Brewery Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

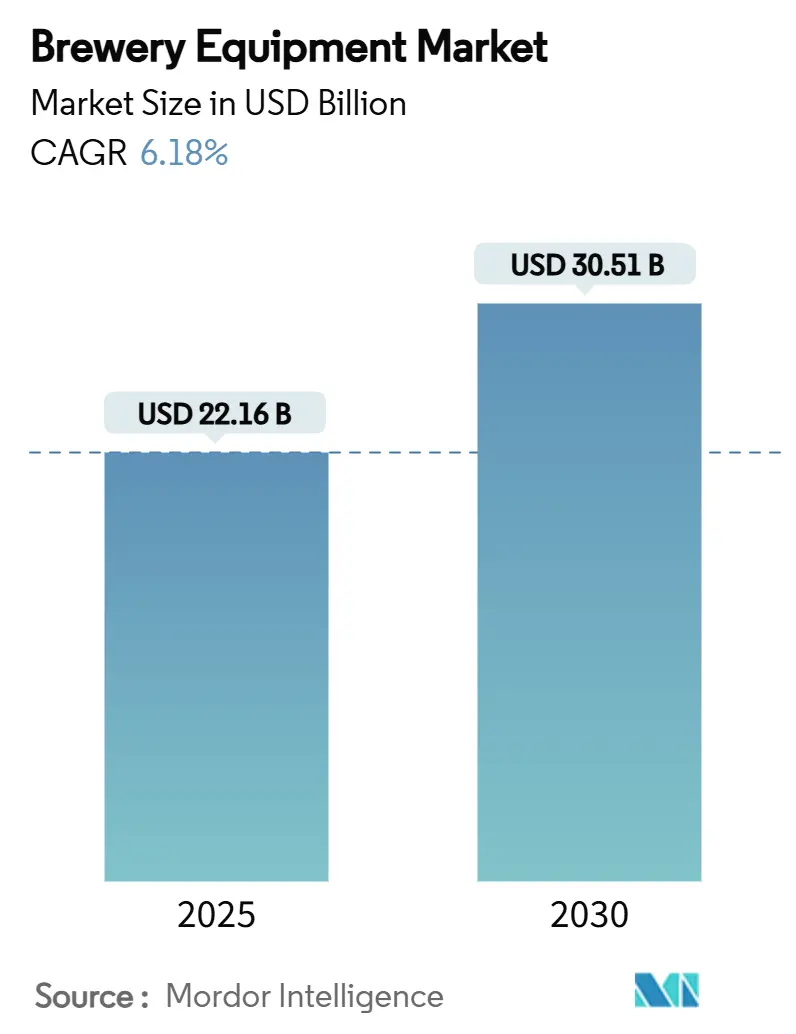

| Market Size (2025) | USD 22.16 Billion |

| Market Size (2030) | USD 30.51 Billion |

| Growth Rate (2025 - 2030) | 6.18% CAGR |

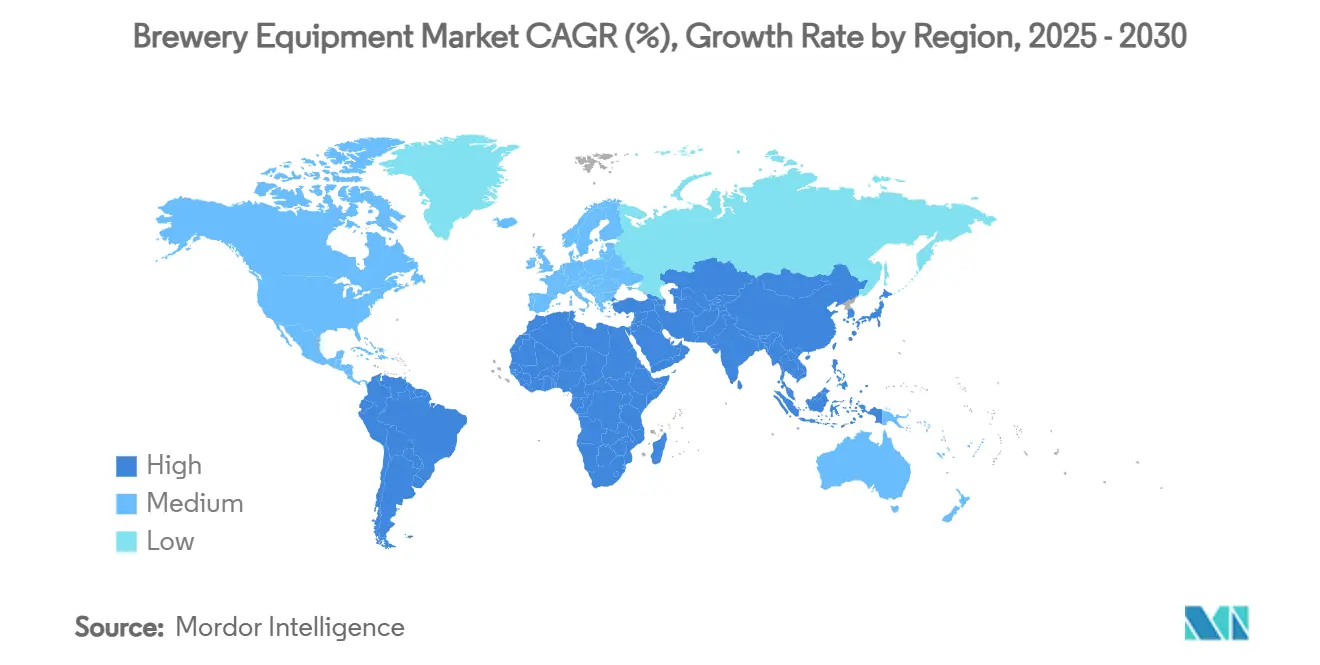

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

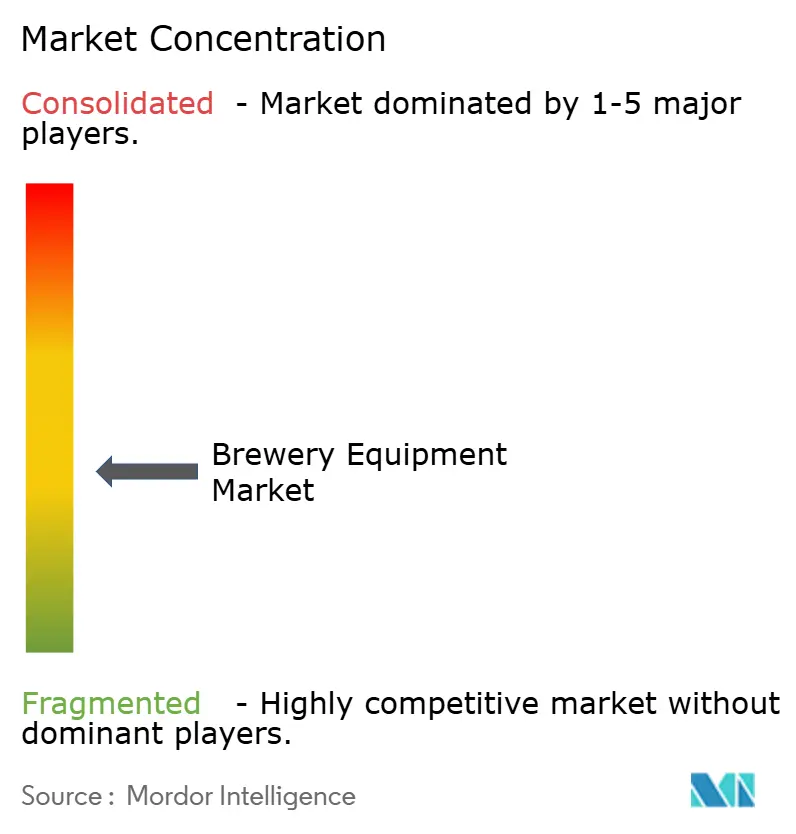

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brewery Equipment Market Analysis by Mordor Intelligence

The brewery equipment market size is valued at USD 22.61 billion in 2025 and is projected to reach USD 30.51 billion by 2030, registering a CAGR of 6.18% during the forecast period. Technological advancements, such as automation, energy-efficient systems, and IoT-enabled monitoring, are transforming brewery operations. These innovations allow manufacturers to enhance productivity, reduce downtime, and maintain product consistency. Europe holds a dominant market share, but the Asia-Pacific region is experiencing swift growth, driven by increasing disposable incomes and evolving beer preferences in countries like India and China. The trend of premiumization and a rising fondness for artisanal beer are fueling both equipment upgrades and new installations. Additionally, as breweries pivot towards sustainable production, they're adopting water-saving and low-emission technologies. The integration of predictive maintenance systems is further helping breweries optimize operations by reducing unexpected equipment failures. Moreover, the adoption of advanced filtration technologies is ensuring higher-quality beer production while minimizing waste. The growing focus on digitalization is also enabling breweries to leverage data analytics for demand forecasting and inventory management.

Key Report Takeaways

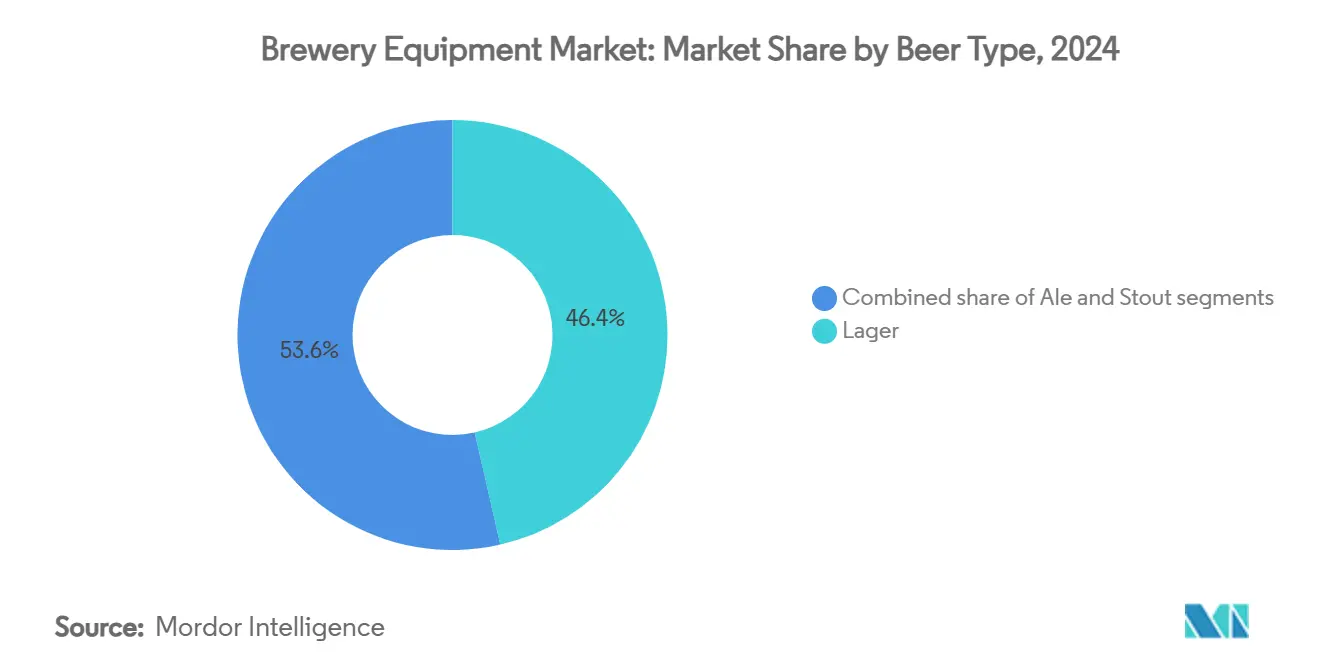

- By beer type, lager led with a 46.43% share in 2024, whereas ale is poised for an 8.58% CAGR over the forecast horizon.

- By equipment, fermentation equipment accounted for 37.65% of 2024 revenue, while packaging equipment is projected to record a 7.52% CAGR through 2030.

- By brewery type, microbreweries held 66.75% of the 2024 share; craft breweries exhibit the highest growth at 9.16% CAGR to 2030.

- By mode of operation, fully-automatic plants captured 79.52% of 2024 installations; the segment is expected to expand at a 6.78% CAGR by 2030.

- By geography, Europe retained 39.54% of 2024 revenue; Asia-Pacific is forecast to advance at an 8.47% CAGR through 2030.

Global Brewery Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased beer tourism | +1.2% | Europe, North America | Medium term (2-4 years) |

| Growing number of microbreweries | +0.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Higher demand for premium and craft beer | +0.6% | Developed markets | Long term (≥ 4 years) |

| Technological advancements in brewing equipment | +0.9% | Europe, North America | Medium term (2-4 years) |

| Rising need for automation and efficiency | +0.7% | High-labor-cost regions | Short term (≤ 2 years) |

| Stricter regulations on food safety and quality standards | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Number of Microbreweries

As the number of microbreweries surges, the brewery equipment market is evolving, increasingly favoring compact systems tailored for small-batch and diverse production. In 2024, the U.S. boasted 9,796 craft breweries, with 2,029 classified as microbreweries. The breakdown included 3,552 brewpubs, 3,936 taproom breweries, and 279 regional craft breweries, underscoring the dominance of small-scale producers [1]Source: Brewers Association, “National Beer Statistics 2024,” brewersassociation.org. This proliferation has heightened the demand for modular, space-efficient brewing systems, enabling swift transitions in both production volumes and beer styles. Similarly, China's craft beer scene is on the rise, with over 13,000 active enterprises as of 2023, signaling a burgeoning need for versatile equipment in these developing markets. Equipment manufacturers are taking note, introducing innovations like Krones’ Craftmate can filler, designed for smaller brewers seeking professional-grade automation without the expansive space or hefty budget. Given that microbreweries typically operate batch sizes between 100 to 15,000 liters, the diverse needs of this segment are propelling innovations in equipment and installations, driving the market's overall growth.

Increased Beer Tourism

Beer tourism is fueling the growth of the brewery equipment market, prompting onsite brewing facilities to expand and modernize in a bid to elevate visitor experiences. In 2023, craft breweries in states like Colorado and Oregon saw record footfall. Many operators responded by investing in visible brewing lines, pilot systems, and taproom-integrated fermenters, all aimed at offering immersive tours. The Brewers Association’s May 2025 Export Development Program report underscores this trend, noting international trade events attracted nearly 44,000 visitors, a 5% uptick from 2024 [2]Source: Brewers Association, “Export Development Program News – May 2025,” brewersassociation.org. The events featured 600 exhibitors, 130 buyers from 47 countries, and attendees hailing from 82 nations. This tourism boom is not only driving demand for core brewing systems but also for smaller, aesthetically designed equipment tailored for public-facing operations. In Europe, cities like Brussels and Prague are upgrading their brewery infrastructures in response to heightened tour bookings. Meanwhile, in India, emerging beer tourism hubs like Bengaluru are investing in visually appealing, space-efficient brewing systems for their brewpubs. Equipment manufacturers are rising to the occasion, crafting modular systems that seamlessly blend automation with design, catering to production needs while amplifying visitor engagement.

Higher Demand for Premium and Craft Beer

As consumers increasingly prioritize flavor diversity and quality, breweries are turning to advanced systems that enable precise control over ingredients, fermentation, and batch customization. There is a shift toward unique flavor profiles that is driving producers to invest in equipment that supports a diverse range of beer styles while ensuring consistency and efficiency. In India, urban brewpubs in cities like Bengaluru and Hyderabad are experiencing a premiumization trend. Operators are upgrading to modular brewhouses and automated filling lines, underscoring a demand for high-end brewing systems. Meanwhile, China's craft beer segment is witnessing rapid expansion, with local players investing in smart brewing equipment to align with shifting consumer tastes. Equipment manufacturers are stepping up, offering systems that emphasize batch flexibility, digital monitoring, and energy efficiency, appealing to producers aiming for premium differentiation. Furthermore, as premium beers typically have shorter shelf lives and demand meticulous handling, there's a rising need for cold-chain optimized storage and advanced kegging systems. The surging popularity of limited-edition and seasonal craft beers is driving breweries to pursue scalable, small-batch systems that facilitate swift formulation changes without disrupting overall operations.

Rising Need for Automation and Efficiency

Breweries are increasingly turning to automation to enhance operational efficiency, streamline production, cut labor costs, and ensure product consistency. In 2023, several mid-sized breweries across the U.S. adopted fully automated brewhouse systems. These systems come equipped with real-time monitoring, CIP (clean-in-place) automation, and predictive maintenance features, helping breweries tackle labor shortages and uphold quality standards. For instance, craft brewers in the Pacific Northwest noted a boost in throughput after they installed semi-automated fermentation controls, which curtailed batch errors and reduced downtime. In India, prominent urban brewpub chains are now using SCADA-based brewing systems. These systems not only optimize daily multi-batch production but also help in conserving energy and water. Meanwhile, breweries in China are harnessing AI-integrated sensors to oversee fermentation stages and automate pivotal decisions, leading to quicker turnaround times. In response, equipment suppliers are rolling out plug-and-play automation modules. These include robotic packaging lines and digital brewing dashboards, specifically designed for small to mid-scale producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Investment Costs | −0.8% | Emerging markets | Short term (≤ 2 years) |

| Strict Regulatory Requirements for Alcohol Production | −0.6% | Global | Long term (≥ 4 years) |

| Supply Chain Disruptions for Raw Materials | −0.4% | Steel/Aluminum regions | Medium term (2-4 years) |

| Complexity of Brewing Diverse Beer Styles | −0.3% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment Costs

Capital intensity poses a significant challenge for the brewery equipment market, particularly for smaller operators and newcomers in emerging markets. In 2024, Tilray's acquisition of four craft breweries from Molson Coors underscored the mounting pressures on independent brewers. Many now face the dilemma of scaling up or exiting the market, primarily due to soaring costs associated with equipment and operational upgrades. Adding to the strain, tariffs on steel and aluminum imports set at 25% and heightened in 2025, have led to a 15–20% surge in brewing equipment prices. This spike has tightened capital budgets for smaller players, who often lack the clout to negotiate bulk discounts. These financial strains aren't limited to equipment purchases. They also encompass installation, commissioning, and specialized maintenance, all of which demand skilled technicians and proprietary parts. Such requirements render entry or expansion a daunting financial hurdle for many startups and microbreweries. Furthermore, disparities in access to financing amplify these challenges. In many emerging markets, the absence of tailored brewery equipment loans or subsidies stalls infrastructure development and curtails equipment adoption.

Supply Chain Disruptions for Raw Materials

Volatility in raw material pricing and availability poses a significant challenge to the brewery equipment market, disrupting cost structures and delaying capital investments. In 2024, while global hop production saw an 11.5% uptick, total hop acreage shrank by 3.3% to 60,641 hectares. This discrepancy injects uncertainty into the brewing supply chain and complicates capacity planning for equipment manufacturers. Such a mismatch underscores the fragility of ingredient supply chains, especially in regions reliant on consistent hop quality and volume. At the same time, breweries are increasingly wary of chemical contaminants, ranging from biogenic amines and heavy metals to mycotoxins and pesticide residues. As a result, many are adopting HACCP-based quality control programs. These programs necessitate investments in specialized monitoring and testing equipment [3]Source: Yanjun Zhang, “Chemical Risk Management in Brewing: Toxins and HACCP Implementation,” mdpi.com. This not only heightens capital intensity but also limits purchasing options, particularly for smaller brewers in cost-sensitive markets. Collectively, these challenges hinder modernization efforts, extend equipment turnover cycles, and foster risk aversion among brewers, ultimately stunting market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Beer Type: Lager Dominance Drives Equipment Standardization

In 2024, lager beer secured a dominant 46.43% share of the global market, underscoring its widespread appeal and the efficiency of its production methods. This stronghold is primarily attributed to standardized brewing techniques. These methods optimize equipment use, especially by maintaining consistent fermentation temperatures and adhering to predictable processing timelines, which in turn boosts production output. Major brewers leverage economies of scale, utilizing uniform, high-capacity brewhouses and fermentation tanks specifically designed for lager production. This strategy not only solidifies their dominance in the beer market but also reinforces their leadership in the global beer equipment sector.

On the other hand, ale is on a rapid ascent, boasting an impressive 8.58% CAGR projected through 2030. This surge is driven by a growing consumer appetite for diverse flavors and the innovative spirit of craft breweries. Producing ale often necessitates higher fermentation temperatures and a variety of yeast strains. As a result, breweries are channeling investments into adaptable, small-batch fermenters and advanced control systems, enabling them to pivot with ease to frequent recipe modifications. While stout production remains a niche, it's witnessing growth, owing in part to the rising trend of nitro beers. This surge has led equipment manufacturers to craft specialized systems tailored for handling roasted malts and infusing nitrogen.

By Equipment Type: Fermentation Technology Leads Market Evolution

In 2024, fermentation equipment captures a dominant 37.65% share of the market, highlighting its pivotal role in beer production and the ongoing adoption of sophisticated control technologies. These modern systems empower brewers to monitor vital parameters like oxygen levels, pH, gravity, pressure, and temperature in real time. Such capabilities not only enhance tank utilization and consistency but also minimize batch variability. These improvements are crucial for both craft and large-scale producers focused on boosting operational efficiency and ensuring top-notch product quality.

Packaging equipment is the standout performer, boasting a robust 7.52% CAGR through 2030. This surge is driven by breweries' growing embrace of automated solutions and a pronounced shift towards canned formats. To cater to the escalating consumer appetite for convenience and variety, high-speed, flexible fillers and automated changeover features are swiftly becoming the norm. Concurrently, mashing equipment is evolving, now supporting extract efficiency and high-gravity brewing. This evolution empowers brewers to amplify output without sacrificing quality. The "Others" category encompasses vital systems like automated cleaning units, quality control instruments, and process automation tools.

By Brewery Type: Microbrewery Segment Shapes Equipment Innovation

In 2024, microbreweries command a dominant 66.75% share of the brewery market, buoyed by a global surge in small-scale brewing ventures. This dominance has spurred a heightened demand for compact and adaptable brewing systems, specifically designed for batch sizes ranging from 100 to 15,000 liters. In response, equipment manufacturers are rolling out solutions that cater to these smaller spaces and reduced volume outputs. Moreover, regulatory shifts, like Thailand's recent decision to lift production caps, are spurring investments in microbreweries, especially in the burgeoning markets of Southeast Asia.

Craft breweries are on a rapid ascent, boasting a 9.16% CAGR projected through 2030. As these operators ramp up capacity and weave in automated systems, they're ensuring quality and efficiency even at elevated volumes. Once seen as niche players, these breweries are now carving out competitive positions in regional markets, skillfully marrying innovation with scale. Equipment suppliers, recognizing this evolution, are providing modular and scalable brewing systems. These systems empower breweries to expand operations while preserving flexibility and distinct product differentiation. This evolution highlights a significant industry trend: as microbreweries mature, they are transitioning into craft-scale operations, all the while maintaining their nimbleness and unique market presence.

By Mode of Operation: Automation Dominance Reflects Efficiency Imperatives

In 2024, fully-automatic systems command a dominant 79.52% share of the operational mode market, and they're not just leading; they're growing at a brisk 6.78% CAGR, projected through 2030. This surge underscores a pronounced industry pivot towards automation, aiming to bolster efficiency, curtail labor reliance, and uphold product quality. By leveraging these systems, breweries can significantly reduce manual interventions, all while exercising stringent control over critical brewing parameters. This makes automation indispensable for large-scale, high-volume operations. On the other hand, semi-automatic systems still hold sway in smaller breweries and specialized niches, where there's a premium on flexibility and direct oversight.

Across the board, from small to mid-sized and even regional craft breweries, the march towards full automation is unmistakable. These establishments are not just observing the trend; they're actively upgrading their equipment to stay in the game. They can swiftly identify and rectify process anomalies, leading to significant reductions in resource wastage and preempting quality pitfalls like contamination or oxidation. These advancements aren't just isolated; they're part of the larger Industry 4.0 movement. Breweries are now embracing Manufacturing Execution Systems (MES) and AI-driven tools, seamlessly guiding production from the initial grain intake all the way to the final packaging.

Geography Analysis

In 2024, Europe dominates the brewery equipment market, capturing 39.54% of the market share. This leadership is anchored in Europe's rich brewing traditions, a dense network of specialized breweries, and a well-established infrastructure. Germany stands out, showcasing established production practices, stringent quality standards, and a demand for advanced equipment catering to both premium and craft beer segments. Moreover, with rising regulatory pressures and a consumer push for sustainability, breweries are channeling investments into technologies that curtail water and energy use, solidifying Europe's stance as a brewing innovation leader.

Asia-Pacific emerges as the region with the most rapid growth, boasting an 8.47% CAGR projected through 2030. This surge is attributed to the rising allure of craft beer, bolstered disposable incomes, and favorable policy shifts in burgeoning economies. Take China, for example: the nation has seen a notable uptick in craft beer production, leading to significant investments in contemporary brewing systems to align with heightened consumer expectations. Meanwhile, in Southeast Asia, countries like Thailand are enacting regulatory reforms, now allowing microbrewery expansions, which in turn is spurring demand for modern brewing equipment.

North America, South America, and the Middle East and Africa are witnessing moderate to steady growth trajectories, influenced by regional market dynamics and strategic pivots. North American breweries, especially mid-sized and craft ones, are leaning into consolidation and automation upgrades, a response to mounting competitive pressures and inflationary costs. On the other hand, while South America and the Middle East grapple with challenges like regulatory hurdles and historically lower beer consumption rates, they are seeing a silver lining: urbanization and a surge in tourism are paving the way for burgeoning equipment opportunities.

Competitive Landscape

In the brewery equipment market, moderate fragmentation shapes the competitive landscape. Key players like Krones AG, GEA Group, and Alfa Laval leverage expansive product lines and a global service infrastructure to command significant market shares. These industry leaders adopt marketing strategies that emphasize value-added services, brand trust, and customization. For instance, Krones positions itself as a comprehensive solution provider, underscoring its end-to-end brewing solutions and robust after-sales support, catering to both large-scale and craft brewers.

Technological innovation stands as the cornerstone of competitive differentiation. Leading firms are embedding automation, AI, and IoT capabilities into their brewing systems. A prime example is Precision Fermentation’s BrewMonitor platform, which facilitates real-time fermentation tracking, aiding breweries in minimizing batch variability and enhancing consistency. On a similar note, Alfa Laval emphasizes a modular, hygienic design coupled with smart monitoring, boosting operational visibility and curtailing downtime. Such innovations not only optimize production but also cater to brewers' demands for scalability and quality assurance, underscoring the significance of tech-driven equipment in procurement decisions.

Strategic maneuvers like mergers, acquisitions, and regional expansions further sculpt market positioning. Krones bolstered its foothold in North America by acquiring W.M. Sprinkman, enhancing its reach to small and mid-sized brewery clientele. Meanwhile, Bühler Group's acquisition of Esau & Hueber signifies a calculated bet on fermentation technology, aiming to bolster synergies in brewing and protein processing. In burgeoning markets, equipment providers are tapping into growth opportunities via localized manufacturing and training collaborations, ensuring swift delivery and on-site support.

Brewery Equipment Industry Leaders

Krones AG

GEA Group AG

Alfa Laval AB

Paul Mueller Company

The Middleby Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Krones, the world’s leading manufacturer of filling and packaging technology, has acquired W.M. Sprinkman Corporation. Founded in 1929, Sprinkman provides engineered food and beverage processing equipment, with a specialization in the dairy and brewing industries.

- June 2025: Diversified Metal Engineering LP acquired Accent Stainless Steel Manufacturing Group to secure turnkey capability for craft breweries. Accent Stainless Steel Manufacturing Group designs and manufactures large- and small-scale turn-key breweries, food processing equipment, soya milk plants, and equipment for the forestry and wastewater treatment industry.

- January 2024: Bwanaz launched its iGulu F1 Automated Smart Home Brewer. This was asserted to be an all-in-one system that uses AI and "BrewOS" technology to automate the brewing process, from fermentation control to pressure regulation. It simplifies homebrewing for beginners and allows for customizable craft beers, ciders, and more with one-touch operation.

- January 2024: Mr. Beer launched Pro Brew Kit 2.0, an update to the brand's beginner-friendly homebrewing system, maintaining the 2-gallon capacity while possibly featuring enhanced materials and a focus on updated ingredient mixes.

Global Brewery Equipment Market Report Scope

| Ale |

| Lager |

| Stout |

| Mashing Equipments |

| Fermentation Equipment |

| Packahing Equipment |

| Others |

| Mirco Brewery |

| Craft Brewery |

| Automatic |

| Semi Automatic |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Beer Type | Ale | |

| Lager | ||

| Stout | ||

| By Equipment Type | Mashing Equipments | |

| Fermentation Equipment | ||

| Packahing Equipment | ||

| Others | ||

| By Brewery Type | Mirco Brewery | |

| Craft Brewery | ||

| Mode of Operation | Automatic | |

| Semi Automatic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the beer brewing equipment market?

The market is valued at USD 22.61 billion in 2025 and is projected to reach USD 30.51 billion by 2030.

Which equipment segment is growing the fastest?

Packaging equipment records the highest 7.52% CAGR during 2025-2030 as breweries shift toward high-speed canning and flexible bottling solutions.

Why are fully-automatic systems preferred?

They captured 79.52% of 2024 installations because automated controls reduce labor costs, improve consistency, and streamline compliance with stringent food-safety standards.

Which region offers the strongest growth prospects?

Asia-Pacific posts an 8.47% CAGR to 2030, driven by rapid craft-beer adoption in China, India, and Southeast Asia.

Page last updated on: