Ice Skating Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 2.9 Billion |

| Market Size (2030) | USD 3.76 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

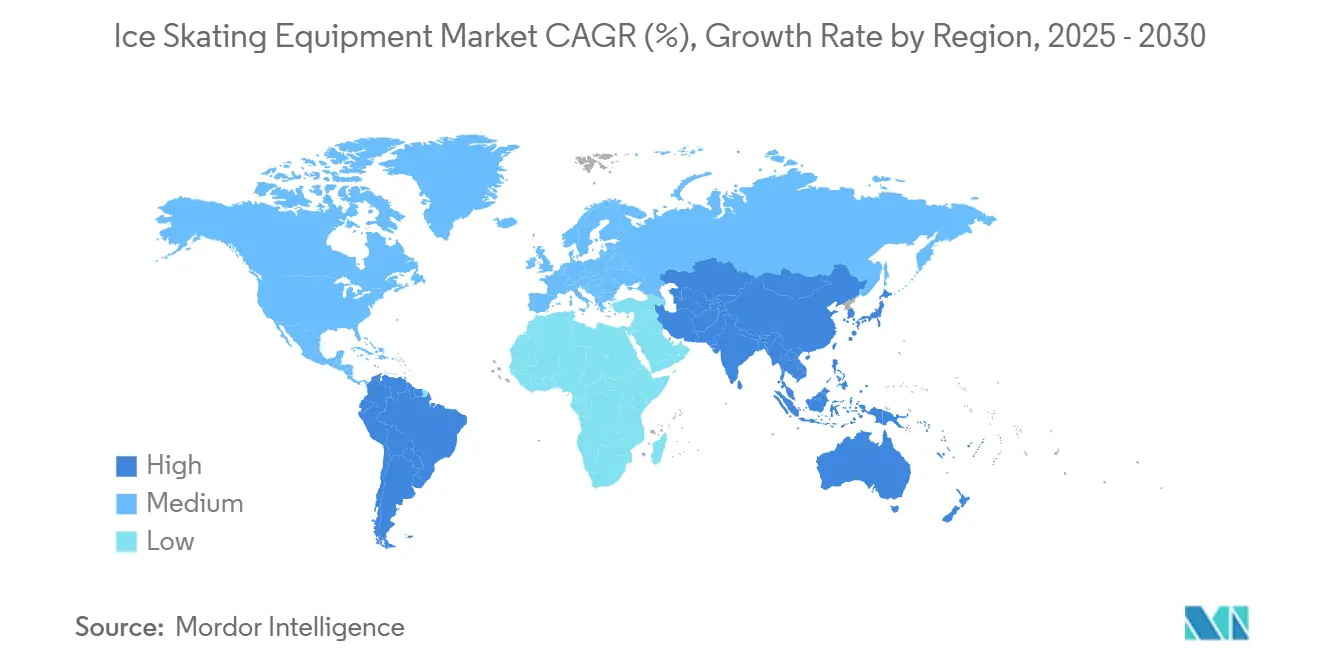

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ice Skating Equipment Market Analysis by Mordor Intelligence

The ice skating equipment market size is estimated to be USD 2.90 billion in 2025 and will advance to USD 3.76 billion by 2030 at a 5.34% CAGR, underscoring the category’s resilience and steady appeal. Heightened participation in winter sports, sustained technological innovation, and rising investment in modern rinks are laying the groundwork for enduring demand across skates, protective gear, and accessories. Moreover, North America remains the revenue anchor, yet Asia-Pacific’s aggressive facility build-out and policy support are shifting the center of gravity of the ice skating equipment market toward the East. Product upgrades, especially lighter composite skates and data-driven protective gear, are raising replacement frequency and margins. Meanwhile, stricter youth safety mandates are enlarging the protective-gear opportunity even faster than core skate demand, creating a two-speed growth dynamic that benefits full-line suppliers.

Key Report Takeaways

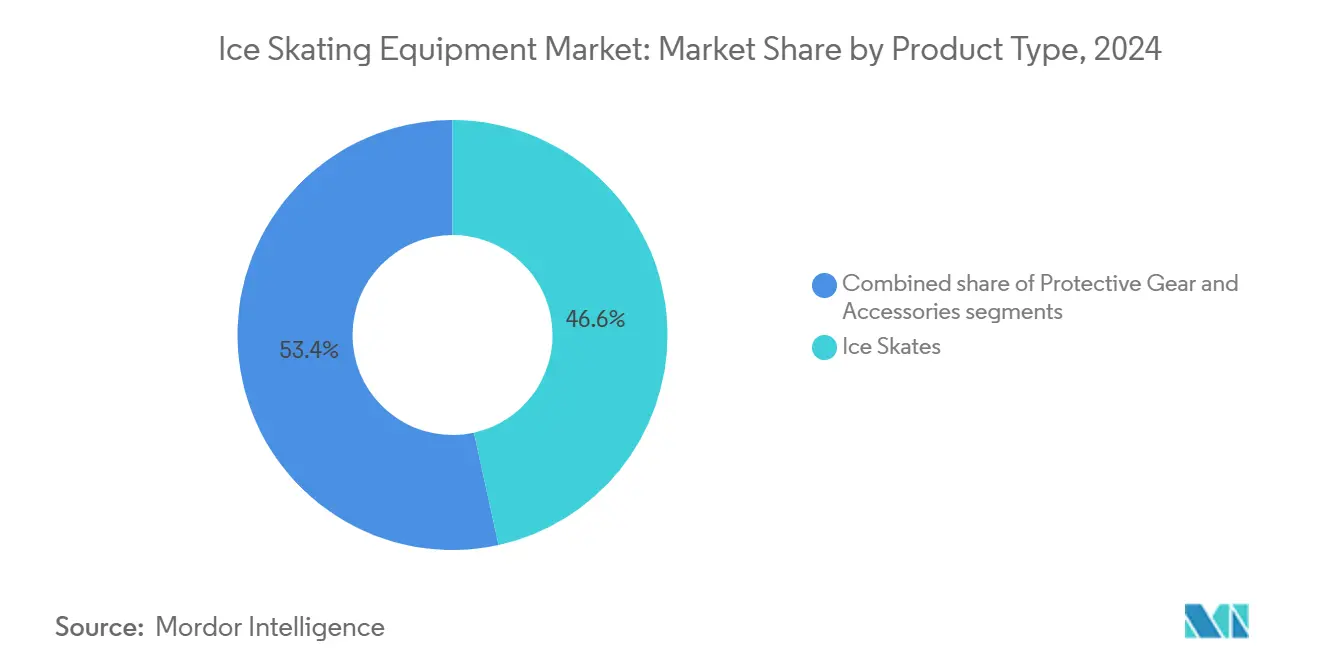

- By product type, ice skates led with 46.57% revenue share in 2024, while protective gear is projected to register a 6.43% CAGR through 2030.

- By sports type, ice hockey commanded 72.35% of 2024 sales, whereas figure skating is on track for the fastest 7.04% CAGR to 2030.

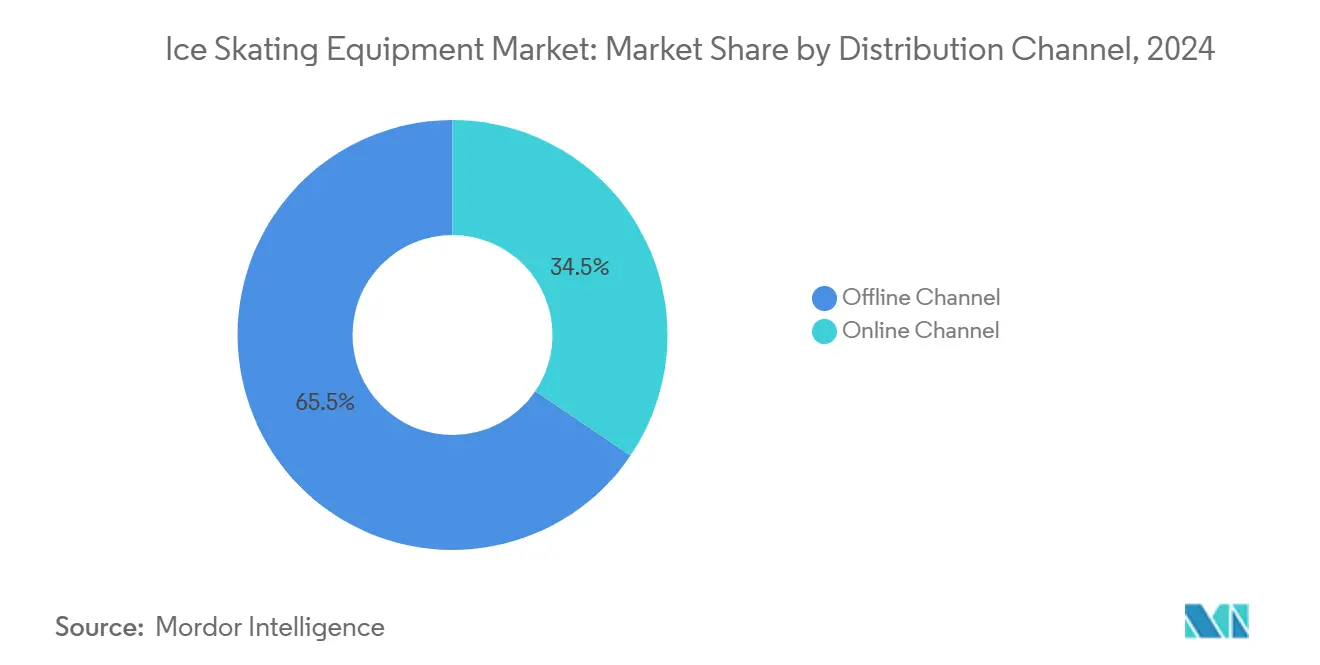

- By distribution channel, offline channels captured 65.53% of 2024 turnover, yet online channels are set to expand at a 6.70 % CAGR during 2025-2030.

- By end-user, personal users accounted for 84.61% of demand in 2024, while commercial users are forecast to post a 7.23% CAGR through 2030.

- By geography, North America contributed 42.89% of 2024 revenue, but Asia-Pacific is expected to deliver the quickest 6.27% CAGR to 2030.

Global Ice Skating Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of winter sports | +1.2% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Olympic and professional league visibility boosts aspirational demand | +0.9% | Global, concentrated in Olympic host regions and major hockey markets | Short term (≤ 2 years) |

| Expanding technological innovation | +1.1% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Surging indoor ice skating facilities | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Medium term (2-4 years) |

| Rising health and fitness awareness | +0.7% | Global, particularly strong in developed markets | Long term (≥ 4 years) |

| Demand for sustainability and eco-friendly materials | +0.6% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of winter sports

Winter sports participation continues to expand across traditional and emerging markets, supported by government initiatives for infrastructure development and public engagement. The Philippines women's ice hockey team's silver medal at the 2024 IIHF Women's Asia & Oceania Cup demonstrates the growing adoption of ice sports in tropical regions. The planned Women's Hockey Philippines League indicates further market development potential. This expansion creates opportunities for equipment manufacturers, particularly in regions with limited local production capabilities. The market growth extends beyond hockey, as figure skating gains popularity through learn-to-skate programs that drive equipment sales. China exemplifies this market evolution, with over 313 million people (22% of the population) participating in ice and snow activities by April 2024, following the Beijing 2022 Winter Olympics. The country's winter sports infrastructure grew to 2,847 venues by the end of 2023, representing a 16.1% increase from the previous year, including facilities in southern regions [1]Source: The State Council of the People’s Republic of China, "Xi Jinping's vision drives China's winter sports boom", english.www.gov.cn . This development pattern indicates a broader global shift in ice sport adoption beyond traditional cold-climate regions, supporting sustained growth in equipment demand through increased participation, infrastructure development, and consumer demand.

Olympic and professional league visibility boosts aspirational demand

Sporting events, such as the 2025 Asian Winter Games in Harbin, play a pivotal role in driving demand for ice skating equipment by enhancing regional market exposure and brand visibility. These events attract significant attention, acting as catalysts for increased public interest and participation in winter sports. The multiyear sponsorship renewal between CCM Hockey and 200x85, along with the 200x85 CCM World Invite tournament featuring over 500 teams, demonstrates the substantial influence of professional leagues, impacting over 80,000 athletes and 4,000 teams annually. Recreational athletes often emulate elite players, fueling demand for premium products and contributing to higher-margin sales for manufacturers. In figure skating, Olympic athletes' equipment preferences directly shape consumer purchasing decisions, further driving growth in the premium segment. Additionally, professional visibility accelerates the adoption of advanced technologies in ice skating equipment. Innovations introduced in elite competitions quickly permeate recreational markets through athlete endorsements and strategic brand marketing. Venues like the renovated Harbin Ice Hockey Arena, hosting the 2025 Asian Winter Games, emphasize technological integration and operational excellence, providing ideal platforms to showcase cutting-edge equipment. This synergy between major competitions and equipment innovation supports market growth by stimulating aspirational consumer demand and expanding reach across diverse regions.

Expanding technological innovation

Manufacturers in the ice skating equipment market are driving innovation by incorporating advanced materials and design technologies to enhance performance and sustainability. For instance, groundbreaking ice skate blades made from high-impact polyamide reinforced with glass fibers deliver a 40% speed improvement over traditional steel blades, reduce weight by 140 grams, and extend service life by three times longer. Bauer’s POWERFLY Holder exemplifies this trend with its stiff front post for efficient energy transfer and a flexible back post for lateral movement, paired with FLY-TI and FLY-X steel runners featuring hyperbolic geometry. Advanced helmet technologies now utilize AI-driven material optimization to lower the risk of traumatic axonal injuries by 5% to 65% under various impact conditions, addressing increasing safety concerns. Additionally, innovations such as heat-moldable technologies, synthetic ice surfaces, and custom-fit systems are creating premium product categories that enhance user experience and performance outcomes. These advancements not only improve equipment functionality but also attract consumers seeking personalized, high-performance, and sustainable gear. Consequently, technological advancements are a critical growth driver in the ice skating equipment market, as industry players leverage cutting-edge materials and designs to meet evolving athlete demands and safety standards.

Surging indoor ice skating facilities

The increasing development of indoor ice skating facilities is driving sustained demand for commercial-grade ice skating equipment, particularly in previously underserved regions. Projects such as Finland’s Kokkola Sports Park, which constructed two new practice ice rinks in 2023 with advanced energy recycling systems, underscore the industry's focus on sustainability. In North America, the Capitals Iceplex in Ballston is undergoing a renovation, and the Braemar Arena is undergoing an extensive expansion in 2024. Both initiatives include the addition of new indoor ice rinks and state-of-the-art cooling systems, reflecting a shift toward high-performance and eco-friendly sports infrastructure. This infrastructure growth is creating multi-year equipment procurement cycles, fostering stable, long-term supplier relationships. The demand for specialized commercial-grade products from these facilities differs significantly from consumer equipment, offering enhanced durability, superior performance features, and compliance with stringent operational standards. As facilities emphasize quality and sustainability, manufacturers are being driven to innovate and customize products to meet the rigorous demands of commercial operators. This trend is reinforcing the expansion of the global ice skating equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limitation due to seasonal and weather dependence | -0.8% | Northern temperate regions, particularly rural areas | Short term (≤ 2 years) |

| High cost of advanced equipment | -0.6% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Limited rink accessibility | -0.5% | Developing markets and rural regions globally | Long term (≥ 4 years) |

| Potential injury risk and safety concerns | -0.4% | Global, with regulatory focus in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limitation due to seasonal and weather dependence

Despite advancements in indoor facilities and synthetic ice alternatives, the global ice skating equipment market grapples with significant limitations due to seasonal and weather dependencies. In Canada, Hockey Canada’s National Arena Census reveals that 45% of rinks have outlived their life expectancy, leading to capacity constraints during peak winter months and limiting year-round access [2]Source: Hockey Canada, "So, how old are Canada's rinks?", hockeycanada.ca. Outdoor facilities face challenges from climate variability, impacting natural ice formation and causing unpredictable season length fluctuations. This issue intensifies in regions experiencing warming trends, shortening and destabilizing traditional outdoor skating seasons, and curtailing market expansion. Yet, technological innovations present hopeful solutions. For instance, the Ben Hotel’s outdoor ice rink in West Palm Beach employs advanced refrigeration systems with aluminum coils, ensuring ice quality even in warmer climates. Such advancements showcase technology's potential to broaden the geographic and seasonal scope of ice skating. Still, the persistent seasonality and weather reliance of outdoor ice sports hinder overall market growth. This underscores the urgent need for sustained investments in sustainable, climate-adaptive infrastructure and equipment.

High cost of advanced equipment

The high cost of advanced ice skating equipment remains a significant obstacle to market growth, particularly in emerging economies where limited purchasing power restricts adoption. Premium products, such as Bauer’s Konekt Goalie Skates, featuring a custom Fit Protocol and offering an additional 22 degrees of flex, are priced at levels that may deter price-sensitive consumers. This issue is compounded by the requirement for multiple equipment categories, including skates, protective gear, and accessories, which result in substantial initial investments for new entrants. Additionally, recurring expenses for equipment replacements create financial strain, especially for growing children who frequently need size adjustments and for competitive skaters requiring performance-optimized gear. To address these affordability challenges, manufacturers are expanding their product portfolios. For example, Jackson Ultima’s Softec Series focuses on comfort and durability while remaining accessible to cost-conscious buyers. Furthermore, financing options and rental programs are increasingly available, providing consumers with alternative ways to access quality equipment and reducing upfront cost barriers. These strategies are essential for expanding the customer base, driving participation, and sustaining growth in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ice Skates Lead Despite Protective Gear Acceleration

Ice skates hold a commanding 46.57% market share in 2024, highlighting their critical role as the primary equipment category. Protective gear, on the other hand, is the fastest-growing segment, registering a 6.43% CAGR through 2030. This growth is driven by evolving safety regulations and increased injury awareness. For example, the mandatory neck protection requirement for youth players under 18, effective August 1, 2024, has significantly boosted neck guard sales, following the United States Hockey mandate. Besides, advanced skate technologies continue to reinforce the category's dominance. Notable innovations include Aura Skates' SKY 200, which features aerospace-grade carbon fiber construction, weighs only 500 grams per skate, and incorporates a patented collar system for independent movement.

Accessories represent a stable yet mature segment, supported by consumable replacement cycles and advancements in blade materials and maintenance equipment. The development of high-impact polyamide blades, which deliver a 40% speed improvement and a service life three times longer, exemplifies how innovation in accessories can drive premium pricing and replacement frequency. Protective gear growth is further accelerated by high school hockey mandates requiring neck laceration protectors. This compliance-driven demand is expanding beyond traditional hockey markets into educational institutions.

By Sport Type: Hockey Dominance Faces Figure Skating Renaissance

In 2024, ice hockey holds a dominant 72.35% market share, driven by its well-established infrastructure and the visibility of professional leagues. In contrast, figure skating exhibits strong growth potential, with a 7.04% CAGR projected through 2030, supported by increased Olympic exposure and expanding recreational participation. The United States Figure Skating's partnership in 2024 with Jackson Ultima, an official supplier, highlights institutional support for the sport's development. This collaboration is expected to accelerate the standardization and improvement of equipment quality, benefiting both recreational and competitive skaters. Additionally, the 2026 U.S. Figure Skating Championships, serving as Olympic qualifiers, are creating aspirational demand cycles that influence equipment purchasing patterns among recreational skaters.

Hockey's market leadership reflects its deep cultural integration in key regions, extensive youth development programs, and professional league marketing, which drive equipment innovation and foster brand loyalty. For instance, CCM Hockey's 2024 partnership with 200x85, impacting over 80,000 young athletes annually, demonstrates the scale of youth hockey infrastructure sustaining equipment demand. Moreover, other sports categories, such as speed skating and recreational skating, are benefiting from facility expansion and health-conscious consumer trends. However, these remain niche segments with specialized equipment requirements that command premium pricing but face limited volume potential.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline channels maintain a 65.53% market share in 2024, highlighting the critical role of equipment fitting, professional consultations, and immediate product availability. In contrast, online channels are experiencing a 6.70% CAGR through 2030, driven by advancements in digital transformation and direct-to-consumer strategies. The complexity of ice skating equipment, particularly in skate fitting and blade selection, continues to favor physical retail environments. These environments offer professional expertise and try-before-purchase options, which digital channels struggle to replicate. However, manufacturers are addressing this gap through innovative solutions such as Bauer's MyBAUER platform, which delivers custom hockey equipment, including player sticks in 5 days and custom skates in 25 days.

Growth in online channels is supported by enhanced product information, virtual fitting technologies, and improved return policies that mitigate purchase risks for consumers. This growth trajectory is further propelled by younger demographics' preference for digital platforms and the convenience of comparing products and prices across multiple brands. Hybrid models, which combine online ordering with in-store fitting services, are emerging as a strategic approach. These models leverage the strengths of both channels while addressing traditional barriers to online equipment purchases.

By End Use Category: Personal Users Drive Volume While Commercial Accelerates

In 2024, personal users account for 84.61% of the market share, highlighting ice skating's recreational focus and extensive participation base. Commercial users, however, are experiencing the highest growth, with a 7.23% CAGR projected through 2030. This growth is driven by facility expansions and institutional procurement cycles. A notable example is Figure Skating in Harlem's planned NHL-sized rink in 2025, which is expected to generate an economic impact exceeding USD 70 million, create over 300 jobs, and require significant equipment procurement for programming and rental operations.

Ice skating participation remains strong, with over 200,000 New York City residents engaging in the activity between 2023 and 2024, according to Figure Skating in Harlem (FSH). This underscores the recreational market's scale and the potential for equipment replacement. Commercial users leverage bulk purchasing power and longer replacement cycles but demand higher-durability products, often at premium prices. This segment includes skating schools, rental services, and competitive programs, which drive consistent demand across multiple equipment categories. Additionally, these entities create opportunities for service-based revenue models, such as maintenance and customization services.

Geography Analysis

In 2024, North America holds a leading 42.89% share of the market, driven by its deeply rooted hockey culture and advanced facility infrastructure. Investments such as the NHL-sized rink planned by Figure Skating in Harlem, expected to deliver significant economic benefits in 2025, reflect the region's ongoing commitment to enhancing ice sports infrastructure. Well-established supply chains, strategic marketing by professional leagues, and youth development initiatives sustain consistent demand for equipment across diverse consumer segments. Additionally, regulatory requirements, including mandatory neck protection for youth hockey players, create opportunities for compliance-driven protective gear. Public health data from Canada, which recorded 4,715 ice skating injuries between 2016 and 2024, with 35% involving safety equipment, highlights the critical role of proper gear [3]Source: Government of Canada, "Injuries from winter sports and activities", health-infobase.canada.ca. This focus on safety drives demand for advanced protective products, further contributing to the market's growth.

The Asia-Pacific region is positioned as the fastest-growing market, with a projected 6.27% CAGR through 2030. China's inclusion of the ice and snow economy in its 15th Five-Year Plan, targeting a CNY 1.5 trillion sector value by 2030, serves as a key growth driver. Government support for equipment upgrades through long-term special bonds aligns with this strategic vision. The 2025 Asian Winter Games in Harbin are expected to accelerate regional development, with upgrades to 16 sports facilities and the launch of the world’s largest indoor ski center in Shenzhen. Beyond China, the Philippines women's ice hockey team is achieving international success despite infrastructure challenges, while Japan and South Korea continue to modernize facilities to accommodate rising participation rates. These developments are driving demand for advanced ice skating equipment and strengthening the region’s role in the global market.

Europe maintains steady growth, supported by the Nordic countries’ strong winter sports heritage and a focus on sustainable facility development. Initiatives such as Finland’s Kokkola Sports Park, featuring energy recycling systems, and Norway’s Maier Arena outdoor rink, which fosters community engagement, exemplify this commitment. The region’s emphasis on environmental responsibility aligns with manufacturers’ sustainability initiatives, creating favorable conditions for eco-friendly equipment and synthetic ice solutions. Meanwhile, South America, and Middle East and Africa remain emerging markets with limited penetration but increasing urban interest in ice sports. Climate-controlled facilities in these regions enable consistent, year-round participation regardless of weather conditions. These areas represent promising long-term growth opportunities, contributing to the diversification and expansion of the market.

Competitive Landscape

Recent mergers and acquisitions, including Altor Fund VI's majority stake purchase of CCM Hockey in October 2024, have intensified the consolidation trend in the global ice skating equipment market. Leading companies, including Bauer with its POWERFLY Holder system and advanced steel runners, are leveraging technology differentiation and vertical integration to strengthen their control over manufacturing and distribution. These established brands benefit from strong consumer loyalty, driven by endorsements from professional athletes that significantly influence purchasing decisions. Substantial investments in research and development further enhance their competitive edge in materials science and performance engineering, reinforcing their market dominance.

Strategic alliances with governing bodies and youth development organizations are critical to maintaining competitive advantages. In October 2024, CCM Hockey renewed its multiyear partnership with 200x85, which engages over 80,000 athletes annually, and Jackson Ultima secured an official supplier agreement with U.S. Figure Skating, underscoring how such partnerships create durable competitive barriers. These collaborations secure early-stage consumer relationships, ensure consistent demand pipelines, and promote brand visibility across grassroots and professional circuits. Sustaining these connections is essential for long-term strategic positioning and brand recognition.

Emerging players are disrupting the market by targeting niche segments, such as synthetic ice solutions and advanced materials. Companies like Glice lead in eco-friendly synthetic ice alternatives, while Aura Skates appeals to performance-driven consumers with aerospace-grade carbon fiber construction. Additionally, the International Skating Union's recent decision to permit manufacturers' logos on costumes and skates introduces new marketing and branding opportunities. This regulatory change is expected to reshape competitive dynamics, offering innovative strategies for visibility and consumer engagement in the evolving ice skating equipment market.

Ice Skating Equipment Industry Leaders

-

Peak Achievement Athletics Inc.

-

CCM Hockey

-

Jackson Ultima Skates Inc.

-

Graf Skates AG

-

Riedell Shoes, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Dsquared2 reissued its Skate boots in a limited edition. The boots, designated "Skate Moss" by consumers, transformed traditional ice skates into stiletto boots incorporating lace-up closures and metallic blade-like soles. The boots were available for pre-order on Dsquared2's website at USD 3,190.00.

- October 2024: CCM Hockey, a designer, manufacturer, and marketer of hockey equipment, established a multiyear partnership with 200×85, an organization focused on youth hockey development. Under this agreement, CCM would serve as the official equipment and apparel supplier for 200×85 and its elite girls' program, Premier Ice Prospects, covering all tournaments and development programs.

- July 2024: The Bauer Supreme Shadow Hockey Skates received significant market attention due to their emphasis on power and explosiveness. The manufacturer developed the skates to enhance energy transfer and responsiveness during play. The Supreme Shadow model incorporated a Carbon CONNECT Outsole that delivered 40% more stiffness than its predecessor, the SUPREME MACH skate.

Global Ice Skating Equipment Market Report Scope

| Ice Skates (e.g., figure skates, hockey skates, racing/speed skates, recreational skates) |

| Protective Gear (e.g., helmets, pads, gloves, jackets, pants) |

| Accessories (e.g., skate blades, blade guards, skate bags, skate sharpeners) |

| Figure Skating |

| Ice Hockey |

| Others |

| Offline Channels |

| Online Channels |

| Personal Users |

| Commercial Users |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Norway | |

| Finland | |

| Switzerland | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Ice Skates (e.g., figure skates, hockey skates, racing/speed skates, recreational skates) | |

| Protective Gear (e.g., helmets, pads, gloves, jackets, pants) | ||

| Accessories (e.g., skate blades, blade guards, skate bags, skate sharpeners) | ||

| By Sport Type | Figure Skating | |

| Ice Hockey | ||

| Others | ||

| By Distribution Channel | Offline Channels | |

| Online Channels | ||

| By End Use Category | Personal Users | |

| Commercial Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Norway | ||

| Finland | ||

| Switzerland | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global ice skating equipment market in 2025?

The ice skating equipment market size is USD 2.90 billion in 2025.

Which region is expanding the fastest?

Asia-Pacific leads with a 6.27% CAGR, propelled by China’s policy push and new rink construction.

What product segment is forecast to grow most rapidly?

Protective gear will outpace other categories at a 6.43% CAGR to 2030 thanks to stricter safety mandates.

Why does commercial demand show higher growth than personal demand?

New multi-pad arenas and school programs are fueling bulk equipment procurement, lifting commercial segment CAGR to 7.23%.

Page last updated on: