Mead Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.73 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 10.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mead Beverages Market Analysis by Mordor Intelligence

The traditional mead market size was valued at USD 0.65 billion in 2025 and estimated to grow from USD 0.73 billion in 2026 to reach USD 1.23 billion by 2031, at a CAGR of 10.95% during the forecast period (2026-2031). Producers are reframing honey wine as a contemporary craft beverage, positioning it to compete directly with dry cider and sessionable beer. They're leveraging terroir narratives, circular-economy honey sourcing, and low-ABV formulations to resonate with the growing emphasis on wellness and sustainability. These strategies aim to expand honey wine's appeal beyond its traditional niche audience, targeting a broader consumer base that values premium and eco-conscious products. With regulatory clarity on “gluten-free” labeling and the upcoming Alcohol Facts panels set for full enforcement in 2030, there's a clear distinction being made between naturally grain-free meads and malt beverages. This regulatory support not only enhances product differentiation but also builds consumer trust in the category. Additionally, e-commerce liberalization is proving beneficial for small brands, allowing them to achieve impressive gross margins of 60-70% through direct-to-consumer (D2C) sales. This shift enables producers to bypass traditional distribution channels, fostering stronger customer relationships and higher profitability.

Key Report Takeaways

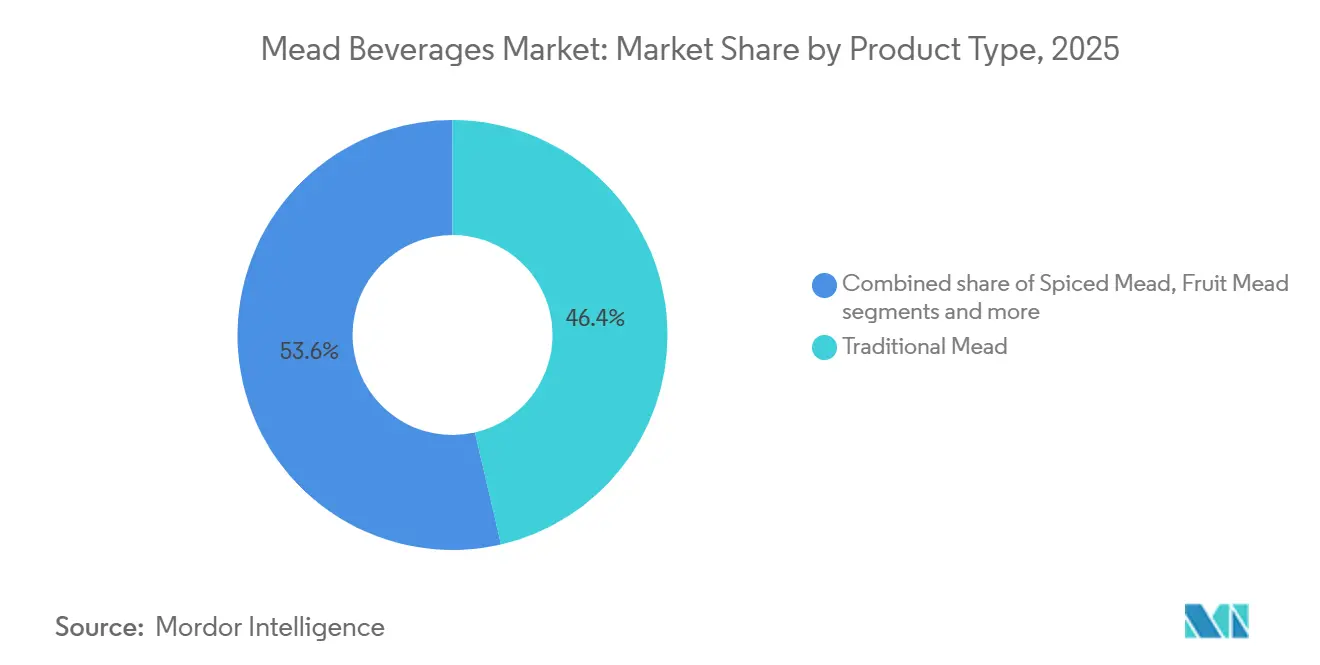

- By product type, Traditional Mead led with 46.38% of the traditional mead market share in 2025, whereas Sparkling Mead is set to expand at an 11.02% CAGR through 2031.

- By packaging, Bottles accounted for 63.19% of 2025 revenue, while Cans are poised to grow at a 12.56% CAGR over 2026-2031.

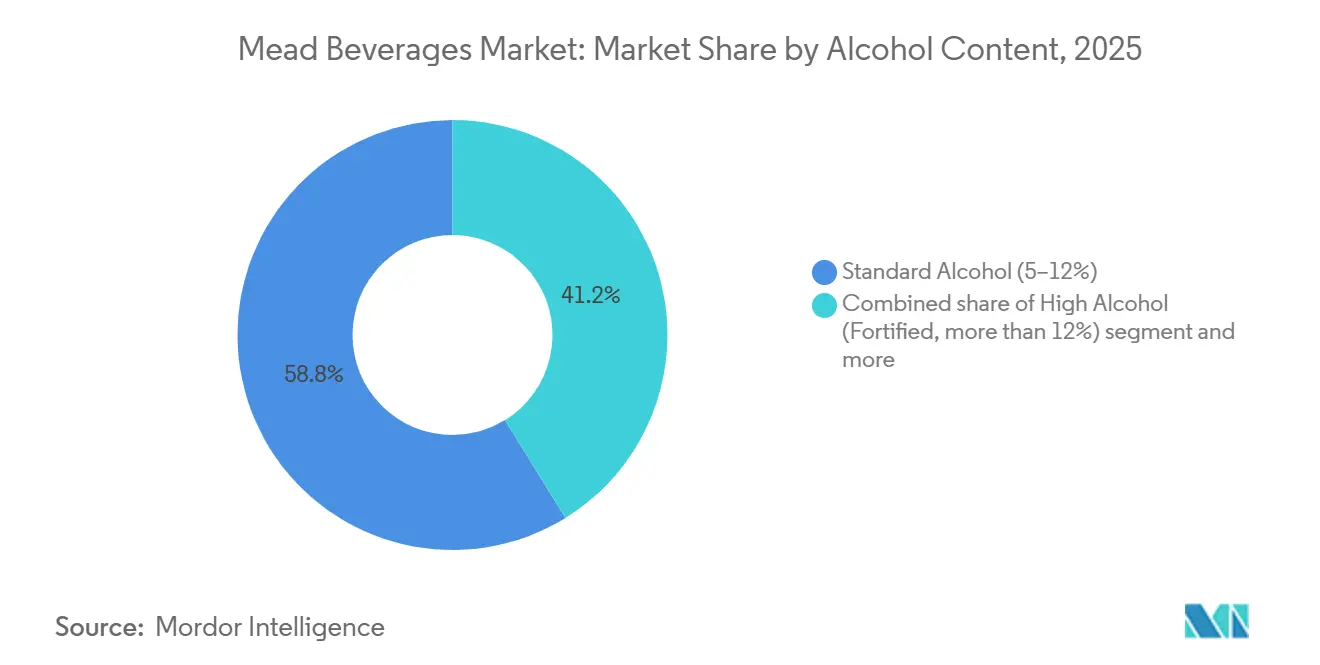

- By alcohol content, Standard-strength formats (5-12% ABV) held a 58.81% share in 2025; Low-alcohol variants (≤5% ABV) are forecast to register a 12.56% CAGR.

- By distribution, Off-trade channels represented 52.54% of 2025 sales, but On-trade is projected to post the fastest pace at 12.04% CAGR as aperitivo-style mead cocktails proliferate in premium venues.

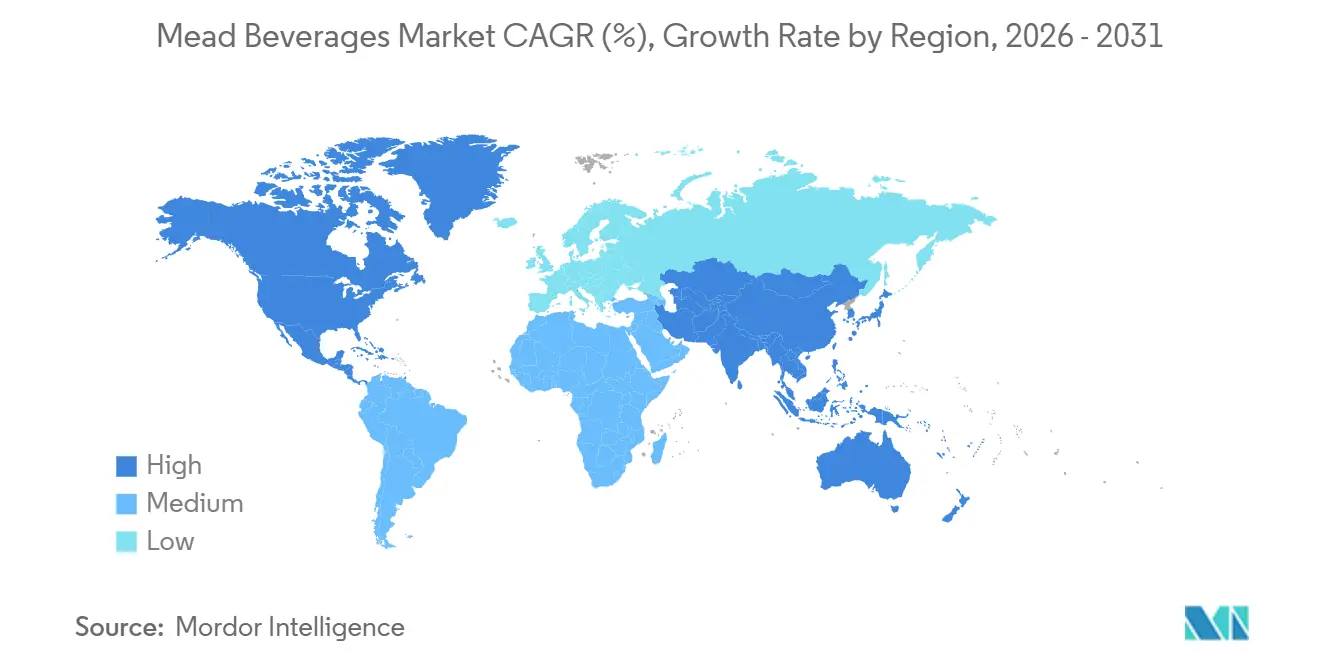

- By geography, Europe dominated with 34.15% of 2025 revenue, whereas Asia-Pacific is expected to deliver the strongest regional growth at 11.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mead Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for craft and artisanal alcoholic beverages | +2.0% | Global, with strongest uptake in North America and Western Europe | Medium term (2-4 years) |

| Growing demand for gluten-free alcohol alternatives | +1.5% | North America, Europe, Australia; emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Rapid e-commerce and D2C expansion for beverage alcohol | +1.8% | North America (led by California, New York), UK, Australia; regulatory barriers in Asia-Pacific | Short term (≤ 2 years) |

| Valorisation of surplus honey through circular-economy partnerships | +0.8% | Europe (Germany, France, Spain), North America (California, Oregon) | Long term (≥ 4 years) |

| Low-ABV mead cocktails gaining traction in premium on-trade venues | +1.2% | Europe (UK, Italy, Spain), North America (urban metros), Australia | Medium term (2-4 years) |

| Integration into functional foods and nutraceuticals | +0.7% | North America, Northern Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for craft and artisanal alcoholic beverages

Craft credentials have shifted from a niche to a mainstream driver of purchase. Millennials and Gen Z consumers, with earnings surpassing USD 60,000, are placing a premium on provenance, small-batch production, and transparent ingredient sourcing. This trend has cultivated a receptive audience for terroir-focused meads, which emphasize the unique characteristics of their origin and production methods. In 2026, Irish producer Kinsale Mead Co. made waves by introducing whiskey-cask-aged meads. By harnessing the allure of dark forest honey and the nuances of oak maturation, they successfully drew in craft spirits aficionados, bridging the gap between traditional meads and premium craft spirits. With the impending mandates of the Alcohol Facts panel, there's set to be an intensified focus on sugar levels. This scrutiny is poised to favor naturally dry meads, which align with consumer preferences for healthier, less sweet alcoholic beverages, sidelining their back-sweetened counterparts.

Growing demand for gluten-free alcohol alternatives

Under TTB Ruling 2025-2, mead producers can label their products as "gluten-free" without further validation, provided their base ingredients are grain-free. This ruling is expected to boost consumer confidence in mead as a safe option for individuals with gluten intolerance or celiac disease.In 2023, studies revealed that about 1% of the U.S. population, or roughly 1 in 133 Americans, suffers from celiac disease, as reported by Beyond Celiac[1]Source: Beyond Celiac, "Celiac Disease: Fast Facts", beyondceliac.org . Alarmingly, research suggests that up to 83% of these cases go undiagnosed or are misdiagnosed. It also provides a competitive edge for mead producers in the growing gluten-free beverage market. Retailers are seizing the opportunity: In 2025, Hive Mind Mead clinched a listing in 50 Marks and Spencer stores, a feat made possible by certification upgrades that also paved the way for exports to Taiwan and Denmark. The inclusion of mead in mainstream retail chains highlights its growing acceptance as a versatile beverage. However, there's still a challenge: Many shoppers who avoid gluten often mistakenly gravitate towards cider instead. Enhanced consumer education and targeted marketing campaigns could help bridge this gap and drive awareness about mead's gluten-free status.

Rapid e-commerce and D2C expansion for beverage alcohol

In 2024, 63% of online alcohol buyers conducted thorough research before making a purchase, turning to digital sources such as brand websites, product reviews, and delivery apps, as reported by the International Wine and Spirits Record[2]Source: International Wine and Spirits Record (IWSR), IWSR Projects Alcohol E-commerce Channel to surpass USD 36 Billion by 2028," theiwsr.com. In 2025, Gosnells made a strategic move by acquiring a London pub, seamlessly merging the allure of on-premise brand theater with the efficiency of online fulfillment. This acquisition underscores a hybrid route-to-market model. By integrating physical and digital channels, Gosnells aims to enhance customer engagement and drive sales growth. The move also reflects a growing trend among beverage producers to diversify their distribution strategies, ensuring resilience in an evolving market landscape. Additionally, this approach allows Gosnells to strengthen its brand presence while catering to a broader consumer base. Meanwhile, California's AB 1246, which extended wine shipping privileges, sparked a compliance arbitrage. As a result, meaderies began reformulating their products to achieve an ABV below 7%, allowing them to meet the "wine" definition and tap into lucrative direct-to-consumer channels.

Valorization of surplus honey through circular-economy partnerships

European cooperatives secure off-spec or crystallized honey through multi-year contracts, reducing raw material costs by as much as 25% and ensuring a consistent income for beekeepers. These contracts provide stability in the supply chain and help mitigate price volatility in the honey market. In California and Oregon, meaderies are adopting a similar approach, forming almond-pollination partnerships that not only enhance their terroir storytelling but also facilitate applications for protected geographical indications (PGI). This strategy allows meaderies to differentiate their products while supporting sustainable beekeeping practices. Additionally, these partnerships strengthen the connection between local agricultural practices and the final product, creating a unique value proposition for consumers. By leveraging these collaborations, meaderies can also contribute to the preservation of regional biodiversity and promote environmentally conscious production methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile honey prices elevating production costs | -1.5% | Global, with acute pressure in North America and Europe due to pollinator decline | Short term (≤ 2 years) |

| Limited consumer awareness beyond niche communities | -1.0% | Global, most pronounced in Asia-Pacific and South America | Medium term (2-4 years) |

| Shorter shelf-life of unpasteurised craft meads limiting distribution scale | -0.8% | North America, Europe (craft segment); less relevant in Asia-Pacific where pasteurization is standard | Medium term (2-4 years) |

| Honey adulteration scandals undermining trust and quality perception | -0.7% | Asia-Pacific (India, China), spillover to global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile honey prices elevating production costs

In 2024, honey prices surged 12% year-over-year, as reported by the USDA. According to the USDA, U.S. honey production hit 688.6 million pounds in 2024, satisfying just 20% of the nation's consumption[3]Source: National Honey Board, "U.S. Honey Consumption Hits All-Time High", honey.com. This spike has tightened gross margins by 4-6 points for meaderies that depend on spot purchases. The rising costs have placed significant pressure on smaller producers, who often lack the resources to hedge against price fluctuations. This has led to increased uncertainty in their operations, with many struggling to maintain competitive pricing while preserving profitability. Larger players, on the other hand, benefit from economies of scale and strategic sourcing, enabling them to better manage cost pressures. Their ability to secure long-term contracts or own apiaries provides a competitive edge, ensuring stability in supply and pricing. While larger players shield themselves through multi-continent supply contracts and direct ownership of apiaries, smaller producers find themselves vulnerable to the whims of spot market volatility.

Limited consumer awareness beyond niche communities

Gosnells rebranded to "Hazy Nectar" in 2024, highlighting a lexical challenge: the term "mead" conjures medieval images, alienating potential new drinkers. This rebranding reflects an effort to modernize the product's perception and align it with contemporary consumer preferences. The term "Hazy Nectar" is designed to evoke curiosity and resonate with younger demographics who are more inclined toward innovative beverage options. For micro-scale operations, in-store demos priced between USD 15,000-25,000 per chain become financially burdensome, hindering sales momentum in traditional retail settings. These high costs limit smaller producers' ability to compete with larger brands that can afford such promotional activities, further slowing their market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Roots and Carbonation Lead Evolution

In 2025, traditional mead commanded the market, securing 46.38% of total revenue and solidifying its dominance. This stronghold is bolstered by deep-rooted consumer familiarity and unwavering demand in key markets. Producers are amplifying the segment's premium allure by harnessing terroir-specific honeys and employing barrel-aging techniques, setting their products apart. Such strategies not only uphold elevated price points but also resonate with consumers who value authenticity and craftsmanship. Moreover, traditional styles showcase versatility across both retail and on-premise channels, driving consistent volume and value growth.

Sparkling Mead is rapidly ascending, with projections indicating a robust CAGR of 11.02%. This surge is fueled by a growing consumer inclination towards crisp, sessionable drinks akin to dry cider. The segment's expansion is bolstered by deeper penetration into multipack formats and on-premise draught programs, enhancing both accessibility and trial. Craft beverage aficionados are particularly drawn to the segment, especially with innovative hybrids like hopped or spirit-cask variants. Concurrently, categories such as fruit, herb, and spiced meads are gaining traction, luring adventurous consumers in taproom environments. While non-traditional sub-types currently command a modest market share, their impressive double-digit growth signals a wealth of innovation potential in the category.

By Packaging Type: Sustainability and Convenience Reshape Format Mix

In 2025, bottles dominated the packaging landscape, clinching 63.19% of total revenue. They continued to be the go-to choice in the traditional mead market, often associated with prestige. This stronghold stems from consumers equating bottles with quality, making them the top pick for gifts and premium buys. Bottling not only showcases a producer's craftsmanship, especially for small-batch and barrel-aged meads, but also aligns with higher price tags, bolstering brand heritage and authenticity. Even with the rise of alternatives, bottles hold their ground, thanks to their entrenched presence in both retail and specialty outlets.

Cans are emerging as the packaging segment to watch, with projections pointing to a robust CAGR of 12.56%. Their growth is largely attributed to sustainability perks and user-friendliness. Aluminum's impressive recycling rate and its reduced carbon footprint, especially when juxtaposed with glass, strike a chord with eco-conscious consumers. The surge in canned ready-to-drink options is paving the way for broader distribution, making their way into convenience stores and petrol stations. This not only boosts accessibility but also diminishes trial barriers. Cans shine in outdoor and event settings, where bottles might be cumbersome. Consequently, producers are weaving cans into their multi-format strategies, tapping into shifting consumption trends and driving volume growth.

By Alcohol Content: Moderation Wave Accelerates Low-ABV Adoption

In 2025, standard-strength meads (5–12% ABV) led the market, capturing 58.81% of total consumer spending. Their balanced profile attracts a diverse consumer base, drawn to moderate alcohol content without sacrificing flavor. The segment's widespread presence in both retail and on-premise channels solidifies its dominance. Producers are honing in on taste consistency and drinkability to keep the momentum going. Additionally, the versatility of standard-strength meads makes them suitable for various consumption occasions, from casual gatherings to formal events. Consequently, standard-strength meads are the primary revenue generators in the traditional mead landscape.

Low-ABV meads (<5% ABV) are the market's rising stars, with a projected CAGR of 12.56%, fueled by a shift towards mindful drinking. These meads are now sharing shelf space with hard seltzers, carving out a niche as a flavorful, grain-free option. Innovations in fermentation, like specialized yeast strains and arrested fermentation, ensure these meads retain their body and mouthfeel, even with reduced alcohol content. Their appeal is bolstered by their fit for casual, sessionable drinking, making them an attractive choice for health-conscious consumers seeking lighter alternatives. Furthermore, the growing trend of low-ABV beverages aligns with the increasing demand for products that offer a balance between indulgence and wellness. While high-ABV meads cater to a premium, niche audience, the spotlight is on low-ABV innovations driving volume growth in the near future.

By Distribution Channel: Experiential On-Trade Rebounds

In 2025, off-trade channels dominated the market, capturing 52.54% of the total share. This dominance was largely bolstered by the at-home consumption habits that took root during the pandemic. Retail formats, especially grocery stores and liquor outlets, have been pivotal in driving volume due to their accessibility and convenience. Yet, smaller producers face hurdles when engaging with large retail chains, grappling with challenges like slotting fees and prolonged payment cycles, which can significantly impact their operational efficiency and financial stability. Despite these challenges, off-trade channels remain a vital revenue stream for meaderies aiming for growth. Many producers are adept at balancing their presence across various retail formats, ensuring consistent cash flow and market penetration. This strategic diversification allows them to mitigate risks associated with over-reliance on a single channel while expanding their consumer base.

On-trade channels are emerging as the fastest-growing segment, with projections indicating a CAGR of 12.04%. This surge is fueled by a rekindled consumer enthusiasm for out-of-home social experiences. Restaurants and cocktail bars are not just serving mead; they're elevating it, crafting innovative offerings like spritzes and Americano-style drinks. These creative applications not only boost mead's visibility but also encourage trial among a broader audience, including those unfamiliar with the product. Moreover, these establishments present more lucrative margin opportunities than traditional beer placements, making them an attractive channel for producers. Concurrently, the e-commerce boom is bolstering on-trade growth, aided by shifting regulations that permit wider shipping of low-ABV mead products. This regulatory evolution has opened new avenues for producers to reach consumers directly, further enhancing category growth. Collectively, these trends underscore the growing significance of experiential and direct engagement channels in propelling the category's expansion.

Geography Analysis

In 2025, Europe accounted for 34.15% of total revenue, driven by the UK's focus on innovation and Germany's partnerships in circular honey. Structures like Protected Geographical Indication allow for rich terroir narratives, and established on-trade networks are increasingly embracing low-ABV aperitivo offerings. The region's mature market dynamics provide a strong foundation for premium product positioning. However, fragmented regulatory landscapes across countries necessitate compliance investments, leading to heightened overhead costs and operational complexities.

Asia-Pacific, with a robust 11.29% CAGR, is spearheaded by India's stringent honey-authentication measures and Japan's growing acceptance of low-strength fermented drinks. While rising disposable incomes and emerging craft-beverage trends present vast opportunities, challenges like state-level licensing and inconsistent cold-chain infrastructure pose hurdles to rapid scaling. The region's diverse consumer preferences further drive innovation in product offerings. Despite these opportunities, logistical inefficiencies remain a significant barrier to seamless market penetration.

North America's well-entrenched craft-beer scene has made taproom culture mainstream. With the TTB's upcoming nutrition and allergen labeling, mead's gluten-free attributes are set to gain attention. The region's established distribution networks and consumer awareness create a favorable environment for product diversification. Yet, challenges remain with interstate shipping limitations. To navigate this, producers are crafting low-ABV SKUs that align with "wine" classifications, granting them direct-to-consumer advantages. However, Canada's interprovincial restrictions and Mexico's state-specific licensing continue to hinder broader regional growth, limiting cross-border synergies.

Competitive Landscape

The traditional mead market is moderately fragmented. Regional leaders like Gosnells, Lyme Bay, Schramm’s Mead, and Kinsale Mead Co. dominate the traditional mead market, using strong storytelling and strategic channel adjacency to carve out their local markets. By emphasizing heritage, provenance, and consumer education, these players cultivate brand loyalty. They also tailor their distribution strategies to enhance visibility and accessibility, both in retail spaces and on-premise environments. Notably, Gosnells is making waves with its vertical integration strategy, acquiring pubs to seamlessly connect the on-premise experience with retail sales, thereby deepening consumer engagement.

Meanwhile, premium producers like Schramm’s Mead are doubling down on barrel-aging programs, solidifying their foothold in high-margin niche segments. These programs allow them to create unique flavor profiles that appeal to discerning consumers seeking premium experiences. Embracing a tech-forward approach, some players are turning to precision fermentation and high-pressure processing. These techniques promise improved consistency, extended shelf life, and reduced batch variability, all while upholding quality standards. By integrating advanced technologies, these producers aim to stay competitive and meet the evolving expectations of modern consumers.

Yet, challenges loom for these incumbents. With the looming threat of commoditization, larger beer and cider companies might harness their expansive scale and distribution prowess to roll out competitively priced honey-based beverages. Such competition could erode market share for smaller players, forcing them to innovate further. In a bid to counter this, craft meaderies are doubling down on differentiation. By focusing on terroir-driven sourcing, launching limited-edition releases, and engaging directly with consumers, they're bolstering their brand equity and shielding themselves from price-centric competition. These strategies not only enhance customer loyalty but also create a distinct identity that sets them apart in an increasingly crowded market.

Mead Beverages Industry Leaders

-

B. Nektar Meadery

-

Superstition Meadery

-

Dansk Mjod A/S

-

Gosnells London

-

Moonlight Meadery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hive Mind has broadened its "classic drinks rethought" range by introducing Sparkling Meads at Marks & Spencer. Targeting the fruited cider enthusiasts, the company crafted canned sparkling meads with a 3.4% ABV, harnessing the essence of British honey. Marks & Spencer's lineup featured three distinct flavors: Pure Honey, Rhubarb, and Elderflower, all elegantly housed in carbon-neutral 330ml cans.

- February 2024: Salud unveiled its latest ready-to-drink (RTD) offering, Salud Viking, boasting a 15% alcohol content and crafted from mead. Infused with an IPA-style hop flavor, the beverage comes elegantly bottled in a 375ml package. Salud Viking reimagines the age-old tradition of mead, being crafted through the fermentation of honey and water.

- August 2023: Moonshine, Asia's pioneering meadery and India's first, has unveiled its latest offering: Lemon Tea Mead. This innovative beverage melds the zest of lemon with Vahdam's Earl Grey tea. Priced at INR 150 and available year-round in Maharashtra, the product seeks to familiarize a broader audience with mead. In a bid to champion zero-waste practices, Moonshine has teamed up with Malaka Spice, repurposing their used lemon zest. Furthermore, the meadery has intentions to broaden this eco-friendly initiative, collaborating with additional restaurants in Pune.

Global Mead Beverages Market Report Scope

| Traditional Mead |

| Spiced Mead |

| Fruit Mead |

| Herb Mead |

| Sparkling Mead |

| Other Meads (including experimental or hybrid variants) |

| Bottles |

| Cans |

| Kegs |

| Low Alcohol (Non/Low-Alc Mead, ≤5%) |

| Standard Alcohol (5 - 12%) |

| High Alcohol (Fortified, more than 12%) |

| On-Trade |

| Off-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Traditional Mead | |

| Spiced Mead | ||

| Fruit Mead | ||

| Herb Mead | ||

| Sparkling Mead | ||

| Other Meads (including experimental or hybrid variants) | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Kegs | ||

| By Alcohol Content | Low Alcohol (Non/Low-Alc Mead, ≤5%) | |

| Standard Alcohol (5 - 12%) | ||

| High Alcohol (Fortified, more than 12%) | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the traditional mead market expected to grow between 2026 and 2031?

The category is projected to advance at a 10.95% CAGR, lifting value from USD 0.73 billion in 2026 to USD 1.23 billion by 2031.

Which product segment generates the most revenue today?

Traditional Mead leads with 46.38% of 2025 sales.

Which format is gaining the most traction for casual occasions?

Canned sparkling mead shows the fastest growth at a 12.56% CAGR, propelled by portability and high aluminum recycling rates.

Why is Asia-Pacific the fastest-growing region?

Rising disposable income, updated honey-authenticity laws, and nascent craft-beverage cultures drive an 11.29% regional CAGR.

Page last updated on: