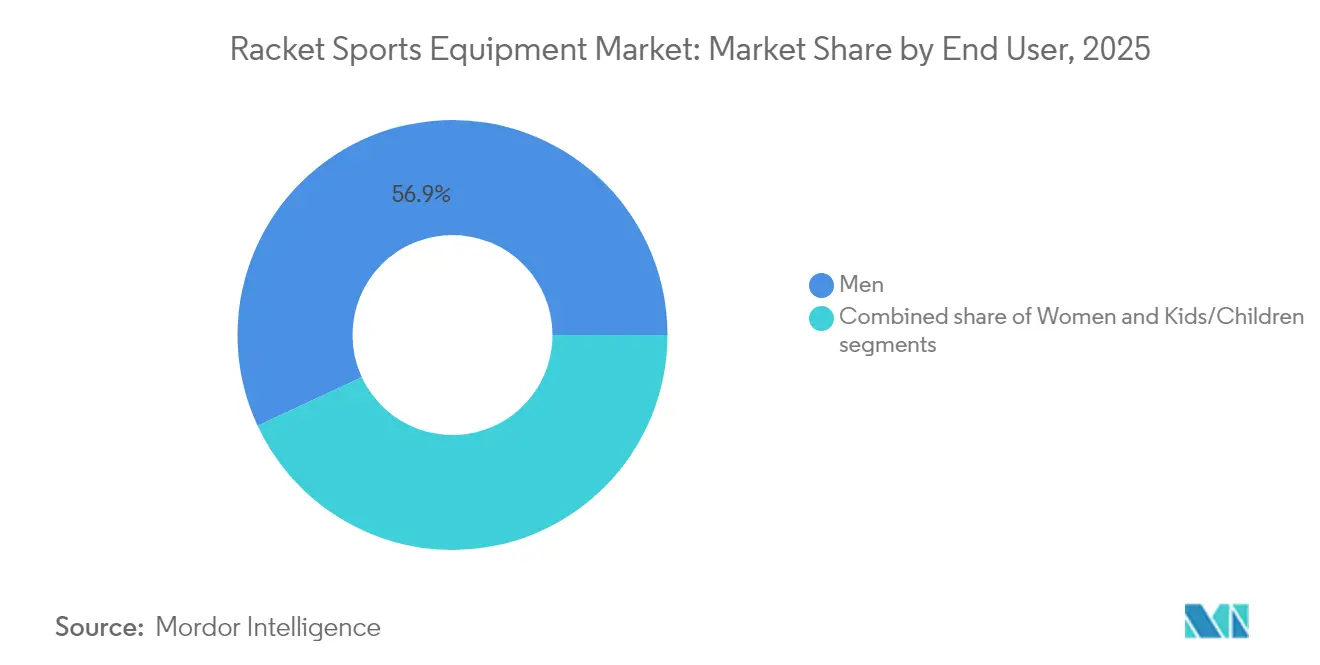

- By end user, men held 56.93% share in 2025; equipment for kids/children is set to post a 7.45% CAGR to 2031.

- By distribution channel, offline retail controlled 73.55% of sales in 2025, yet online retail stores are growing at 7.6% CAGR.

- By geography, North America remained the largest region with 32.15% in 2025, whereas Asia-Pacific is on track for an 8.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Racket Sports Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing number of racquet sports courts worldwide | +1.2% | Global, with concentrated growth in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Rising number of tournaments and leagues | +0.8% | Global, with premium impact in North America and Europe | Short term (≤ 2 years) |

| Government initiatives and sports promotion | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Increasing participation of women and children | +0.9% | Global, with accelerated adoption in developed markets | Medium term (2-4 years) |

| Technological advancements in equipment | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Influence of social media platforms and celebrity endorsements | +0.6% | Global, with youth-centric impact across all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing number of racquet sports courts worldwide

The global court construction market is witnessing significant growth, driven by the rapid expansion of padel facilities and other racquet sports infrastructure. For instance, the UK added 250 new courts between 2022 and 2023, reflecting a remarkable 116% increase. This surge highlights the growing popularity of padel across Europe. Similarly, Singapore's Punggol Regional Sport Centre, scheduled to open in 2026, will feature international-standard tennis courts designed to host major competitions. This development demonstrates how infrastructure investments are strategically targeting both recreational and professional markets to meet rising demand. The expansion of sports facilities is creating a ripple effect, the Asia-Pacific region, in particular, is experiencing a robust infrastructure boom, supported by government-backed initiatives. These initiatives focus on constructing synthetic courts and multipurpose halls that accommodate multiple racquet sports, thereby maximizing facility utilization and driving equipment demand across a broad spectrum of users. This trend underscores the region's commitment to fostering sports participation and supporting the associated industries.

Rising number of tournaments and leagues

The rapid expansion of professional tournament structures is significantly influencing recreational equipment purchasing decisions by creating aspirational demand. For instance, the Australian Open's inclusion of pickleball in 2025 highlights the sport's growing mainstream acceptance and its integration into established tournament frameworks, signaling a shift in the perception of emerging sports. Similarly, the International Table Tennis Federation's introduction of innovative formats, such as the Mixed Team World Cup, not only broadens competitive opportunities but also fosters sustained participation and drives regular equipment replacement cycles[1]The International Table Tennis Federation, " The International Table Tennis Federation Annual General Meeting", www.ittf.com. This growth in the tournament ecosystem generates a cascading impact: professional equipment preferences increasingly shape amateur purchasing trends, while enhanced media coverage boosts overall market awareness. Furthermore, grassroots league structures play a pivotal role by offering organized participation pathways. These pathways help convert casual interest into long-term engagement, ensuring consistent equipment demand as players meet the requirements of structured play and advance through competitive levels. Together, these factors create a robust and dynamic environment that supports both market growth and sustained consumer interest.

Government initiatives and sports promotion

India's Ministry of Youth Affairs and Sports has allocated ₹3,794 crores for the fiscal year 2025-26, with a significant focus on infrastructure development and athlete support programs. These initiatives include the establishment of racquet sports facilities and the procurement of necessary equipment, aiming to strengthen the foundation for sports development. In Hong Kong, the "Sport for All" culture promotes widespread participation through major events such as badminton and tennis competitions[2]Hong Kong Special Administrative Region Government, "Major Sports Events and Sports Schemes", www.gov.hk. The Young Athletes Training Scheme further supports youth development, creating a talent pipeline that contributes to the long-term expansion of the racquet sports market. Similarly, Andhra Pradesh's Sports Policy 2024-2029 prioritizes the development of world-class sports infrastructure, integrating advanced technology and emphasizing the creation of racquet sports academies and high-performance centers[3]Government of Andhra Pradesh, "Youth Advancement, Tourism & Culture(Sps.&Ys) Department", www.apiic.in. These strategic measures collectively drive sustained demand through institutional procurement channels while fostering participation pathways. As a result, government investments are effectively converted into long-term market growth, catering to multiple demographic segments and ensuring a robust foundation for the racquet sports market.

Increasing participation of women and children

Efforts to expand demographic participation are effectively extending market reach beyond traditional male-dominated patterns. The United States Professional Tennis Association has strengthened its initiatives by forming strategic partnerships with organizations like RacquetFit and introducing expanded certification programs. These programs are specifically designed to promote youth development, improve accessibility, and address critical barriers to entry. Globally, governments are implementing gender-inclusive sports policies aimed at overcoming historical challenges. These policies focus on upgrading sports facilities, providing equipment subsidies, and offering targeted coaching programs to encourage broader participation. Additionally, private sector involvement in funding and sponsorships is further accelerating the adoption of these initiatives. Youth engagement strategies, particularly those supported by institutional frameworks such as school sports programs, are proving instrumental in creating a pipeline effect. Early exposure to sports through these programs fosters lifelong participation habits, drives sustained demand for sports equipment, and cultivates a culture of inclusivity, supporting growth.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Risk of injury and safety concerns | -0.8% | Global, with heightened awareness in developed markets | Medium term (2-4 years) |

| Lack of time and lifestyle constraints | -1.1% | North America and Europe, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Limited access to facilities and infrastructure | -0.9% | Emerging markets, rural areas globally | Long term (≥ 4 years) |

| Counterfeit and low-quality products | -0.6% | Asia-Pacific manufacturing hubs, global distribution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risk of injury and safety concerns

Overuse injuries, including shoulder issues, tennis elbow, wrist ailments, and ankle problems, are the leading causes of reduced player participation in tennis. These injuries highlight the need for effective preventive measures within the market. While growing safety awareness has driven demand for protective equipment, it has also created a paradox by discouraging participation among risk-averse individuals, thereby impacting market growth. To address these challenges, equipment manufacturers are introducing advanced injury-prevention solutions, such as ergonomic grip designs and optimized string tension, aimed at reducing repetitive stress injuries. However, the high medical costs and extended recovery periods associated with racquet sports injuries remain significant barriers to long-term participation. This issue is particularly pronounced among older adults, a demographic increasingly interested in low-intensity exercise options but often deterred by the physical risks and recovery challenges associated with the sport.

Counterfeit and low-quality products

Legitimate manufacturers encounter significant obstacles in market access and brand integrity due to challenges in intellectual property enforcement. In fiscal year 2022, U.S. Customs and Border Protection seized over 21,000 items infringing intellectual property rights, with an estimated value of nearly USD 3 billion. These seizures included counterfeit sports equipment, which not only jeopardizes consumer safety but also damages brand reputation. The 2024 Special 301 Report highlights persistent deficiencies in intellectual property enforcement across key manufacturing regions[4]Office of the United States Trade Representative, "2024 Special 301 Report", www.ustr.gov. These weaknesses have facilitated the proliferation of counterfeit racquet sports equipment, which adversely impacts legitimate manufacturers by eroding their pricing power and weakening their market positioning. Counterfeit products present dual risks: they displace legitimate revenue streams and pose safety hazards. Inferior materials used in counterfeit goods can lead to equipment failures or user injuries, further harming the reputation of the entire product category.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rackets and Bats Dominance

In 2025, rackets and bats dominate the market with a 47.05% share, underscoring their pivotal role in driving market entry and forging brand-consumer relationships. Their prominence in racquet sports is evident, as the quality and performance of these tools significantly influence both player experience and competitive results. Regular replacement cycles, spurred by wear and tear, performance upgrades, and tech innovations, fuel frequent purchases, especially among dedicated players. Endorsements from professional athletes and visibility in tournaments generate aspirational demand, swaying recreational players in their equipment choices. Moreover, advancements in materials science not only facilitate continuous product differentiation but also support premium pricing strategies.

Meanwhile, bags and accessories are the market's fastest-growing segment, boasting a 7.2% CAGR through 2031. This surge signals a maturation phase, with established players broadening their portfolios beyond just rackets and balls. As consumers become more sophisticated, the integration of sports into fashion and lifestyle becomes evident, enhancing the overall experience. The segment's lower price points promote frequent purchases and gifting, while social media amplifies demand for accessories that resonate with current athletic wear trends.

By Sport Type: Badminton Leadership

In 2025, badminton commands a dominant 35.02% market share, bolstered by its deep-rooted cultural significance and robust infrastructure across the Asia-Pacific. Here, badminton enjoys not just widespread participation but also strong governmental backing. The sport's indoor nature allows for uninterrupted play throughout the year, irrespective of weather. Its modest space requirements make it a perfect fit for urban locales with limited outdoor facilities. Badminton's inherent technical complexity fuels a demand for specialized equipment, catering to a spectrum from casual players seeking affordable shuttlecocks to professionals investing in premium-grade rackets.

Meanwhile, other sports are witnessing the fastest growth, boasting an 7.85% CAGR. This surge is largely attributed to the rise of racquet sports like pickleball and padel. These newcomers prioritize accessibility and social interaction, diverging from the technical focus of their predecessors. They resonate with demographics often overlooked by tennis and badminton, such as older adults in search of low-impact exercise and younger enthusiasts attracted to the social scene. Their growth is underpinned by simplified rules and compact court sizes, lowering entry barriers. Additionally, the novelty of these sports garners significant media spotlight and social media buzz, fueling swift adoption. This landscape presents a golden opportunity for innovative manufacturers, allowing them to seize market share through tailored product development and focused marketing initiatives.

By End User: Men's Market Leadership

In 2025, men represent 56.93% of the end-user market, a reflection of historical participation trends in racquet sports. These trends are shaped by cultural influences and greater accessibility to facilities for male players. This dominance is further reinforced by structured participation pathways, heightened visibility through professional tournaments, and robust social networks that encourage sustained involvement. Male players exhibit strong purchasing power, particularly for premium equipment and technology-driven products designed to enhance performance. Additionally, frequent equipment replacement among male participants is driven by the demands of competitive play and brand loyalty, which is often cultivated through endorsements by professional athletes and associations with major tournaments.

Kids/children constitute the fastest-growing segment, with a CAGR of 7.45%, driven by targeted youth engagement initiatives and increasing parental investment in sports development. Government programs, such as India's Khelo India Scheme, play a significant role by focusing on youth development through improved school sports programs and upgraded facilities, thereby enhancing accessibility and participation. This segment benefits from institutional purchases made by schools and sports academies, while parents prioritize high-quality and safe sports equipment for their children, often placing less emphasis on cost. Early exposure to sports fosters long-term engagement, creating a pipeline effect that sustains market demand.

By Distribution Channel: Offline Retail Dominance

In 2025, offline retail stores captured a dominant 73.55% share of the market, underscoring the importance of hands-on equipment evaluation and professional fitting services for racquet sports enthusiasts. These physical retail spaces allow customers to assess racket weight, grip size, and string tension prior to purchase. Moreover, knowledgeable staff offer technical insights that significantly sway buying choices. Immediate product availability, coupled with services like stringing and equipment maintenance, fosters lasting customer relationships. Specialized sporting goods retailers leverage product expertise, strategic brand partnerships, and strong community ties, often supporting local sports programs and tournaments, to maintain their competitive edge.

Online retail stores are on a rapid ascent, boasting an 7.6% CAGR. This growth is fueled by digital transformation efforts and enhanced e-commerce experiences, effectively addressing traditional hurdles in sports equipment purchases. Key drivers of this online expansion include advanced product visualization technologies, comprehensive product specifications, and robust customer review systems, all aiding consumers in making informed choices without the need for physical inspection. Manufacturers, through direct-to-consumer strategies, not only retain margin control but also cultivate direct relationships with customers, bolstering brand loyalty and encouraging repeat purchases.

Geography Analysis

In 2025, North America secures its position as the market leader with a 32.15% share, driven by its advanced infrastructure and well-established consumer spending patterns. These factors cater to both premium and mass-market equipment categories, ensuring a balanced market presence. While traditional segments face saturation, the region's growth is sustained by the increasing adoption of emerging sports and the integration of advanced technologies into equipment. The presence of professional tournaments, including major championships and extensive media coverage, fosters aspirational demand, influencing recreational equipment purchases and shaping brand preferences.

Asia-Pacific emerges as the fastest-growing region, recording an impressive 8.05% CAGR. This growth is fueled by comprehensive government initiatives and large-scale infrastructure development programs that establish strong institutional demand channels. In India, the Khelo India Programme, supported by substantial funding for sports infrastructure and youth development, creates structured participation pathways, driving sustained market growth across diverse demographic groups. Singapore exemplifies the region's commitment to premium market development through investments in world-class facilities, such as the Punggol Regional Sport Centre, which enhance infrastructure quality and position the country as a hub for hosting international events.

Europe demonstrates steady growth, underpinned by the increasing adoption of premium products and ongoing facility modernization efforts that cater to both traditional and emerging racquet sports. The region's strong focus on sustainability and environmental responsibility has driven demand for eco-friendly equipment and innovative materials, which often command premium pricing. Government initiatives, such as the UK's "Get Active" strategy, emphasize community engagement and improved access to sports facilities, addressing participation disparities and unlocking growth potential in underserved market segments. Additionally, Europe's inclination toward technological advancements and consumer preferences for high-quality, innovative products create opportunities for manufacturers to introduce advanced offerings.

Competitive Landscape

The racket sports equipment market is moderately consolidated, with a mix of regional and global players competing for market share. Prominent companies in this market include Yonex Company, Limited, Anta Sports Products Co., Ltd., HEAD Sport GmbH, and Li-Ning Company Limited. These manufacturers primarily focus on expansion and new product development as key growth strategies. They are actively innovating their product portfolios while adopting sustainable manufacturing practices, such as utilizing recycled materials in the production of rackets and other equipment essential for racket sports.

Technological advancements are transforming the competitive landscape, compelling traditional equipment manufacturers to adapt to emerging trends like smart equipment, performance analytics, and digital customer engagement platforms. These innovations are reshaping consumer expectations and driving the demand for more advanced and connected products.

Strategic partnerships and collaborative innovations are playing a pivotal role in redefining business models. For instance, advancements in material science, particularly in sustainable composites, are enabling companies to align with evolving market demands. Additionally, white-space opportunities are emerging in underserved demographics and niche sports categories, presenting avenues for growth. Supply chain innovations are further enhancing competitiveness across various sports segments by leveraging shared manufacturing capabilities and specialized expertise, which facilitate market expansion beyond traditional boundaries.

Racket Sports Equipment Industry Leaders

-

Yonex Company, Limited

-

Anta Sports Products Co., Ltd.

-

HEAD Sport GmbH

-

BABOLAT VS SAS

-

Li-Ning Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Truls Möregårdh and STIGA Sports have launched the Pro Carbon+ Cybershape Truls Edition, a special five-star bat featuring a unique hexagonal blade with five layers of wood and two of carbon fibre, optimized for a larger sweet spot and enhanced speed and spin. Developed in close collaboration with Möregårdh, this flagship model uses advanced Touch Carbon technology and STAR5 rubber, delivering professional-level power and control without extra weight, according to the brand.

- April 2025: HEAD launched the limited-edition BOOM RAW tennis racquet on Earth Day, marking a significant step toward sustainability in racquet sports. According to the brand, the BOOM RAW is constructed entirely from Toray’s bio-circular carbon fibers, which are derived from agricultural and forestry waste that would otherwise be sent to landfill.

- April 2025: Joma and A1 Padel have launched a special edition of the high-end OPEN sneakers as the official footwear for the A1 Padel circuit. According to the brand, this edition features two new colorways—one predominantly white and the other blue—each with an avant-garde abstract print inspired by the circuit’s logo, which is also displayed on the technical mesh upper.

- April 2025: Automobili Lamborghini and Babolat, in collaboration together launched a new collection of padel racquets. According to the brand, this partnership merges Lamborghini’s iconic design and engineering excellence with Babolat’s expertise in racquet sports, resulting in high-performance padel racquets that feature advanced materials and innovative technology.

Global Racket Sports Equipment Market Report Scope

Racket sports are sports that involve hitting a ball or shuttlecock with a racket. Some examples of racket sports include tennis, badminton, squash, table tennis, racquetball, and pickleball. In these sports, players use rackets to hit a ball or shuttlecock back and forth across a net or a designated playing area. These sports can be played individually or in doubles and are popular around the world.

The racket sports equipment market is segmented by product into rackets, balls, eyewear, racket bags, shoes, and accessories. By sport, the market is segmented as equipment dedicatedly used in lawn tennis, table tennis, badminton, and squash. Based on the distribution channel, the market is classified into supermarkets/hypermarkets, specialty stores, online stores, and other distribution channels. The market is also segmented by geography into North America, Europe, Asia Pacific, South America, and the Middle East and Africa regions.

For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Rackets/Bats |

| Balls |

| Bags and Accessories |

| Apparel |

| Footwear |

| Lawn Tennis |

| Table Tennis |

| Badminton |

| Other Sport Types |

| Men |

| Women |

| Kids/Children |

| Offline Retail Stores |

| Online Retaile Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rackets/Bats | |

| Balls | ||

| Bags and Accessories | ||

| Apparel | ||

| Footwear | ||

| By Sport Type | Lawn Tennis | |

| Table Tennis | ||

| Badminton | ||

| Other Sport Types | ||

| By End User | Men | |

| Women | ||

| Kids/Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retaile Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Racquet sports equipment market?

The market generated USD 102.29 billion in 2026 and is projected to reach USD 139.69 billion by 2031.

Which product segment dominates sales?

Rackets and bats held 47.05% of 2025 revenue, making them the core purchase category.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at an 8.05% CAGR due to large-scale public investment in new courts and youth programs.

How significant is online retail for racquet sports equipment?

While brick-and-mortar stores still command 73.55% of sales, online channels are climbing at 7.6% CAGR as virtual fitting tools improve.

Page last updated on: