Poland Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

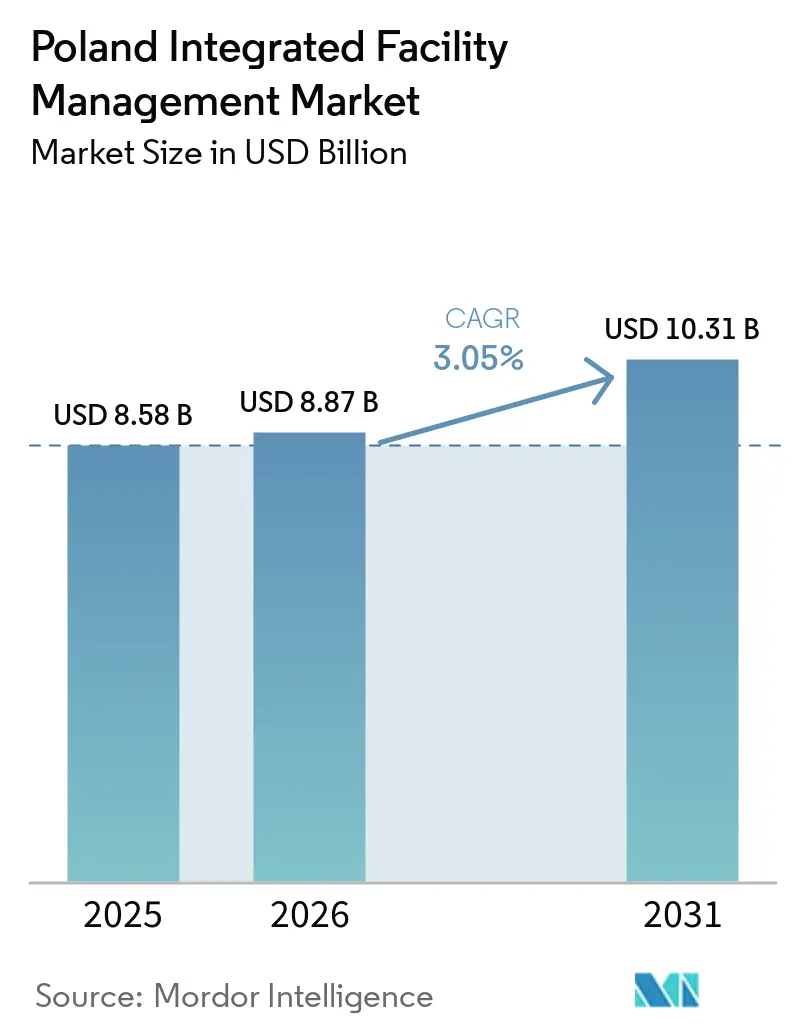

| Base Year Market Size (2025) | USD 8.58 Billion |

| Market Size (2026) | USD 8.87 Billion |

| Market Size (2031) | USD 10.31 Billion |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Integrated Facility Management Market Analysis by Mordor Intelligence

The Poland Integrated Facility Management Market size is projected to be USD 8.58 billion in 2025, USD 8.87 billion in 2026, and reach USD 10.31 billion by 2031, growing at a CAGR of 3.05% from 2026 to 2031.

The Poland integrated facility management (IFM) market is advancing on the back of practical building needs rather than short-lived demand, as older assets require more technical upkeep and compliance-led upgrades. EU sustainability rules are also pushing owners to treat facilities spending as part of asset performance, tenant retention, and financing readiness. In this setting, integrated contracts are becoming more relevant because buyers want one provider to coordinate technical maintenance, cleaning, security, and reporting in a more consistent way. The Poland IFM market is also benefiting from the gradual move away from fragmented, in-house service models toward bundled contracts that provide clearer cost control. At the same time, labour shortages and delayed regulatory transposition are keeping growth measured, which means providers that combine technical depth, digital tools, and local execution are likely to capture the best opportunities.

Key Report Takeaways

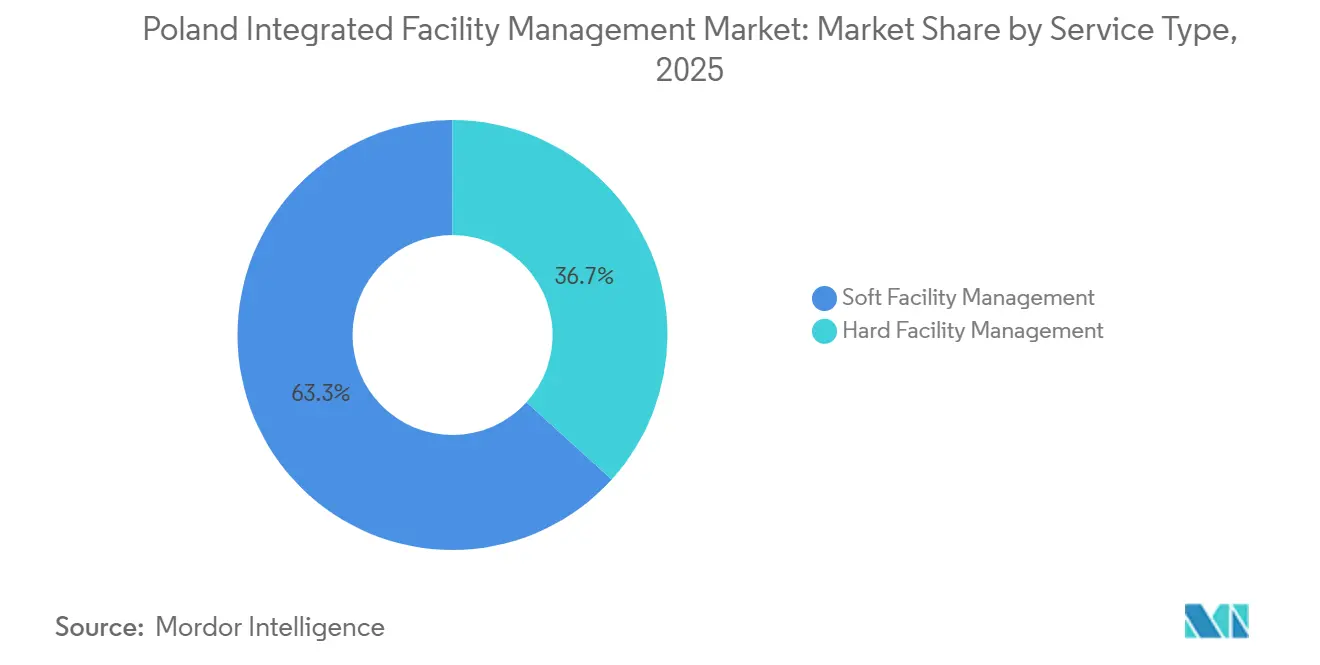

- By Service Type, Soft Facility Management held 55% to 65% of the Poland Integrated Facility Management Market in 2025, while Hard Facility Management recorded the highest projected CAGR of 3.25% to 3.9% through 2031.

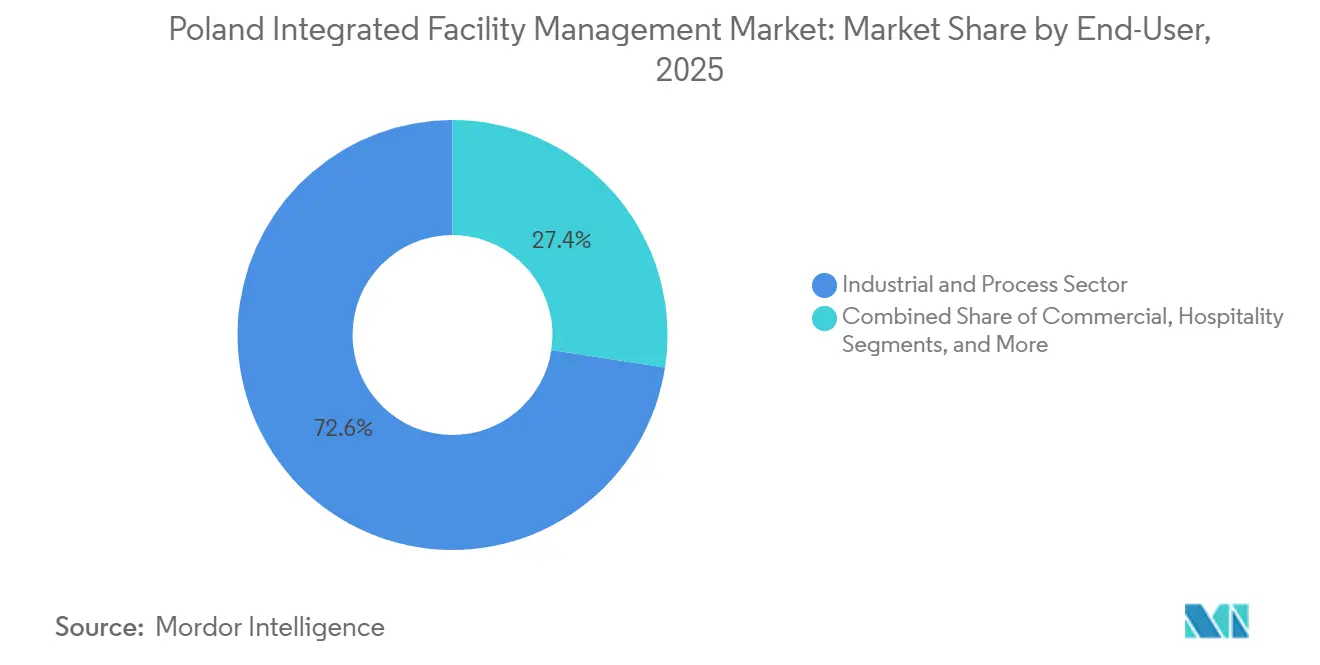

- By End-User, the Industrial and Process Sector accounted for 25% to 35% of the Poland Integrated Facility Management (IFM) Market in 2025, while the commercial segment posted the fastest growth CAGR of 3.25% to 3.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Focus on Energy Efficiency Compliance with ESG Directives | +0.8% | National, with intensity in Warsaw, Kraków, and Wrocław | Short term (≤ 2 years) |

| Expansion of International Competitive Offices in Poland | +0.6% | Warsaw, Kraków, Wrocław, Tricity | Medium term (2-4 years) |

| Rising Adoption and Outsourcing to Cut Operating Costs | +0.5% | National | Medium term (2-4 years) |

| Growth of International Real Estate Stock in Major Polish Cities | +0.4% | Warsaw primarily, growing in Kraków and Wrocław | Medium term (2-4 years) |

| Continued Smart Industry and National Industry 4.0 Programme | +0.3% | Industrial hubs, Katowice, Łódź, Wrocław | Long term (≥ 4 years) |

| IoT-Enabled Predictive and Smart Facility Operations | +0.2% | National, primarily dense urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Energy Efficiency Compliance with ESG Directives

The recast Energy Performance of Buildings Directive has created a direct compliance cycle for the Poland Integrated Facility Management Market because Poland must complete national transposition by May 29, 2026.[1]Concerted Action EPBD, “CA EPBD Overview and National Transposition Work,” CA EPBD, ca-epbd.eu The directive also requires non-residential buildings with heating or combined HVAC systems above 290 kW to install automation and control systems, and the threshold will extend to systems above 70 kW by December 2029.[2]European Parliament and Council, “Directive (EU) 2024/1275 on the Energy Performance of Buildings,” Official Journal of the European Union, europa.eu This changes technical upgrades from optional capital work into recurring service obligations that pull more Hard FM activity into integrated contracts. The scale of building adaptation is material because the SET Foundation estimated that bringing Polish buildings into line with the new EU standards. The compliance effect is spreading beyond offices because the planned amendment under draft UC77 would require full corporate energy audits for companies consuming more than 10 TJ per year, which widens the service need across industrial assets as well.[3]DB Energy, “Draft UC77 and Corporate Energy Audit Requirements,” DB Energy, dbenergy.pl

Expansion of International Competitive Offices in Poland

The Poland Integrated Facility Management (IFM) Market continues to draw support from multinational occupiers that use Poland as a regional office and service delivery base. These occupiers usually prefer bundled contracts because workplace services, technical maintenance, and sustainability reporting must work together in one operating model. That preference is important because it raises the value of IFM contracts beyond routine cleaning or guard services alone. It also favours vendors that can support tenant experience and compliance reporting at the same time, which is harder for smaller single-line contractors to match. The result is a demand pattern in which office expansion does not only add floor space, but it also increases the need for integrated governance, vendor accountability, and more standardized service delivery across large portfolios.

Rising Adoption and Outsourcing to Cut Operating Costs

Outsourcing remains a major growth lever for the Poland Integrated Facility Management Market because PRFM estimated that outsourced FM represented 44% of the total Polish FM market in 2022, leaving a larger in-house share still open to conversion. This structure suggests that Poland still has room to deepen professional outsourcing compared with more mature Western European markets, where outsourced FM has a much larger role in day-to-day operations. Buyers are moving in this direction because labour management, energy control, and service coordination are becoming harder to handle internally across multiple sites. Integrated contracts help shift operational risk to providers that can spread staffing, procurement, and technology costs across broader client portfolios. The Poland IFM Market is therefore seeing outsourcing treated less as a convenience decision and more as a method for stabilizing service quality, budget visibility, and compliance readiness.

Growth of International Real Estate Stock in Major Polish Cities

The Poland Integrated Facility Management Market is also being shaped by the quality and ownership profile of commercial real estate in major cities. As more institutional assets enter Warsaw and other leading urban markets, owners are more likely to appoint professional managers from the start rather than rely on fragmented local arrangements. That shift matters because institutional ownership often requires multi-year service consistency, stronger technical documentation, and better reporting discipline. Newer buildings also tend to carry more complex building systems, which raises the need for specialist maintenance, controls management, and coordinated service delivery. Even when headline construction volumes are moderate, the mix of newer and more technically demanding assets can still lift average contract value across the Poland Integrated Facility Management (IFM) Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Technical Workforce for Building Management | -0.50% | National, most acute in Warsaw, Kraków, and Wrocław | Short term (≤2 years) |

| Fragmented Regulatory Oversight Lacking Harmonized Standards | -0.30% | National, with enforcement gaps in secondary municipalities | Medium term (2-4 years) |

| Price Sensitivity Among Public Sector Clients | -0.20% | National | Short term (≤2 years) and medium term (2-4 years) |

| Cybersecurity Risk to Building Management Systems | -0.10% | Urban centers with dense BMS and IoT deployment | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Technical Workforce for Building Management

Labor availability remains the clearest operational brake on the Poland Integrated Facility Management Market. Cedefop identified Poland among the EU countries facing severe high-skilled occupational shortages through 2035, driven by demographic contraction, low mobility, and education gaps in specialized technical roles. That challenge is especially relevant for Hard FM because certified technicians are needed for HVAC, controls, fire systems, and energy-related inspections. When those skills are scarce, providers face wage pressure and service gaps at the same time, which weakens margins and slows the pace at which new contracts can be absorbed. The Poland IFM Market therefore has real demand, but part of that demand cannot be captured efficiently unless the technical labour base improves.

Fragmented Regulatory Oversight Lacking Harmonized Standards

Regulatory fragmentation is also holding back the Poland Integrated Facility Management Market because providers must manage a mix of current rules, incoming EU requirements, and uneven local enforcement. BUILD UP noted that Poland's existing building registers still provide only partial coverage of the stock, particularly in older assets, and certificate quality remains inconsistent. At the same time, the EPBD requires Poland to introduce a harmonized A-G EPC scale and digital renovation passports, which means the system is moving while many assets are still being assessed under older arrangements. This creates uncertainty for buyers that want multi-year contracts but are not yet fully clear on the compliance path for each site. The result is slower decision-making, narrower contract scopes in some tenders, and more cautious pricing on projects that involve technical compliance obligations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Requirements Are Lifting the Value of Hard Facility Management

Soft Facility Management (FM) held 55% to 65% of the Poland Integrated Facility Management (IFM) Market share in 2025, which shows that cleaning, catering, security, and office support still formed the largest service base. This position remained strong because these services are embedded across offices, industrial portfolios, institutions, and mixed-use assets. Soft FM also stayed essential in hybrid workplaces, where buyers now expect service schedules that follow actual occupancy rather than fixed routines. That has made delivery more flexible, but it has not reduced the importance of soft services in day-to-day operations.

Hard FM is the fastest-growing service type, and the Poland IFM Market size for technical services is projected to expand at a 3.25%-3.9% CAGR through 2031. The main reason is that compliance obligations are making technical intervention unavoidable in building portfolios that previously delayed upgrades. The EU directive on building performance has widened the need for automation, controls, and system oversight across non-residential buildings with larger heating and HVAC loads. Poland's transposition process is reinforcing the urgency because owners know the national framework is moving toward tighter performance expectations. The SPIE LTEC project at Warszawa Zachodnia railway station shows the scale of technical scope now being delivered in Poland, with one BMS system covering ventilation, heating, air conditioning, utility monitoring, and photovoltaic tracking across the station complex. As a result, Hard FM is moving from a maintenance line item to a more central contract layer inside the Poland Integrated Facility Management (IFM) Market.

By End-User: Industrial Demand Gives Scale While Commercial Clients Raise Service Complexity

The Industrial and Process Sector held 25% to 35% of the Poland IFM Market size in 2025, making it the largest end-user group. This position reflects the steady need for continuous technical coverage across manufacturing sites, energy infrastructure, mining operations, and logistics-linked facilities. Industrial locations usually require multi-site coordination, planned maintenance, fire and safety support, and closer control of utility systems than standard office buildings. These needs make contract terms longer and churn lower, which helps stabilize revenue for providers active in this part of the Poland Integrated Facility Management Market.

Industrial demand is also becoming more advanced in the type of service it expects. Smart industry programs and Industry 4.0 adoption are pushing plant operators toward predictive maintenance, monitored assets, and better energy management. That does not remove basic FM work, but it adds a digital layer that rewards firms with stronger technical platforms and reporting capabilities. The draft amendment referenced by DB Energy shows how energy-intensive companies are moving toward tighter audit obligations, which pulls facility and energy management closer together in industrial settings. Over time, this makes industrial contracts more valuable because the service bundle extends beyond repair and upkeep into compliance support and performance management.

Geography Analysis

Warsaw remains the clearest center of the Poland Integrated Facility Management Market because the city combines the largest concentration of modern office assets, institutional ownership, and compliance-sensitive occupiers. It is also one of the locations where the impact of energy efficiency directives is most immediate, which raises demand for technical maintenance, automation, and energy-related reporting. The capital's larger stock of multi-tenant properties means integrated delivery is often more practical than managing a wide list of single-service contractors. This is especially true where owners want better control of operating standards across premium office or mixed-use space. The Poland Integrated Facility Management (IFM) Market in Warsaw is therefore shaped by a mix of tenant pressure, technical asset complexity, and the need for consistent governance across larger portfolios.

Kraków, Wrocław, and Tricity are important growth centers because they combine office-based occupier demand with rising expectations around service consistency and ESG readiness. These cities were highlighted in the driver table as key locations for office expansion and energy-led compliance activity, which shows that growth is not limited to the capital. As international occupiers expand in regional markets, they tend to bring procurement standards that favour integrated contracts and clearer vendor accountability. This supports broader demand for workplace services, technical maintenance, and centralized reporting across regional portfolios.

Industrial hubs such as Katowice, Łódź, and Wrocław add a different geographic layer to the Poland IFM Market. In these locations, the service need is tied less to front-of-house office experience and more to uninterrupted plant operations, asset reliability, and energy monitoring. Smart industry adoption is gradually raising the technical threshold for FM delivery in these areas, which benefits providers that can combine site maintenance with monitored performance workflows. Secondary cities still represent white space because integrated contract penetration remains lower and regulatory enforcement can be less uniform than in leading urban centers. Yet those same features create room for future expansion once building upgrades, outsourcing adoption, and compliance requirements become more standardized across the national market.

Competitive Landscape

The Poland Integrated Facility Management Market remains moderately fragmented, with large international operators and a long tail of domestic providers competing across different contract sizes and customer groups. PRFM estimated that Poland had approximately 3,400 FM companies, which explains why no small group of firms can fully dominate the field despite the presence of major international brands. The international tier includes ISS, Sodexo, Compass Group, CBRE, Cushman and Wakefield, and JLL, while domestic and regional specialists continue to defend ground through price flexibility and local operating familiarity. In practical terms, the Poland Integrated Facility Management Market rewards scale in larger integrated contracts, but it still leaves room for smaller firms in regional assets, public tenders, and narrower service scopes. This mixed structure is why the market has not consolidated as quickly as some Western European peers.

The basis of competition is also changing. Service breadth still matters, but digital coordination, reporting quality, and technical self-delivery are becoming stronger decision factors in renewals and new tenders. Buyers want operators that can connect maintenance records, compliance workflows, and energy oversight without creating separate reporting streams for each service line. This is where larger firms are pressing their advantage, because they are better placed to invest in CAFM systems, predictive maintenance capability, and broader client governance tools. Domestic firms remain relevant, but they face more pressure when contracts move beyond local delivery and into platform-based service management.

Recent company moves show how leading operators are positioning themselves. In January 2025, ISS took over full technical maintenance for two CPI Property Group assets in Warsaw, myhive IO-1 and myhive Park Postępu, including energy efficiency optimization and sustainable development services, which shows a clear push into technical and compliance-linked mandates. In December 2025, ISS expanded a multi-country European contract with a financial services client by an additional annual value of DKK 100 million 9USD 14.3 million) bringing total annual revenue from that client to more than DKK 300 million (USD 42.9 million) with the five-year extension ramping up through Q1 2026. In January 2026, SPIE LTEC completed a BMS-based automation system at Warszawa Zachodnia railway station, which demonstrates the scale of technically complex assignments now feeding into the Poland Integrated Facility Management (IFM) Market. These moves matter because they highlight where competitive advantage is shifting toward technical depth, long-duration client relationships, and the ability to deliver measurable building performance outcomes.

Poland Integrated Facility Management Industry Leaders

CBRE Group, Inc.

ISS A/S

Sodexo S.A.

Cushman & Wakefield plc

Dussmann Service Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: OPG Property Professionals was appointed to manage the Lixa D office building in Warsaw under a 3-year contract, as landlords in Poland's tightening office market raised competitiveness through enhanced building management quality.

- March 2026: MVGM Polska extended its property management agreement with SICORE Real Assets, covering 3 class A office buildings in Warsaw and logistics assets in Poznań and Wrocław totaling 133,000 sqm, the continuation signaled growing multi-asset consolidation among institutional owners.

- December 2025: ISS expanded a multi-country European contract with a financial services client by an additional annual value of DKK 100 million ( USD 14.3 million) bringing total annual revenue from this client to more than DKK 300 million (USD 42.9 million). The five-year extension ramps up through Q1 2026.

- January 2025: SPIE LTEC completed installation of a BMS-based building automation system at Warszawa Zachodnia railway station, covering ventilation, HVAC, utility consumption monitoring, and photovoltaic generation tracking across all station concourses. The project ran from November 2021 through December 2025.

Poland Integrated Facility Management Market Report Scope

The Poland Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the 2031 outlook for integrated facility management in Poland?

The Poland Integrated Facility Management Market is expected to reach USD 10.31 billion by 2031 from USD 8.87 billion in 2026, with a 3.05% CAGR from 2026 to 2031.

Which service category is growing faster in Poland?

Hard FM is growing faster, with a projected CAGR of 3.25% to 3.9% through 2031, while Soft FM remained the larger service base in 2025 with a 55% to 65% share.

Why are technical services gaining importance in Polish facilities?

EU building performance rules are pushing owners to install automation, improve energy performance, and strengthen system oversight, which directly expands Hard FM scope.

Which end-user group contributes the most demand?

The Industrial and Process Sector held the largest share at 25% to 35% in 2025 because it needs continuous technical coverage across manufacturing, energy, and logistics-linked sites.

What is driving outsourcing adoption in Poland?

Buyers are turning to integrated outsourcing for better cost control, labour management, and compliance coordination, especially since outsourced FM still accounted for only 44% of the broader Polish FM market in 2022.

How competitive is the supplier landscape in Poland?

The market is moderately fragmented. Large international firms lead many complex integrated contracts, but PRFM estimated there were around 3,400 FM companies in Poland, which keeps the field broad.

What is the biggest risk to delivery over the forecast period?

The most important operating risk is the shortage of technical labour in roles tied to HVAC, electrical maintenance, and IoT-enabled building services, which can slow execution even when demand remains strong.

Page last updated on: