Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24.59 Billion |

| Market Size (2026) | USD 25.72 Billion |

| Market Size (2031) | USD 32.18 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Home Decor Market Analysis by Mordor Intelligence

The United Kingdom home decor market size in 2026 is estimated at USD 25.72 billion, growing from 2025 value of USD 24.59 billion with 2031 projections showing USD 32.18 billion, growing at 4.58% CAGR over 2026-2031. Expansion continues even while consumers face higher living costs because of hybrid work patterns, insulation incentives, and a growing preference for sustainable products keep renovation activity robust. Energy-efficiency upgrades under the Great British Insulation Scheme, coupled with stable home-ownership levels, are steering spending toward furniture, textiles, lighting, flooring, and accessories that improve both comfort and resale value[1]Department for Energy Security & Net Zero, “Great British Insulation Scheme Launches,” gov.uk. Retailers have redesigned supply chains to handle Red Sea shipping risks while still maintaining service levels, helping preserve shopper confidence despite longer global lead times. E-commerce penetration, already at 37% of sales for market leaders, continues to expand as AI search tools and mobile-first checkouts reduce friction for big-ticket purchases[2]Dunelm Group plc, “FY 2025 Annual Report,” dunelm.com.

Key Report Takeaways

- By product type, furniture led with 31.12% of the United Kingdom home decor market share in 2025, while home accents and accessories are advancing at a 5.02% CAGR through 2031.

- By distribution channel, homeware and furniture specialists held 36.92% of revenue in 2025; online pure-players are projected to grow fastest at a 5.86% CAGR to 2031.

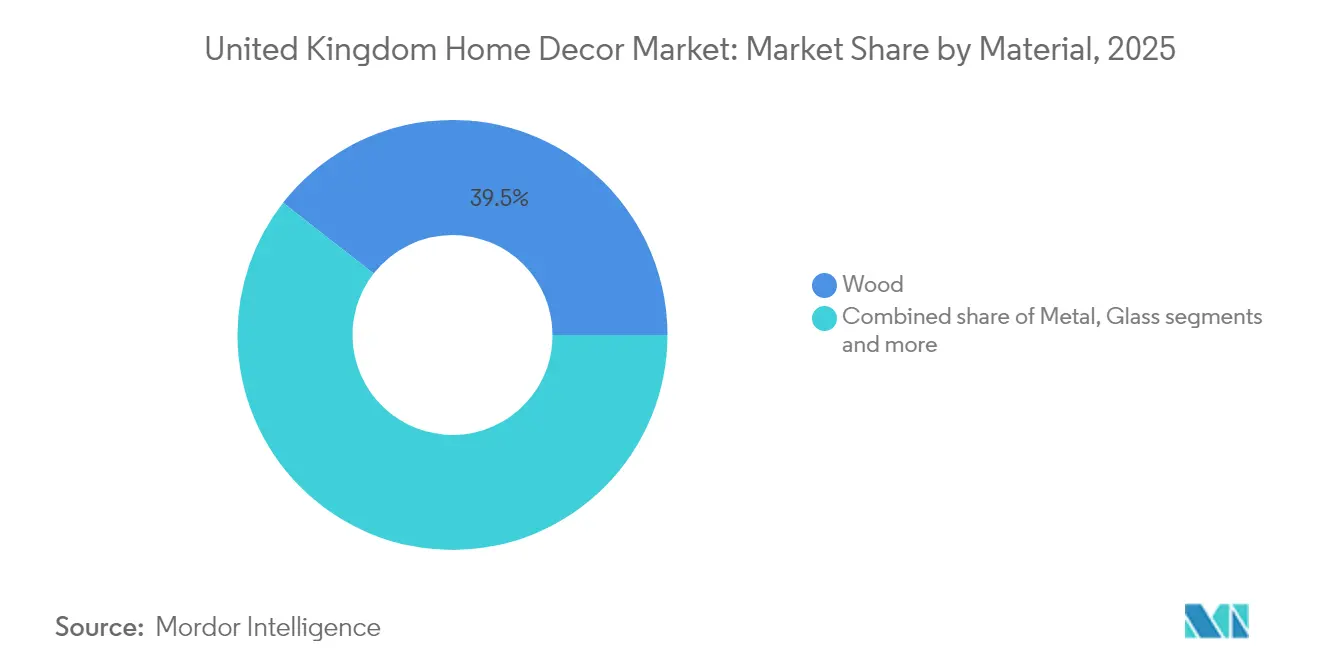

- By material, wood accounted for a 39.45% share of the United Kingdom home decor market size in 2025, whereas sustainable and recycled materials are expected to post a 6.24% CAGR through 2031.

- By geography, England captured 46.85% of revenue in 2025 and is forecast to expand at a 5.36% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Home Decor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & home-ownership | +1.2% | England, Scotland, with concentration in metropolitan areas | Medium term (2-4 years) |

| Growth of DIY & hybrid-work refurbishments | +0.8% | National, with higher impact in suburban and rural areas | Short term (≤ 2 years) |

| Expansion of e-commerce & omnichannel retail | +1.0% | National, with early gains in urban centers | Medium term (2-4 years) |

| Demand for sustainable décor materials | +0.6% | England, Wales, with premium market concentration | Long term (≥ 4 years) |

| Micro-living driving multifunctional furniture | +0.4% | London, Manchester, Birmingham metropolitan areas | Medium term (2-4 years) |

| VAT incentives for energy-efficient upgrades | +0.3% | National, with higher uptake in lower-income households | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Homeownership

Home-ownership stability and gradual wage growth have created an environment where households feel secure enough to resume discretionary decor projects deferred during pandemic uncertainty. Millennials entering prime purchasing ages prefer personalized interiors, resulting in per-square-foot spending that exceeds prior generations. Regional variations help premium brands thrive in southern England, while value lines find volume in northern cities where affordability remains paramount. Government programs supporting first-time buyers add incremental demand because new owners typically invest heavily in furniture and decoration during their first two years of occupancy. The wealth effect from rising property values in London, Manchester, and Birmingham further encourages spending on premium furnishings.

Growth of DIY & Hybrid-Work Refurbishments

Permanent hybrid work arrangements have reshaped room layouts, elevating demand for ergonomic desks, screens, and versatile storage that toggle between professional and leisure use. Remote-work tax relief increases disposable budgets for home office improvements, and retailers have seized the moment by offering virtual design advice and modular kits that simplify do-it-yourself assembly. Social media tutorials have deepened DIY sophistication, enabling consumers to tackle complex projects once left to contractors. Click-and-collect orders for small hardware and décor items grew 40% year-over-year as shoppers sought quick upgrades between virtual meetings. Retailers now schedule smaller but more frequent deliveries to align with this wave of micro-projects.

Expansion of E-commerce & Omnichannel Retail

Digital transformation in the United Kingdom home decor market extends well beyond basic online storefronts to immersive virtual showrooms and AI-powered recommendation engines. Dunelm reports that omni-shoppers place larger baskets than store-only buyers, justifying big data investments in search, personalization, and predictive replenishment[3]Furniture Industry Research Association, “Lifecycle Standards Update,” fira.co.uk. Buy-now-pay-later services reduce the psychological barrier to purchasing high-priced sofas and modular wardrobes. Partnerships like the IKEA–Tesco pickup network add more than 100 collection points, increasing geographic reach without new store builds. Mobile devices now drive over 60% of online transactions, forcing retailers to optimize every stage of the purchase journey for handheld screens.

Demand for Sustainable Décor Materials

Environmental concern has evolved into a mainstream buying criterion, helping sustainable and recycled materials log the fastest segment growth at 6.31% CAGR. The United Kingdom's net-zero pledge pushes manufacturers to adopt circular design, and leading trade bodies have created new standards to quantify environmental performance. Consumers willingly pay premiums for FSC-certified timber, reclaimed wood, and bio-based fabrics because transparency labels build trust. Retailers leverage circular initiatives like furniture buyback programs to keep valuable material in use and strengthen brand equity. Innovation in recycled composites, ocean plastics, and low-VOC finishes shows that sustainability is now intertwined with product differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -0.7% | National, with higher impact on manufacturing regions | Short term (≤ 2 years) |

| Low-cost import price pressure | -0.5% | National, with concentration in price-sensitive segments | Medium term (2-4 years) |

| Supply-chain lead-time disruptions | -0.4% | National, with higher impact on import-dependent retailers | Short term (≤ 2 years) |

| Growth in second-hand/circular channels | -0.3% | Urban areas, with concentration in younger demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Cost Volatility

Timber, steel, and energy costs continue to fluctuate sharply, squeezing margins for firms unable to hedge effectively. Softwood lumber swung more than 40% in several quarters, while fabricated steel prices jumped 15.7% year-on-year by mid-2024[4]Department for Business & Trade, “Construction Material Price Indices May 2024,” gov.uk. Rising energy tariffs have raised manufacturing overhead, raising the share of production costs tied to electricity and gas from 8-12% before 2022 to 15-20% today. Red Sea shipping disruption layered higher container charges onto Asian imports, complicating inventory planning. Smaller brands face capital constraints when stockpiling inputs, potentially accelerating consolidation.

Low-Cost Import Price Pressure

Asian suppliers maintain a 30-50% landed-cost advantage, forcing United Kingdom manufacturers to compete on design, speed, and sustainability rather than price alone. Even after adding CE, REACH, and fire-safety compliance costs, imported furniture still undercuts domestic equivalents by wide margins. The rise of Amazon-based Chinese brands that ship direct to United Kingdom consumers bypasses wholesaler markups, creating retail price points that the United Kingdom producers struggle to match. Post-Brexit customs protocols add paperwork but have not meaningfully eroded the cost gap, so imports hold their volume share. Dropship models further intensify competition by eliminating inventory risk for online sellers and keeping upfront capital needs minimal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Furniture Dominance Faces Accessory Innovation

Furniture delivered 31.12% of the United Kingdom home decor market share in 2025 because large pieces like sofas and beds anchor every room’s utility and style. Hybrid work boosted sales of adjustable desks and ergonomic chairs as knowledge workers outfitted permanent offices within the home. Textiles such as bedding and curtains recorded brisk turnover because they allow inexpensive seasonal refreshes, while smart lighting extended beyond utility to mood-setting and video call aesthetics. Rug and flooring updates help divide open-plan layouts into functional zones, driving demand for luxury vinyl tile and engineered wood that offer durability with design flexibility. Accessories are projected to outpace all other categories at a 5.02% CAGR as shoppers embrace low-commitment items that align with fast-changing social trends.

Accessories thrive because they enable constant micro-upgrades without the financial strain of replacing core furniture. Multifunctional pieces that combine storage with decor resonate in micro-apartments, where Bonbon Compact Living and similar brands provide solutions built for constrained footprints. Subscription boxes introduce consumers to emerging designers while guaranteeing predictable revenue for suppliers, amplifying discovery beyond traditional showrooms. Limited-edition seasonal collections from mainstream retailers achieve margins 20-30% above evergreen lines by creating urgency-driven buying. Social-commerce ads on Instagram and Pinterest further catalyze accessory demand because impulse-friendly price points pair naturally with visual platforms.

By Distribution Channel: Digital Disruption Reshapes Retail Landscape

Homeware and furniture specialists retained 36.92% revenue share in 2025 thanks to curated assortments, experienced sales teams, and in-store consultancy that foster trust for big-ticket purchases. DIY warehouses expanded furniture ranges to capture hybrid-work demand, while supermarkets introduced value-priced décor lines to lift basket values. Department stores compressed floor space devoted to home goods, ceding ground to niche chains and online platforms. Direct-to-consumer startups gained visibility through authenticity-focused branding and transparent supply chains, appealing to younger audiences seeking originality. Online pure-players are forecast to grow 5.86% CAGR, propelled by advanced logistics, robust AR visualization tools, and AI recommendation engines.

Technology is the decisive battleground for channel supremacy. Wayfair’s 3D room planner and AR app reduce return rates by showing customers exactly how a sofa or lamp will fit before purchase. IKEA’s Tesco pickup partnership pushes the brand closer to customers without major cap-ex, marrying the convenience of click-and-collect with grocery errands. Live-stream demos replicate showroom walk-throughs and let influencers answer questions in real time, shrinking the guidance gap between digital and physical browsing. Mobile-optimized checkouts must now handle complex financing and delivery scheduling seamlessly because smartphones drive most traffic. Traditional retailers are racing to retrofit their tech stacks, but the investment burden threatens margins.

By Material: Sustainability Drives Premium Material Innovation

Wood held 39.45% of 2025 revenue because its warmth and versatility span both classic and contemporary styles. Engineered products that pair wood veneers with recycled fiberboard appeal to eco-aware shoppers seeking durability without old-growth logging. Metal frames and accents satisfy minimalist and industrial tastes, while powder-coat finishes add scratch resistance that buyers demand in busy households. Glass dividers create light-sharing zones inside compact flats, aligning with tenant-friendly removable construction trends. Plastic and acrylic have evolved into high-design materials due to 3D printing technologies that enable complex shapes impossible with traditional joinery.

Sustainable materials deliver the fastest expansion at 6.24% CAGR because regulation and consumer sentiment converge around circularity. Reclaimed hardwood from demolished structures enters mainstream catalogs, and retailers leverage story-driven marketing that details each plank’s origin to justify premium pricing. Post-consumer recycled plastics now appear in indoor chairs and side tables that maintain color consistency through advanced pellet sorting. Bio-based resources such as bamboo, cork, and hemp fabrics satisfy durability tests while meeting renewable sourcing criteria, offering a credible alternative to petroleum-derived inputs. Certification labels from FSC and Cradle to Cradle bolster shopper trust and permit price premiums, transforming sustainability from a cost center to a profit avenue.

Geography Analysis

England dominated the United Kingdom home décor market with 46.85% of 2025 revenue because its dense metropolitan hubs combine higher incomes with lively housing turnover. London’s luxury segment commands price tags that run 30-50% above national averages, yet it still posts strong sell-through because global buyers treat décor as lifestyle signalling. Southern counties display a taste for minimalist Scandinavian lines, whereas northern cities gravitate toward traditional forms that emphasize comfort and durability. E-commerce service levels are highest in England as next-day delivery networks cluster around major fulfillment nodes. The Great British Insulation Scheme has found the widest adoption here, further stoking demand for décor upgrades that pair with energy-saving retrofits.

Scotland’s market values heritage craftsmanship, favoring wool textiles and locally milled timber that withstand harsh climates. Heavy draperies and insulation-focused soft furnishings outsell lighter alternatives because weather extremes demand both warmth and durability. Scottish consumers also pay premiums for items that highlight regional identity, fostering a vibrant artisan sector. Logistics challenges in rural Highlands inflate delivery fees, encouraging retailers to partner with local makers who can bypass long-haul routes. Government-backed energy subsidies see slower uptake here, partly because stone tenements require bespoke insulation solutions that complicate standard grant processes.

Wales and Northern Ireland account for smaller but strategically important slices of the United Kingdom home décor market. Welsh shoppers increasingly reward brands that minimize transport miles, tying sustainability to regional economic support. Northern Irish retailers manage cross-border complexities that influence inventory selection, currency exposure, and promotional timing relative to the Republic of Ireland holidays. Rural postcodes across both regions struggle with limited showroom access, prompting omnichannel retailers to use augmented reality and mobile trailers to demonstrate product lines in community hubs. Distinct architectural formats—from Welsh terraced homes to Northern Irish detached houses—create varied room dimensions that require SKU customization for optimal fit.

Competitive Landscape

Competition is moderate to high because legacy chains, digital natives, value imports, and sustainability pioneers all vie for consumer share of wallet. The top five retailers held 38% of 2024 revenue, yielding a landscape where no single player can dictate pricing, yet scale advantages matter for AI tooling and supply-chain agility. Dunelm lifted its United Kingdom home decor market share to 7.7% by integrating data science into inventory planning and expanding made-to-measure services that boost average order value. IKEA slashed prices on roughly one-third of its lineup and committed over GBP 10 million to staff pay improvements, positioning itself as both affordable and socially responsible. Vertical integration grants certain brands control from design to final-mile delivery, shielding them from spot-rate freight spikes and raw-material swings.

Supply-chain resilience has become a key differentiator after Red Sea disruptions exposed vulnerabilities in far-east sourcing networks. Retailers with multiregional factories or near-shoring partnerships sustained stock levels and won share while rivals issued back-order notices. Sustainability credentials also separate leaders from laggards as circular economy services move from pilot to core revenue stream. IKEA’s buyback initiative processed 52,600 returned items in 2024, feeding refurbished goods back into stores and reinforcing green positioning. Direct-to-consumer upstarts exploit social media targeting and micro-influencers to slice narrow demographics, but many will face scaling challenges once acquisition costs climb.

Technology-first disruptors invest aggressively in augmented reality, machine-learning personalization, and predictive logistics. Legacy chains must modernize quickly or risk sliding into price-only competition that erodes margins. Partnerships—whether with fintech for seamless checkout or with grocery giants for collection points—emerge as force multipliers that help incumbents close capability gaps without overextending capital budgets. International entrants such as Pottery Barn see an opportunity to import recognizable aesthetics and omnichannel best practices from the U.S., raising the stakes across style and service dimensions. As circular resale platforms approach mainstream adoption, incumbents will need to integrate refurbishment, rental, or trade-in programs or risk ceding volume to secondary channels.

United Kingdom Home Decor Industry Leaders

IKEA Ltd (UK)

Dunelm Group plc

DFS Furniture plc

B&Q (Kingfisher plc)

John Lewis & Partners

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2022: The online home furnishings retailer has opened its first brick-and-mortar store under the AllModern banner, at MarketStreet Lynnfield in Lynnfield, Massachusetts. A second location is set to open this fall at Legacy Place in Dedham, Massachusetts. Wayfair announced in December that it planned to open physical stores under all of its banners beginning in 2022, with two AllModern and one Joss & Main location at Burlington Mall in Burlington, Massachusetts.

- October 2022: IKEA launched the new IKEA Home smart app, and DIRIGERA, a new hub for smart products, will enable a rich and intuitive experience, including new features to personalize and enhance everyday moments in the home

United Kingdom Home Decor Market Report Scope

The United Kingdom Home Decor Market is Segmented by Product (Home Furniture, Home Textile, Flooring, Wall Decor, Tableware and Cookware, Lighting and Lamps, Sanitaryware, Home Accessories, and Other Products) and by Distribution Channel (Supermarkets and Hypermarkets, Home Decor Stores, Gift Shops, Direct to Consumer, Online, and Other Distribution Channels). The report offers market size and forecast values for the United Kingdom Home Decor Market in USD billion for the above segments.

By Product Type

| Furniture |

| Home Textiles (Bedding, Curtains) |

| Decorative Lighting |

| Flooring (Rugs, Carpets, Hard Flooring) |

| Wall Décor (Paint, Wallpaper, Art) |

| Home Accents & Accessories |

By Distribution Channel

| Homeware & Furniture Specialists |

| DIY / Home Improvement Stores |

| Supermarkets & Hypermarkets |

| Department & Variety Stores |

| Online Pure-Players |

| Direct-to-Consumer Brands |

By Material

| Wood |

| Metal |

| Glass |

| Plastic & Acrylic |

| Textiles & Fabrics |

| Sustainable / Recycled Materials |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Type | Furniture |

| Home Textiles (Bedding, Curtains) | |

| Decorative Lighting | |

| Flooring (Rugs, Carpets, Hard Flooring) | |

| Wall Décor (Paint, Wallpaper, Art) | |

| Home Accents & Accessories | |

| By Distribution Channel | Homeware & Furniture Specialists |

| DIY / Home Improvement Stores | |

| Supermarkets & Hypermarkets | |

| Department & Variety Stores | |

| Online Pure-Players | |

| Direct-to-Consumer Brands | |

| By Material | Wood |

| Metal | |

| Glass | |

| Plastic & Acrylic | |

| Textiles & Fabrics | |

| Sustainable / Recycled Materials | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How big is the United Kingdom Home Decor Market?

The United Kingdom Home Decor Market size is expected to reach USD 25.72 billion in 2026 and grow at a CAGR of 4.58% to reach USD 32.18 billion by 2031.

What is the current United Kingdom Home Decor Market size?

In 2026, the United Kingdom Home Decor Market size is expected to reach USD 25.72 billion.

Who are the key players in United Kingdom Home Decor Market?

Ikea, Bed Bath & Beyond, Wayfair Stores Ltd, DFS Furniture PLC and Dunelm Group PLC are the major companies operating in the United Kingdom Home Decor Market.

What years does this United Kingdom Home Decor Market cover, and what was the market size in 2025?

In 2025, the United Kingdom Home Decor Market size was estimated at USD 24.59 billion. The report covers the United Kingdom Home Decor Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the United Kingdom Home Decor Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: