Volleyball Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

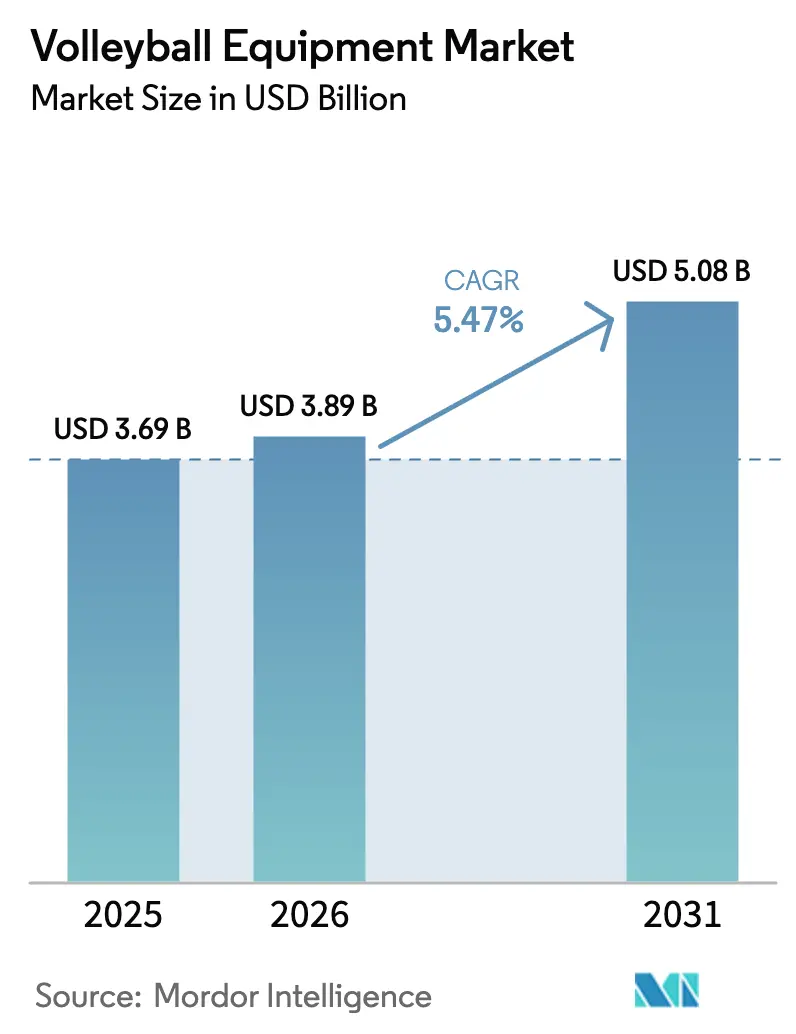

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East and Africa |

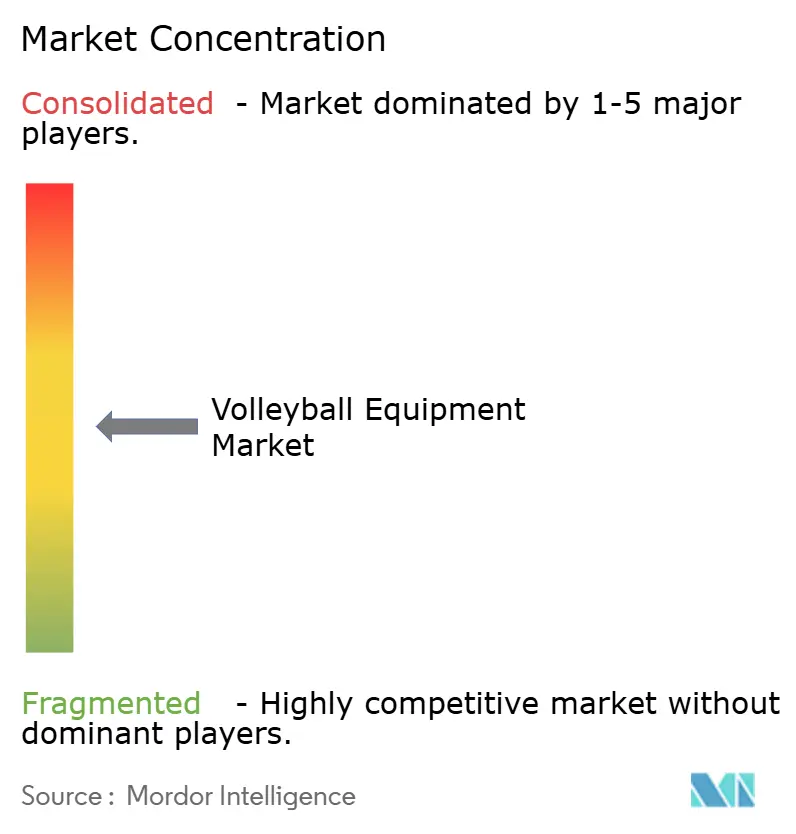

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Volleyball Equipment Market Analysis by Mordor Intelligence

The volleyball equipment market size in 2026 is estimated at USD 3.89 billion, growing from 2025 value of USD 3.69 billion with 2031 projections showing USD 5.08 billion, growing at 5.47% CAGR over 2026-2031. Persistently rising global participation, federation-backed prize purses, and a push to professionalize regional leagues lift baseline demand for certified balls, net systems, and court infrastructure. Institutional spending is amplified by the Fédération Internationale de Volleyball’s USD 44 million Volleyball Empowerment program and its commitment to return 70% of income as prize money by 2028, a policy that cascades procurement across 222 member federations[1]Source: Fédération Internationale de Volleyball, “Beach Pro Tour Statistics,” fivb.com. Asia-Pacific retained leadership with a 35.71% revenue share in 2024 on the back of China’s 4.6 million sports venues and India’s bolstered Khelo India budget, while the Middle East and Africa are growing fastest at 7.16% thanks to Qatar-hosted FIVB events and the UAE’s Special Olympics success. At a product level, volleyballs accounted for 44.84% of revenue in 2024, while sensor-enabled training gear was the fastest-growing category at 6.85%, as clubs seek data-rich coaching aids. Offline retail still accounts for 67.43% of global turnover, but online channels are advancing at a 7.43% CAGR.

Key Report Takeaways

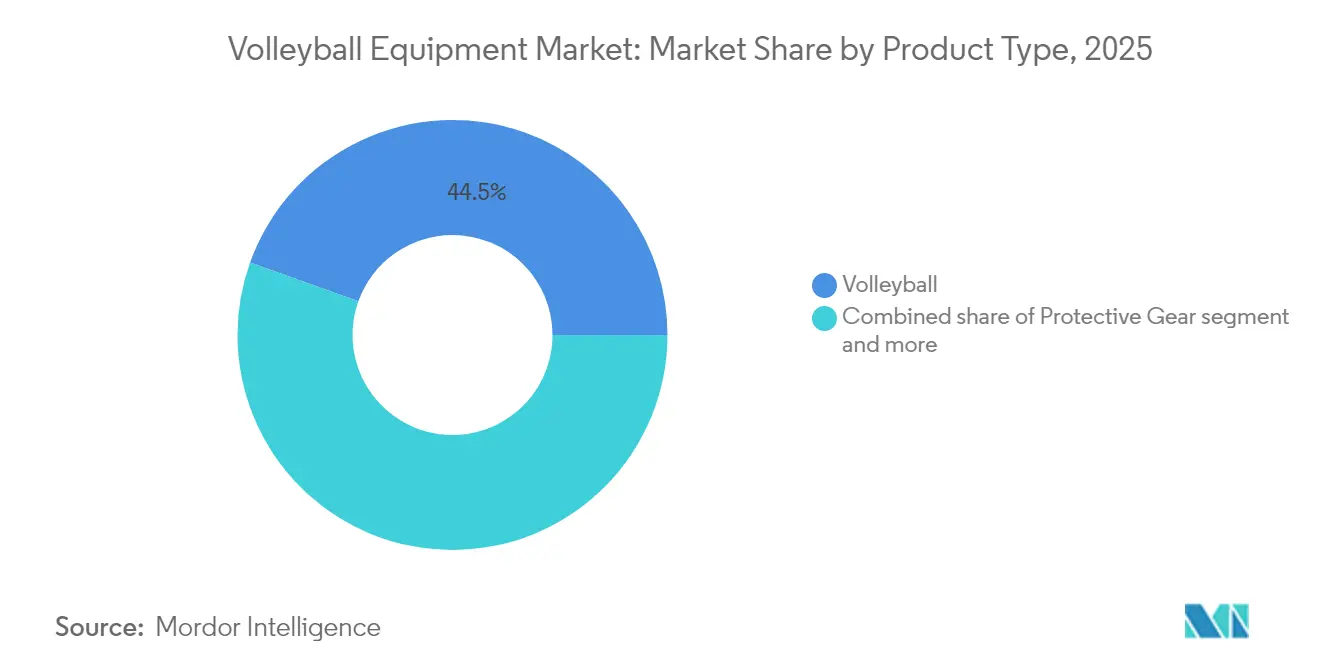

- By product type, volleyballs led with a 44.53% revenue share in 2025, whereas training equipment and accessories are expected to expand at a 6.75% CAGR through 2031.

- By volleyball type, indoor products commanded a 61.02% share of the volleyball equipment market size in 2025, while beach variants are projected to grow at a 5.93% CAGR through 2031.

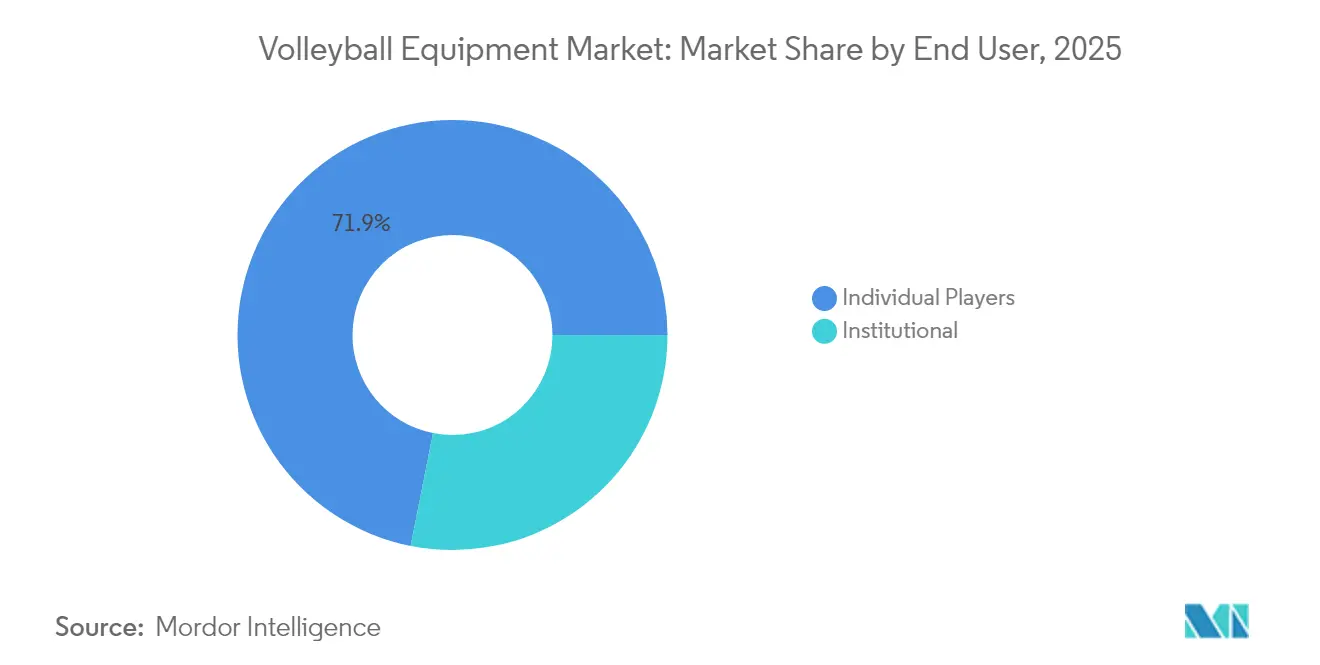

- By end-user, individual players accounted for 71.88% of the volleyball equipment market share in 2025, while institutional buyers were projected to register the highest CAGR of 6.42% through 2031.

- By distribution channel, offline channels accounted for 66.95% of the revenue in 2025, while online channels are projected to achieve a 7.32% CAGR through 2031.

- By geography, the Asia-Pacific region secured a 35.44% share in 2025, whereas the Middle East & Africa is slated for the fastest 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Volleyball Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global participation and professional leagues | +1.2% | Global, especially Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Expansion of school and collegiate sports programs | +0.9% | North America, Europe, India, China | Long term (≥4 years) |

| Smart, sensor-enabled equipment adoption | +0.7% | North America, Europe, Japan | Short term (≤2 years) |

| Sustainable material innovation in balls and nets | +0.6% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| High demand for performance-engineered balls | +0.8% | Global, led by pro and collegiate circuits | Short term (≤2 years) |

| Expansion of club, school, and academy ecosystems | +1.0% | India, China, Middle East and Africa, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global Participation and Professional Leagues

The FIVB Volleyball Nations League expanded its field to 18 national squads in 2025, and the Beach Pro Tour increased entries by 41%, rising from 704 teams in 2024 to 992 in 2025, backed by USD 6.75 million in prize money, according to the International Volleyball Federation (FIVB). Each newly ranked team triggers incremental purchases of match balls, practice balls, referee stands, and certified net systems that meet FIVB homologation. Japan’s SV.League rebrand lifted foreign-player limits and targets Premier League status by 2030, a move that is already lifting demand for Mikasa’s FIVB-approved balls and Senoh’s carbon-fiber poles[2]Source: Japan Times, “SV.League Rebranding,” japantimes.co.jp. Official-supplier agreements effectively lock brands into multi-year equipment contracts, while grassroots clubs, eager to mirror elite standards, gravitate toward the same vendors. This halo effect increases lifetime revenue per customer, especially in emerging federations that are pressing for Olympic qualification. Consequently, securing federation tenders becomes a pivotal growth lever for both established and challenger brands.

Expansion of School and Collegiate Sports Programs

The NCAA lists 1,053 men’s volleyball teams, while the National Christian College Athletic Association elevated the sport to championship status in 2024–25, generating measurable demand for entry-level balls, nets, and protective gear, according to the NCAA. In India, the Volleyball Federation achieved Centre of Excellence status for the Bengaluru Torpedoes Academy in March 2024, and the Khelo India budget increased to INR 1,000 crore (approximately USD 120 million) for the 2025–26 fiscal year, supporting court construction and coaching certifications, as per the Ministry of Youth Affairs and Sports. China’s national mandate for 4.6 million sports venues highlights institutional investment in multipurpose halls that often include volleyball courts. Schools typically refresh equipment every two to three years, creating annuity-style revenue streams for certified suppliers. Early exposure fosters brand loyalty, as alumni often choose the same gear for recreational or club play, thereby extending customer lifetime value well beyond the scholastic market.

Smart, Sensor-Enabled Equipment Adoption

Sensor-embedded balls are transforming formerly qualitative coaching into quantitative, data-driven instruction by capturing serve speed, spin rate, and impact load[3]Source: IEEE, “Sensor Technology in Sports Equipment,” ieeexplore.ieee.org. In the United States, Division I programs increasingly deploy AI-enabled tracking cameras that require balls engineered with precise surface-reflectivity parameters to ensure stable optical readings, driving demand for tightly specified match balls. Wilson’s 2024 Impact Report highlights lifecycle-assessment protocols that integrate data analytics with sustainability objectives, indicating that “design for data” and “design for environment” are converging in next-generation equipment. Bundled offerings that pair hardware with cloud-based analytics are enabling recurring subscription revenues and creating proprietary ecosystems similar to the razor-and-blade model used in wearables. As hardware prices fall, adoption is expected to expand to mid-tier colleges and aspirational clubs, accelerating a technology flywheel that rewards early movers with scalable software platforms.

Sustainable Material Innovation in Balls and Nets

Covestro’s bio-based TPU blends cut petrochemical use while still meeting FIVB rebound standards, helping manufacturers hedge against volatile PVC prices and comply with EU ESG requirements. Mikasa’s BV550C beach ball, featuring recycled nylon, showcased this shift when it debuted at the Paris 2024 Olympics. EU policy is accelerating the adoption of circular design: the Ecodesign Regulation 2024/1781 bans landfilling unsold footwear and apparel from July 2026, prompting brands to adopt circular design[4]Source: European Commission, “Ecodesign Regulation 2024/1781,” europa.eu. ISO 14001 certification and third-party lifecycle assessments increasingly shape European tenders, making sustainability a procurement prerequisite rather than a branding tool. Early movers that integrate recyclable polymers and launch take-back programs are gaining preferential access to school, municipal, and other public-sector contracts governed by green mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of professional-grade balls | -0.5% | Global; acute in Latin America, Africa, South Asia | Short term (≤2 years) |

| Inconsistent standards across leagues and regions | -0.4% | Global; highest fragmentation in Asia-Pacific, Latin America | Medium term (2-4 years) |

| High maintenance and installation costs of courts | -0.6% | Emerging markets in Africa, South Asia, Latin America | Long term (≥4 years) |

| PU/PVC price volatility and tightening ESG regulation | -0.7% | Global; regulatory pressure greatest in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Professional-Grade Balls

Top-tier leather balls from Mikasa, Molten, and Baden retail for USD 85–150, placing them out of reach for many schools in South Asia and sub-Saharan Africa, according to Baden Sports Canada. India’s September 2025 GST reduction to 5% helps ease pricing but does not offset the high cost of imported synthetic-leather inputs used by factories in Jalandhar and Meerut. As a result, budget-strained programs rely on USD 20–30 PVC balls that degrade quickly, limiting skill development but creating steady replacement demand. Manufacturers that introduce thermoplastic-elastomer composite balls in the USD 40–60 range can tap institutions seeking durability at accessible prices. Narrowing this affordability gap is essential for expanding participation and sustaining long-term market growth.

Inconsistent Standards Across Leagues and Regions

The FIVB, NCAA, and major national federations enforce differing ball dimensions, pressure levels, and color requirements, prompting manufacturers to engage in costly short-run production. Smaller brands struggle to fund multiple homologation fees, which can exceed USD 50,000 per model. Clubs in emerging markets often purchase non-compliant balls unknowingly, only to face replacement costs when their equipment fails to meet tournament certification standards. These fragmented standards increase SKU complexity, inflate logistics burdens, and compress supplier margins. A unified global specification could streamline manufacturing and unlock economies of scale, but until then, compliance friction will remain a structural drag on the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Volleyballs Anchor Revenue, Training Equipment Accelerates

Volleyballs accounted for 44.53% of revenue in 2025, highlighting their essential role at every level of play. Nets and posts follow, supported by institutional upgrades from aging steel systems to corrosion-resistant carbon-fiber designs, such as Senoh’s DE53 poles priced above USD 1,000. The training equipment segment is the fastest-growing, projected to grow at a 6.75% CAGR through 2031, driven by sensor-enabled balls and AI video trackers that enhance coaching programs. Protective gear is benefiting from increased injury-prevention awareness, particularly among female athletes, who have higher rates of ACL injuries. Footwear remains highly competitive, with Nike’s Zoom Hyperset 2 at USD 135 targeting elite players and the USD 75 HyperQuick appealing to budget-conscious buyers.

Bundled procurement is gaining traction: Baden’s Champions set, which combines a ball, net, posts, and lines for USD 239.99, is popular among community clubs that lack sourcing expertise, according to Baden Sports Canada. Training equipment software add-ons, such as IMU sensor recalibration subscriptions, generate recurring revenue. While footwear and braces have lower margins than balls, they drive brand loyalty and cross-selling opportunities. Suppliers that balance high-margin core items with complementary ecosystem offerings strengthen customer retention and expand the overall volleyball equipment market.

By Volleyball Type: Indoor Dominates, Beach Gains Momentum

Indoor volleyball accounted for 61.02% of equipment sales in 2025, driven by scholastic leagues and professional franchises that rely on hardwood courts and leather- or composite balls engineered for controlled rebound, according to the International Volleyball Federation (FIVB). Beach volleyball, supported by an increase in participating teams and rising prize pools, is projected to grow at a 5.93% CAGR through 2031. Equipment specifications differ: beach balls feature softer, water-resistant covers and lower internal pressure, while posts require rust-proof coatings to withstand outdoor conditions.

Growth in beach formats is shifting demand toward portable, weather-resistant kits, such as Senoh’s DE5000 pole set, which includes anodized tubing and sand anchors priced at USD 395. Junior beach events hosted by the Qatar Foundation illustrate geographic expansion beyond traditional North American and European markets. Brands offering modular systems that accommodate indoor, beach, and even snow volleyball will appeal to multipurpose facilities aiming to maximize asset utilization.

By End-User: Individual Players Lead, Institutions Accelerate

Individual players accounted for 71.88% of volleyball equipment revenue in 2025, driven largely by backyard sets and recreational balls priced between USD 20 and USD 40. Institutional buyers, including schools, colleges, and clubs, are expected to outpace overall market growth at a 6.42% CAGR, supported by government grants such as India’s INR 1,000 crore Khelo India program and FIVB’s Volleyball Empowerment Fund. Institutions typically replace match balls each season to meet homologation standards, creating predictable reorder cycles.

Individual consumers remain highly price-sensitive with lower brand loyalty, yet aspirational players increasingly seek NFHS-approved composite balls in the USD 50-70 range, presenting mid-tier growth opportunities for brands that combine quality with affordability. In the United States, club volleyball blurs the line between individual and institutional demand, as parent-organized teams make bulk purchases through direct-to-consumer channels. Volume-based discounts and customization options, including logos and color choices, enhance supplier positioning in this hybrid segment.

By Distribution Channel: Offline Holds Share, Online Surges

Offline retailers accounted for 66.95% of volleyball equipment revenue in 2025, reflecting the tactile nature of ball evaluation and the logistical efficiency of bulk-order fulfillment for schools. Online channels, however, are growing at a 7.32% CAGR, supported by an increase in sports-equipment e-commerce traffic. While desktops still dominate conversions for complex purchases, mobile devices now account for 63% of browsing traffic, indicating that product discovery is increasingly beginning on handheld screens.

Brands are adopting omnichannel strategies: Wilson and Baden operate proprietary e-commerce sites while maintaining partnerships with Dick’s Sporting Goods and Decathlon for in-store trials. Paid search accounts for 56.5% of online traffic, underscoring the importance of SEO and sponsored listings. Subscription models, such as quarterly ball shipments and annual net replacements, reduce churn and stabilize revenue, creating a defensible advantage against price-driven competitors.

Geography Analysis

The Asia-Pacific region held the largest regional share at 35.44% of volleyball equipment revenue in 2025, supported by China’s 4.07 billion square meters of sports facilities and government mandates promoting broader physical activity. India is the fastest-growing sub-market, driven by Khelo India budget increases, GST reductions on sports goods, and FIVB-certified academies, which collectively boost demand for certified balls and portable net systems. Japan’s SV.League rebrand presents a mixed outlook: rising professional standards drive premium equipment sales, while demographic headwinds cause youth participation to decline.

The Middle East and Africa are projected to record the fastest CAGR at 7.05% through 2031, spurred by Qatar hosting major tournaments and the UAE’s 2025 Unified Volleyball World Cup victory. The FIVB’s USD 47 million global investment channel provides equipment grants to emerging federations; however, the fragmented distribution and price sensitivity require hybrid approaches that combine local wholesalers with direct-to-consumer e-commerce. North America and Europe, though mature, sustain steady replacement cycles, with the NCAA’s 1,053 men’s teams alone ensuring seasonal reorders of FIVB-approved balls, and EU green procurement rules favoring ISO 14001-certified suppliers.

Latin America remains underpenetrated. Brazilian federal spending on sports and leisure is well below previous levels, limiting public-sector purchases, while Argentina’s Liga ACLAV relies on club funding rather than centralized procurement, fragmenting demand and raising per-unit logistics costs. Nevertheless, WHO data indicate the region has one of the highest shares of inactive adults globally, suggesting latent growth potential if affordability improves and grassroots programs expand. Challenger brands using direct-to-consumer channels are well-positioned to bypass inefficient retail networks and capture this untapped demand.

Competitive Landscape

The volleyball equipment market remains moderately fragmented, led by Mikasa, Molten, Wilson, Tachikara, and Spalding. Mikasa leverages Olympic sponsorships and the Beach Pro Tour to secure premium visibility, while Molten’s FLISTATEC technology reinforces its presence across NCAA championships. Senoh, via exclusive North American partner Sports Imports, captures over 90% of FIVB-approved net systems in U.S. collegiate programs, demonstrating a near-monopolistic niche.

Consolidation pressure is rising: RIP-IT Sports acquired Tachikara in January 2024, gaining a Japan-to-North America supply chain that reduces per-unit freight and homologation costs. White-space opportunities focus on sustainable materials, sensor integration, and distribution agility. Wilson’s 2024 lifecycle-assessment report highlights transparent ESG metrics, increasingly required for European tenders, while Covestro’s bio-based TPU offers upstream material differentiation.

Challenger brands increased their market share between 2019 and 2024 by adopting digital-first, direct-to-consumer strategies that undercut incumbents on price. Legacy companies are responding with augmented-reality product previews and AI sizing tools to replicate in-store experiences online. Modular smart-equipment ecosystems, combining hardware and software subscriptions, generate recurring revenue and raise switching costs, positioning early adopters for outsized gains as sensor technology becomes more affordable.

Volleyball Equipment Industry Leaders

Mikasa Corporation.

Spalding Sports Equipment.

Tachikara Holdings, Ltd.

Wilson Sporting Goods Co.

Molten Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mikasa was appointed as the official ball supplier for AVC events in 2025 and 2026, providing high-quality balls for key tournaments including the AVC Champions League and Nations Cup across Asia. The partnership, supported by Volleyball World, continues Mikasa’s long-standing involvement in international volleyball competitions.

- June 2024: Mikasa Corporation announced a multi-year partnership with League One Volleyball (LOVB) Pro, supplying official match balls for the new professional women's league launching in 2025. The deal extends Mikasa's dominance in North American professional volleyball and provides brand visibility among the league's target audience of collegiate and recreational players.

- April 2024: Mikasa has released the Paris 2024 Olympic volleyball line, which includes the BV550C beach ball featuring a recycled nylon cover, in alignment with the International Olympic Committee's sustainability mandates. The product launch positions Mikasa as a leader in eco-friendly equipment, creating a halo effect for its broader product portfolio.

- January 2024: RIP-IT Sports acquired Tachikara Holdings, consolidating two mid-tier brands and gaining access to Tachikara's distribution network in Japan and North America. The acquisition signals consolidation pressure in a fragmented market, as smaller brands lack the scale to navigate FIVB homologation processes and multi-region distribution.

Global Volleyball Equipment Market Report Scope

Essentially, volleyball is a game played with a net and a ball in the open air. Equipment includes balls, shoes, protective equipment such as knee pads and elbow pads, as well as nets and courts, bags and posts, and cables. The global volleyball equipment market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into balls, shoes, protective gear, and others. By volleyball type, the market is segmented into indoor volleyball and outdoor Volleyball. By end-user, the market is segmented into institutional users and personal users. Based on the distribution channel, the market studied is segmented into offline stores and online stores. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| Volleyballs |

| Nets and Posts |

| Shoes |

| Protective Gear |

| Training Equipment and Accessories |

| Indoor Volleyball |

| Beach Volleyball |

| Institutional (School, Colleges, Sports Clubs, and more) |

| Individual Players |

| Offline Channels |

| Online Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Neatherlands | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Thailand | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Qatar | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Volleyballs | |

| Nets and Posts | ||

| Shoes | ||

| Protective Gear | ||

| Training Equipment and Accessories | ||

| By Volleyball Type | Indoor Volleyball | |

| Beach Volleyball | ||

| By End-User | Institutional (School, Colleges, Sports Clubs, and more) | |

| Individual Players | ||

| By Distribution Channel | Offline Channels | |

| Online Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Neatherlands | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Thailand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Qatar | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the volleyball equipment market in 2026?

It was valued at USD 3.89 billion in 2026 and is forecast to hit USD 5.08 billion by 2031.

Which product category dominates current sales?

Volleyballs lead with 44.53% of global revenue, although training accessories are growing fastest at 6.75% CAGR.

Which region is expanding quickest?

The Middle East and Africa region is projected for a 7.05% CAGR through 2031, the highest among all geographies.

Who are the main ball suppliers?

Mikasa and Molten top the list, backed by FIVB and NCAA official-ball contracts that secure premium visibility.

What sustainability regulations impact manufacturers most?

The EU’s Ecodesign Regulation 2024/1781 bans disposal of unsold goods from July 2026 and, together with CSRD reporting rules, is pushing suppliers toward recycled and bio-based materials.

Page last updated on: