Table And Floor Lamps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.41 Billion |

| Market Size (2031) | USD 33.08 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

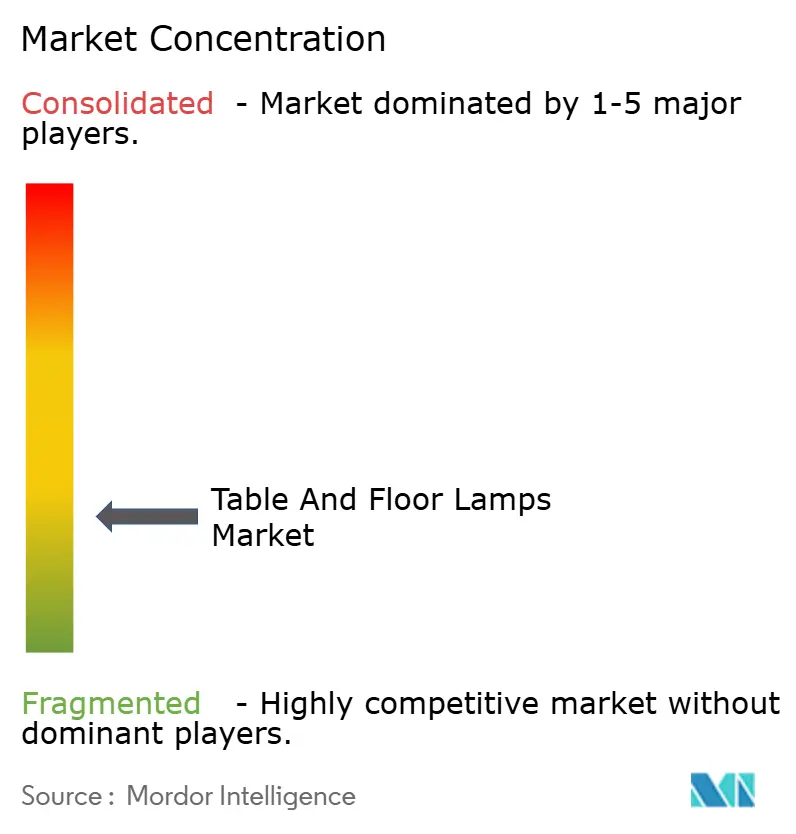

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Table And Floor Lamps Market Analysis by Mordor Intelligence

The table and floor lamps market size in 2026 is estimated at USD 26.41 billion, growing from 2025 value of USD 25.24 billion with 2031 projections showing USD 33.08 billion, growing at 4.62% CAGR over 2026-2031. Hybrid work patterns, hospitality refurb cycles, and the democratization of LED technology keep demand resilient, while connected fixtures capture a growing premium as they serve as vital endpoints in home-automation ecosystems. Manufacturers extend product lifecycles through firmware updates, recurring software services, and modular components that allow aesthetic refresh without full replacement. A parallel pricing squeeze persists: do-it-yourself furniture giants amplify private-label competition, and raw-material cost swings pressure margins, yet strong secondary LED replacement demand cushions revenue. The market balances premium margins for connectivity with margin pressure from DIY furniture private labels and raw-material volatility, yet stricter energy-efficiency mandates continue to favor advanced LED designs, evidenced by the U.S. Department of Energy’s 2024 lamp rule that boosts annual consumer savings and drives manufacturer compliance[1]Source: U.S. Department of Energy, “Energy conservation standards for general service lamps,” Federal Register, federalregister.gov.

Key Report Takeaways

- By product type, desk/task lamps led with 48.62% of the table and floor lamps market share in 2025, while floor lamps poised for the fastest 14.02% CAGR through 2031.

- By material, metal accounted for 35.78% revenue in 2025; wood is set to expand at 14.28% CAGR to 2031 in the table & floor lamps market.

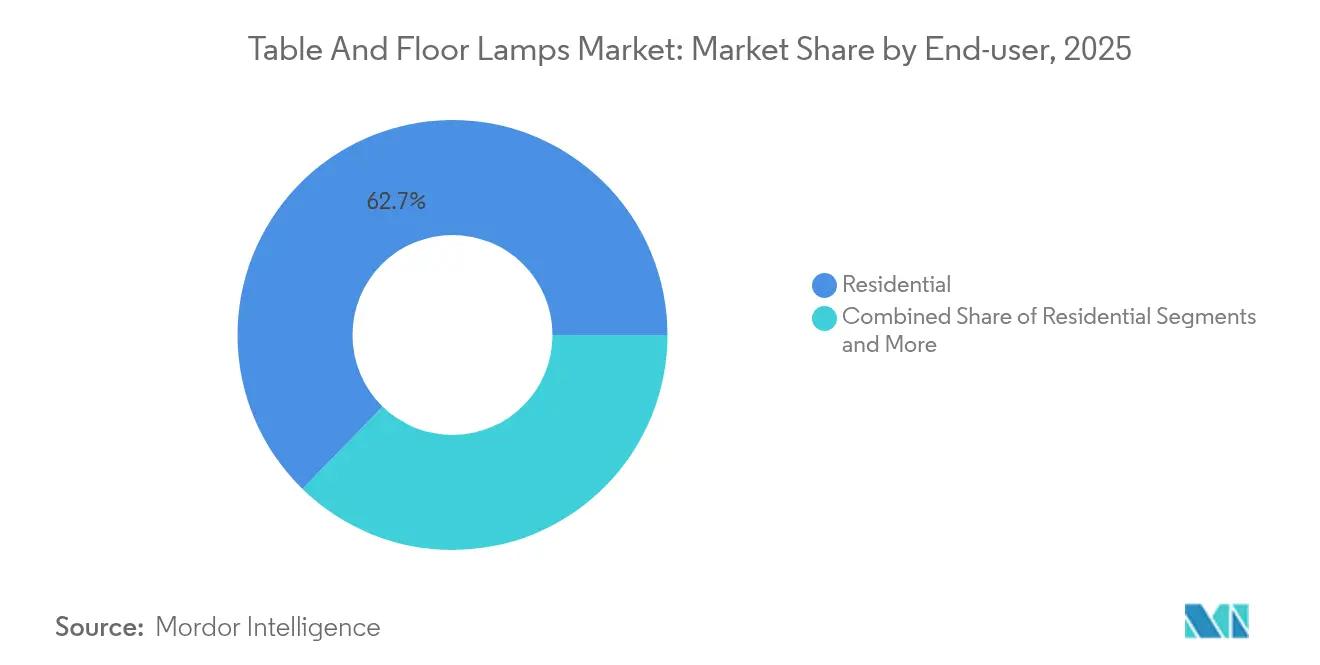

- By end user, the residential sector captured 62.71% of revenue in 2025 and is forecast to grow 13.92% to 2031 in the table & floor lamps market.

- By distribution, offline outlets held 40.62% revenue in 2025, whereas online sales will accelerate at 13.68% CAGR through 2031 in the table & floor lamps market.

- By geography, Asia-Pacific commanded 34.11% revenue in 2025; Middle East & Africa is the fastest-growing region at 9.21% CAGR.

- Top 5 player such as Signify (Philips Lighting), IKEA Group, Acuity Brands Lighting, FLOS, Artemide holds major market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Table And Floor Lamps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart-home ecosystems boosting connected lamps | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing penetration of LED-integrated decorative lamps | +0.8% | Global, accelerated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Rapid hotel-room refurb cycles in lifestyle and boutique segments | +0.6% | North America & EU hospitality markets, expanding to APAC | Medium term (2-4 years) |

| Workplace wellness programs embracing circadian-lighting task lamps | +0.4% | North America & EU corporate markets | Long term (≥ 4 years) |

| Surge in short-term rental hosts demanding statement lighting | +0.5% | Global urban centers, concentrated in North America & EU | Short term (≤ 2 years) |

| AI-driven design-to-manufacture platforms enabling micro-brands | +0.3% | Global, with technology hubs leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart-Home Ecosystems Boosting Connected Lamps

Connected fixtures stand at the forefront where illumination converges with IoT, transforming the table and floor lamps market from commodity décor pieces into interactive nodes that respond to voice, occupancy, and security cues. Consumers expect seamless pairing with voice assistants and mobile dashboards, making interoperability a baseline rather than a luxury. The value comes not just from switching or dimming but from color-temperature tuning that syncs to circadian rhythms, adaptive light levels informed by ambient sensors, and predictive usage analytics that conserve energy. These functions justify higher average selling prices and subscription revenues for cloud-based scene libraries and remote diagnostics, lifting margins while binding customers to brand ecosystems. The desk-lamp category benefits disproportionately, as knowledge workers demand granular control to reduce eye strain and extend productive focus windows. Brands now embed upgradeable wireless chips and open APIs to future-proof purchases, turning lamps into long-life platforms rather than disposable appliances.

Growing Penetration of LED-Integrated Decorative Lamps

LED maturity has erased the historical efficiency-price trade-off, pushing the table and floor lamps market toward unqualified LED standardization. LEDs cover 70% of global lamp sales, and the looming secondary replacement wave—5.8 billion units in 2024—sustains volume even as lifetimes lengthen. Miniaturized emitter footprints unleash daring shapes and ultra-thin profiles, while addressable RGB arrays let one lamp toggle between task brightness and lounge mood at the swipe of a screen. Manufacturing cost curves now allow mainstream price points, making decorative LED pieces accessible in mass retail and hospitality alike. For designers, LED boards embedded in organic or translucent substrates enable fresh narratives; for consumers, top-tier color rendering and 50,000-hour lifespans translate to longer satisfaction cycles and reduced maintenance costs.

Rapid Hotel-Room Refurb Cycles in Lifestyle and Boutique Segments

Social-media-driven brand storytelling compels hotels to refresh lighting schemes every few years, shortening refurb cycles that once spanned a decade. Unique floor lamps and sculptural table pieces act as Instagram backdrops, enhance perceived room value, and influence booking conversions, driving premium procurement budgets. Operators deploy dynamic LED arrays to match daytime business energy with evening leisure ambiance, optimizing revenue per available room through experiential differentiation. Energy-efficient fixtures cut utility bills and maintenance downtime, easing payback calculations. Brands increasingly specify connected controls that integrate with property-management systems to monitor occupancy and automate dimming when rooms are vacant, lifting sustainability credentials while streamlining operations.

Workplace Wellness Programs Embracing Circadian-Lighting Task Lamps

Corporate wellness budgets have spotlighted lighting as a quantifiable performance lever, with many employers allocating 20–30% extra for circadian-aligned systems that regulate melatonin and cortisol cycles. Task lamps that shift from cool noon whites to warm evening ambers support focus in open offices and minimize after-work fatigue, directly feeding retention targets as hybrid workers weigh in-office experience against home comfort. Employers capture granular usage data through connected drivers, correlating light patterns with productivity dashboards and tailoring future layouts based on empirical feedback. The market monetizes via premium optics, tunable LEDs, and Bluetooth mesh modules embedded in otherwise familiar form factors, creating upgrade triggers even where general ceiling lighting has already migrated to LED.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin pressure from DIY furniture-store private labels | -0.7% | Global, particularly intense in North America & EU | Short term (≤ 2 years) |

| Safety-code tightening on portable luminaires (fire and tip-over) | -0.3% | Global, with varying implementation timelines by region | Medium term (2-4 years) |

| Volatility in metal and glass commodity prices | -0.4% | Global, with manufacturing hubs most affected | Short term (≤ 2 years) |

| Lengthening replacement cycles due to ultra-long-life LEDs | -0.2% | Global, mature markets experiencing first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure from DIY Furniture-Store Private Labels

Mega-retailers exploit integrated supply chains to debut private-label lamps that undercut branded rivals by double-digit percentages while offering acceptable build quality. IKEA’s top-five market status exemplifies how bundled home-furnishing assortments steer shoppers away from specialist brands. Mid-tier producers feel the squeeze, prompting portfolio rationalization, regional exit strategies, or downstream mergers financed by private equity. Kingswood Capital’s USD 256 million sweep of Kichler and Progress Lighting into Coleto Brands illustrates that scale consolidation is a preferred defense. Legacy names now couple proprietary app ecosystems and designer collaborations to justify price premiums and shield margin integrity.

Safety-Code Tightening on Portable Luminaires

Regulators have refreshed standards such as UL 1598 to add tougher fire, tip-over, and wet-location requirements, imposing fresh engineering, testing, and documentation expenses. China’s GB/T 9473-2022 for reading lamps adds another compliance layer for exporters. Certification bottlenecks lengthen time-to-market, particularly for artisanal labels unfamiliar with multi-region regimes. Costs also rise for component traceability, grounding, and safety labeling, reshaping design priorities and nudging smaller firms toward OEM partnerships or exit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Task Lighting Dominates Amid Wellness Focus

Desk/task lamps generated the largest slice of the table and floor lamps market in 2025, seizing 48.62% revenue as employers and home workers converge on circadian-aligned illumination. Segment revenue reached USD 12.27 billion in 2025, and analysts project a steady 3.82% CAGR through 2031 as hybrid workflows persist. Floor lamps remain the breakout star, poised for a 14.02% CAGR, because hospitality operators and short-term landlords crave sculptural pieces that double as statement art. Traditional table lamps stay relevant, particularly when retrofitted with Wi-Fi drivers or voice-control modules that enable automation scenes. Accent, torchiere, and niche reading formats maintain modest volume, yet achieve healthy margins thanks to specialized optics and materials that address aging eyesight and design eccentricities. Competitive dynamics encourage multipurpose hybrids—task heads mounted on ambient towers—allowing a single SKU to satisfy living-room ambiance and focused worktop duties. Such versatility sustains upselling potential even as minimalism trends influence furniture footprints.

Second-generation smart task lamps integrate occupancy sensors, glare-control louvers, and USB-C charging docks, streamlining desktop clutter. Employers quantify lighting efficacy via wellness audits, correlating spectrum shifts with biometric feedback from wearables, thereby turning lamps into participatory wellbeing assets. The segment’s premium tier enjoys lower price elasticity: corporate buyers allocate budget based on productivity gains rather than unit cost. Conversely, entry-level desk fixtures sold through mass e-commerce lean on commodity LEDs and plastic housings, showing thin margins yet vast unit potential. The table and floor lamps market size for desk/task lamps is set to approach USD 15.36 billion by 2031, underscoring persistent dominance even as newer categories accelerate.

By Material: Metal Leadership Faces Sustainable Innovation

Metal remained the material of choice in 2025, holding 35.78% revenue, primarily through steel and aluminum constructions that grant durability, thermal management for LEDs, and broad aesthetic range. Robust supply chains and CNC versatility streamline design iterations, letting brands combine brushed finishes with powder-coat colors for rapid trend response. Nonetheless, wood posts the highest 14.28% CAGR outlook thanks to sustainability appeal and emerging research on transparent, phosphorescent wood panels that emit soft afterglow while showcasing natural grain. Such composites ally eco-credentials with functional luminosity, attractive to eco-conscious millennials who value carbon narratives simplified through FSC-certified sourcing.

Glass persists as the premium medium for sculptural statement lamps, leveraging optical clarity and hand-blown craftsmanship to tap luxury price bands. Glass also benefits from LED’s low heat output, allowing thinner profiles without thermal cracks. Ceramic resurges in boutique studios where tactile glazes produce individualistic finishes; small-batch ceramic runs exploit local clay traditions and align with the burgeoning “slow décor” movement. Recycled plastic alloys and hemp-fiber biopolymers populate budget-friendly lines, their color flexibility supporting seasonal palettes. As commodity metals face price unpredictability, design teams adopt mixed-material strategies—metal frames with wooden arms or rattan shades—to hedge costs and lift perceived artisanal value. Segment leaders now disclose life-cycle assessments, reinforcing transparency and tipping procurement decisions among contract buyers weighing ESG metrics.

By End-User: Residential Dominance Amid Commercial Innovation

Homeowners remained the central buyers, accounting for 62.71% of sales in 2025 as the work-from-anywhere wave spurred home-office upgrades and living-room mood-lighting makeovers. Residential demand is forecast to climb 13.92% through 2031, encouraged by falling prices for Wi-Fi modules and the mainstreaming of voice-controlled ecosystems. Within the commercial channel, hospitality venues drive premium orders: lifestyle hotels specify unique floor statements to anchor lobby identity, and chain operators pre-install smart dimming to satisfy green-building certifications. Offices, coworking hubs, and tech campuses adopt personal desk luminaires that sync circadian rhythms, often bundled under corporate wellness budgets for demonstrable return.

Retailers and restaurants deploy color-tunable lamps to evoke brand mood, while healthcare facilities specify glare-free, disinfectant-resistant housings aimed at patient comfort and staff efficacy. Education sectors migrate toward LED systems primarily to slash energy bills and maintenance downtime, but limited capital expenditures cap adoption of advanced controls. Government buildings and public libraries participate, spurred by mandates that align procurement with national efficiency or circularity goals. Industrial buyers remain a niche, focusing on rugged fixtures that handle vibration and dust, though interest grows in biologically optimized break-room lighting that reduces shift-worker fatigue. The table and floor lamps market size for residential applications should exceed USD 20.86 billion by 2031, reinforcing retail dominance even as high-margin commercial niches flourish.

By Distribution Channel: Digital Transformation Accelerates

Physical retail retained 40.62% in 2025, capitalizing on tactile evaluation—color rendition and material heft still matter—especially for high-value art pieces. Specialty lighting boutiques curate designer assortments and offer shade customization, justifying double-digit price premiums. Home-center chains deploy aisle-end vignettes that encourage basket bundling with furniture, rugs, and paint, capturing impulse purchases. Department stores remain relevant in emerging markets where urban malls dominate middle-class shopping journeys.

Online channels, posting a 13.68% CAGR, evolve from simple click-through catalogs into immersive showrooms featuring 360-degree configurators, AR placement previews, and AI chat advisers that propose bulb color temperatures based on room photos. Brand-owned storefronts raise gross margins, collect first-party data, and nurture repeat business through loyalty perks. Marketplaces scale selection breadth and expedite delivery, but customer acquisition costs escalate, pressing vendors to optimize keyword bids and refine listing imagery. Social-commerce clips on platforms such as TikTok accelerate viral launches, enabling micro-brands to sell thousands of units overnight. Warranty and returns infrastructure improve, alleviating customer hesitation historically tied to shipping fragile glass. For wholesalers, e-procurement portals simplify contractor orders, integrating project schedules and digital spec sheets.

Geography Analysis

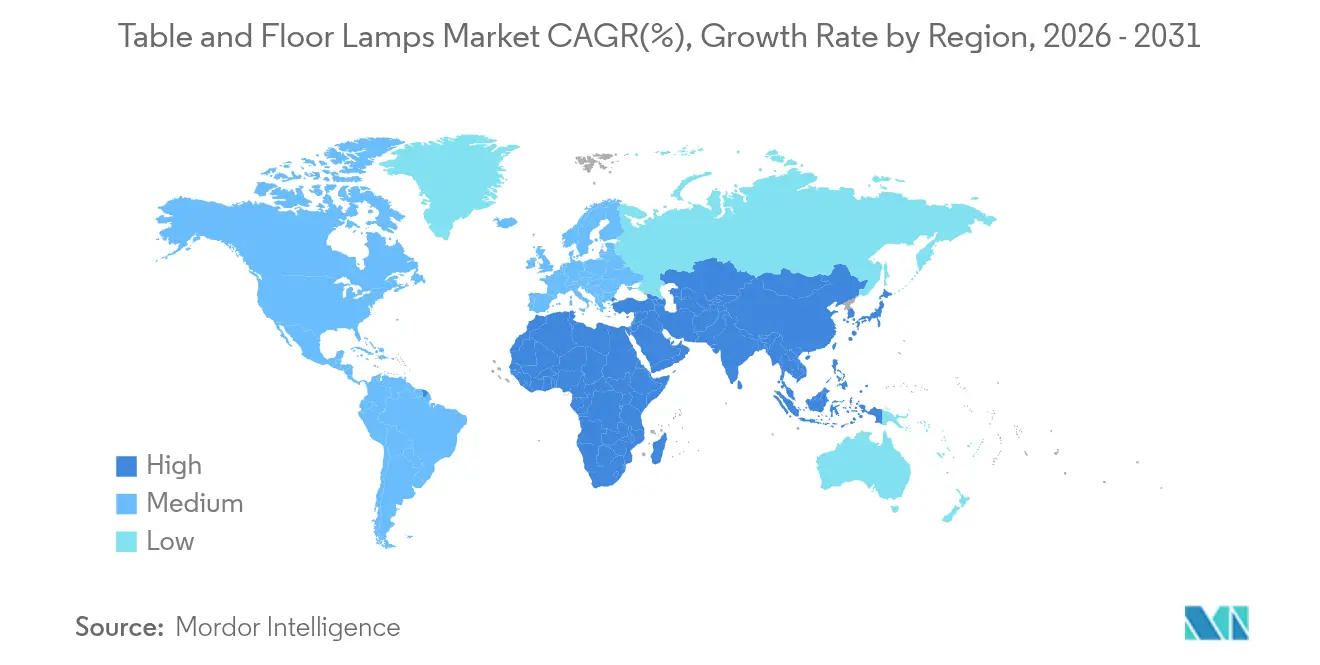

Asia-Pacific led the table and floor lamps market with 34.11% revenue in 2025 on the back of concentrated manufacturing clusters, competitive labor costs, and expanding urban middle-class consumption. China’s introduction of eight lighting standards in January 2024 underscores regulatory drive to elevate quality and safety while encouraging domestic innovation. Japan and South Korea showcase early-adopter appetite for voice-assistant lighting scenes and ultra-compact desk lamps suited to dense living spaces. India’s Smart Cities Mission and rising disposable incomes spur premium demand, although fragmented distribution networks pose reach challenges beyond tier-one metros. Southeast Asian economies, including Vietnam and Indonesia, see accelerating project pipelines in hospitality and residential high-rises, generating contract volumes for both domestic and foreign brands.

Middle East & Africa posts the fastest 9.21% CAGR forecast to 2031, propelled by mega-projects in Gulf states, energy diversification strategies, and robust hospitality pipelines targeting tourism diversification. The UAE lighting sector, valued at USD 336 million, targets 15% growth as Dubai’s solar-park initiatives dovetail with architectural showpieces that specify smart LED installations. Saudi Arabia’s Vision 2030 funds cultural hubs, entertainment districts, and luxury resorts that demand high-spec lamps for guest rooms and public lounges. African metros from Nairobi to Lagos modernize hotel stock and upscale residences, though erratic power supply pushes appetite for LED efficiency and integrated battery backup.

North America continues to display strong adoption of connected solutions; the U.S. Department of Energy’s tightened lamp efficiency rules effective July 2024 accelerate the shift toward integrated LED fixtures. Consumers embrace voice synchronization across smart-speaker ecosystems, and corporate buyers scale datacentric wellness pilots. European markets mirror North America in maturity but intensify circular-economy criteria, rewarding brands that offer repairable modules and certified recycled content. In Germany and the Nordics, public procurement frameworks now award points for end-of-life recyclability, steering tenders toward modular designs. Despite slower unit growth, both regions offer high average selling prices and early adoption for emerging control protocols such as Matter, reinforcing their influence on global standards.

Competitive Landscape

The table and floor lamps market maintains moderate concentration, with Signify, IKEA Group, Acuity Brands, FLOS, and Artemide collectively anchoring revenue leadership. Private equity is an active reshape, Kingswood Capital forged Coleto Brands by acquiring Kichler and Progress Lighting for USD 256 million, aiming to unlock shared logistics, digital marketing, and cross-brand product lines. Technology giants likewise expand stakes; Siemens’ planned USD 10.6 billion purchase of Altair Engineering bundles the Toggled controls platform, signaling alignment between lighting and holistic building-automation stacks.

Established brands differentiate through R&D into multisensor drivers that measure sound, temperature, and air quality, positioning lamps as infrastructure for broader smart-space analytics. FLOS leans on Italian design heritage, partnering with architects for limited editions that command luxury margins. IKEA scales affordability through vertically integrated supply chains and diode-on-board (DoB) modules that minimize part counts. Signify fortifies connected ecosystems via the Hue portfolio and open APIs, licensing Zigbee and Matter firmware to third-party luminaires and collecting subscription revenue from cloud scene libraries. Acuity Brands invests in AI algorithms that orchestrate building-wide daylight harvesting and occupant-based energy optimization, evident in its 2025 acquisition of QSC that broadens its sensor and control logic footprint.

Threats arise from white-label imports featuring basic Bluetooth control at a fraction of branded prices. To preserve pricing power, leaders emphasize compliance with evolving standards like UL 1598 and EU-wide EcoDesign, which require rigorous photobiological safety and energy metrics. Micro-brands court Instagram aesthetics but face certification costs that hamper scaling. Strategic OEM alliances and contract manufacturing in Vietnam or Mexico help incumbents balance tariff risks and shorten lead times to North American and European markets. Emerging ESG scrutiny pushes all players to publish Scope 3 emissions baselines and commit to recyclable packaging, with early movers gaining procurement preference among institution buyers.

Table And Floor Lamps Industry Leaders

Signify

Artemide

Flod

IKEA

Acuity Brands Lighting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Coleto Brands announced as the umbrella entity uniting Kichler and Progress Lighting after Kingswood Capital’s acquisitions, aiming to exploit shared distribution efficiencies and digital commerce scale.

- November 2024: Sonepar added USD 2 billion revenue in 2024 through acquisitions and branch expansions, reinforcing distributor demand for connected lighting.

Global Table And Floor Lamps Market Report Scope

A floor Lamp is a tall lamp that stands on the floor, and a Table Lamp is a small lamp designed to stand on a table. A complete background analysis of the Table and Floor Lamps Market, which includes an assessment of the economy and the contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, and market dynamics, are covered in the report. The Table And Floor Lamps Market is Segmented By Product Type (Table Lamps and Floor Lamps), By Application (Residential and Commercial), and By Geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The report offers market size and values in (USD) during the forecast period for the above segments.

| Table Lamps |

| Floor Lamps |

| Desk/Task Lamps |

| Accent and Decorative Lamps |

| Torchieres and Uplights |

| Others |

| Metal |

| Wood |

| Glass |

| Ceramic |

| Plastic and Others |

| Residential | |

| Commercial | Hospitality |

| Offices and Co-working Spaces | |

| Retail and Restaurants | |

| Healthcare Facilities | |

| Educational Institutions | |

| Others (Commercial) | |

| Institutional | |

| Industrial and Others |

| Offline | Specialty Lighting Stores |

| Furniture and Home-center Chains | |

| Hypermarkets / Department Stores | |

| Online | Brand-owned Webstores |

| Marketplaces (Amazon, Wayfair, etc.) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Table Lamps | |

| Floor Lamps | ||

| Desk/Task Lamps | ||

| Accent and Decorative Lamps | ||

| Torchieres and Uplights | ||

| Others | ||

| By Material | Metal | |

| Wood | ||

| Glass | ||

| Ceramic | ||

| Plastic and Others | ||

| By End-user | Residential | |

| Commercial | Hospitality | |

| Offices and Co-working Spaces | ||

| Retail and Restaurants | ||

| Healthcare Facilities | ||

| Educational Institutions | ||

| Others (Commercial) | ||

| Institutional | ||

| Industrial and Others | ||

| By Distribution Channel | Offline | Specialty Lighting Stores |

| Furniture and Home-center Chains | ||

| Hypermarkets / Department Stores | ||

| Online | Brand-owned Webstores | |

| Marketplaces (Amazon, Wayfair, etc.) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size of the table and floor lamps market?

The table and floor lamps market size stands at USD 26.41 billion in 2026 and is projected to reach USD 33.08 billion by 2031.

Which product segment leads the market?

Desk/task lamps lead with 48.62% of revenue in 2025, reflecting widespread adoption in both home offices and corporate wellness programs.

How fast are floor lamps growing?

Floor lamps register the quickest expansion, forecast at a 14.02% CAGR through 2031 due to hospitality refurbishments and demand from short-term rental hosts.

Which region is expanding fastest?

Middle East & Africa shows the highest projected growth at 9.21% CAGR, propelled by large-scale urban developments and ambitious energy-efficiency mandates.

How is e-commerce affecting sales channels?

Online channels are forecast to grow at 13.68% CAGR, supported by augmented-reality visualization tools and direct-to-consumer brand strategies that enhance buyer confidence.

Page last updated on: