Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

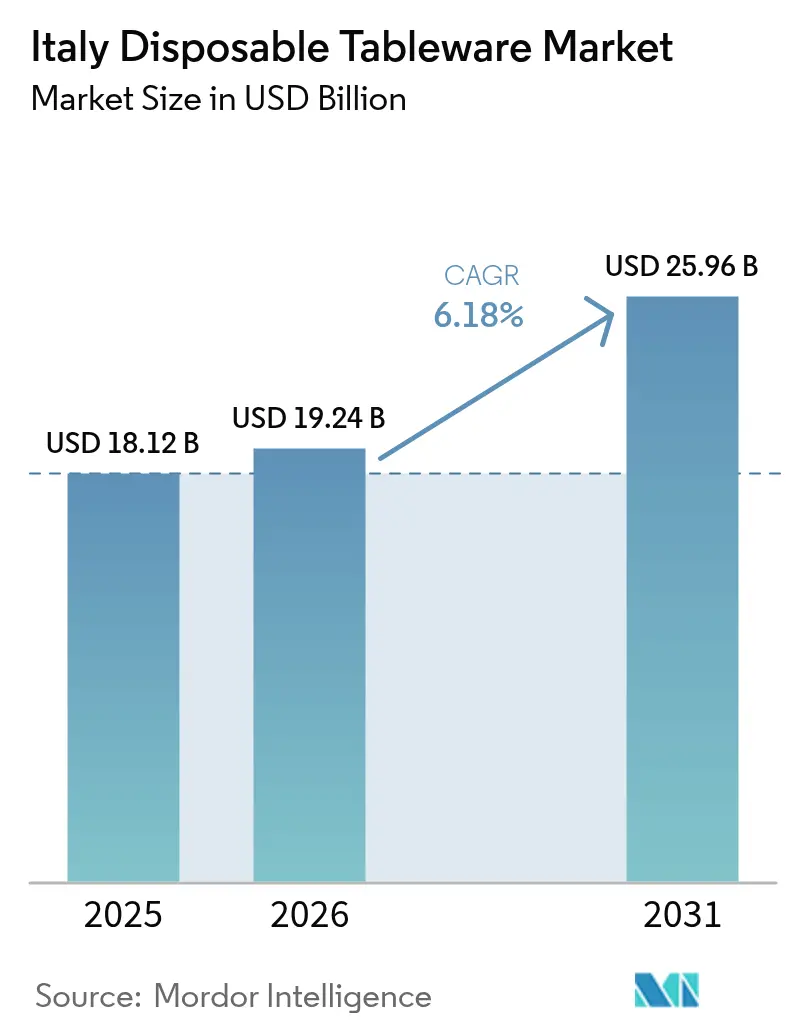

| Base Year Market Size (2025) | USD 18.12 Billion |

| Market Size (2026) | USD 19.24 Billion |

| Market Size (2031) | USD 25.96 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Disposable Tableware Market Analysis by Mordor Intelligence

The Italy disposable tableware market size was valued at USD 18.12 billion in 2025 and estimated to grow from USD 19.24 billion in 2026 to reach USD 25.96 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). The growth of Italy's disposable tableware market is primarily attributed to regulatory measures such as the EU Single-Use Plastics Directive and the implementation of Italy's EUR 0.45/kg (0.53/kg) MACSI plastic tax [1]European Commission, “Single-Use Plastics,” commission.europa.eu . Additionally, the sustained increase in food delivery services and outdoor dining occasions has significantly contributed to market expansion. The rising influx of tourists, coupled with intensified efforts to promote agritourism, has further bolstered demand. Investments in automated pulp-molding technologies are also playing a pivotal role in meeting this growing demand. Premium compostable tableware designs are increasingly being leveraged by brand owners as strategic marketing tools to enhance brand value and consumer appeal. Furthermore, the adoption of digital procurement platforms is streamlining supply chain operations by reducing replenishment cycles and expanding product assortments. These factors collectively drive capital investment into biopolymer compounding facilities and the development of regional distribution hubs, solidifying the market's growth trajectory.

Key Report Takeaways

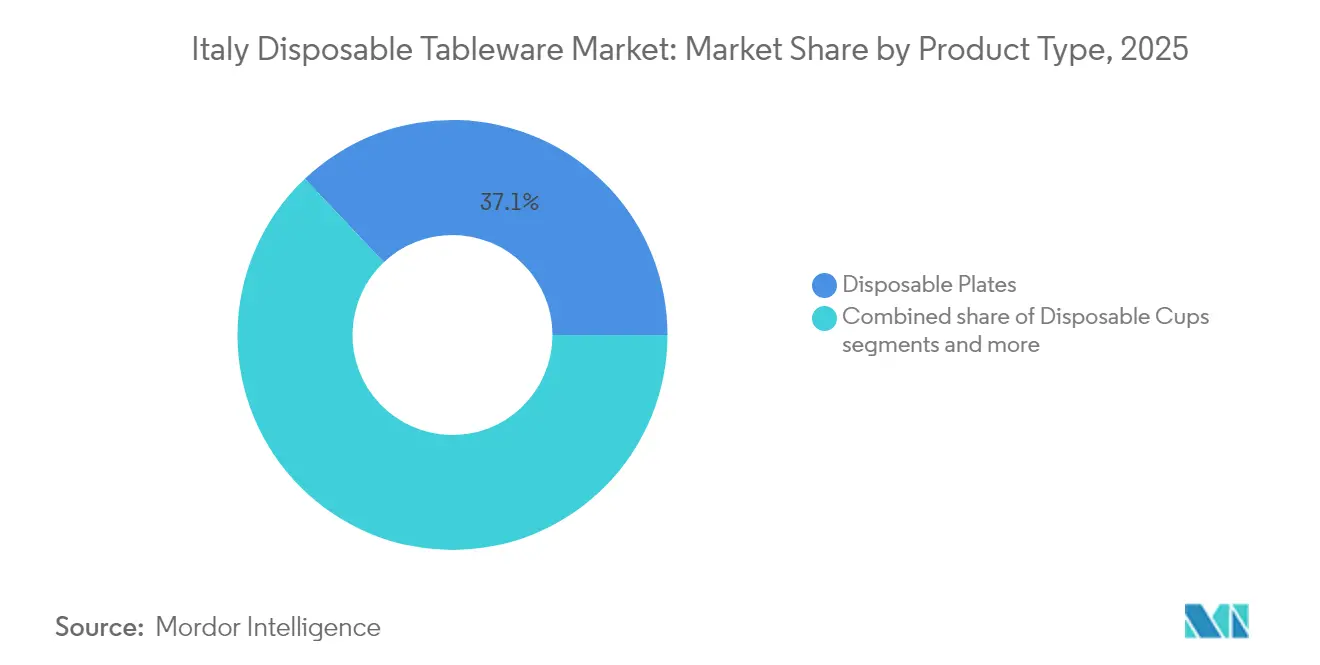

- By product type, disposable plates led with a 37.05% share of the Italy disposable tableware market in 2025, while disposable bowls are projected to expand at a 8.76% CAGR through 2031.

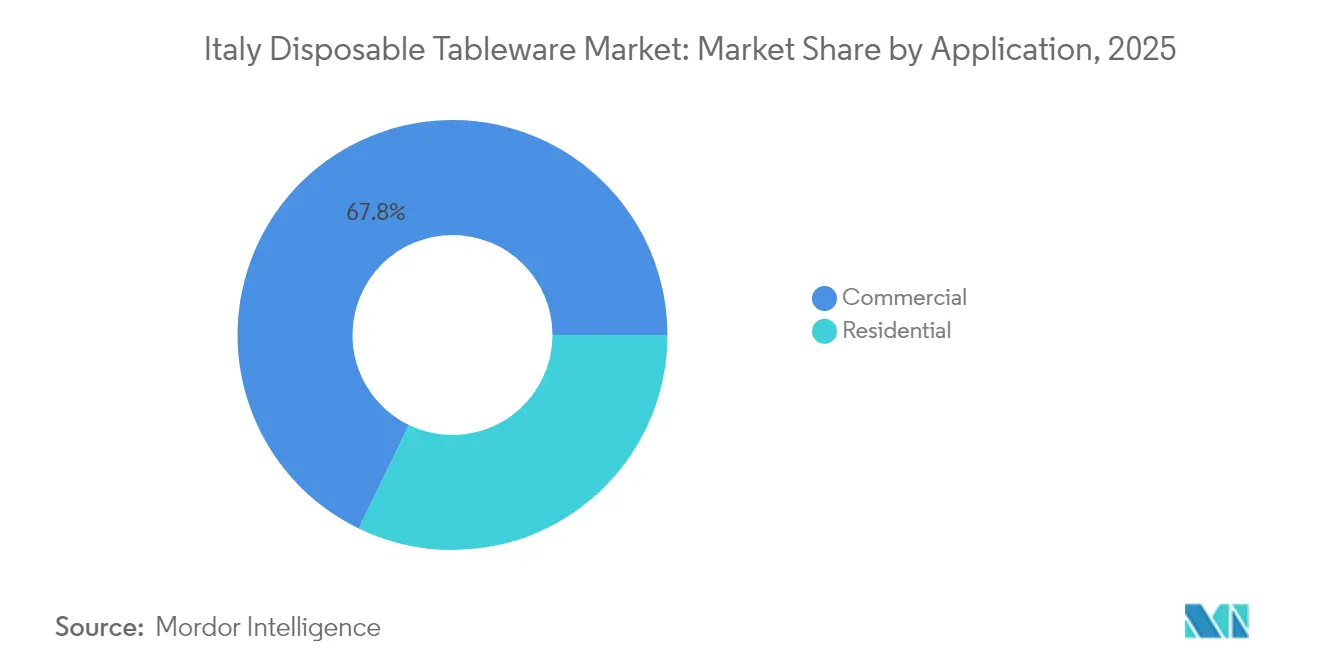

- By application, the commercial segment accounted for 67.82% of the Italy disposable tableware market share in 2025; online/direct-to-consumer recorded the fastest 11.65% CAGR outlook to 2031.

- By distribution channel, hypermarkets and supermarkets commanded 47.05% of the Italy disposable tableware market size in 2025, whereas online channels are set to grow at 11.92% CAGR through 2031.

- By geography, Northwest Italy held 38.88% of the Italy disposable tableware market in 2025, while South & Islands is advancing at an 7.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Disposable Tableware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU single-use plastics (SUP) directive enforcement | +1.8% | National, with stronger enforcement in Northern regions | Medium term (2-4 years) |

| Surge in outdoor catering & food-delivery occasions post-COVID-19 | +1.5% | National, concentrated in urban centres and tourist areas | Short term (≤ 2 years) |

| Premiumisation of eco-friendly tableware in the HoReCa channel | +1.2% | Northwest and Central Italy, expanding to the South | Medium term (2-4 years) |

| Growth of agritourism & open-air events in Central & Southern Italy | +0.9% | Central Italy and South & Islands regions | Long term (≥ 4 years) |

| Retailer private-label expansion in compostable SKUs | +0.7% | National, led by major retail chains | Short term (≤ 2 years) |

| Automated thermoforming & pulp-moulding lines lowering unit costs | +0.6% | Manufacturing regions in the North, cost benefits nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Single-Use Plastics Directive Enforcement Accelerates Material Transition

Italy’s transposition of the EU Single-Use Plastics Directive bans expanded polystyrene food containers and widens producer responsibility, making virgin plastics uneconomic relative to compostable substrates. Simultaneous application of the MACSI tax tightens margins for legacy resin users, pushing distributors and foodservice chains toward PLA, bagasse, and paper-pulp options. Domestic biopolymer leader Novamont reported double-digit order growth for Mater-Bi compounds in 2025, evidencing early-mover advantage. Northern municipalities supervise enforcement more strictly, creating a geographic pull for compliant inventory. Firms investing ahead of the curve secure shelf space and lock in price premiums, whereas laggards encounter immediate share erosion.

Post-COVID Surge in Outdoor Catering and Food Delivery Transforms Consumption Patterns

The persistence of restaurant terraces, kiosks, and delivery formats, initially implemented to comply with distancing mandates, highlights a significant shift in consumer preferences even after the removal of restrictions. FIPE reported a notable increase in take-away concepts between 2024 and 2025, reflecting the growing demand for convenient dining options. Concurrently, foodservice distributor MARR maintained stable revenue levels in Q3 2024, despite experiencing a minor decline in traditional dine-in services. Industry operators have strategically adapted by incorporating innovative packaging solutions, such as heat-retaining lids, tamper-evident seals, and durable fiber bowls, to enhance the efficiency and reliability of food transport. Furthermore, key tourist destinations, including Rome, Florence, and coastal resorts, have extended outdoor-seating permits, effectively integrating disposable tableware into routine operations. This shift has resulted in the Italian disposable tableware market achieving a sustained increase in baseline volume, even as consumer traffic returns to indoor dining establishments.

HoReCa Premiumization Drives Eco-Friendly Tableware Adoption

Hospitality brands increasingly use compostable plates embossed with logos or artisanal textures to signal sustainability credentials. Consumer surveys show three-quarters of Italians view climate change as an urgent concern, with nearly half basing purchase choices on environmental impact. Premium eco-friendly items cost more than conventional plastic yet gain traction because they satisfy regulation, marketing, and customer experience simultaneously. Northwest Italy sets the tone owing to higher disposable incomes and international patronage, but demand is spreading south as luxury agritourism venues and boutique beach clubs aim to elevate guest perception. Manufacturers respond with bagasse designs resembling ceramic and PLA-lined paper cups suitable for espresso service.

Agritourism Growth in Central and Southern Italy Creates Niche Demand

Rural hospitality properties promote alfresco dining amid vineyards and olive groves, preferring tableware that complements farm-to-table positioning. The National Recovery and Resilience Plan steers funds toward experiential tourism, sparking new venues that require compostable wares aligned with circular-economy messaging. Central Italy’s UNESCO landscapes seek premium aesthetics, whereas Southern operators balance cost and authenticity using molded-fiber trays sourced from nearby mills. Suppliers catering to this channel enjoy seasonal peaks during harvest festivals and wine events, diversifying revenue beyond city-centre foodservice[2]OECD, “Improving Plastics Management,” oecd.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile biopolymer feedstock prices (PLA, bagasse) | -1.1% | National, affecting all market segments | Short term (≤ 2 years) |

| Limited industrial composting capacity south of Rome | -0.8% | Central Italy and South & Islands regions | Long term (≥ 4 years) |

| Consumer push-back on perceived "green-washing" claims | -0.6% | National, more pronounced in educated urban markets | Medium term (2-4 years) |

| Rising penetration of reusable rental tableware services | -0.4% | Urban centres, particularly Milan, Rome, Naples | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biopolymer Feedstock Price Volatility Constrains Market Expansion

During the forecast period of 2024–2025, the costs of corn-based PLA and sugarcane bagasse exhibited significant fluctuations, driven by crop cycle variations and persistent logistical disruptions. Larger Italian converters adopted risk mitigation strategies such as supplier diversification and inventory pre-purchasing to manage these cost swings effectively. However, smaller firms faced heightened financial strain due to limited cash flow, leaving them more vulnerable to market volatility. The imposition of sudden surcharges often impacted caterers, occasionally delaying planned menu enhancements. In response, industrial buyers increasingly sought extended price lock agreements, effectively transferring the financial risk to producers. To address these challenges and stabilize supply chain dynamics, Novamont announced plans to expand its Mater-Bi production capacity in Terni. This strategic initiative aims to reduce transportation distances and achieve improved economies of scale, thereby mitigating cost volatility and enhancing operational efficiency.

Limited Industrial Composting Infrastructure South of Rome Impedes Circular Economy

Northern regions hold the bulk of Italy’s 3.9 million ton annual composting capacity, while Central and Southern provinces rely on longer haul routes or landfill alternatives[3]Banca d’Italia, “Regional Economies,” bancaditalia.it. Municipal collection systems often mix organic and residual waste, lowering feedstock purity and discouraging facility investment. Without nearby processors, restaurants hesitate to pay premiums for compostables that ultimately enter general waste. The government has earmarked PNRR funds for seven new plants, yet completion dates extend into 2028. Until capacity equalizes, the Italy disposable tableware market must balance end-of-life claims with on-the-ground realities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Material innovations widen functional scope

Disposable plates retained a 37.05% share of the Italy disposable tableware market in 2025, underscoring their ubiquity for pizza slices, antipasti, and buffet service. Bowls, however, post the fastest 8.76% CAGR because salad bars, poke outlets, and soup kiosks favour deep-walled formats that prevent spillage during delivery. The Italy disposable tableware market for plates is projected to experience steady growth by 2025, driven by the decreasing costs of molded-fiber tooling. This reduction in production costs is anticipated to enhance market accessibility and encourage broader adoption of disposable plates across various end-user segments. Demand for bowls benefits from health-forward menus and convenience meals popular among urban professionals.

Manufacturers differentiate through geometry, vented lids for hot broths, compartment designs for grain bowls, and through coatings that eliminate PFAS while maintaining grease resistance. Silverware growth stays moderate because reusable cutlery rentals gain share at corporate cafeterias, yet bundled sets remain essential for takeaway. Specialty items such as compartment trays, clamshells, and micro-ovenable dishes address niche catering requirements, supporting incremental revenue. High-volume manufacturing facilities located in Lombardy and Veneto utilize advanced automated pulp-molding presses, which significantly reduce cycle times. This operational efficiency enhances the cost-effectiveness of producing sustainable substrates, aligning with the growing demand for environmentally friendly materials in the market.

By Application: Digital commerce upshifts procurement behavior

The commercial segment controlled 67.82% of the Italy disposable tableware market in 2025 as restaurants, caterers, hotels, and institutional feeders consumed steady volumes across multiple SKUs. Chains integrate demand planning with POS data to schedule pallet-level replenishment, driving efficiency in hypermarket and cash-and-carry channels. Simultaneously, online/direct-to-consumer ordering is on track for a 11.65% CAGR, propelled by meal-kit subscriptions, ghost kitchens, and grocery platforms bundling tableware with prepared foods. The Italian disposable tableware market size for online applications is set to double by 2030, aided by low-order-minimum portals tailored to micro-entrepreneurs.

Residential demand remains resilient thanks to seasonal celebrations, park picnics, and casual gatherings on balconies where dishwashing space is limited. Even so, e-commerce absorbs a rising share of household purchases via same-day delivery. Commercial buyers prioritize durability and cost-per-use, whereas households lean toward aesthetics and composability claims. Compliance with EU food-contact rules and ISCC PLUS certification now appear on bid checklists, making traceable sourcing a ticket to participate in public tenders.

By Distribution Channel: Omnichannel strategies redefine reach

Hypermarkets and supermarkets represented 47.05% of the Italy disposable tableware market in 2025, leveraging national footprints and promotional cycles timed around Easter, summer holidays, and December festivities. Their dominance rests on scale purchasing, private-label rollouts, and in-store displays that educate shoppers on recycling symbols. However, online marketplaces will expand at a 11.92% CAGR, eroding share from brick-and-mortar as restaurateurs embrace one-click restocking. E-tail platforms such as Eco to Go and mainstream grocers’ web shops now list SKU-level environmental attributes, allowing buyers to filter by composability or recycled content.

Convenience stores capture impulse demand from tourists and office workers in transit hubs, while wholesale distributors retain importance for small towns lacking big-box outlets. Direct sales by manufacturers grow selectively for high-volume clients requiring bespoke embossing. Across channels, EU regulations mandating digital passports for packaging from 2026 onward accelerate investment in traceability systems that record resin origin, recyclability, and end-of-life guidance.

Geography Analysis

Northwest provinces generated nearly two-fifths of the 2025 value, reflecting higher household income, dense restaurant networks, and mature waste management. Regional agencies report organics diversion above half, making certified compostable plates a logical fit. The local business climate also favours automation, with several Lombardy plants installing high-speed pulp-molding lines that raise output and cut labour expense.

Northeast and Central territories post mid-single-digit growth as tourism and public-sector catering stabilize post-pandemic. Venice cruise traffic and Emilia-Romagna food processors maintain baseline volume, while university campuses in Bologna and Florence pilot reusable-versus-compostable trials that influence procurement choices across the peninsula.

South & Islands, though currently smaller in absolute spending, outpaces the national average thanks to coastal resort openings, agritourism ventures, and expanded airport routes. Logistics hurdles and limited composting capacity temper full-scale adoption of bio-plastics, so fibre-based plates coated with water-based barriers serve as interim solutions until new processing plants come online by 2028. Targeted investment in collection infrastructure will be decisive for translating latent demand into realized sales.

Competitive Landscape

The top five suppliers collectively held more than half of the 2024 revenue, signifying a moderately concentrated field. Incumbents leverage long-standing retail relationships, vertically integrated resin production, and proprietary tooling to protect share. Novamont's expansion in Terni enhances its upstream integration by improving control over Mater-Bi feedstock, a critical input for its bioplastics production. Similarly, deSter's strategic acquisition of Nupik strengthens its manufacturing capabilities in Southern Europe, ensuring a robust supply chain to meet regional demand. Furthermore, DOpla Group's attainment of ISCC PLUS certification positions the company as a preferred partner for airlines and quick-service chains, which prioritize cradle-to-gate traceability in their procurement processes.

Mid-tier regional specialists exploit localized preferences, offering small batch runs and rapid design changes for wedding caterers and festival organizers. Some producers incorporate recycled pulp sourced from Veneto paper mills, reducing exposure to volatile imported bio-plastics. Emerging competitors include rental-service platforms that supply reusable dishware to stadiums and concert venues, potentially capping single-use volumes in dense metropolitan areas.

Technology investment remains the principal differentiator. Automated thermoformers enhance operational efficiency by minimizing scrap rates and offering a wider range of shape configurations. Concurrently, digital printing facilitates brand differentiation through personalized designs, eliminating the requirement for separate labeling processes. Firms unwilling to retool face commoditization pressures and may pivot toward contract manufacturing or private-label supply for grocery groups.

Italy Disposable Tableware Industry Leaders

Flo SpA

DOpla SpA

Huhtamaki Oyj

Duni AB

Sabert Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Mondi has initiated operations at its Duino mill, marking a significant milestone. This development reinforces the company's position as a key player in the production of high-quality, sustainable packaging solutions, while contributing to its long-term value generation strategy.

- September 2024: Coop Italia widened its assortment with more than 5,000 eco-friendly SKUs—including compostable plates, cups, and cutlery- to meet surging consumer demand for greener single-use options.

- February 2024: deSter completed the acquisition of Spanish packaging firm Nupik, enlarging its European production footprint for sustainable tableware.

- February 2024: Berry Global introduced RFID-enabled reusable dishware systems for European food-service clients, positioning the line as a high-cycle alternative to single-use items in Italian stadiums and corporate cafeterias.

Italy Disposable Tableware Market Report Scope

Disposable tableware products, intended for one-time use, consist of coated or plastic resins. These products are predominantly employed in dining settings, encompassing beverages, dishes, cups, bowls, and platters. A complete background analysis of the Italian disposable tableware market, including an assessment of the disposable tableware market in Italy, emerging trends by market segments, and significant changes in market dynamics, is covered in the report.

The Italian disposable tableware market is segmented by product type, application, and distribution channel. The market is segmented by product types, such as disposable cups, disposable plates, disposable bowls, disposable silverware, and other product types. By application, the market is segmented as residential and commercial. Under the distribution channel segment, the market is segmented into hypermarkets and supermarkets, convenience stores, online stores, and other distribution channels. The report gives market size and forecasts for Italy's disposable tableware market in value (USD) for all the above segments.

By Product Type

| Disposable Cups |

| Disposable Plates |

| Disposable Bowls |

| Disposable Silverware |

| Other Product Types |

By Application

| Residential |

| Commercial |

By Distribution Channel

| Hypermarkets and Supermarkets |

| Convenience Stores |

| Online |

| Other Distribution Channels |

By Geography

| Northwest Italy |

| Northeast Italy |

| Central Italy |

| South & Islands |

| By Product Type | Disposable Cups |

| Disposable Plates | |

| Disposable Bowls | |

| Disposable Silverware | |

| Other Product Types | |

| By Application | Residential |

| Commercial | |

| By Distribution Channel | Hypermarkets and Supermarkets |

| Convenience Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Northwest Italy |

| Northeast Italy | |

| Central Italy | |

| South & Islands |

Key Questions Answered in the Report

What will the Italy disposable tableware market be worth by 2031?

It is projected to reach USD 25.96 billion, expanding at a 6.18% CAGR from 2026.

Which product type generates the highest revenue in Italy’s disposable tableware space?

Disposable plates lead with a 37.05% share of the 2025 value.

Which regional block is growing the fastest for disposable tableware sales?

South & Islands is forecast to rise at an 7.95% CAGR through 2031.

Why are compostable materials gaining traction among Italian food-service operators?

EU single-use plastics curbs, the national EUR 0.45/kg MACSI tax, and consumer preference for eco-friendly choices favour compostable products.

What supply-side risk could slow expansion over the next two years?

Volatile prices for PLA and bagasse feedstocks may squeeze margins and delay purchasing decisions.

How concentrated is competition among suppliers?

The top five companies control roughly a little more than half of the 2024 revenue, indicating moderate concentration with room for mid-sized challengers.

Page last updated on: