Football Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

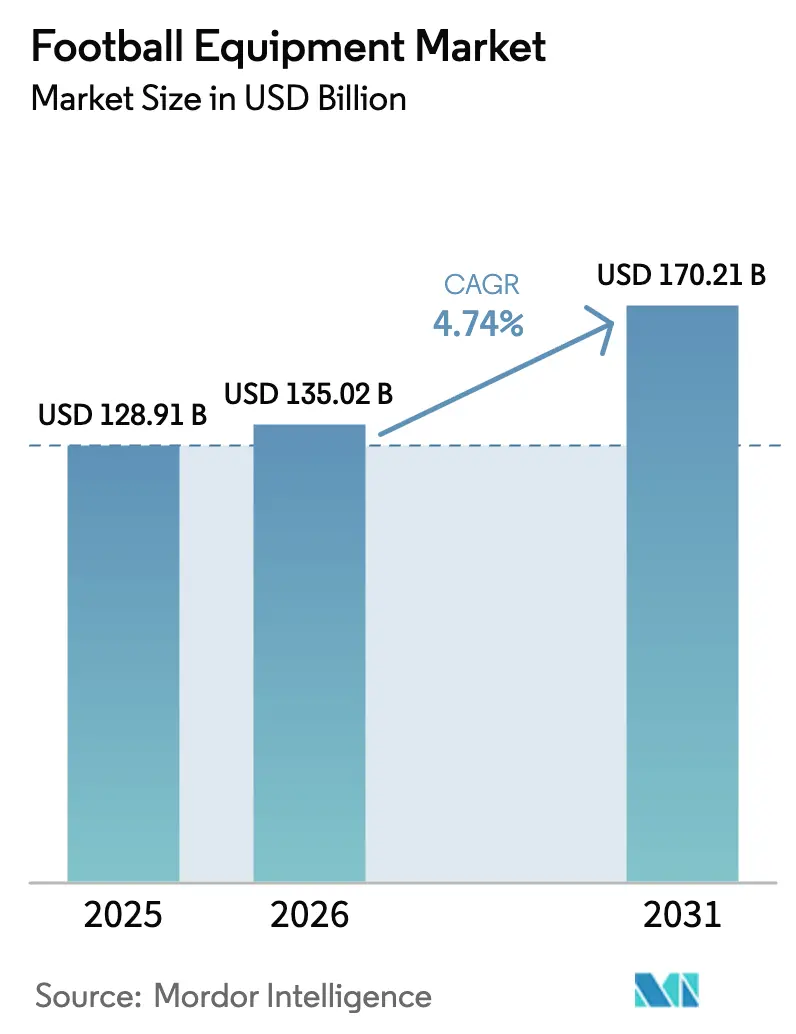

| Market Size (2026) | USD 135.02 Billion |

| Market Size (2031) | USD 170.21 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

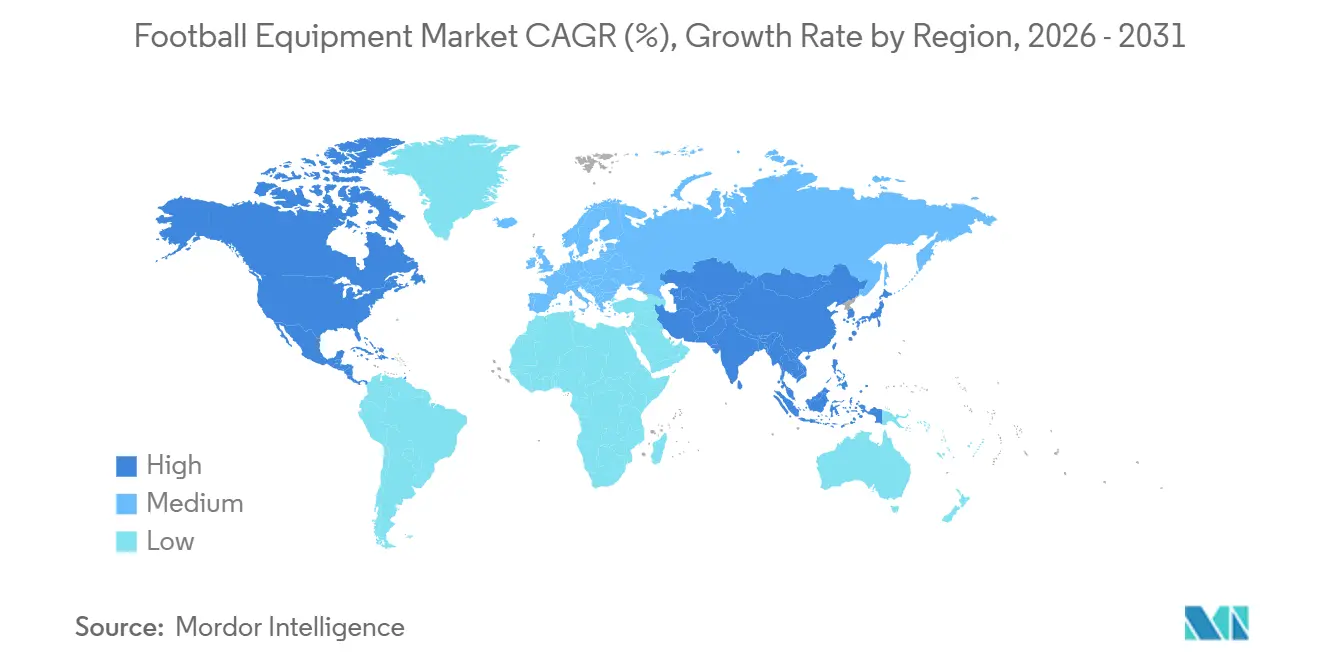

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

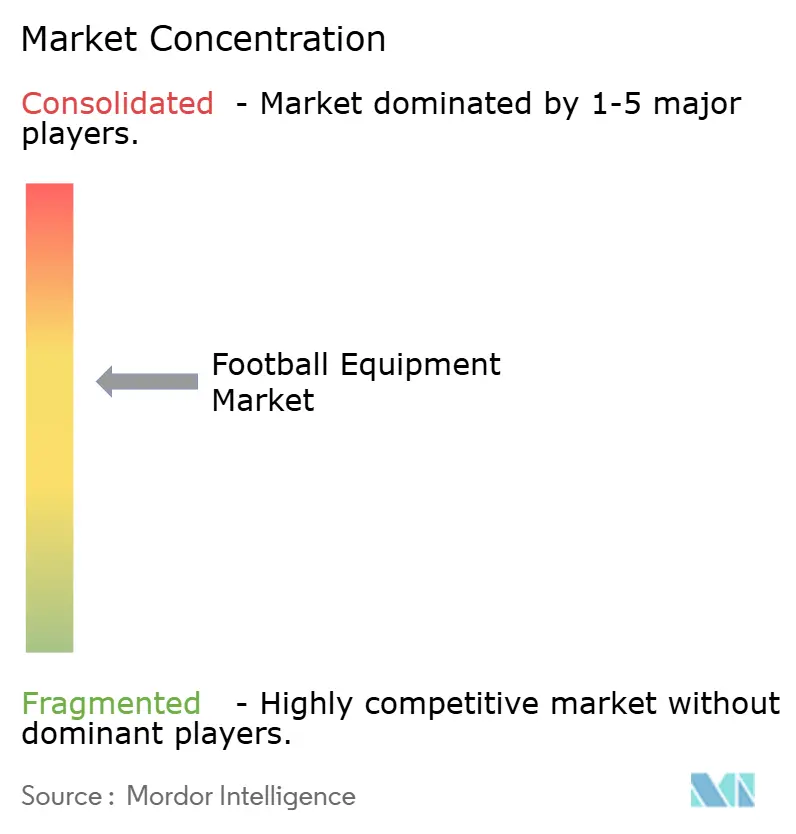

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Football Equipment Market Analysis by Mordor Intelligence

The football equipment market size was valued at USD 128.91 billion in 2025 and estimated to grow from USD 135.02 billion in 2026 to reach USD 170.21 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031). Rising grassroots participation, especially among women and children, sustained sponsorship spending, and rapid rollout of sensor-enabled gear collectively underpin volume and price growth for the football equipment market. Clubs are channeling broadcast windfalls into youth academies, which lifts baseline demand for certified boots, balls, and protective wear. Direct-to-consumer e-commerce is narrowing the gap between brands and consumers, allowing faster rollouts of limited collections and data-driven replenishment. Meanwhile, technology upgrades, carbon-fiber soleplates, graphene-infused fabrics, and NFC (Near-Field Communication) authentication chips support premiumization even as mass-market volumes dominate. Heightened counterfeit enforcement in the European Union and new ISO (International Organization for Standardization) safety mandates in Asia-Pacific are nudging consumers toward verifiable, federation-approved gear.

Key Report Takeaways

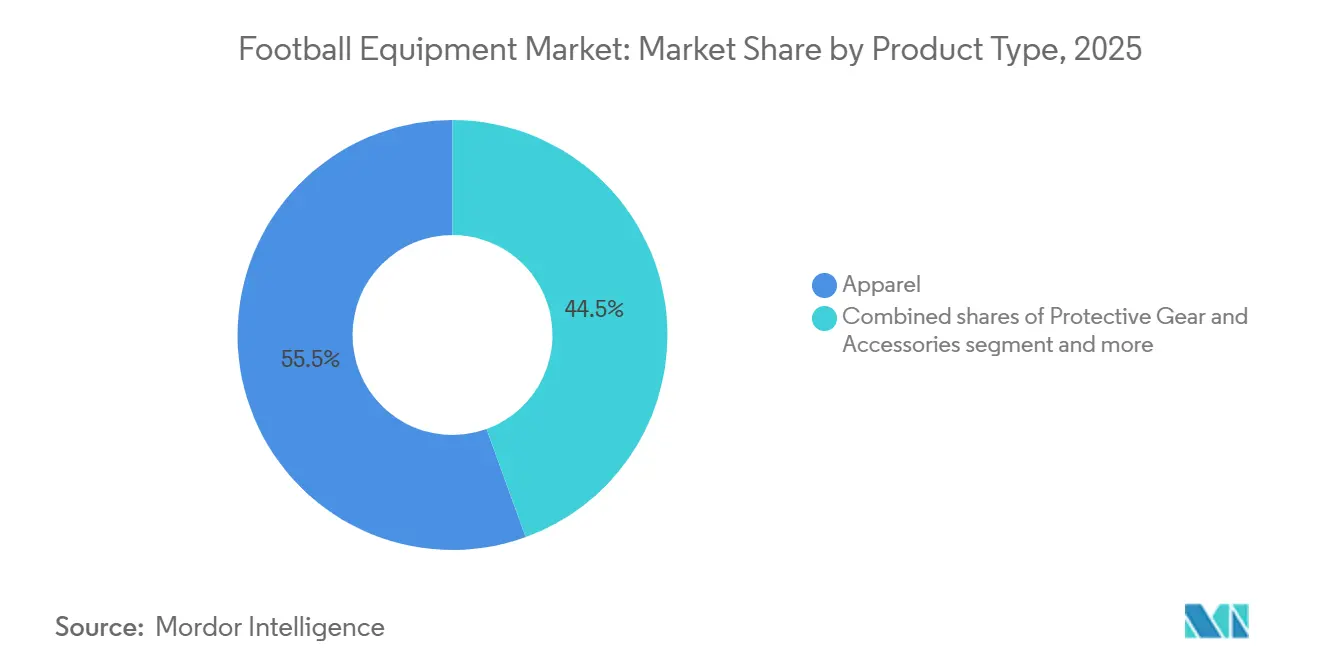

- By product type, apparel led with 55.54% of the football equipment market share in 2025, while protective gear and accessories are on track for the fastest expansion at 5.47% CAGR through 2031.

- By category, the mass segment captured 71.22% of the football equipment market size in 2025, whereas premium products are forecast to rise at a 6.03% CAGR during 2026-2031.

- By end-user, adults accounted for 53.27% of spending in 2025; the children segment is projected to advance at a 6.26% CAGR to 2031.

- By distribution channel, offline outlets retained 53.26% of sales in 2025, yet online platforms are set for a 5.21% CAGR as virtual try-on tools boost conversion and slash return rates.

- By geography, Europe controlled 33.47% of revenue in 2025; Asia-Pacific is the fastest-growing region with a 4.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Football Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in organized football globally | +1.2% | Global, acceleration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Enhanced marketing and athlete endorsement campaigns | +0.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Growth of smart and wearable sports tech gear | +0.9% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Rising female participation in football activities | +1.0% | Europe, North America, Middle East | Long term (≥ 4 years) |

| Technological innovation in equipment materials and design | +1.1% | Innovation hubs in North America, Europe, Japan | Medium term (2-4 years) |

| Expanding popularity of major international football events | +0.7% | Host nations for 2026 and 2034 World Cups | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Participation in Organized Football Globally

More schools, corporations, and municipal programs are integrating league-sanctioned football, converting social players into paying equipment buyers. FIFA (International Federation of Association Football) counted 270 million active players in 2024, while China aims for 50 million registered participants by 2025, each needing boots, apparel, and protective gear. Saudi Arabia’s Public Investment Fund bought majority stakes in four Pro League clubs, tripling league market value and triggering a surge in sales of official match balls and training kits [1]Source: Saudi Vision 2030, "VISION2030.GOV.SA, vision2030.gov.sa. India’s Super League grew to 12 franchises in 2024, mandating standardized gear for youth squads, and Australia’s A-League expansion lifted demand for shin guards and keeper gloves. Moving from street games to formal leagues raises safety expectations and channels spending toward ISO-certified products.

Enhanced Marketing and Athlete Endorsement Campaigns

Endorsements remain a powerful purchase catalyst for consumers aged 15-25. Nike outfits more than 1,000 footballers across 70 countries, driving billions of social-media impressions during tournaments. Adidas renewed exclusive rights to supply UEFA (Union of European Football Associations) match balls through 2030, ensuring brand exposure to the Champions League’s base of 220 million viewers [2]Source: UEFA (Union of European Football Associations), "Champions League’s", uefa.com. Puma’s tie-up with Neymar Jr. generated limited-edition boots that sold out in hours, illustrating scarcity-led demand. The global transfer market showed a hike in 2024, with women’s transfers up 20.8%, underlining the commercial heft of star power. Brands are layering in AR try-ons and influencer-led livestreams to turn social engagement into immediate sales.

Growth of Smart and Wearable Sports Tech Gear

Connected boots, balls, and GPS vests are filtering down from elite clubs to amateur fields. FIFA’s Electronic Performance and Tracking Systems (EPTS) rules codify accuracy thresholds for heart rate and positional data, giving early-mover suppliers a compliance edge. Nike’s smart insoles track ground-contact time, while Adidas embedded inertial sensors inside official balls for real-time spin data [3]Source: United States Patent and Trademark Office, "Creating heaven from organized Chaos", USPTO.GOV.. Japan’s J-League rolled out wearables across youth tiers in 2024, and Australia’s Football Federation now requires GPS vests for national U-17 teams. The technology premium lifts average selling prices by 15-20% and unlocks data-subscription revenue streams.

Rising Female Participation in Football Activities

Women’s football is vaulting from niche to mainstream. The 2023 FIFA Women’s World Cup drew 1.42 billion viewers and 5 billion social engagements, lifting demand for women-specific boots and compression tops. Saudi Arabia fielded 10 top-flight women’s clubs and counted 700,000 girls in school leagues by 2024. UEFA women’s competitions attracted 8 million stadium spectators in 2024, prompting sponsors to earmark dedicated female athlete budgets. Brands responded with narrower heel counters, lighter studs, and tailored biomechanics. Growth in the children segment points to future adult spending as today’s academy girls mature. As the sport garners more attention, media rights and sponsorship deals are witnessing a significant uptick. This surge not only underscores the sport's rising prominence but also hints at its lucrative potential in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit and low-quality equipment | -0.6% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| High cost of premium football gear products | -0.5% | Emerging markets in Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Seasonal demand fluctuations impacting sales cycles | -0.4% | Europe, North America | Short term (≤ 2 years) |

| Affordability limitations in emerging country markets | -0.7% | Asia-Pacific (ex-Japan, Australia), Africa, parts of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Counterfeit and Low-Quality Equipment

Global counterfeit trade dilutes brand equity and jeopardizes player safety. EU customs seized EUR 10 billion worth of fake goods in 2023, with sports items at a EUR 300 million slice, including substandard football boots and shin guards. Online marketplaces enable sellers to undercut authentic products by 40-60%. Brands are deploying blockchain tags and NFC chips, adding USD 2-5 to unit costs but restoring consumer trust. Federations now require ISO-20344-certified protective gear, steering buyers toward verified channels. The counterfeit trade's reach extends beyond mere financial losses, threatening the very essence of trust that brands have built over decades. As counterfeiters become more sophisticated, the challenge for brands intensifies, pushing them to innovate and adapt. With the stakes this high, the battle against counterfeiting is not just a legal fight but a race against time and technology.

High Cost of Premium Football Gear Products

Flagship boots priced at USD 200-300 strain consumer budgets in emerging markets where monthly incomes average USD 500-800. Rapid 12-18-month product cycles exacerbate affordability gaps. Local makers in India, Indonesia, and Nigeria fill the void with USD 30-50 offerings, sacrificing advanced materials and endorsements. Yet aspirational urban buyers continue to reach for hero models tied to marquee athletes, sustaining the premium segment’s 6.03% CAGR. Despite the financial strain, the allure of these flagship boots remains strong, highlighting a cultural significance that transcends mere affordability. As global brands grapple with pricing strategies, the dance between aspiration and budget becomes ever more pronounced in these burgeoning markets. The resilience of the premium segment underscores a broader narrative: in the world of fashion, desire often trumps economic constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominates, Protective Gear Accelerates

In 2025, apparel claimed a dominant 55.54% share of the football equipment market, driven by frequent jersey refreshes and the emotional resonance of club colors. As youth leagues become increasingly aware of concussion risks, the demand for protective gear and accessories is projected to grow at a 5.47% CAGR. Footwear is evolving, with smart-insole integrations and carbon-fiber plates leading the charge, and certain models commanding prices above USD 300. As sensor costs decrease, the market for football boots is set to expand, with analytics becoming a standard feature even in entry-level lines.

Regulatory developments are fueling the surge in protective gear. FIFA’s EPTS (FIFA Electronic Performance and Tracking Systems) regulations have expanded to include shin-guard sensors and GPS vests, elevating these once-specialized products to essentials for academy teams. Apparel's stronghold is bolstered by limited-edition releases and sustainability initiatives; for instance, Parley's ocean-plastic kits and Flyknit jerseys frequently sell out within days. On the horizon, biodegradable innovations like Puma’s Re: Suede boots suggest a shift towards a circular economy, potentially shortening replacement cycles while enhancing brand loyalty.

By Category: Mass Market Leads, Premium Segment Gains Momentum

In 2025, the mass category dominated the football equipment market, capturing a substantial 71.22% share. Catering primarily to price-sensitive consumers, these mass-market offerings found their primary sales channels in general-trade outlets. Meanwhile, the premium segment is on an upward trajectory, boasting a robust 6.03% CAGR. This growth is largely driven by elite clubs, semi-professional players, and urban enthusiasts, all of whom are increasingly seeking performance enhancements. These enhancements come in the form of advanced materials like carbon fiber, moisture-wicking fabrics, and cutting-edge wearables. As the market evolves, premium boots are not only commanding a larger slice of the football equipment market but are also benefiting from the rise of direct-to-consumer channels. These channels are proving lucrative, enabling brands to secure higher profit margins.

In a bid to capture market share, mass-market suppliers have rolled out competitive designs priced at just one-third of their global counterparts. This aggressive pricing strategy has often swayed consumers in rural and suburban areas. However, these suppliers grapple with challenges, notably the persistent issue of counterfeit products and the constraints of modest R&D budgets. On the other hand, premium vendors, while facing their own set of challenges, have found innovative solutions to address cost concerns. They offer instalment payment plans, subscription programs, and buy-back schemes, effectively distributing the financial burden over multiple seasons. This strategy not only eases the immediate financial strain on consumers but also fosters brand loyalty and repeat business.

By End-User: Adults Lead, Children Segment Surges

In 2025, adults accounted for a significant 53.27% of total spending, largely propelled by professional and corporate leagues that have a penchant for premium boots and apparel. Meanwhile, the children's segment is set to experience a robust 6.26% CAGR through 2031, fueled by substantial investments from China, India, and Saudi Arabia into school programs. As government grants increasingly cover starter kits and federation rules tighten on safety specifications, the allocation of the football equipment market is shifting, with a notable expansion towards junior lines.

Adult consumers are increasingly gravitating towards premium footwear, with many opting to replace their boots every 12-18 months to stay in sync with professional upgrades. On the other hand, youth programs prioritize affordability, but the need for frequent size adjustments leads to a consistent refresh cycle. In response to these dynamics, brands are innovating by customizing junior boots, incorporating narrower lasts and lighter uppers. These junior boots are strategically priced 20-30% below their adult counterparts, yet maintain design continuity, ensuring they resonate with the aspirational desires of young consumers.

By Distribution Channel: Offline Stores Retain Edge, Online Gains Ground

Offline outlets still captured 53.26% of 2025 sales, supported by fit-focused purchases and immediate availability. However, online channels are rising at a 5.21% CAGR on the back of virtual sizing tools and exclusive web-only launches. The football equipment market size transacted online will continue to climb as broadband penetration improves and social commerce integrates one-click checkout features. As consumers increasingly prioritize convenience, the shift towards online platforms is becoming more pronounced. This trend is further bolstered by the growing trust in digital transactions and the allure of exclusive online deals.

Brick-and-mortar chains are adding experiential services, cleat customization, gait analysis, and heat-molding to fend off showrooming. Meanwhile, brands’ own apps bundle content, training plans, and loyalty points, nudging repeat purchases. In developing regions where logistics remain patchy, traditional retailers and informal kiosks still dominate last-mile sales. These localized players leverage their understanding of community preferences, ensuring they cater to specific regional demands. As a result, they maintain a competitive edge, even as global brands push for a larger footprint.

Geography Analysis

Europe maintained a 33.47% foothold in 2025, underpinned by Germany’s 7.1 million and England’s 11.5 million registered players. High per-capita spend and rapid upgrade cycles keep the region profitable, though growth is tapering as participation in Western Europe saturates. Funding from UEFA’s development grants is redirecting incremental gains toward Eastern Europe, where Poland and the Czech Republic are investing in artificial-turf pitches and academy scholarships.

Asia-Pacific is the quickest-advancing region with a 4.89% CAGR through 2031. China’s goal of 50 million registered players by 2025 feeds multi-year equipment pipelines. India’s Super League expansion and Japan’s rollout of a wearable mandate bolster demand for technology-rich kit. Affordability gaps remain; premium boots above USD 150 are aspirational buys for urban elites, leaving ample room for domestic producers to supply USD 30-50 alternatives. North America is undergoing structural lift as MLS attendance hit 11.2 million in 2025 and stadium capex crossed USD 11 billion ahead of the 2026 World Cup. Replica sales are predicted to jump 40% in the six months before kickoff. Canada and Mexico add tailwinds through national-team qualification and Liga MX viewership. High youth participation, 3 million U.S. Youth Soccer registrations, creates repetitive equipment purchases as children outgrow boots annually.

South America remains a heritage bulwark. Argentina injected ARS 4.25 billion into 800 clubs, improving pitch and locker-room standards. Brazil’s export pipeline feeds replica-jersey demand as fans follow transferred stars abroad. Economic volatility and counterfeit prevalence weigh on premium adoption, yet ingrained passion secures baseline consumption. The Middle East and Africa hold high potential as public budgets finance stadiums and academies. Saudi Arabia’s 15-stadium blueprint tied to the 2034 World Cup will catalyze wholesale equipment tenders. The UAE and Qatar host annual youth tournaments that require standardized kits. Affordability hurdles persist; most buyers opt for mass-market boots unless subsidized by federations or NGOs.

Competitive Landscape

The football equipment market shows a moderate concentration, dominated by Nike, Adidas, and Puma, yet open to regional challengers. Nike booked USD 51.4 billion in 2024 revenue, enabling tighter control over pricing and data. Adidas posted EUR 21.4 billion in 2023 sales, and its e-commerce arm delivered 22% of turnover. Puma differentiates with sustainability plays such as the Re: Suede biodegradable boot and visibility from Neymar Jr. endorsements.

Patent portfolios around smart insoles, NFC-enabled match balls, and moisture-wicking knits provide technological moats. Compliance costs linked to FIFA EPTS, IEC, and IEEE standards erect barriers for low-capex rivals. Counterfeit leakage squeezes margins, pushing incumbents toward authentication tech and legal enforcement. In emerging markets, local makers leverage lower labor costs and tariff shelters to supply USD 30-50 boots, sometimes bundling entry-level wearables as optional extras.

Strategic alliances are reshaping the ecosystem. Adidas holds UEFA contracts through 2030, guaranteeing product exclusivity on Champions League nights. Nike’s minority stake in Zelus Analytics accelerates sensor integration, while Puma’s Saudi Pro League partnership secures visibility ahead of the 2034 World Cup. Circular-economy pilots, take-back programs, and refurb lines are nascent but could extend product lifespans and reshape revenue recognition.

Football Equipment Industry Leaders

-

Adidas AG

-

Nike Inc.

-

Under Armour, Inc.

-

New Balance, Inc

-

ASICS Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Adidas unveiled the Predator football boot with advanced POWERSPINE and NANOSTRIKE+ technologies for improved control and traction. The boot is engineered for modern play and is available globally in select stores and online.

- August 2025: New Balance expanded its partnership with Boston College to include the football program, marking its first involvement in American football cleats and apparel for the school’s team.

- April 2025: Nike and the NFL launched the Rivalries Program, introducing new uniforms and fan gear inspired by local communities. The initiative spans four seasons and will roll out jerseys and related apparel globally.

Global Football Equipment Market Report Scope

The basic equipment worn by most football players, including helmets, shoulder pads, gloves, shoes, thigh and knee pads, a mouthguard, and a jockstrap or compression shorts, is designed to protect them from injury while playing the sport, and is collectively referred to as football equipment. The global football equipment market is segmented by product type, category, end-user, distribution channel, and geography. By product type, the market is segmented as football shoes, footballs, protective gear, and accessories. By category, the market is segmented into mass and premium. By end-user, the market is divided into adults and children. By category, the market is divided into mass and premium. By distribution channel, the market is segmented into offline and online retail stores. The study also provides a global-level analysis of the major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Football Shoes |

| Football Apparel |

| Protective Gear and Accessories |

| Footballs |

| Mass |

| Premium |

| Adults |

| Children |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Football Shoes | |

| Football Apparel | ||

| Protective Gear and Accessories | ||

| Footballs | ||

| Category | Mass | |

| Premium | ||

| End-User | Adults | |

| Children | ||

| Distribution Channel | Offline Stores | |

| Online Stores | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the football equipment market?

The football equipment market size stands at USD 135.02 billion in 2026.

How fast is demand for protective gear growing?

Protective gear and accessories are forecast to expand at 5.47% CAGR through 2031.

Which region will add sales the fastest?

Asia-Pacific is expected to register the quickest gains with a 4.89% CAGR during 2026-2031.

How big is the children segment opportunity?

Spending on children’s equipment is projected to rise at 6.26% CAGR as school programs scale across China, India, and Saudi Arabia.

Page last updated on: