Tennis Shoes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

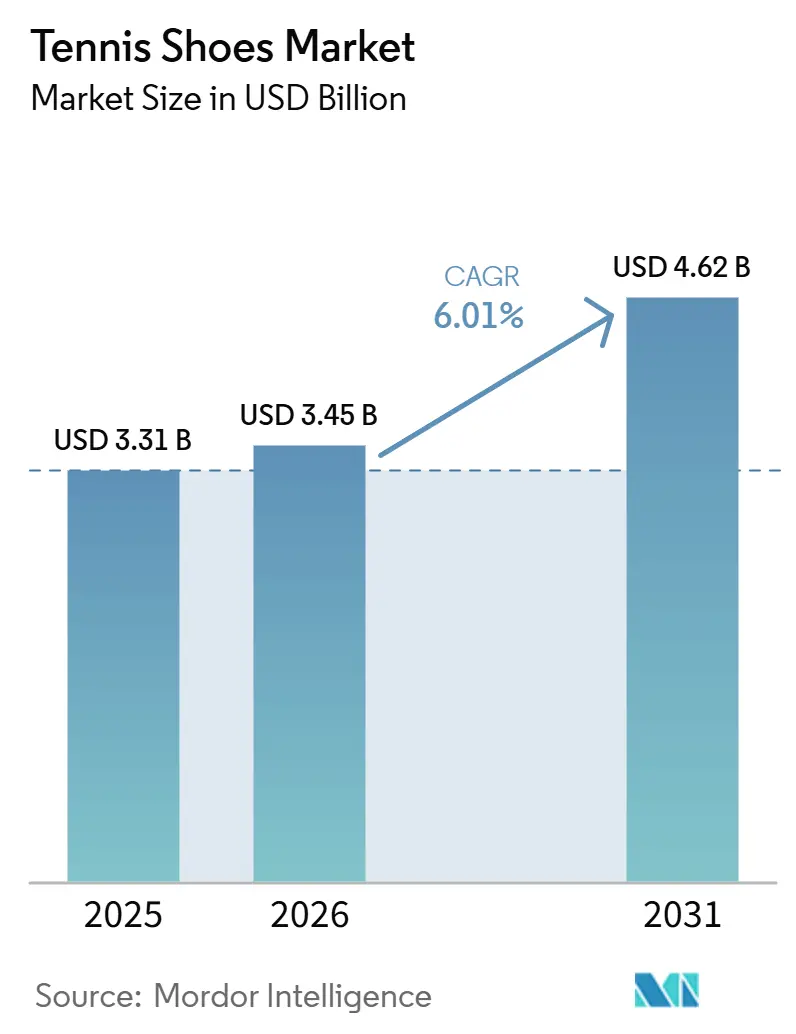

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tennis Shoes Market Analysis by Mordor Intelligence

The global tennis shoes market size is expected to grow from USD 3.31 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 4.62 billion by 2031 at a 6.01% CAGR over 2026-2031. The global tennis shoes market is primarily driven by increasing sports participation and the rising popularity of athleisure trends, where consumers seek footwear that combines performance with everyday style. The growth of professional and amateur tennis tournaments globally, along with endorsements by prominent athletes, has enhanced product visibility and brand recognition. Technological advancements, including improved cushioning, lightweight materials, and enhanced grip, are attracting both professional athletes and recreational users by offering greater comfort and reducing the risk of injuries. Furthermore, growing health awareness and fitness-focused lifestyles are prompting consumers to invest in specialized sports footwear. The expansion of e-commerce platforms, along with targeted marketing efforts and product innovations by major brands, is further driving market growth in both developed and emerging regions.

Key Report Takeaways

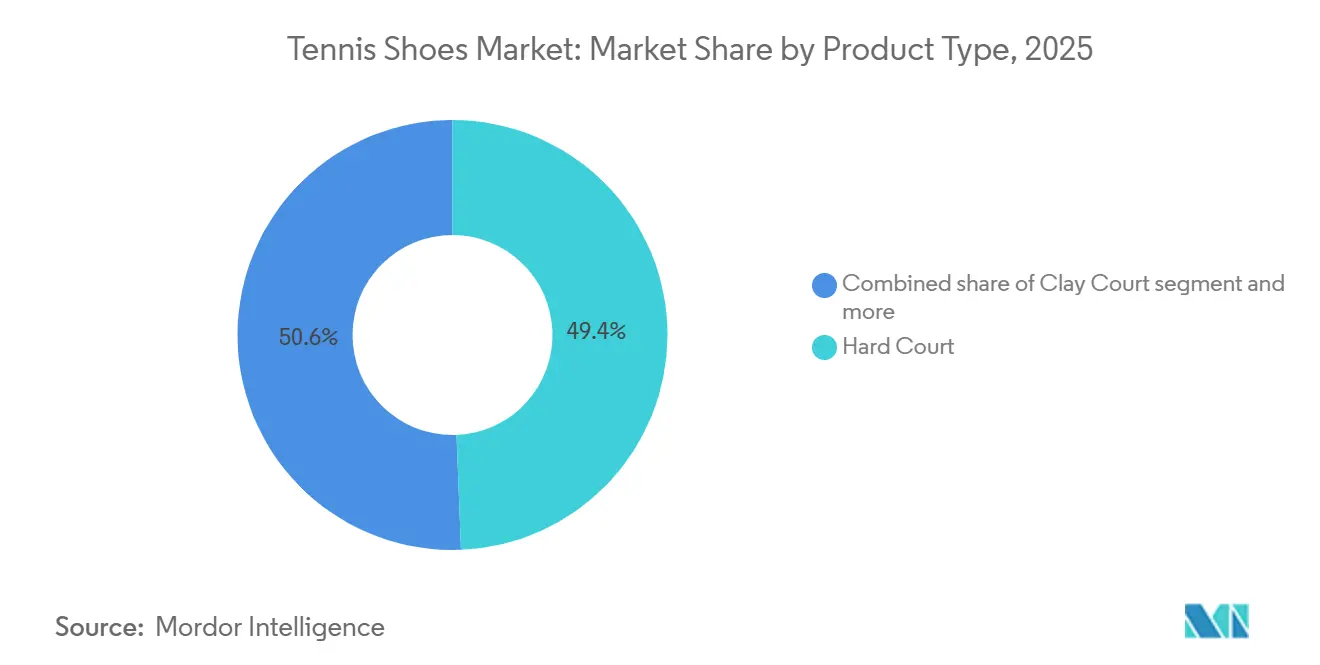

- By product type, hard court models led with 49.37% of the tennis shoes market share in 2025, while grass court footwear is expected to post the fastest 6.59% CAGR over the same period.

- By end user, men accounted for 52.41% revenue in 2025; however, the women’s segment is forecast to grow at 6.22% CAGR during the period 2026-2031.

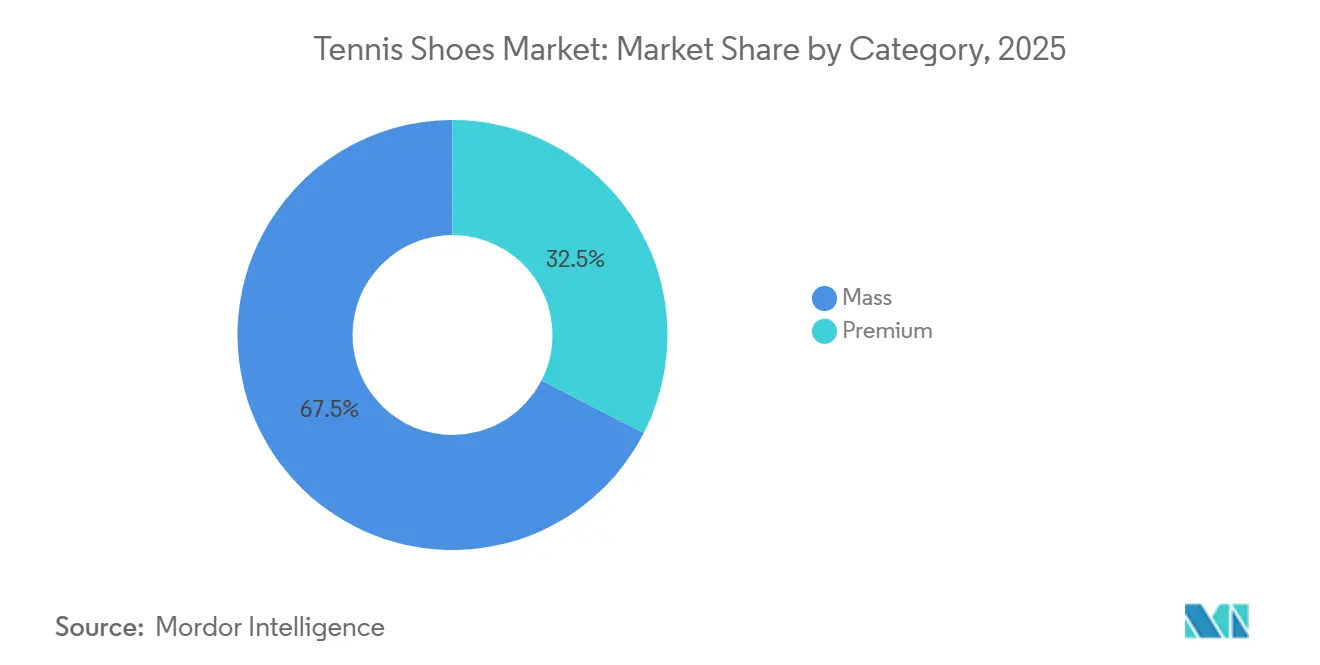

- By category, the mass segment captured 67.46% revenue in 2025, whereas premium shoes are expected to post a 6.68% CAGR to 2031, fueled by technology and customization.

- By distribution channel, offline retail retained 69.18% share in 2025, yet online sales are forecast to expand at 7.13% CAGR through 2031.

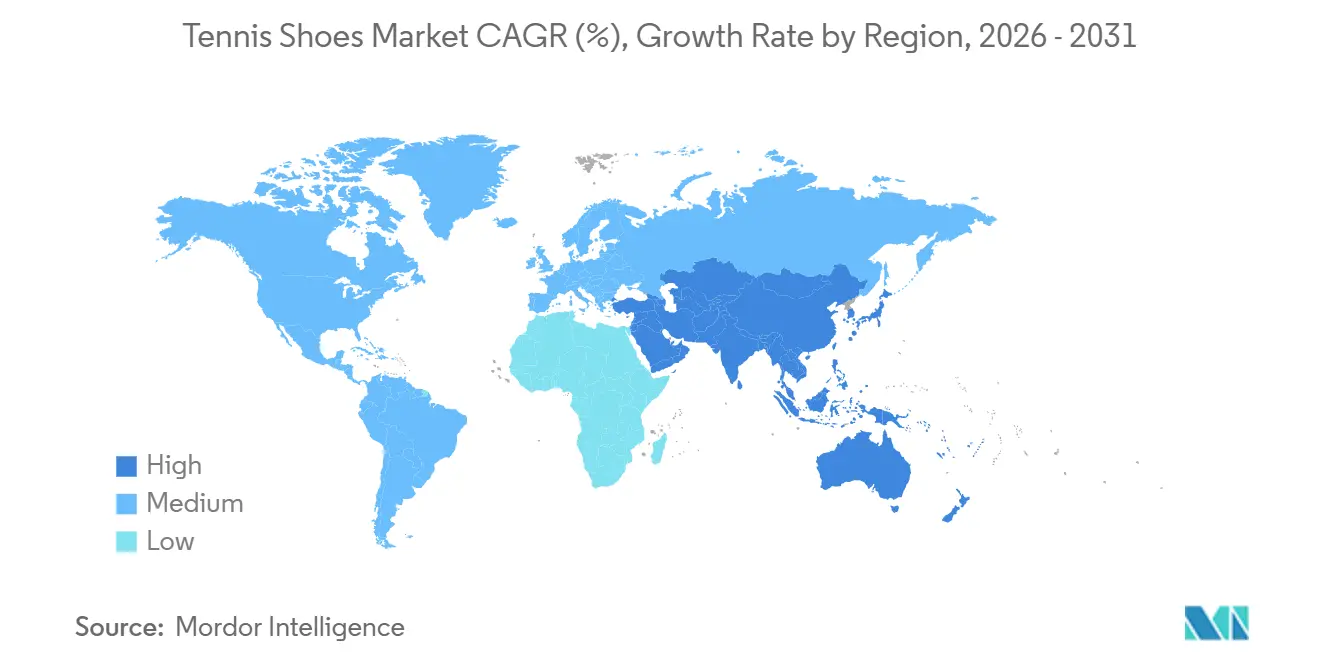

- By geography, North America led with 34.53% revenue in 2025, while Asia-Pacific is projected to register the highest 6.27% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tennis Shoes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in tennis and racquet sports | +1.2% | Global, with strongest gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in footwear design | +1.0% | Global, led by North America and Europe for R&D, manufacturing in Asia | Long term (≥ 4 years) |

| Rising influence of professional athletes and sponsorships | +0.8% | Global, with premium segment concentration in North America and Europe | Short term (≤ 2 years) |

| Growth of women's and youth participation in sports | +0.9% | Global, with accelerated adoption in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of athleisure and sportswear culture | +1.1% | Global, strongest in North America and Europe urban centers | Medium term (2-4 years) |

| Product customization and personalization trends | +0.7% | North America and Europe early adopters, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing participation in tennis and racquet sports

The surge in tennis participation globally is a significant driver for the tennis shoes market. In the United States, participation increased by 54% between 2019 and 2025, reaching 27.3 million players, fueling sustained demand for specialized footwear across recreational and competitive segments, according to the U.S. Tennis Association[1]Source: U.S. Tennis Association, "Tennis participation continues to surge with six consecutive years of growth, reaching 27.3 million players in 2025," usta.com. Asia contributed 35.3 million players during this period, driven by government investments in public courts and school programs in countries like China and India[2]Source: Tennis World, "Asia got an impressive lead in tennis industry," tennisworldusa.org. In North America, growth was influenced by post-pandemic lifestyle changes, with a shift toward outdoor and socially distanced activities that persisted into 2025. In the United States, women's participation rose by 10%, while youth enrollment in tennis programs expanded as parents prioritized skill development and college scholarship opportunities[3]Source: U.S. Tennis Association, "Tennis participation continues to surge with six consecutive years of growth, reaching 27.3 million players in 2025," usta.com. Furthermore, the diversification of the player base, particularly among Hispanic and Asian-American communities, has prompted brands to tailor their marketing strategies and product sizing to meet the needs of these previously underserved groups, further boosting the demand for tennis shoes.

Technological advancements in footwear design

Technological advancements in footwear design are driving the growth of the global tennis shoes market, as manufacturers focus on innovations to improve performance, comfort, and durability. Modern tennis shoes feature advanced cushioning systems, responsive midsoles, and shock-absorbing materials to minimize impact stress during rapid lateral movements and intense play. The use of lightweight yet durable materials, such as engineered mesh and synthetic composites, enhances breathability while ensuring structural support. Furthermore, advancements in outsole design, including optimized tread patterns and high-abrasion rubber compounds, deliver improved traction on various court surfaces, enhancing player agility and confidence. Brands are increasingly utilizing data-driven design and biomechanical research to create shoes tailored to specific playing styles, further raising performance standards. These ongoing innovations attract not only professional athletes but also recreational players seeking high-performance footwear, contributing to market growth.

Rising influence of professional athletes and sponsorships

The growing influence of professional athletes and sponsorships is a key driver of the global tennis shoes market. Top players significantly impact consumer preferences and brand perception. Endorsements by elite athletes enhance product credibility by demonstrating performance in high-profile tournaments, making their footwear choices appealing to both amateur and recreational players. Leading brands invest in long-term partnerships with Grand Slam champions to enhance visibility and differentiate their products in a competitive market. For example, Carlos Alcaraz extended his endorsement deal with Nike in 2024, reportedly valued at USD 15 million to USD 20 million annually. This underscores the importance of athlete-brand associations in building consumer trust and driving demand. Such collaborations not only strengthen brand equity but also encourage product adoption, as fans aspire to replicate the performance, style, and identity of their favorite players, contributing to sustained growth in the tennis shoes market.

Expansion of athleisure and sportswear culture

The growth of athleisure and sportswear culture is a key factor driving the global tennis shoes market, as consumers increasingly prefer versatile footwear that combines athletic performance with everyday usability. Originally designed for on-court activities, tennis shoes are now widely adopted as lifestyle products, reflecting consumer preferences for comfort, functionality, and style. Leading brands such as Nike, Adidas, and Puma are responding to this trend by launching visually appealing designs, limited-edition collections, and collaborations targeting both athletes and style-conscious consumers. Additionally, the rising impact of social media, celebrity endorsements, and the adoption of casual dress codes in workplaces and social settings is boosting the popularity of tennis shoes as everyday footwear. This trend toward multifunctional apparel is broadening the market's consumer base beyond traditional sports enthusiasts, contributing to consistent market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality products | -0.6% | Global, with highest seizure volumes in North America and Europe | Short term (≤ 2 years) |

| Intense competition from multi-sport footwear | -0.5% | Global, particularly in mass segment and emerging markets | Medium term (2-4 years) |

| Performance limitations across court types | -0.3% | Global, affecting players who compete on multiple surfaces | Long term (≥ 4 years) |

| Regulatory and compliance challenges | -0.2% | Europe and North America, driven by sustainability mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-quality products

The prevalence of counterfeit and low-quality products serves as a significant restraint on the global tennis shoes market by undermining brand integrity and diminishing consumer trust. These imitation products, often sold at considerably lower prices through unauthorized online and offline channels, appeal to price-sensitive consumers but fail to meet the performance, durability, and safety standards of authentic footwear. This negatively affects the revenue and reputation of established brands such as Nike and Adidas, while also leading to poor user experiences that may deter repeat purchases within the category. Furthermore, counterfeit goods hinder fair competition by diluting brand differentiation and reducing incentives for innovation, as companies face difficulties in protecting intellectual property and maintaining premium market positioning. The widespread availability of these products, particularly on e-commerce platforms with limited regulatory oversight, remains a significant obstacle to sustainable growth in the tennis shoes market.

Intense competition from multi-sport footwear

Intense competition from multi-sport footwear serves as a significant restraint on the global tennis shoes market. Consumers increasingly prefer versatile athletic shoes, such as running shoes, training shoes, and cross-trainers, which can be used across various activities. These multi-purpose options offer convenience, cost-effectiveness, and adequate performance for casual tennis play, reducing the demand for sport-specific tennis shoes among recreational users. Major brands, including Nike, Adidas, and ASICS, actively promote hybrid designs, creating internal competition within their product portfolios. This consumer shift toward all-in-one footwear limits the growth potential of specialized tennis shoes, particularly in price-sensitive markets where value and functionality are prioritized over sport-specific performance features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hard Courts Dominate, Grass Court Gains Prestige

Hard court tennis shoes accounted for 49.37% of the market share in 2025. The demand for these shoes in the global tennis shoes market is primarily driven by the widespread use of hard courts, which are the most common playing surface across professional tournaments, clubs, and recreational facilities worldwide. Hard courts, known for their abrasive nature, require footwear with superior durability, reinforced outsoles, and advanced cushioning systems to endure intense wear and reduce the impact on players’ joints during fast-paced rallies. As a result, manufacturers such as Nike, Adidas, and ASICS have heavily invested in technologies that enhance shock absorption, lateral stability, and outsole resilience. These features make hard court tennis shoes highly appealing to both professional and amateur players. Furthermore, the global popularity of major tournaments played on hard courts strengthens consumer preference for this segment, as players often choose footwear suited to the most frequently used playing conditions.

Grass court tennis shoes, though a niche segment, are projected to grow at a CAGR of 6.59% through 2031. The growth of this segment is driven by the demand for specialized footwear designed to provide optimal traction and stability on slippery, low-friction natural grass surfaces. Unlike hard courts, grass courts require outsoles with nubbed or pimpled patterns to prevent slipping while allowing smooth movement, making surface-specific design a key factor influencing demand. Although grass courts are less prevalent globally, their association with prestigious tournaments and traditional tennis culture sustains consistent demand for this segment. Brands such as Nike and Adidas address this niche by offering performance-oriented designs that combine lightweight construction with enhanced grip and flexibility. Additionally, the influence of professional players competing on grass surfaces motivates enthusiasts to invest in dedicated footwear, supporting steady growth despite the segment’s relatively limited geographic presence.

By End User: Women's Segment Outpaces Men's Growth

Men accounted for 52.41% of end-user demand in 2025, driven by high participation rates in both professional and recreational tennis. This demand is further influenced by major tournaments and athlete endorsements, which significantly shape purchasing behavior. Male players often prioritize performance-oriented features such as durability, stability, and impact protection, particularly for high-intensity and competitive play. As a result, brands continue to innovate with advanced cushioning systems and reinforced designs. Additionally, the widespread presence of men’s leagues, clubs, and training programs across regions sustains consistent demand. The influence of sports culture and fitness-focused lifestyles further encourages investment in specialized tennis footwear among male consumers.

The women's tennis shoe segment is expanding at a 6.22% CAGR through 2031, driven by increasing female participation in sports, empowerment initiatives, and the rising visibility of women’s tennis at global events. As more women engage in both competitive and recreational tennis, there is a growing demand for footwear that combines performance with comfort, fit, and aesthetic appeal. Leading brands such as Nike and Adidas are addressing this demand by developing gender-specific designs that consider anatomical differences, offering improved support, flexibility, and style variations. Furthermore, the expanding influence of female athletes, social media trends, and the popularity of athleisure fashion are encouraging women to adopt tennis shoes not only for sports but also for casual wear. This trend is broadening the consumer base and driving segment growth.

By Category: Premium Segment Captures Innovation Premium

The mass segment accounted for 67.46% of the market share in 2025, driven by its affordability, accessibility, and appeal to a broad consumer base, including beginners, casual players, and price-sensitive buyers. These shoes are designed to provide basic performance features such as moderate cushioning, durability, and comfort at a lower price point, making them suitable for everyday use and recreational play. The growth in grassroots sports participation and the increasing adoption of tennis as a fitness activity further bolsters demand in this segment. Additionally, brands are adopting volume-driven strategies, utilizing large-scale production, extensive retail networks, and e-commerce platforms to target diverse consumer groups, particularly in emerging markets where affordability is a critical purchase factor.

The premium category is projected to grow at a 6.68% CAGR through 2031, driven by rising demand for high-performance footwear offering superior comfort, advanced technology, and enhanced durability for competitive and professional play. Consumers in this segment are willing to invest in specialized features such as responsive cushioning, lightweight construction, superior grip, and ergonomic design, which enhance agility and reduce injury risks during intense matches. Premium products are also heavily influenced by endorsements from elite athletes and limited-edition launches, which enhance brand perception and exclusivity. Leading companies continue to innovate by integrating advanced materials and design technologies to meet the needs of serious players and enthusiasts. Additionally, the growing trend of associating premium sportswear with status, performance, and lifestyle further drives the expansion of this segment.

By Distribution Channel: Online Gains, Offline Retains Fitting Advantage

In 2025, offline retail stores account for a significant 69.18% market share in tennis shoe sales. This dominance is attributed to consumers' preference for in-store shopping, which allows them to physically evaluate product fit, comfort, and quality before purchasing. Tennis shoes, being performance-focused footwear, often require precise sizing and support assessment, prompting customers to visit specialty sports outlets and brand stores. The availability of retail staff assistance, personalized recommendations, and the opportunity to try multiple models enhances buyer confidence, especially for first-time buyers and serious players. Established brands capitalize on this trend by offering exclusive in-store collections, promotional campaigns, and immersive brand experiences to attract customers. Furthermore, the presence of organized retail networks in urban areas and sports-focused outlets near clubs and training centers bolsters offline sales.

Online retail channels are experiencing the fastest growth, with a projected CAGR of 7.13% through 2031. This growth is fueled by increasing digital adoption, the convenience of online shopping, and access to a wide range of products across various price segments and brands. E-commerce platforms enable consumers to compare features, prices, and reviews easily, facilitating informed purchasing decisions without geographical constraints. Attractive discounts, seasonal sales, and direct-to-consumer strategies by brands further encourage online purchases. Additionally, advancements in virtual try-on technologies, detailed product descriptions, and flexible return policies mitigate the perceived risks of buying footwear online. The growing impact of social media marketing, influencer promotions, and targeted digital advertising also contributes significantly to driving traffic to online platforms, accelerating the growth of this distribution channel.

Geography Analysis

North America accounted for 34.53% of the market share in 2025, driven by a well-established sports culture, high participation in tennis at both professional and recreational levels, and robust consumer spending on premium athletic footwear. The presence of major tournaments, extensive club networks, and school-level sports programs sustains consistent demand for specialized tennis shoes. Additionally, consumers in the region exhibit a strong preference for technologically advanced and performance-oriented products, prompting brands such as Nike and Under Armour to focus on continuous innovation. The widespread adoption of athleisure and fitness-focused lifestyles, along with the dominance of organized retail and e-commerce channels, further supports market growth in the region.

Asia-Pacific is the fastest-growing region, with a CAGR of 6.27% through 2031, driven by increasing sports participation, rising urbanization, and growing awareness of fitness and active lifestyles among a large and diverse population. Emerging economies such as China and India are experiencing an expanding middle class and improved access to sports infrastructure, encouraging greater adoption of tennis and related equipment. International tournaments, government initiatives promoting sports, and the influence of global brands like Adidas and ASICS are enhancing market visibility and demand. Additionally, the rapid growth of digital commerce platforms and increasing brand penetration into tier-2 and tier-3 cities are improving product accessibility, accelerating regional market expansion.

The tennis shoes market in Europe, South America, and the Middle East and Africa is influenced by a combination of established sports traditions, emerging consumer markets, and growing interest in fitness and recreational activities. Europe benefits from a strong tennis heritage, widespread participation, and a high concentration of professional events, which support steady demand for premium and performance footwear. In South America and the Middle East and Africa, rising urbanization, improving sports infrastructure, and increasing exposure to international sports are driving participation and product adoption. Brands such as Nike, Adidas, and Puma are expanding their presence through retail partnerships and digital platforms to capitalize on these growing markets. Furthermore, the influence of global sports culture and the increasing preference for casual sportswear in daily life are contributing to demand across these regions.

Competitive Landscape

The global tennis shoes market exhibits a moderately concentrated structure, with a few dominant players maintaining significant control while facing increasing competition from emerging brands. Established companies such as Nike, Adidas, and ASICS hold substantial market shares due to their global reach, strong brand equity, and diverse product offerings. However, their market dominance is being challenged by rising competitors like Hoka, On Holding, and New Balance, which are gaining popularity among performance-focused consumers seeking enhanced comfort and specialized footwear features. The competitive landscape remains dynamic, with both established and emerging brands competing for consumer attention across various market segments.

Market competition is further driven by evolving consumer preferences and the growing emphasis on product differentiation. Leading brands focus on offering advanced performance features, particularly in areas such as cushioning, stability, and durability, which are essential for both professional and recreational players. Meanwhile, challenger brands are effectively addressing niche demands by prioritizing comfort-oriented innovations and targeting players concerned with injury prevention and long-term usability. This shift has slightly impacted the dominance of established players, while emerging brands have experienced rapid growth, leading to a gradual redistribution of market share fueled by innovation and changing consumer priorities.

The competitive landscape also includes specialized tennis-focused brands such as Wilson, Babolat, and Yonex, which maintain strong positions in niche segments by catering specifically to the needs of tennis players. These brands compete with large multi-sport companies that leverage economies of scale, global distribution networks, and cross-category brand recognition. Consequently, the market is becoming increasingly fragmented, with a mix of global leaders, fast-growing challengers, and specialized players contributing to a competitive ecosystem. Differentiation, brand loyalty, and targeted consumer engagement remain critical factors in determining market positioning.

Tennis Shoes Industry Leaders

-

Nike Inc.

-

Adidas AG

-

ASICS Corporation

-

New Balance Athletics Inc.

-

Babolat VS SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: New Balance launched the CT-Rally v2 "Outdoor Court" edition in collaboration with athlete Tommy Paul, featuring Realtree EDGE camouflage and priced at USD 150, marking the first use of this camo pattern on a performance tennis shoe and targeting consumers who value aesthetic personalization alongside Fresh Foam X cushioning and durability

- January 2026: ASICS globally launched its "Move Your Body, Move Your Mind" campaign, accompanied by the introduction of the SOLUTION SPEED™ FF 4 tennis shoe.

- December 2025: Adidas launched the 14th-generation Barricade tennis shoe with LIGHTTRAXION outsole and Lightstrike Pro foam in the forefoot, representing the first use of this running-shoe technology in a tennis model and targeting players who demand improved traction, durability, and reduced weight versus prior models

Global Tennis Shoes Market Report Scope

| Hard Court |

| Clay Court |

| Grass Court |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hard Court | |

| Clay Court | ||

| Grass Court | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the tennis shoes market in 2031?

It is expected to reach USD 4.62 billion by 2031, growing at a 6.01% CAGR over 2026-2031

Which region will grow the fastest?

Asia-Pacific is projected to post the fastest 6.27% CAGR, underpinned by China’s huge participant base and rising disposable incomes.

Which product segment leads current sales?

Hard court shoes hold the largest 49.37% share owing to the prevalence of concrete and acrylic surfaces worldwide.

Why is the women’s segment appealing for growth?

Women’s tennis shoes are projected to expand at 6.22% CAGR as brands introduce gender-specific lasts that address historical fit gaps.

Page last updated on: