Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 78.98 Billion |

| Market Size (2031) | USD 96.52 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

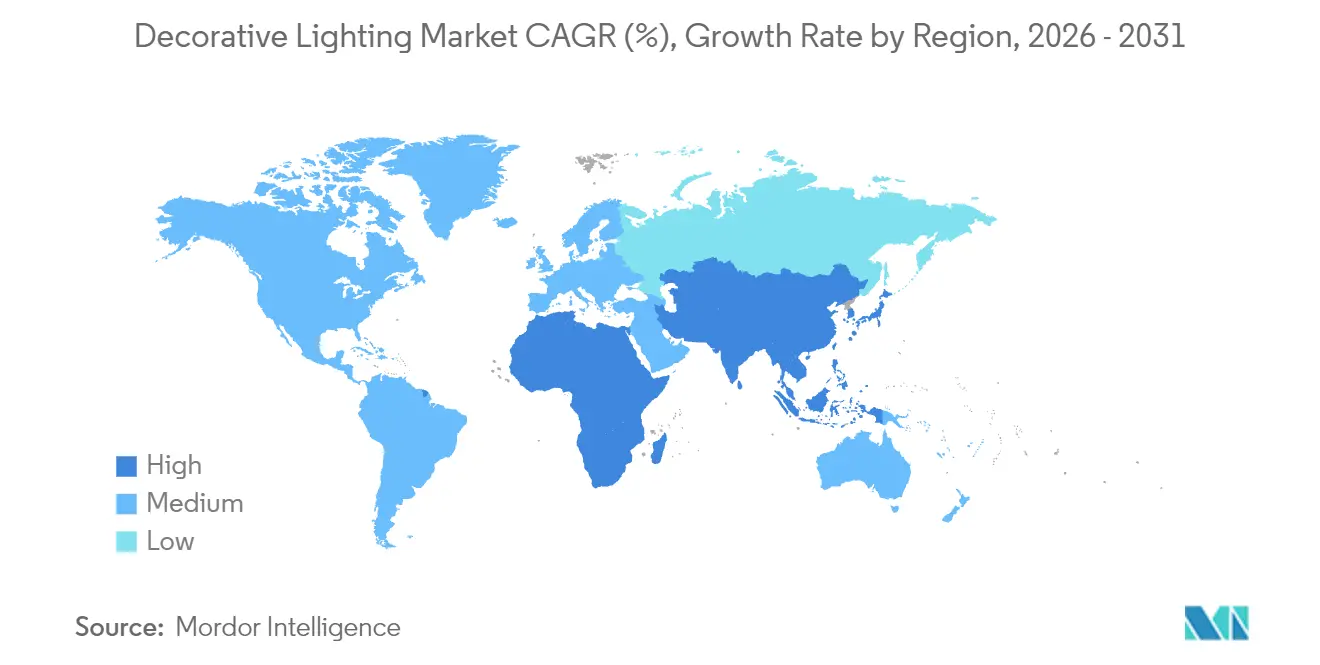

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decorative Lighting Market Analysis by Mordor Intelligence

The decorative lighting market size reached USD 75.88 billion in 2025, is projected at USD 78.98 billion in 2026, and is expected to attain USD 96.52 billion by 2031, registering a 4.09% CAGR. Near-term growth in the decorative lighting market is supported by policy-driven replacement cycles as the United States' efficacy rules converge with European lamp phase-outs. This policy backdrop intersects with a shift toward design-led fixtures, human-centric features, and smart connectivity, which push consumers toward higher value products. Smart-ready controls and interoperability are now part of baseline expectations in new construction and high-spec retrofits. Asia-Pacific’s scale in manufacturing and urban development positions the region to lead expansion in the decorative lighting market through 2031.

Key Report Takeaways

- By product type, ceiling lights and chandeliers with 35.02% of the decorative lighting market share in 2025, while table and floor lamps are forecast to expand at a 5.21% CAGR through 2031.

- By light source, LED technology commanded 70.12% of the decorative lighting market share in 2025, whereas OLED and solar solutions are projected to record the fastest 4.88% CAGR through 2031.

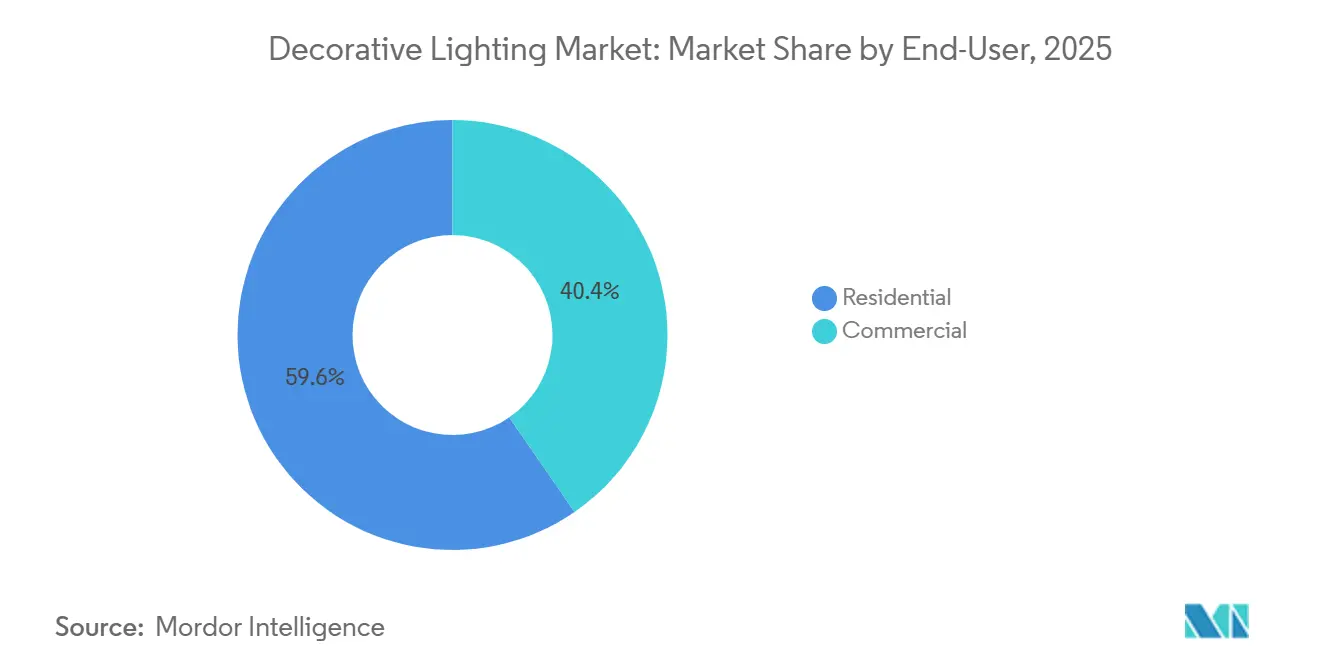

- By end-user, residential accounted for 59.65% of the decorative lighting market share in 2025, while commercial is projected to grow at a 5.55% CAGR through 2031.

- By distribution channel, B2C retail captured 63.92% of the decorative lighting market share in 2025, whereas online sub-channels are set to grow at a 4.98% CAGR through 2031.

- By geography, Asia-Pacific held 35.70% of the decorative lighting market share in 2025 and is projected to record the fastest 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Decorative Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory LED phase-outs accelerate replacement demand | +1.2% | Global, concentrated in the United States (10 states), the European Union-27, and China | Short term (≤ 2 years) |

| Premiumization and design-led purchasing | +0.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Smart/connected decorative lighting adoption | +0.9% | Global, early gains in North America, Scandinavia, and South Korea | Medium term (2-4 years) |

| E-commerce assortment depth and convenience lift conversion | +0.7% | Global, spill-over to emerging markets via Amazon expansion | Medium term (2-4 years) |

| Human-centric lighting (WELL/health-oriented) influences specs | +0.4% | North America commercial, select European Union/Asia-Pacific premium residential | Long term (≥ 4 years) |

| Social media and short-video content are shaping décor choices | +0.3% | Global, particularly Gen Z/Millennial cohorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory LED Phase-Outs Accelerate Replacement Demand

State and national policies are catalyzing a synchronized replacement wave in the decorative lighting market as legacy lamps exit shelves. The United States Department of Energy set a new 120+ lumens per watt threshold for general service lamps effective in 2028, displacing incandescent and halogen technologies and locking in LED as the default platform. In Europe, updated Ecodesign and RoHS measures are phasing out mercury-containing fluorescents by 2025, which removes a major legacy category and funnels demand to LED-based decorative fixtures[1]International Energy Agency, “Efficient and Mercury-Free Lighting Transitions,” iea.org . Similar policy momentum is visible in Africa through regional harmonization and Minamata Convention proposals that target compact and linear fluorescent lamps, further consolidating the shift. These coordinated standards shorten replacement cycles and reward brands that can rapidly update SKUs, qualify products to safety standards such as IEC 60598, and document compliance for multiple jurisdictions. As a result, procurement teams and consumers converge on compliant LED luminaires, lifting value mix and accelerating the penetration of connected decorative solutions in both residential and commercial settings.

Premiumization and Design-Led Purchasing

Consumers in mature economies now view decorative fixtures as part of interior identity, which lifts the average selling price mix in the decorative lighting market. Premium manufacturers are expanding curated collections and designer collaborations to meet this taste shift, as seen in Kichler’s 2025-2026 launches that include the Larousse chandelier, priced within the USD 1,889–USD 4,599 range[2]Kichler Lighting, “New Collections and Design Trends,” kichler.com . Hinkley is following a similar playbook with the Fantine chandelier series positioned from USD 4,599 to USD 6,799, signaling sustained willingness to pay for craftsmanship, finishes, and brand heritage. Foscarini’s recent portfolio moves and material experimentation underscore how design houses differentiate through aesthetic innovation that supports premium positioning in decorative categories. In India, Havells has pushed into experiential retail with thematic collections and expanded “Home Art Lights” stores, capturing aspirational demand with design-led assortments that favor margins over unit volumes. This premium mix skews segment growth toward accent and statement pieces, sustaining revenue even as commoditized categories experience price pressure.

Smart/Connected Decorative Lighting Adoption

Connectivity is becoming a default expectation in higher-end residential projects and most commercial renovations, which lifts feature content and supports pricing power in the decorative lighting market. Large platforms are building durable installed bases, exemplified by Signify’s 167 million connected light points by the end of 2025, which strengthens ecosystem loyalty and accessory pull-through[3]Signify, “Connected Light Points and Platform Ecosystem,” signify.com . Smart control mandates are also deepening in building codes, which drives the specification of adaptive lighting controls in hospitality, office, and mixed-use spaces. California’s Title 24 framework and demand-response provisions raise the bar for control readiness in many building types. The 2024 IECC expanded occupancy and dimming requirements across additional room types, aligning code pressure with energy and wellness outcomes in decorative applications such as lobbies, meeting areas, and premium retail. Product innovation is also targeting connectivity friction at the home level, with brands like Havells introducing BLE mesh-based GenieLit to remove Wi Fi dependency and simplify multi-room control. M&A in building technologies, including Acuity’s acquisition of QSC, is bundling audio, video, and environmental controls with lighting to deliver integrated experiences that favor specification of smart decorative fixtures.

E-Commerce Assortment Depth and Convenience Lift Conversion

Digital channels expand the decorative lighting market by aggregating breadth that is impossible to replicate in physical showrooms. Online sub-channels within B2C retail are projected to outgrow the overall market due to richer content, attribute filtering, and visualization tools that reduce purchase friction for higher ticket decorative fixtures. Brands are complementing marketplaces with direct-to-consumer sites that feature digital lookbooks and configuration options, as seen in EGLO’s extensive online catalogs that increase reach for European-design portfolios. This online shift favors agile brands that can manage high-SKU environments and respond to fast design cycles. It also supports value migration toward design-led assortments and connected SKUs where storytelling and software features can be demonstrated through digital experiences. Retail channel dynamics are shifting as home centers emphasize private labels, which is prompting incumbents to prioritize online-native and project-driven channels that better reward differentiated offerings. The net effect is consolidation of online share across major marketplaces and brand sites, raising the bar for digital merchandising and post-purchase support as determinants of loyalty in decorative categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price deflation and intense competition in non-connected SKUs | -0.9% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Regulatory phase-outs are stranding legacy inventory | -0.5% | United States state-level, European Union-27 | Short term (≤ 2 years) |

| Product safety recalls and compliance burdens | -0.2% | Global, heightened scrutiny in North America, the European Union | Medium term (2-4 years) |

| Marketplace compliance barriers (labels, DOE filing) | -0.3% | United States, Canada, and emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Deflation and Intense Competition in Non-Connected SKUs

Long-term declines in LED component costs keep price pressure high in commodity decorative categories, which weighs on margins in the decorative lighting market. Government programs that scaled LED volumes also drove reference price anchors, as seen in India, where UJALA helped cut LED lamp prices in ways that influence consumer expectations across adjacent categories. Company disclosures reflect this pressure, with Havells reporting that the lighting segment value growth lagged volumes as price deflation offset unit gains, even as contribution margins improved on value-added innovation. Signify’s recent results also show headwinds in non-connected consumer lines, while connected offerings maintained growth, highlighting a structural bifurcation. At the same time, technical ceilings are moving higher, as evidenced by OPPLE’s 230 lm/W streetlight module performance, which compresses room for differentiation on efficacy alone. In response, incumbents are realigning portfolios toward proprietary controls, integrated platforms, and design-led SKUs to escape commodity pricing traps, a strategy echoed in sustainability and corporate reports.

Regulatory Phase-Outs Stranding Legacy Inventory

The timing of national and subnational bans can create stranded inventory and retooling costs, which temporarily drag on the decorative lighting market. United States efficacy rules combined with state-level fluorescent restrictions require distributors to accelerate the sell-down of legacy stock and reconfigure assortments toward compliant LED fixtures. The DOE quantified industry-wide transition costs for general service lamps in associated rulemakings, indicating a material, near-term burden on manufacturers and channel partners. In Europe, the combination of RoHS mercury restrictions and Ecodesign rules rapidly removes fluorescent lamps from circulation, compressing distributor sell-through windows and forcing fixture redesign to LED modules. Industry associations project a high LED share of residential lamps by 2030 in the European Union, which underscores the permanence of the technology shift and the short-term write-down risk for legacy products. Brands with modular or upgradable light engines can mitigate obsolescence by facilitating field conversions, though such platforms have deeper traction in professional settings than in mass-market residential decorative fixtures today.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceiling Lights Command Share, Table Lamps Capture Design Spend

Ceiling lights and chandeliers captured 35.02% of the decorative lighting market share in 2025, and table and floor lamps are on track to grow at a 5.21% CAGR through 2031. This category leadership reflects the central role of overhead fixtures in residential living spaces and commercial public areas where visual impact and ambient quality are prioritized. Premium brands are using sculptural forms and material finishes to lift the price mix in ceiling fixtures, evidenced by Kichler’s Larousse chandelier range positioned between USD 1,889 and USD 4,599. Hinkley’s Fantine series underscores how artisan finishes and high-touch construction engage affluent renovators and specification buyers. Catalog expansion by European brands such as EGLO is broadening access to curated styles, which supports assortment depth across online and specialty channels. In healthcare and office applications, wellness-driven specifications are increasing the use of tangible and low-glare solutions in ceiling formats, aligned with contemporary codes and voluntary standards.

Table and floor lamps benefit from sustained work-from-home patterns, motivating purchases that blend task utility with decorative appeal. This subcategory also serves as a primary canvas for designer collaborations and seasonal refreshes, which supports repeat purchases in the decorative lighting market. Foscarini’s recent launches exemplify interchangeable elements and distinctive silhouettes that resonate in design-centric retail and online merchandising. Specialty wall-mounted fixtures, such as picture lights and sconces, continue to expand as homeowners and commercial operators refine layered lighting plans for zones and vignettes. Brands also extend color temperature selectability and dimming ranges across product families to align with wellness and ambiance goals without requiring complex controls. Standards like IEC 60598 and ANSI C78.79 frame safety and performance fundamentals in retrofit and new luminaire designs, which help de-risk purchase and installation decisions across categories.

By Light Source: LED Dominance Solidifies, OLED Emerges in Niche Premium Roles

LED technology accounted for 70.12% of the light-source mix in 2025, while OLED and solar solutions are projected to post a 4.88% CAGR through 2031. The decorative lighting market is shifting from technology substitution toward feature enrichment as LED reaches dominance in developed economies. Signify’s connected installed base provides a scale reference for LED platforms that now anchor whole-home and whole-building solutions with software-defined features. On the frontier, OLED technologies emphasize thin, diffuse, and glare-free emission to unlock new form factors in premium ambient and accent applications. Universal Display Corporation reports cumulative power savings from phosphorescent OLED emitters across the color spectrum that position OLED for selective use cases where aesthetic benefits outweigh cost premiums. Solar-LED hybrids continue to serve off-grid and sustainability-oriented buyers, and manufacturers are incorporating these into decorative elements for outdoor living and balcony spaces[4]. Technical boundaries are still being pushed in LED efficacy, illustrated by OPPLE’s 230 lm/W module development, though decorative differentiation is increasingly shifting toward controls, optics, and design.

Regulatory momentum is reinforcing LED’s status as the baseline choice across geographies, which steers R&D and SKU development in the decorative lighting market. Energy codes, safety standards, and labeling norms are aligning specification behavior on LED solutions, while OLED remains a niche premium material that enriches specific product families. Over the forecast period, growth drivers move to smart features, tunability, and integration with wellness goals, rather than raw lumen-per-watt improvements. Those dynamic lift systems are valuable for connected LED luminaires in upscale residential and commercial projects. Decorative product roadmaps are therefore emphasizing aesthetics, controls interoperability, and modularity, which reflects a mature LED core and selective exploration of OLED and solar in design-forward niches.

By End-User: Residential Dominates Share, Commercial Accelerates on Wellness Retrofits

Residential end-users held 59.65% share in 2025, while commercial spaces are projected to expand at 5.55% CAGR through 2031. Residential demand centers on kitchen, dining, and bedroom zones where decorative fixtures are both focal design elements and functional light sources. Premiumization trends and the adoption of smart control features are influencing replacement decisions and new builds, particularly in urban and high-income segments. Households that are invested in work-from-home setups continue to refine task and ambient layers through table, floor, and wall-mounted accents. In cost-sensitive segments, integrated LED ceiling lights and long-life bulbs support lower maintenance and consistent light quality across rooms. Solar-enhanced decorative products address outdoor and balcony use, a niche that resonates with sustainability-minded buyers.

Commercial end-users are pivoting toward experience and wellness as core design narratives that shape decorative lighting choices. Hospitality is a key vector, where lobbies, dining spaces, and guest rooms rely on statement fixtures and dimming curves to shape ambiance for brand identity. Offices and mixed-use spaces are adopting tunable white and sensor-integrated luminaires to support circadian goals and energy codes, which elevates the specification of smart-ready decorative fixtures. Retail environments continue to value high-CRI and glare control in decorative elements that frame merchandise while shaping the customer journey. The decorative lighting market size for commercial projects is projected to expand to a 5.55% CAGR between 2026 and 2031 as upgrades align with code, ESG, and tenant-experience priorities.

By Distribution Channel: Omnichannel Retail Dominates, Online Surges on Assortment Depth

B2C retail channels accounted for 63.92% of revenue in 2025, while online sub-channels are expected to grow at a 4.98% CAGR through 2031. Modern assortment architecture now spreads across hypermarkets, home centers, specialty showrooms, and brand sites, with digital surfaces enabling richer discovery and content. EGLO’s roll-out of comprehensive digital catalogs has widened the reach for European styles in North America and beyond, reinforcing the value of digital merchandising in decorative categories. Home centers are expanding private labels, which exerts price pressure on mid-market national brands and accelerates the channel shift toward online and project specification. Company disclosures indicate that branded retail sell-through can lag when private labels take precedence on shelves, further nudging brands into direct and professional channels. The decorative lighting market rewards brands that can serve both comparison-driven online buyers and service-intensive showroom customers with consultative sales. Post-purchase support and installation content are also becoming decisive, especially for larger fixtures that represent meaningful investments for homeowners and businesses.

Online marketplaces and direct-to-consumer sites are improving visualization and configurators that help consumers assess scale, finish, and light quality, which raises conversion for higher-value decorative purchases. This is particularly important for pendants and chandeliers, where proportion and finish are prominent in decision-making. Brands that invest in product detail pages, style guides, and compatibility documentation see stronger engagement, while poor content or limited attributes can suppress discovery even with strong aesthetics. Digital operations also allow faster reaction to trend cycles, enabling agile SKU introductions and retirements that align with seasonal design narratives. As fulfillment networks mature, delivery reliability and damage mitigation in packaging become part of the brand experience, which matters more for large decorative fixtures. Overall, omnichannel execution is a competitive differentiator in the decorative lighting market as assortment breadth, content quality, and service intersect to guide share shifts.

Geography Analysis

Asia-Pacific held 35.70% of the decorative lighting market share in 2025 and is forecast to post the fastest regional growth at 5.98% CAGR through 2031. Scale advantages in manufacturing, rapid urbanization, and continued infrastructure investment sustain above-global growth in core markets. Policy support has been an enduring driver, with national and regional programs across Asia-Pacific moving procurement and standards toward LEDs, which then pull through into decorative segments. India’s policy framework and manufacturing incentives are expanding domestic capability from components to finished luminaires, while premiumization and smart adoption are lifting value in urban centers. Company disclosures reinforce this trajectory, with Havells’ lighting portfolio showing resilience in value-added segments even as base prices softened, supported by innovations such as Vita Dlight and smart offerings. OEM investment footprints in Southeast Asia, such as expansions in Vietnam, add supply chain flexibility for exports and regional projects in decorative categories.

North America remains a large, sophisticated buyer base where codes and standards continue to steer upgrades and connected adoption in the decorative lighting market. The DOE’s 2028 efficacy rules for general service lamps are expected to reinforce LED as the default choice, accelerating replacement of legacy technologies in both homes and businesses. In commercial settings, the 2024 IECC expands control requirements, aligning decorative lighting specifications with energy outcomes and occupant comfort goals. Major incumbents report stable project demand in intelligent spaces, with recent results from Acuity referencing momentum tied to integrated controls and platform strategies. Manufacturing footprints in the region are also broadening as companies diversify supply chains to enhance lead-time reliability for specification and retail channels. This environment supports mid-single-digit growth as regulatory compliance, renovation cycles, and smart-home integrations sustain investments in decorative categories.

Europe’s replacement activity is anchored by the phase-out of mercury-containing fluorescents under Ecodesign and RoHS frameworks, which lifts the LED share in decorative applications. Industry associations indicate residential LED penetration will approach near-universal levels by 2030, aligning with circularity expectations that encourage repairability and documentation across fixtures. Regional brands are investing in North American capabilities to access growth, as illustrated by EGLO’s decision to establish a larger United States base for design and distribution operations. Across South America, user-provided forecasts point to a 4.1% CAGR through 2031, while the Middle East and Africa are set to grow 4.6–5.0% on hospitality projects and off-grid solar-LED adoption. South Africa’s minimum performance requirements for general service lamps further accelerate LED preference, reinforcing regional alignment with global efficiency trajectories.

Competitive Landscape

The decorative lighting market is fragmented, and competition remains intense across price tiers and channels. Scale players deploy multi-brand strategies to serve consumer, professional, and connected segments, while design houses focus on distinctive aesthetics and collaborations. Signify reported USD 6.78 billion (EUR 5.77 billion) in sales in 2025 across categories, with comparable sales declining by 3.4%, underscoring the pressure in non-connected consumer lines even as connected ecosystems stay resilient. USD 6.78 billion (EUR 5.77 billion) is equivalent to USD 6.2 billion. Acuity Brands posted USD 4.3 billion in fiscal 2025 revenue, supported by Intelligent Spaces momentum and portfolio extension into integrated controls following its QSC acquisition. Havells showed lighting growth in India tied to wellness features and smart introductions, supporting contribution margins in a price-deflationary environment.

Strategic emphasis is coalescing around ecosystem building, software-enabled value, and compliance-readiness. Signify’s large, connected base solidifies a services and accessories flywheel that benefits decorative categories, where aesthetics and software work together to shape the experience. Acuity continues to allocate capital toward platforms that extend beyond illumination to space intelligence, positioning decorative fixtures within an integrated envelope for commercial clients. European brands such as EGLO are expanding manufacturing and distribution footprints in North America to capture growth in omnichannel and project channels. In Asia-Pacific, OPPLE’s R&D investments, including USD 42.84 million (RMB 300 million) in 2024, reflect sustained innovation capacity and patent activity that support performance at scale.

Differentiation paths in the decorative lighting market cluster into three themes. First, design-forward portfolios that prioritize finishes, sculptural forms, and curated collections earn durable premiums in the consumer and hospitality arenas. Second, connectivity and control ecosystems are unlocking software-defined value that supports recurring revenue and specification loyalty. Third, operational agility and omnichannel execution enable faster reaction to trend cycles and digital merchandising standards, which increasingly drive purchase behavior. Compliance alignment across IEC safety norms and region-specific codes further differentiates brands that can update SKUs rapidly and document traceability, enhancing credibility with specifiers and regulators. Collectively, these strategies determine who captures share as the decorative lighting market evolves through 2031.

Decorative Lighting Industry Leaders

Signify (Philips, Hue, WiZ)

Acuity Brands (Lithonia, Juno, Aculux, Peerless, Gotham)

LEDVANCE (Sylvania, LEDVANCE)

OPPLE Lighting

EGLO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: EGLO released a broad set of digital catalogs for Interior Lighting 2025/26, Outdoor Luminaires 2026/27, Portables 2026/27, and other lines to support omnichannel demand.

- August 2025: Havells Lighting LLC and Krut LED LLC opened a United States manufacturing and distribution hub in Anderson, South Carolina, to serve North American projects.

- June 2025: Signify introduced Philips GrowWise smart spectrum to optimize horticultural LED lighting based on real-time sunlight conditions, with potential transferability to human-centric tuning in residential contexts.

- April 2025: Havells India agreed to invest USD 71 million in Goldi Solar Private Limited to strengthen access to solar modules and inverters, with an expected stake approaching 9%.

Global Decorative Lighting Market Report Scope

Decorative lighting refers to lighting fixtures designed primarily for aesthetic appeal while also providing functional illumination in interior or exterior spaces. These lighting solutions enhance ambiance, interior décor, and architectural elements in residential and commercial environments. The decorative lighting market includes a wide range of fixtures such as lamps, chandeliers, wall lights, and designer fittings that combine style, material innovation, and lighting technology.

The decorative lighting market is segmented by product type, light source, distribution channel, end-user, and geography. By product type, the market is divided into table and floor lamps, ceiling lights and chandeliers, wall-mounted fixtures, light bulbs and fittings, and other products. By light source, the market includes LED, incandescent, fluorescent and CFL, halogen, and other lighting technologies. By distribution channel, the market is segmented into B2C/retail and B2B/direct sales and projects. By end-user, the market is categorized into residential and commercial segments. Geographically, the market analysis covers North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The report provides market size and forecasts for the decorative lighting market in value (USD) across all the above segments.

By Product Type

| Table & Floor Lamps |

| Ceiling Lights & Chandeliers |

| Wall-Mounted Fixtures |

| Light Bulbs & Fittings |

| Other Products (Pendant, Strip & Rope, Spot, Track etc.) |

By Light Source

| LED |

| Incandescent |

| Fluorescent & CFL |

| Halogen |

| Others (OLED, Solar, etc.) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Hypermarkets and Supermarkets |

| Home Centers | |

| Specialty Lighting Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct Sales & Projects |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Table & Floor Lamps | |

| Ceiling Lights & Chandeliers | ||

| Wall-Mounted Fixtures | ||

| Light Bulbs & Fittings | ||

| Other Products (Pendant, Strip & Rope, Spot, Track etc.) | ||

| By Light Source | LED | |

| Incandescent | ||

| Fluorescent & CFL | ||

| Halogen | ||

| Others (OLED, Solar, etc.) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Hypermarkets and Supermarkets |

| Home Centers | ||

| Specialty Lighting Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct Sales & Projects | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the decorative lighting market?

The decorative lighting market size stands at USD 75.88 billion in 2025 and is projected to reach USD 96.52 billion by 2031 at a 4.09% CAGR.

Which region leads to growth in decorative lighting through 2031?

Asia-Pacific leads with a 35.70% share in 2025 and the fastest forecast growth at 5.98% CAGR, supported by urbanization and strong manufacturing ecosystems.

What product types are gaining the most traction in decorative lighting?

Ceiling lights and chandeliers hold the largest share at 35.02% in 2025, while table and floor lamps show the fastest growth at 5.21% CAGR due to design-led purchases and home-office needs.

How are regulations shaping the decorative lighting market?

United States DOE efficacy rules for 2028 and European fluorescent phase-outs are accelerating LED adoption and replacement demand, favoring compliant, connected fixtures.

Which technologies and features are shaping competitive differentiation?

Connected ecosystems, tunable lighting for wellness, and premium design collaborations are leading differentiation and supporting higher value capture in decorative categories.

What channels will see the fastest growth in decorative lighting sales?

Online sub-channels within B2C are projected to grow faster than store-based retail due to broader assortments, rich content, and improved visualization tools.

Page last updated on: