Version Control System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

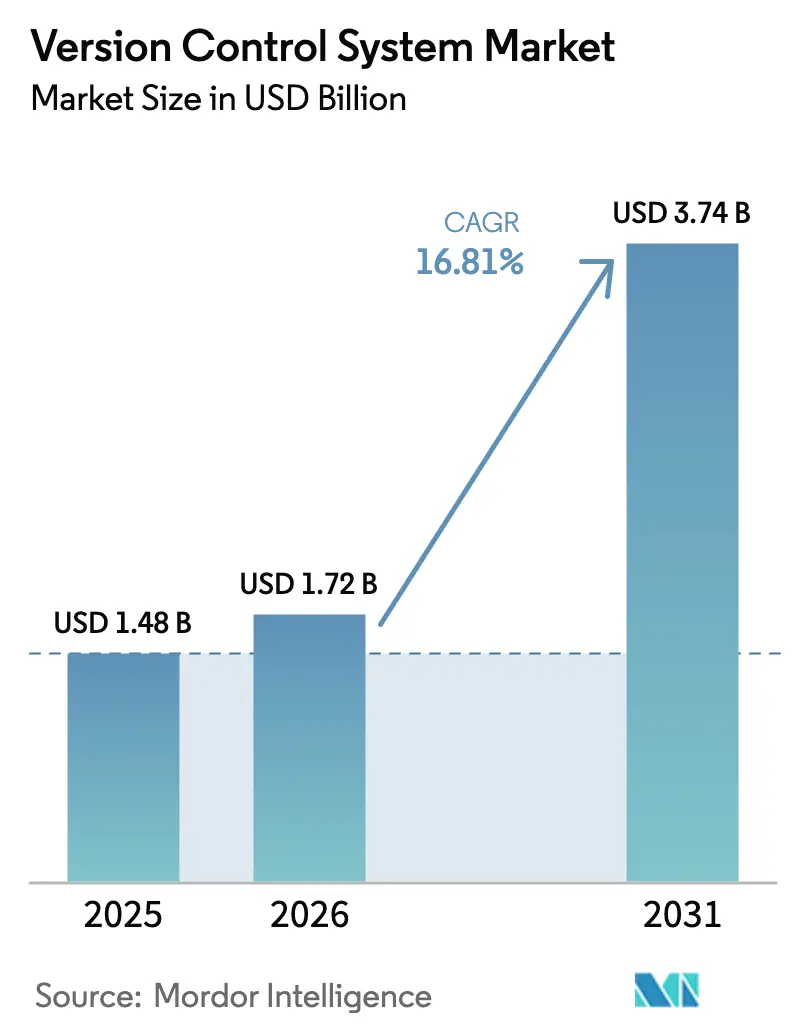

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 16.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Version Control System Market Analysis by Mordor Intelligence

The version control system market size is projected to be USD 1.48 billion in 2025, USD 1.72 billion in 2026, and reach USD 3.74 billion by 2031, growing at a CAGR of 16.81% from 2026 to 2031. Enterprises are consolidating fragmented toolchains around Git-based platforms that now bundle continuous integration, security scanning and artifact provenance, reflecting a shift to single-vendor DevSecOps suites. Joint software bill of materials guidance released by twenty-one cybersecurity agencies in September 2025 intensified buyer focus on compliance-ready repositories, while the rapid rollout of agentic AI services such as GitHub Copilot and GitLab Duo is turning the repository into a hub for human-AI collaboration. Demand is reinforced by cloud deployment’s elasticity, which supports surging commit volumes as teams adopt continuous delivery, and by the need for data-residency options that satisfy emerging sovereignty rules in Europe, Australia and the United States. Competitive intensity is growing as Microsoft, GitLab, and Atlassian race to integrate AI, signed-commit enforcement, and single-tenant architectures that appeal to regulated sectors.

Key Report Takeaways

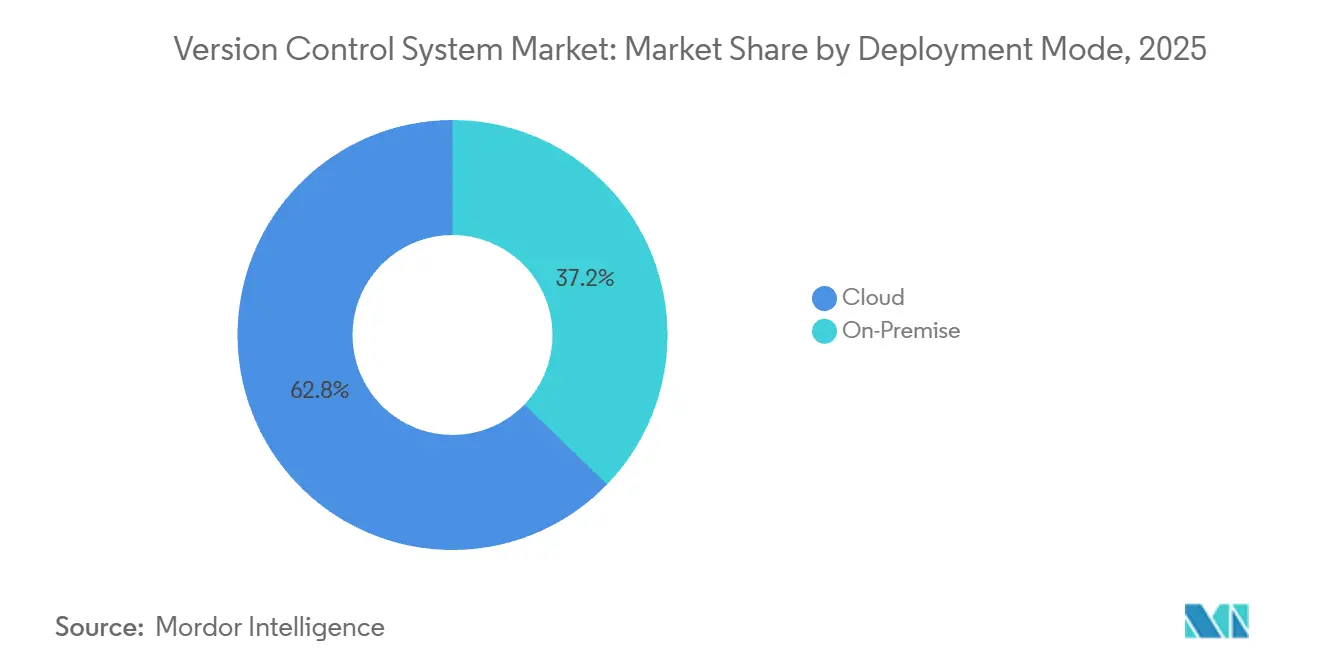

- By deployment mode, cloud held 62.77% of the version control system market share in 2025, while on-premise is forecast to expand at a 17.32% CAGR through 2031.

- By type, distributed platforms commanded 92.43% of the version control system market in 2025; centralized systems are projected to grow at a 17.64% CAGR through 2031.

- By end-user industry, IT and telecom led with 36.67% of share in 2025, whereas gaming and digital content is advancing at an 18.11% CAGR to 2031.

- By organization size, large enterprises accounted for 63.76% of the share in 2025, yet small and medium enterprises are growing at a 17.49% CAGR over 2026-2031.

- By organization size, large enterprises accounted for 63.76% of share in 2025, yet small and medium enterprises are growing at a 17.49% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Version Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream DevOps Pipeline Adoption | +4.2% | Global, high in North America, Europe and Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Cloud-Native Workflows | +3.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| AI-Assisted Code Review and Traceability | +3.5% | North America and Europe early, Asia-Pacific catching up | Short term (≤ 2 years) |

| Digital Product Compliance (SBOM, Secure Supply Chain) | +2.9% | North America and Europe, expanding in Asia-Pacific finance | Long term (≥ 4 years) |

| Cost Optimization Imperatives in Software Delivery | +2.1% | Global, acute in Asia-Pacific SMEs and North American mid-market | Medium term (2-4 years) |

| Real-Time Asset Collaboration in Gaming and Media | +0.9% | Major gaming hubs in North America, Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream DevOps Pipeline Adoption

Continuous integration workloads are soaring, illustrated by 11.5 billion GitHub Actions minutes consumed during 2024-2025, a 35% year-over-year increase that underscores tighter coupling between commits and automated testing.[1]Cassidy Williams, “What 986 Million Code Pushes Say About the Developer Workflow in 2025,” GitHub Blog, github.com Automotive firms such as Jaguar Land Rover trimmed feedback cycles by 99% and executed as many as 70 daily deploys after moving to GitLab’s unified DevSecOps environment. Survey data from Perforce shows 30% of automotive teams now bundle static analysis, version control, and continuous testing to raise code quality. Rising transaction volumes demand scalable branching strategies, conflict-resolution automation, and feature-flag management, favoring enterprise-grade Git platforms. Organizations, therefore, view integrated version control as a prerequisite for reliable, rapid software delivery.

Shift Toward Cloud-Native Workflows

Cloud-hosted repositories remove infrastructure burden and expose elastic compute that supports AI services unavailable in self-managed environments. GitLab’s SaaS revenue grew 39% year-over-year in its fiscal Q2 2026, constituting 30% of company turnover. Microsoft is migrating hundreds of thousands of Azure Repos seats to GitHub so customers can tap Copilot’s autonomous code generation. GitHub Enterprise Cloud introduced EU data residency in 2024 and expanded to Australia and the United States in 2025, removing sovereignty hurdles for financial services clients. Atlassian will add EU data residency for Bitbucket Cloud in 2026 to court risk-averse enterprises.[2]Atlassian, “You Can Now Sign Commits with SSH Keys,” atlassian.com Although cloud adoption raises vendor lock-in concerns, hybrid models that mix on-premise repositories for sensitive assets with cloud instances for collaboration are easing migration inertia.

AI-Assisted Code Review and Traceability

Generative AI is transforming repository activity. GitHub Copilot exceeded 15 million users and reached USD 2 billion in annualized revenue by mid-2024. Microsoft launched a Copilot agent in May 2025 that autonomously refactors code and submits pull requests, positioning the repository as an AI collaboration workspace. GitLab’s Duo Agent Platform, in public beta since September 2025, orchestrates multiple foundation models to remain cloud-agnostic. As AI-generated code proliferates, enterprises insist on provenance metadata model version, prompt and training lineage captured directly in the commit history to satisfy auditors. Platforms embedding that traceability gain advantage in regulated environments.

Digital Product Compliance (SBOM, Secure Supply Chain)

Global policy now mandates software transparency. A joint advisory from CISA, NSA, and 18 allied agencies in September 2025 recommends machine-readable SBOMs generated at build time and aligned with vulnerability exchange formats. Europe’s Digital Operational Resilience Act and Cyber Resilience Act require up-to-date SBOMs and rapid vulnerability disclosure, favoring repositories with native export, dependency scanning, and VEX integration. GitLab 18 introduced custom compliance frameworks and immutable tag management, positioning the suite as a turnkey solution. Atlassian embedded SSH-key commit signing in March 2025, aligning Bitbucket Cloud with CISA recommendations. Buyers view these features as essential for government and critical-infrastructure procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Multi-Vendor Toolchains | -1.8% | Global, acute in North America and Europe enterprises with legacy stacks | Medium term (2-4 years) |

| Repository Scalability Limitations | -1.3% | Global, prominent in large enterprises and monorepo adopters | Short term (≤ 2 years) |

| Shortage of Advanced VCS Skill Sets | -0.9% | Global, higher in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Open-Source License and Vulnerability Exposure | -0.7% | Global, heightened in regulated sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Vendor Toolchains

Nearly three-quarters of organizations run seven or more security tools, yet fewer than half scan both code and binaries, illustrating integration gaps that slow delivery.[3]JFrog Ltd., “Software Supply Chain State of the Union 2025,” jfrog.com Atlassian’s attempt to charge separately for Bitbucket self-hosted runners in December 2025 triggered backlash, revealing how layered pricing amplifies friction. Enterprises migrating from Azure DevOps to GitHub must rewire pipelines, boards, and testing suites, extending transformation timelines. API tokens spread across repositories, CI/CD, and registries increase compliance risk, prompting demand for unified identity management. The complexity of harmonizing disparate tools remains a brake on market expansion.

Repository Scalability Limitations

Monorepos and binary-heavy workloads expose performance ceilings. Perforce markets Helix Core for petabyte-scale repositories that support 10,000 transactions per minute, citing ISO 26262 certification as a differentiator. Unity Version Control offers smart locks that travel across branches, reducing merge conflicts on 3D assets functionality Git struggles to emulate. GitLab recorded 35-45% year-over-year growth in CI pipeline runs during 2025, straining artifact storage and network bandwidth. GitHub introduced virtual file sync and sparse checkout to mitigate long clone times, yet large enterprises still deploy regional caching proxies, adding operational cost. Performance bottlenecks thus temper adoption among teams working with multi-terabyte repositories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Gains Momentum Through AI and Compliance

Cloud deployment commanded 62.77% of the version control system market share in 2025 as enterprises prioritized elasticity and zero-maintenance operations. The segment is forecast to grow at a 17.32% CAGR through 2031, supported by the integration of AI copilots that rely on hyperscale compute. GitHub Enterprise Cloud’s data-residency rollout in the EU, Australia and the United States has neutralized many sovereignty objections and catalyzed migrations from Azure Repos and self-managed Git servers. The version control system market size for cloud users will therefore expand fastest where regulators now accept SaaS platforms that hold FedRAMP, ISO 27001 and SOC 2 credentials.

On-premise installations persist among defense, semiconductor and aerospace organizations that mandate air-gapped environments. GitLab revealed that self-managed licenses still generated 70% of revenue in fiscal Q3 2026, although SaaS growth is outpacing on-premise sales. Perforce Helix Core and Unity Version Control remain staples for studios and automotive firms manipulating large binary assets under ISO 26262 workflows. Hybrid strategies—on-premise for sensitive IP and cloud for external collaboration—are closing the confidence gap and extending the version control system market to conservative buyers.

By Type: Distributed VCS Dominates, Centralized Retains Niche Strength

Distributed platforms such as Git held 92.43% of the version control system market share in 2025, a dominance born of flexible branching, offline commits and a rich plugin ecosystem. GitHub crossed the 100 million-developer threshold, while GitLab now counts more than half of the Fortune 100 among active customers, confirming the ubiquity of distributed workflows. The version control system market size attached to distributed tools will continue to rise as AI code generation multiplies commit events.

Centralized systems are expected to post a faster 17.64% CAGR through 2031 from a smaller base because binary-centric industries are revisiting exclusive locking models. Perforce’s acquisition of Snowtrack, rebranded P4 One, makes the workflow friendlier for artists and designers, while Unity Version Control pitches smart locks that travel across branches. Automotive, gaming, and media teams value linear history, deterministic builds, and petabyte repositories. Their specialized needs create pockets of growth that preserve centralized tools’ relevance inside the broader version control system market.

By End-User Industry: Gaming Surges on Real-Time Collaboration

IT and telecom remained the largest spenders, contributing 36.67% of share in 2025 as cloud-native microservices and API management demand sophisticated repositories. Yet gaming and digital content is the fastest rising adopter with an 18.11% CAGR forecast to 2031, pushed by real-time Unreal and Unity pipelines that juggle massive binary assets. Unity Version Control and Perforce Helix Core dominate this workflow thanks to file locking and delta transfer optimization, and the segment draws incremental licenses as live-service games shift to weekly content drops.

BFSI growth is propelled by Europe’s Digital Operational Resilience Act and U.S. SBOM mandates, which push banks toward platforms offering data residency, signed commits and automated compliance. Healthcare, retail and education exhibit steadier uptake, emphasizing secure mobile apps and infrastructure-as-code. Automotive and embedded systems also widen the version control system market because ISO 26262 compliance ties firmware, models and test data to immutable repositories, a use case GitLab demonstrated at Jaguar Land Rover. These patterns underscore how sector-specific regulation and asset types steer purchasing decisions.

By Organization Size: SMEs Accelerate on Freemium SaaS

Large enterprises held 63.76% of share in 2025, leveraging multi-year contracts, single-tenant deployments, and priority support. Microsoft’s bundling of Azure DevOps Basic rights with GitHub Enterprise licenses trimmed procurement friction and deepened account penetration. GitLab, meanwhile, reported 1,344 customers generating more than USD 100,000 in annual recurring revenue, up 25% year on year, evidencing ongoing consolidation around full-stack suites.

Small and medium enterprises represent the fastest-growing cohort, expanding at a 17.49% CAGR, as freemium tiers remove entry barriers and managed CI/CD reduces operational overhead. GitHub’s free repositories and GitLab’s community edition offer production-grade tooling without capital expenditure, letting startups adopt enterprise-class practices from inception. Price sensitivity remains, illustrated by SME backlash when Atlassian briefly placed Bitbucket runners behind a paywall, yet the availability of flexible monthly tiers keeps switching costs low and enlarges the version control system market footprint among smaller teams.

Geography Analysis

North America dominated 39.78% of the market share in 2025, owing to GitHub’s heavy Fortune 100 penetration and federal procurement rules that require FedRAMP Moderate authorization for DevSecOps suites. GitLab secured the same clearance for its Dedicated for Government service in early 2026, enabling public agencies to solicit competitive bids while preserving data sovereignty. Canada and Mexico trail the United States but are adopting SaaS repositories across fintech and near-shore software outsourcing, extending the regional version control system market.

Asia-Pacific is forecast to post an 18.02% CAGR through 2031, the fastest worldwide. India’s services firms, China’s internet conglomerates, and Southeast Asia’s e-commerce leaders are migrating monolithic code bases to distributed Git workflows. Gaming hubs in Japan and South Korea rely on Perforce and Unity to manage terabyte-scale art assets, while Australia’s public sector adopts GitHub Enterprise Cloud with local data storage. Fragmented regulations and lower SME spending temper growth, yet hyperscale cloud rollouts continue to unlock latent demand.

Europe’s share is shaped by the Cyber Resilience Act, effective January 2024, and the Digital Operational Resilience Act, enforceable since January 17 2025. Both laws require SBOM generation and vulnerability disclosure, spurring demand for compliance-ready platforms. Germany, the United Kingdom and France lead adoption in automotive, finance and industrial IoT. South America, the Middle East and Africa still contribute a small portion of the version control system market, yet sovereign cloud mandates in Brazil, Saudi Arabia and South Africa signal future upside as local data centers come online and developer populations expand.

Competitive Landscape

Competition is moderately fragmented, with Microsoft’s GitHub, GitLab, and Atlassian’s Bitbucket capturing the bulk of cloud-hosted Git workloads. Microsoft leverages Azure integration to migrate Azure Repos users into GitHub, offering Copilot features unavailable elsewhere and bundling Azure DevOps entitlements to cement account control. GitLab pursues a cloud-agnostic positioning with single-tenant Dedicated deployments and the Duo Agent Platform, which orchestrates multiple AI models, achieving 29% year-over-year revenue growth in fiscal Q2 2026. Atlassian differentiates via a hybrid license that allows Bitbucket Data Center and cloud instances to coexist, paired with upcoming EU data residency, reducing migration friction for regulated customers.

Perforce and Unity Technologies dominate centralized and binary-optimized niches. Perforce Helix Core serves automotive and game studios needing petabyte repositories, ISO 26262 certification and exclusive file locking, while Unity Version Control extends similar features to creators embedded in the Unity engine workflow. Smaller disruptors such as GitKraken integrate cross-repository visualization and AI commit suggestions after acquiring CodeSee, catering to developers frustrated by multi-tool fragmentation. JFrog and Sonatype embed security scanning into pipelines but still rely on external Git providers, underscoring how full-suite incumbents are raising barriers by incorporating vulnerability management, SBOM export and artifact registries.

Strategic moves center on AI monetization and compliance. GitHub Copilot’s growth trajectory prompted GitLab to preview a hybrid seat-plus-usage pricing model once Duo Agent hits general availability. Atlassian embedded SSH-key commit signing, while GitLab 18 launched custom compliance frameworks tailored to SOC 2 and ISO 27001. Vendors vying for government contracts pursue FedRAMP and ISO certifications. As features converge, differentiation shifts toward ecosystem lock-in, migration tooling and the breadth of first-party integrations that compress total cost of ownership for enterprise buyers.

Version Control System Industry Leaders

Github, Inc.

Gitlab, Inc.

Bitbucket.org (Atlassian Corporation Plc)

Beanstalk (Wildbit, LLC)

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Atlassian reversed its December 2025 decision to charge for Bitbucket self-hosted runners, pledging to keep a free tier and introduce a premium option with supported orchestration.

- December 2025: GitLab posted fiscal Q3 2026 revenue of USD 244.4 million, up 25% year over year, and announced Duo Agent Platform nearing general availability.

- November 2025: Microsoft made GitHub Advanced Security features for Azure DevOps generally available, adding work-item linking and one-click dependency scanning.

- November 2025: Atlassian detailed Bitbucket Cloud and Data Center compliance enhancements, including signed commits and integration with Jira Service Management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the version control system market as all licensed or subscription-based software platforms that record, manage, and synchronize source-code or other digital asset changes for professional development teams, whether deployed on-premise or delivered through the cloud. These platforms typically bundle workflow tools such as branching, merge conflict resolution, and policy enforcement.

Scope exclusion: file sync utilities and revision features embedded solely inside content management or creative design suites are outside our count.

Segmentation Overview

- By Deployment Mode

- On-Premise

- Cloud

- By Type

- Distributed VCS

- Centralized VCS

- By End-user Industry

- IT and Telecom

- BFSI

- Retail and E-commerce

- Healthcare and Life Sciences

- Media and Entertainment

- Education

- Gaming and Digital Content

- Automotive and Embedded Systems

- Aerospace and Defense

- Other End-user Industries

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with DevOps architects, procurement heads, and open source foundation members across North America, Europe, and Asia Pacific. Their perspectives clarified average seat pricing, cloud versus on-premise splits, and the pace at which AI-assisted coding add-ons lift revenue, allowing us to fine-tune regional assumptions.

Desk Research

Analysts began with authoritative datasets from bodies such as the US Bureau of Labor Statistics (developer workforce growth), International Telecommunication Union (broadband penetration), and Eurostat Digital Economy reports. Insight on usage intensity came from open repositories like GitHub Octoverse and the Stack Overflow Developer Survey, while D&B Hoovers and Dow Jones Factiva supplied vendor financial cues and transaction news. Additional triangulation drew on patent filings, trade association briefs, and corporate 10-Ks. The sources cited above illustrate our approach; many others were reviewed to confirm figures and context.

Market-Sizing & Forecasting

A top-down build estimates spend by multiplying the active professional developer pool by tool penetration rates and weighted average price per seat. Supplier roll-ups and select channel checks provide the bottom-up cross-check that aligns totals. Variables such as cloud infrastructure spend, DevOps toolchain adoption share, GDP per capita, active repository count, and average license renewal cycles feed a multivariate regression that projects figures through 2030. Scenario analysis handles uncertainty around AI-driven premium tiers and macroeconomic swings.

Data Validation & Update Cycle

Outputs flow through automated anomaly scans, senior analyst peer review, and lead analyst sign-off. Models refresh every twelve months, with interim updates triggered by material events like major vendor price resets or large-scale security mandates.

Why Mordor's Version Control System Baseline Commands Credibility

Published estimates often differ; boundary choices, currency timing, and price tier treatment vary widely. Our disciplined scope and annual refresh keep the baseline aligned with real developer economics.

Key gap drivers are whether personal use tiers are monetized, how bundled DevSecOps add-ons are counted, the aggressiveness of AI-assisted upsell assumptions, and the share of on-premise maintenance that is recognized as market revenue.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.48 B (2025) | Mordor Intelligence | - |

| USD 1.13 B (2025) | Global Consultancy A | Omits enterprise support tiers and hybrid deployments |

| USD 0.72 B (2023) | Regional Consultancy B | Earlier base year and partial coverage of distributed platforms only |

| USD 0.61 B (2025) | Industry Journal C | Counts SME on-premise licenses, excludes SaaS revenue streams |

This comparison shows that Mordor's clearly bounded scope, transparent variables, and timely refresh deliver a balanced, decision-ready baseline for stakeholders.

Key Questions Answered in the Report

What is the expected value of the version control system market by 2031?

The market is forecast to reach USD 3.74 billion by 2031, expanding at a 16.81% CAGR from 2026.

Which deployment mode is growing fastest in this space?

Cloud repositories are projected to grow at a 17.32% CAGR through 2031 as enterprises seek elastic scalability and AI features.

Why are gaming companies adopting new version control tools rapidly?

Live-service game models require real-time collaboration on large binary assets, driving an 18.11% CAGR for the segment to 2031.

How do regulatory mandates influence buying decisions in Europe?

The Cyber Resilience Act and Digital Operational Resilience Act oblige organizations to produce SBOMs and signed commits, favoring platforms with native compliance automation.

What role does AI play in next-generation version control systems?

Generative AI agents automate code review, refactoring and test creation, increasing repository activity and encouraging adoption of integrated DevSecOps suites.

Are small and medium enterprises significant customers for these platforms?

Yes, SMEs are expanding at a 17.49% CAGR because freemium SaaS tiers lower entry barriers and bundle managed CI/CD services.

Page last updated on: