Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

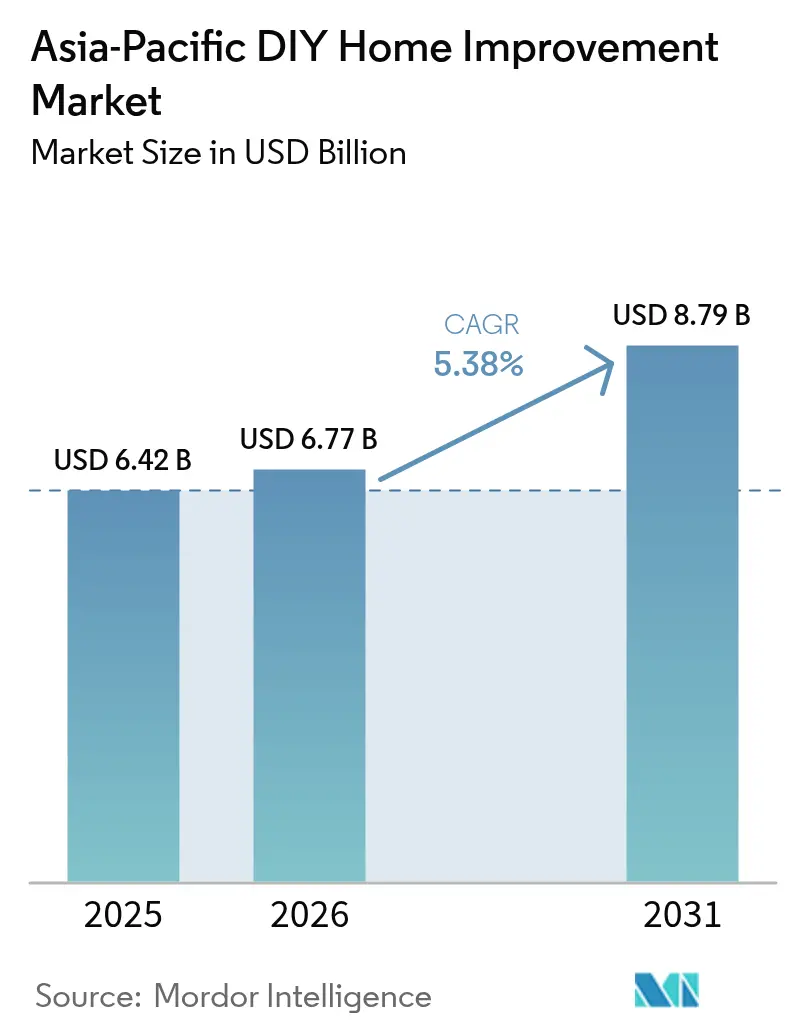

| Base Year Market Size (2025) | USD 6.42 Billion |

| Market Size (2026) | USD 6.77 Billion |

| Market Size (2031) | USD 8.79 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific DIY Home Improvement Market Analysis by Mordor Intelligence

The Asia-Pacific DIY home improvement market size is expected to grow from USD 6.42 billion in 2025 to USD 6.77 billion in 2026 and is forecast to reach USD 8.79 billion by 2031 at 5.38% CAGR over 2026-2031. Demand growth benefits from sustained urban migration, higher disposable incomes, and rising acceptance of self-directed renovation projects. Embedded finance options such as buy-now-pay-later have improved affordability, while omnichannel retail investments shorten delivery lead times and strengthen customer engagement. Consumer preference for manageable cosmetic upgrades and plug-and-play smart-home devices continues to lift transaction volumes. Regulatory shifts toward low-VOC and fire-safe materials are steering category premiumization, creating opportunities for compliant suppliers.

Key Report Takeaways

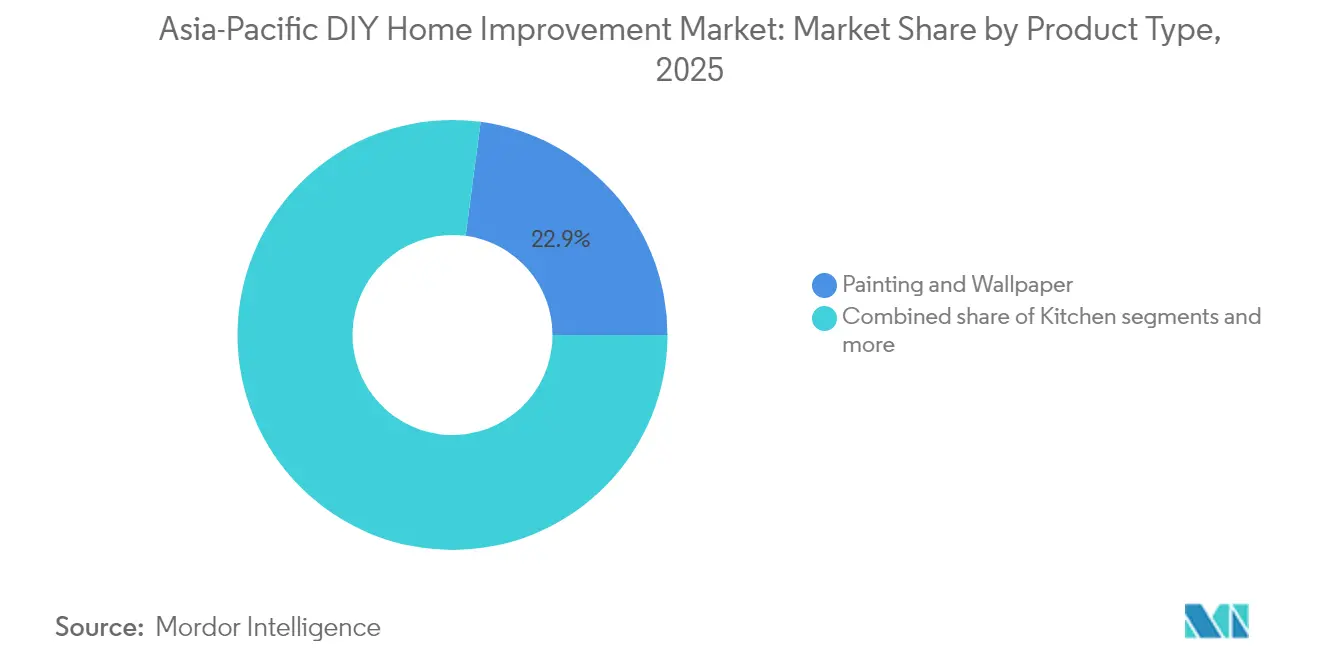

- By product type, painting and wallpaper led with 22.91% of the Asia-Pacific DIY home improvement market share in 2025, while smart-home installation add-ons are projected to advance at a 13.10% CAGR through 2031.

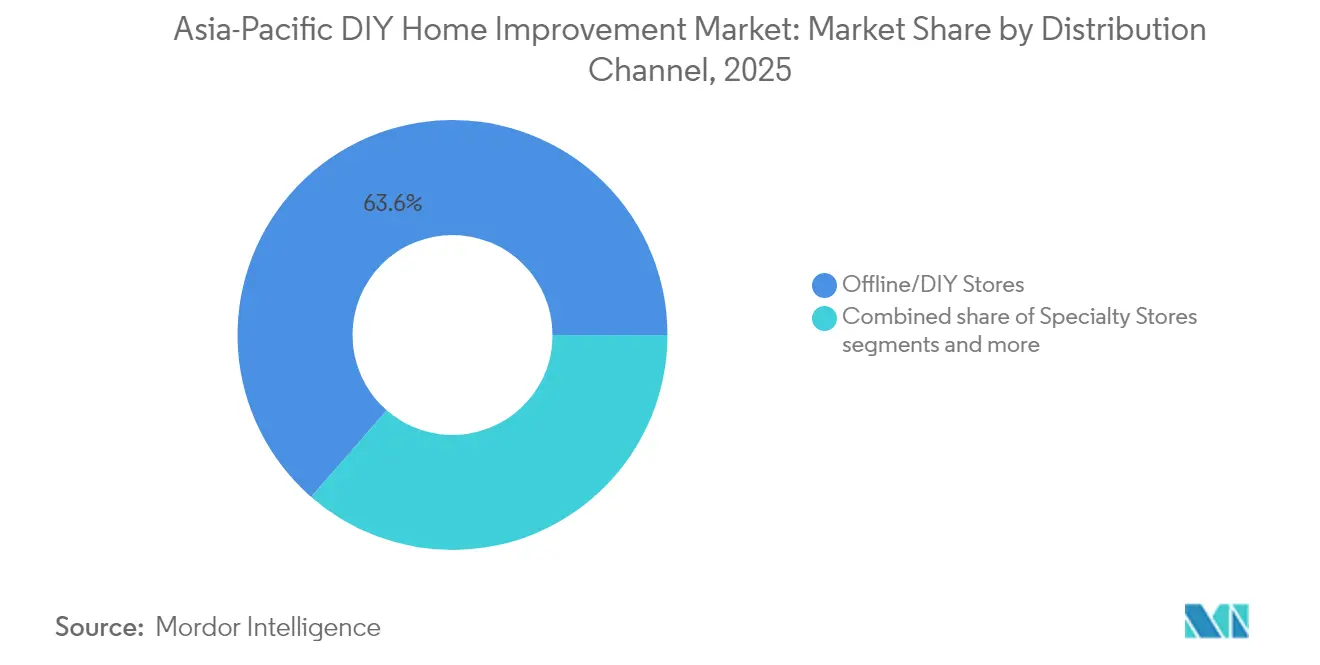

- By distribution channel, DIY home improvement stores held 63.58% share of the Asia-Pacific DIY home improvement market size in 2025; online channels are set to expand at an 17.68% CAGR between 2026-2031.

- By project complexity, minor cosmetic upgrades accounted for 44.71% of the Asia-Pacific DIY home improvement market size in 2025, and smart-home installations are tracking a 12.84% CAGR to 2031.

- By geography, China captured 31.88% of the Asia-Pacific DIY home improvement market share in 2025, whereas India is positioned for the fastest 10.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific DIY Home Improvement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and rising disposable incomes | +1.8% | China, India, and key Southeast Asian economies | Long term (≥ 4 years) |

| Omnichannel expansion of big-box DIY retailers | +1.2% | Australia, Thailand, Malaysia, Vietnam | Medium term (2-4 years) |

| E-commerce tutorials and influencer-led DIY culture | +0.9% | South Korea, Japan, wider Asia-Pacific | Short term (≤ 2 years) |

| Embedded finance and BNPL integrations | +0.7% | Southeast Asia, India | Medium term (2-4 years) |

| Regulatory push for low-VOC and fire-safe materials | +0.5% | China, Japan, Australia | Long term (≥ 4 years) |

| European softwood import diversification | +0.4% | Japan, South Korea, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid urbanization and rising disposable incomes

Urban migration in India is driving increased housing turnover and reducing renovation cycle durations. The preference for DIY solutions over contractor services in smaller urban apartments is driving a notable shift in consumer behavior, effectively expanding the addressable market beyond traditional metropolitan areas. Parallel demographic trends in countries such as Indonesia and Vietnam are contributing to the emergence of new households characterized by increased purchasing power and a growing inclination toward self-managed home improvement projects. These combined factors are expected to underpin long-term growth in the Asia-Pacific DIY home improvement market, presenting significant opportunities for businesses operating in this space.

Omnichannel expansion of big-box DIY retailers

Regional chains are digitizing inventory and fulfilment to match e-commerce standards while leveraging store networks for click-and-collect convenience. Bunnings recorded 5.1% digital sales growth in the first half of fiscal 2024, supported by two-hour collection windows for loyalty members[1]Wesfarmers Limited, “2024 Half-year Report,” wesfarmers.com.au . Big-box retailers enhance their in-store value proposition by offering integrated tutorials, tool rental services, and project consultations, which cater to customer needs and foster engagement. Additionally, the strategic implementation of micro-fulfillment within existing outlets optimizes last-mile logistics by reducing associated costs and improving delivery efficiency for bulky goods. This approach strengthens the competitive positioning of big-box formats in the market.

E-commerce tutorials and influencer-led DIY culture

Online content lowers perceived project complexity, boosting consumer confidence in tackling advanced tasks. Retailers are increasingly integrating augmented-reality applications into their websites, enabling consumers to visualize room transformations before making a purchase. This technological advancement has contributed to a measurable decline in product return rates. Additionally, influencer endorsements are playing a pivotal role in driving product discovery, particularly among younger demographics who place significant value on peer-driven recommendations. In response to these trends, manufacturers are strategically designing visually appealing, easy-to-assemble kits that cater to consumer preferences and are optimized for social media engagement, thereby enhancing brand visibility and customer interaction.

Embedded finance and BNPL integrations

Atome agreements with Southeast Asian retailers exemplify this shift toward frictionless credit at the point of sale[2]Atome Financial, “BNPL Services in Southeast Asia,” atome.sg . Efficient KYC verification processes enable swift approvals, significantly improving consumer access to high-value products, including power tools and multi-room paint bundles. Regulatory bodies generally regard BNPL as a strategic instrument for advancing financial inclusion. This supportive regulatory perspective is anticipated to sustain the market's growth trajectory over the medium term, further solidifying its role in expanding consumer purchasing power and driving market development.

Restraints Impact Analysis*

| Restraint | (~) ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortages and material cost inflation | -1.4% | Japan, Australia, South Korea | Medium term (2-4 years) |

| Commodity and freight volatility are causing stockouts | -0.8% | Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Low DIY skill levels are driving professional outsourcing | -0.6% | China, India, Indonesia | Long term (≥ 4 years) |

| Stringent insurance and permit rules in hazard zones | -0.3% | Australia, Japan, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-labour shortages and material cost inflation

Since 2020, Japan has experienced a significant decline in its construction workforce, resulting in extended contractor wait times of up to six months. This labour shortage has compelled homeowners to explore alternative self-help solutions to address their construction and renovation needs. In 2024, Queensland experienced a significant increase in installer wages, reflecting heightened demand for skilled labour. The state faces a critical shortage, requiring an additional 18,000 tradespeople to meet market needs and sustain ongoing projects. Tool makers that simplify installation steps gain share as consumers replace labour costs with equipment purchases. Complex electrical or plumbing work remains out of scope for most DIY enthusiasts, limiting uptake in higher-value renovation categories.

Low DIY skill levels are driving professional outsourcing

The preference for professional craftsmanship in China and India significantly limits the adoption of self-installation practices for complex tasks. This trend is further reinforced by insurance policies that exclude coverage for installations performed by non-professionals, discouraging risk-averse homeowners from undertaking such activities. Recognizing these barriers, manufacturers and retailers are implementing targeted strategies, including the development of localized instructional videos and the organization of in-store workshops. These initiatives aim to enhance consumer proficiency, gradually bridging the skills gap and fostering greater confidence among homeowners in managing installation tasks independently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Integration Drives Category Evolution

Painting and wallpaper retained 22.91% of the Asia-Pacific DIY home improvement market share in 2025, highlighting consumer interest in visually impactful yet straightforward projects. Smart-home add-ons are set to register a 13.10% CAGR through 2031, fueled by falling IoT hardware prices and the adoption of the Matter 1.4 interoperability standard MATTER.ORG. Demand for smart lighting, automated blinds, and voice-controlled devices lifts accessory tool sales, benefiting hardware suppliers. Kitchen renovation products sustain momentum as cooking-at-home habits persist, while modular cabinet kits attract renters seeking reversible upgrades. Regulatory requirements limit consumer forays into high-voltage electrical work, but low-voltage LED and switch replacements remain accessible. Lumber and landscape management growth trails other categories due to climate-related supply disruptions, although stabilized softwood imports support volume recovery. Across categories, manufacturers embed guided instructions and QR-linked videos, further lowering entry barriers.

Smart-home penetration reshapes competitive dynamics by encouraging partnerships between device makers and traditional DIY retailers. Tools bundled with calibration apps shorten installation time, and cross-selling opportunities emerge as homeowners integrate sensors with existing renovation plans. Premium paints formulated for low-VOC compliance command margins despite broader price sensitivity. Flooring and building materials benefit from urban apartment refurbishments, especially in China, where renovation cycles shorten and regulatory standards raise material specifications. Integrated product-service bundles, such as paint plus virtual colour simulation, help retailers differentiate and increase basket size.

By Distribution Channel: Digital Acceleration Reshapes Retail

DIY home improvement stores captured 63.58% of the Asia-Pacific DIY home improvement market size in 2025, reflecting entrenched footfall and the tactile nature of product selection. Nevertheless, online sales are projected to climb at an 17.68% CAGR to 2031, driven by mobile commerce expansion and improved logistics infrastructure. Amazon’s Global Selling program facilitated USD 13 billion in Indian exports by end-2024, with home improvement categories recording 20% annual growth . Cross-border platforms allow regional manufacturers to reach distant customers, compressing traditional distribution hierarchies. Specialty stores pivot toward niche assortments and expert consultation to defend against pricing pressure from larger rivals. Social commerce channels blend content and checkout, capturing younger demographics seeking inspiration and immediate purchase. Traditional retailers respond with robust click-and-collect offerings and loyalty programs that integrate online and offline rewards, preserving traffic to physical outlets.

Transformational logistics investments deepen competitive advantages for scale players. In September 2025, Flipkart strategically increased its fulfilment capacity by 3.5 million square feet across India. This expansion is expected to significantly enhance the company's operational efficiency and broaden its two-day delivery coverage, thereby strengthening its competitive position in the e-commerce market. Bunnings deploys branch stores as micro-fulfilment nodes, achieving same-day delivery in metropolitan Australia. Consistent on-shelf availability remains critical for in-store conversion, prompting retailers to adopt predictive replenishment tools that leverage transaction data from both channels.

By Project Complexity: Simplification Enables Market Expansion

Minor cosmetic upgrades held 44.71% of the Asia-Pacific DIY home improvement market size in 2025, underscoring the dominance of quick weekend tasks that carry limited risk. Smart-home installations represent the fastest-growing complexity tier at a 12.84% CAGR, propelled by wireless connectivity that avoids invasive rewiring. Manufacturers design plug-and-play hubs and adhesive mounts to bypass drilling, and retailers curate starter bundles that include step-by-step mobile app guidance. Structural renovations still demand contractor involvement owing to regulatory permits and safety considerations, though prefabricated wall panels and modular extensions gradually lower entry hurdles for advanced enthusiasts. Outdoor landscaping projects gain seasonal momentum, especially in drought-prone markets where water-efficient gardens appeal to cost-conscious homeowners. Augmented-reality measurement tools help consumers plan layouts accurately, reducing material wastage and boosting purchase confidence.

Regulatory authorities in high-risk zones establish clear guidelines distinguishing tasks that homeowners can perform independently from those requiring the expertise of licensed professionals. This regulatory framework ensures consumer protection while enabling the growth of the DIY market in non-critical areas. Additionally, collaborations between retailers and insurance providers focus on implementing educational initiatives that define the scope of compliant projects. These efforts aim to reduce liability risks and encourage the adoption of responsible DIY practices, fostering a balanced and sustainable market environment.

Geography Analysis

China led with 31.88% Asia-Pacific DIY home improvement market share in 2025, supported by an integrated manufacturing base that keeps unit costs competitive. The dishwasher market demonstrated strong performance in 2023, achieving a valuation of USD 1.53 billion (11.2 billion CNY), reflecting sustained demand for appliance upgrades. The extensive penetration of e-commerce platforms, particularly in major urban centres, has played a pivotal role in driving consumer behavior. Features such as same-day delivery have significantly influenced impulsive renovation-related purchases, further bolstering market growth.

India is forecast to deliver the fastest 10.95% CAGR through 2031. Shorter renovation cycles and rising middle-class income underpin growth, while tier-2 and tier-3 cities emerge as new demand centres. Amazon’s cumulative USD 26 billion investment pipeline earmarks significant fulfillment and seller services spending for home categories. IKEA’s plan to double its Indian store count by 2030, complemented by compact formats, signals confidence in long-term DIY potential.

Japan and South Korea exhibit mature DIY cultures with high technological sophistication. Homeowners favor energy-saving smart systems, aligning with national sustainability goals. South Korea’s smart-home market is on track to surpass USD 6 billion by 2026, reflecting high broadband penetration and consumer appetite for integrated automation solutions. Australia and New Zealand maintain stable growth based on high home-ownership rates and an established project culture. Emerging Southeast Asian economies, Indonesia, Thailand, Vietnam, and Malaysia, deliver double-digit growth as urbanization and disposable income rise. Retailers entering these markets adapt assortments to local housing formats, humidity conditions, and regulatory standards. The Rest of Asia-Pacific cluster presents pockets of opportunity but requires tailored go-to-market strategies acknowledging divergent cultural views on self-installation.

Competitive Landscape

The Asia-Pacific DIY home improvement market is moderately fragmented, with the top participants collectively controlling roughly one-fourth of revenue. Big-box channels such as Bunnings and Mr DIY rely on deep product assortments, installation services, and rapidly growing online storefronts to reinforce customer loyalty. Bunnings is transforming select stores into family-oriented Hammerbarn concepts following a media partnership, boosting footfall during off-peak periods. Mr DIY continues fast expansion across Southeast Asia, supported by standardized store designs that optimize inventory turns.

E-commerce leaders Amazon and Flipkart pour capital into warehousing and last-mile fleets to capture the bulky goods share. Amazon commissioned 12 new fulfillment centers with 8.6 million cu ft capacity in 2025, enhancing one-day coverage for paint and power-tool categories. Flipkart countered with dark-store expansion supporting quick-commerce pilots that deliver small hardware items within one hour. Supply chain technology, including AI-driven demand forecasting, allows these platforms to manage SKU complexity and minimize stockouts.

Disruption stems from fintech and social-commerce entrants. BNPL providers integrate loyalty analytics that recommend complementary items based on project flow, lifting basket sizes. Direct-to-consumer tool brands leverage influencer partnerships to penetrate niche segments such as precision woodworking kits. Compliance costs tied to new environmental regulations favour scale players capable of funding certification and eco-label audits. Mergers and strategic property transactions, such as Wesfarmers’ USD 143 million BWP Trust management split, realign capital toward core retail innovation.

Asia-Pacific DIY Home Improvement Industry Leaders

Wesfarmers Ltd (Bunnings)

Mr DIY Group (Berhad)

HomePro Public Co.

Komeri Co. Ltd.

Kingfisher plc (B&Q China)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Flipkart and Amazon India expanded fulfillment networks by 3.5 million sq ft and 8.6 million cu ft, respectively, ahead of the festive season to enhance delivery of bulky DIY products.

- June 2025: Wesfarmers finalized a AUD 143 million management split of BWP Trust to unlock capital for Bunnings' digital upgrades.

- April 2025: IKEA confirmed plans to double its Indian store count by 2030 with compact formats targeting tier-2 cities.

- May 2025: IKEA enlarged its Family loyalty program across Asia-Pacific, adding cross-channel rewards.

Asia-Pacific DIY Home Improvement Market Report Scope

Do-it-yourself (DIY) is the act of designing and modifying anything by yourself. Customers could develop eye-catching projects without any professional help.

The Asia-Pacific DIY home improvement market is segmented by product type, distribution channel, and geography. By product type, the market is sub-segmented into lumber and landscape management, décor and indoor garden, kitchen, painting and wallpaper, tools and hardware, building materials, lighting, plumbing and equipment, flooring, repair and replacement, and electrical work. By distribution channel, the market is sub-segmented into DIY home improvement stores, specialty stores, online stores, and other stores. By geography, the market is sub-segmented into Australia, China, India, Japan, New Zealand, South Korea, Indonesia, and the rest of Asia-Pacific.

The report offers market sizes and forecasts in value (USD) for all the above segments.

By Product Type

| Lumber and Landscape Management |

| Decor and Indoor Garden |

| Kitchen |

| Painting and Wallpaper |

| Tools and Hardware |

| Building Materials |

| Lighting |

| Plumbing and Equipment |

| Flooring |

| Repair and Replacement |

| Electrical Work |

By Distribution Channel

| DIY Home Improvement Stores |

| Specialty Stores |

| Online |

| Other Channels |

By Geography – Country Level

| China |

| India |

| Japan |

| South Korea |

| Australia & New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Rest of Asia-Pacific |

By Project Complexity

| Minor Cosmetic Upgrades |

| Structural Renovations |

| Outdoor Landscaping Projects |

| Smart-Home Installations |

| By Product Type | Lumber and Landscape Management |

| Decor and Indoor Garden | |

| Kitchen | |

| Painting and Wallpaper | |

| Tools and Hardware | |

| Building Materials | |

| Lighting | |

| Plumbing and Equipment | |

| Flooring | |

| Repair and Replacement | |

| Electrical Work | |

| By Distribution Channel | DIY Home Improvement Stores |

| Specialty Stores | |

| Online | |

| Other Channels | |

| By Geography – Country Level | China |

| India | |

| Japan | |

| South Korea | |

| Australia & New Zealand | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| By Project Complexity | Minor Cosmetic Upgrades |

| Structural Renovations | |

| Outdoor Landscaping Projects | |

| Smart-Home Installations |

Key Questions Answered in the Report

How big is the Asia-Pacific DIY home improvement market in 2026?

The market stands at USD 6.77 billion in 2026 and is forecast to reach USD 8.79 billion by 2031.

Which product category holds the largest share?

Painting and wallpaper lead with a 22.91% share in 2025 because it offers high visual impact with low technical complexity.

What is the fastest-growing product segment?

Smart-home installation add-ons are projected to grow at a 13.10% CAGR through 2031 as IoT device prices fall and installation becomes easier.

What years does this Asia-Pacific DIY Home Improvement Market cover, and what was the market size in 2025?

In 2025, the Asia-Pacific DIY Home Improvement Market size was estimated at USD 6.77 billion. The report covers the Asia-Pacific DIY Home Improvement Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Asia-Pacific DIY Home Improvement Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

What role does BNPL play in the sector?

Embedded buy-now-pay-later finance increases average order values by up to 60% by spreading out payments without added interest.How fragmented is the competitive landscape?

How fragmented is the competitive landscape?

The top players together hold about one-fourth of regional revenue, indicating moderate fragmentation and room for new entrants.

Page last updated on: