Ceiling Lights & Chandeliers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 42.18 Billion |

| Market Size (2031) | USD 54.69 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

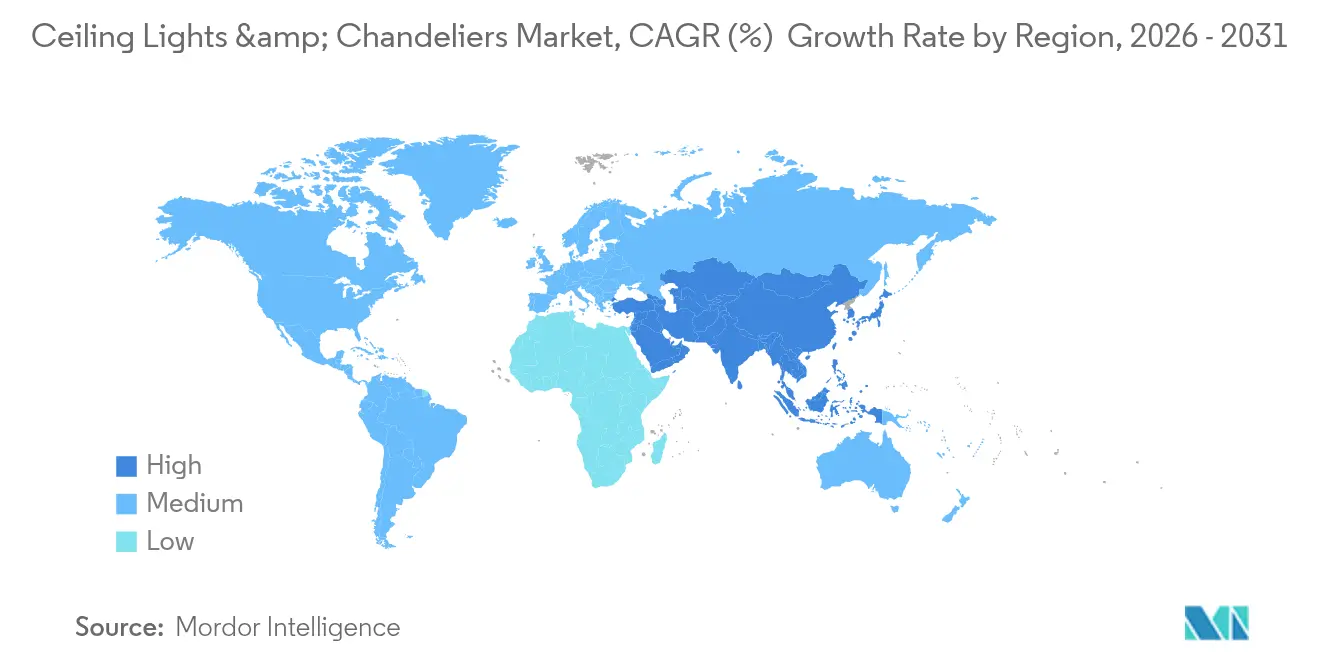

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

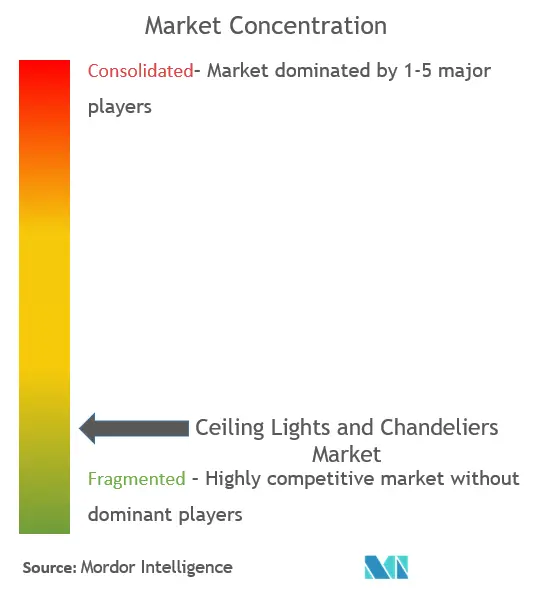

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceiling Lights & Chandeliers Market Analysis by Mordor Intelligence

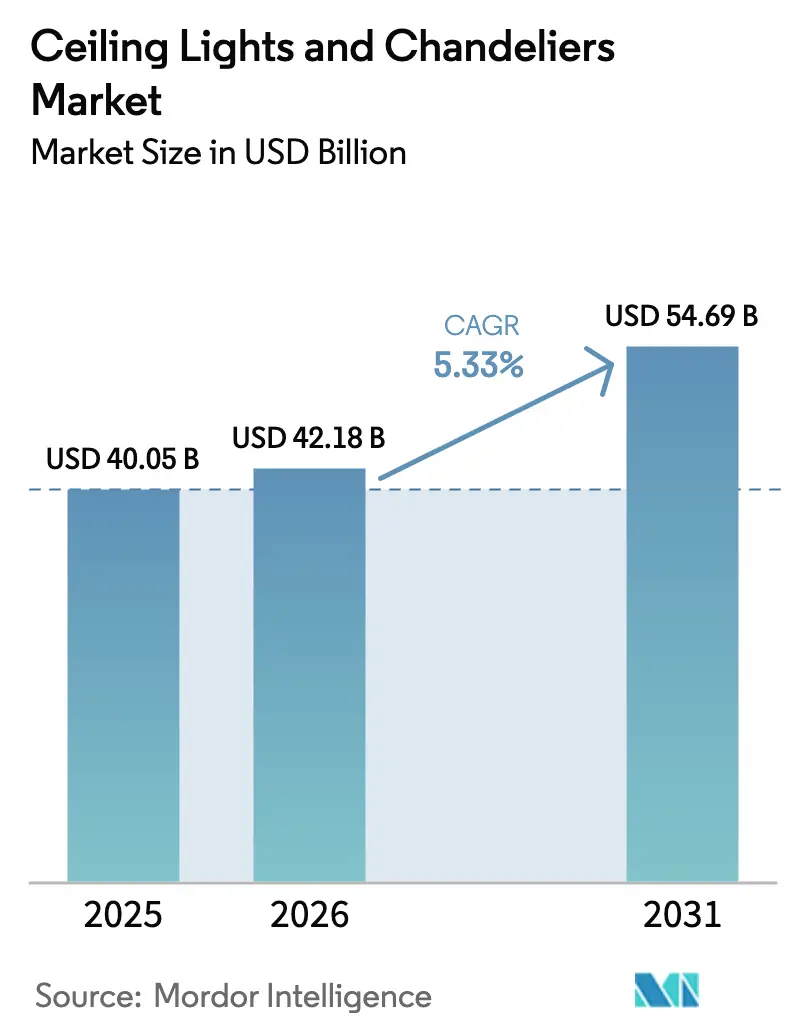

The Ceiling Lights & Chandeliers Market size was valued at USD 40.05 billion in 2025 and estimated to grow from USD 42.18 billion in 2026 to reach USD 54.69 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031).

Demand is underpinned by rapid LED adoption, the rising appeal of connected fixtures, and steady residential renovation outlays. Smart luminaires now account for more than one-third of the leading vendors’ portfolios, a share that expanded quickly after 2024 as interoperability standards matured. North America retains the largest regional share thanks to high smart-home penetration and an aging housing stock that drives retrofit activity, whereas Asia-Pacific is the fastest-growing region on the strength of urban housing starts and expanding middle-class incomes. Product substitution remains brisk—traditional sources continue to cede ground to LEDs, and ceiling lights command a 62.9% revenue share even as decorative chandeliers post the briskest growth.

Key Report Takeaways

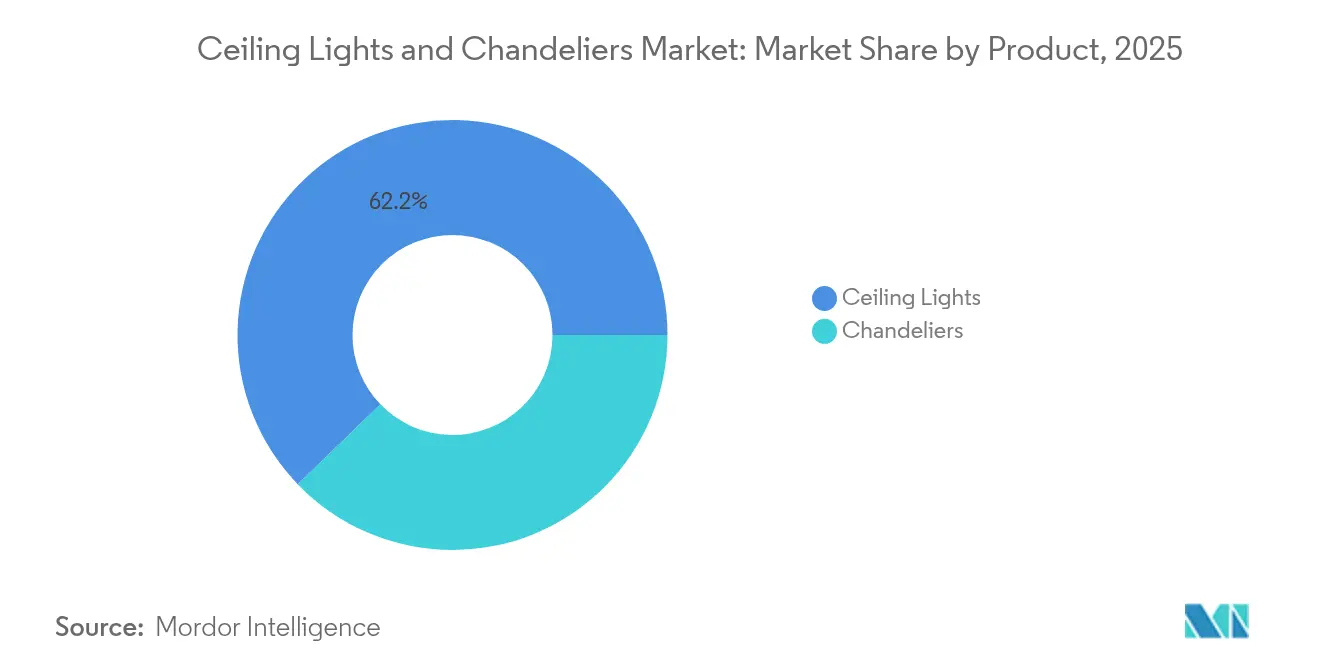

- By product type, ceiling lights led with 62.20% of the ceiling lights & chandeliers market share in 2025; chandeliers are projected to expand at a 6.12% CAGR through 2031.

- By lighting technology, LED solutions captured 53.51% of the ceiling lights & chandeliers market size in 2025, while smart/connected LED systems are projected to grow at an 10.95% CAGR to 2031.

- By material, metal frameworks accounted for 39.59% of the ceiling lights & chandeliers market size in 2025; crystal components are set to grow at a 7.25% CAGR through 2031.

- By end-user, residential applications held 57.56% of the ceiling lights & chandeliers market share in 2025, whereas commercial installations are advancing at a 6.86% CAGR through 2031.

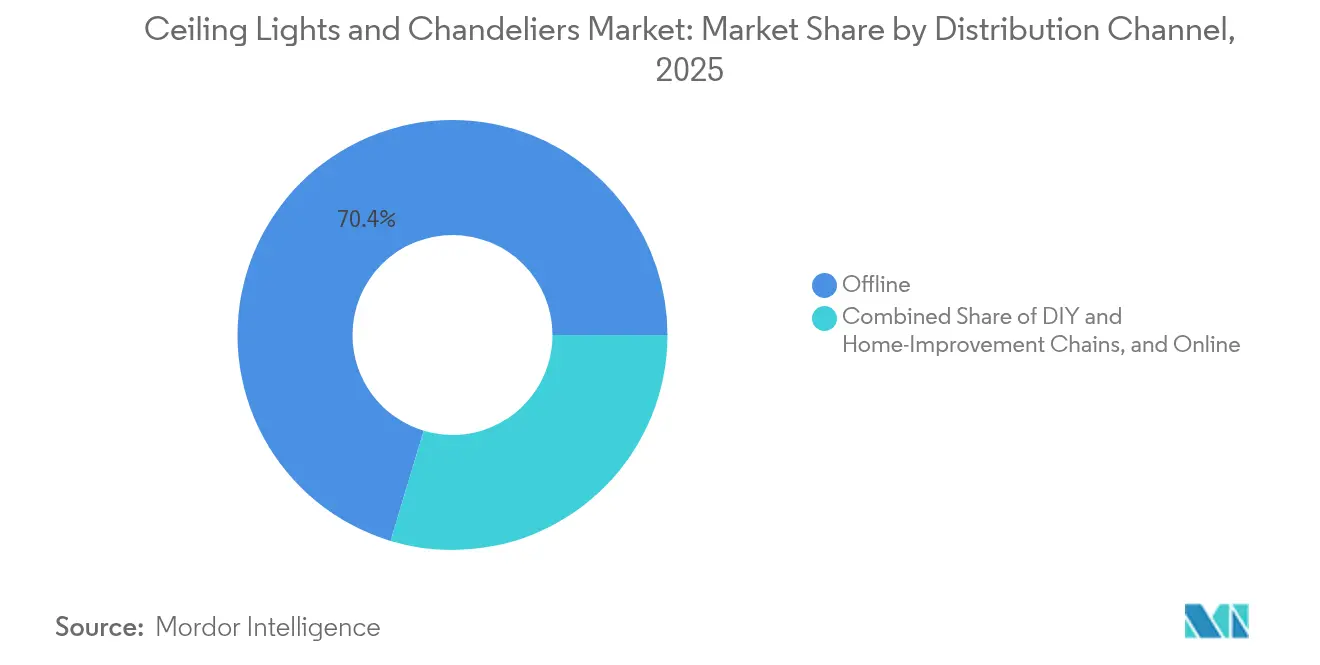

- By distribution channel, offline showrooms and home-center outlets retained 70.35% of 2025 sales; the online segment is expanding at an 8.52% CAGR to 2031.

- By region, North America remains the largest geographic contributor around 34.50% of market share in 2025, while Asia-Pacific is forecast to advance at a 8.78% CAGR between 2026-2031.

- Signify, Acuity Brands Lighting, OSRAM GmbH, Eglo Leuchten, and Kichler Lighting collectively held major market share in the 2024 global market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ceiling Lights & Chandeliers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Home Aesthetics & Interior Design | + 3.8% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Urbanization and Rising Residential Construction | + 4.2% | Asia Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Technological Advancements (Smart & Energy-Efficient Lighting) | + 3.5% | North America, Europe, developed Asia Pacific | Medium term (2-4 years) |

| Growth in Hospitality & Commercial Real Estate Sectors | + 2.1% | Global, with concentration in urban centers | Medium term (2-4 years) |

| Expanding E-Commerce & Online Retail Channels | + 1.7% | Global, with higher impact in developed economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising home aesthetics and interior design

Lighting has shifted from a purely functional commodity to a defining design element, encouraging homeowners to replace basic fixtures with statement pieces that deliver both ambience and efficiency. Residential lighting still consumes roughly 10% of household electricity, and ENERGY STAR now lists more than 60,000 certified models that blend design and low wattage [1]Source: U.S. Department of Energy, “Solid-State Lighting Program,” energy.gov. Americans spend close to 90% of their time indoors, so improved visual environments consistently rank among the top five home improvement projects. Around 3.7 million United States households upgraded lighting in 2024, underlining steady replacement demand.

Urbanization and Rising Residential Construction

Rapid city growth across Asia-Pacific, the Middle East, and Latin America fuels new-build demand for ceiling-mounted illumination. United Nations data shows 56.2% of the global population lived in urban areas in 2024, with the share tracking toward 68.4% by 2050. Countries will need roughly 2.5 billion new housing units, each requiring multiple fixtures. In the United States, privately owned housing starts hit an annualized 1.56 million in 2024, a 7.2% rise that directly lifts fixture sales.

Technological Advances in Smart and Energy-Efficient Lighting

Internet-enabled luminaires are turning ceilings into nodes for sensing, communications, and efficiency optimization. The U.S. Department of Energy estimates LEDs could trim national lighting energy use by 75% by 2035. Laboratory efficacy already exceeds 200 lumens per watt, and federal guidance promotes occupancy sensing and daylight harvesting in connected fixtures. Standards under development at NIST support cross-brand interoperability, accelerating mainstream adoption.

Growth in Hospitality and Commercial Real Estate Sectors

Commercial landlords target lighting upgrades for both energy savings and experiential value. Lighting represents about 17% of electricity in U.S. commercial buildings. LEED-certified spaces that integrate high-quality fixtures achieve rental premiums near 11%. Employment growth of 1.9 million jobs in leisure and hospitality through 2030 will spur hotel and restaurant openings, each requiring decorative yet efficient ceiling installations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium and Designer Fixtures | -1.9% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Energy Regulations & Compliance Standards | -1.2% | North America, Europe, developed Asia markets | Long term (≥ 4 years) |

| Installation Complexity & Maintenance Issues | -0.8% | Global | Short term (≤ 2 years) |

| Volatility in Raw Material Prices (Glass, Crystal, Metal) | -1.1% | Global, with manufacturing hubs most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium and Fixtures Designer

Statement chandeliers can cost several multiples of standard flush mounts, limiting penetration in price-sensitive segments. Household spending on durable goods is highly elastic above certain thresholds, and tariffs have lifted landed costs for imported components by up to 25% since 2024. Top-income United States households spend 4.7 times more on home furnishings than middle-income peers, illustrating the income asymmetry that caps addressable volume.

Energy Regulations and Compliance Standards

Minimum efficacy rules push lagging technologies out of the market yet also raise compliance costs. California’s Title 24 and U.S. DOE appliance standards demand high lumens-per-watt and quality metrics such as flicker control and CRI ≥90. Manufacturers fund iterative redesign cycles to comply, raising R&D overhead that can pressure pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceiling Lights Retain Volume Leadership While Chandeliers Accelerate

Ceiling lights represented 62.20% of 2025 revenue and remain the default choice across living rooms, kitchens, corridors, and commercial settings. Average United States homes host 12.3 fixtures, two-thirds of which are ceiling mounted . Flush and surface mounts ship in the highest volumes, but pendants show faster growth, reflecting consumer interest in bespoke aesthetics. Chandeliers occupy a smaller slice yet are projected to post a 6.12% CAGR, bolstered by rising installations in dining rooms and hotel lobbies. Imports of decorative fixtures climbed 18.3% in 2024, confirming a resilient appetite for standout designs even when traditional categories mature.

Second-order effects ripple through the ceiling lights & chandeliers market as design expectations converge with smart-home functionality. Leading chandelier makers now experiment with embedded Bluetooth-mesh drivers and tunable-white LEDs, features previously reserved for utilitarian luminaires. New United States single-family builds featuring at least one chandelier rose to 68% in 2024, up 12 points from 2020. These shifts foreshadow a future where decorative form and networked intelligence coexist, widening consumer choice and nudging average selling prices higher.

By Lighting Technology: LED Supremacy Underpins Smart Growth

LED captured 53.51% of sales in 2025 and is on track to exceed 80% penetration by 2030, displacing fluorescent and halogen incumbents. Efficacy gains of nearly 90% over incandescent lamps deliver compelling paybacks for both homeowners and facility managers. Crucially, smart or connected LEDs register an 10.95% medium-term CAGR, reinforcing the ceiling lights & chandeliers market as an IoT on-ramp. Network-ready drivers, integrated sensors, and firmware upgrades transform fixtures into data points for occupancy analytics and asset management.

Fluorescent lighting maintains a presence in certain commercial and institutional applications, though its market share continues to decline as LED retrofits offer compelling returns on investment with payback periods typically under two years.

By Material: Metal Frameworks Anchor the Industry, Crystal Outpaces in Luxury Tier

Metal frames account for 39.59% of revenue because aluminum and steel remain indispensable for structural integrity across price points. The sector consumed about 287,000 tons of aluminum and 143,000 tons of steel in 2024, with recycled content approaching 48% as sustainability goals spread. Rising metal prices—aluminum rose 12.3%—drive manufacturers to adopt precision stamping and additive methods that reduce scrap.

Crystal elements, while smaller in absolute volume, expand at 7.25% CAGR as aspirational homeowners and hospitality operators seek high-impact optics. Imports of crystal parts rose 22.7% in 2024, sourced mainly from Europe’s long-established artisan clusters. Glass diffusers remain mainstream, aided by tempered and borosilicate innovations that improve light distribution and durability. Sustainable-specification projects increasingly specify wood accents, responding to green-building procurement guidelines that favor renewable materials.

By End-user: Residential Holds Majority; Commercial Gains Momentum

Homeowners commanded 57.56% of global revenue in 2025, reflecting steady do-it-yourself upgrades and professional remodels. Lighting ranks among the top five renovation tasks, with 3.7 million United States households performing fixture updates last year. Energy codes embedded in mortgage insurance guidelines further motivate efficient replacements. Digital dimming and color-tuning features, once restricted to commercial niches, now reach the living room, boosting ticket sizes.

Commercial installations grow faster at a projected 6.86% CAGR. Offices, retail, healthcare, and hospitality properties target lighting to lower operating costs and enhance occupant well-being. LEED and WELL building standards reward optimal lux levels, glare control, and circadian-supportive spectra, raising specification complexity and value. Government facility standards, echoed by private developers, increasingly dictate integrated controls, propelling demand for network-ready ceiling-mounted luminaires.

By Distribution Channel: Showrooms Still Dominate, Online Sales Accelerate

Brick-and-mortar showrooms and home centers process 70.35% of 2025 transactions. Tactile evaluation—finish, scale, brightness—remains critical for many buyers, and roughly 3,200 United States lighting showrooms continue to draw foot traffic. However, the 8.52% CAGR online segment steadily chips away, powered by enriched content, free returns, and last-mile capacity improvements. Furniture and décor e-commerce outpaced overall retail growth by a factor of three in 2024, with AR overlays easing visualization hurdles for large fixtures.

Marketplace convergence is inevitable: leading vendors pursue omnichannel strategies such as buy-online-pickup-in-store and virtual consultations. Regulations like the FTC’s merchandise delivery rule safeguard consumer rights, fostering trust in web-based purchases that include fragile or oversized items. Over time, channel lines will blur as physical stores evolve into experiential hubs while online platforms excel at assortment breadth.

Geography Analysis

North America retains the greatest chunk of the ceiling lights & chandeliers market revenue with 34.50% of market share in 2025. United States households spent USD 457 billion on improvements in 2024, with lighting upgrades a large beneficiary . Around 2.1 billion ceiling fixtures are installed nationally, and replacement rates sit near 8.3% each year. Canadian policy leans heavily on energy performance, advancing LED share beyond United States levels. Mexico’s domestic factories saw lighting output rise 12.7% in 2024 as exporters diversified away from Asia.

Asia-Pacific is the fastest-growing territory, set for 8.78% CAGR to 2031. China added 106 million new urban residents between 2020-2024, swelling demand for residential fixtures. India needs 25 million additional homes by 2030, and lighting typically equals 2.7% of construction budgets. Japan’s domestic LED output climbed 15.3% in 2024 as renovation cycles accelerated. Korea reached 78% LED penetration in 2024 on the back of stringent energy codes. Singapore’s Green Mark program pushes Southeast Asian developers toward efficient luminaires.

Europe remains influential owing to its design heritage and tight regulation. The Ecodesign Directive fully phased out most halogen lamps by 2024, focusing sales on high-efficacy LEDs. Eurostat shows households spend EUR 213 (USD 187.21) yearly on lighting products and power, with daylight variability shaping regional differences. The UK cites lighting as 18% of commercial electricity load, spurring retrofit projects. Germany’s fixture manufacturing rose 3.7% in 2024 as suppliers pivoted to premium lines. France’s strict light-pollution rules strengthen demand for controlled-beam optics.

Competitive Landscape

Giants such as Signify, Acuity Brands, and OSRAM leverage scale to integrate lighting with broader smart-building platforms. Signify is piloting LiFi networks that convert fixtures into data-transmission nodes. Acuity Brands’ USD 1.115 billion acquisition of QSC brings cloud-managed audio-video systems under one roof, aligning with its “Intelligent Spaces” strategy. Mid-tier players pursue specialization—Eglo thrives on European-centric decorative portfolios, while Kichler targets North American residential upgrades.

White-space emerges at the crossroads of daring design and embedded intelligence. Agile newcomers combine artisanal crystal craft with Bluetooth-mesh drivers to capture design-led but tech-savvy buyers. Digitally enabled manufacturing lets incumbents cut lead times by 40%, unleashing mass customization that addresses varied ceiling heights, color temperatures, and control protocols. Supply-chain resilience also shapes strategies: Signify shifted production out of China to mitigate tariff and geopolitical risks, partnering with Dixon Technologies in India in 2025 to serve both local and export demand.

Ceiling Lights & Chandeliers Industry Leaders

Signify (Philips Lighting)

Acuity Brands Lighting

OSRAM GmbH

Eglo Leuchten

Kichler Lighting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Signify and Dixon Technologies unveil a joint venture aimed at expanding Indian fixture manufacturing capacity, signifying diversification beyond China.

- May 2025: Signify pilots a WiFi-over-light initiative with US Ignite, showcasing LiFi’s city-scale potential.

- March 2025: Proluxe by American Lighting introduces ChromaDMX Downlight for affordable color-tunable installs.

- December 2024: Bond expands its smart-home platform to unify multi-brand lighting control.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the ceiling lights and chandeliers market as factory-built indoor fixtures that are permanently fastened to the ceiling and provide general or decorative illumination. Product styles span flush and semi-flush mounts, recessed downlights, pendants, drop lights, and branched chandeliers that range from traditional crystal pieces to contemporary LED designs. All revenues are recorded at ex-factory level and expressed in USD.

Scope exclusion: Portable table or floor lamps, outdoor luminaires, and aftermarket bulbs are outside the study.

Segmentation Overview

- By Product Type

- Ceiling Lights

- Flush/Surface Mount

- Semi-Flush

- Recessed Downlights

- Pendant & Drop Lights

- Chandeliers

- Traditional

- Transitional

- Modern / Contemporary

- Ceiling Lights

- By Lighting Technology

- LED

- Fluorescent

- Incandescent & Halogen

- HID & Others

- By Material

- Metal

- Crystal

- Glass

- Wood & Natural Materials

- Plastics & Composites

- By End-user

- Residential

- Commercial

- Offices and Co-Working Spaces

- Hospitality (Hotels, Resorts, Restaurants)

- Retail & Shopping Malls

- Healthcare Facilities

- Educational Institutions

- Industrial

- By Distribution Channel

- Offline/Showrooms & Specialty Stores

- DIY and Home-Improvement Chains

- Online/E-commerce Platforms

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with fixture manufacturers, distributors, builders, and lighting designers across North America, Europe, and Asia-Pacific validate ASP brackets, channel margins, and adoption of smart LED drivers. Surveys of homeowners and hotel procurement teams further refine penetration rates for premium chandeliers versus mass-market flush mounts.

Desk Research

Our analysts begin by mapping the installed base and replacement cycle using open datasets such as the U.S. Department of Energy Solid-State Lighting program, Eurostat building permits, UN Comtrade HS940510 trade flows, and LightingEurope shipment reports. Macro indicators, housing completions from the U.S. Census, hospitality pipeline counts from STR, and renovation spending from FRED help size demand pools across residential and commercial end users. Paid databases including D&B Hoovers for company revenues and Dow Jones Factiva for press releases add context on pricing moves and capacity expansions. The sources listed are illustrative; many additional public and proprietary references feed our desk review.

Market-Sizing & Forecasting

A blended top-down, bottom-up model is applied. Top-down sizing derives ceiling fixture demand from new-build floor area, renovation spend, and average fixture density per square meter, which are then multiplied by region-specific ASPs. Bottom-up checks roll up sampled manufacturer shipments and online sales audits to align totals. Key variables include LED share, urban household growth, hotel room additions, renovation frequency, retail price dispersion, and currency movement. Forecasts use multivariate regression with GDP per capita, residential starts, and LED price elasticity as drivers; ARIMA smoothing adjusts for pandemic and policy shocks. Data gaps in emerging regions are bridged with trade-flow proxies and calibrated expert opinions.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance tests against historical series, ratio checks versus housing stock, and peer sense checks. Reports refresh every twelve months, with interim updates triggered by material events such as tariff shifts or major code changes. A final pre-publication pass ensures the client receives the latest numbers.

Why Our Ceiling Lights & Chandeliers Baseline Earns Trust

Published estimates often diverge because each publisher defines fixtures, geographic coverage, and replacement timing in unique ways.

According to Mordor Intelligence, aligning scope to permanent indoor ceiling units and using square-meter penetration ratios yields a balanced view that avoids both over-aggregation and narrow undercounts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.05 B (2025) | Mordor Intelligence | - |

| USD 38.00 B (2025) | Regional Consultancy A | Excludes smart recessed fixtures; treats chandelier imports separately, lowering base |

| USD 47.96 B (2024) | Trade Journal B | Combines ceiling lights with architectural downlights and applies full list prices, inflating total |

| USD 8.47 B (2025) | Industry Association C | Reports chandelier segment only, omitting flush/surface mounts |

Taken together, the comparison shows that our disciplined scope selection, mixed-method modeling, and annual refresh give decision-makers the most dependable baseline for sizing opportunities and planning strategy.

Key Questions Answered in the Report

What is the current size of the ceiling lights & chandeliers market?

The market is valued at USD 42.18 billion in 2026 and is projected to reach USD 54.69 billion by 2031.

Which region leads the ceiling lights & chandeliers market?

North America holds the largest regional share, supported by high renovation spending and smart-home adoption.

How fast are smart LED fixtures growing within the ceiling lights & chandeliers industry?

Smart or connected LED systems are forecast to register an 10.95%CAGR between 2026-2031.

What share of sales still moves through physical stores?

Offline showrooms and home-center chains captured 70.35% of global revenue in 2025, though e-commerce is expanding at a 8.52% CAGR.

Who are the top companies in this space?

Signify, Acuity Brands Lighting, OSRAM GmbH, Eglo Leuchten, and Kichler Lighting together controlled major market share of worldwide revenue in 2024.

Page last updated on: