Spain Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

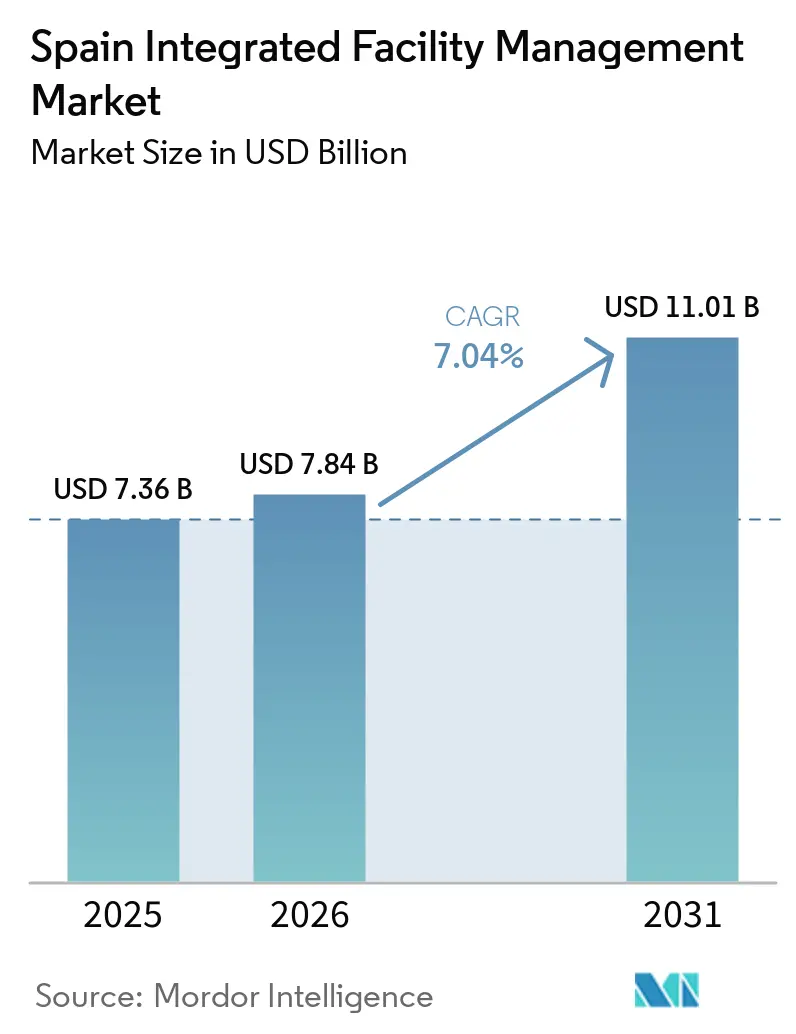

| Base Year Market Size (2025) | USD 7.36 Billion |

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 11.01 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Integrated Facility Management Market Analysis by Mordor Intelligence

The Spain Integrated Facility Management Market size is expected to grow from USD 7.36 billion in 2025 to USD 7.84 billion in 2026 and is forecast to reach USD 11.01 billion by 2031 at 7.04% CAGR over 2026-2031.

Spain’s broader facility management sector also remained large in 2025 at EUR 49 billion (USD 55.3 billion), and integrated models accounted for more than 35% of sector turnover, which shows that bundled service delivery is moving further into the mainstream of occupier and public estate management. Organizations across offices, factories, logistics sites, and public estates are shifting fixed in-house overhead to variable service contracts because single-vendor models provide clearer accountability, simpler coordination, and stronger performance tracking across multi-site portfolios. Regulatory pressure from the recast EPBD, tighter labour availability in technical trades, and rising digital reporting needs are also pushing the Spanish integrated facility management market away from reactive maintenance and toward planned, data-backed asset management. Competition remains active between large domestic operators and international service providers, while many regional specialists still matter in execution, especially where technical trades, local relationships, or public procurement routines shape contract awards. The Spain integrated facility management market therefore has room to grow through energy management, automation-enabled maintenance, and ESG reporting support, although labour cost inflation and skilled technician shortages continue to shape contract pricing, supplier selection, and margin discipline.

Key Report Takeaways

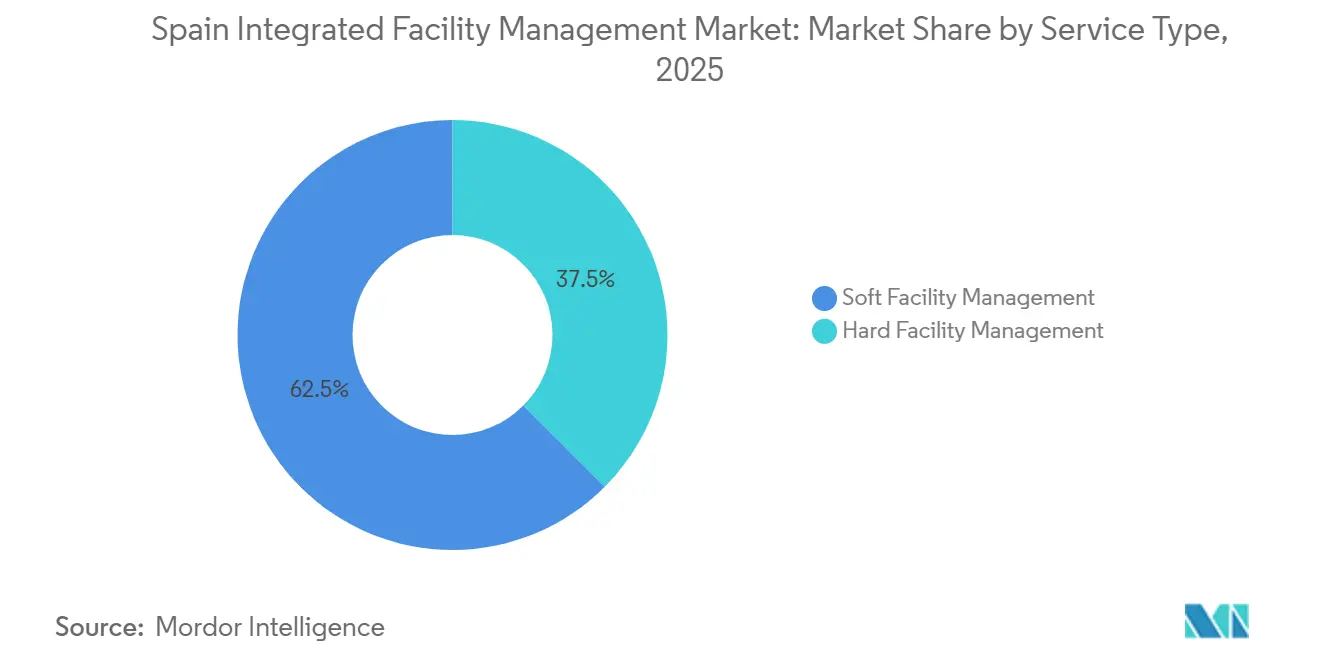

- By service type, soft facility management held 62.53% of the Spain integrated facility management market share in 2025, while hard facility management is projected to record the highest CAGR at 7.91% through 2031.

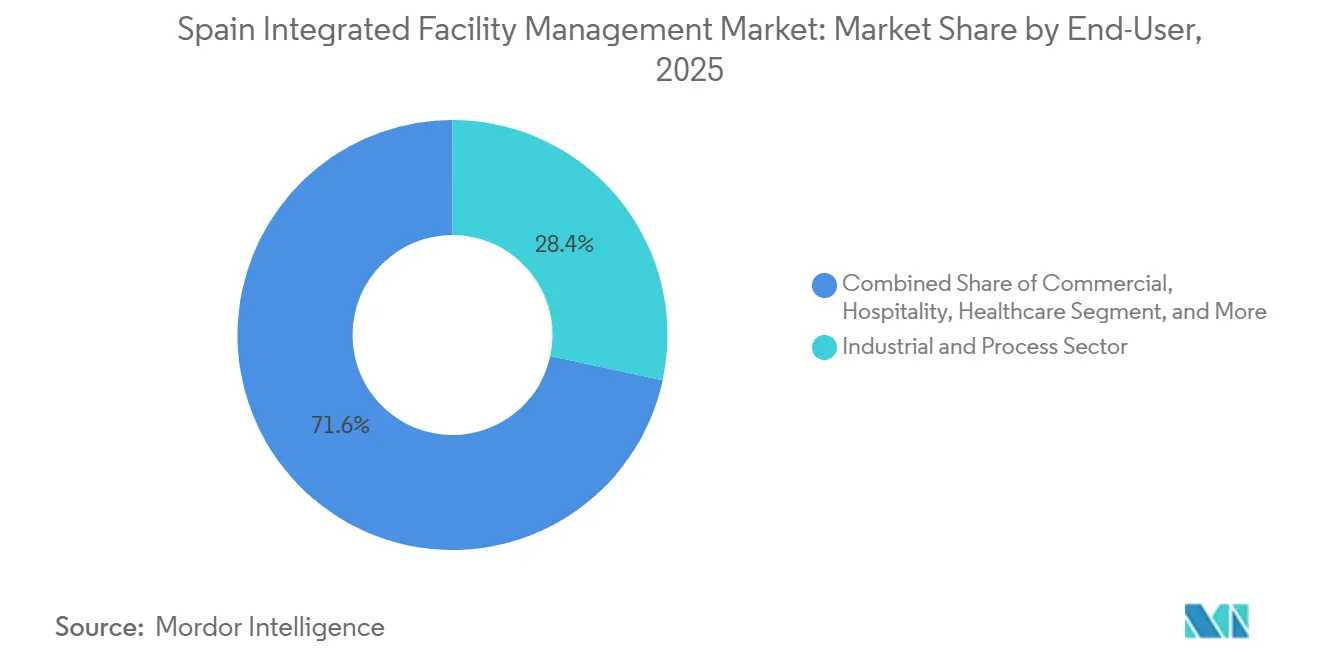

- By end-user, industrial and Process sector held 28.38% of the Spain integrated facility management market share in 2025, while Commercial is forecast to post the fastest CAGR at 8.03% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Outsourcing of Non-Core Activities | +1.8% | National, with early gains in Madrid and Barcelona corporate clusters | Short term (≤ 2 years) |

| Rising Demand for Energy-Efficient Buildings | +1.6% | National, strongest in non-residential stock in Madrid, Catalonia, and Andalucía | Medium term (2-4 years) |

| Expansion of Smart Building Technologies | +1.2% | National, concentrated in Tier-1 office, industrial, and data center markets | Medium term (2-4 years) |

| EU Taxonomy Pressure on ESG Reporting | +0.9% | National, with spillover into EU institutional portfolios and cross-border supply chains | Medium term (2-4 years) |

| Increase In Corporate Wellness Focus | +0.7% | National, highest adoption in commercial office and healthcare end-user segments | Short term (≤ 2 years) |

| Deployment of AI-Enabled Predictive Maintenance | +0.6% | National, early adoption concentrated in industrial, energy, and large public estate portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Outsourcing of Non-Core Activities

Strategic outsourcing has become a structural operating model in the Spain integrated facility management market because buyers now want simpler governance across cleaning, security, catering, technical maintenance, and workplace support under one contract. The shift is no longer framed only around cost reduction, because large occupiers also want fewer vendor interfaces, tighter reporting lines, and stronger control over service quality across dispersed sites. Mid-sized companies are also moving beyond single-service contracts, which is helping integrated providers win broader scopes and longer terms than they did in earlier outsourcing cycles. Public administration is reinforcing this direction because larger contracts increasingly require stronger digital workflows, clearer performance evidence, and better delivery consistency across public estates. Spain’s Plan BIM for Public Procurement made BIM compulsory for public contracts above EUR 5.5 million (USD 6.2 million) from October 2025, which raised the qualification threshold for suppliers seeking larger public assignments.[1]Internal Revenue Service, “Yearly Average Currency Exchange Rates,” IRS As a result, the Spain integrated facility management market is rewarding operators that can combine operational scale, compliance capacity, and multi-service coordination rather than those that compete only on unit pricing.

Rising Demand for Energy-Efficient Buildings

Energy efficiency is becoming a core growth engine for the Spain integrated facility management market because regulation is turning energy monitoring and optimization into standard contract requirements rather than optional add-ons. Directive (EU) 2024/1275 entered into force in May 2024, and Spain must transpose it into national law by May 2026, which is creating a compliance-led demand cycle for building upgrades, control systems, and technical maintenance. Spain’s National Building Renovation Plan is being developed under the recast directive, and the policy framework includes milestones to renovate the weakest-performing non-residential floor area by 2030 and 2033 while targeting a 65% reduction in primary energy use in non-residential buildings by 2050.[2]European Commission, “Recast EPBD Implementation Content,” BUILD UP Spain is also among the EU countries testing the Smart Readiness Indicator, which increases the relevance of building automation, data verification, and third-party performance evidence in technical service contracts. The March 2025 award to ACCIONA Energía for a 5-year EUR 5.6 million (USD 6.3 million) contract covering energy management across more than 400 Madrid City Council buildings shows that municipalities are already outsourcing this work at scale. Providers that can connect compliance, metering, analytics, and operational delivery are therefore likely to capture more renewals as the Spain integrated facility management market moves deeper into energy-led procurement.

Expansion Of Smart Building Technologies

Smart building adoption is widening the addressable scope of the Spain integrated facility management market because real-time monitoring is changing how providers inspect assets, schedule work, and document outcomes. IoT sensors, digital twins, and machine-learning tools are shifting Hard FM from fixed maintenance intervals to condition-based interventions, improving service precision and strengthening performance reporting. EMVS Madrid launched the SCAMIA system in February 2026 as a EUR 4.5 million (USD 4.9 million) project across 14 public housing developments, using digital twins, IoT sensors, and machine-learning algorithms for predictive and preventive maintenance across HVAC, electrical, plumbing, and elevator systems.[3]EMVS Madrid, “SCAMIA Predictive Maintenance Project,” EMVS Madrid This matters beyond one project, because lower sensor costs and more practical software tools are making technology-led FM relevant to a wider building base than prime office towers alone. The EPBD also requires non-residential buildings with larger HVAC systems to install building automation and control systems by 2027, which creates a mandated retrofit pipeline for technical services, whether discretionary budgets expand or not. That combination of regulatory pull and operational value is helping the Spanish integrated facility management market move from labor-led maintenance toward software-assisted service delivery with stronger lifecycle visibility.

EU Taxonomy Pressure on ESG Reporting

ESG disclosure is becoming a procurement filter in the Spain integrated facility management market because building owners increasingly need service partners that can support auditable operational reporting. The CSRD started extending to large companies from January 2025 and is expected to reach a far larger reporting base by 2028, which means more buyers will need traceable data on outsourced operations and building performance. Scope 3 reporting raises the relevance of facilities vendors because contracted cleaning, technical services, and other outsourced building activities can directly affect the emissions trail that occupiers and owners disclose. Optima Grupo’s ESG 360° project, recognized by EuroFM, shows how FM providers are using detailed operational metrics as a commercial differentiator rather than a branding exercise. The commercial effect is that reporting capability now influences qualification, renewal, and contract scope in the same way that coverage, staffing, and technical competence already do. This is pushing the Spain integrated facility management market toward larger providers that can link service delivery with sustainability data, audit readiness, and enterprise-level reporting support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor Cost Inflation | -1.2% | National, disproportionately affecting Soft FM labour-intensive contracts | Short term (≤ 2 years) |

| Fragmented Supplier Base in Specific Trades | -0.9% | National, most acute in industrial and energy end-user segments outside Tier-1 cities | Medium term (2-4 years) |

| Data Privacy Concerns in IoT Connectivity | -0.6% | National, concentrated in healthcare, government, and financial sector facilities | Medium term (2-4 years) |

| Shortage of Certified HVAC Technicians | -0.5% | National, most pronounced in southern Spain and secondary cities with limited training infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Labor Cost Inflation

Labor cost pressure is the clearest near-term constraint on the Spain integrated facility management market because its largest service areas still depend heavily on labour-intensive delivery models. Soft FM remains especially exposed, since cleaning, security, catering, and front-of-house services are often contracted at fixed prices even when wage obligations rise during the contract term. Spain’s FM sector supports more than 600,000 workers directly and indirectly, which means sector-wide wage agreements and social contribution costs have an immediate effect on provider margins and bid discipline. This pressure is also changing investment priorities, because providers are accelerating automation in tasks such as cleaning and monitoring in order to offset the wage path built into multi-year contracts. Spain’s General Disability Law adds another compliance layer for larger employers by requiring companies with 50 or more workers to maintain a 2% workforce quota for employees with disabilities. The result is that the Spain integrated facility management market is still growing, but price resets, staffing models, and contract terms are under much closer review than they were in earlier outsourcing cycles.

Fragmented Supplier Base in Specific Trades

A fragmented trade ecosystem is holding back the Spain integrated facility management market because broad-scope operators still rely on many local subcontractors for HVAC, electrical work, fire safety, and mechanical services. This is less of a problem in large metropolitan areas, but it becomes more visible in industrial corridors and secondary cities where supplier depth, certifications, and reporting systems are less consistent. IFM providers that win multi-service contracts can therefore face delivery risk if local trade partners cannot meet service-level agreements, documentation needs, or digital reporting requirements at the required speed. The challenge is becoming more serious in public procurement, because digital workflow and BIM readiness are now more important in qualification and execution than they were a few years ago. Spain’s BIM rules also raised expectations for public contracts above EUR 2 million (USD 2.3 million) from October 2025, which widened the capability gap between larger integrators and smaller specialist firms that have delayed digital investment. Until more local trade partners improve certification depth and digital readiness, the Spain integrated facility management market will continue to face bottlenecks in the very technical workstreams that are expanding fastest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Facility Management Leads Today While Hard Facility Management Builds Faster Structural Momentum

Soft Facility Management (FM) held 62.53% of the Spain integrated facility management (IFM) market share in 2025, reflecting the scale and recurrence of cleaning, security, catering, and front-of-house services across public, commercial, and healthcare estates. The segment remains dominant because these activities were among the first building functions that Spanish occupiers and public entities moved outside the organization, which drew greater management attention, while security services are evolving through centralized alarm reception models and remote supervision, giving large FM operators a long runway to build workforce depth and national coverage. That historical path still matters in 2026, because large buyers continue to prefer bundled labor-based services that can be rolled out quickly across many sites without changing the underlying asset base. Spain’s General Disability Law also shapes procurement behavior in parts of the market, since buyers often favor established providers with mature workforce programs and broader compliance capacity. Catering is gaining added relevance as workplace quality and employee wellness receive more management attention, while security services are changing through centralized alarm reception models and remote supervision that reduce the need for purely site-bound coverage.

Hard FM is projected to expand at 7.91% CAGR, making it the fastest-growing part of the Spain IFM market size outlook through 2031. The segment is structurally advantaged because technical compliance, building automation, and energy performance are now rising together instead of as separate spending lines. The recast EPBD and Spain’s renovation agenda are widening the need for asset management, mechanical and electrical services, fire and life safety work, and energy optimization across non-residential buildings. Spain’s HVAC sector grew 11.4% in 2025, driven by aerothermal and geothermal adoption across residential, commercial, and industrial uses, and that larger installed base will need maintenance, diagnostics, and performance verification over time. This shift strengthens the technical side of the Spain integrated facility management industry because compliance, equipment complexity, and lifecycle planning are becoming part of everyday service delivery rather than occasional project work.

By End-User: Industrial And Manufacturing Anchor Revenue While Commercial Expands Fastest

Industrial and Manufacturing was the largest end-user segment with 28.38% of the market in 2025, and it accounted for a leading share of the Spain IFM market size because uptime, safety, and environmental compliance are direct operating priorities in production environments. This segment is highly suited to integrated service delivery because unplanned stoppages, inefficient utility use, and weak maintenance coordination can quickly affect output and cost control. Catalonia, the Basque Country, Aragón, and Valencia continue to concentrate much of this demand through manufacturing, logistics, and energy-related assets that need reliable technical support and continuous operational reporting. Large operators have an advantage here when they can combine Hard FM and Soft FM in one model, especially where predictive maintenance, waste handling, energy management, and audit support sit under the same contract. The segment also illustrates how the Spain integrated facility management industry is moving toward service models that connect plant reliability, compliance documentation, and site-wide operational visibility.

Commercial is the fastest-growing end-user segment with an 8.03% CAGR through 2031, which places it among the strongest growth pockets in the Spain IFM market size outlook. Hybrid work patterns have changed the way office portfolios are run, since building usage now shifts more often and requires more flexible cleaning, workplace support, occupancy planning, and service scheduling. ESG obligations are adding another layer, because office owners and occupiers need clearer evidence on energy use, emissions, and occupant conditions across large property portfolios. CBRE GWS’s December 2025 expansion into stadium and hospital asset management from a Spanish revenue base of EUR 180 million (USD 203.2 million) shows that service providers are extending the same operating model into a wider set of commercial and institutional properties. Government and Public Administration remains a large and stable buyer, while healthcare, education, transportation, logistics, energy, mining, retail, multi-tenant residential, and sports and leisure continue to add contract depth, with Renfe cleaning awards totalling EUR 242.7 million (USD 273.9 million) illustrating the scale that transport-related outsourcing can reach.

Geography Analysis

Madrid remains the single most important demand center in the Spain IFM market because it combines the country’s largest concentration of corporate offices, government facilities, and finance-linked real estate. The city also acts as the main proving ground for advanced service models, which means vendors often test automation, energy management, and data-led maintenance in the capital before scaling them elsewhere. EMVS Madrid’s February 2026 launch of SCAMIA across 14 public housing developments shows how predictive maintenance is moving into the public estate through digital twins, IoT sensors, and machine-learning tools. Madrid is also leading the outsourcing of energy performance management, as seen in ACCIONA Energía’s 5-year contract covering more than 400 municipal buildings and 3,850 metering points. This gives the capital a wider contract scope than standard building upkeep alone, because technical services, data monitoring, and sustainability performance are being bundled together more often.

Catalonia forms the second major hub of the Spain integrated facility management market, with a strong mix of industrial maintenance, logistics, property management, healthcare estates, and office assets. The region’s concentration in pharmaceuticals, food processing, chemicals, and automotive activity supports steady demand for certified Hard FM work across mechanical, electrical, fire safety, and environmental management tasks. Clece’s January 2025 award for Hospital Vall d’Hebron in Barcelona, valued at EUR 60 million (USD 67.7 million), shows the scale available in Catalonia’s healthcare infrastructure. Professionalization in the regional ecosystem is also helping mid-tier owners and institutional investors move from in-house models toward more integrated outsourcing structures.

Andalucía, Valencia, the Basque Country, and other regions are taking a larger role as the Spain integrated facility management market expands beyond the biggest urban cores. Andalucía is notable for large healthcare outsourcing programs, including Clece’s November 2025 contract in Almería valued at EUR 110 million (USD 124.2 million) for cleaning and internal logistics services. The Basque Country adds another layer through advanced manufacturing demand, where HVAC, fire protection, and energy management services are closely tied to production continuity and regulatory compliance. The Twin 4.0 initiative at Euskalduna Palace in Bilbao, supported through SPRI, offers a clear example of how BIM-linked digital twins and predictive maintenance are moving into regional assets outside Madrid and Barcelona. As EPBD-related obligations spread across the country, regional municipalities and industrial clusters are likely to generate a broader base of technical and integrated service demand.

Competitive Landscape

The Spain integrated facility management market is moderately fragmented, with a top layer of large domestic and international operators competing for broad multi-service contracts while many regional firms continue to serve trade-specific or locally bounded needs. ACCIONA Facility Services and Clece remain prominent domestic competitors, while CBRE GWS, JLL, Johnson Controls, and other international names are building their position through technology, technical depth, and multinational client relationships. Competitive strength now depends less on labour scale alone and more on the ability to combine compliance, reporting, procurement discipline, and service delivery across multiple sites and asset types. Public tenders show how narrow the room for differentiation has become, because pricing, service model design, technical evidence, and documentation quality all matter at the same time in award decisions. This keeps the Spain integrated facility management market active at the top end while still leaving room for smaller firms that can deliver niche expertise or local responsiveness.

Technology adoption is becoming the main strategic divider within the Spain integrated facility management market because digital tools now affect both operating efficiency and renewal prospects. Johnson Controls’ OpenBlue platform illustrates how major vendors are using predictive maintenance, remote diagnostics, and energy analytics to make contracts more data-driven, with the company indicating energy savings potential of up to 10% in deployments. Optima Grupo’s integrated FM work for BBVA across 22 buildings and 1,198 offices, covering 707,674 m², shows that large enterprise accounts increasingly expect reporting architecture that can connect operations with ESG metrics and portfolio oversight. The next competitive step is likely to center on providers that can combine CMMS, BIM, IoT, and sustainability reporting in one operating stack instead of treating them as separate tools.

Regulation is also changing how value is judged in the Spain integrated facility management market because buyers now need support on building performance, energy compliance, and disclosure readiness as well as day-to-day service quality. The EPBD, ISO 50001-led energy management expectations, and CSRD reporting needs are gradually moving procurement away from a lowest-cost model and toward a broader total-value assessment. That shift favours integrated operators with proven reporting systems, technical certifications, and multi-site governance, especially in public estate and institutional portfolios. At the same time, regional specialists remain necessary in many contracts, because local delivery capacity in HVAC, electrical maintenance, fire safety, and site support is still essential outside the main metro markets.

Spain Integrated Facility Management Industry Leaders

ACCIONA Facility Services, S.A.

ISS Facility Services S.A.

Sodexo España, S.A.

Clece, S.A.

Serveo Servicios, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Johnson Controls launched Metasys 15.0, an upgraded building automation system offering 24/7 multi-server data resilience, three-click energy information access via an integrated Energy Management suite, and scalability for up to 1,000 IP devices per server across building, campus, and enterprise deployments, representing a significant expansion of the platform's IFM applicability for Spain's large institutional and commercial property managers.

- April 2026: Johnson Controls launched its pan-European Innovation Studio roadshow, bringing next-generation critical building technologies including OpenBlue AI-integrated solutions and data center thermal management systems directly to clients across Spain and Europe, targeting facility managers facing energy compliance and decarbonization planning requirements under the EPBD.

- February 2026: EMVS Madrid (Madrid's Municipal Housing and Land Company) launched SCAMIA, a EUR 4.5 million (USD 4.9 million) AI-powered predictive maintenance system co-financed by the European Regional Development Fund (FEDER), deploying digital twins, IoT sensors, and ML algorithms across 14 public housing developments for HVAC, electrical, plumbing, and elevator systems management.

- February 2026: Clece Care Services, the UK subsidiary of Spain-headquartered Clece S.A., acquired CK Facilities Management, a UK provider of cleaning and soft FM services for healthcare and education clients including Guy's and St Thomas' NHS Foundation Trust and King's College Hospital NHS Foundation Trust, marking Clece's formal entry into the UK integrated FM market.

Spain Integrated Facility Management Market Report Scope

The Spain Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current outlook for Spain integrated facility management demand through 2031?

The Spain integrated facility management market was valued at USD 7.36 billion in 2025 and is expected to reach USD 11.01 billion by 2031, growing at a 7.04% CAGR over 2026-2031.

Which service area is growing fastest in Spain?

Hard FM is the fastest-growing service type, with a 7.91% CAGR through 2031, supported by energy regulations, building automation requirements, and rising technical asset complexity.

Which customer group contributes the most revenue?

Industrial and Manufacturing led demand with 28.38% share in 2025, because uptime, compliance, and energy performance are critical in factories, logistics sites, and production assets.

Why are integrated contracts becoming more common across Spanish facilities?

Buyers want fewer vendors, better accountability, stronger reporting, and more flexible cost structures, while public and private estates also face tighter compliance and digital workflow requirements.

What are the biggest risks for providers over the next few years?

Labor cost inflation, fragmented trade subcontracting, data governance concerns in connected buildings, and shortages of certified HVAC technicians are the main operating constraints.

Which regions matter most for expansion plans in Spain?

Madrid and Catalonia remain the strongest demand centers, while Andalucía, Valencia, and the Basque Country are gaining importance as outsourcing spreads into regional public estates and industrial clusters.

Page last updated on: