Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.76 Billion |

| Market Size (2031) | USD 24.55 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

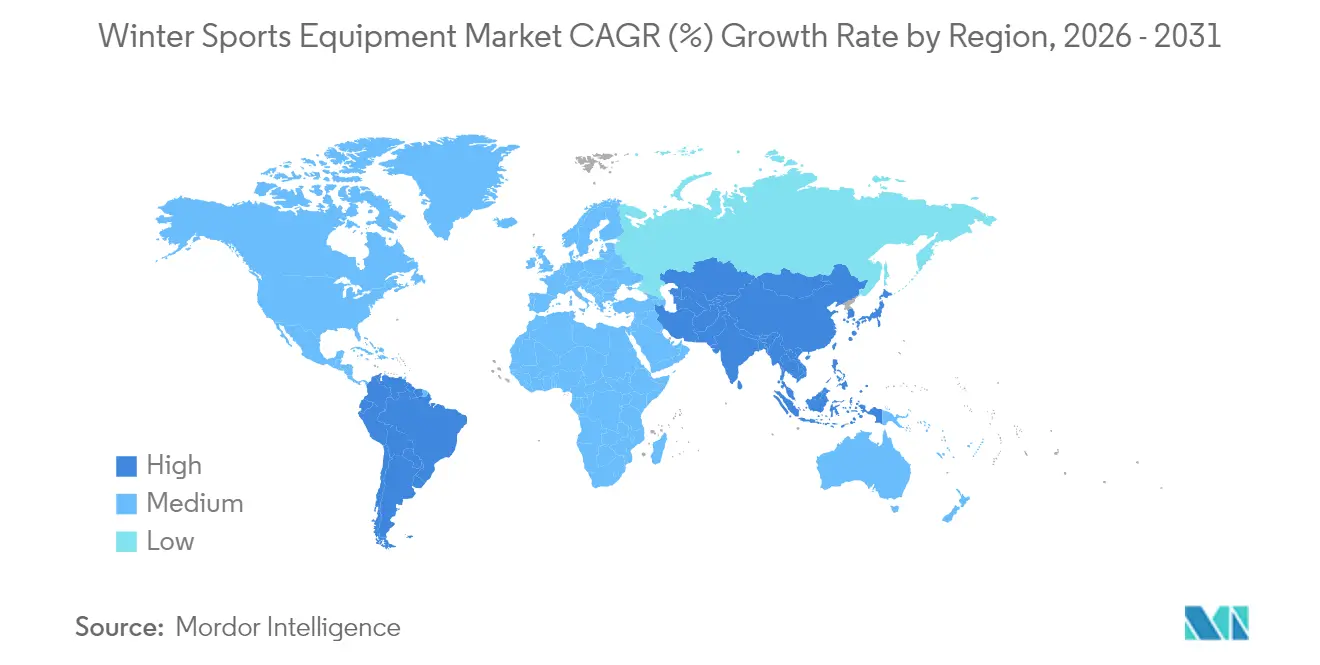

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Winter Sports Equipment Market Analysis by Mordor Intelligence

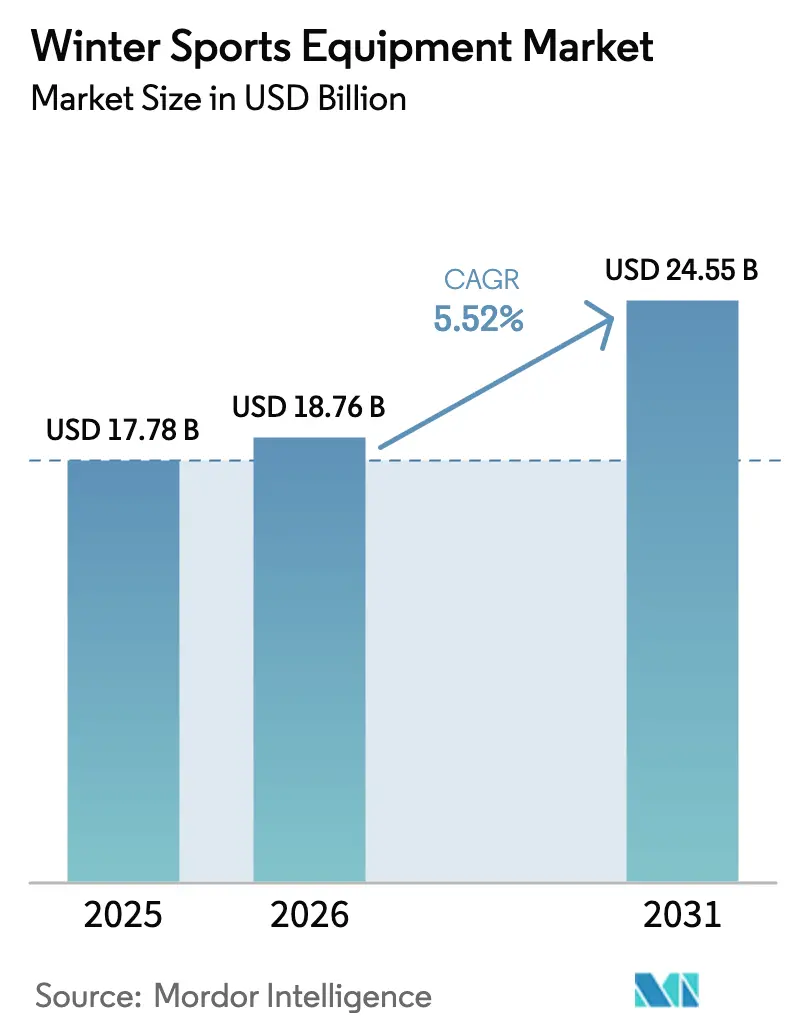

The winter sports equipment market size was valued at USD 17.78 billion in 2025 and estimated to grow from USD 18.76 billion in 2026 to reach USD 24.55 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). China's ice-and-snow economy initiative drives this growth, increased Asian participation following the Olympics, and consistent premium product demand in established markets. Technological advancements in equipment, including carbon-fiber composites and sensor-integrated textiles, contribute to higher average selling prices and enhanced performance capabilities. The market benefits from growing female participation and the shift of fitness enthusiasts toward outdoor activities, particularly boosting sales in apparel and safety equipment. However, market growth faces challenges from weather unpredictability, increasing resort fees, and entry barriers for beginners, leading to higher demand for rental services and second-hand equipment. The competitive landscape maintains equilibrium between large multinational companies with extensive research and development capabilities and specialized manufacturers serving specific segments like freestyle, backcountry, and environmentally conscious consumers.

Key Report Takeaways

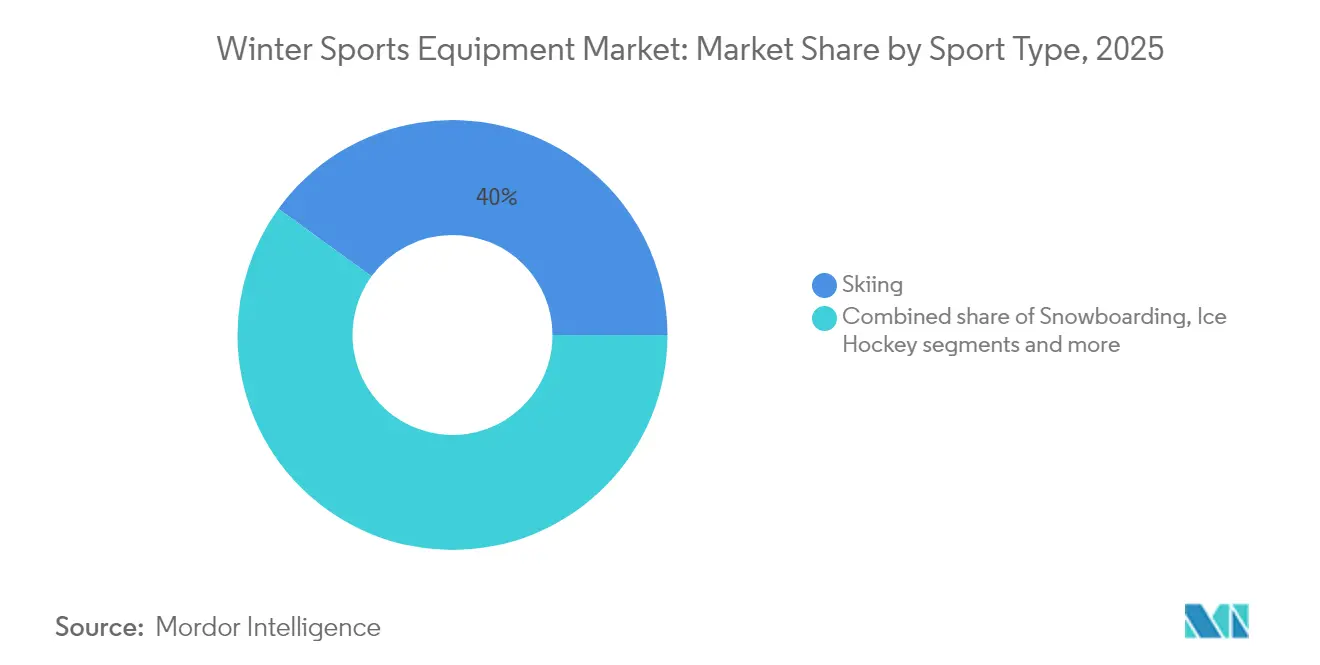

- By sports type, skiing led with 40.02% of the winter sports equipment market share in 2025; snowboarding is forecast to grow at a 6.05% CAGR between 2026-2031.

- By equipment category, skis and snowboards captured 42.10% of 2025 revenue, while apparel and accessories are set to expand at a 6.45% CAGR through 2031.

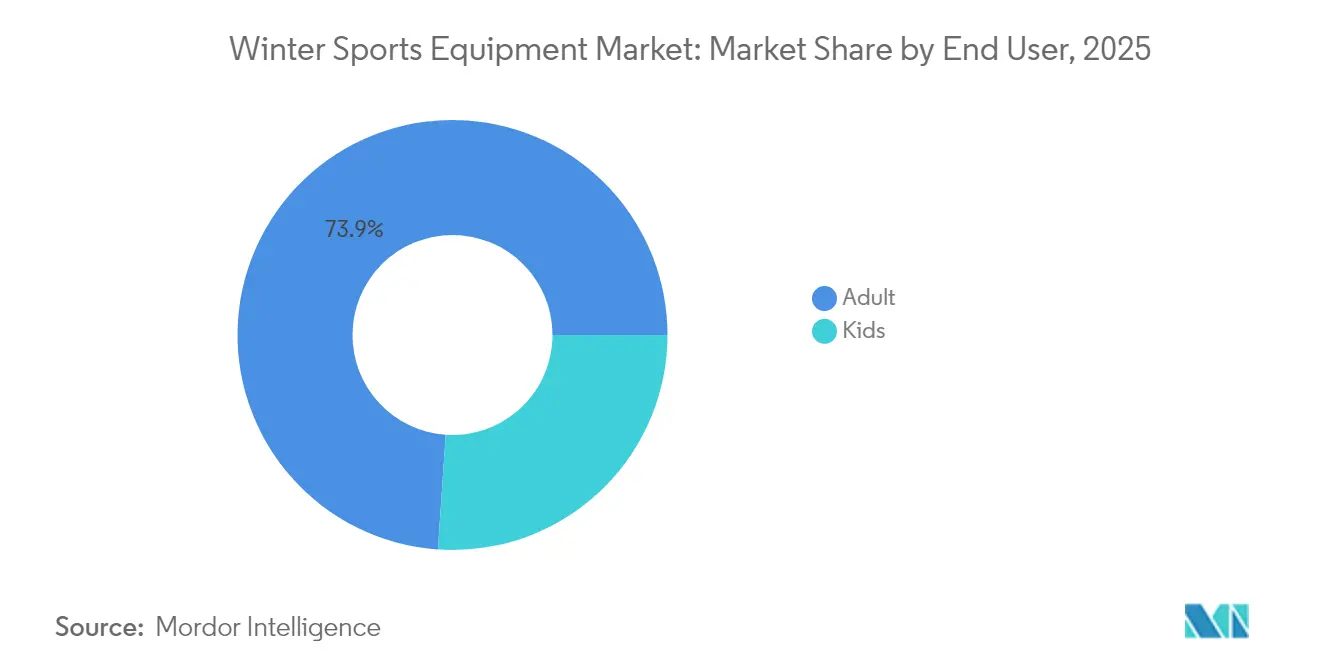

- By end user, adults accounted for 73.92% of the 2025 demand; the kids segment is poised for a 6.75% CAGR to 2031.

- By distribution channel, offline outlets held 68.90% share in 2025; online stores will post a 7.05% CAGR over the forecast period.

- By geography, North America commanded 36.10% of 2025 revenue, whereas Asia-Pacific is projected to lead growth with a 7.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Winter Sports Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Fitness Awareness | +1.0% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Influence of Winter Sports Events | +0.7% | APAC core, spill-over to global markets | Short term (≤ 2 years) |

| Technological Advancements in Equipment Production | +0.9% | Global, led by European manufacturing hubs | Long term (≥ 4 years) |

| Growing Popularity of Backcountry and Freestyle Disciplines | +0.6% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Expanding Winter Tourism and Infrastructure | +1.0% | APAC leading, followed by North America expansion | Long term (≥ 4 years) |

| Development of Sustainable and Eco-Friendly Winter Sports Equipment | +0.8% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Fitness Awareness

The growing focus on wellness is transforming winter sports participation patterns, as more people choose outdoor activities over traditional gym workouts for their physical and mental well-being. Consumers increasingly view winter sports equipment as long-term health investments, driving significant demand for premium gear across all categories. This shift particularly benefits the technical apparel and protective equipment segments, where advanced materials and ergonomic designs deliver superior performance and safety features. Equipment manufacturers are integrating sophisticated health monitoring capabilities into their products, with smart textiles and sensors becoming standard features across product lines. Additionally, the rising number of older participants seeking low-impact winter activities continues to drive innovation in comfort-oriented equipment, expanding the market for specialized gear designed for this demographic.

Influence of Winter Sports Events

Major winter sports events significantly influence global equipment demand patterns, creating sustained market opportunities across multiple regions. International brands strategically capitalize on this momentum, exemplified by Bogner's ambitious expansion plan to establish 80 retail stores in China within five years - a direct response to the growing equipment demand stimulated by Olympic exposure. The events' impact transcends geographical boundaries, with global broadcast coverage inspiring equipment purchases in emerging winter sports markets previously untapped. Equipment manufacturers carefully orchestrate product launches to coincide with major competitions, utilizing athlete endorsements and performance achievements to establish premium pricing for advanced technologies. These international competitions generate predictable demand cycles that manufacturers systematically integrate into their long-term production planning and inventory management frameworks, ensuring optimal market responsiveness.

Technological Advancements in Equipment Production

The widespread adoption of carbon fiber materials and AI-based modeling techniques has significantly reduced research and development timelines in the sports equipment industry. This technological advancement has enabled manufacturers to incorporate premium features, previously exclusive to professional athletes, into consumer products at accessible price points [1]Source: International Olympic Committee, “Carbon fiber tech trickles down,” olympics.com. Modern helmets and jackets now integrate smart textiles with sophisticated crash sensors and fall-alert systems, fundamentally transforming traditional safety gear into intelligent protection devices. In response to environmental concerns, companies are increasingly transitioning to recyclable composites in their manufacturing processes. Several European manufacturing facilities have implemented comprehensive product recycling programs, demonstrating a commitment to sustainable production practices.

Growing Popularity of Backcountry and Freestyle Disciplines

The backcountry skiing equipment market has grown significantly due to changes in winter sports participation patterns. The growth has expanded beyond traditional alpine segments into freestyle activities, as younger participants seek adventure through winter sports. According to the Canadian Avalanche Centre, this represents a long-term change in consumer behavior rather than a seasonal trend. Equipment manufacturers have responded by developing versatile gear that incorporates features from multiple disciplines, creating hybrid products for various skiing styles. The increased participation has also driven higher demand for safety equipment as users become more aware of backcountry risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment | –0.9% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Learning curve and skill barriers | –0.4% | Emerging APAC and developing regions | Medium term (2-4 years) |

| Competition from alternative recreation | –0.6% | North America and Europe | Medium term (2-4 years) |

| Seasonal and weather dependency | –1.2% | Global; latitude/elevation dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Fitness Equipment

The escalating costs of winter sports equipment significantly restrict participation among middle-class consumers, fundamentally altering market demographics. Increasing lift ticket prices at major resorts during peak seasons, combined with substantial equipment investments ranging from skis to protective gear, create insurmountable financial barriers to entry. Manufacturers face complex challenges in balancing advanced product development costs with market accessibility, particularly in introducing new technology and materials. While the strategic focus on affluent consumers enables premium product development and innovation, it simultaneously constrains overall market growth as price-sensitive consumers increasingly migrate to more affordable recreational alternatives. The equipment rental market continues to expand rapidly as consumers adopt cost-effective participation strategies, transforming traditional retail channels and forcing manufacturers to adapt their direct sales approaches.

Learning Curve and Skill Barriers

The winter sports market faces growth limitations due to participation barriers, particularly in emerging regions where participants lack family traditions or peer support. Equipment technology advancements create performance differences between entry-level and advanced products, which can discourage new participants. The need for professional instruction adds costs and scheduling difficulties, while backcountry activities require specialized safety training. Equipment manufacturers develop simplified products with safety features to address these barriers, though these modifications may reduce performance aspects valued by experienced users. These challenges are especially evident in the Asia-Pacific region, where winter sports are relatively new recreational activities rather than established traditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sports Type: Skiing Leads Despite Snowboarding Acceleration

Skiing commands 40.02% of the winter sports equipment market revenue in 2025, driven by extensive resort infrastructure, established training programs, and consistent participation across all age demographics. The skiing equipment segment continues its growth trajectory, supported by regular equipment replacement cycles every 3-5 years and technological advancements in material composition. The snowboarding segment, representing a smaller market share, demonstrates robust growth at 6.05% CAGR, fueled by expanding youth participation, significant investments in terrain park facilities, and rising adoption rates across Asian markets, particularly in Japan and South Korea.

The market exhibits significant fragmentation in participation patterns, with backcountry touring and cross-country skiing emerging as key components of the "others" category. These activities, alongside snowshoeing and winter hiking, experience increased popularity due to growing consumer focus on outdoor fitness and adventure sports. Manufacturers have responded by implementing dual-focus product development strategies, allocating resources between high-performance racing skis for competitive segments and versatile, all-terrain boards that accommodate both freestyle maneuvers and powder conditions in a single design.

By Equipment Category: Technical Innovation Drives Apparel Growth

In 2025, skis and snowboards made up 42.10% of total sales, buoyed by a demand for high-performance gear and a predictable replacement cycle of three to five years. Innovations like carbon fiber reinforcements, hybrid wood-foam cores, and rocker-camber profiles are captivating both seasoned athletes and casual users. Boots, bindings, and protective gear are witnessing steady volume growth, bolstered by safety regulations and features such as heat-moldable liners, BOA fit systems, and lightweight carbon composites. Furthermore, the shift towards sustainable materials, including bio-based resins and recycled components, is resonating with consumers' growing preference for eco-friendly performance gear.

Meanwhile, the apparel and accessories segment is on an upward trajectory, growing at a 6.45% CAGR. This growth is fueled by consumers' increasing adoption of performance outerwear—ranging from breathable shells to insulated layers—for both winter sports and daily urban activities. Brands are leveraging premium materials like stretch Gore-Tex, Primaloft, and antimicrobial fabrics, allowing them to offer high-margin products that prioritize function, durability, and comfort. The appeal of these products extends beyond the slopes, thanks to their year-round usability. Concurrently, companies are bolstering brand loyalty through circular initiatives, including recycling programs, repair services, and sustainable packaging.

By End User: Youth Development Programs Drive Kids Segment Growth

The adult segment dominates the market with a 73.92% share in 2025, driven by established purchasing power and regular equipment replacement cycles. The kids segment is projected to grow at a 6.75% CAGR through 2031, supported by youth development programs, family winter sports initiatives, and partnerships with educational institutions. This growth in youth participation ensures market sustainability, as children often continue winter sports into adulthood, providing consistent demand for equipment manufacturers.

Product development for young users focuses on safety, adjustable sizing, and cost-effective solutions to address growth phases and family budgets. Industry efforts to expand participation beyond traditional winter sports families include investments by ski resorts and equipment manufacturers in youth programs offering equipment access and training. In China, the growth in youth participation is particularly notable, with first-generation winter sports families prioritizing their children's equipment and activities.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline retail stores hold 68.90% of the market share in 2025, as winter sports equipment requires hands-on evaluation and professional fitting services for optimal performance. Online retail stores are expected to grow at a 7.05% CAGR through 2031, supported by enhanced product information, virtual fitting technologies, and manufacturers' direct-to-consumer initiatives. The distribution landscape continues to evolve while addressing the sector's requirements for expert consultation and technical support.

Retailers are adopting hybrid models that integrate online convenience with in-store expertise through omnichannel strategies. Major brands' direct-to-consumer programs affect traditional retail partnerships while creating opportunities for specialized retailers with superior service capabilities. China's developed e-commerce infrastructure particularly benefits this transformation, with online retail reach surpassing physical store coverage in emerging winter sports markets. Equipment manufacturers continue to develop digital sales capabilities while maintaining wholesale partnerships to ensure comprehensive market coverage and customer support.

Geography Analysis

North America maintains a commanding 36.10% market share in 2025, underpinned by decades of strategic winter sports infrastructure development and robust consumer spending on premium equipment. The region's projected 5.60% CAGR through 2031 reflects a mature market characterized by systematic equipment replacement cycles and adoption of advanced technologies. Alterra Mountain Company's substantial USD 300 million capital investment program reinforces market stability by enhancing resort accessibility, modernizing facilities, and elevating the overall visitor experience across multiple destinations.

The Asia-Pacific region dominates the market with a 7.30% CAGR, driven by China's target to establish a 1 trillion-yuan ice-and-snow economy by 2025. Government initiatives, Bogner's expansion of 80 new retail locations, and increased e-commerce adoption by new winter sports participants fuel this growth. The market expansion continues as more countries embrace winter sports. In January 2024, India's Ministry of Youth Affairs and Sports approved the country's participation in the 9th Asian Winter Games (AWG) 2025, scheduled for February 7-14 in Harbin, China .

The European winter sports market benefits from a strong sporting culture and ongoing technological advancements, along with sustainability initiatives that encourage equipment upgrades. The European Union's ski and snowboard production has shown growth, with Austria maintaining its position as the leading manufacturer and demonstrating robust export performance to markets outside the EU . Furthermore, Scandinavian nations are seeing a surge in backcountry and cross-country skiing participation, driving up demand for lightweight gear and specialized apparel.

Competitive Landscape

The winter sports equipment market demonstrates moderate consolidation, characterized by a dynamic competitive landscape where established multinational corporations compete with specialized manufacturers and regional players. Major companies such as Stockli Swiss Sports AG, Fischer Sports, Bauer Hockey, LLC, and Amer Sports maintain their market positions through extensive brand portfolios and robust global distribution networks. These companies navigate current market challenges through strategic partnerships, product diversification, and continuous innovation in their manufacturing processes.

Technology integration has emerged as a critical competitive differentiator in the market, with manufacturers making substantial investments in AI-driven materials research, smart textiles, and connected equipment capabilities. These technological advancements enable real-time performance monitoring and enhanced safety features, meeting the growing consumer demand for smart winter sports equipment. Companies that successfully balance innovation with manufacturing efficiency gain significant market advantages, particularly as premium features transition from differentiators to standard offerings across product lines.

The market presents significant growth opportunities across multiple segments, including sustainable product development, direct-to-consumer digital sales platforms, and expansion into emerging markets with first-time winter sports participants. Climate change impacts have reshaped market dynamics, creating advantages for companies developing weather-adaptable products and supporting infrastructure modifications. Organizations that demonstrate adaptability to changing weather patterns and invest in sustainable manufacturing practices position themselves favorably against competitors who remain dependent on traditional seasonal patterns and conventional production methods.

Winter Sports Equipment Industry Leaders

Stockli Swiss Sports AG

Bauer Hockey, LLC

Fischer Sports

Graf Skates AG

Amer Sports

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: J.Crew and U.S. Ski & Snowboard have established a strategic three-year partnership, positioning J.Crew as the organization's official lifestyle-apparel partner.

- February 2025: Bcomp partnered with Jones Snowboards to incorporate natural fiber composites into their snowboard designs. This collaboration advances the use of sustainable, high-performance materials in snowboard manufacturing.

- July 2024: WNDR Alpine strategically expanded its product portfolio by integrating skis, snowboards, and splitboards into a comprehensive outdoor equipment range, leveraging biotechnology innovations to enhance performance and sustainability across all seasons

Global Winter Sports Equipment Market Report Scope

The study scope covers the analysis of equipment used in different winter sports like ice skating, skiing, snowboarding, ice hockey, and others. The global winter sports equipment market is segmented by sports type, distribution channel, and geography. By sports type, the market is segmented into skiing, snowboarding, figure skating, ice hockey, and others. By distribution channel, the market is segmented into offline retail stores and online retail stores. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Sports Type

| Skiing |

| Snowboarding |

| Ice Hockey |

| Figure Skating |

| Other Sports Type |

By Equipment Category

| Skis and Snowboards |

| Boots and Bindings |

| Protective Gear and Helmets |

| Apparel and Accessories |

| Other Equipment Category |

By End User

| Adult |

| Kids |

By Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Sweden | |

| Norway | |

| Finland | |

| Switzerland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Sports Type | Skiing | |

| Snowboarding | ||

| Ice Hockey | ||

| Figure Skating | ||

| Other Sports Type | ||

| By Equipment Category | Skis and Snowboards | |

| Boots and Bindings | ||

| Protective Gear and Helmets | ||

| Apparel and Accessories | ||

| Other Equipment Category | ||

| By End User | Adult | |

| Kids | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Sweden | ||

| Norway | ||

| Finland | ||

| Switzerland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the winter sports equipment market?

The market is valued at USD 18.76 billion in 2026 and is projected to reach USD 24.55 billion by 2031.

Which sports type dominates sales?

Skiing leads with 40.02% of 2025 revenue, although snowboarding is growing the fastest at a 6.05% CAGR.

How is technology changing equipment design?

Carbon-fiber composites, AI-driven flex tuning, and embedded sensors are elevating performance while enabling real-time safety monitoring.

What are the main challenges facing manufacturers?

High retail prices, climate-induced season shortening, and competition from alternative leisure activities restrain mass-market expansion.

Which channel is growing quickest?

Online retail stores are advancing at a 7.05% CAGR as virtual fitting tools and direct-to-consumer models gain acceptance.

Page last updated on: