Nordic SaaS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

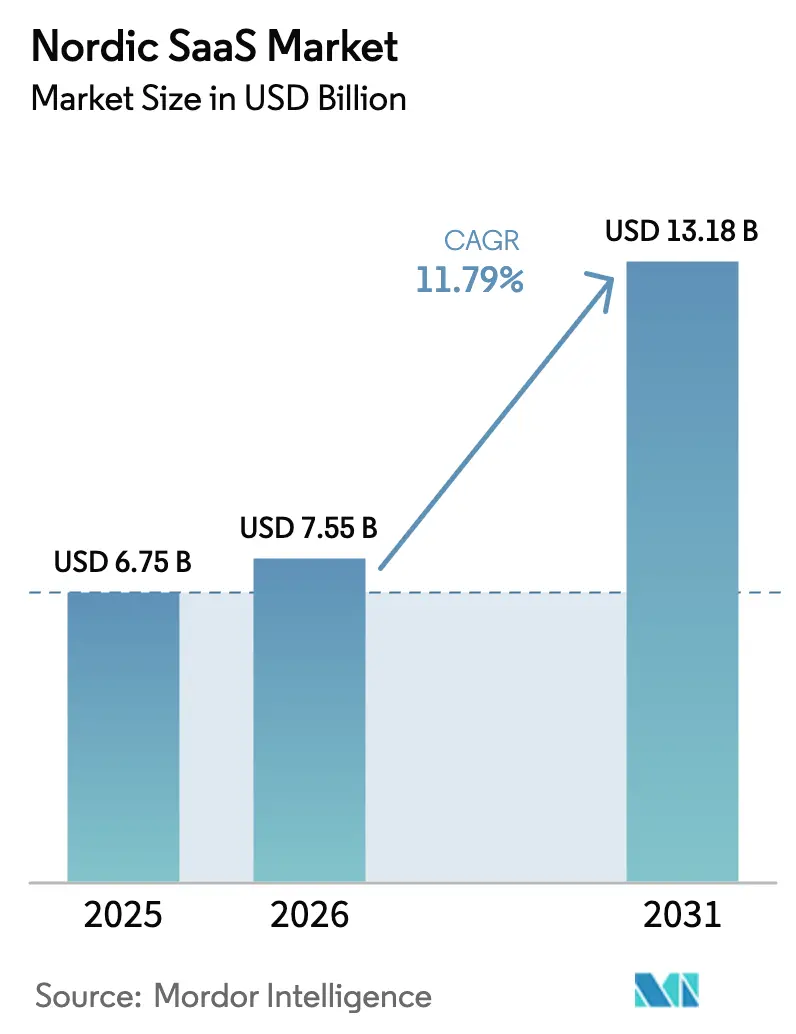

| Base Year Market Size (2025) | USD 6.75 Billion |

| Market Size (2026) | USD 7.55 Billion |

| Market Size (2031) | USD 13.18 Billion |

| Growth Rate (2026 - 2031) | 11.79% CAGR |

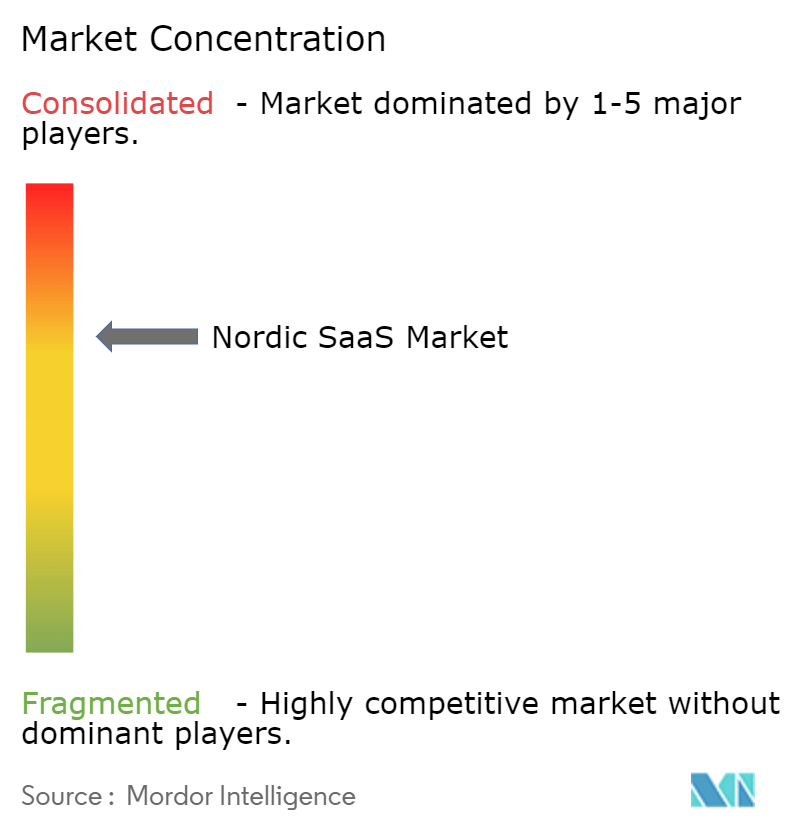

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic SaaS Market Analysis by Mordor Intelligence

The Nordic SaaS market size is expected to grow from USD 6.75 billion in 2025 to USD 7.55 billion in 2026 and is forecast to reach USD 13.18 billion by 2031 at 11.79% CAGR over 2026-2031. The region’s public-sector cloud-first mandates, high-speed 5G and fiber backbones, and a widening base of renewable-energy data centers create favorable conditions for digital sovereignty. These structural advantages combine with usage-based pricing models that lower entry barriers for small firms, while the rapid roll-out of EU AI Act compliance tools lifts demand for trusted, in-region software. Competitive momentum is intensifying: Microsoft has committed USD 3.2 billion to Swedish cloud and AI capacity, Visma closed 32 acquisitions in 2024, and a wave of vertical micro-SaaS start-ups is reshaping niche workflows.

Key Report Takeaways

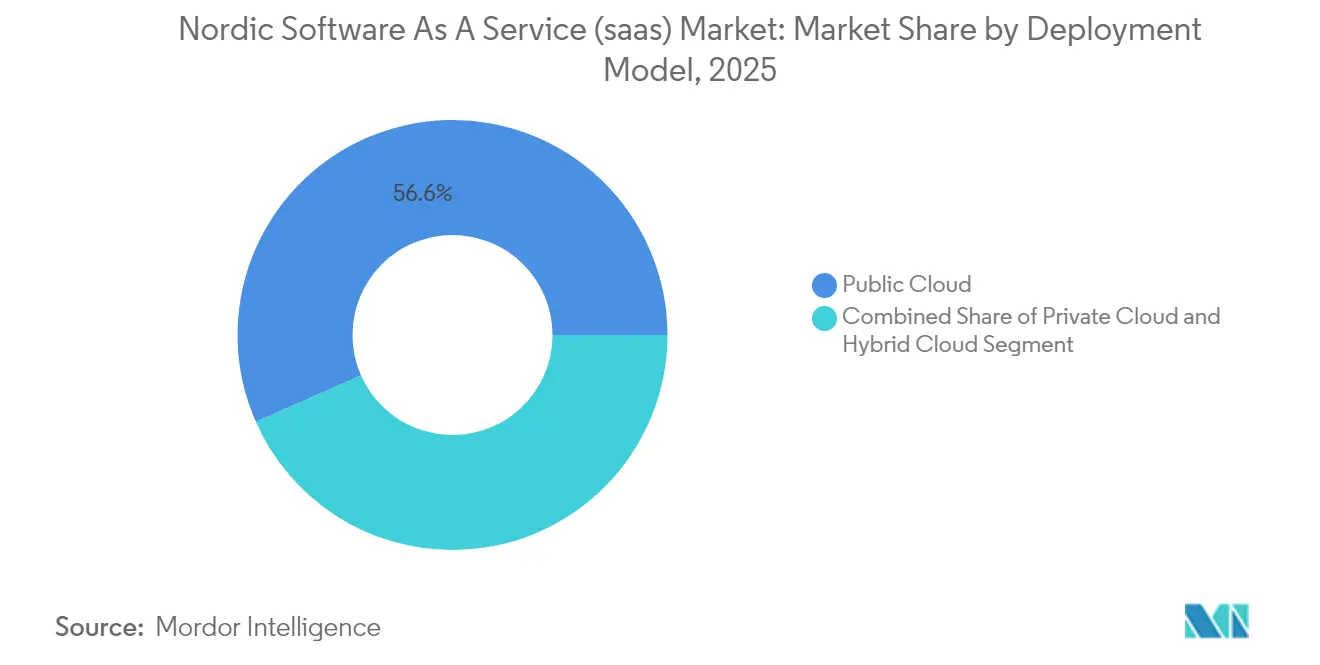

- By deployment model, Public Cloud captured 56.62% Nordic SaaS market share in 2025; Hybrid Cloud is the fastest-growing model, rising at 15.15% CAGR to 2031.

- By enterprise size, Small and Medium Enterprises held 61.55% of Nordic SaaS market share in 2025; the segment is accelerating at a 17.35% CAGR through 2031.

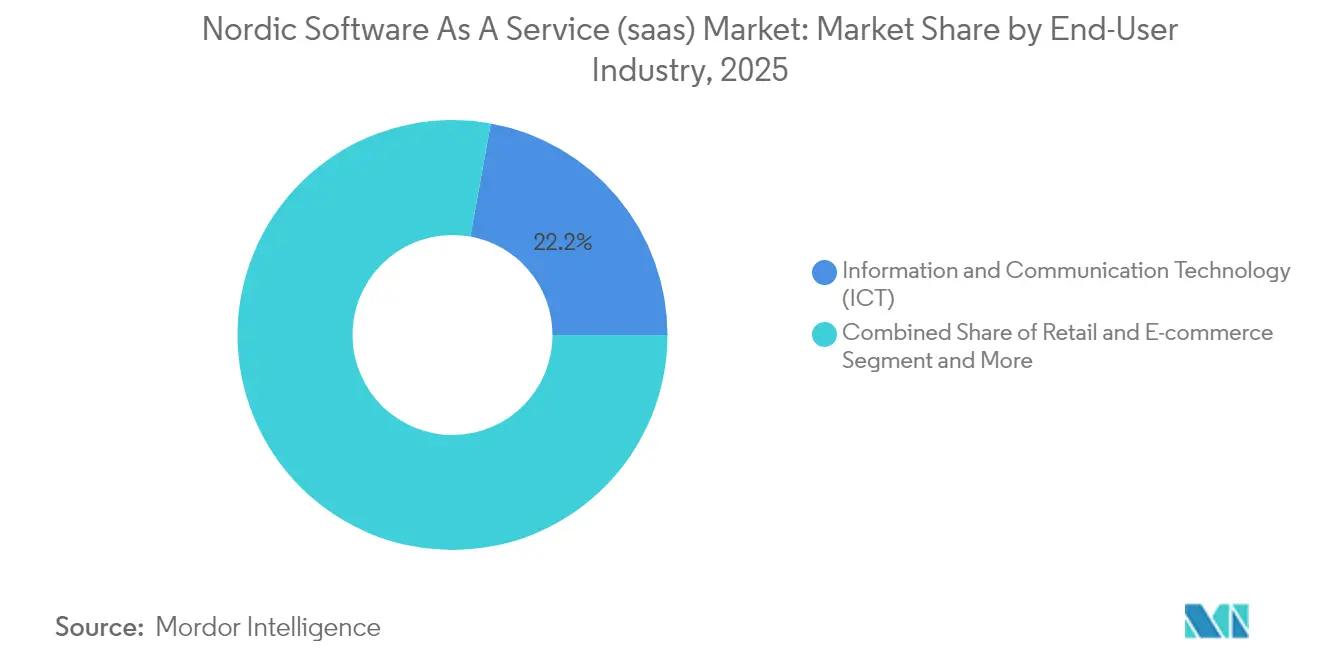

- By end-user industry, the Information and Communication Technology sector led with 22.15% revenue share in 2025, while Healthcare and Life Sciences is projected to expand at a 19.18% CAGR to 2031.

- By functional application, Collaboration and Productivity tools accounted for 25.22% share of the Nordic SaaS market size in 2025; Business Intelligence and Analytics is advancing at a 22.94% CAGR through 2031.

- By geography, Sweden commanded 34.12% share of the Nordic SaaS market size in 2025, whereas Finland is climbing at a 15.28% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nordic SaaS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High digital maturity and cloud-first public sector | +2.8% | Nordic-wide, strongest in Sweden and Denmark | Medium term (2-4 years) |

| Robust 5G/FTTH backbone enabling low-latency SaaS | +2.1% | Nordic-wide, led by Denmark and Sweden | Short term (≤ 2 years) |

| Surge in Nordic green-energy data centers | +1.9% | Sweden and Finland | Long term (≥ 4 years) |

| EU AI Act compliance accelerating trusted SaaS tools | +1.7% | EU-wide with Nordic early adoption | Medium term (2-4 years) |

| Proliferation of vertical micro-SaaS start-ups | +1.4% | Sweden and Norway | Short term (≤ 2 years) |

| Shift to usage-based pricing models | +1.2% | Nordic-wide, SME-focused | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Digital Maturity and Cloud-First Public Sector

Nordic governments frame cloud adoption as a prerequisite for efficient service delivery. Sweden’s 2025-2030 digitalization blueprint earmarks EUR 2.8 billion for online health records, AI-enabled public services, and open data platforms. Denmark’s Ministry of Digitalization is migrating half its workforce to open-source office suites, signaling a policy tilt toward vendor-agnostic sovereignty. Municipalities extend this momentum by deploying Visma’s collaborative budgeting modules that streamline financial reporting and heighten transparency. Public procurement hubs such as Mercell have already cut tender lead times by 80%, underscoring efficiency gains that reinforce SaaS demand. Collectively, these moves deepen the Nordic SaaS market’s public-sector revenue base while setting best-practice templates for regulated industries.

Robust 5G/FTTH Backbone Enabling Low-Latency SaaS

Denmark leads Europe with 83.4% 5G availability, and Sweden follows closely, enabling ultra-low-latency workloads and edge computing pilots. Factbird leverages this network headroom to deliver cloud-based manufacturing analytics that boost uptime for 250 Nordic plants, marking 300% growth since 2021. Ericsson’s rollout of cloud-native 5G cores across Nordic operators further eases the integration of carrier-grade SaaS, underlined by 120 commercial 5G Core contracts worldwide. These infrastructure gains encourage autonomous logistics, immersive training, and remote patient monitoring services that depend on sub-10 ms round trips, reinforcing the Nordic SaaS market’s differentiation on performance.

Surge in Nordic Green-Energy Data Centers

Microsoft’s USD 3.2 billion Swedish campus taps 100% renewable power and reroutes waste heat into district heating grids through Fortum partnerships[1]Microsoft Corp., “Microsoft invests in cloud and AI infrastructure in Sweden,” microsoft.com. EcoDataCenter 2 in Östersund invests SEK 18 billion to operate at 15 g CO₂eq/kWh, roughly one-tenth the European average. Apple’s Danish facility and the LUMI supercomputer in Finland likewise run entirely on clean energy. These assets shorten latency for regional users of hyperscale platforms and let local vendors market carbon-neutral services, which is vital for enterprises with ESG mandates. The pattern fosters a virtuous cycle: each fresh build attracts more vendors, which in turn justifies further grid upgrades and renewable capacity.

EU AI Act Compliance Accelerating Trusted SaaS Tools

The EU AI Act places transparency, human oversight, and risk management at the heart of software design. ComplyCloud’s automated documentation engine helps Nordic firms score AI risks and track mitigation steps. Visma has already embedded 13 AI-enhanced modules in public-administration suites, including Ecare for elderly services, while earning ISO 27001 extensions that reassure data controllers. WithSecure (formerly F-Secure) adds AI-based threat exposure tools that align with the Act’s audit requirements and national cybersecurity directives. Ethical-by-design reputations allow Nordic vendors to compete against larger platforms facing heavier scrutiny, thereby lifting the Nordic SaaS market’s ARR potential in regulated segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-jurisdictional data-privacy rules | –1.8% | Nordic-wide with EU spillover | Medium term (2-4 years) |

| High technical-talent costs vs. off-shore hubs | –2.3% | Sweden and Norway | Long term (≥ 4 years) |

| Vendor lock-in risk with hyperscale IaaS | –1.4% | Nordic-wide, enterprise-focused | Medium term (2-4 years) |

| Rising cyber-sovereignty concerns | –1.1% | Government and critical sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Jurisdictional Data-Privacy Rules

GDPR forms a baseline, yet each Nordic state layers sector-specific safeguards that oblige SaaS vendors to maintain discrete instances and audit trails. Denmark’s retreat from Microsoft 365 reflects heightened sovereignty demands that compel alternate hosting arrangements. Tele2’s Sweden-only collaboration suite based on the Matrix protocol mirrors the trend but sacrifices scale economies. Healthcare and financial regulations add another compliance tier, driving up legal and DevOps overhead for smaller providers. Orange Business now markets sovereign clouds with in-country key management to mitigate the burden, but such solutions inflate unit economics, trimming the Nordic SaaS market growth premium.

High Technical-Talent Costs vs. Off-Shore Hubs

Demand for AI engineers, full-stack developers, and cloud architects outpaces supply across Sweden and Norway. The oil and gas revival in Norway and Stockholm’s expanding fintech cluster push median developer salaries to multiples of Eastern-European rates, squeezing gross margins. Aging demographics cap domestic graduate output, while immigration bottlenecks limit inflow. Employers respond by forming near-shore centers in Poland or Portugal, yet distributed teams can erode the iterative, design-thinking culture prevalent in Nordic product management. Persistent wage inflation therefore narrows runway for bootstrapped start-ups and delays feature roadmaps, dampening the Nordic SaaS industry’s overall velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Solutions Bridge Sovereignty Gaps

Public Cloud kept a 56.62% share of the Nordic SaaS market in 2025. Hybrid architectures, however, are moving fastest with a 15.15% CAGR as enterprises mix hyperscale elasticity with sovereign nodes for regulated workloads. Several ministries follow Denmark’s lead in piloting LibreOffice and adopting open standards, revealing a preference for stack control over vendor convenience. The shift positions integrators like Tietoevry as orchestrators of multi-tenant governance, compliance automation, and workload portability. Nordic SaaS market size for hybrid deployments is set to reach USD 5.48 billion by 2031, underpinning demand for policy-based routers, edge security, and cross-cloud billing analytics.

Organizations now pair Amazon Web Services or Microsoft Azure for low-risk workloads with local cloud partners that physically segregate sensitive datasets. This architecture reduces latency spikes and avoids unilateral price revisions typical of single-provider contracts. Swedish municipalities increasingly request sovereign-hosting clauses, compelling ISVs to embed region selection tools at onboarding. Advisory roadmaps therefore prioritize zero-trust design, proactive data residency dashboards, and encryption-in-use modules that reconcile compliance with agility.

By Enterprise Size: SME Dominance Drives Innovation

SMEs accounted for 61.55% Nordic SaaS market share in 2025, and the cohort is expanding at 17.35% CAGR through 2031. Usage-based pricing lowers capex, while pre-configured integrations shorten time-to-value for firms with lean IT staff. The Nordic SaaS market size arising from SME demand is poised to exceed USD 8.1 billion by 2031, signaling outsized influence on product roadmaps.

Fortnox illustrates the economics: 536,000 accounts, SEK 268 ARPC, and a 41% operating margin prove volume-based models can scale profitably. Visma amplifies this dynamic by absorbing local developers and layering cross-selling APIs that simplify payroll, accounting, and e-invoicing workflows. Micro-vertical innovators, such as BRP Systems for fitness clubs, win niches through domain features that larger suites overlook, reinforcing the Nordic SaaS market’s fragmentation and opportunity pool.

By End-User Industry: Healthcare Surge Reshapes Priorities

ICT services remained the largest buyer group with 22.15% of Nordic SaaS market revenue in 2025, but Healthcare and Life Sciences post the steepest ascent at 19.18% CAGR. Telemedicine, remote diagnostics, and AI-assisted triage tools align with national mandates that shorten care queues and control costs. Consequently, Nordic SaaS market size attributable to healthcare is projected to surpass USD 2.86 billion by 2031.

Nordhealth’s 13,000-clinic footprint, Curoflow’s appointment automation, and MedHelp’s absenteeism analytics highlight demand for integrated EHR connectors and GDPR-aligned data lakes. Banking, Financial Services and Insurance modernizes at measured pace, replatforming loan origination and anti-fraud modules. Manufacturing and retail adopt SaaS for supply-chain visibility, often bundling IoT telemetry and predictive inventory models. Public sector projects continue to escalate via statewide tender frameworks that favor locally hosted platforms.

By Functional Application: Analytics Revolution Accelerates

Collaboration and Productivity tools controlled 25.22% of Nordic SaaS market revenue in 2025 as hybrid work became entrenched. Yet Business Intelligence and Analytics leads growth, forecast at 22.94% CAGR through 2031. The segment’s momentum stems from accessible machine-learning pipelines and self-service dashboards that demystify advanced analytics for non-technical users.

Accobat’s AI-infused Power BI extensions typify the new wave, automating outlier detection and scenario planning for mid-market finance teams. SuperOffice repositions CRM as a sustainability cockpit, pledging carbon negative status by 2025 to mirror buyers’ ESG KPIs. WithSecure’s Elements platform embeds identity-based defense layers, underscoring the convergence of analytics and security. Retail-specific players like Voyado inject customer-journey insights, funded by strategic investors seeking data-centric margin expansion.

Geography Analysis

Sweden’s dominance rests on a robust innovation pipeline, extensive capital access, and near-ubiquitous gigabit coverage. Microsoft’s USD 3.2 billion datacenter expansion cements low-latency regional zones that anchor hyperscale workloads. State investments of EUR 2.8 billion toward e-government maintain steady demand across administrative units. Visma and Fortnox magnify network effects by integrating invoicing, payroll, and analytics into cohesive suites.

Finland’s ascent mirrors strategic alignment between public investment and private enterprise. Microsoft’s multi-site campus leverages hydro and wind resources, ensuring carbon-neutral compute for domestic ISVs. Heeros and Finadeck automate cash-flow forecasting for SMEs, while the LUMI supercomputer opens AI sandbox capacity, encouraging algorithm-heavy applications in healthcare diagnostics and forest-yield modeling.

Norway emphasizes industrial data clouds that serve offshore energy platforms and grid-balancing operators. Cognite’s asset data fusion and Volue’s market-clearing software scale across Europe, aided by generous R&D tax incentives. Denmark advocates open-source stack independence, steering ministries toward LibreOffice while nurturing identity-management start-ups. Iceland reinforces the regional talent cycle by exporting fresh analytics concepts backed by geothermal data centers that assure low-carbon footprints.

Competitive Landscape

Consolidation accelerates but fragmentation persists. Visma’s 32 acquisitions in 2024, adding 190 companies across Europe and Latin America, reveal an orchestration strategy that pairs broad functionality with local compliance anchors[3]Visma Group, “Visma annual report 2024,” visma.com. EQT and First Kraft’s USD 5.5 billion proposal for Fortnox underscores investor appetite for sticky financial administration platforms. SuperOffice refreshes its CRM modules around net-zero dashboards, while WithSecure pivots toward exposure management as identity-based threats rise.

Midsized challengers exploit white spaces. Nordic Capital’s purchase of BRP Systems positions the investor to scale a fitness-specific ERP globally. Factbird raises USD 16 million to globalize its real-time factory-floor intelligence. Vertical depth, sovereign hosting, and AI explainability stand out as the strategic levers for differentiation.

Hyperscalers raise the bar on platform completeness. Microsoft’s renewable-powered zones and AWS Local Zones provide latency parity with local offerings. European AI regulation nonetheless provides shelter for regional providers skilled in human-in-the-loop compliance workflows. Competitive chess now centers on ecosystem breadth, sustainability credentials, and transparent AI governance.

Nordic SaaS Industry Leaders

Visma Solutions

Microsoft Corporation

Salesforce, Inc.

SAP SE

Fortnox AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Klarna launched an AI-powered direct communication line to CEO Sebastian Siemiatkowski, signaling deeper conversational commerce integration.

- March 2025: EQT and First Kraft offered USD 5.5 billion for Fortnox, underscoring premium valuations in Scandinavian SaaS.

- March 2025: ServiceNow acquired Advania’s Quality 360 to boost AI-driven manufacturing performance.

- February 2025: Klarna enabled automatic onboarding for WooCommerce merchants under a new distribution pact.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Nordic Software-as-a-Service market as all subscription-based, multi-tenant business software delivered over public, private, or hybrid cloud networks to paying users in Denmark, Finland, Iceland, Norway, and Sweden. The figures cover net annual recurring revenue generated inside the region, regardless of vendor headquarters, and are expressed in constant 2024 US dollars.

Scope exclusion: One-time perpetual licenses, infrastructure-as-a-service, platform-as-a-service, and managed hosting revenues fall outside this estimate.

Segmentation Overview

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- Information and Communication Technology (ICT)

- Retail and E-commerce

- Media and Entertainment

- Government and Public Sector

- Education

- Manufacturing

- Healthcare and Life Sciences

- Others

- By Functional Application

- Customer Relationship Management (CRM)

- Enterprise Resource Planning (ERP)

- Human Capital Management (HCM) and Payroll

- Collaboration and Productivity

- Business Intelligence and Analytics

- Cyber-Security SaaS

- Vertical-specific / Micro-SaaS

- By Country

- Norway

- Sweden

- Denmark

- Finland

- Iceland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then held structured interviews and short surveys with Nordic CIOs, SaaS controllers, telecom wholesalers, and data-center operators. The discussions helped us validate average seat prices, churn bands, and public-sector procurement timelines, filling gaps that desk research alone cannot close.

Desk Research

We started with government open data such as Statistics Norway enterprise cloud spend, Eurostat cloud-use surveys, and Swedish Post and Telecom Authority connectivity reports, which anchor adoption rates. Trade bodies, including IT-Branchen and FINTECH Finland, provided sector spending benchmarks, while company filings, IPO prospectuses, and investor presentations supplied vendor revenue splits. We strengthened context through paid databases like D&B Hoovers for private-company financials and Dow Jones Factiva for deal news. Patent searches on Questel flagged emerging vertical micro-SaaS niches in manufacturing execution. These secondary inputs build the factual backbone, yet the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

We reconstruct regional spend through a top-down model that begins with enterprise software budgets reported by national statistics offices, adjusts for cloud penetration, and applies SaaS share by vertical. Results are cross-checked through bottom-up samples of key suppliers' Nordic billings and channel checks. Variables such as SME formation rates, fiber-to-the-home coverage, electricity prices for green data centers, payroll digitization mandates, and average SaaS seat costs feed the model and signal inflection points. Forecasts to 2030 rely on a multivariate regression blended with ARIMA to capture both structural growth and short-term cyclicality, with scenario analysis used where regulatory change could alter data-residency rules. Missing supplier data are bridged by median EV-to-sales multiples and peer growth curves before final triangulation.

Data Validation & Update Cycle

Outputs pass a multi-layer review. Our team contrasts model totals with import statistics on cloud services, screens anomalies, and reruns sensitive variables. Reports refresh annually, with interim updates triggered by material events such as a VAT rule change or a hyperscaler region launch, and an analyst signs off every release.

Why Mordor's Nordic Software as a Service Baseline Stands Firm

Published estimates often diverge because firms slice the market differently, time-stamp exchange rates at varied points, or refresh models irregularly.

Key gap drivers include inclusion of ancillary cloud services, country coverage that omits Iceland, reliance on vendor revenue roll-ups without user-side checks, and single-point currency conversions, which are then left static for years. Mordor Intelligence mitigates these by pairing demand-side spending series with supplier samples, updating FX quarterly, and revisiting assumptions after every major policy shift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.75 B (2025) | Mordor Intelligence | - |

| USD 8.30 B (2025) | Regional Consultancy A | Counts managed cloud services and Icelandic hosting revenue |

| USD 2.07 B (2024, Sweden only) | Trade Journal B | Geography limited to Sweden; extrapolates from public cloud share |

| USD 0.73 T (2025, Nordic cloud stack) | Global Consultancy C | Bundles IaaS, PaaS, and SaaS; employs spend surveys only |

These comparisons show that when scope, data cadence, and triangulation discipline vary, totals swing widely. By anchoring definitions tightly, refreshing inputs yearly, and balancing top-down demand with bottom-up supplier reality, Mordor Intelligence delivers a dependable baseline that decision-makers can replicate and audit.

Key Questions Answered in the Report

What is the current Nordic SaaS market size and its growth outlook?

The market is valued at USD 7.55 billion in 2026 and is expected to hit USD 13.18 billion by 2031, reflecting an 11.79% CAGR.

Which segment is expanding fastest within the Nordic SaaS market?

Business Intelligence and Analytics software leads segment growth at a 22.94% CAGR through 2031, outpacing collaboration and ERP tools.

Why are SMEs so important to the Nordic SaaS market?

SMEs account for 61.55% of revenue and are growing at 17.35% CAGR because usage-based pricing and pre-built integrations fit limited IT budgets.

How are data-sovereignty rules shaping deployment choices?

They are driving Hybrid Cloud adoption at 15.15% CAGR as firms distribute sensitive data on sovereign nodes while keeping scalable workloads on hyperscalers.

Which Nordic country is growing fastest in SaaS adoption?

Finland leads with a projected 15.28% CAGR, propelled by renewable-energy data centers and proactive digitalization policies.

Page last updated on: