Online Survey Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.43 Billion |

| Market Size (2031) | USD 15.12 Billion |

| Growth Rate (2026 - 2031) | 18.67% CAGR |

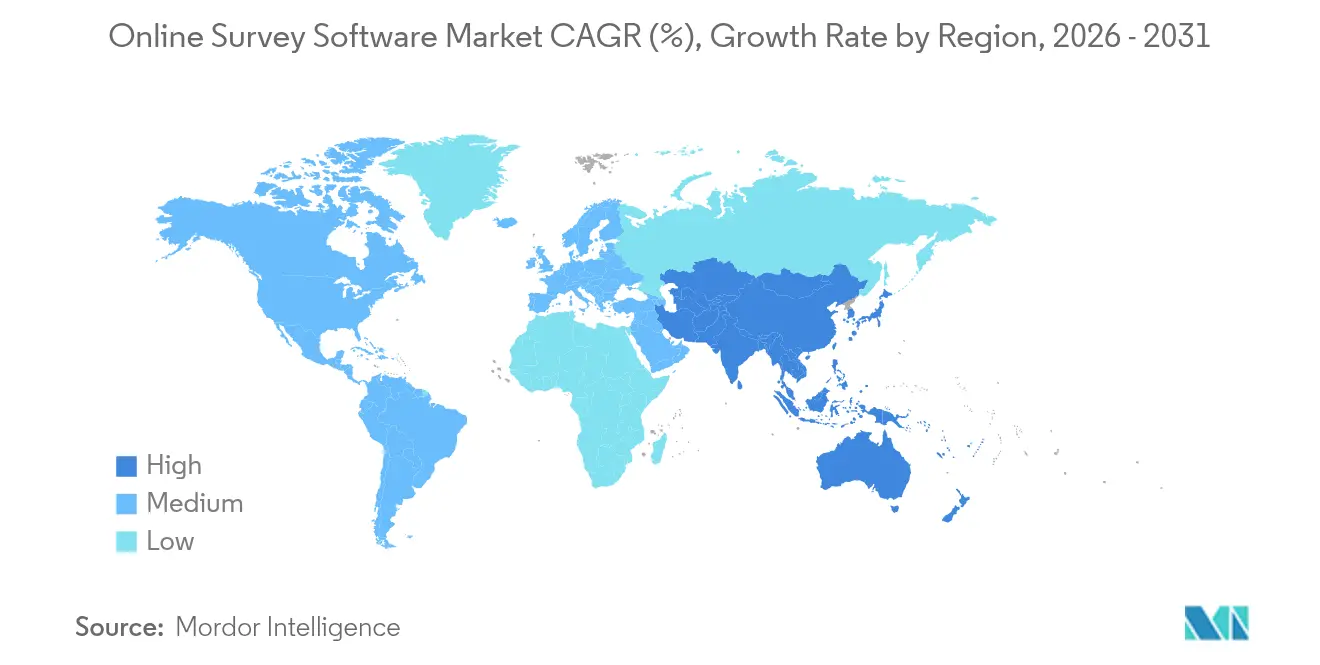

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Survey Software Market Analysis by Mordor Intelligence

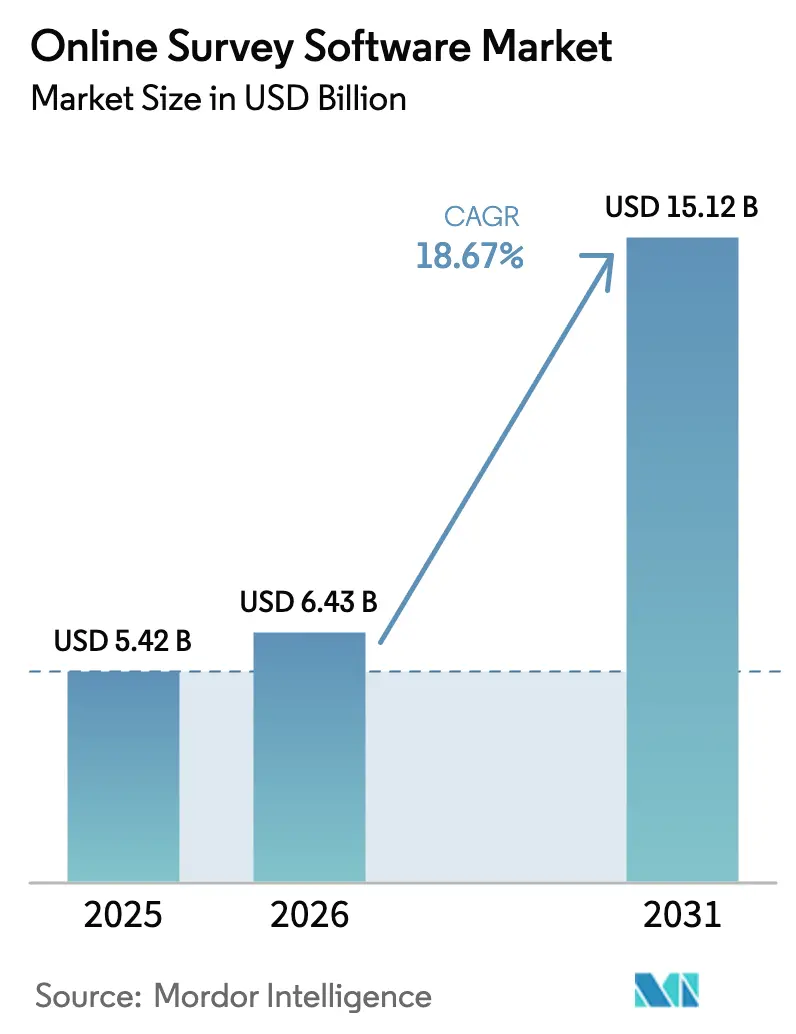

The Online Survey Software Market size is projected to expand from USD 5.42 billion in 2025 and USD 6.43 billion in 2026 to USD 15.12 billion by 2031, registering a CAGR of 18.67% between 2026 to 2031.

At this scale, the online survey software market size for 2025 positions the category among the fastest-expanding cloud applications. Growth rests on three structural forces: enterprises embedding survey tools in experience-management workflows, generative AI reducing response friction, and privacy-preserving analytics keeping data collection compliant in stricter regulatory climates. Cloud deployment already accounts for more than 70% of spend, and mobile-first channels such as WhatsApp surveys deliver materially higher response rates, supporting sustained adoption. Competitive dynamics remain moderate; market leaders retain scale advantages yet still face disruption from niche providers that exploit localization, vertical templates, and conversational interfaces

Key Report Takeaways

- By organization size, large enterprise platforms captured 64.62% of the online survey software market share in 2025; small and medium businesses are expanding at a 21.12% CAGR through 2031.

- By deployment model, cloud solutions commanded 71.85% of the online survey software market size in 2025 and are set to advance at a 19.78% CAGR.

- By application, customer experience and feedback led with 42.15% revenue share in 2025, while academic and public sector research is projected to grow at 23.15% CAGR to 2031.

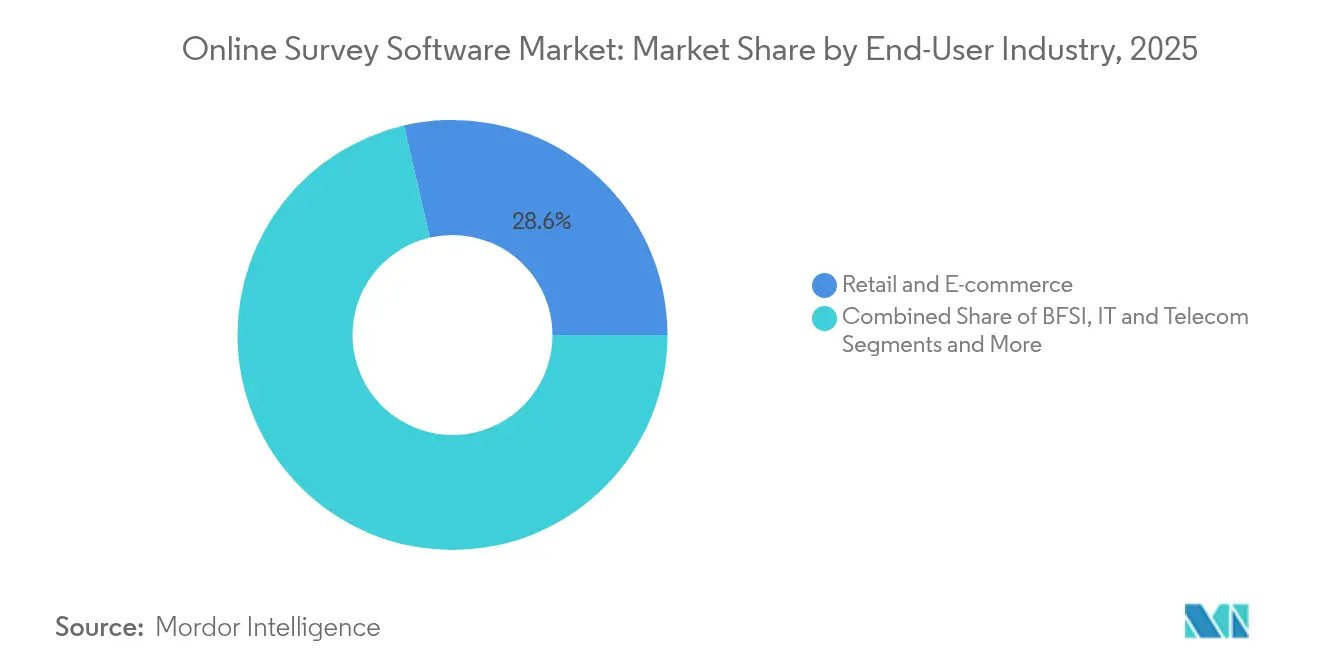

- By end-user industry, retail and e-commerce held 28.63% of the online survey software market share in 2025; the government and public sector will post the fastest 21.07% CAGR.

- By distribution channel, email and web links delivered 40.12% of responses in 2025, whereas social media and messaging apps will accelerate at 22.09% CAGR.

- By Geography, North America delivered 40.88% of responses in 2025, whereas Asia Pacific will accelerate at 24.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Survey Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile internet and smartphone expansion | +3.2% | Global (Asia-Pacific strongest) | Medium term (2-4 years) |

| Demand for data-driven decision-making | +4.1% | North America, EU, Asia-Pacific | Long term (≥ 4 years) |

| Cloud-based SaaS survey adoption | +2.8% | Global (SMB focus) | Short term (≤ 2 years) |

| Generative-AI real-time questionnaire optimisation | +1.9% | North America, EU | Medium term (2-4 years) |

| Privacy-preserving analytics | +2.3% | EU leading | Long term (≥ 4 years) |

| Vertical-specific templates for SMBs | +1.5% | Emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-based SaaS survey adoption

Cloud-first procurement dominates as 72.41% of spending now flows to subscription models that avoid on-premise capital outlays.[1]Macquarie Group, “Global Cloud Spending Outlook 2024,” macquarie.coPublic-cloud spending surpassed USD 585 billion in 2024, reinforcing the appetite for elastic infrastructure. Among United States SMBs, SaaS penetration has climbed to 86% and is projected to reach 96%, widening the online survey software market by removing the technical debt often linked to older survey tools. Continuous delivery lets vendors roll out security patches and AI features with no customer intervention. Hybrid pricing blending seat-based and usage-based components is growing at 21% median rates, aligning vendor revenue with delivered value maxio.com. Together these factors cement cloud platforms as the default choice when organizations refresh feedback technology.

Generative-AI real-time questionnaire optimisation

Forty-four percent of SaaS suppliers now charge separately for AI modules, validating demand for automated question design.[2]Maxio, “The SaaS Pricing Benchmark Report 2024,” maxio.com SurveyMonkey’s Genius engine recommends phrasing that lifts completion rates, and early adopters capture 33% higher revenue from AI-enhanced insights. Generative AI personalizes question order in real time, nudging respondents through conversational flows that lower abandonment. Bias detection algorithms refine wording before launch, safeguarding data quality. As survey fatigue rises, this adaptive capability differentiates platforms beyond classic form builders and sustains user engagement at scale.

Demand for data-driven decision-making

Across industries, feedback loops are being wired straight into operational systems. In healthcare, 89% of providers already run digital projects that depend on patient sentiment measurements.[3]ATandT Business, “Healthcare Digital Transformation Survey 2025,” att.comUniversities mirror the pattern: 88% of UK higher-education institutions rely on Jisc online surveys for accreditation and governance. Qualtrics’ USD 12.5 billion valuation highlighted how survey data underpins experience-management platforms that influence daily decisions, from product roadmaps to employee retention plans. This strategic framing turns the online survey software market into critical infrastructure for customer and workforce intelligence.

Privacy-preserving analytics

Seventy percent of consumers now block tracking cookies, magnifying the value of consent-based zero-party data collected through engaging surveys. GDPR and CCPA pressure platforms to encrypt, anonymize, and store data under explicit consent models. Vendors embedding privacy-by-design gain a compliance moat, appealing to multinational buyers concerned about fines. First-party survey data also substitutes for third-party analytics eroded by browser restrictions, ensuring organizations still gauge sentiment without invasive tracking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent privacy and compliance rules | -1.8% | EU leading | Long term (≥ 4 years) |

| Low switching cost and price competition | -2.1% | Global (SMB) | Short term (≤ 2 years) |

| Survey fatigue diminishing response rates | -1.5% | North America, EU | Medium term (2-4 years) |

| Anti-tracking measures limiting channels | -1.2% | Global mobile ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Survey fatigue diminishing response rates

Repeated survey requests erode willingness to participate, especially in education settings where multiple studies collide within a single term. Fatigue appears both before response, when invitations overwhelm users, and during longer questionnaires that strain attention. Despite the hazard, average response rates climbed from 48% in 2005 to 68% by 2020, signalling that gamification, micro-surveys, and progressive profiling can reverse attrition. Vendors now insert conversational interfaces and logic branching that shorten perceived length, yet fatigue remains a ceiling on growth until design best practices become universal.

Low switching cost and price competition

Cloud architectures make vendor migration as simple as exporting CSV files and reconnecting APIs, compressing margins in the online survey software industry. Freemium tiers proliferate, and promotional discounts abound as suppliers jostle for SMB wallets. Roughly 40% of SaaS deals now include multi-year terms, an attempt to lock-in customers contractually rather than technically. While buyers benefit from cheaper entry, the race to the bottom can starve smaller providers of R&D funds, slowing product innovation across the ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Dominance Drives Revenue Concentration

Large Enterprises generated 64.62% of revenue in 2025, consolidating the online survey software market around platforms that integrate with CRM, ERP, and identity-management stacks. Large organizations pay premiums for role-based access, advanced encryption, and multi-language support. Conversely, SMBs deliver the steepest 21.12% CAGR, propelled by template libraries aligned to retail, hospitality, and professional-services use cases. The online survey software market size for SMB adoption is expected to nearly triple between 2026 and 2031 as subscription pricing removes capital barriers. Providers balance both cohorts through tiered editions that share a common codebase yet scale from solo entrepreneurs to multinational rollouts.

The enterprise segment is maturing in North America and Western Europe, prompting vendors to upsell analytical add-ons rather than net-new seats. Growth shifts to emerging markets where midsize firms leapfrog on-premise legacy tools. SMB expansion also fuels ecosystem partnerships; accounting software vendors embed white-label survey functions, and payment gateways bundle feedback widgets to enrich merchant insights.

By Deployment Model: Cloud Migration Accelerates Infrastructure Transformation

Cloud implementations accounted for 71.85% of spending in 2025 and will widen their lead at 19.78% CAGR through 2031. In this segment, the online survey software market share favors vendors that engineered multitenant architectures from day one. Continuous delivery pipelines permit weekly feature drops, and usage-based billing aligns costs with seasonal survey bursts. On-premise installs persist in government, defense, and heavily regulated financial services where data sovereignty must remain inside national borders. That cohort, however, shrinks annually as sovereign-cloud regions and private-cloud offerings satisfy compliance yet retain SaaS convenience.

Hybrid models—cloud authoring with local data vaulting—bridge the two worlds. Enterprises in Japan and Germany increasingly demand such configurations, enabling them to meet strict residency rules while still tapping AI analytics that run in vendor clouds. The architectural flexibility extends the online survey software market size without forcing customers into an either-or deployment decision.

By Application: Customer Feedback Leadership Faces Academic Disruption

Customer experience programs still generate 42.15% of total spend, anchored by retail, banking, and travel brands tracking Net Promoter Scores in real time through survey software. Academic and public-sector surveys, however, post a 23.15% CAGR, signaling a diversification of demand. Universities use online instruments to satisfy accreditation bodies, and local governments field citizen panels for policy vetting. As these segments mature, vendors localize question banks to education and civic terminology, sharpening competitive moats within the survey software market.

Employee-engagement studies also rise, amplified by hybrid-work models seeking pulse checks on culture and well-being. Market-research agencies adopt AI-assisted survey logic to compress project timelines, while product managers embed micro-surveys in apps to steer release roadmaps. This breadth demonstrates how the online survey software market underpins feedback loops across organizational silos.

By End-User Industry: Retail Leadership Challenged by Government Growth

Retail and e-commerce players accounted for 28.63% of 2025 revenue, leveraging in-store QR codes and post-transaction emails to refine omnichannel journeys. Government and public entities, though, record the fastest 21.07% CAGR. National digital-service units deploy multilingual surveys to monitor citizen satisfaction with tax, licensing, and healthcare portals. Hospitals rank next in adoption intensity, integrating patient-reported outcomes into quality dashboards.

Financial-services groups employ surveys to gauge compliance experiences, especially after regulatory filings, while technology firms use developer-community feedback to optimize APIs. The dispersion of use cases underlines that the online survey software market is less a point solution and more a horizontal layer stitching together diverse operational insights.

By Survey Distribution Channel: Email Dominance Faces Social Media Disruption

Email and web links still deliver 40.12% of completions, supported by automation triggers in marketing clouds. Yet messaging apps and social networks are expanding at 22.09% CAGR, propelled by mobile-first usage in Asia and Latin America. WhatsApp surveys yield 35% higher response and 70% lower acquisition cost compared with legacy channels. Anti-tracking browser changes reduce efficacy of cookie-based pop-ups, nudging platforms toward authenticated first-party channels.

QR codes remain popular for transient contexts such as events, while SDK-embedded in-app surveys capture feedback at the moment of product interaction. These shifts ensure the online survey software market remains adaptive to evolving communication habits.

Geography Analysis

North America contributed 40.88% of 2025 revenue, reflecting long-standing SaaS maturity and headquarters concentration of major vendors. Enterprises in the United States routinely integrate survey outputs into CRM workflows and compliance dashboards, supporting sticky usage. Europe follows with strong demand anchored in GDPR-driven privacy innovation; many vendors pilot consent controls in the region before global release. The continent’s stringent rules shape product roadmaps that later appeal to multinational buyers.

Asia-Pacific stands out with a 24.31% CAGR through 2031. Smartphone ubiquity, super-app ecosystems, and government digital-identity projects create fertile ground for localized survey platforms. China’s domestic providers embed WeChat mini-program surveys, while India’s public-sector digitization amplifies need for citizen-satisfaction tools. Localization—language support, right-to-left layouts, and low-bandwidth optimization—proves decisive in capturing regional share.

Competitive Landscape

The online survey software market displays moderate concentration. Qualtrics, SurveyMonkey, and Typeform collectively account for a significant revenue block yet leave room for mid-tier challengers. Qualtrics secured a USD 12.5 billion take-private transaction in 2023, underscoring investor belief in experience-management platforms. SurveyMonkey posted USD 313 million in 2024 revenue, while Typeform advanced from USD 100 million to USD 141.1 million in twelve months, proving that differentiated UX and conversational design can carve share.

Artificial intelligence now frames competition: 44% of SaaS companies monetize AI features, forcing laggards to accelerate product roadmaps. Partnerships serve as force multipliers—Kantar with QuestionPro for panel access, SightX with Netquest for global sampling. Meanwhile, niche players attack verticals: healthcare-compliant offerings tout HIPAA certification; academic specialists integrate citation workflows. Mobile-native entrants exploit WhatsApp and Telegram APIs to sidestep email fatigue.

Online Survey Software Industry Leaders

SurveyMonkey (Momentive Inc.)

Qualtrics International Inc.

Alchemer LLC

Medallia Inc.

Typeform SL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Typeform appointed Bryce Winkelman as Chief Revenue Officer to drive global growth and launched “Typeform for Growth,” boosting enterprise clients by 36% year-over-year.

- December 2024: QuestionPro acquired SpatialChat, adding conversational engagement tools to its portfolio.

- November 2024: ProProfs bought PeopleGoal, merging performance-management and survey capabilities.

- October 2024: SurveyMonkey opened a new Bengaluru office, reinforcing its commitment to Asia-Pacific expansion.

Global Online Survey Software Market Report Scope

Online Survey Software enables individuals, businesses, and organizations to effortlessly create, distribute, and analyze surveys online. This digital tool simplifies the collection of data and feedback from target audiences, including customers, employees, and the general public, leveraging both web-based and mobile technologies.

The online survey software market is segmented by product (enterprise grade, individual grade), deployment (on-premise, cloud), application (education, healthcare and pharmaceutical, BFSI, retail, telecom and IT, others), and geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa)

The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Large Enterprises |

| Small and Medium Businesses (SMBs) |

| Cloud |

| On-premise / Self-Hosted |

| Customer Experience and Feedback |

| Employee Engagement and HR |

| Market Research and Product Testing |

| Academic and Public Sector Research |

| Event Feedback and Others |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| IT and Telecom |

| Education |

| Government and Public Sector |

| Others |

| Email and Web Links |

| Social Media and Messaging Apps |

| QR Codes and Kiosks |

| In-App / SDK Embedded |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Organization Size | Large Enterprises | ||

| Small and Medium Businesses (SMBs) | |||

| By Deployment Model | Cloud | ||

| On-premise / Self-Hosted | |||

| By Application | Customer Experience and Feedback | ||

| Employee Engagement and HR | |||

| Market Research and Product Testing | |||

| Academic and Public Sector Research | |||

| Event Feedback and Others | |||

| By End-User Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| IT and Telecom | |||

| Education | |||

| Government and Public Sector | |||

| Others | |||

| By Survey Distribution Channel | Email and Web Links | ||

| Social Media and Messaging Apps | |||

| QR Codes and Kiosks | |||

| In-App / SDK Embedded | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the online survey software market?

The online survey software market size reached USD 6.43 billion in 2026 and is projected to hit USD 15.12 billion by 2031.

Which segment grows fastest within the market?

Small and medium businesses are expanding at 21.12% CAGR, the highest among organization-size segments.

How important is cloud deployment for survey platforms?

Cloud models already hold 71.85% share and will continue to widen their lead at 19.78% CAGR thanks to scalability and cost efficiency.

What role does AI play in modern survey tools?

Generative AI optimizes question phrasing in real time, lifts completion rates, and now appears as a paid add-on in 44% of SaaS offerings.

Page last updated on: