Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

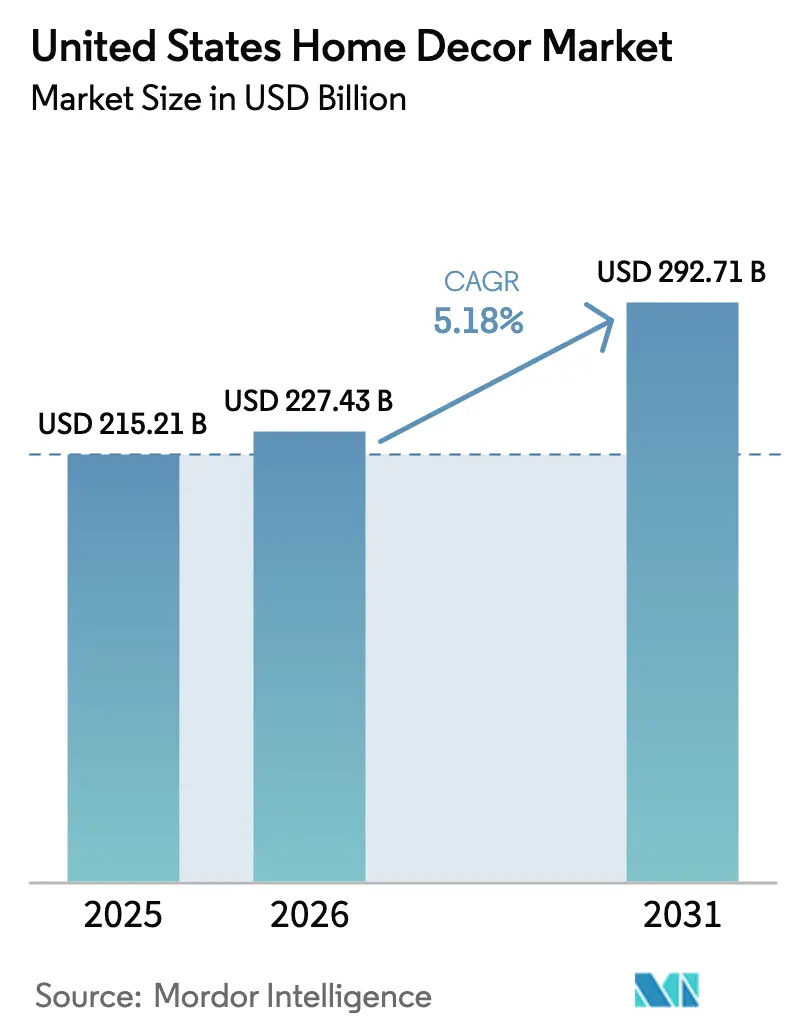

| Base Year Market Size (2025) | USD 215.21 Billion |

| Market Size (2026) | USD 227.43 Billion |

| Market Size (2031) | USD 292.71 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Home Decor Market Analysis by Mordor Intelligence

The United States home decor market is expected to increase from USD 215.21 billion in 2025 to USD 227.43 billion in 2026 and reach USD 292.71 billion by 2031, growing at a CAGR of 5.18% over 2026-2031. The United States home Decor market is experiencing steady growth driven by long-term structural trends rather than short-term cyclical factors. Aging housing stock is prompting increased renovation activity, while remote work patterns are reshaping how consumers utilize and furnish their homes. Home office furniture and Decor are emerging as high-growth segments, reflecting the persistence of hybrid work and the repurposing of residential spaces. Sustainability is becoming a key factor, with eco-friendly materials and certifications influencing both product development and consumer purchase decisions.

Digital transformation is accelerating, as online and e-commerce channels gain share alongside traditional retail stores, supported by technology-enabled fulfillment and discovery tools. Premium and luxury segments are expanding as affluent consumers prioritize craftsmanship, customization, and high-quality design. Market fragmentation allows specialized players to capture niche demand, while competitive pressures across price bands encourage innovation in logistics, customer experience, and digital engagement. Overall, the market’s growth is anchored in behavioral shifts, technological adoption, and the need for functional, sustainable, and aesthetically appealing home environments.

Key Report Takeaways

- By product type, furniture led with 39.36% of the United States home decor market size in 2025, while home office furniture and decor are projected to expand at an 11.87% CAGR through 2031.

- By material, wood held 44.44% of the United States home decor market share in 2025, and sustainable and reclaimed wood variants are set to grow at a 10.29% CAGR through 2031.

- By distribution channel, home-improvement and furniture stores held 46.74% of the United States home decor market share in 2025, while online and e-commerce are advancing at a 12.84% CAGR through 2031.

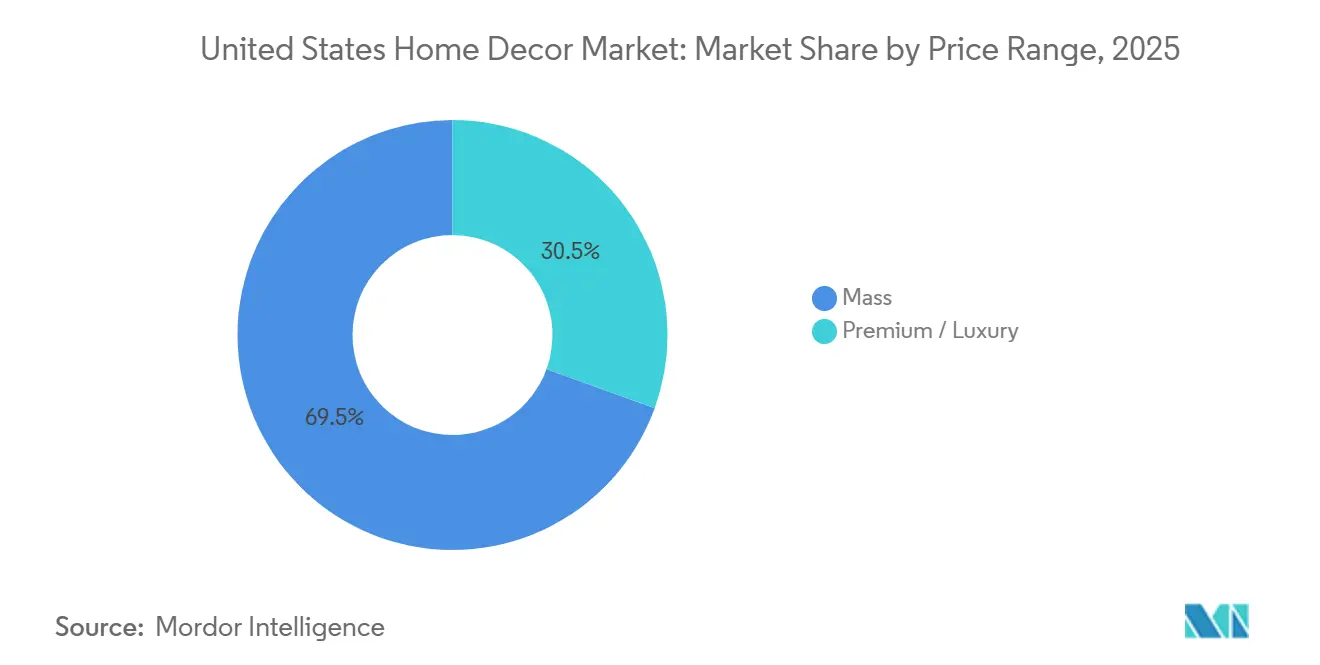

- By price range, mass-market accounted for 69.47% of the United States home decor market share in 2025, while premium and luxury segments are projected to grow at a 9.24% CAGR through 2031.

- By room, living rooms held 30.37% of the United States home decor market share in 2025, while home offices are expanding at an 11.87% CAGR through 2031.

- By geography, the South region accounted for 35.87% of the United States Home Decor Market share in 2025, while the West region is projected to advance at an 8.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Home Decor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging United States Housing Stock Supporting Renovation-Driven Décor Spending | 1.2% | Global, with the strongest impact in the Northeast (median age 60 years) and the Midwest (50 years) per U.S. Census data | Medium term (2-4 years) |

| Expansion in Single-Family Housing Starts and Existing Home Sales | 0.8% | National, with early gains in the South (35.87% market share) and the West (8.84% CAGR growth regions) | Short term (≤ 2 years) |

| Remote Work Driving Increased Home Office Décor Investment | 1.5% | National, with the strongest impact in knowledge-worker hubs (San Francisco, Austin, Boston, New York) | Long term (≥ 4 years) |

| Social Media–Influenced Trends Accelerating Décor Purchase Cycles | 0.7% | National, with spillover to suburban markets adopting Instagram/TikTok-driven aesthetics | Short term (≤ 2 years) |

| Omnichannel and AR Shopping Enhancing the Customer Experience | 1.1% | National, concentrated in metropolitan areas with high smartphone penetration and broadband access. | Medium term (2-4 years) |

| Sustainability and Eco-Conscious Preferences Driving Green Décor Demand | 0.9% | National, strongest in coastal regions (West, Northeast), with environmental consciousness | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging United States Housing Stock Supporting Renovation-Driven Décor Spending

The aging United States housing stock is a key driver of renovation-led spending in the home decor market. Housing starts finished 2024 on a strong upward trend, with single-family construction showing notable resilience, even as multifamily development remained mixed. The National Association of Home Builders reported that overall starts rose to a 1.50 million annualized pace in December, the highest level since early 2024. This increase was driven by resilience in single‑family construction, which grew to just over 1 million units, even as multifamily development showed mixed results. For the full year 2024, total housing starts reached about 1.36 million units, slightly lower than the previous year, while single‑family starts increased compared with 2023. Multifamily starts, however, ended the year down significantly, highlighting a shift in builder focus [1]National Association of Home Builders, “Housing Starts End 2024 on an Up Note,” NAHB, nahb.org. Federal Reserve data shows that home purchases trigger significant increases in home-related outlays, with renovation, repairs, and furnishings representing the largest categories. Emotional and experiential factors also drive spending, as homeowners invest in projects that enhance satisfaction and comfort. Kitchen and other major home upgrades often spark complementary decor purchases, reinforcing overall market growth. Overall, both structural housing trends and consumer behaviour combine to maintain steady demand for home decor and renovation-led expenditures in the United States.

Expansion in Single-Family Housing Starts and Existing Home Sales

The growth in single-family housing starts and existing home sales continues to support demand for home Decor. Single-family housing starts registered 890,000 units at a seasonally adjusted annual rate in August 2025, with completions rising 6.7% month over month and 5.6% year over year, reflecting ongoing pipeline conversion even as new permits remain weak. Strong completions contribute to higher occupancy and create immediate furnishing and Decor needs as new homes are delivered. New home sales reached 800,000 units in August 2025, while the months’ supply compressed to 7.4 months as builders used incentives to move inventory and sustain sales volume. The limited supply of available homes further stimulates demand for interior upgrades and Decor items. Rising single-family activity and healthy home sales reinforce opportunities for renovation, furnishing, and aesthetic enhancements. Homeowners and new buyers increasingly invest in decorating and personalizing their spaces, boosting overall market growth. This trend highlights the strong connection between housing activity and sustained expenditure in the U.S. home Decor sector [2]U.S. Census Bureau, “New Residential Sales Press Release,” U.S. Census Bureau, census.gov. Existing home sales showed a modest improvement toward the end of the year, supported by some relief in mortgage rates, though overall activity remained below previous peaks. This trend shifts demand toward renovation and refresh cycles rather than complete home furnishing projects. Looking ahead, housing starts are expected to remain steady, providing a stable foundation for the home Decor market as household formation and new deliveries continue. For brands and retailers, this environment emphasizes opportunities to partner with builders and showcase staged model homes.

Remote Work Driving Increased Home Office Décor Investment

Telework rates stabilized at 22.9% of employed persons in early 2024, confirming that hybrid work arrangements are enduring and that households will continue allocating space and budget to home office setups. This shift drives sustained demand for ergonomic seating, adjustable desks, lighting, storage solutions, and sound management as homes accommodate intermittent work throughout the week [3]U.S. Bureau of Labor Statistics, “Telework rates increased over the year at all levels of educational attainment, first quarter 2024,” U.S. Bureau of Labor Statistics, bls.gov. Productivity research and industry reports show that sectors with higher remote work adoption experienced output gains, reinforcing employers’ ongoing support for flexible work models. Telework is more prevalent among highly educated and higher-income professionals, concentrating demand for premium-quality home office furnishings. Additionally, hybrid work often extends into adjacent living and dining areas, creating opportunities for modular and multifunctional furniture that balances aesthetics with functionality. These dynamics collectively underpin a long-term growth trajectory for home office Decor that is expected to outpace traditional categories within the United States Home Decor market.

Omnichannel and AR Shopping Enhancing the Customer Experience

The rise of e-commerce continues to transform how consumers discover and purchase home Decor, with online sales growing faster than overall retail and solidifying the importance of digital channels. Despite this shift, physical stores remain critical for high-touch and bulky items, with home-improvement and furniture retailers continuing to play a central role in major purchases. Leading e-commerce players are investing in tools that help translate inspiration into actionable purchases, enhancing the shopping experience. Wayfair reported USD 11.85 billion in revenue for 2024, returned to top-line growth in the third quarter of 2025, and continues to invest in tools that translate inspiration into action for home categories [4]Wayfair Inc., “Wayfair Announces Third Quarter 2025 Results,” Wayfair Inc., investor.wayfair.com. In early 2026, Wayfair introduced a generative AI tool that produces photorealistic room scenes from text prompts, allowing customers to shop directly from these visualizations and shifting value from traditional search to guided curation. Similarly, Target has combined content and commerce by offering curated experiences through conversational interfaces, helping shoppers discover multi-item baskets across home Decor and other categories. These innovations highlight a broader trend of integrating speed, selection, visualization, and trusted in-store environments. By enhancing the shopping journey and making inspiration actionable, retailers are expanding the accessible consumer base. Collectively, AI-driven visualization and curated experiences are strengthening engagement and supporting sustained growth in the United States Home Decor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Lumber and Textile Costs Pressuring Margins | -0.9% | National, with heightened pressure in timber-dependent regions and textile import hubs | Short term (≤ 2 years) |

| Higher Mortgage Rates Constraining Home Turnover and Spending | -1.3% | National, with stronger effects in high-cost metros where turnover is most constrained | Long term (≥ 4 years) |

| Supply Chain Bottlenecks Elevating Lead Times and Inventory Expenses | -0.7% | National, with an acute impact on coastal ports and import-dependent regions | Medium term (2-4 years) |

| Rising Inflation Reducing Consumer Discretionary Purchases | -0.8% | National, most pronounced in regions with high living costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Lumber and Textile Costs Pressuring Margins

Volatile lumber and textile input costs create near-term pressures that affect pricing, assortment, and margins across the United States Home Decor market. Tariffs on building materials and related inputs can significantly increase project costs, impacting categories like cabinetry, flooring, and furniture tied to renovation activity. Import and export price trends in 2025 were mixed, with furniture-related imports rising while textiles and plastics saw modest declines, complicating vendor negotiations and retail pricing strategies. Policy changes and elevated tariff rates added uncertainty for buyers, prompting sourcing diversification and more complex logistics management. Premium brands with strong pricing power have been able to offset some of these pressures, while larger-scale operators leverage supplier terms and network efficiencies to absorb short-term cost spikes. The ability to manage input volatility effectively, as demonstrated by companies like Williams-Sonoma, highlights how vertical control and strategic channel mix can cushion the impact on margins.

Higher Mortgage Rates Constraining Home Turnover and Spending

Rising mortgage rates since 2024 have limited home sales turnover and deferred full-home furnishing projects, shifting consumer spending toward targeted room refreshes and replacement purchases. Existing home sales improved modestly, but activity remains below recent highs, emphasizing reliance on aging-in-place dynamics rather than move-related demand. Retailers are adjusting merchandising and marketing strategies to focus on incremental upgrades spread over multiple years instead of concentrated move-in purchases. Although the labour market and household finances are supportive, higher financing costs continue to restrict mobility, reducing the flow of first-time and move-up buyers who typically purchase across multiple rooms. Categories such as home office and bathrooms have captured share as messaging around comfort, wellness, and productivity resonates more than purely cyclical appeals. Overall, the market favours steady execution, clear value propositions, and strong omnichannel capabilities while demand for large-ticket items remains constrained by financing pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Home Office Decor Outpaces Traditional Categories

Furniture commanded 39.36% of market size in 2025, while home office furnishings and Decor posted the fastest trajectory with an 11.87% CAGR projected through 2031 as hybrid work patterns persist. Consumers are increasingly investing in ergonomic chairs, adjustable desks, lighting, and sound management solutions to support flexible work routines and video calls at home. Telework has become a stable part of employment trends, sustaining demand for functional yet stylish home office infrastructure. Retailers are emphasizing multipurpose solutions such as modular shelving and cable-managed desks that integrate technology without compromising living space aesthetics. The market has adapted by balancing productivity essentials with decorative accents, boosting the popularity of curated bundles and room sets in both online and in-store experiences.

Home textiles continue to perform strongly, driven by regular refresh cycles and wellness-oriented features, while performance fabrics gain traction for their durability and comfort properties. Flooring and carpet demand shows mixed momentum as households prioritize materials that offer long-term resilience and easy maintenance. Wall Decor is experiencing a modest resurgence as homeowners seek personalization, with customization and made-to-order options helping differentiate retailers. Lighting is shifting toward smart, modular solutions that serve both task and ambient needs while optimizing energy use. Overall, the United States Home Decor market is increasingly focused on spaces that serve multiple functions, with home office furnishings leading the transformation.

By Material: Sustainable Wood Commands Premium While Synthetics Gain Share

Wood retained a 44.44% market share in 2025, supported by durability, repairability, and cross-style appeal, while sustainable and reclaimed wood posted a 10.29% CAGR outlook as certifications and responsible sourcing become stronger differentiators. Retailers have expanded certified assortments, and brands adopting rigorous sourcing and traceability standards are seeing measurable gains in consumer trust and market positioning. Initiatives such as increasing certified content in products and switching packaging to sustainable paper are becoming part of broader environmental strategies. Collaborations with international suppliers ensure the availability of certified wood for imported furniture, while niche manufacturers emphasize domestic and regional sourcing to appeal to sustainability-conscious buyers. Overall, certified and reclaimed wood are capturing a premium, while mass-market offerings balance affordability with responsible material choices.

Other materials, such as metal, textiles, glass, plastics, and stone, serve targeted purposes within home Decor assortments, meeting distinct functional and aesthetic needs. Metal benefits from recycled content and structural stability, although tariffs can influence costs and delivery timing. Textiles vary between organic fibres and advanced synthetics, with adoption influenced by household budgets and preference for premium features in bedding and upholstery. Recycled glass is popular in lighting and decorative tiles, while plastics and synthetics dominate outdoor and storage applications due to weather resistance and ease of maintenance. Stone and ceramic continue to stand out in premium spaces, and the market increasingly emphasizes durability, care guidance, and clearly labelled material claims to extend product life and enhance perceived value.

By Distribution Channel: E-Commerce Surges While Physical Stores Anchor High-Touch Categories

Home-improvement and furniture stores held a 46.74% market share in 2025, which underscores the importance of sensory validation and project support for big-ticket and bulky purchases, while online and e-commerce channels recorded a 12.84% CAGR. Online penetration is expanding as digital-first platforms combine logistics density with tools that simplify discovery and purchasing. Innovative solutions, such as AI-driven room visualization and curated shopping experiences, allow consumers to move from inspiration to purchase with less reliance on in-person browsing. Large omnichannel retailers are experimenting with conversational commerce and integrated curation, linking inspiration, checkout, and pickup to encourage multi-category baskets. The market increasingly favours hybrid models that merge speed, visualization, design support, and installation capability across both physical and digital channels.

Home centers and specialty retailers are investing heavily in delivery networks and professional services to enhance reliability for Decor items that accompany building projects. Strategic acquisitions and partnerships strengthen design, distribution, and installation capabilities, supporting both professional and consumer spending. Smaller specialty boutiques face pressure from scaled omnichannel players and pure e-commerce platforms that offer broader selection and faster delivery. Supermarkets and hypermarkets continue to play a minor role, focusing mainly on small Decor items and textiles that complement regular shopping. Overall, physical stores remain critical for high-touch categories, while e-commerce drives growth and sets higher expectations for visualization, delivery speed, and seamless returns.

By Price Range: Mass Market Dominates Volume, Premium Captures Margin Growth

Mass-market products held 69.47% market share in 2025, which reflects broad price sensitivity and the strength of accessible formats, while premium and luxury segments are projected to grow at a 9.24% CAGR due to sustained demand for craftsmanship, customization, and transparent sourcing. Premium players in the United States Home Decor market leverage supply chain efficiencies and proprietary product designs to maintain strong operating margins even during periods of uneven demand. High-income consumers are drawn to differentiated brand narratives, artisanal materials, FSC-certified wood, and elevated finishes, which increase willingness to pay. Retailers like Ingka Group focus on affordability and operational efficiency while expanding formats that cater to planning-intensive categories such as kitchens and wardrobes. These strategies create a broad price spectrum, enabling households to mix high-end and value items within rooms as budgets evolve. The combination of premium offerings and operational discipline allows brands to capture both aspirational and core segments effectively.

Value-driven retailers emphasize price leadership, flexible financing, and durable assortments to attract households that delay large-ticket purchases but continue to refresh rooms with accessories and textiles. Mass-market offerings focus on versatile designs and resilient finishes that extend product lifecycles across multiple aesthetics. At the premium end, curated collaborations and made-to-order programs maintain freshness and support margins even when volumes fluctuate. The market continues to expand at the premium tier, driven by high-income demand and supply chain advantages that protect service levels and availability. Overall, clear communication of total value, including durability, service, and delivery speed, helps retailers succeed across the full price spectrum.

By Room: Living Room Leads Share, Home Office Commands Growth

Living rooms held 30.37% of the total market size within the room segments in 2025, which reflects their central role in household life, while the home office remains the fastest-growing room at an 11.87% CAGR outlook as hybrid work stabilizes. Bedrooms continue to see steady demand, driven by a wellness focus on sleep systems and textiles, with innovations that enhance comfort and functionality. Kitchens and dining areas exhibit a split in consumer behaviour, as high-income households pursue renovations featuring premium appliances and surfaces, while budget-conscious buyers update in stages. Bathroom projects benefit from aging-in-place considerations and comfort-oriented features, with upgrades often triggering additional accessory and Decor purchases. Outdoor and patio furnishings are expanding to support entertaining and relaxation, with durable materials and performance fabrics extending product lifecycles in varying climates. Overall, these trends highlight the importance of both functional improvements and aesthetic appeal across core living spaces.

The home office segment reflects space reallocation within existing homes rather than major expansions, sustaining demand for modular furniture that fits into living rooms, bedrooms, and dens. Desks with built-in power management and cable organization cater to long-term hybrid work requirements, while adjustable lighting supports video calls and reading tasks. Sound management solutions, such as rugs and panelling, address open-plan acoustics and encourage coordinated Decor across adjoining areas. While living rooms remain the largest segment by market share, the fastest spending growth occurs in rooms that support productivity and recovery, including home offices and bathrooms. Regional differences shape product selection, with larger Southern homes favouring full-suite office setups and urban apartments prioritizing compact, space-saving solutions.

Geography Analysis

The South accounted for a 35.87% market share in 2025, supported by lower housing costs, net in-migration, and a younger housing stock that shapes product mix and installation needs. Dense home centre networks in the region strengthen last-mile delivery for bulky renovation items, often paired with decor purchases. Value-oriented strategies remain prominent, as national chain expansions improve access and accelerate fulfilment. Outdoor living categories perform well due to milder climates and larger yards, supporting demand for durable and weather-resistant materials. Overall, stable household formation and migration from higher-cost areas help maintain project activity even when national sales volumes soften.

The West, with a smaller base, is projected to grow at the fastest regional pace with an 8.84% CAGR, supported by technology sector incomes and sustainability preferences that favour certified materials and premium craftsmanship. California leads with format innovations that combine design support, digital ordering, and planning-focused experiences for kitchens, wardrobes, and storage solutions. Households prioritize sustainability and material provenance, boosting demand for FSC-certified wood, low-emission finishes, and ethically sourced textiles. Port logistics can create lead-time challenges for imports, which favours retailers with diversified sourcing and strategically located warehouses. This regional growth emphasizes the importance of curated assortments and efficient logistics to meet consumer expectations.

The Northeast and Midwest provide complementary market dynamics, supporting both renovation and refresh cycles. The Northeast’s older housing stock drives replacement-heavy projects and space-saving solutions tailored to urban living, while strong concentrations of knowledge workers sustain home office demand. In the Midwest, renovation needs align with affordability, enabling full-suite furniture purchases and leveraging North American sourcing to reduce freight delays. Omnichannel approaches across both regions enhance in-store validation, visualization tools, and fast delivery, meeting consumer expectations for Decor items. These geographic trends collectively ensure that the United States Home Decor market remains diverse, resilient, and adaptable through 2031.

Value Chain Analysis

The United States home decor value chain runs from raw materials and components (wood, textiles, metal, glass, stone/ceramic, and mechanisms) into manufacturing and finishing, which typically combines domestic production with import sourcing. Products then move through importers, wholesalers, and retailers into consumer and professional end demand tied to renovations and new-home completions.

Wholesaling intermediaries help aggregate global and domestic supply for specialty decor stores, home-improvement and furniture chains, and online-first platforms, while last-mile delivery is a key differentiator for big-and-bulky and fragile, mixed-SKU shipments. Retailers increasingly compete on fulfillment reliability and omnichannel inventory visibility, shifting more volume through specialized warehousing, consolidation, and white-glove delivery networks. In 2025, Wayfair expanded CastleGate by making its Multichannel logistics service available as a 3PL-style offering for big-and-bulky home goods suppliers, which reflects the move toward shared fulfillment infrastructure across sales channels. Logistics capacity additions, such as Floor & Decor's 1,000,000 square foot distribution facility development at Sparrows Point, Maryland (April 2025), also underscore how regional distribution density can matter for project-driven categories where lead times and damage rates affect customer satisfaction and returns.

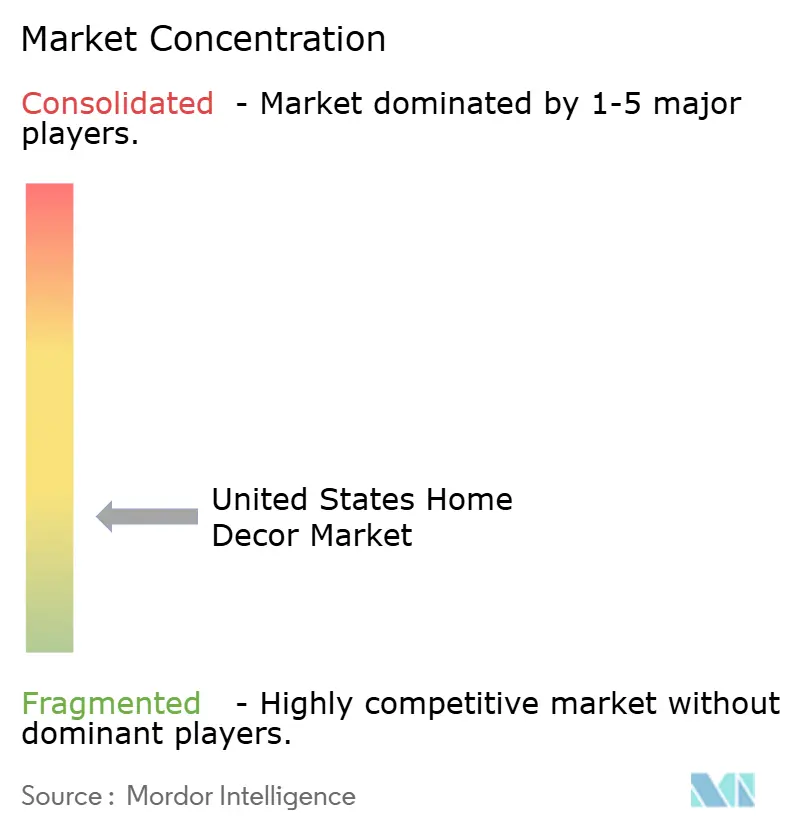

Competitive Landscape

The United States home decor market exhibits low concentration, reflecting a highly fragmented landscape where the largest companies collectively hold a modest share, and no single player dominates. This structure creates opportunities for national and regional specialists to carve out positions across channels and price tiers. Home Depot and Lowe’s capture significant portions of the broader home goods landscape, leveraging dense store networks, professional partnerships, and fast delivery that also support Decor categories tied to renovation projects. Home Depot’s deal for SRS Distribution to acquire GMS expands access to specialty building product distribution, enhancing contractor relationships and delivery capabilities that complement Decor sales. Similarly, Lowe’s acquisition of Artisan Design Group strengthens its design, distribution, and installation offerings for interior surfaces, which drives adjacent Decor demand. Together, these moves reinforce omnichannel strategies that integrate product availability, visualization, and fulfillment across categories.

IKEA USA continues to focus on affordability and footprint expansion, opening new formats that combine consultative selling with digital ordering for kitchens and storage planning. Ingka Group reported improvements in operating income and net profit while expanding its North American presence, reflecting a long-term commitment to the United States market. Williams-Sonoma executes a premium strategy, maintaining high margins through proprietary designs, supply chain efficiencies, and a mix of Decor and seasonal accessories that turn quickly. Wayfair returned to growth in 2025 and introduced Muse, a generative AI-powered discovery tool, which converts inspiration into actionable furniture and Decor purchases. Collectively, these companies illustrate different approaches to scale, from logistics-driven efficiency to design-led differentiation, that shape competitive dynamics.

Competition is centered on three key battlegrounds that will define performance through 2031. Speed favors scaled networks that deliver bulky items quickly, meeting customer expectations around remodel schedules. Discovery is increasingly driven by AI and AR tools that reduce hesitation and build confidence in online Decor and furniture purchases. Brand authority, fueled by sustainability credentials, proprietary designs, and multi-brand portfolios, allows premium pricing and cohesive room solutions. In this fragmented market, second-tier and regional players can still grow by focusing on localized assortments, service quality, and partnerships with marketplaces to extend reach, while larger players leverage scale, design, and omnichannel strength to maintain durable advantages.

United States Home Decor Industry Leaders

The Home Depot Inc.

Lowe’s Companies Inc.

IKEA USA (Ingka Holding)

Williams-Sonoma Inc.

Wayfair Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Omnichannel expansion that links digital discovery with physical planning and pickup is a clear whitespace as large home and furnishings players broaden formats for higher-consideration categories. In 2026, IKEA U.S. announced plans to open 10 new U.S. stores, while Wayfair disclosed additional large-format retail expansion, including a new Cincinnati store announcement in May 2026. These steps reinforce the role of showrooms and planning-led stores in converting high-ticket furniture and decor baskets, while still building on e-commerce growth.

AI-enabled visualization and assisted shopping are also moving from feature to purchase-enabling infrastructure, with opportunities for retailers, marketplaces, and suppliers to integrate room-scene generation, placement testing, and curated bundles into the path to purchase. Usage is measurable based on Adobe-published survey data in June 2026, which found that 49% of Americans have used AI for home interior design projects and that many use it to test furniture placement before buying. On the product side, private label and differentiated surfaces create an opportunity to capture renovation-linked demand using style-forward, durable materials, illustrated by Floor & Decor's NatureMatch private label line debut (June 2026) alongside continued warehouse store and design center openings tied to its fiscal 2026 growth plan.

Recent Industry Developments

- May 2026: The Home Depot expanded its partnership with Google Cloud and rolled out agentic AI tools nationally, including an AI-powered materials list capability aimed at professional customers. The update embeds AI into project planning and ordering workflows, strengthening the link between renovation demand and decor-adjacent attachment sales through better basket building and reduced friction.

- November 2025: IKEA U.S. and Best Buy opened shop-in-shop kitchen and laundry planning centers in select Best Buy stores in Texas and Florida. The partnership extends IKEA planning-led categories into additional physical touchpoints, supporting omnichannel conversion for high-consideration home projects that drive follow-on decor purchases.

- March 2024: The Home Depot announced its planned acquisition of SRS Distribution, targeting expansion of its professional distribution capabilities. The change reinforces pro-focused delivery and jobsite-ready fulfillment for decor categories purchased alongside remodel and repair work by improving availability and service levels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of home decor products bought for residential use in the United States, counted at the first point of retail across physical and online channels. It includes items like furniture, home textiles, floor and wall coverings, indoor decorative lighting, and decorative accessories.

Scope exclusions: We exclude major appliances, consumer electronics, core building materials, and second-hand or rental items.

Segmentation Overview

- By Product Type

- Furniture

- Home Textiles

- Flooring & Carpets

- Wall Décor (Paintings, Wallpapers)

- Lighting Fixtures

- Decorative Accessories (Vases, Candles, Clocks)

- By Material

- Wood

- Metal

- Textile

- Glass

- Plastic & Other Synthetics

- Stone & Ceramic

- By Distribution Channel

- Home-Improvement & Furniture Stores

- Specialty Décor Stores

- Supermarkets & Hypermarkets

- Online / E-commerce

- Others (Boutiques, Art Galleries)

- By Price Range

- Mass

- Premium / Luxury

- By Room

- Living Room

- Bedroom

- Kitchen & Dining

- Bathroom

- Home Office

- Outdoor & Patio

- By Geography

- Northeast

- Midwest

- Southeast

- Southwest

- West

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand and supply context for US home decor, and it also helps set clear boundaries so adjacent categories do not get mixed in. Public sources such as the US Census Bureau (retail trade and housing indicators), Bureau of Labor Statistics (CPI and household spend patterns), and BEA (personal consumption trends) are used to anchor macro movement and inflation behavior.

We also refer to sources such as USITC and US Census import statistics for decor-related product flows, along with trade bodies like the American Home Furnishings Alliance for industry context and definitions. Company filings and investor presentations help us understand channel mix, pricing commentary, and category exposure, and reputable press is used to time major demand shocks. In addition, approved paid subscriptions for company financials and intelligence, news and financials, import and export shipment-level data, and patent databases help fill gaps where public tables are not granular enough. These desk research sources are illustrative and not exhaustive, and other references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to stress-test the desk assumptions and make the sizing model realistic, especially around what gets counted as home decor at retail and how prices move by category. We spoke with a mix of manufacturers, distributors, retailers, importers, and industry experts across the US, and the discussion focused on volume trends, promo intensity, input-cost pass-through, and online versus store sales shifts, which were then used to refine the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 29% | |

| Smaller Players: 15% | Managers: 57% |

Market-Sizing & Forecasting

The core build follows a top-down approach where retail demand is reconstructed from category-level spending signals and then mapped to the defined home decor basket before the totals are finalized. To keep it grounded, results are corroborated with selective bottom-up approximations, such as sampled price point checks across key categories, channel mix checks, and supplier and retailer roll-ups for a limited set of well-covered product lines.

Inputs that matter in this market include housing turnover and housing starts, remodeling activity indicators, CPI and category inflation for furniture and home furnishing items, import intensity for decor products, and the online share trend that affects realized pricing and promotion. Price is handled in current dollars, with inflation and mix separated so that the model does not overstate growth when units are flat. Where bottom-up coverage is incomplete, gaps are handled by using penetration and mix ratios validated in interviews, and then tested against independent retail trade totals.

Forecasts are built using scenario analysis, because demand moves with housing and consumer confidence and does not follow a perfectly smooth curve. We keep a base case, then stress the model with higher and lower assumptions for housing activity, discretionary spending, and price normalization. The final forecast path is selected after it matches what industry participants expect by category and channel.

Data Validation & Update Cycle

Validation is done by triangulating the modeled market totals against independent signals such as retail sales direction, inflation benchmarks, and trade flow movement for decor-related goods. If a category shows an unusual jump, it is traced back to the driver assumptions, and the inputs are rechecked until the variance is explainable.

Before sign-off, the model and its assumptions go through a multi-step analyst review that includes logic checks, year-over-year consistency checks, and spot checks on pricing and mix. Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp shifts in housing activity, tariff changes, or a major swing in promotional pricing. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's US Home Decor Market Estimate Compared With Other Published Estimates

Published market sizes for US home decor can vary because the product basket is not identical across sources, and the counting point can shift between manufacturer value, shipped value, or retail value. Differences also come from how inflation is treated, which years are used as anchors, and how aggressively forward demand is assumed to follow housing and consumer spend trends.

Import clearance patterns, retail sales direction, and category CPI movement are the checks that keep the 2026 total aligned to a first-point-of-retail view in Mordor Intelligence, with imported decor counted when it clears US customs and with resale excluded from the spend pool. Another common driver is scope creep into home improvement materials, or the opposite issue where textiles, coverings, or accessories are undercounted because the cut is made too narrow. Gaps can also appear when current-dollar timing and update cadence are not aligned to the same year of promotions and online mix shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 227.43 B (2026) | |

| Industry Publisher A | USD 191.50 B (2025) | Anchors the series on a different year and can apply a narrower included basket across decor lines, which reduces the summed retail-value total even when category trends are directionally similar. |

| Global Consultancy B | USD 185.00 B (2024) | Uses an earlier base year and may blend valuation points across the chain, so the number becomes more sensitive to inflation pass-through assumptions and channel mix during heavy promotion periods. |

The table shows that year selection, included product lines, and valuation point explain most of the difference, not just the growth math. When the basket is kept consistent and cross-checked against housing activity, inflation, and trade signals, the resulting market size can be repeated and updated without large unexplained swings.

Key Questions Answered in the Report

What is the current size and growth outlook for the United States Home Decor market?

The United States Home Decor market size is USD 227.43 billion in 2026 and is projected to reach USD 292.71 billion by 2031 at a 5.18% CAGR.

Which categories are growing fastest within United States home Decor?

Home office furnishings and Decor lead growth with an 11.87% CAGR through 2031 as hybrid work stabilizes and rooms get reconfigured for productivity.

How are channels shifting in the United States Home Decor market?

Online/E-commerce are growing at a 12.84% CAGR, while home-improvement and furniture stores remain the largest channel at 46.74% share.

Which materials and sustainability signals matter most to United States buyers?

FSC-certified and reclaimed wood lead premium growth, supported by retailer commitments and broader sustainability programs that build trust.

Which United States regions are most influential for home Decor demand?

The South holds the largest share at 35.87% in 2025, while the West is projected to post the fastest growth at 8.84% CAGR through 2031.

How are leading companies competing in the United States home Decor?

Leaders invest in speed, visualization, and brand authority, seen in logistics expansions, AI-led discovery tools, and proprietary design portfolios that sustain margins.

Page last updated on: