Sparkling Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

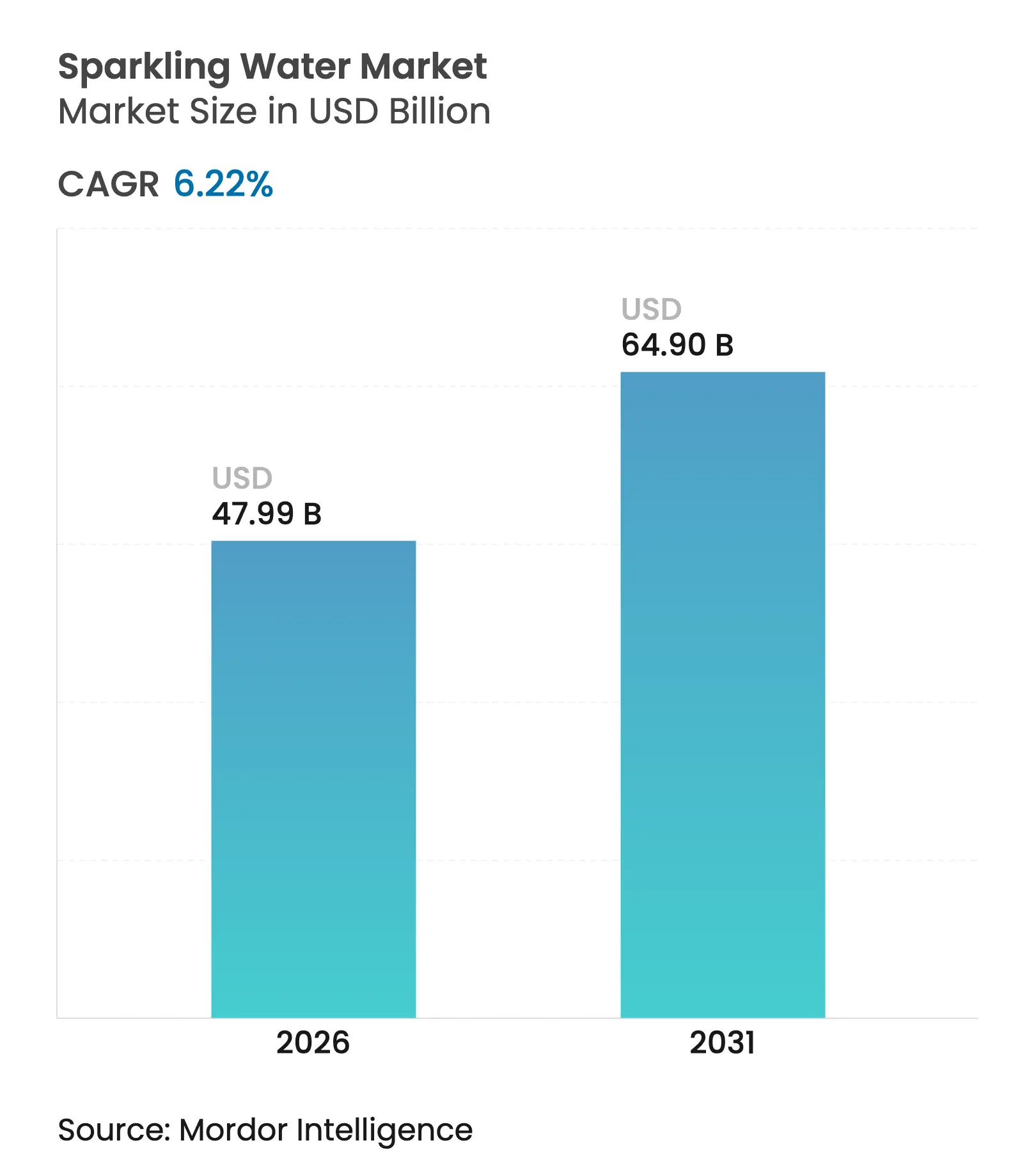

| Market Size (2026) | USD 47.99 Billion |

| Market Size (2031) | USD 64.9 Billion |

| Growth Rate (2026 - 2031) | 6.22 % CAGR |

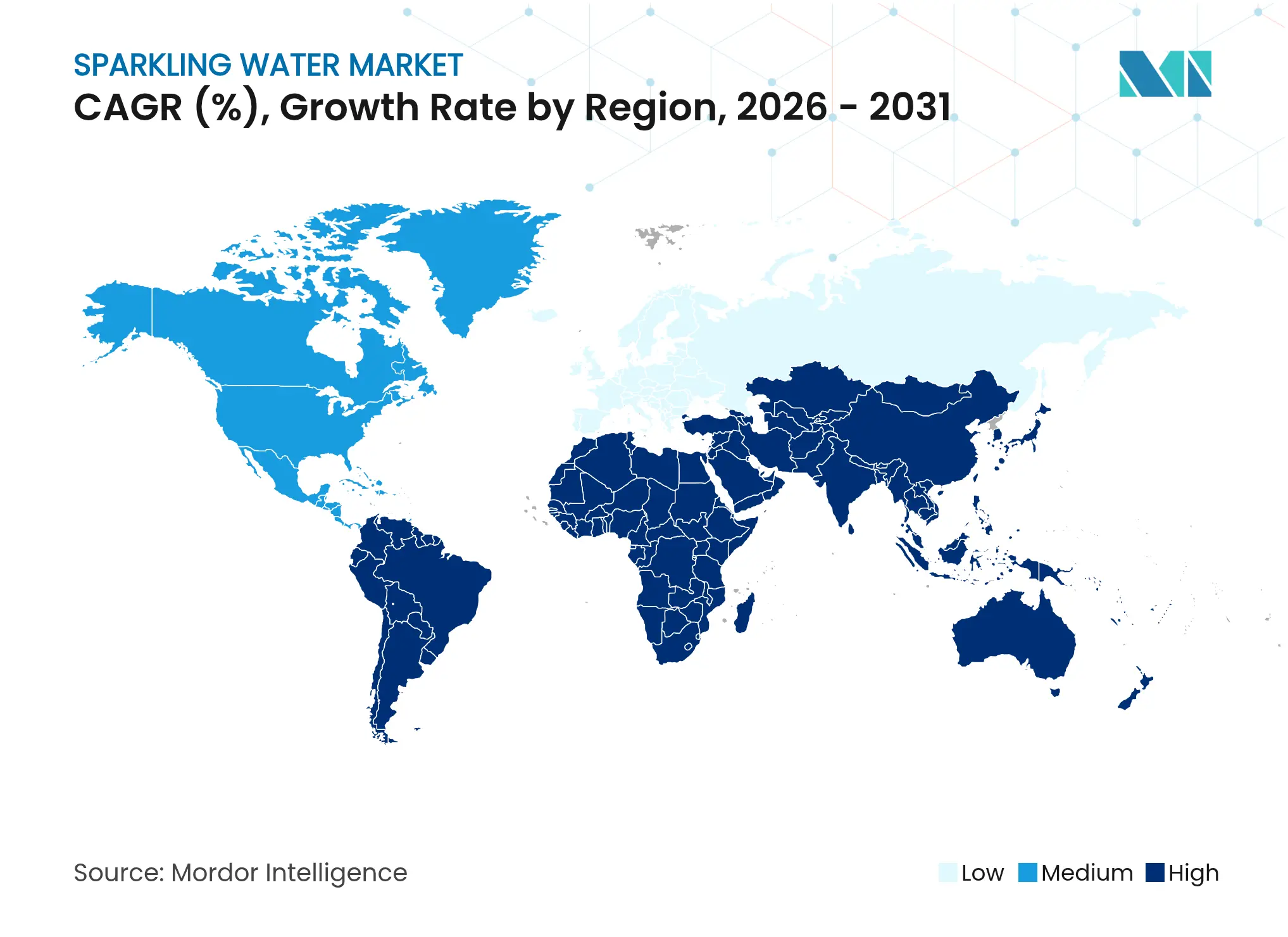

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Sparkling Water Market Analysis by Mordor Intelligence

Sparkling water market size in 2026 is estimated at USD 47.99 billion, growing from 2025 value of USD 45.18 billion with 2031 projections showing USD 64.9 billion, growing at 6.22% CAGR over 2026-2031. Accelerating health awareness, shifting taste preferences, and packaging regulations continue to pull consumers away from sugar-laden sodas toward calorie-free carbonation. Functional innovation, such as prebiotic and caffeinated lines, amplifies differentiation while premium glass-bottled mineral waters broaden trading-up occasions. Aluminum cans are gaining acceptance as nations tighten circular-economy rules, and on-premise dining recovery is re-routing volume to restaurants that can serve profit-rich sparkling pours. However, price sensitivity in emerging markets restricts penetration, while private-label options in mature markets address affordability challenges. Increasing competition from flavored waters, sports drinks, and enhanced still beverages is driving innovation in flavors, functionality, and sustainability within the sparkling water market.

Key Report Takeaways

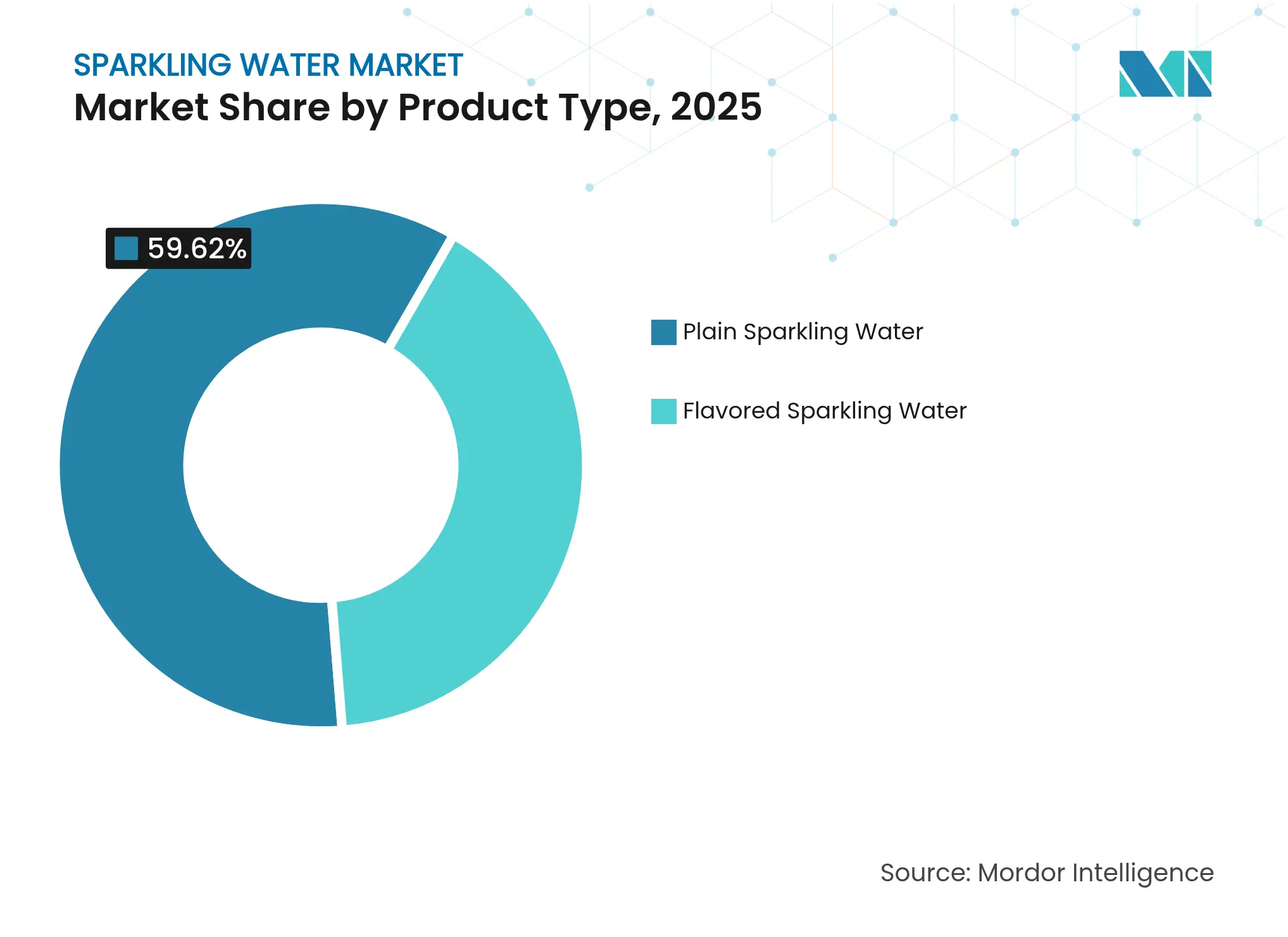

- By product type, plain commanded 59.62% sparkling water market share in 2025; flavored variants are forecast to advance at a 7.45% CAGR to 2031.

- By packaging type, rPET and PET bottles held 56.05% of the sparkling water market size in 2025, while aluminum cans are projected to post a 7.21% CAGR through 2031.

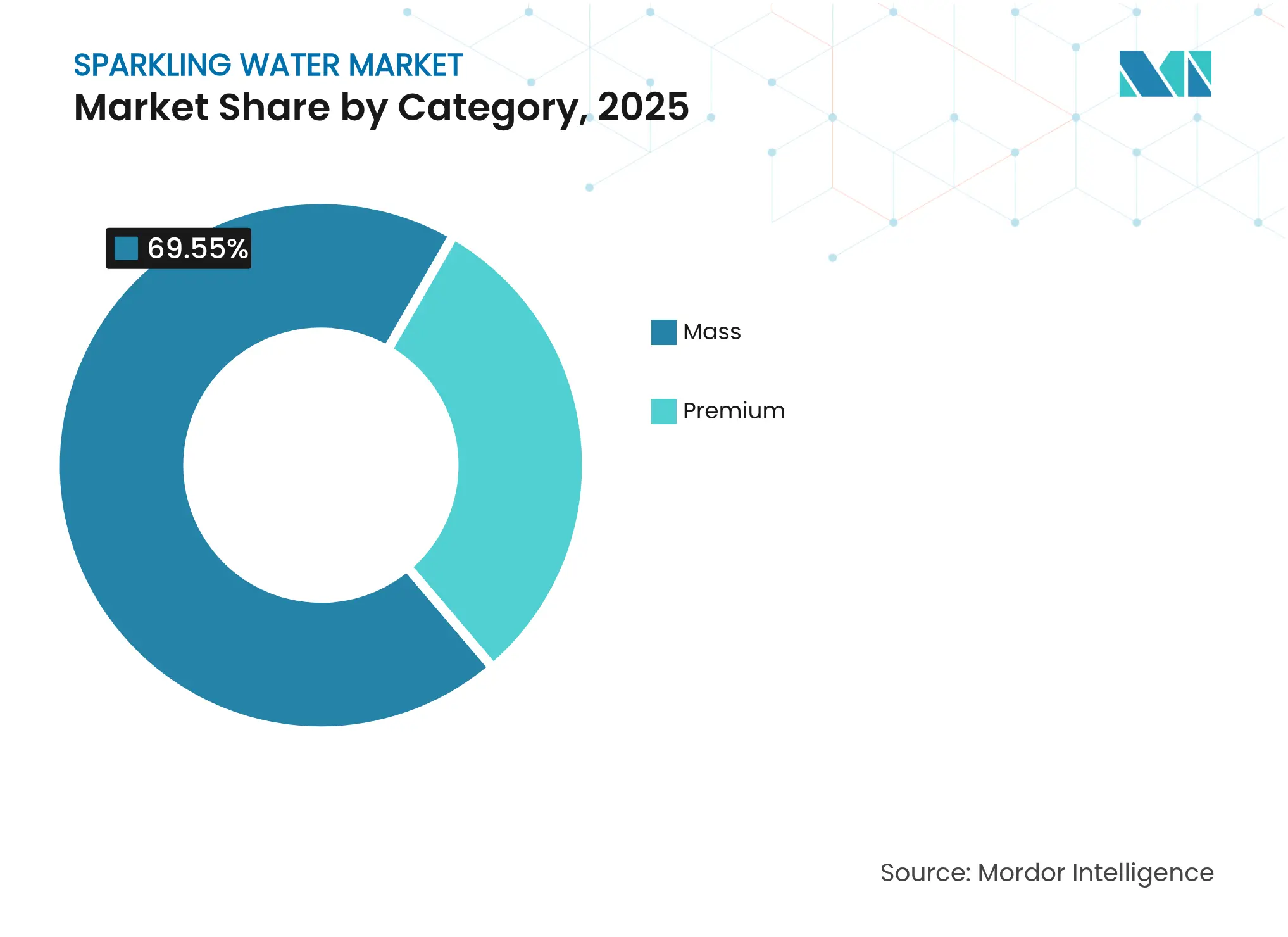

- By category, the mass segment accounted for 69.55% revenue in 2025, whereas premium offerings are on track for a 7.79% CAGR up to 2031.

- By distribution channel, off-trade outlets captured 63.88% of 2025 sales, yet on-trade venues are poised for a 7.6% CAGR as dining-out rebounds.

- By geography, North America accounted for 27.95% revenue share in 2025, while Asia-Pacific is projected to post the fastest growth at a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sparkling Water Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising health consciousness promotes sparkling water as low-calorie alternative to sugary sodas Rising health consciousness promotes sparkling water as low-calorie alternative to sugary sodas | +1.2% | Global, with strongest adoption in North America and Western Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with strongest adoption in North America and Western Europe | Impact Timeline:Short term (≤ 2 years) |

Innovation in flavors attracts diverse consumer tastes Innovation in flavors attracts diverse consumer tastes | +0.9% | Global, particularly Asia-Pacific and North America | Medium term (2-4 years) | |||

Growing preference for sustainable packaging like recyclable cans drives eco-focused sales Growing preference for sustainable packaging like recyclable cans drives eco-focused sales | +0.8% | North America and European Union, with regulatory spill-over to Asia-Pacific | Medium term (2-4 years) | |||

Expansion of functional variants such as caffeinated types appeals to energy-seeking users Expansion of functional variants such as caffeinated types appeals to energy-seeking users | +0.7% | North America and Asia-Pacific core markets | Short term (≤ 2 years) | |||

Premiumization through mineral-sourced products elevates market positioning Premiumization through mineral-sourced products elevates market positioning | +0.6% | Europe and North America, emerging in urban Asia-Pacific | Long term (≥ 4 years) | |||

Wellness trends emphasize digestion and hydration benefits of carbonated water Wellness trends emphasize digestion and hydration benefits of carbonated water | +0.5% | Global, with early traction in wellness-focused demographics | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising health consciousness promotes sparkling water as a low-calorie alternative to sugary sodas

Health-conscious consumers are increasingly favoring sparkling water as a low-calorie alternative to sugary sodas. In the United States, declining carbonated soft drink consumption and rising sparkling water volumes highlight a clear shift toward zero-calorie hydration. This trend is particularly prominent among Millennials and Gen Z, who together represented over 42% of the United States population in 2024 (Millennials at 21.81% and Gen Z at 20.81%, according to the United States Census Bureau) [1]Source: United States Census Bureau, "Population and Housing Unit Estimates", census.gov . These demographics are reshaping beverage preferences, viewing sparkling water as a functional option that combines carbonation’s sensory appeal with the absence of added sugars or artificial sweeteners. Health-behavior surveys from 2024 reveal stronger label scrutiny among younger consumers, further driving this shift. Convenience stores have supported this growth, with single-serve formats becoming popular impulse purchases for urban consumers amid rising foot traffic in 2023–24. Product launches, such as Waiākea’s volcanic-sourced sparkling water in 2023, have capitalized on wellness narratives emphasizing natural minerals and purity. Moreover, FDA regulations under 21 CFR 165.110, which distinguish “sparkling natural mineral water” from “carbonated drinking water,” allow brands to highlight origin and mineral content, appealing to health-focused audiences. These factors collectively position sparkling water as a preferred hydration choice, meeting modern consumer demands for taste, functionality, and metabolic simplicity.

Innovation in flavors attracts diverse consumer tastes

Flavors are playing a critical role in expanding the appeal of sparkling water, as brands diversify beyond traditional citrus options to include botanical infusions such as elderflower, hibiscus, and cucumber-mint, alongside exotic fruits like yuzu, lychee, and passion fruit. These innovations cater to evolving consumer preferences for novelty and wellness, driving category growth. Companies like Spindrift, which uses real squeezed fruit instead of essences, are capitalizing on this trend by attracting clean-label shoppers willing to pay a premium for authenticity. Established players are also intensifying their efforts, with Polar Beverages set to launch its Seltzer’ade line in March 2024, featuring six lemonade-infused variants aimed at younger consumers seeking fresher flavor profiles. Additionally, garden-inspired flavor combinations, such as those introduced by Aura Bora, highlight the rising demand for herbal and floral profiles that resonate with experience-driven buyers. These shifts align with the broader movement toward natural ingredients, as flavor houses report increased interest in plant-derived extracts and cold-pressed fruit components for sparkling water applications. Seasonal limited releases, including options like summer mango-cayenne or winter cranberry-clove, further sustain consumer engagement and exploration. Collectively, these strategies position sparkling water as a customizable, sensorially rich alternative to sugary beverages, appealing to diverse demographics across global markets.

Growing preference for sustainable packaging like recyclable cans drives eco-focused sales

The increasing focus on sustainable packaging is driving the adoption of aluminum cans, projected to grow at an annual rate of 7.34% through 2030. This growth is underpinned by regulatory measures and evolving consumer preferences for recyclable materials and lower carbon footprints. At COP28 in December 2023, 40 nations committed to achieving 80% aluminum can recycling by 2030 and near-100% by 2050, as per the International Aluminium Institute, aligning policy frameworks with the shift of sparkling water brands toward can-based packaging [2]Source: International Aluminium Institute, "Global Aluminium Can Recycling Reaches 75%, Marking Major Step Toward Circular Economy", international-aluminium.org . Rising consumer scrutiny of single-use plastics further amplifies the demand for packaging solutions that emphasize circularity and reduced environmental impact. Between 2024 and 2025, beverage companies expanded their use of lightweight aluminum designs and increased recycled content, reflecting broader sustainability trends across global FMCG portfolios. For example, Waterloo announced in 2024 its integration of greater recycled aluminum across all sparkling water cans, positioning the format as both environmentally responsible and adaptable to premium branding. Innovations such as water-based inks, low-carbon aluminum sourcing, and localized canning logistics enhance the environmental profile of aluminum cans while meeting consumer expectations for transparency in packaging claims. These developments reinforce aluminum’s role as the preferred packaging choice for sparkling water, combining sustainability, convenience, and alignment with the global transition to circular-economy hydration solutions.

Expansion of functional variants, such as caffeinated types, appeals to energy-seeking users

Caffeinated sparkling water variants are gaining traction as a distinct sub-segment, appealing to energy-seeking consumers who prefer a low-sugar, lighter alternative to traditional energy drinks or hot coffee. This format combines carbonation with functional benefits, targeting busy adults who regularly consume caffeine. Regulatory and health considerations significantly influence product positioning. The FDA’s guidance, which identifies 400 mg of caffeine per day as a safe intake level for most adults, serves as a benchmark for brands in formulating caffeine levels [3]Source: Food and Drug Administration (FDA), "Spilling the Beans: How Much Caffeine is Too Much?", fda.gov. Public health messaging from agencies like the CDC, particularly regarding energy drink consumption among adolescents, has driven brands to emphasize "adult-oriented" communication and moderate dosing. Established and emerging players are innovating with caffeinated water products, such as Liquid Death's caffeinated extensions and newer launches marketed as "sparkling energy" beverages. Ingredient strategies often include naturally sourced caffeine, such as coffee-bean extracts, paired with B-vitamins or adaptogens to enhance functionality while maintaining clean-label simplicity. As consumers mix caffeine sources throughout the day, clear on-pack dosing and educational efforts aligned with FDA and NIH guidelines are critical for building trust and promoting responsible consumption. Caffeinated sparkling water now represents a distinct functional category, meeting energy needs, aligning with health preferences, leveraging natural ingredient claims, and requiring regulation-conscious marketing to ensure consumer trust.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Premium price versus still water Premium price versus still water | -0.8% | Global, particularly price-sensitive emerging markets in Asia-Pacific, Latin America, and Middle East and Africa | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, particularly price-sensitive emerging markets in Asia-Pacific, Latin America, and Middle East and Africa | Impact Timeline:Short term (≤ 2 years) |

Intense competition from flavored waters and sports drinks fragments market share Intense competition from flavored waters and sports drinks fragments market share | -0.6% | Global, with heightened intensity in North America and Europe | Medium term (2-4 years) | |||

Plastic-waste and carbon-footprint scrutiny Plastic-waste and carbon-footprint scrutiny | -0.5% | Europe and North America, with regulatory spill-over to Asia-Pacific | Medium term (2-4 years) | |||

Consumer skepticism about carbonation's health impacts limits adoption Consumer skepticism about carbonation's health impacts limits adoption | -0.4% | Global, concentrated in health-conscious demographics | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Premium price versus still water

Sparkling water's premium pricing, often 2 to 3 times higher than still bottled water, creates a significant affordability challenge in price-sensitive markets, limiting its reach among lower-income consumers despite growing health-conscious demand. The elevated cost stems from production factors such as carbonation technology, pressurized packaging, and cold-chain logistics, which brands struggle to offset through economies of scale. In emerging regions like Asia-Pacific, Latin America, and Middle East and Africa, where per-capita bottled water consumption remains below that of developed markets, this price disparity hinders trial and repeat purchases, slowing category growth. In mature markets such as the United States, private-label sparkling waters from retailers like Costco and Kroger have gained traction since 2024 by offering lower prices, appealing to cost-sensitive consumers, and compressing national brand margins. Inflationary pressures on raw materials, including aluminum, glass, and rPET, which peaked in 2024, have further intensified pricing challenges, forcing brands to balance cost absorption with potential volume loss. In 2025, several United States beverage producers adjusted can sizes and pack formats to mitigate material cost increases while maintaining accessibility. Similarly, premium regional brands in Europe and the Middle East introduced smaller format SKUs or multipacks to enhance affordability without compromising the perceived luxury experience, shaping growth trajectories and consumer adoption patterns globally.

Intense competition from flavored waters and sports drinks fragments market share

Competition within the sparkling water segment is intensifying due to the expansion of functional hydration products, including enhanced waters, electrolyte drinks, coconut water, and sports beverages, all catering to overlapping consumer demands for hydration, refreshment, and wellness. Sports drinks such as Gatorade and Powerade continue to command strong consumer loyalty, while coconut water brands leverage natural electrolytes and unique sourcing to distinguish themselves. Enhanced still waters infused with vitamins, minerals, or botanical extracts attract consumers seeking non-carbonated options for reasons such as digestive comfort or taste preferences, further fragmenting the market. This competitive landscape challenges marketing efficiency and shelf space allocation, driving sparkling water brands to focus on flavor innovation, functional ingredients, and sustainability to differentiate their offerings. Product launches in 2024–2025 across North America and Europe have underscored this trend, with brands introducing adaptogen-infused or lightly caffeinated sparkling waters to appeal to wellness-conscious consumers. The overlap with sports and functional beverages necessitates innovative packaging and storytelling, emphasizing carbonation, natural ingredient sourcing, and eco-friendly materials to enhance perceived value. Saturated retail channels further complicate efforts to achieve sufficient SKU velocity for permanent shelf placement, pressuring brands to balance innovation, marketing expenditure, and distribution strategies to remain competitive in this dynamic market.

Segment Analysis

By Product Type: Flavored Variants Outpace Plain Despite Smaller Base

In 2025, plain sparkling water held approximately 59.62% of the market share. However, flavored sparkling water is projected to grow at an annual rate of 7.45% from 2026 to 2031, driven by increasing consumer demand for taste variety and premium positioning. The appeal of exotic fruit-derived flavors, such as yuzu, lychee, passion fruit, and guava, enables brands to charge premium prices and differentiate themselves in competitive retail spaces. Companies like Waterloo Sparkling Water, which uses proprietary fruit essences to deliver calorie-free, full-flavored options, and Bubly, leveraging extensive distribution networks, exemplify the rapid growth of flavored variants. As health and wellness trends continue to shift consumers away from sugary sodas, flavored sparkling water is becoming a preferred "zero-calorie yet flavorful" alternative, particularly among younger, taste-driven demographics.

Plain sparkling water remains resilient in specific markets, particularly in European countries, where consumers value mineral-sourced purity and a straightforward hydration experience. This cultural preference sustains the dominance of plain sparkling water, aligning with traditional taste expectations and the heritage of mineral water. At the same time, the rise of functional and flavored sparkling water, featuring zero-sugar, naturally flavored, and botanical-infused options, is reshaping the competitive landscape. For many brands, flavored sparkling water represents a strategic opportunity, combining hydration, taste diversity, and low-calorie appeal, driving faster growth despite its smaller market base.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Aluminum Cans Gain as Sustainability Trumps Convenience

Aluminum cans are anticipated to grow at an annual rate of 7.21% through 2031, representing the fastest growth among packaging formats. This expansion is driven by regulatory requirements and consumer preference for infinitely recyclable materials. In 2025, rPET and PET bottles held 56.05% of the market share; however, their growth is constrained by concerns over plastic waste and challenges in achieving large-scale closed-loop recycling. The International Aluminum Institute reports that aluminum cans achieve a global recycling rate exceeding 70%, with U.S. cans averaging 73% recycled content, significantly outperforming PET bottles. At COP28 in December 2023, 40 nations committed to achieving an 80% aluminum can recycling rate by 2030 and nearly 100% by 2050. Flow Beverage introduced sparkling water in aluminum bottles containing 70% recycled aluminum in Canada in August 2024, followed by U.S. expansion. Clearly Canadian launched 12-ounce aluminum SleekCans and expanded distribution to major retailers, including Walmart, Kroger, and Costco, by 2024.

Glass bottles continue to hold a premium position in European markets, with heritage brands such as Perrier, San Pellegrino, and Gerolsteiner leveraging their association with purity, tradition, and on-premise consumption. A 2024 German-Austrian lifecycle study highlighted that glass bottles are 10 times heavier than PET bottles and offer a shelf life more than twice as long for carbonated water. However, they produce higher carbon emissions during production and transportation compared to aluminum. Highland Spring invested GBP 10 million (USD 12.7 million) in 2024 to expand glass-bottle production capacity, achieving GBP 148.2 million (USD 188 million) in sales, a 13.5% increase. Meanwhile, rPET and PET bottles dominate mass-market channels due to their lightweight logistics and shatter resistance, with brands like Perrier targeting 50% rPET content by 2025 and Amcor launching 100% post-consumer recycled bottles in 2024.

By Category: Premium Segment Grows Fastest Despite Mass Dominance

The mass segment, holding a 69.55% market share in 2025, continues to lead due to its scale, competitive pricing, and extensive distribution. LaCroix's 2.4% volume growth and 8.5% dollar growth in Q1 FY2025, supported by National Beverage's USD 1.3 billion FY2024 revenue, demonstrate the segment's ability to maintain relevance through innovation and strong retail networks. Brands like Bubly and Topo Chico capitalize on broad retail partnerships to secure shelf space in supermarkets and club stores. Retailers such as Kroger and Costco further enhance affordability by offering private-label sparkling water options that appeal to cost-conscious consumers. Since 2023, leading beverage companies have increased promotional efforts and expanded multipack offerings to sustain consumer interest. The adoption of cleaner labels and natural flavors, often sourced from suppliers like Firmenich, has also helped mass brands narrow the gap with premium offerings while retaining their scale advantages.

The premium sparkling water segment, forecasted to grow at 7.79% annually from 2026 to 2031, is driven by consumer preferences for provenance, mineral sourcing, and premium packaging. Region-specific offerings, such as Rayyan's Halal-certified glass-bottled lemon variant in Qatar, cater to local preferences, emphasizing authenticity over imports. Post-2023 launches, including mineral-enriched variants from established brands, highlight efforts to strengthen premium positioning. Asian brands like Chi Forest, which expanded to 40 countries and entered retailers such as Costco and Tesco by 2024, are reshaping the premium narrative in Western markets. The focus on flavor sophistication and natural ingredients, including botanical extracts from suppliers like Döhler, underscores the segment's appeal. These factors explain why consumers are willing to pay higher prices, even as premium volumes remain smaller than those of the mass market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: On-Trade Recovery Outpaces Off-Trade Growth

Off-trade channels continue to dominate the sparkling water market, supported by supermarkets, hypermarkets, and e-commerce platforms, which collectively accounted for a 63.88% market share in 2025. Retailers are leveraging private-label sparkling water to attract customers and emphasize value amid inflation-sensitive consumer behavior. Convenience stores recorded notable growth in 2024, driven by the demand for single-serve formats as convenient hydration options for urban consumers. Post-2023, e-commerce growth accelerated due to subscription-based models and bulk delivery services, enhancing affordability and accessibility, particularly for digitally native brands. Direct-to-consumer players, such as Sanzo, have utilized online channels to introduce global flavors and culturally inspired formulations through targeted campaigns. These factors collectively position off-trade channels as the primary volume driver, offering diverse formats at competitive price points.

The on-trade channel is projected to grow at an annual rate of 7.6% through 2031, driven by the recovery of dining-out trends and the inclusion of premium, mineral-sourced sparkling waters in beverage menus. Restaurants and hotels are increasingly positioning sparkling water as a high-margin, health-conscious alternative to sugary sodas and alcoholic beverages. Fine-dining establishments now feature curated offerings, such as Gerolsteiner and region-specific artisanal waters, while incorporating refillable glass packaging to align with sustainability goals. Emerging trends, including chef-curated water lists and terroir-driven water selections, further reinforce sparkling water’s role in enhancing premium dining experiences. The on-trade channel serves as both a discovery platform and a brand-building avenue, amplifying the appeal of premium formats globally.

Geography Analysis

North America accounted for approximately 27.95% of the sparkling water market share in 2025, supported by increasing health consciousness and a well-established retail infrastructure that caters to both mass-market and premium sparkling water products. In the United States, the shift from sugary soft drinks to zero-calorie sparkling water has positioned sparkling variants as the fastest-growing sub-segment of packaged water. Similarly, Canada experienced a rise in sparkling water consumption in 2024, reflecting similar health-focused and urban lifestyle trends. In Mexico, the expansion of heritage brands such as Topo Chico (owned by The Coca-Cola Company) and the introduction of flavored variants have extended the distribution of sparkling water, reinforcing North America’s leading position in the market.

The Asia-Pacific region is projected to achieve the fastest growth in the sparkling water market between 2026 and 2031, with an estimated CAGR of 6.88%. This growth is driven by rapid urbanization, rising disposable incomes, and the increasing adoption of Western lifestyle habits in countries such as China, India, and across Southeast Asia. Export-oriented brands are also contributing to this expansion by scaling globally; for instance, Chinese sparkling water brands are entering Western markets, showcasing a trend of cross-regional brand penetration. In Australia, growing health awareness and familiarity with bottled hydration are expected to further boost demand for sparkling water. These factors highlight the region’s potential as a key growth area for the sparkling water market.

Europe remains a stronghold for premium, mineral-sourced sparkling water, supported by cultural preferences for carbonated hydration and regulatory measures promoting sustainable packaging. The expansion of deposit-return schemes (DRS) in countries like Austria, Sweden, and the Netherlands is driving the adoption of recyclable packaging formats, appealing to environmentally conscious consumers. Meanwhile, emerging markets in South America and the Middle East and Africa are experiencing increased demand due to urbanization, rising incomes, tourism, and expatriate consumption. However, price sensitivity continues to limit mass-market penetration in these regions, though the growing consumer base signals potential for future growth.

Competitive Landscape

Market Concentration

The global sparkling water market exhibits moderate consolidation, with large multinationals such as Coca‑Cola, PepsiCo, Nestlé, and Danone maintaining significant control over shelf space and distribution networks. However, smaller disruptors are carving out niches through direct-to-consumer branding and innovative positioning. Both established and emerging players are increasingly focusing on functional hydration products, including electrolyte-infused, adaptogen- or caffeine-enhanced, and vitamin/mineral-fortified variants. These offerings cater to premium consumers seeking enhanced hydration options, enabling smaller brands to compete effectively despite limited scale.

Recent developments underscore the shifting competitive dynamics. Liquid Death, recognized for its lifestyle-oriented branding and aluminum-canned sparkling water, secured USD 67 million in financing in March 2024, achieving a valuation of USD 1.4 billion. This reflects strong investor confidence in niche, brand-driven products. However, challenges persist, as evidenced by the temporary suspension of Liquid Death's United Kingdom and European operations in early 2025, highlighting the complexities of scaling global distribution. This combination of market volatility and branding innovation illustrates both opportunities and risks for challengers redefining the sparkling water market.

Packaging innovation has emerged as a key competitive differentiator. Aluminum cans are gaining traction due to their high recyclability, up to 95% infinite recyclability, and lower carbon footprint compared to glass or PET. Lifecycle assessments by the Aluminum Association indicate that aluminum production uses 80% less energy than alternative materials. Regulatory measures, such as the EU's mandatory deposit return systems introduced in 2024, further incentivize sustainable practices. Functional disruptors like HOP WTR leverage these trends by combining adaptogen-forward formulations with sustainable packaging. Additionally, brands like Topo Chico are adopting fully recycled cans to enhance their sustainability narratives. These advancements in packaging, coupled with functional innovations, enable both established players and challengers to strengthen their market positions while addressing consumer demand for sustainability and wellness.

Sparkling Water Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Carlsberg Britvic’s Aqua Libra brand expanded its infused sparkling water range with the addition of a watermelon and strawberry flavor. Offered in multipacks of four and 24 through the United Kingdom grocery channel, the flavor combined sweet taste profiles and contained no sugar or preservatives. It was calorie-free and described as delivering a "clean, crisp taste."

- April 2024: Bisleri International, an Indian company, announced a limited edition of its "Vedica Himalayan Sparkling Water" in the domestic market. To support its promotion, the company collaborated with celebrity Gauri Khan, who featured in marketing campaigns and advertisements to increase the product's visibility and consumer appeal.

- March 2024: PepsiCo introduced its sweetened sparkling water product, which was made available in six flavors: Triple Berry, Peach Mango, Watermelon Lime, Pineapple Tangerine, Cherry Lemonade, and Tropical Punch. This product line was designed to appeal to consumers seeking a refreshing beverage that combined sparkling water with sweet fruit flavors.

Table of Contents for Sparkling Water Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising health consciousness promotes sparkling water as a low-calorie alternative to sugary sodas

- 4.2.2Innovation in flavors attracts diverse consumer tastes

- 4.2.3Growing preference for sustainable packaging like recyclable cans drives eco-focused sales

- 4.2.4Expansion of functional variants, such as caffeinated types, appeals to energy-seeking users

- 4.2.5Premiumization through mineral-sourced products elevates market positioning

- 4.2.6Wellness trends emphasize digestion and hydration benefits of carbonated water

- 4.3Market Restraints

- 4.3.1Premium price versus still water

- 4.3.2Intense competition from flavored waters and sports drinks fragments market share

- 4.3.3Plastic-waste and carbon-footprint scrutiny

- 4.3.4Consumer skepticism about carbonation's health impacts limits adoption

- 4.4Value Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Flavored Sparkling Water

- 5.1.2Plain Sparkling Water

- 5.2By Packaging Type

- 5.2.1Cans

- 5.2.2Glass Bottles

- 5.2.3rPET/PET Bottles

- 5.3By Category

- 5.3.1Mass

- 5.3.2Premium

- 5.4By Distribution Channel

- 5.4.1On-Trade/HoReCa

- 5.4.2Off-Trade

- 5.4.2.1Supermarkets/Hypermarkets

- 5.4.2.2Convenience Stores

- 5.4.2.3Online Retail Stores

- 5.4.2.4Other Distribution Channels

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.1.4Rest of North America

- 5.5.1.5Germany

- 5.5.1.6United Kingdom

- 5.5.1.7Italy

- 5.5.1.8France

- 5.5.1.9Spain

- 5.5.1.10Netherlands

- 5.5.1.11Poland

- 5.5.1.12Belgium

- 5.5.1.13Sweden

- 5.5.1.14Rest of Europe

- 5.5.2Asia-Pacific

- 5.5.2.1China

- 5.5.2.2India

- 5.5.2.3Japan

- 5.5.2.4Australia

- 5.5.2.5Indonesia

- 5.5.2.6South Korea

- 5.5.2.7Thailand

- 5.5.2.8Singapore

- 5.5.2.9Rest of Asia-Pacific

- 5.5.3South America

- 5.5.3.1Brazil

- 5.5.3.2Argentina

- 5.5.3.3Colombia

- 5.5.3.4Chile

- 5.5.3.5Peru

- 5.5.3.6Rest of South America

- 5.5.4Middle East and Africa

- 5.5.4.1South Africa

- 5.5.4.2Saudi Arabia

- 5.5.4.3United Arab Emirates

- 5.5.4.4Nigeria

- 5.5.4.5Egypt

- 5.5.4.6Morocco

- 5.5.4.7Turkey

- 5.5.4.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Nestlé S.A.

- 6.4.2PepsiCo Inc.

- 6.4.3The Coca-Cola Company

- 6.4.4Danone S.A.

- 6.4.5National Beverage Corp.

- 6.4.6Keurig Dr Pepper Inc.

- 6.4.7Primo Water Corp.

- 6.4.8Talking Rain Beverage Co.

- 6.4.9Spindrift Beverage Co.

- 6.4.10Waterloo Sparkling Water Corp.

- 6.4.11Polar Beverages

- 6.4.12Gerolsteiner Brunnen GmbH

- 6.4.13Asahi Group Holdings

- 6.4.14Chi Forest

- 6.4.15Highland Spring Group

- 6.4.16Liquid Death Mountain Water Co.

- 6.4.17Flow Beverage Corp.

- 6.4.18A.G. Barr plc

- 6.4.19Ferrarelle S.p.A.

- 6.4.20HOP WTR Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Sparkling Water Market Report Scope

Sparkling water is carbonated water infused with dissolved carbon dioxide gas, resulting in the formation of small bubbles and an effervescent quality.

The market is segmented into product types, packaging, category, distribution channels, and geography. The market is segmented into flavored and plain sparkling water based on product type. Based on packaging type, the market is segmented into packaging types, glass bottles, and rPET/PET bottles. Based on the category, the market is segmented into mass and premium. Besides, the distribution channel is segmented into on-trade and off-trade. Off-trade is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. The report also covers a detailed analysis of major economies across major regions, including North America, Europe, Asia Pacific, South America, and Middle East Africa.

The Market Forecasts are Provided in Terms of Value (USD).