Surface Water Sports Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.26 Billion |

| Market Size (2031) | USD 17.15 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

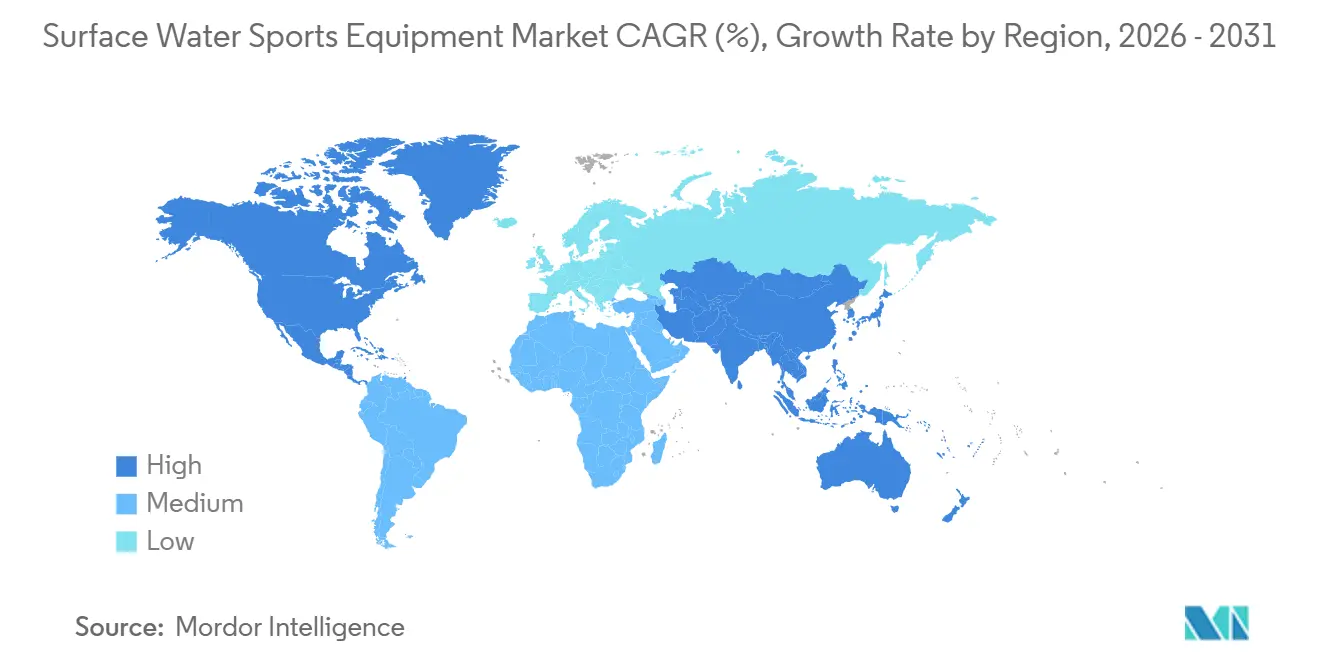

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Surface Water Sports Equipment Market Analysis by Mordor Intelligence

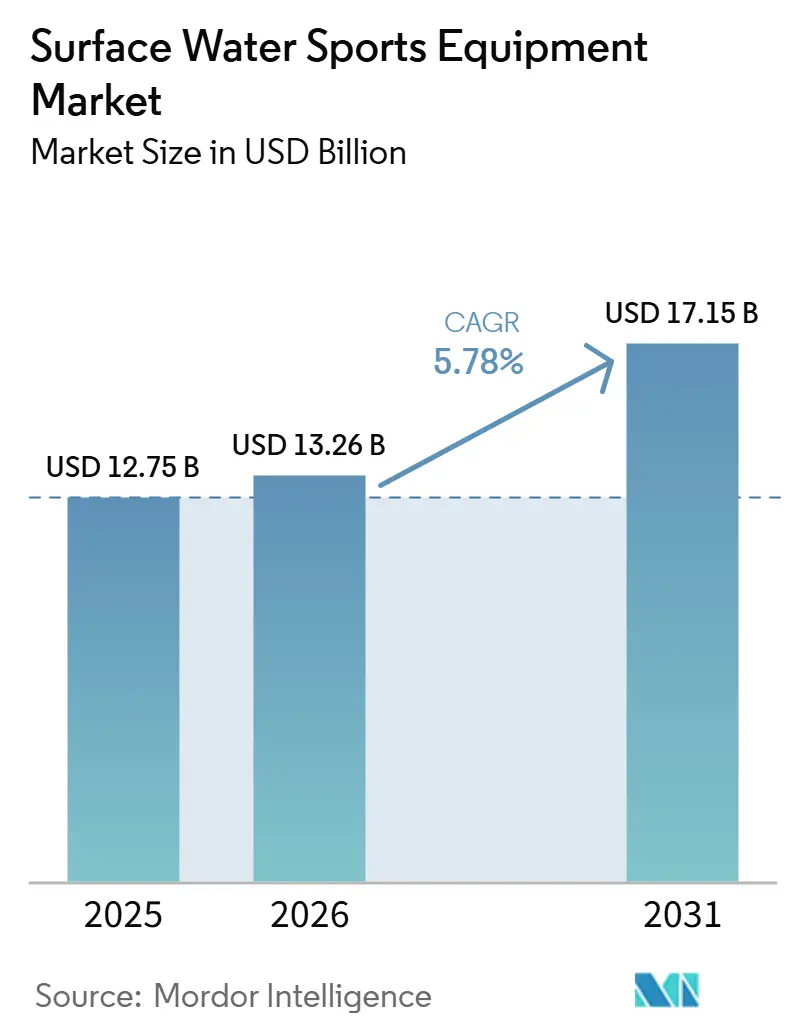

The surface water sports equipment market size was valued at USD 12.75 billion in 2025 and estimated to grow from USD 13.26 billion in 2026 to reach USD 17.15 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). Pandemic-era shifts toward outdoor recreation, record coastal tourism investments, and accelerating technology upgrades are reinforcing demand across both developed and emerging regions. Governments are adding surf parks and waterfront amenities that expand participation windows and temper weather-related sales swings. Manufacturers are embedding bio-based composites, sensors, and app connectivity into boards and wetsuits, encouraging consumers to replace older gear sooner. Sustainability mandates in the European Union and California are steering brands toward recycled or plant-based materials that command price premiums and improve margin profiles. Direct-to-consumer strategies are gaining traction as digital natives seek seamless shopping experiences and price transparency.

Key Report Takeaways

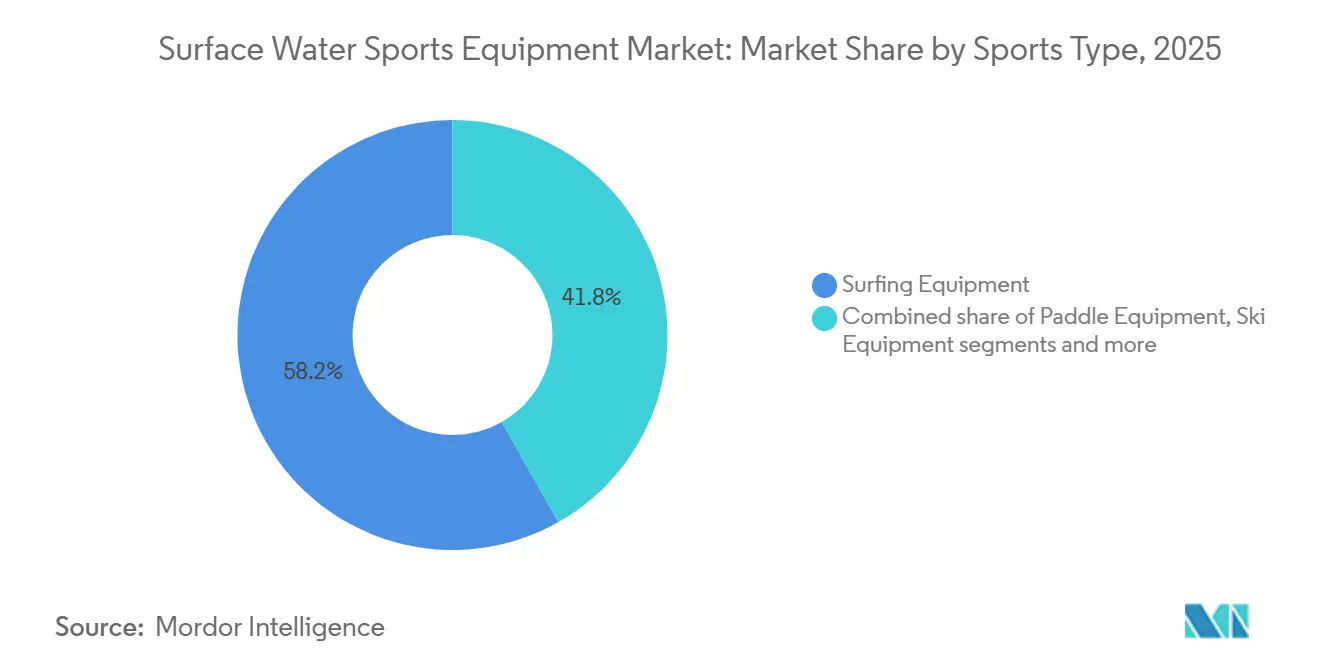

- By sports type, surfing equipment led with 58.21% of the surface water sports equipment market share in 2025, while paddle equipment is advancing at a 6.58% CAGR to 2031.

- By price tier, the mass segment accounted for 65.21% of the surface water sports equipment market size in 2025; the premium tier is projected to grow at the fastest growth at 7.34% CAGR through 2031.

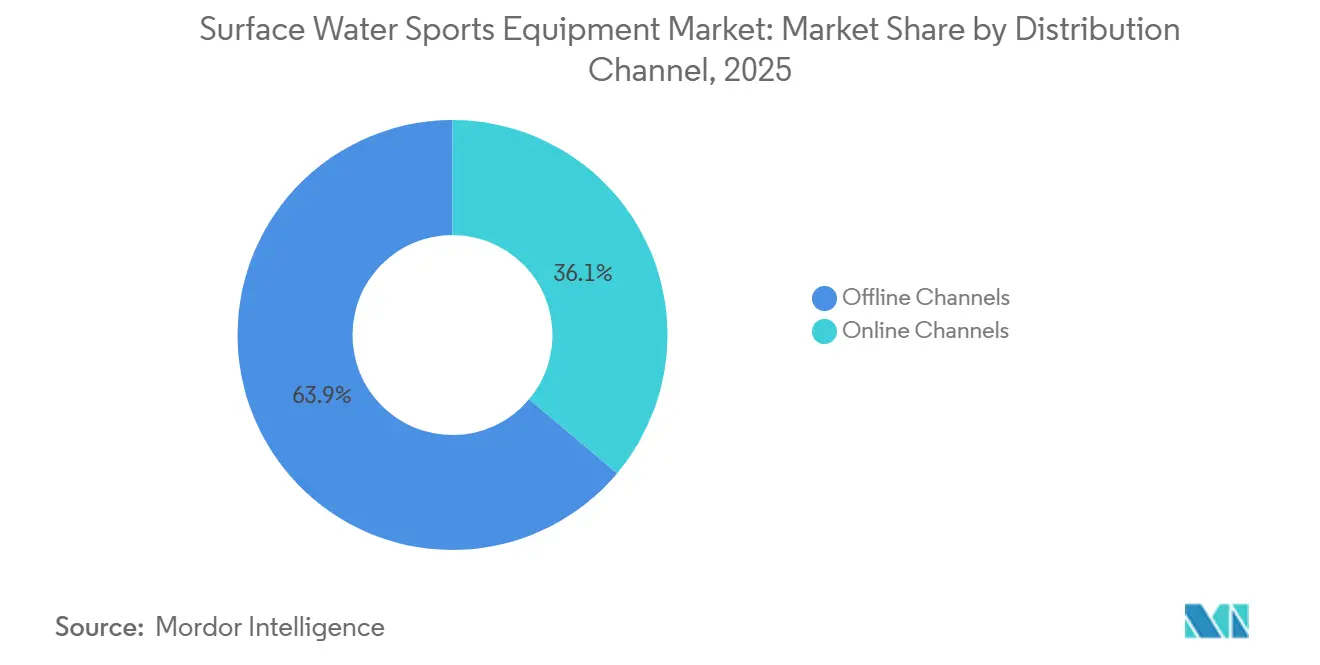

- By distribution channel, offline retail dominated with 70.28% revenue in 2025, whereas online platforms are set to expand at a 6.89% CAGR over 2026-2031.

- By end user, adults held an 86.59% share in 2025, but the kids segment is forecast to climb at a 7.45% CAGR to 2031.

- By geography, North America captured 35.68% of 2025 demand, yet Asia-Pacific is on track for the quickest regional rise with a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Surface Water Sports Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Interest In Outdoor Recreation | +1.2% | Global, with concentration in North America, Europe, Australia | Medium term (2-4 years) |

| Rising Coastal Tourism And Investments In Surf Parks | +0.9% | Coastal regions globally; early-mover hubs in Australia, North America, Western Europe | Medium term (2-4 years) |

| Expanding Technological Innovation In Water Sports Equipment | +0.8% | Global, led by North America and Europe R&D centers | Short term (≤ 2 years) |

| Increased Water Sports Events And Tournaments | +0.5% | Global, with Olympic and ICF-sanctioned events driving visibility | Medium term (2-4 years) |

| Growth Of Rental And Sharing Economy Models | +0.6% | North America and Europe core; emerging in urban coastal Asia Pacific | Short term (≤ 2 years) |

| Demand For Sustainability And Eco‑Friendly Materials | +0.7% | Global, regulatory push strongest in EU and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Interest In Outdoor Recreation

In 2024, outdoor recreation has expanded into a USD 1.3 trillion sector, contributing 2.4% to the U.S. GDP[1]Source: Bureau of Economic Analysis, “Outdoor Recreation Satellite Account, 2024,” bea.gov. This highlights a shift in discretionary spending, with water sports equipment seeing significant growth. The Outdoor Foundation reports that 18.6 million Americans kayaked in 2022, while paddle sports engaged 23 million participants, reaching beyond niche surf communities. Remote work flexibility post-pandemic has increased participation beyond weekends. Municipalities are improving access with investments in boat ramps, storage facilities, and watercraft zones. Millennials and Gen Z, attracted to Instagram-worthy and wellness-focused activities, are driving demand for visually striking equipment like inflatable SUPs and foil boards. Rental platforms are capitalizing on trial-before-purchase models, with the Boatsetter and GetMyBoat merger creating a USD 500 million booking platform across 50 countries, turning hesitant users into repeat buyers.

Rising Coastal Tourism And Investments In Surf Parks

Coastal tourism is evolving from passive beach visits to active water sports, driving investments in infrastructure beyond natural surf breaks. Examples include Perth's AUD 120 million (USD 78 million) surf park, Jacksonville's USD 110 million wave-generation complex, and Portugal's EUR 25 million (USD 27 million) Praia da Vagueira facility[2]Source: Perth Surf Park, “Perth Surf Park Development,” perthsurfpark.com. These projects, co-funded by municipalities and private developers, aim to generate year-round revenue. By ensuring consistent wave quality regardless of ocean conditions, these venues extend operational calendars for rentals and instruction services. In landlocked areas, such as California's inland projects targeting populations over 100 miles from the coast, surf parks create new demand. They also serve as brand activation hubs, with companies like Rip Curl and O'Neill hosting demo days and athlete appearances to boost sales. Additionally, surf parks drive growth in hospitality and retail, anchoring mixed-use developments with hotels, restaurants, and pro shops. Local governments are adapting regulations, offering tax incentives and expedited permits to attract these projects and diversify tourism beyond traditional beach economies.

Expanding Technological Innovation In Water Sports Equipment

Advancements in material science are setting new performance standards and enabling premium pricing. Starboard's switch from virgin carbon fiber to basalt fiber in SUP boards cut its carbon footprint by 98% while maintaining rigidity, appealing to eco-conscious consumers. In June 2025, Rip Curl will integrate OCENA rubber, a 74% bio-based neoprene alternative, into its E-Bomb and Dawn Patrol wetsuits, with the material expected to cover 60% of its wetsuit range. Decathlon's Yulex100 wetsuit, launched in June 2024, reduced CO2 emissions by 80% compared to neoprene and is priced at EUR 20 (USD 22) for kids, proving sustainability can be affordable. Sensor integration is also advancing, with patents for wetsuit-embedded composites that monitor body temperature and wave impacts, offering real-time feedback via apps. Yamaha's 2026 CrossWave watercraft, priced at USD 32,499, features a 1.9-liter engine and a 26.4-gallon fuel tank, targeting fishing and adventure touring. These innovations shorten product replacement cycles, driving upgrades but challenging retailers with inventory management.

Increased water sports events and tournaments

Regulatory momentum and shifting consumer preferences are making sustainability a baseline expectation. Rip Curl aims to source 75% of its wetsuits from plant-based neoprene alternatives by 2030, with 60% already using OCENA rubber. Its wetsuit recycling program, active in Australia, North America, France, Portugal, and Spain, has diverted over 40,000 units from landfills in four years, setting a circular economy model now adopted by competitors. Fanatic is expanding material use in windsurf boards with bio-resin (Sicomin GreenPoxy), flax fiber, cork cores, and bamboo. FCS and Futures incorporate recycled fishing nets via the Net Plus program, while sugarcane bio-foam replaces petroleum-based cores in fins. Patagonia’s Yulex plant-based rubber, derived from guayule trees, is an industry standard for wetsuit linings, with licensing agreements extending its use. European retailers increasingly require ISO 14001 certifications, driving compliance and adoption. Brands leading in sustainability attract premium buyers willing to pay 15-20% more, while laggards risk de-listing as chains like Decathlon and REI enforce stricter supplier standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limitations Due To Seasonal And Weather Dependence | -0.8% | Global, most acute in temperate and northern climates | Short term (≤ 2 years) |

| High Cost Of Advanced And Premium Equipment | -0.6% | Emerging markets in Asia Pacific, South America, Middle East & Africa | Medium term (2-4 years) |

| Shortage Of Skilled Instructors In Emerging Markets | -0.4% | Asia Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) |

| Counterfeit And Low‑Quality Imports Diluting Brand Equity | -0.3% | Asia Pacific, with cross-border e-commerce channels amplifying reach | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limitations Due To Seasonal And Weather Dependence

Weather volatility narrows revenue cycles, with temperate markets generating 60-70% of annual sales between May and September. Cool summers or prolonged rain can reduce annual performance by double digits, a risk surf park investments aim to mitigate but remains significant for ocean-dependent activities like surfing and sailing. Rental operators face inventory challenges, with equipment idle for 6-8 months annually in regions like northern Europe and Canada, impacting returns on capital. Small independent retailers, lacking financial resilience, often face consolidation as larger chains acquire distressed assets. Climate change adds unpredictability, with shifting wind patterns affecting sailing seasons and warming waters altering fish migration, impacting kayak fishing demand. Insurance costs are rising in hurricane-prone areas, with some carriers excluding water sports equipment or imposing high deductibles. Manufacturers are addressing this by creating modular, multi-season products, such as kayaks with ice-fishing attachments and wetsuits with thermal linings, though these add cost and complexity. Geographic diversification is now critical, with brands expanding into Southern Hemisphere markets to offset Northern Hemisphere seasonality, despite the need to duplicate supply chains and marketing infrastructure.

High Cost Of Advanced And Premium Equipment

In emerging markets, where median household incomes are one-tenth of those in developed economies, premium surfboards over EUR 1,000 (USD 1,090) and O'Neill wetsuits at EUR 454-530 (USD 495-578) remain out of reach. Liquid Force's USD 1,799 electric hydrofoil targets affluent early adopters, limiting broader appeal. Brands using sensors, sustainable materials, and proprietary composites justify high prices but exclude price-sensitive buyers. Entry-level surfboards at EUR 300-500 (USD 327-545) use lower-grade materials, reducing durability and increasing replacement costs, discouraging repeat purchases. Financing options are limited, with few retailers offering installment plans or lease-to-own models common in bicycles or fitness equipment. In Asia Pacific and South America, import tariffs adding 20-40% to costs further inflate prices. Second-hand markets, like BuoyShare, offer rentals at EUR 23 per day (USD 25), but this impacts new sales. Manufacturers are introducing tiered products, such as Decathlon's EUR 350 (USD 382) Tamahoo 100 inflatable windsurf kit for budget-conscious buyers, though slim margins limit R&D reinvestment. The challenge lies in balancing volume growth in emerging markets with margin preservation in developed economies, favoring vertically integrated players controlling manufacturing costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sports Type: Paddle Equipment Gains On Surfing Dominance

In 2025, surfing equipment contributed 58.21% of total revenue, highlighting its cultural importance and strong retail presence. Paddle equipment, however, is growing at a 6.58% CAGR through 2031, surpassing the overall market by 80 basis points. Stand-up paddleboarding is attracting fitness enthusiasts, touring paddlers, and yoga practitioners, expanding its market beyond traditional surfers. Inflatable SUPs, priced at EUR 350-500 (USD 382-545), are lowering entry barriers. In December 2025, Starboard announced its 2026 All-Star race board with improved rails, drainage, and stability, showcasing ongoing innovation to sustain premium pricing. Kayaks and canoes are benefiting from fishing and adventure tourism trends, with Pelican International and Confluence Outdoor offering durable, affordable rotomolded polyethylene models.

Board equipment, including bodyboards, skimboards, and wakeboards, appeals to younger audiences but faces competition from skateboarding and BMX. Ski equipment, such as water skis and kneeboards, is declining as wakeboarding and wakesurfing gain popularity, though slalom skiing retains a niche competitive following. Sailing and yachting gear, including small sailboats and catamarans, targets affluent buyers and club programs, with Hobie Cat and BIC Sport (Tahe Outdoors) leading through dealer networks and instructional partnerships. The International Canoe Federation’s 2026 SUP World Championships and other events are boosting visibility, historically driving 15-20% sales growth in host regions.

By Price Tier: Premium Segment Outpaces Mass Despite Smaller Base

In 2025, mass-tier products accounted for 65.21% of sales, targeting budget-conscious buyers and rental operators focused on cost over performance. The premium segment, however, is growing at a 7.34% CAGR, outpacing the overall market by 156 basis points. This reflects a divide in consumer preferences, with affluent buyers spending EUR 454-530 (USD 495-578) on O'Neill wetsuits with OCENA bio-based rubber or USD 1,799 on Liquid Force electric hydrofoils for unique experiences. Premium consumers also value sustainability, as seen in Rip Curl's OCENA rubber wetsuits and Starboard's basalt-fiber SUPs, which command 15-20% price premiums.

Advanced technologies, sensor-enabled wetsuits, GPS-tracked boards, and app-connected watercraft are exclusive to premium tiers, justifying higher prices. Yamaha's 2026 CrossWave PWC, priced at USD 32,499, targets adventure and fishing enthusiasts with features like 4-seat capacity and a 26.4-gallon fuel tank, expanding use cases beyond recreation. Mass-tier products face commoditization and slim margins, with manufacturers relying on price competition and volume for profitability. Decathlon's EUR 20 (USD 22) kids' wetsuit and EUR 350 (USD 382) inflatable windsurf kit illustrate this approach, offering acceptable quality at low prices. However, higher return rates and shorter replacement cycles due to lower durability reduce customer lifetime value. Brands must choose between volume-driven mass-market strategies or margin-rich premium positioning, with few excelling in both.

By Distribution Channels: Online Gains Share But Offline Retains Majority

In 2025, offline channels captured 70.28% of sales, led by specialty retailers, sporting goods chains, and marina pro shops offering hands-on trials and expert advice. Online channels, growing at a 6.89% CAGR, gained from direct-to-consumer strategies and second-hand marketplaces like BuoyShare, which facilitated EUR 2.5 million (USD 2.7 million) in transactions. Decathlon's July 2025 launch of a nautical rental service in Gran Canaria showcased omnichannel strategies, offering paddleboards at EUR 35 per day (USD 38) and kayaks at EUR 40 per day (USD 44).

Online sales grew in consumables like wetsuits and traction pads due to standardized sizing, while boards and kayaks remained in-store purchases due to shipping costs and trial preferences. Brexit and customs reforms disrupted cross-border e-commerce, with UK-EU shipments facing delays and tariff uncertainties, benefiting local online retailers. Social commerce expanded as Instagram and TikTok enabled influencers to link directly to product pages, driving transactions. However, online channels faced higher return rates of 15-20% compared to 5-8% offline, reducing margins due to sizing issues and buyer's remorse. Hybrid models are emerging, with brands like Rip Curl and O'Neill opening experiential flagship stores that act as showrooms and community hubs.

By End User: Kids Segment Accelerates As Schools Integrate Water Sports

In 2025, adults made up 86.59% of demand, highlighting their purchasing power and established habits. Meanwhile, the kids segment is growing rapidly at a 7.45% CAGR, driven by schools and municipalities incorporating water safety and aquatic sports into curricula. Regions like Australia, California, and Scandinavia mandate swimming and paddling lessons for students aged 8-14. Decathlon’s June 2024 launch of a EUR 20 (USD 22) kids' shorty wetsuit and a EUR 25 (USD 27) adult snorkel top, made from Yulex100 neoprene-free material, has lowered barriers for families entering water sports.

Manufacturers are downsizing and lightening equipment for smaller frames, with inflatable SUPs and kayaks offering adjustable features for extended usability. Youth tournaments and summer camps are increasing, with the International Canoe Federation supporting junior-level SUP and kayak competitions to build early brand loyalty. However, the kids segment faces retention challenges as participation drops during adolescence due to competing activities like team sports and video games. A key opportunity lies in offering starter equipment that upgrades to advanced tiers to retain customers as they age. Adult participation is steady in mature markets like North America and Western Europe, with growth focused on the 35-55 age group seeking low-impact fitness. Younger adults (18-34) are shifting toward high-adrenaline activities like wakeboarding and foiling.

Geography Analysis

In 2025, North America accounted for 35.68% of revenue, driven by 47.3 million motorized boating participants and 23 million paddle sports enthusiasts[3]Source: Outdoor Foundation. "Outdoor Participation Trends Report 2022." outdoorfoundation.org.. The Asia Pacific region, growing at a 6.78% CAGR, surpasses the global average by 100 basis points. China's coastal tourism investments, Japan's aging population favoring low-impact recreation, and Australia's surf culture are fueling demand, supported by government spending on waterfront infrastructure and aquatic safety. India and Southeast Asia offer growth potential, though instructor shortages and affordability challenges hinder immediate expansion. In Europe, mature markets like Germany, the UK, France, Italy, and Spain are growing modestly, with demand focused on premium and sustainable products such as Rip Curl's OCENA rubber wetsuits, which comply with EU environmental standards. South America, led by Brazil, Argentina, and Chile, benefits from domestic surf tourism and improved retail distribution, though economic instability and currency depreciation pose challenges. The Middle East and Africa, with the UAE, Saudi Arabia, and South Africa as key players, are scaling rapidly as luxury resorts incorporate water sports and governments invest in Red Sea and Arabian Gulf tourism. Regulatory frameworks vary, with the EU and California enforcing eco-certifications that drive sustainable material adoption, while emerging markets lack standardized safety and environmental protocols. Companies must adapt product portfolios to regional needs—compact equipment for space-constrained Asian markets versus larger, feature-rich models for North American buyers with ample storage.

In 2025, Europe's established markets, led by Germany, the UK, France, and Spain, maintained stable demand, while growth shifted to Scandinavia and Eastern Europe, where participation is rising from lower levels. Portugal's EUR 25 million (USD 27 million) Praia da Vagueira surf park investment highlights Southern Europe's efforts to extend tourism beyond summer peaks. The Netherlands and Belgium are expanding canal and lake-based paddle sports with municipal investments in launch facilities and storage lockers. Poland's growing middle class is adopting kayaking and windsurfing, with domestic brands like Kubus Sports gaining traction. Stricter regulatory compliance, such as ISO 14001 environmental certifications, benefits established brands with strong sustainability programs but creates barriers for smaller players.

South America's markets, led by Brazil, Argentina, and Chile, feature strong domestic surf cultures, but affordability issues and import tariffs limit premium product penetration. Brazil's extensive coastline and warm waters support surfing and stand-up paddleboarding, with local manufacturers competing on price with imports. In Argentina's Patagonia region, kayak touring and whitewater activities are growing, though infrastructure remains underdeveloped outside cities. Chile's coastal cities, including Santiago, Valparaíso, and Concepción, are seeing retail growth, with specialty shops targeting first-time buyers. Frontier markets like Peru and Colombia show potential, but growth depends on tourism and rising disposable incomes. Currency volatility, including peso and real depreciation, continues to pressure dollar-denominated earnings for multinational brands.

Competitive Landscape

Key players such as Decathlon, Johnson Outdoors, Yamaha, Bombardier, and Rip Curl hold significant positions in the surface water sports equipment market, employing strategies like vertical integration, athlete sponsorships, and omnichannel distribution to maintain their market share. Decathlon's planned launch of a nautical rental service in Gran Canaria in July 2025, along with the introduction of the Yulex100 wetsuit in June 2024, highlights its approach to expanding market reach while reducing price barriers. Johnson Outdoors' acquisition of Endless Summer Technologies for USD 12.2 million in October 2024 aims to enhance its SCUBAPRO division, showcasing mergers and acquisitions as a strategy for capability growth.

Additionally, its December 2025 shipments of the HYDROS PRO 2 BCD emphasize its focus on product innovation. Rip Curl's 8-year, multi-million-dollar sponsorship agreement with Stephanie Gilmore, signed in March 2024, demonstrates its strategy to leverage athlete credibility for driving premium-tier sales. Yamaha's Spring 2026 launch of the CrossWave PWC, priced at USD 32,499, targets fishing and adventure segments, signaling diversification beyond traditional recreational applications. White-space opportunities are expanding in rental platforms. The merger of Boatsetter and GetMyBoat has created a USD 500 million booking ecosystem, effectively converting hesitant consumers into repeat buyers. Sustainability is emerging as a key differentiator in the market. Starboard has achieved a 98% reduction in carbon footprint by using basalt fiber as a substitute, while Rip Curl has committed to sourcing 75% of its neoprene responsibly by 2030.

However, challenges such as counterfeit imports and instructor shortages in the Asia Pacific and Middle East & Africa regions threaten profit margins and slow adoption rates. To address these issues, brands are investing in authentication technologies and forming training partnerships. Furthermore, the integration of advanced technologies, such as sensor-enabled wetsuits and GPS-tracked boards, is creating performance advantages that justify premium pricing but require ongoing R&D investments. The competitive landscape increasingly favors companies that can balance innovation with cost efficiency, leveraging their scale to manage material inflation while maintaining product differentiation.

Surface Water Sports Equipment Industry Leaders

-

Decathlon S.A.

-

Authentic Brands Group

-

Aqua Lung International

-

Cressi S.p.A.

-

Johnson Outdoors Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Morey introduced two new bodyboards for the Summer: the MACH 7-7 PLC Pro, developed in collaboration with two-time World Champion Pierre Louis Costes, and the Turbo 4, which updated a classic bodyboard design.

- March 2025: ACCIONA and DDB Melbourne introduced the first product from 'Turbine Made', an initiative that converted decommissioned wind turbine blades into new materials and products to prevent landfill disposal. The initiative produced the world's first 'Turbine Made' surfboard, which was developed in collaboration with Australian professional surfer Josh Kerr and his team at Draft Surf.

- February 2025: Chanel released a new luxury surfboard priced at USD 8,900. Philippe Barland, a surfboard shaper based in Bayonne, France, manufactured the board. The silver-colored surfboard, part of the spring-summer collection, differed from the previous year's model. The board's construction incorporated fiberglass and polyurethane foam, with aluminum elements.

Global Surface Water Sports Equipment Market Report Scope

| Surfing Equipment (Surfboards, Wetsuits, Leashes, Traction Pads) |

| Paddle Equipment (Kayaks, Canoes, Stand‑Up Paddleboards) |

| Board Equipment (Bodyboards, Skimboards, Wakeboards Apart From Pure Surfing Boards) |

| Ski Equipment (Water Skis, Kneeboards) |

| Sailing And Yachting Equipment (Small Sailboats, Catamarans) |

| Mass |

| Premium |

| Offline Channels |

| Online Channels |

| Kids |

| Adults |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| Sports Type | Surfing Equipment (Surfboards, Wetsuits, Leashes, Traction Pads) | |

| Paddle Equipment (Kayaks, Canoes, Stand‑Up Paddleboards) | ||

| Board Equipment (Bodyboards, Skimboards, Wakeboards Apart From Pure Surfing Boards) | ||

| Ski Equipment (Water Skis, Kneeboards) | ||

| Sailing And Yachting Equipment (Small Sailboats, Catamarans) | ||

| Price Tier | Mass | |

| Premium | ||

| Distribution Channels | Offline Channels | |

| Online Channels | ||

| End User | Kids | |

| Adults | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the surface water sports equipment market in 2026?

The surface water sports equipment market size is estimated at USD 13.26 billion in 2026.

Which region is growing fastest for water sports gear?

Asia-Pacific is advancing at a 6.78% CAGR thanks to coastal tourism spending in China, Japan, and Australia.

What product category is expanding most quickly?

Paddle equipment, especially stand-up paddleboards, is growing at a 6.58% CAGR through 2031.

Why are premium items gaining share?

Bio-based materials, sensor technology, and higher performance specifications justify premiums and drive a 7.34% CAGR in the segment.

Page last updated on: