Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

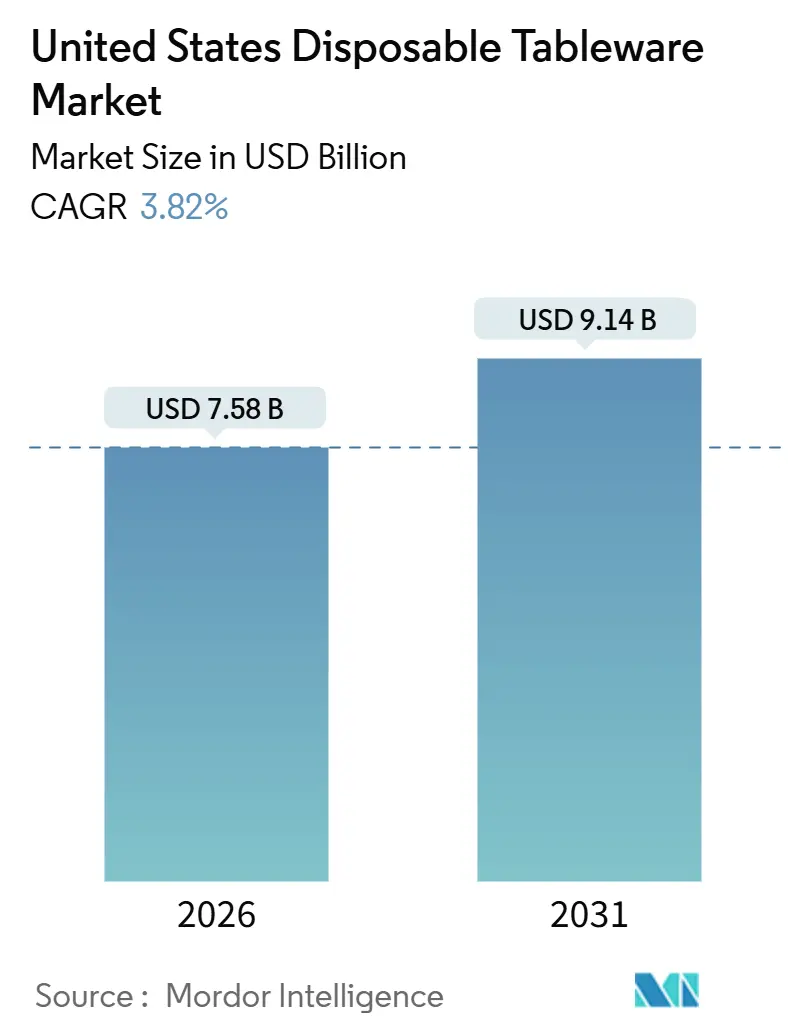

| Market Size (2026) | USD 7.58 Billion |

| Market Size (2031) | USD 9.14 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

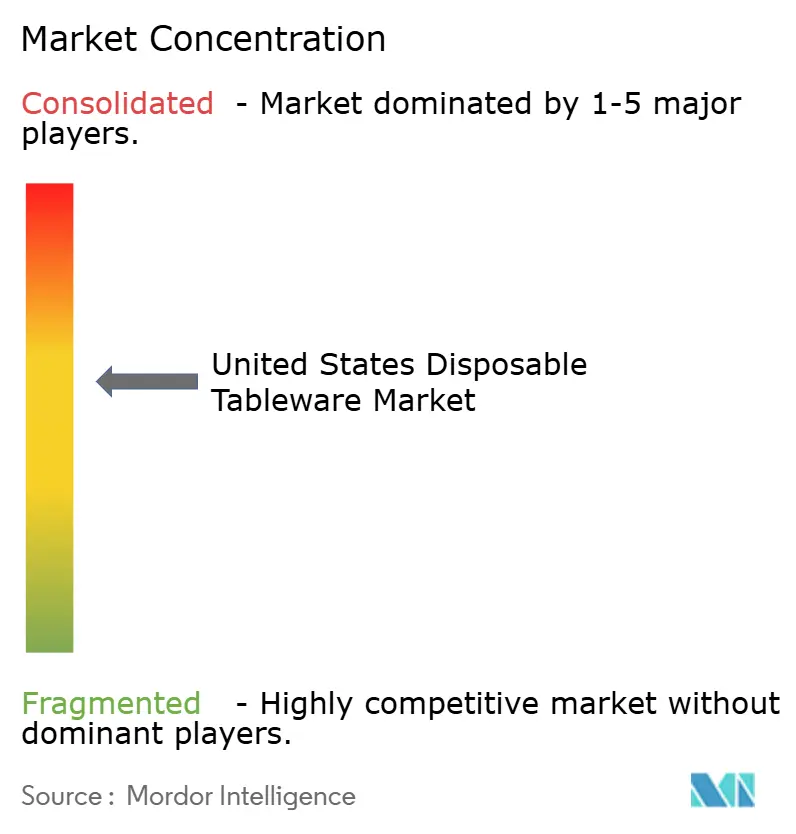

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Disposable Tableware Market Analysis by Mordor Intelligence

The United States disposable tableware market size is USD 7.58 billion in 2026 and is projected to reach USD 9.14 billion by 2031, reflecting a 3.82% CAGR over the forecast period. Operators continue to standardize on single-use formats that support takeout, delivery, and high-throughput beverage programs. State-level restrictions on expanded polystyrene and non-essential single-use items are accelerating substitution toward paper, moulded fibre, and certified-compostable lines where compliance pressure is highest[1]Source: Sustainable Packaging Coalition, “Packaging Policy News: December 2025,” Sustainable Packaging Coalition, sustainablepackaging.org. Federal procurement policies under Secretarial Order 3407 (2022) targeted single-use plastics elimination, but May 2025 reversals by Interior Secretary Burgum disrupted frameworks, delaying private-sector transitions in tourism and retail industries. Capacity expansions in fibre-based tableware and portfolio realignments toward PFAS-free barriers reflect structural changes that support the availability of compliant products at scale.

Key Report Takeaways

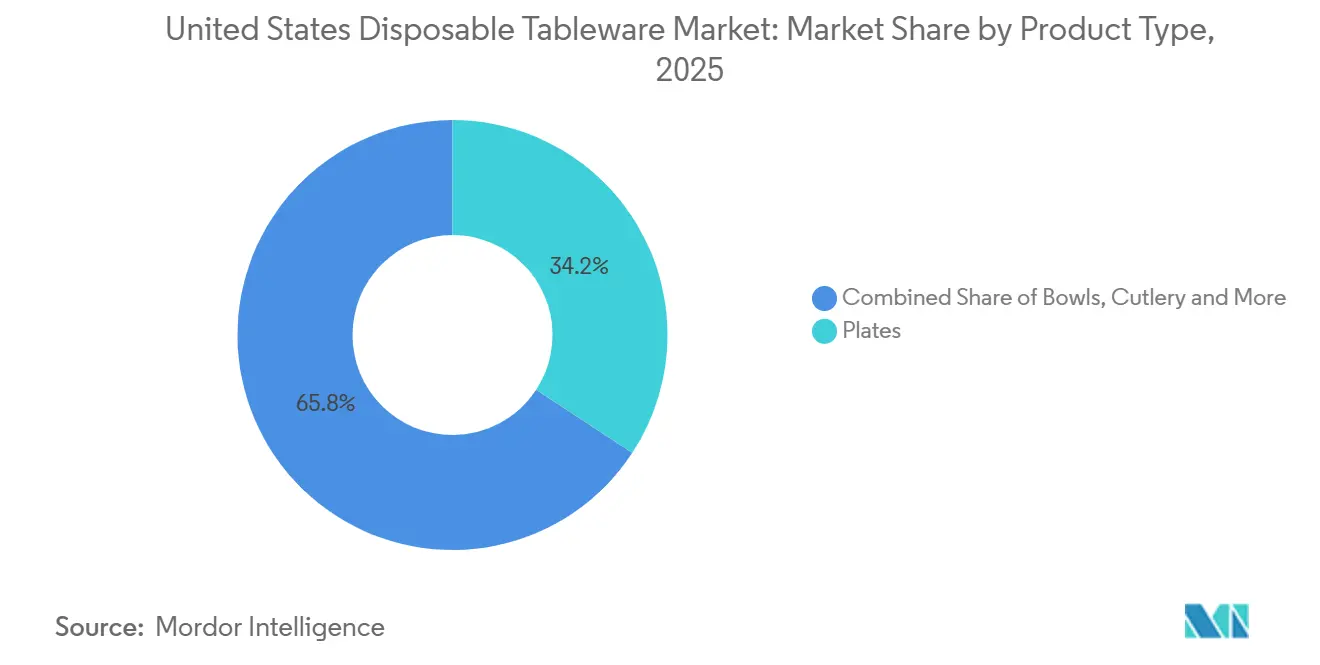

- By product type, plates led with 34.23% of the United States disposable tableware market share in 2025, while trays and containers are forecast to expand at a 4.94% CAGR to 2031.

- By material, plastic accounted for 47.92% of the United States disposable tableware market share in 2025, while bioplastics are projected to grow at a 5.13% CAGR through 2031.

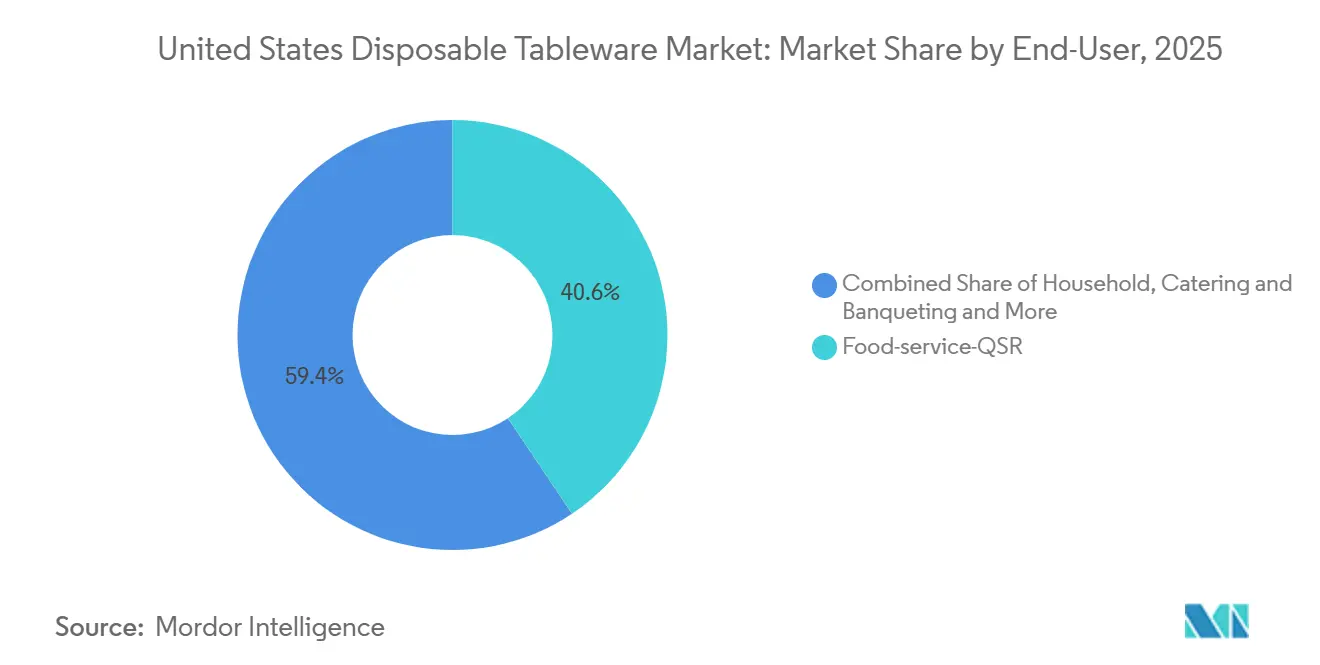

- By end-user, quick-service restaurants held 40.63% of the United States disposable tableware market share in 2025, while catering is set to expand at a 4.61% CAGR through 2031.

- By distribution channel, offline foodservice distributors held 54.91% of the United States disposable tableware market share in 2025, while online e-commerce channels are expected to grow at a 4.78% CAGR through 2031.

- By geography, the South region held 34.32% of the United States disposable tableware market share in 2025, and the West region is projected to record a 4.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Disposable Tableware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient food-service solutions from QSRs | +1.2% | National, concentrated in the South and West urban corridors | Medium term (2-4 years) |

| Growth of e-commerce meal-kit & food-delivery services | +0.8% | National, strongest in Northeast metros and West Coast tech hubs | Short term (≤ 2 years) |

| Increasing on-the-go consumption & outdoor events | +0.5% | National, seasonal peaks in South and West during Q2 and Q4 | Short term (≤ 2 years) |

| Expansion of biodegradable and compostable product lines | +0.9% | West Coast and Northeast with organics mandates | Long term (≥ 4 years) |

| Surge in ghost-kitchen proliferation in Tier-2 cities | +0.6% | Midwest and South secondary MSAs | Medium term (2-4 years) |

| Corporate zero-waste catering programs | +0.4% | National, early adoption on the West Coast and institutions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient Food-Service Solutions from QSRs

Quick-service formats keep the United States disposable tableware market on a stable footing because large networks rely on standardized, transit-ready packaging that moves quickly through drive-thru and delivery channels. Policy actions in major states have discouraged foam and certain single-use items, which pushes operators to align on compliant alternatives across multi-state footprints. This pattern reduces SKU complexity and favours paper, moulded fibre, and certified-compostable solutions in regions with strong enforcement. The combination of regulatory changes and scale purchasing reinforces consistent demand for plates, bowls, cups, lids, cutlery, and containers in the United States disposable tableware market.

Growth of E-commerce Meal-Kit & Food-Delivery Services

Online ordering, direct channels, and aggregator delivery require containers that keep food intact under stacking, transit, and varied hold times. Operators prioritize leak resistance, lid integrity, and tamper-evident packaging for main dishes, sides, and beverages, which leads to a higher use of trays, clamshells, bowls, and portion cups. Brands with multi-state operations select compliant packaging sets to avoid last-minute changes when local rules tighten, especially in the West and Northeast. Infrastructure access influences material picks, since compostable items need reliable collection and industrial processing to deliver intended end-of-life benefits. These conditions keep performance-focused single-use formats central to delivery-led growth in the United States disposable tableware market.

Increasing On-the-Go Consumption & Outdoor Events

Seasonal outdoor dining and high-traffic venues create demand spikes for plates, bowls, cups, lids, trays, and cutlery during peak months. Event organizers in leading states prefer compliant items and clear labelling to minimize contamination and meet municipal rules. West Coast programs often include organics collection, which can support food and packaging co-collection where facilities accept those items[2]Source: Closed Loop Partners, “Compostable Packaging Infrastructure Investment Report,” Closed Loop Partners, closedlooppartners.com. The availability of composting access remains uneven, which keeps many event series focused on fiber-based or recyclable selections that fit local conditions[3]Source: Sustainable Packaging Coalition, “New Composting Access Data 2025,” Sustainable Packaging Coalition, sustainablepackaging.org. As venue calendars expand, this mix sustains steady volume for single-use formats in the United States disposable tableware market.

Expansion of Biodegradable and Compostable Product Lines

PFAS restrictions in food-contact articles are prompting suppliers to replace legacy coatings with alternative barriers and to scale certified-compostable options. Producers have announced portfolio shifts to remove PFAS while maintaining grease and moisture performance for foodservice use cases. Policy updates in leading states reinforce the need for compliant alternatives and encourage faster catalogue updates by larger manufacturers. These moves are complemented by capacity investments in fibre-based lines that meet new standards for public and private procurement. As certified options expand, institutions and national accounts can scale consistent, compliant selections in the United States disposable tableware market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent state-level bans on EPS and single-use plastics | -0.9% | West, Mid-Atlantic, select Northeast | Short term (≤ 2 years) |

| Volatility in pulp and paper input prices | -0.6% | National, stronger in import-reliant corridors | Medium term (2-4 years) |

| Emerging re-use subscription models in venues | -0.3% | West Coast metros and select institutions | Long term (≥ 4 years) |

| Limited industrial composting infrastructure | -0.5% | National, pronounced urban-rural divide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Pulp & Paper Input Prices

Fiber supply, energy costs, and logistics conditions drive variability in production costs for paper and moulded-fibre items. Integrated producers with captive pulp or large-scale contracts tend to manage volatility more effectively than smaller converters. Recent investments in Southern and Midwestern capacity indicate structural confidence in fibre-based demand, which supports regional supply depth and shorter lead times. Buyers balance cost variability with multi-year contracts and diversification by substrate to stabilize operations. This environment adds planning complexity and can slow switching decisions within the United States disposable tableware market.

Emerging Re-Use Subscription Models in Venues

Reusable container programs are expanding in controlled environments where returns and cleaning can be managed with on-site equipment and staff. Operators test deposit-return workflows and digital tracking in campuses and corporate facilities to reduce waste under stable conditions. Large packaging suppliers are partnering with reuse brands to learn deployment models and hedge exposure to policy shifts. These programs are still limited in scale and remain concentrated in select metros, which contains their near-term impact. The net effect is a localized restraint rather than a broad structural shift in the United States disposable tableware market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transit-Optimized Containers Outpace Plates

Plates accounted for a 34.23% share of the United States disposable tableware market size in 2025, and trays and containers are projected to advance at a 4.94% CAGR through 2031. Delivery-centric models reward stackable footprints and tight lid seals that maintain temperature and texture under transit conditions. Multi-unit operators favour standardized sizes to simplify pick, pack, and order assembly. Beverage programs sustain steady volume for cups and lids across cold and hot occasions. These patterns keep procurement focused on predictable performance and fit across dayparts and menu builds in the United States disposable tableware market.

Delivery-only expansions illustrate the operational shift toward sealed containers, multi-compartment trays, and tamper-evident closures, especially in secondary metros with rising off-premise traffic. Regulatory transitions away from foam in key states encourage national brands to align on compliant containers to avoid sudden changes when rules tighten. These constraints support the relative outperformance of transit-optimized formats versus traditional plate-only setups. As a result, trays, clamshells, bowls, and portion-cup systems gain momentum across ordering channels in the United States disposable tableware market.

By Material Type: Regulatory Tailwinds Propel Bioplastics

Plastic retained 47.92% of the United States disposable tableware market share in 2025, while bioplastics are projected to grow at a 5.13% CAGR through 2031. PFAS restrictions in food-contact packaging are accelerating portfolio updates and barrier innovations that support compliant performance in grease and moisture applications. Vendors are removing PFAS and scaling alternative substrates, including moulded fibre and certified-compostable lines, to serve public-sector bids and large private accounts. Fiber-based capacity investments and egg-carton platform expansions provide supply-side reinforcement for moulded pulp and paperboard formats. This set of changes supports a durable shift toward compliant materials in the United States disposable tableware market.

Producers with integrated networks and regional plants are positioned to navigate feedstock volatility with shorter lead times and stronger quality control. New and expanded facilities in the South and Midwest indicate long-term confidence in fibre-based demand backed by policy tailwinds. As multi-state brands unify specifications, plastics remain in use where allowed, while fibre and compostable options gain traction in restricted jurisdictions. This balanced approach supports compliance while preserving operational continuity. The net effect is gradual mix evolution rather than abrupt displacement in the United States disposable tableware market.

By End-User: Ghost Kitchens Elevate QSR Dominance

Quick-service restaurants held 40.63% of the United States disposable tableware market share in 2025, and catering is projected to expand at a 4.61% CAGR through 2031. QSR purchasing emphasizes standardized containers, lids, and cutlery that can move across formats with minimal retraining and low error rates. Institutions adopt certified-compostable SKUs to support diversion goals where collection exists and where facilities accept food-contact packaging. Procurement teams seek consistent documentation and certifications to pass bid screens and operate across mixed markets. These needs keep end-user demand anchored to dependable and verifiable packaging in the United States disposable tableware market.

Delivery-only operations add predictable ordering patterns that favour sealed containers, tamper-evident closures, and stackable sizes. Institutions add long-duration contracts that support vendor investments in PFAS-free barriers and moulded fibre capacity. Catering growth aligns with client sustainability requests that require certified items and clear disposal instructions. These end-user dynamics preserve high-frequency consumption of plates, bowls, cups, lids, cutlery, and containers. The combined effect is stable, compliance-led adoption in the United States disposable tableware market.

By Distribution Channel: E-commerce Disrupts Foodservice Oligopoly

Offline foodservice distributors accounted for 54.91% of the United States disposable tableware market size in 2025, while online channels are projected to grow at a 4.78% CAGR through 2031. Broadline suppliers remain essential for multi-unit accounts that want consolidated deliveries and invoicing. Distributors also support compliance, certification tracking, and SKU vetting as state rules evolve, which raises the value of documentation and service support. E-commerce portals aggregate long-tail assortments and serve small and mid-sized operators with flexible ordering. That mix of offline and online access improves the availability of compliant products across regions in the United States disposable tableware market.

Large manufacturers are also building direct-to-business capabilities alongside distributor partnerships. Recent portfolio combinations broaden logistics reach, increase SKU depth, and make compliance-aligned assortments easier to deploy nationally. This dual approach helps brands respond to local policy shifts without disrupting service. As online channels scale, buyers still rely on distributor services for training and compliance support. The result is an omnichannel distribution structure in the United States disposable tableware market.

Geography Analysis

The South region accounted for 34.32% of the United States disposable tableware market size in 2025, and the West is projected to expand at a 4.17% CAGR through 2031. Southern share reflects a large base of quick-service and casual dining formats and ongoing investments in regional paper-based capacity, which tighten lead times and reinforce supply reliability. Western growth is tied to state-level restrictions that curb foam foodservice ware and require higher recovery performance, which drives substitution toward compliant lines. Municipal organics mandates and acceptance of compostable food-contact items in many facilities support scale use where programs operate. This policy and infrastructure alignment is a distinct feature of the West in the United States disposable tableware market.

The Midwest posts stable growth supported by delivery-only expansion into secondary metros and by supply-side investments in moulded fibre and paperboard. Regional plants support institutional buyers and private accounts that demand documented compliance and reliable deliveries. The Northeast combines dense urban demand with a regulatory environment that discourages specific single-use items and favours compliant alternatives. Organics program access continues to expand, although city-by-city differences remain important for end-of-life planning. These conditions shape procurement choices for institutions and national brands in the United States disposable tableware market.

Federal steps to phase out single-use plastics across public lands give the West a public-sector demonstration effect for compliant tableware selections. This influence extends beyond parks and concessions as suppliers and operators adapt labelling and certifications for broader use. The resulting standardization reduces switching costs when state or municipal rules tighten and improves training outcomes for staff. Where composting access is limited, buyers balance compostable benefits with practical considerations around disposal and contamination. These regional realities guide how products are selected and deployed in the United States disposable tableware market.

Competitive Landscape

The competitive field is moderately consolidated with multi-brand portfolios that span paper, moulded fibre, plastic, and compostable lines. Large players have invested in capacity, PFAS-free barriers, and certification-ready catalogues to fit policy-driven demand in key regions. Acquirers are combining logistics networks and broadening SKU depth to serve both distributor partners and direct enterprise accounts. This reach supports rapid deployment of compliant products and documentation across multi-state networks. These moves align portfolios with the needs of the United States disposable tableware market.

Recent combinations have unified complementary brand sets and created scale advantages in direct-to-business fulfillment. The largest of these transactions adds substantial SKU breadth and national coverage for food, beverage, and specialty packaging. Producers are also participating in reuse pilots and strategic investments to learn operational models and hedge long-term exposure to policy shifts. The combination of single-use innovation and selective reuse testbeds indicates an incremental approach to circularity. This balance is tuned to compliance and customer needs in the United States disposable tableware market.

Material innovation focuses on PFAS-free barriers, moulded fibre forming, and certifications that facilitate municipal acceptance and institutional bids. Vendors with integrated pulp and converting assets can better manage input volatility and lead times. Municipal and facility acceptance policies still vary by substrate and process, which makes labeling and documentation essential for scale use. These dynamics shape product roadmaps and capacity allocation across the United States disposable tableware market.

United States Disposable Tableware Industry Leaders

Dart Container Corporation

Georgia-Pacific LLC (Dixie)

Reynolds Consumer Products (Hefty)

Huhtamaki (Oscar Mayer Chinet)

Pactiv Evergreen Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Intervine partnered with Better Earth to address in-flight waste challenges in the aviation industry. Better Earth provides durable, BPI-certified compostable service ware, including moulded fibre containers, cutlery, and cups, alongside infrastructure partnerships, digital tools like the Betterbin portal, and consulting services to help airlines expand composting capacity and scale sustainability initiatives effectively.

- September 2025: Dickey’s Barbecue Pit expanded its ghost-kitchen footprint with 28 new delivery-only facilities across ten states. The rollout into secondary metros increases the use of standardized, stackable containers and tamper-evident closures for reliable delivery integrity. The expansion reinforces demand for transit-optimized packaging in new local markets that rely on off-premise ordering. The network growth supports the broader diffusion of delivery-first packaging standards in the United States disposable tableware market.

- April 2025: Novolex completed its acquisition of Pactiv Evergreen, combining more than 250 brands with expanded national coverage. The transaction strengthens direct-to-business fulfillment, broadens material portfolios, and aligns compliance documentation for multi-state operators. The combined scale supports faster deployment of compliant SKUs and certifications in regulated regions.

- April 2025: Huhtamaki acquired Zellwin Farms for USD 15 million to reinforce moulded-fibre capacity and North American positioning. The acquisition complements prior platform investments that support institutional buyers and large private accounts. It also strengthens supply depth for fibre-based formats aligned with PFAS-free and compostability requirements. The move supports long-term growth in compliant fibre offerings in the United States disposable tableware market.

United States Disposable Tableware Market Report Scope

By Product Type

| Plates |

| Bowls |

| Cups & Lids |

| Cutlery |

| Trays & Containers |

| Napkins & Others |

By Material Type

| Plastic |

| Paper & Paperboard |

| Bagasse / Molded Fiber |

| Bioplastics (PLA, PHA) |

| Aluminum Foil |

By End-User

| Household |

| Food-service-QSR |

| Food-service -Full-service Restaurants |

| Catering & Banqueting |

| Institutional (Schools, Hospitals) |

| Others (Airlines, Events) |

By Distribution Channel

| Super/Hypermarkets |

| Cash & Carry |

| Food-service Distributors |

| E-commerce Retail |

| Online-Direct-to-Business Portals |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Plates |

| Bowls | |

| Cups & Lids | |

| Cutlery | |

| Trays & Containers | |

| Napkins & Others | |

| By Material Type | Plastic |

| Paper & Paperboard | |

| Bagasse / Molded Fiber | |

| Bioplastics (PLA, PHA) | |

| Aluminum Foil | |

| By End-User | Household |

| Food-service-QSR | |

| Food-service -Full-service Restaurants | |

| Catering & Banqueting | |

| Institutional (Schools, Hospitals) | |

| Others (Airlines, Events) | |

| By Distribution Channel | Super/Hypermarkets |

| Cash & Carry | |

| Food-service Distributors | |

| E-commerce Retail | |

| Online-Direct-to-Business Portals | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current size and projected growth of the United States disposable tableware market?

The United States disposable tableware market size is USD 7.58 billion in 2026 and is projected to reach USD 9.14 billion by 2031 at a 3.82% CAGR.

Which segments are expanding fastest within the United States disposable tableware market?

Trays and containers are projected to grow at a 4.94% CAGR, bioplastics at a 5.13% CAGR, online channels at a 4.78% CAGR, and catering at a 4.61% CAGR.

How are regulations shaping material choices in the United States disposable tableware market?

State-level rules discourage foam and PFAS in food-contact packaging, which accelerates a shift to PFAS-free barriers, molded fiber, and certified-compostable options.

What regional factors drive adoption patterns across the United States?

The South holds the largest 2025 share at 34.32%, while the West grows fastest due to policy and organics programs; local composting access often determines end-of-life pathways.

Which developments could influence supply reliability?

New United States paper-based capacity, fiber platform investments, and portfolio combinations increase SKU depth and improve compliance-aligned supply in regulated states.

How do institutional buyers affect demand in this space?

Institutions prioritize certified-compostable options and clear documentation for audits, which supports steady adoption where organics collection programs accept food-contact packaging.

Page last updated on: