Tennis Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

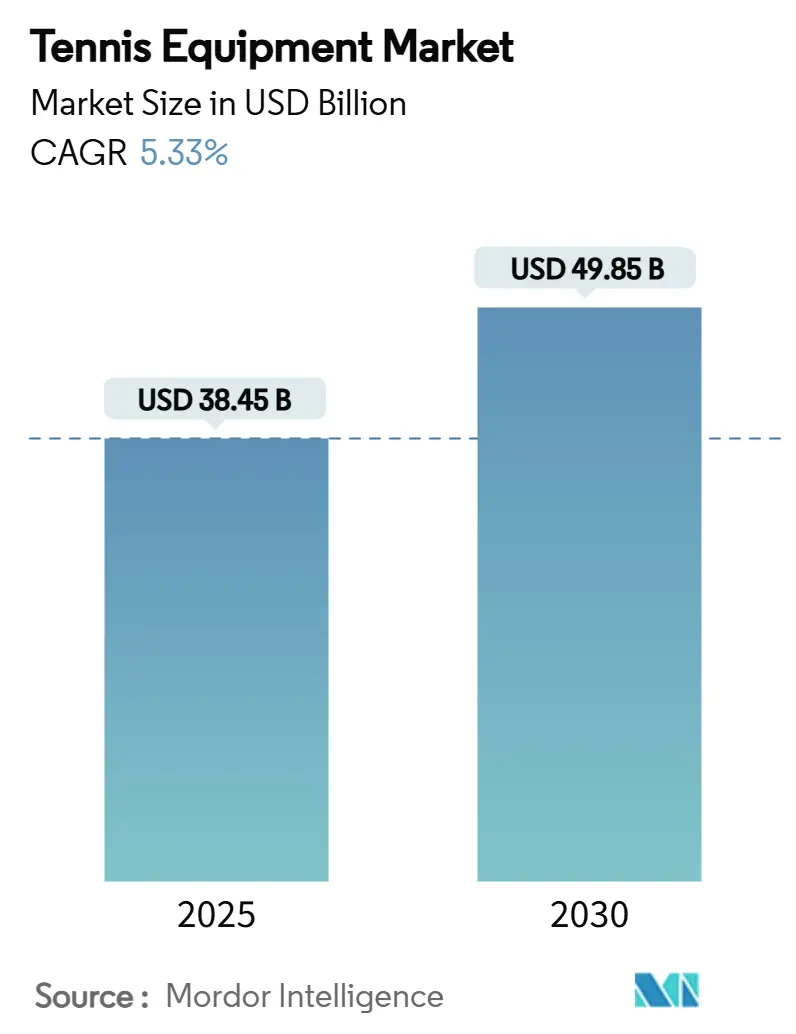

| Market Size (2025) | USD 38.45 Billion |

| Market Size (2030) | USD 49.85 Billion |

| Growth Rate (2025 - 2030) | 5.33% CAGR |

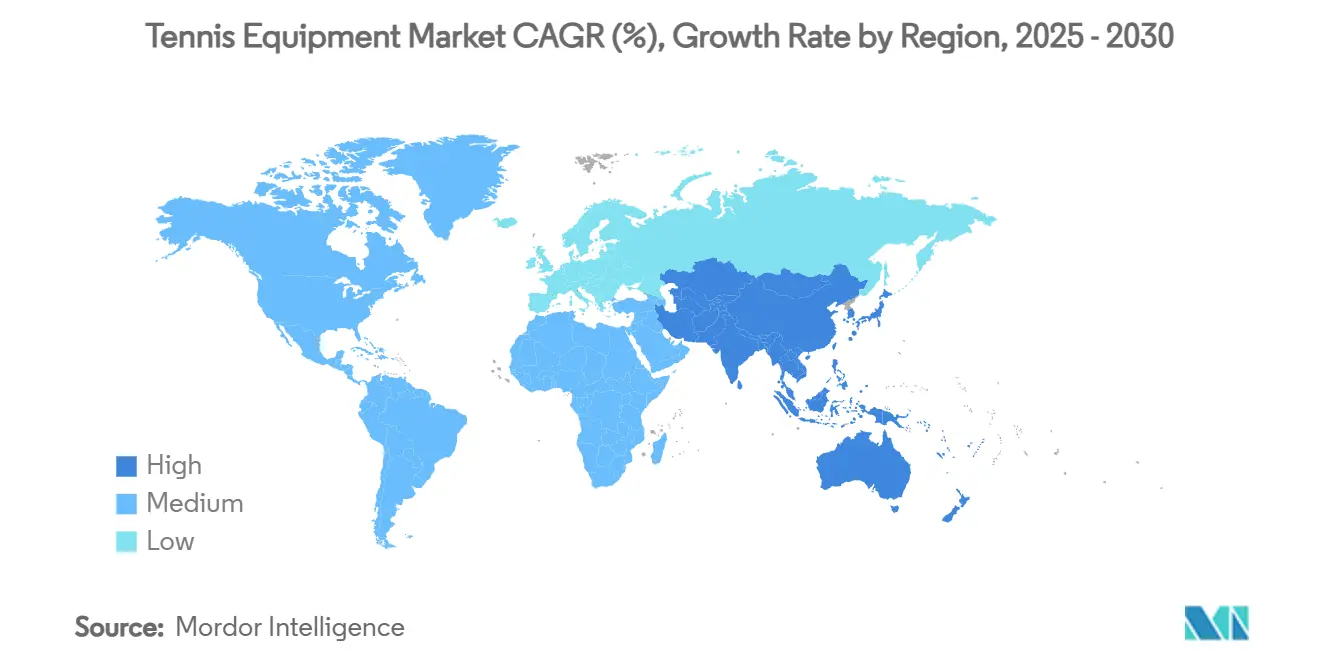

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

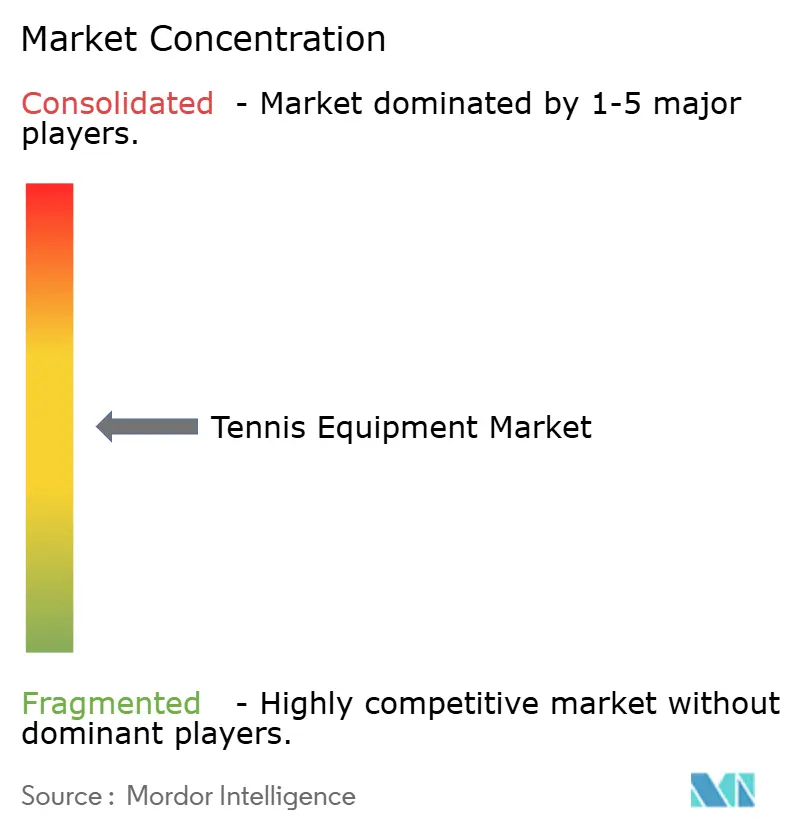

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tennis Equipment Market Analysis by Mordor Intelligence

The tennis equipment market size is estimated to be USD 38.45 billion in 2025 and is forecast to reach USD 49.85 billion by 2030, reflecting a 5.33% CAGR over the period. Rising global participation of tennis players, continued facility upgrades, and rapid product innovation collectively underpin this steady expansion. Also, companies are embedding smart materials, artificial intelligence, and sustainability features into racquets, shoes, and balls to meet players’ higher performance expectations while differentiating in a crowded field. A robust youth pipeline, fueled by grassroots programs and Olympic inspiration in China, India, and the United States, ensures a stable long-term demand base. Simultaneously, direct-to-consumer e-commerce strategies are reshaping retail economics by compressing distribution costs and capturing shopper data at scale. Although raw-material volatility and counterfeit goods weigh on margins in the short term, a moderate industry concentration enables both incumbents and challengers to pursue profitable growth.

Key Report Takeaways

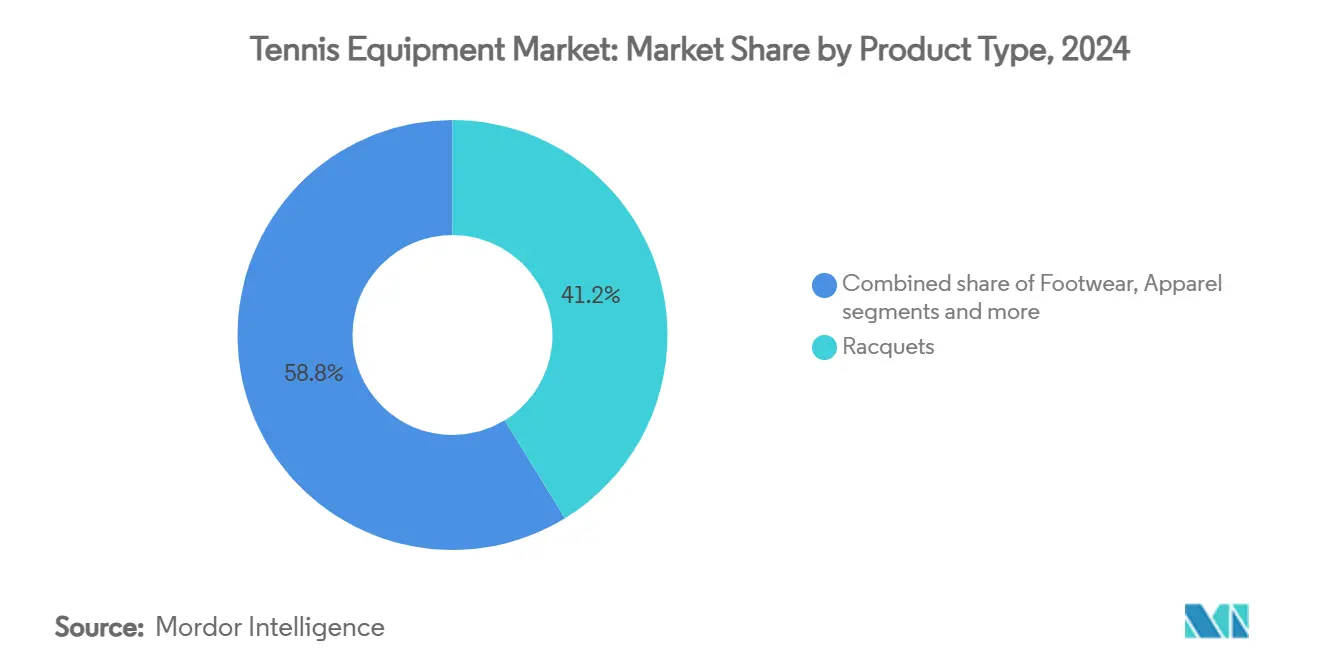

- By product type, racquets led with 41.23% of tennis equipment market share in 2024, while footwear is projected to post the fastest 5.97% CAGR through 2030.

- By end user, adults accounted for 82.09% share of the tennis equipment market in 2024; the kids segment is advancing at a 6.14% CAGR to 2030.

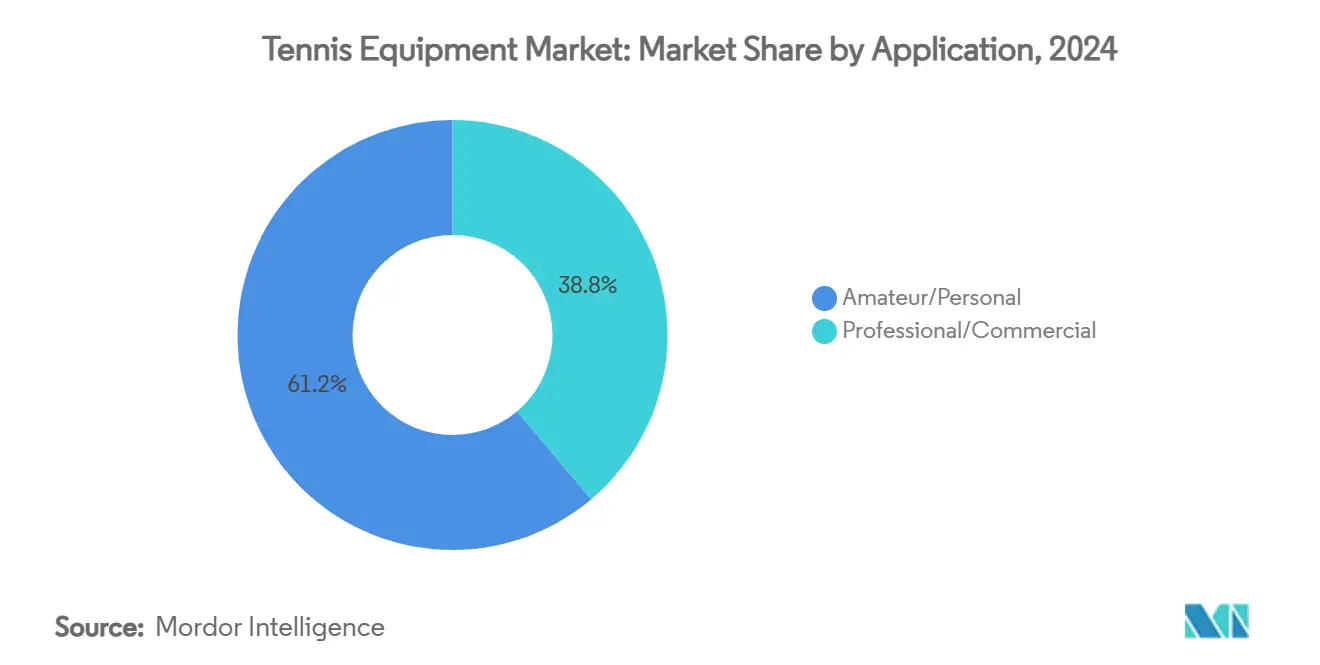

- By application, amateur/personal use held 61.16% share of the tennis equipment market in 2024 and is progressing at a 5.58% CAGR during the forecast horizon.

- By distribution channel, offline retail stores controlled 66.05% share of the tennis equipment market in 2024, whereas online channels are expanding at a 6.66% CAGR through 2030.

- By geography, North America captured 31.91% of tennis equipment market share in 2024, while Asia-Pacific is on track for a 7.30% CAGR between 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Tennis Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in tennis events and local tournaments | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surge in technological advancements | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Boosting promotion through sports celebrities and endorsements | +0.9% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Product innovation in sports apparel | +0.7% | Global, with premium adoption in developed markets | Medium term (2-4 years) |

| Retailers' shift to direct-to-consumer e-commerce models | +0.6% | Global, accelerated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Surging middle-class spending on racquet sports in Asia-Pacific | +1.1% | Asia-Pacific core, spill-over to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in tennis events and local tournaments

The expansion in volume and visibility of tennis tournaments globally and locally drives market growth for tennis equipment. Major tournaments stimulate amateur participation, accelerate product development, and generate marketing opportunities for equipment manufacturers. The increasing base of tennis players and enthusiasts strengthens the demand for racquets, balls, apparel, and accessories, supporting the market's growth worldwide. Also, the rise of tennis tournaments significantly impacted equipment demand patterns, as evidenced by the International Tennis Federation's expanded tournament schedules across regions. The ITF's appointment of Yonex as the official tennis ball supplier for three ATP tournaments from 2025 demonstrated how tournament expansion influenced equipment standardization and supply requirements. This impact extended to local tournaments, which drove equipment adoption at the grassroots level. The United States Tennis Association's (USTA) USD 800 million investment in the Billie Jean King National Tennis Center renovation in 2025, including a USD 250 million Player Performance Center, indicated a long-term commitment to tournament infrastructure development. The growth in tournaments established consistent replacement cycles for equipment such as balls, strings, and court surfaces, while providing venues to test new equipment technologies before their introduction to consumer markets.

Surge in technological advancements

Tennis equipment manufacturers are experiencing significant changes in 2025, driven by the integration of advanced materials and technology. Major manufacturers like Wilson, Babolat, and HEAD are incorporating sensor technology and data analytics into rackets to help players improve their technique and performance metrics. The market has seen notable product launches, such as Tennibot's "The Partner" ball machine in April 2025, which uses AI to adapt to players' skill levels during practice sessions. The integration of advanced materials, including graphene and carbon nanotubes, has improved racket performance and durability while enhancing player comfort. Companies are demonstrating their commitment to innovation through research and development, as evidenced by Yonex's establishment of its Performance Innovation Center in 2024. The market now encompasses a broader range of products, including technology-enabled equipment, customizable rackets produced through 3D printing, and digital coaching applications. These technological advancements have enabled manufacturers to implement premium pricing strategies while attracting both professional and recreational players, thereby strengthening market demand and establishing new industry standards.

Boosting promotion through sports celebrities and endorsements

Celebrity partnerships in tennis equipment manufacturing are evolving beyond traditional sponsorship deals into strategic brand collaborations that target diverse consumer segments. For instance, ASICS's signing of Olympic bronze medalist Lorenzo Musetti in January 2025, alongside their partnership with Novak Djokovic, demonstrates how companies build comprehensive athlete portfolios to enhance market penetration across demographics. Similarly, Frances Tiafoe's transition from Nike to lululemon in January 2025 indicates the growing influence of lifestyle brands in tennis, attracting style-conscious consumers to the sport. Also, in the Asia-Pacific region, endorsements from local athletes and Olympic champions drive regional demand and equipment adoption. Yonex's equipment contracts with players like Madison Keys, combined with their Australian Open 2025 successes, help create strong consumer connections and enhance brand loyalty. The current endorsement landscape includes athlete collaboration in product development, incorporating both performance requirements and personal style elements. Moreover, social media platforms enable athletes to directly engage with consumers and influence purchasing decisions while promoting tennis participation. These strategic celebrity partnerships contribute to market growth, product innovation, and broader consumer appeal in the tennis equipment manufacturing industry.

Retailers' shift to direct-to-consumer e-commerce models

Tennis equipment retailers are adopting direct-to-consumer (DTC) e-commerce models to establish closer customer relationships and gain data insights. The USTA's 2023 partnership with Deloitte to enhance e-commerce and private-label offerings illustrates how organizations are prioritizing digital capabilities to develop sustainable revenue streams and increase brand engagement. The DTC approach enables brands to achieve higher margins, deliver personalized experiences, and adjust inventory based on consumer behavior analysis. The 2025 E-commerce Trends Report by DHL Group indicates that 26% of global consumers purchase sports, leisure, and hobby items, including tennis equipment, through online marketplaces, while 23% make purchases via social media platforms [1]Source: DHL Group, "2025 E-Commerce Trends Report", dhl.com. Moreover, brands are using data analytics to enhance marketing strategies, personalize product recommendations, and build customer loyalty. This transformation is reflected in companies' investments in digital-first strategies, AI-powered customer service, and influencer marketing campaigns across Instagram and TikTok platforms. Consumer preferences for online shopping convenience and personalized experiences drive market expansion, influencing brand innovation, consumer engagement, and competitive dynamics.

Restraints Impact Analysis of Tennis Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw material availability | -0.4% | Global, with acute impact in manufacturing hubs | Short term (≤ 2 years) |

| Increase in Imitation/fake branded products | -0.3% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Slow adoption of circular-economy recycling programs | -0.2% | Developed markets leading, emerging markets lagging | Long term (≥ 4 years) |

| Limited tennis infrastructure in certain emerging regions | -0.5% | Emerging markets in Africa, Latin America, and parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating raw material availability

Raw material availability challenges are significantly impacting tennis equipment manufacturing operations, affecting production costs and delivery schedules across manufacturers. Supply vulnerabilities persist in synthetic materials for racquet frames, including carbon fiber, composites, and polymers, as well as rubber and felt for tennis balls. Recent tariff implementations in key markets have increased costs and forced companies to reevaluate their sourcing strategies. The environmental impact is significant, with annual production of 330 million tennis balls, of which 95% end up in landfills, creating pressure to secure sustainable material alternatives as per the Ellen MacArthur Foundation in 2023 [2]Source: Ellen MacArthur Foundation, "Running rings: why we need a circular economy for sports kit", ellenmacarthurfoundation.org. In response, manufacturers are adopting vertical integration strategies, exploring alternative sourcing options, and developing products using single materials and recycled content. Examples include the International Tennis Federation's single-material ball prototypes and Phoenix Tennis Ball's recycled products. However, smaller manufacturers struggle to secure long-term contracts or manage cost increases, potentially leading to market consolidation. The market's future performance increasingly depends on developing robust supply chains and advancing material innovation to address both supply disruptions and environmental concerns.

Limited tennis infrastructure in certain emerging regions

Limited tennis infrastructure in emerging regions creates significant market barriers, restricting both grassroots participation and player development. Countries across Asia, Africa, and parts of Latin America encounter substantial barriers to entry, including high initial construction costs and a shortage of skilled maintenance personnel. These regions demonstrate a notable scarcity of public access facilities, tennis clubs, school programs, and municipal investments compared to established markets in North America and Europe. The infrastructure deficit directly impacts equipment sales potential, as players without reliable access to quality courts are less likely to make regular purchases of racquets, balls, and apparel. Additional challenges include increasing urbanization pressures, competition for recreational space, and the tendency to prioritize sports with lower infrastructure requirements. While some countries are making progress through targeted infrastructure initiatives, such as Canada and China's investments in year-round facilities and community programs, development remains slow in many populous nations. Market growth will continue to be asymmetrical, primarily concentrated in established markets and regions that emphasize sports infrastructure development, until emerging markets implement viable solutions for expanding court access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tennis Equipment Market Segment Analysis

By Product Type:

Racquets Lead Despite Footwear's Rapid AscentRacquets hold a 41.23% market share in 2024, maintaining their position as the essential equipment purchase for tennis players across all skill levels. This segment's strength is supported by technological advancements, as seen in Wilson's Clash V3 series with SI3D technology launched in 2025, which offers improved frame flexibility and off-center stability. Natural wear of strings and frames creates consistent replacement cycles, providing manufacturers with stable revenue streams.

The footwear segment is projected to grow at 5.97% CAGR during 2025-2030, making it the fastest-expanding category. Growth is exemplified by ASICS's GEL-RESOLUTION X tennis shoe release in January 2025, which features FF BLAST PLUS ECO foam for cushioning and DYNAWALL technology for lateral stability. Moreover, tennis balls maintain consistent demand due to regular replacement needs, while apparel growth is supported by designs that appeal to both athletic and casual consumers. The bags and accessories segment shows increasing potential, demonstrated by Wilson's 2025 Roland-Garros Collection's premium pricing strategy. The "Others" category, comprising training aids and court equipment, is expanding through the integration of AI technology and smart training solutions.

By End User:

Adult Dominance Challenged by Youth MomentumAdults account for 82.09% of the market in 2024, driven by their higher purchasing power and continuous engagement with tennis. This segment shows strong adoption of premium products, as professionals and dedicated amateurs invest in high-performance equipment to improve their game. The stable adult market provides manufacturers with consistent revenue and opportunities in the premium segment. Besides, tennis serves as both a fitness activity and a social sport for adults, driving regular equipment upgrades and repeat purchases.

The kids segment is growing at 6.14% CAGR, fueled by rising youth participation and increased parental investment in children's athletic development. Manufacturers have responded with specialized products, including lightweight racquets and size-appropriate equipment to improve playability for young players. According to the United States Tennis Association, players under 35 contributed to two-thirds of the 8% growth in US tennis participation in 2024 [3]Source: United States Tennis Association, "2025 U.S. Tennis Participation Report", usta.com. The expansion of school programs and junior development initiatives continues to drive equipment demand, while parents increasingly view tennis as a valuable skill. Additionally, the influence of professional athletes and Olympic success stories inspires young players to pursue tennis, maintaining steady demand for beginner and intermediate equipment.

By Application:

Amateur Market Drives Accessibility InnovationAmateur/personal application segment accounts for 61.16% of the market share in 2024 and is expected to grow at a CAGR of 5.58% through 2030. This dominance reflects tennis's widespread popularity as a recreational activity. The segment's strength stems from consistent demand for accessible, user-friendly equipment that combines performance with playability, enabling manufacturers to develop products specifically for recreational players. The growth is further supported by increasing health and wellness awareness, as tennis provides an effective form of exercise suitable for various age groups.

Professional/commercial segment, despite its smaller volume, maintains significant market influence through premium pricing and technological innovation. Professional equipment usage in tournaments and media coverage shapes consumer preferences and purchasing patterns among recreational players. The market expansion is supported by continued infrastructure development, including public court renovations and facility improvements. For instance, the UK's Department for Culture, Media and Sport initiated the renovation of 1,000 public courts in 2023, enhancing accessibility for both amateur and professional players.

By Distribution Channel:

Digital Transformation Accelerates Online GrowthOnline retail stores are growing at 6.66% CAGR, outpacing traditional offline channels as consumers shift toward digital shopping platforms. Growth stems from improved online experiences, including virtual fitting tools and AI-powered product recommendations that enhance consumer decision-making. Lawn Tennis Association's 2024 partnership with Pro:Direct Tennis exemplifies governing bodies' utilization of digital distribution channels to expand reach. E-commerce growth strengthens through direct-to-consumer strategies, allowing brands to develop stronger customer relationships while improving profit margins.

Offline retail stores hold 66.05% market share in 2024, highlighting the importance of physical product interaction, especially for premium equipment like racquets, where grip size and weight distribution are essential considerations. For instance, in June 2024 acquisition of Tennis-Point by Fromuth Racquet Sports demonstrates retail sector consolidation as companies integrate online capabilities with physical stores. Traditional retailers implement omnichannel strategies that combine online and offline experiences, including in-store pickup options for online purchases and digital catalogs in physical locations. Distribution landscape continues to evolve toward hybrid models that combine the advantages of both channels to address varying consumer preferences.

Geography Analysis

North America Tennis Equipment Market

North America holds 31.91% market share in 2024, with the United States leading regional growth through its 25.7 million tennis players and continuous infrastructure development. Key investments include the USTA's USD 800 million transformation of the Billie Jean King National Tennis Center and the USD 125.4 million Swing Racquet + Paddle facility in Raleigh, scheduled for May 2025. Canada and Mexico contribute to market expansion through increased participation and facility development. The region's established market structure supports premium product adoption, backed by robust corporate sponsorship, developed retail networks, and widespread sports participation across demographics.

APAC Tennis Equipment Market

The Asia-Pacific tennis equipment market is experiencing significant growth, with certain segments expected to reach CAGRs of 7.30% during 2025-2030. This expansion is primarily driven by increasing urbanization, government investments in sports facilities, and growing tennis participation across major cities. Equipment manufacturers are responding by expanding their product lines and establishing partnerships with regional athletes and sports organizations. The market demonstrates strong performance in shoes and racquet sales, supported by an increase in international tournament hosting and national fitness programs. The combination of grassroots tennis development initiatives and the strong presence of both global and regional manufacturers is strengthening the region's position in the global market. With continuous development in tennis infrastructure and a growing player base, Asia-Pacific is positioned to be a key growth driver in the global tennis equipment market through 2030.

EMEA and South America Tennis Equipment Market

Europe demonstrates consistent growth, supported by its strong tennis heritage and infrastructure investments, including the UK's GBP 30 million public court renovation program planned for June 2025. Major tournaments, particularly Wimbledon, stimulate equipment demand and enhance brand visibility. Germany, France, and Italy represent established markets with consistent demand, while Eastern European countries present growth opportunities through rising participation rates and economic advancement. The Middle East and Africa, alongside South America, show substantial growth potential through developing tennis infrastructure and increasing participation rates, supported by international development initiatives and sports investments.

Competitive Landscape

Tennis equipment manufacturing exhibits moderate fragmentation, with established manufacturers maintaining significant market positions while competing against new entrants and specialized equipment producers. Competition in tennis equipment manufacturing spans multinational corporations and specialized manufacturers across product development, athlete sponsorships, and international distribution. Companies like Nike, Adidas, Yonex, Wilson, and Head maintain market leadership through research and development investments, product improvements, and professional player endorsements. These companies utilize extensive distribution channels and substantial marketing resources to maintain market presence and support premium product positioning. The market has also attracted lifestyle brands targeting tennis-inspired fashion segments, while specialized manufacturers enter with distinct products focused on sustainability or customization options.

Product innovation remains a key competitive factor, with manufacturers focusing on developing lightweight racquets, incorporating smart technologies, and improving string materials and clothing designs. Recent product launches, including Babolat's Pure Drive Gen11 and ASICS' tennis footwear, demonstrate the industry's focus on performance optimization and player comfort. Companies are also responding to changing consumer behaviors, particularly the increase in online purchases and demand for customized equipment. Market differentiation strategies include tournament sponsorships, special edition releases, and partnerships that build customer loyalty across both recreational and professional segments.

The market faces competitive pressures from counterfeit products, raw material price volatility, and limited market access in developing regions. Large manufacturers address these challenges through supply chain improvements and strategic inventory placement, while smaller companies typically experience extended delivery times and higher production costs. Environmental sustainability has become increasingly important, with companies developing recycled materials and environmentally responsible manufacturing processes. As tennis participation grows and consumer preferences change, companies must combine product innovation with effective pricing and distribution strategies to maintain market positions.

Tennis Equipment Industry Leaders

-

Head Sport GmbH

-

Amer Sports, Inc.

-

Babolat VS SAS

-

Yonex Co., Ltd.

-

Sumitomo Rubber Industries

- *Disclaimer: Major Players sorted in no particular order

Tennis Equipment Market Companies Covered in this Report

- Amer Sports, Inc.

- Head Sport GmbH

- Babolat VS S.A.S

- Yonex Co., Ltd.

- Sumitomo Rubber Industries, Ltd. (Dunlop Sports)

- Tecnifibre, S.A.

- Authentic Brands Group LLC

- Diadem Sports

- Furi Sport

- Mizuno Corporation

- PACIFIC GmbH

- Volkl Tennis

- Asics Corporation

- Nike, Inc.

- Adidas AG

- New Balance Athletics, Inc.

- Lotto Sport Italia S.p.A.

- PowerAngle LLC

- Gamma Sports

- Joma Sport, S.A.

Recent Industry Developments in Tennis Equipment Market

- March 2025: ASICS and French fashion label A.P.C. established a strategic partnership to introduce a Tennis Collection before the European Tennis Tour. The collection incorporated both on-court and off-court apparel. The 20-piece on-court collection integrated ASICS' performance technology with A.P.C.'s design specifications. The women's collection consisted of the Crew Dress, Crew Sleeveless Top, 2-N-1 Short, Longline Bra, and 7-inch Sprinter Short. The men's collection comprised the Crew Short Sleeve Top, Crew Sleeveless Top, and 5-inch Short.

- January 2025: ASICS announced the launch of the GEL-RESOLUTION™ X tennis shoe. The latest model in the series provided enhanced comfort and stability. The GEL-RESOLUTION™ X would be available from January 10, 2025, at ASICS stores, asics.com, and global retail partners.

- August 2024: Wilson launched the RF Collection, a tennis equipment line designed and developed in collaboration with Roger Federer. The RF 01 line included three racket models, each of which was tested by Federer. The collection also included performance bags and accessories. The RF Collection was available for purchase online and in Wilson stores.

Global Tennis Equipment Market Report Scope

Segmentation Overview

| Racquets |

| Balls |

| Apparel |

| Footwear |

| Bags and Accessories |

| Others |

| Adults |

| Kids |

| Professional/Commercial |

| Amateur/Personal |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Racquets | |

| Balls | ||

| Apparel | ||

| Footwear | ||

| Bags and Accessories | ||

| Others | ||

| By End User | Adults | |

| Kids | ||

| By Application | Professional/Commercial | |

| Amateur/Personal | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current tennis equipment market size and expected growth?

The tennis equipment market size is USD 38.45 billion in 2025 and is projected to reach USD 49.85 billion by 2030, delivering a 5.33% CAGR.

Which region is expanding fastest in the tennis equipment market?

Asia-Pacific is forecast to grow at a 7.30% CAGR between 2025-2030, driven by rising middle-class incomes and substantial infrastructure investment.

Which product category leads revenue today?

Racquets dominate with 41.23% tennis equipment market share in 2024, benefiting from continuous technological upgrades and predictable replacement cycles.

How are sales channels changing?

Online retail is posting 6.66% CAGR as brands pivot to direct-to-consumer models, although offline stores still capture 66.05% of 2024 sales owing to hands-on fitting services.

Page last updated on: